© institute for fiscal studies disease and cure in the uk: the fiscal impact of the crisis and the...

Post on 20-Dec-2015

217 views

TRANSCRIPT

© Institute for Fiscal Studies

Disease and cure in the UK: The fiscal impact of the crisis and the policy response

Slides prepared by Carl Emmerson for SOLACE

November 2010

http://www.ifs.org.uk/projects/346

Conclusions

• Permanent hit to public finances from financial crisis estimated at £86 billion a year (in today’s terms)

• Response is a £98 billion fiscal tightening by 2015–16, comprising a £24 billion tax rise and a £74 billion spending cut (in today’s terms)– OBR estimates 60% chance of hitting fiscal mandate on current policies

• Overall post crisis tax and benefit reforms regressive across most of the income distribution, although very focussed on richest 2%– cuts to welfare payments for working-age individuals

• Four years from next April will be the tightest sustained squeeze to public service spending since April 1976 to March 1980– total DELs cut by 11% in real terms

– overseas aid budget increased sharply

– in England: NHS and schools relatively protected; largest cuts to: Communities and Local Government, DEFRA and BIS

• Would be sensible to review plans in 2012

© Institute for Fiscal Studies

Disease

• Outlook for the public finances dramatically weakened since Budget 2008

• Much of deterioration expected to be impervious to economic recovery– ‘structural’ rather than ‘cyclical’ increase in borrowing

• Forecasting borrowing difficult– estimates of the size of the structural hole have changed over time

– latest (June 2010) forecasts are slightly worse than the forecast made before the general election (March 2010)

© Institute for Fiscal Studies

© Institute for Fiscal Studies

2008

–09

2009

–10

2010

–11

2011

–12

2012

–13

2013

–14

2014

–15

2015

–16

2016

–17

2017

–18

0

2

4

6

8

10

12Extra cyclicalExtra structuralBudget 2008

Per

cent

age

of n

atio

nal i

ncom

e

Permanent

damage =

5.8% of GDP

(£86bn)

Note: Author’s calculations comparing HM Treasury June 2010 Budget with HM Treasury March 2010 Budget.

Disease: size of the problem

© Institute for Fiscal Studies

Disease: change over time

PBR 2008 Budget 2009 PBR 2009 Budget March 2010

Budget June 2010

0

1

2

3

4

5

6

7

8£47bn £94bn £86bn £78bn £86bn

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Sources: HM Treasury; IFS calculations.

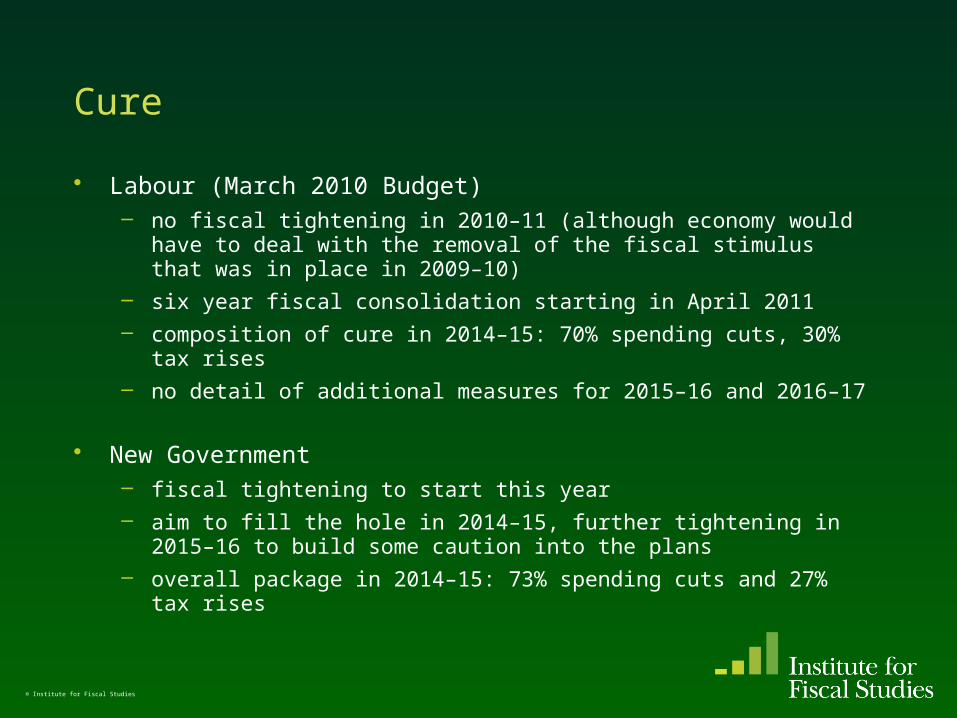

Cure

• Labour (March 2010 Budget)– no fiscal tightening in 2010–11 (although economy would have to deal with

the removal of the fiscal stimulus that was in place in 2009–10)

– six year fiscal consolidation starting in April 2011

– composition of cure in 2014–15: 70% spending cuts, 30% tax rises

– no detail of additional measures for 2015–16 and 2016–17

• New Government– fiscal tightening to start this year

– aim to fill the hole in 2014–15, further tightening in 2015–16 to build some caution into the plans

– overall package in 2014–15: 73% spending cuts and 27% tax rises

© Institute for Fiscal Studies

© Institute for Fiscal Studies

Fiscal tightening: Labour’s plans

20

08

–0

9

20

09

–1

0

20

10

–1

1

20

11

–1

2

20

12

–1

3

20

13

–1

4

20

14

–1

5

20

15

–1

6

20

16

–1

7-2

-1

0

1

2

3

4

5

6

7

8UnknownTax increasesOther spending cutsInvestment cutsBenefit cuts

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Sources: HM Treasury; IFS calculations.

70%

30%

© Institute for Fiscal Studies

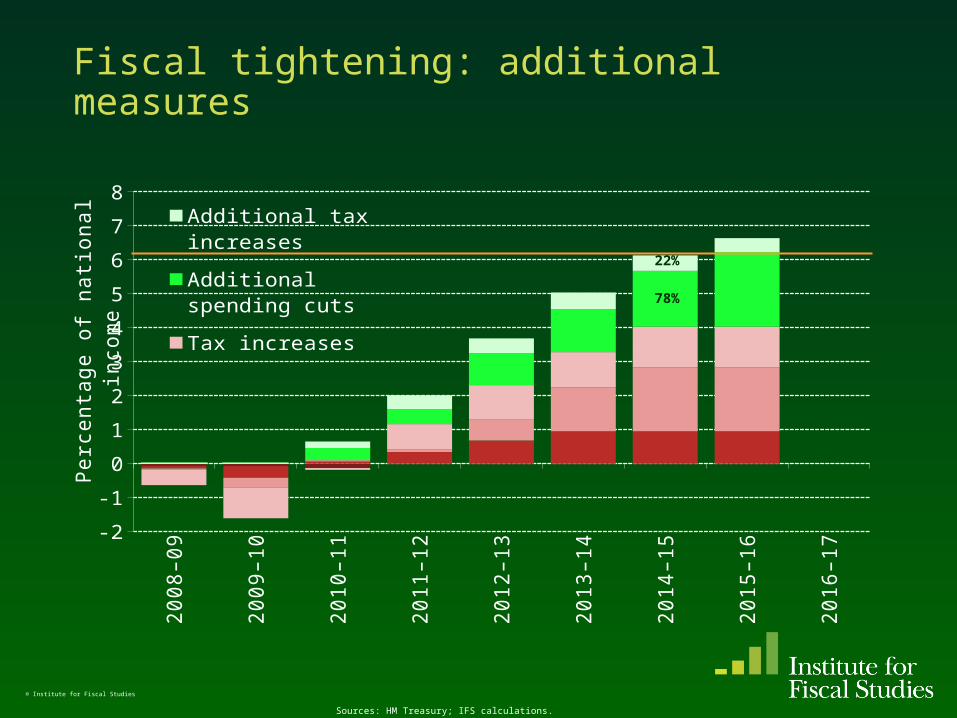

Fiscal tightening: additional measures

20

08

–0

9

20

09

–1

0

20

10

–1

1

20

11

–1

2

20

12

–1

3

20

13

–1

4

20

14

–1

5

20

15

–1

6

20

16

–1

7-2

-1

0

1

2

3

4

5

6

7

8Additional tax increases

Additional spending cuts

Tax increases

Other spending cuts

Investment cuts

Benefit cuts

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Sources: HM Treasury; IFS calculations.

22%

78%

© Institute for Fiscal Studies

Fiscal tightening: coalition plan

20

08

–0

9

20

09

–1

0

20

10

–1

1

20

11

–1

2

20

12

–1

3

20

13

–1

4

20

14

–1

5

20

15

–1

6

20

16

–1

7-2

-1

0

1

2

3

4

5

6

7

8

Tax increasesOther spending cutsInvestment cutsBenefit cuts

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Sources: HM Treasury; IFS calculations.

27%

73%

Differences in cure (2014–15)

• Overall tightening: new Government to tighten by more

• Composition of tightening– mix between tax and spending very similar to March 2010 Budget plan

– sharper fall in borrowing leads to greater reduction in debt interest spending

– similar £bn cut to investment spending (both very deep)

– significant welfare cuts announced since election (not known whether Labour would have done this)

– bigger £bn tax rises, and deeper £bn cut to non-investment spending, than implied by the March 2010 Budget plan

© Institute for Fiscal Studies

Composition of the tightening in 2014–15

© Institute for Fiscal Studies

£ billion (nominal) March 2010 Budget

October 2010 Spending Review

Tax 21.5 29.8Spending 50.9 80.5

Investment spending 17.2 17.0Current spending 33.7 63.5Of which:

Debt interest 7 10Benefits –0.3 17.7Public services 27.0 35.7

Total tightening (£bn) 72.4 110.3% Spending 70 73% Tax 30 27

Latest forecasts

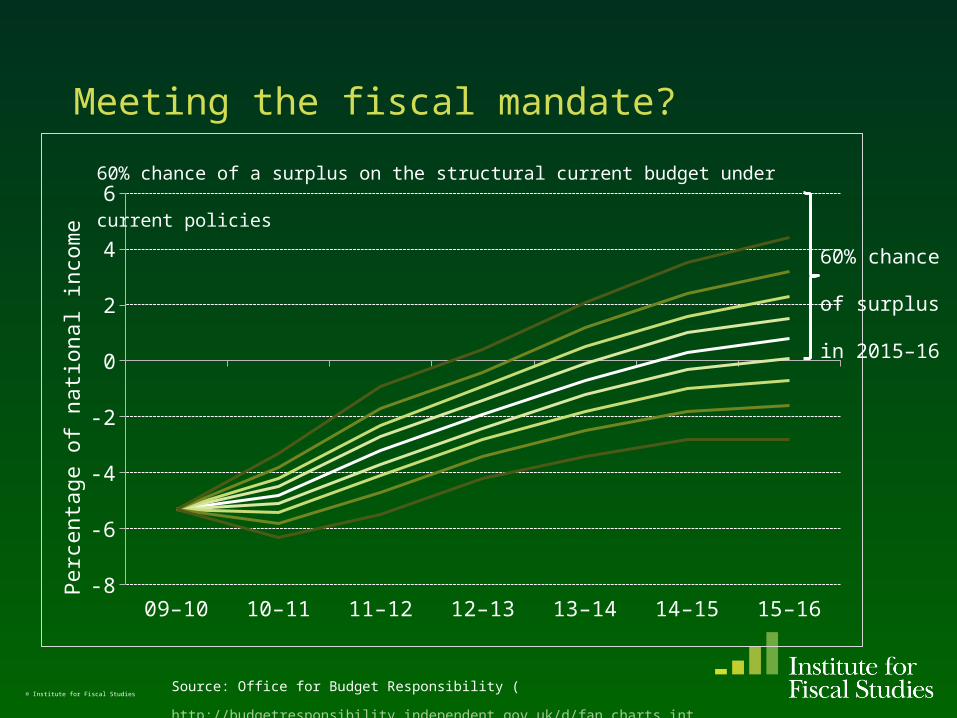

• Measures forecast to offset increase in underlying borrowing seen Budget 2008– deficit to return to pre-crisis levels in 2015–16

• Measures also to return debt to a sustainable path– but constant borrowing beyond 2015–16 would see not debt return to pre-

crisis levels until late 2020s

– if no further tax rises / spending cuts to offset costs of ageing population then debt still sustainable, but may not return to below 40% of national income

• Significant uncertainty remains– if latest forecasts are as accurate as previous ones then 60% chance of

meeting the Government’s fiscal mandate on current policies

– 40% chance that further tax rises or deeper spending cuts required

© Institute for Fiscal Studies

Cure: borrowing back to pre-crisis levels

© Institute for Fiscal Studies

20

07

–0

8

20

08

–0

9

20

09

–1

0

20

10

–1

1

20

11

–1

2

20

12

–1

3

20

13

–1

4

20

14

–1

5

20

15

–1

6

20

16

–1

7

20

17

–1

8

0

2

4

6

8

10

12 Budget 2008Budget June 2010 – no policy changeBudget June 2010

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Sources: Author’s calculations using all Budgets and Pre-Budget Reports since March 2008 (all available at http://www.hm-

treasury.gov.uk/).

Cure: debt sustainable but not back to pre-crisis levels for a generation

© Institute for Fiscal Studies

19

74

–7

5

19

77

–7

8

19

80

–8

1

19

83

–8

4

19

86

–8

7

19

89

–9

0

19

92

–9

3

19

95

–9

6

19

98

–9

9

20

01

–0

2

20

04

–0

5

20

07

–0

8

20

10

–1

1

20

13

–1

4

20

16

–1

7

20

19

–2

0

20

22

–2

3

20

25

–2

6

20

28

–2

9

20

31

–3

2

20

34

–3

5

20

37

–3

8

20

40

–4

1

0

40

80

120

160

200

Budget 2008

Budget June 2010 – no policy action

Budget June 2010

Budget June 2010 – including impact of demographic pressures

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Source: Author’s calculations based on the March 2008 and June 2010 Budget.

Meeting the fiscal mandate?

© Institute for Fiscal Studies

09–10 10–11 11–12 12–13 13–14 14–15 15–16-8

-6

-4

-2

0

2

4

6

Pe

rce

nta

ge

of

na

tion

al i

nco

me

60% chance of a surplus on the structural current budget under current policies

Source: Office for Budget Responsibility (

http://budgetresponsibility.independent.gov.uk/d/fan_charts_intervals.xls).

60% chance

of surplus

in 2015–16

Tax & spend

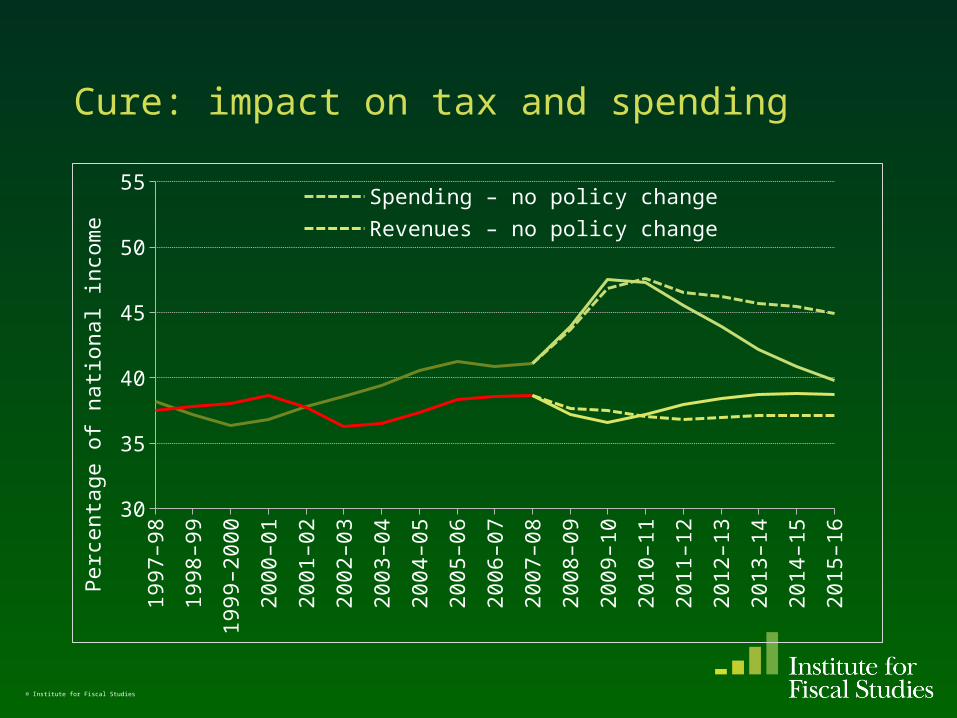

• Crisis depressed tax revenues and increased public spending as a share of national income– tax revenues: lower financial sector profits, lower house and equity prices

– public spending: public service spending set in cash terms for three years in 2007 and economy turned out much smaller than expected

• As a share of national income increase in spending greater than the fall in revenues– provides possible rationale for more of the policy response being on

spending than on tax

– aim to return spending to slightly below, and revenues to slightly above, pre-crisis levels

© Institute for Fiscal Studies

Cure: impact on tax and spending

© Institute for Fiscal Studies

19

97

–9

8

19

98

–9

9

19

99

–2

00

0

20

00

–0

1

20

01

–0

2

20

02

–0

3

20

03

–0

4

20

04

–0

5

20

05

–0

6

20

06

–0

7

20

07

–0

8

20

08

–0

9

20

09

–1

0

20

10

–1

1

20

11

–1

2

20

12

–1

3

20

13

–1

4

20

14

–1

5

20

15

–1

6

30

35

40

45

50

55Spending – no policy change

Revenues – no policy change

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Impact of tax rises and welfare cuts

• Measures reduce net incomes across the income distribution

• Impact regressive across most of the income distribution– with notable exception of the richest the losses are larger among low income

groups than among higher income groups

• Throughout the income distribution pensioners lose, on average, less than families with children

© Institute for Fiscal Studies

Cure: all in this together?

© Institute for Fiscal Studies

Impact of tax & benefit reforms to be in place by 2014–15, by income

Poorest

2 3 4 5 6 7 8 9 Richest

-£4,000

-£3,500

-£3,000

-£2,500

-£2,000

-£1,500

-£1,000

-£500

£0

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

October 2010 Spending ReviewJune 2010 BudgetAnnounced by previous governmentTotal as a % of income (right axis)

Income decile group

Ch

an

ge

in n

et

inco

me

Cure: all in this together?

© Institute for Fiscal Studies

Impact of tax & benefit reforms to be in place by 2014–15, by family type

Poorest

2 3 4 5 6 7 8 9 Richest

-8%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

Families with childrenPensionersOthers

Income decile group

Ch

an

ge

in n

et

inco

me

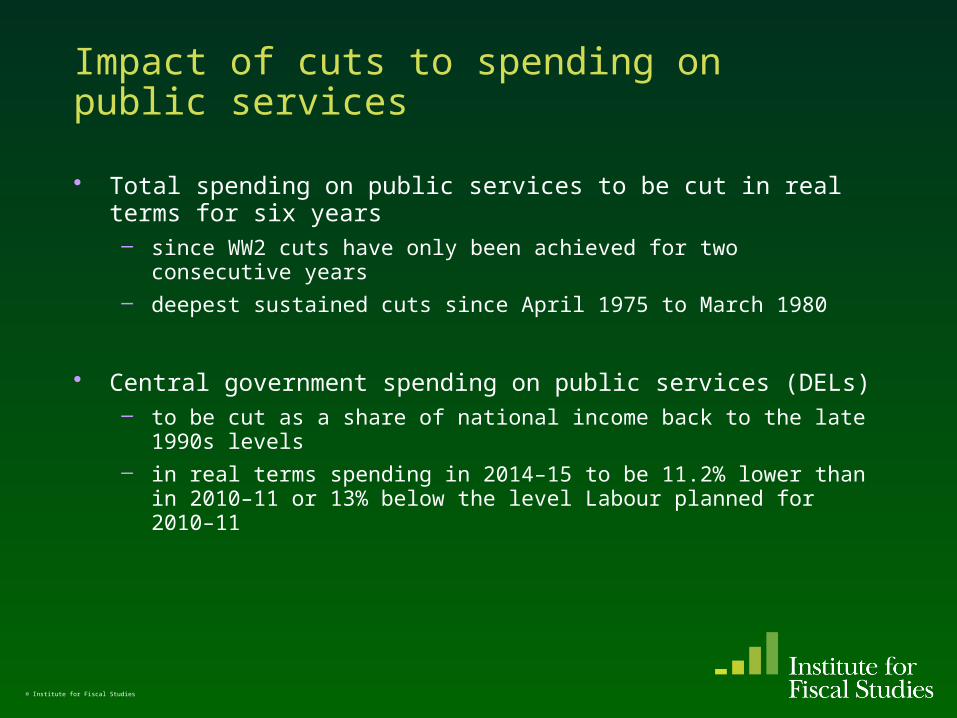

Impact of cuts to spending on public services

• Total spending on public services to be cut in real terms for six years– since WW2 cuts have only been achieved for two consecutive years

– deepest sustained cuts since April 1975 to March 1980

• Central government spending on public services (DELs)– to be cut as a share of national income back to the late 1990s levels

– in real terms spending in 2014–15 to be 11.2% lower than in 2010–11 or 13% below the level Labour planned for 2010–11

© Institute for Fiscal Studies

Cure: public service spending set for a squeeze

© Institute for Fiscal Studies

19

50

–5

1

19

55

–5

6

19

60

–6

1

19

65

–6

6

19

70

–7

1

19

75

–7

6

19

80

–8

1

19

85

–8

6

19

90

–9

1

19

95

–9

6

20

00

–0

1

20

05

–0

6

20

10

–1

1

20

15

–1

6

-10

-5

0

5

10

15

Labour ConLib Historic 6 year moving average

An

nu

al p

erc

en

tag

e r

ea

l in

cre

ase

Note: Figure shows total public spending less spending on welfare benefits and debt

interest.

DELs: The grand old Duke of York?

© Institute for Fiscal Studies

19

98

–9

9

19

99

–2

00

0

20

00

–0

1

20

01

–0

2

20

02

–0

3

20

03

–0

4

20

04

–0

5

20

05

–0

6

20

06

–0

7

20

07

–0

8

20

08

–0

9

20

09

–1

0

20

10

–1

1

20

11

–1

2

20

12

–1

3

20

13

–1

4

20

14

–1

5

10

15

20

25

30October 2010 Spending Review

March 2010 Budget

Pe

rce

nta

ge

of

na

tion

al i

nco

me

Note: Figure shows Departmental Expenditure Limits (DELs) as a share of national income under current policies.

DELs: deep cuts coming

© Institute for Fiscal Studies

2010–11 2011–12 2012–13 2013–14 2014–1580

85

90

95

100

105March 2010 Budget

October 2010 Spending Review

Ind

ex:

La

bo

ur

20

10

–1

1 =

10

0

–11%

–10%

– 13%

Sharing the pain

• Two winners?– spending on international aid and energy & climate change

• Relative protection for NHS and schools?– tightest settlement for NHS spending since early 1950s

– schools spending per pupil to fall in all but most deprived schools

• Several losers?– Home office, Justice, Local Government and Department for Business,

Innovation and Skills all face cuts of around one-quarter

– latter primarily comes from deep cuts to taxpayer support for higher education teaching

• One big loser?– DCLG communities budget to be cut by two-thirds, with capital budgets cut

by three-quarters: public investment in new social housing the big loser

© Institute for Fiscal Studies

‘Winners’

Average DEL cut

Education

Defence

NHS (England)

Work and pensions

Energy and climate change

International development

-20 -10 0 10 20 30 40

-11.2

-10.8

-7.3

0.3

1.4

16.2

34.2

Real budget increase 2011–12 to 2014–15

© Institute for Fiscal Studies

Note: Figures show real change in total (resource + capital) DEL

‘Losers’

CLG Communities

Environment, food and rural affairs

Business, innovation and skills

CLG Local government

Justice

Home office

Culture, media and sport

Transport

Average DEL cut

-80 -70 -60 -50 -40 -30 -20 -10 0

-67.6

-30.9

-28.5

-26.8

-25.3

-25.2

-21.1

-14.6

-11.2

Real budget increase 2011–12 to 2014–15

© Institute for Fiscal Studies

Note: Figures show real change in total (resource + capital) DEL

© Institute for Fiscal Studies

English schools spending

• DfE to receive total real-terms cut in DEL of 10.8%

• Schools spending including pupil premium to grow by 0.1% per year in real-terms (or 0.4% in total)– but total pupil numbers to increase by average of 0.7% per year

– total schools spending per pupil to be cut in real-terms by 0.6% per year (total of 2¼%)

• Assuming flat-rate pupil premium of £2,400 (stated total cost £2.5 billion) and underlying funding per pupil frozen in cash-terms– 60% of primary school pupils in schools where real funding falls

– 87% of secondary school pupils in schools where real funding falls

– 43% of pupils in (less deprived) schools would see cuts of 5% or more

– 1 in 8 pupils in (very deprived) schools would see increase of 5% or more

Note: Assumes all schools experience the same growth in pupil numbers.

Record breakers?

• Real increase over next 4 years– total spending: tightest since World War II

– spending on public services: tightest since April 1975 to March 1980

– NHS: tightest since April 1951 to March 1956

– (ODA: greatest since Jan 2002 to Dec 2006)

© Institute for Fiscal Studies

Conclusions

• Permanent hit to public finances from financial crisis estimated at £86 billion a year (in today’s terms)

• Response is a £98 billion fiscal tightening by 2015–16, comprising a £24 billion tax rise and a £74 billion spending cut (in today’s terms)– OBR estimates 60% chance of hitting fiscal mandate on current policies

• Overall post crisis tax and benefit reforms regressive across most of the income distribution, although very focussed on richest 2%– cuts to welfare payments for working-age individuals

• Four years from next April will be the tightest sustained squeeze to public service spending since April 1976 to March 1980– total DELs cut by 11% in real terms

– overseas aid budget increased sharply

– in England: NHS and schools relatively protected; largest cuts to: Communities and Local Government, DEFRA and BIS

• Would be sensible to review plans in 2012

© Institute for Fiscal Studies

© Institute for Fiscal Studies

Disease and cure in the UK: The fiscal impact of the crisis and the policy response

Slides prepared by Carl Emmerson for SOLACE

November 2010

http://www.ifs.org.uk/projects/346