1 fin 2802, spring 10 - tang chapter 27: practical portfolio management fin 2802: investments...

TRANSCRIPT

1FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

Fin 2802: Investments

Spring, 2010Dragon Tang

Fin 2802: Investments

Spring, 2010Dragon Tang

Lecture 19Practical Portfolio Management

April 8, 2010

Readings: Chapter 27Practice Problem Sets: 1,2

2

OverviewOverview

• Treynor-Black model– Optimization using analysts’ forecasts of superior

performance

– Adjusting model for tracking error

– Adjusting model for analyst forecast error

• Black-Litterman model

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

3

Table 27.1 Construction and Properties of the Optimal Risky Portfolio (properties 1-5)

Table 27.1 Construction and Properties of the Optimal Risky Portfolio (properties 1-5)

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

4

Table 27.1 Construction and Properties of the Optimal Risky Portfolio (properties 6-11)

Table 27.1 Construction and Properties of the Optimal Risky Portfolio (properties 6-11)

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

5

Table 27.2 Stock Prices and Analysts’ Target Prices for June 1, 2006

Table 27.2 Stock Prices and Analysts’ Target Prices for June 1, 2006

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

6

Figure 27.1 Rates of Return on the S&P 500 (GSPC) and the Six StocksJune 2005 – May 2006

Figure 27.1 Rates of Return on the S&P 500 (GSPC) and the Six StocksJune 2005 – May 2006

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

7

Table 27.3 The Optimal Risky Portfolio with the Analysts’ New Forecasts Table 27.3 The Optimal Risky Portfolio with the Analysts’ New Forecasts

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

8

Table 27.4 The Optimal Risk Portfolio with Constraint on the Active Portfolio (WA < 1)

Table 27.4 The Optimal Risk Portfolio with Constraint on the Active Portfolio (WA < 1)

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

9

Figure 27.2 Reduced Efficiency when Benchmark Is Lowered Figure 27.2 Reduced Efficiency when Benchmark Is Lowered

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

10

Table 27.5 The Optimal Risky Portfolio with the Analysts’ New Forecasts (benchmark risk constrained to 3.85%)

Table 27.5 The Optimal Risky Portfolio with the Analysts’ New Forecasts (benchmark risk constrained to 3.85%)

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

11

Figure 27.3 Histogram of the Alpha ForecastFigure 27.3 Histogram of the Alpha Forecast

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

12

Figure 27.4 Organizational Chart for Portfolio Management Figure 27.4 Organizational Chart for Portfolio Management

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

13

Steps in the Black-Litterman ModelSteps in the Black-Litterman Model

• Step 1: Estimate the covariance matrix from historical data

• Step 2: Determine a baseline forecast

• Step 3: Integrating the manager’s private views

• Step 4: Developing revised (posterior) expectations

• Step 5: Apply portfolio optimization

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

14

Figure 27.5 Sensitivity of Black Litterman Portfolio Performance to Confidence Level (view is correct)

Figure 27.5 Sensitivity of Black Litterman Portfolio Performance to Confidence Level (view is correct)

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

15

Figure 27.6 Sensitivity of Black Litterman Portfolio Performance to Confidence Level (view is false)

Figure 27.6 Sensitivity of Black Litterman Portfolio Performance to Confidence Level (view is false)

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

16

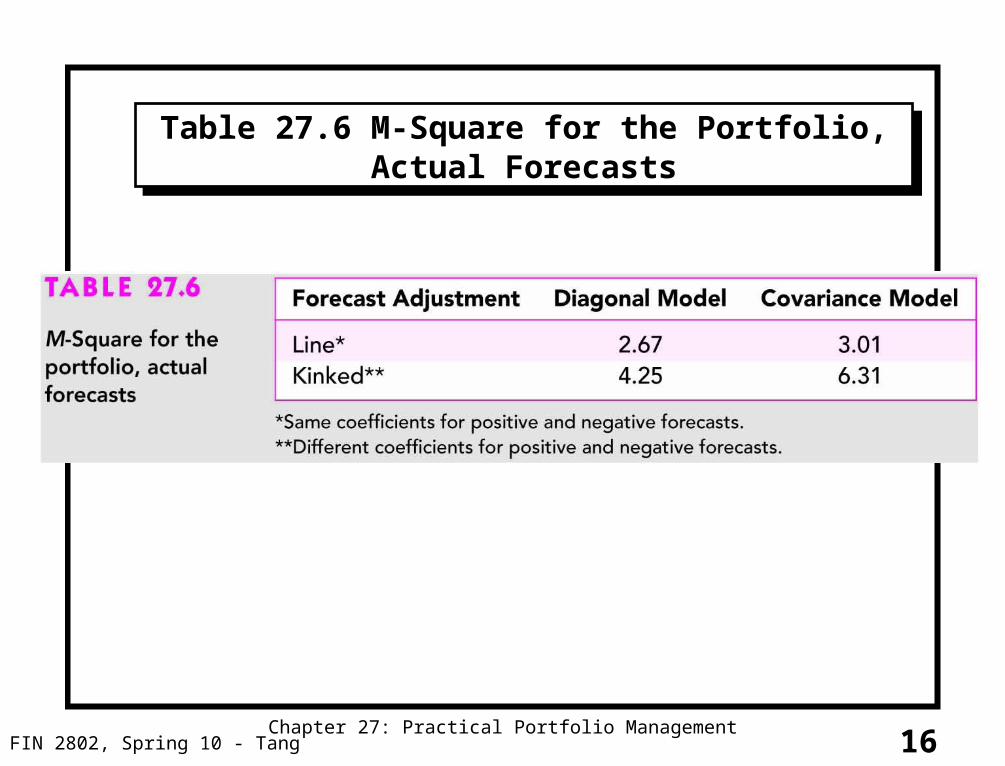

Table 27.6 M-Square for the Portfolio, Actual ForecastsTable 27.6 M-Square for the Portfolio, Actual Forecasts

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

17

Table 27.7 M-Square for the Simulated PortfoliosTable 27.7 M-Square for the Simulated Portfolios

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

18

Concluding Remarks on the Theory of Active InvestmentsConcluding Remarks on the Theory of Active Investments

• The gap between theory and practice has been narrowing in recent years

• The CFA is expanding knowledge base in the industry

• Specific lack of application of the Treynor-Black model may be related to lack of application of adjusting for analysts’ errors

FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

19FIN 2802, Spring 10 - TangChapter 27: Practical Portfolio Management

SummarySummary

• Treynor-Black model• Black-Litterman Model• Next Class: Performance Evaluation