1 fin 48 and other developments with potential to impact a captive’s financial statements march...

TRANSCRIPT

1

FIN 48and other developments

with potential to impact a captive’s financial

statements

March 12, 2008

Daniel Kusaila Kate Westover

2

Agenda

Part One: What’s with us now?

• Fin 48

Part Two: What is coming?

• Treasury Decision 9329

• FAS 157

• FAS 159

3

Part One: FASB Interpretation No. 48 (FIN 48) - Agenda

• Initial Pronouncement• Pre-FIN 48• Overview• Steps in FIN 48• Classification• Interest & Penalties• Disclosures• Common Concerns for Captives

3

4

FASB Interpretation No. 48(FIN 48)

• FIN 48- FASB’s latest pronouncement in accounting for income taxes.

–Released July 13, 2006

• FIN 48 interprets FAS 109

• Intent is to decrease the diversity in accounting for uncertainty in income tax financial statement positions.

4

5

Pre-FIN 48

• Uncertainties in tax positions were handled under SFAS 5, Accounting for Contingencies.

• SFAS 5 included income taxes as well as all other taxes (excise, property, franchise, sales and use, employment and others).

• FIN 48 amends SFAS 5, which is no longer applicable to income taxes.

5

6

Overview• Prior to recognizing the benefit of a tax

position for financial reporting purposes, the tax position must be more-likely-than-not (MLTN) of being sustained solely on its technical merits (excluding detection risk)

• Tax positions recognized are reported at the largest amount that is MLTN to be sustained

4

7

Overview

• Effective Date for Years Beginning on or After December 15, 2006

• ALL GAAP FINANCIAL STATEMENTS

5

8

Overview

FASB Staff Position FIN 48-2

(Feb. 1, 2008)

–Defers the effective date for all nonpublic enterprises for fiscal years beginning after December 15, 2007.

–Nonpublic consolidated entities of public enterprises applying GAAP are not eligible for deferral.

8

9

FIN 48• FIN 48 applies to all tax positions within

SFAS 109– Does not apply to non-income taxes

• Tax positions:– Deductions taken (or expect to be taken)– Taxable income excluded– Conclusions not to file an income tax return

• STATE TAXES!– Conclusions that an entity or transaction is

tax-free

9

10

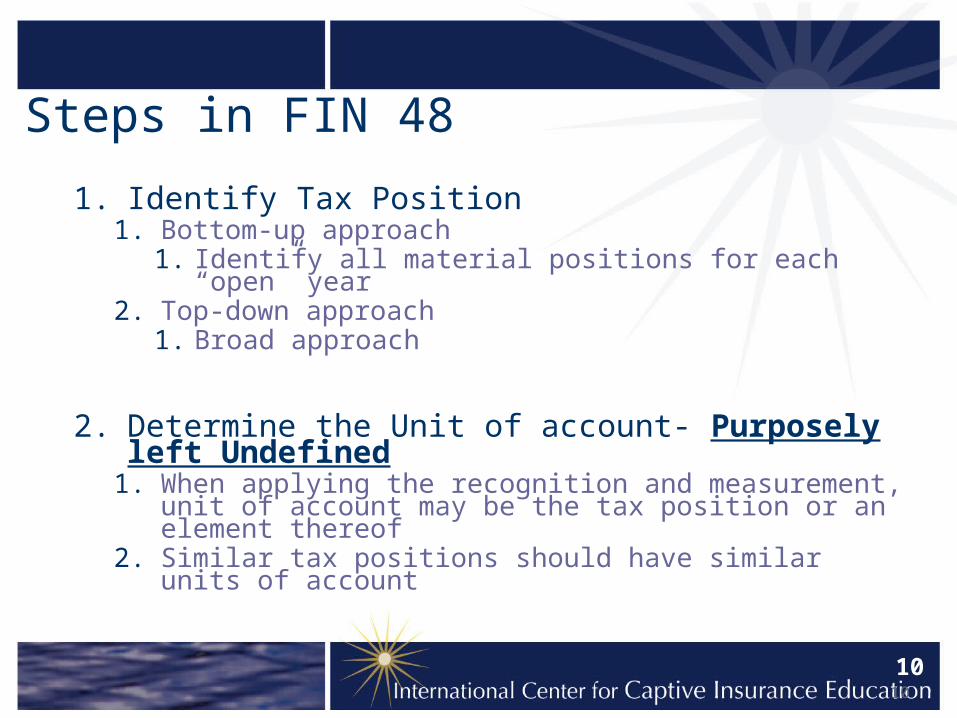

Steps in FIN 48

1. Identify Tax Position1. Bottom-up approach

1. Identify all material positions for each “open” year2. Top-down approach

1. Broad approach

2. Determine the Unit of account- Purposely left Undefined

1. When applying the recognition and measurement, unit of account may be the tax position or an element thereof

2. Similar tax positions should have similar units of account

10

11

Steps in FIN 48

3. Evaluate the position for recognition

1. In order to recognize any amount of the benefit, the position must be MLTN of being sustained

1.The position will be examined

2.The examiner will have full knowledge of all relevant info

3.Evaluation based solely on technical merits

4.No offset or aggregation of positions

5.Should assume resolution in the court of last resort

11

12

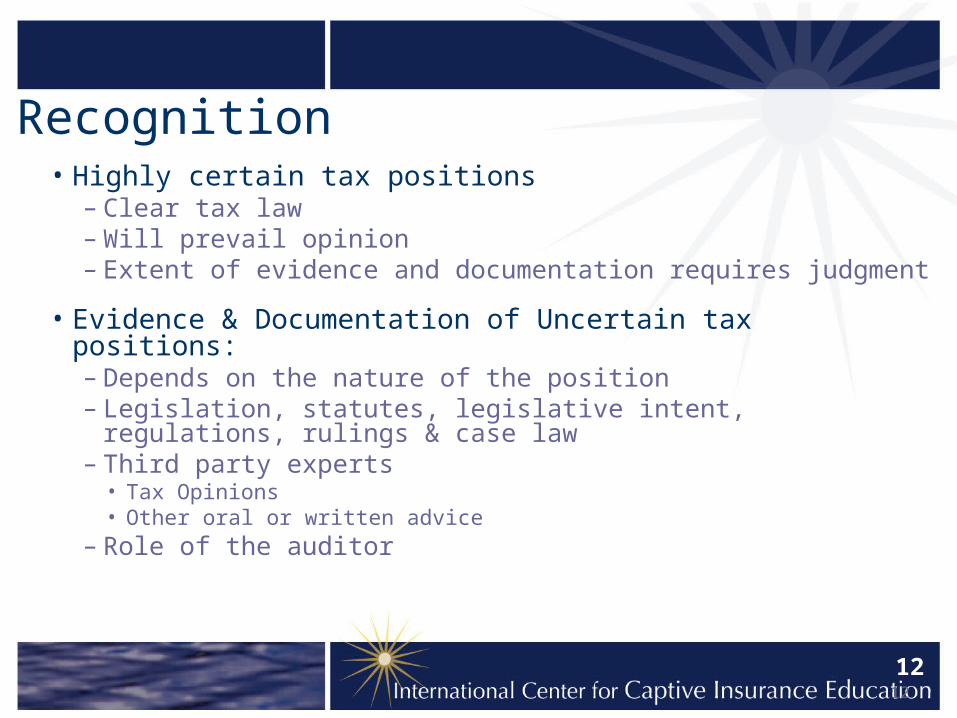

Recognition• Highly certain tax positions

– Clear tax law– Will prevail opinion– Extent of evidence and documentation requires judgment

• Evidence & Documentation of Uncertain tax positions:– Depends on the nature of the position– Legislation, statutes, legislative intent, regulations, rulings &

case law– Third party experts

• Tax Opinions• Other oral or written advice

– Role of the auditor

12

13

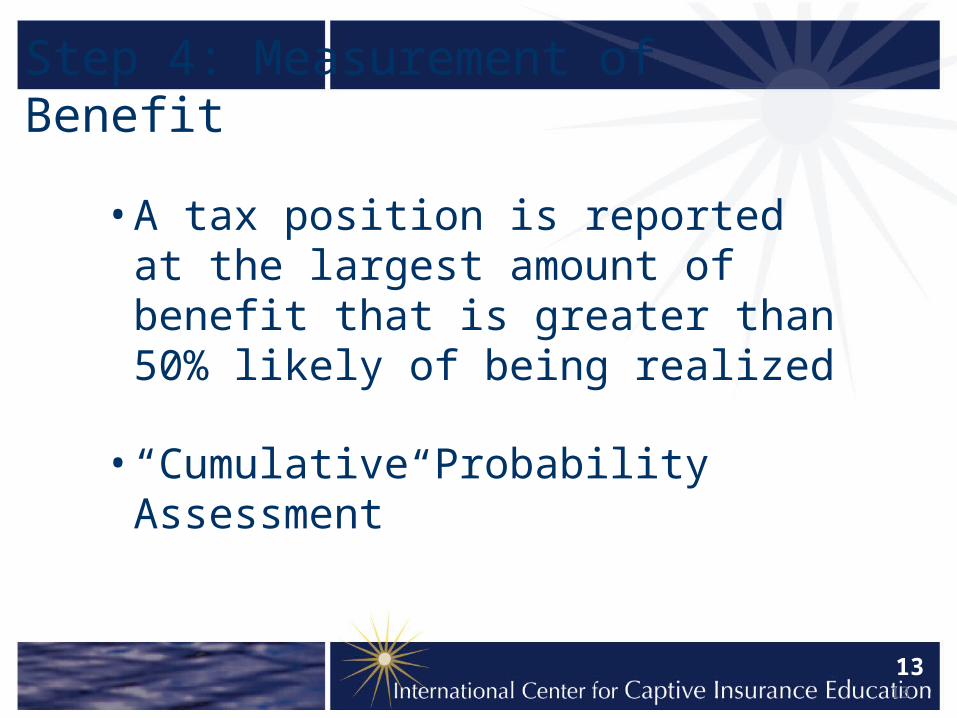

Step 4: Measurement of Benefit

• A tax position is reported at the largest amount of benefit that is greater than 50% likely of being realized

• “Cumulative Probability Assessment”

13

14

Step 4: Measurement of Benefit Continued…

Example… Loss Reserve was understated

Estimated Individual CumulativeOutcome Probability (%) Probability (%)

100$ 35 3575$ 25 6050$ 40 100

14

15

• Chart is not required

• Realistically, making the estimates in the chart would often be extremely difficult.

15

Step 4: Measurement of Benefit Continued…

16

Used Incorrect Discount Factors:

Book Tax Basis FIN 48 Basis

Reserves 500 400 300

Premium 1,000 1,000 1,000Underwriting (500) (400) (300)GAA (100) (100) (100)

Income 400 500 600

Tax Rate 34% 34% 34%

Tax Payable 136 170 204

16

Step 4: Measurement of Benefit Continued…

17

Current Tax Expense 170 204Current Income Tax Payable 170 170

FIN 48 Liability 34

Deferred Tax Expense 34 68Deferred Tax Asset 34 68

As Filed FIN 48

17

Step 4: Measurement of Benefit Continued…

18

Perm (Tax Exempt Interest):

Book FIN 48 Tax Basis100 20 0

Current Tax Expense 20Current Tax Payable 20

18

Step 4: Measurement of Benefit Continued…

19

Step 5: Classification• Differences between the (as-filed) tax

basis and the FIN 48 basis usually result in the recognition of a liability.

• FIN 48 liabilities are long term unless expected to be settled within one year

• May need to reduce NOL Carryforwards or refunds

19

20

Step 6: Accrue Interest

• FIN 48 provides that classification of interest is an accounting policy– Interest expenses or disclosed under

income taxes

• Accrue interest on the difference between the FIN 48 and the as-filed as the interest would be due under the law

20

21

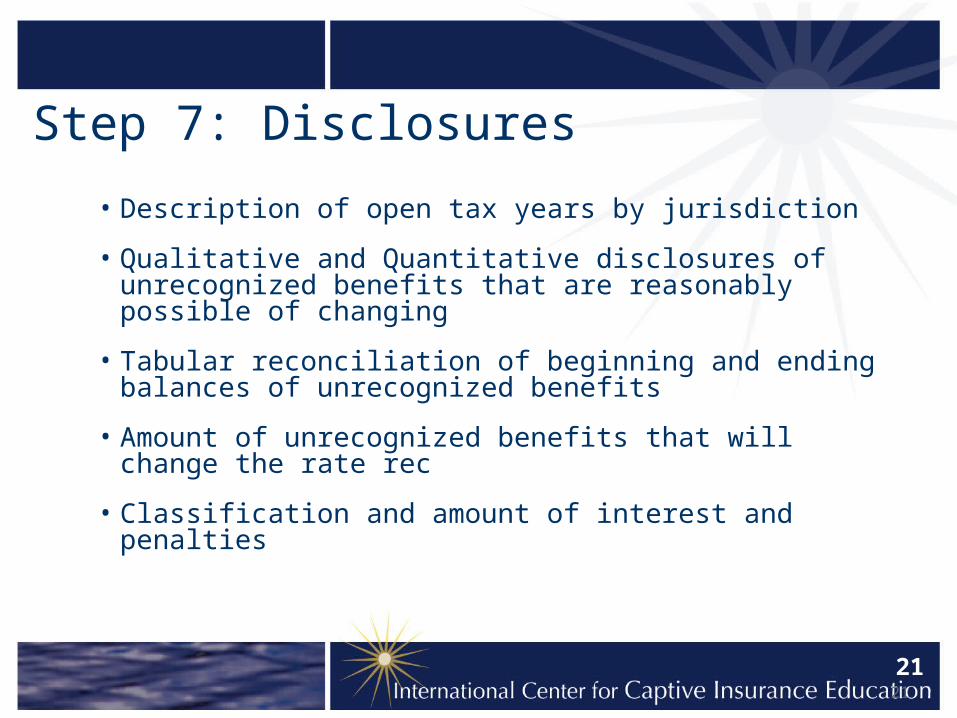

Step 7: Disclosures

• Description of open tax years by jurisdiction

• Qualitative and Quantitative disclosures of unrecognized benefits that are reasonably possible of changing

• Tabular reconciliation of beginning and ending balances of unrecognized benefits

• Amount of unrecognized benefits that will change the rate rec

• Classification and amount of interest and penalties

21

22

Step 7: Example Disclosure

The following example illustrates disclosures about uncertainty in income taxes. In this illustrative example, the reporting entity has adopted the provisions of this Interpretation for the year ended December 31, 2007:

22

23

Step 7: Example Disclosure continued…The Company, or one of its subsidiaries, files income tax returns in the

U.S. federal jurisdiction, and various states and foreign jurisdictions. With few exceptions, the Company is no longer subject to U.S. federal, state and local, or non-U.S. income tax examinations by tax authorities for years before 2001. The Internal Revenue Service (IRS) commenced an examination of the Company’s U.S. income tax returns for 2002 through 2004 in the first quarter of 2007 that is anticipated to be completed by the end of 2008. As of December 31, 2007, the IRS has proposed certain significant adjustments to the Company’s transfer pricing and research credits tax positions.

Management is currently evaluating those proposed adjustments to determine if it agrees, but if accepted, the Company does not anticipate the adjustments would result in a material change to its financial position. However, the Company anticipates that it is reasonably possible that an additional payment in the range of $80 to $100 million will be made by the end of 2008.

23

24

The Company adopted the provisions of FASB Interpretation No. 48, Accounting forUncertainty in Income Taxes, on January 1, 2007. As a result of the implementationof Interpretation 48, the Company recognized approximately a $200 million increasein the liability for unrecognized tax benefits, which was accounted for as a reductionto the January 1, 2007, balance of retained earnings. A reconciliation of the beginningand ending amount of unrecognized tax benefits is as follows:

(in millions)Balance at January 1, 2007 $370,000Additions based on tax positions related to the current year 10,000Additions for tax positions of prior years 30,000Reductions for tax positions of prior years (60,000)Settlements (40,000)Balance at December 31, 2007 $310,000

Included in the balance at December 31, 2007, are $60 million of tax positions forwhich the ultimate deductibility is highly certain but for which there is uncertaintyabout the timing of such deductibility. Because of the impact of deferred taxaccounting, other than interest and penalties, the disallowance of the shorterdeductibility period would not affect the annual effective tax rate but wouldaccelerate the payment of cash to the taxing authority to an earlier period.

24

Step 7: Example Disclosure continued…

25

The Company recognizes interest accrued related to unrecognizedtax benefits in interest expense and penalties in operating Expenses. During the years ended December 31, 2007, 2006, and 2005, the Company recognized approximately $10, $11, and $12 million in interest and penalties. The Company had proximately $60 and $50 million for the payment of interest and penalties accrued at December 31, 2007, and 2006, respectively.

25

Step 7: Example Disclosure continued…

26

Common Concerns for Captives1. Meeting Qualifications of Insurance2. Qualifying as a Reciprocal for IRS purposes3. Dividends & Tax Exempt Interest

1. Mutual fund dividends2. Tax exempt bonds

4. Loss Reserve Discounting 1. Correct Lines of Business2. Correct IRS Factors

5. Advanced Premium6. Controlled Group Elections7. Tax exempt status

1. 501(c)(15)2. Private Letter Ruling

8. State Income Taxes (including unitary)

26

27

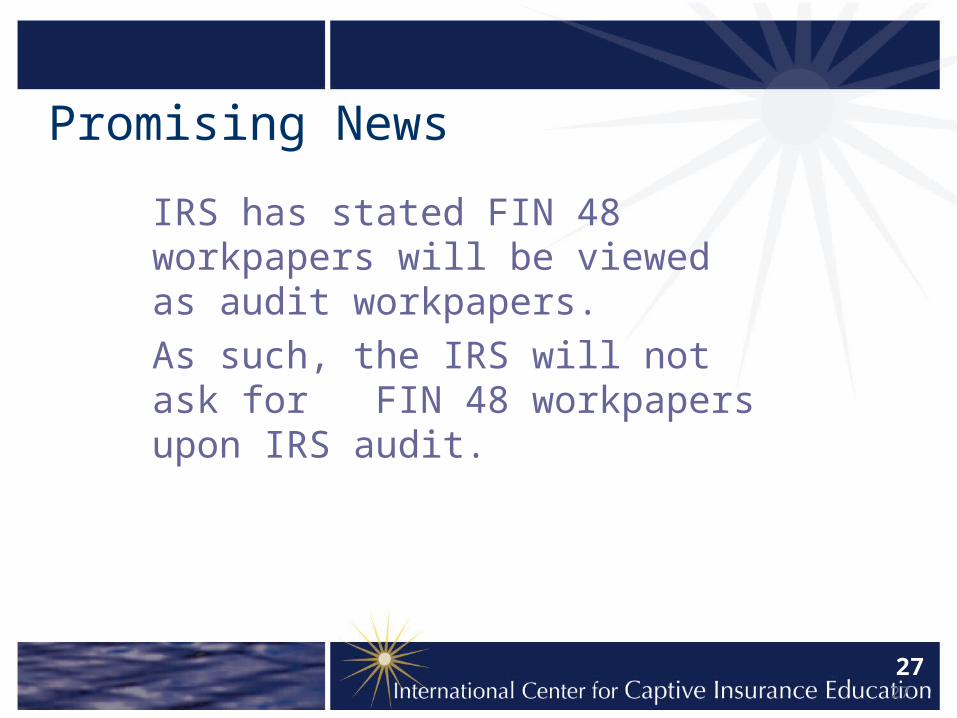

Promising News

IRS has stated FIN 48 workpapers will be viewed as audit workpapers.

As such, the IRS will not ask for FIN 48 workpapers upon IRS audit.

27

28

Part Two: The Future

• Treasury Decision 9329

• FAS 157

• FAS 159

29

Treasury Decision 9329

• Issued June 2007– Finalizes IRS Regulations Sec. 1.6012-2

• Every domestic life and non-life insurer filing a US federal income tax return must attach an annual statement– NAIC blank – 953(d) companies required to file a “pro-forma”

annual statement– No guidance but potential SAP requirement

30

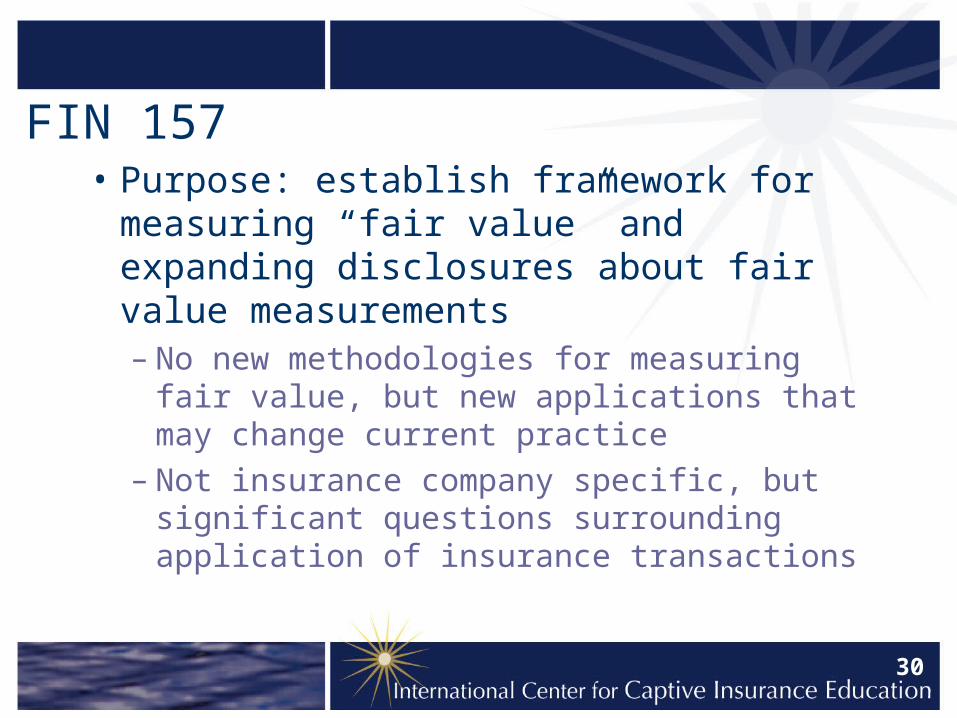

FIN 157• Purpose: establish framework for

measuring “fair value” and expanding disclosures about fair value measurements– No new methodologies for measuring fair

value, but new applications that may change current practice

– Not insurance company specific, but significant questions surrounding application of insurance transactions

31

“Fair Value” Definitions

• Prior to Statement No. 157 multiple possible definitions, limited guidance as to how to apply them in GAAP

• Objective is increased consistency• Retains/reinforces concept that “fair value”

is based on an “exchange price”• Any gain or loss resulting from

reclassification reported as a cumulative adjustment to retained earnings.

32

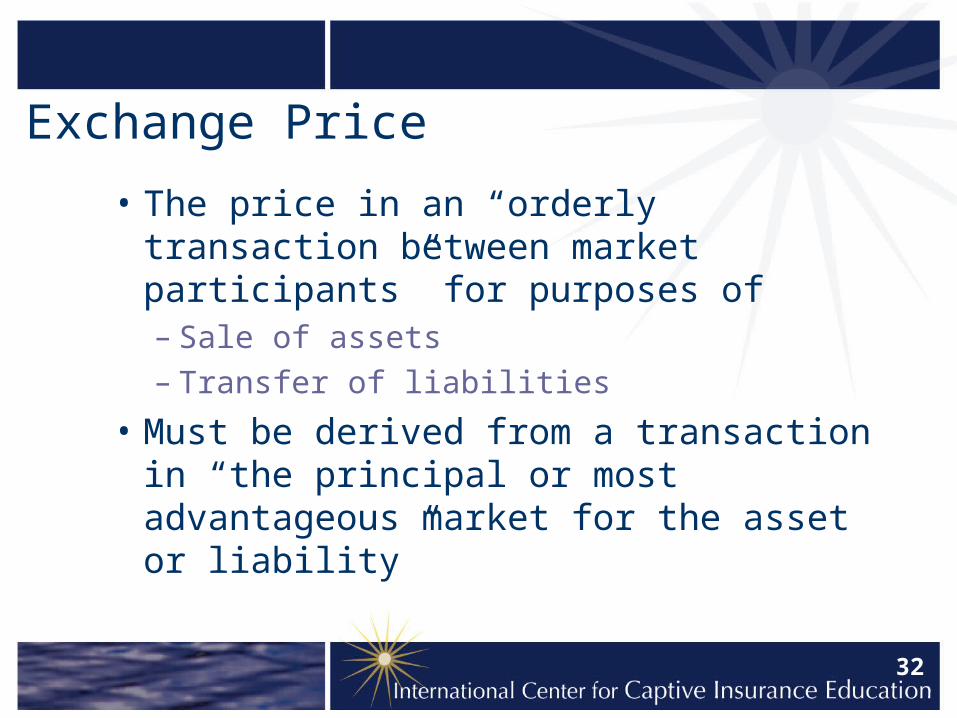

Exchange Price

• The price in an “orderly transaction between market participants” for purposes of– Sale of assets

– Transfer of liabilities

• Must be derived from a transaction in “the principal or most advantageous market for the asset or liability”

33

Fair Value Accounting

• Uses the exchange price based on a hypothetical transaction at the measurement date– The price that would be received if the asset

sold or liability transferred (exit price), not the price paid to acquire the asset or assume the liability (entry price)

• Must be market not entity based– Establishes a “market hierarchy”

34

Market Hierarchy

Level 1: Observable price i.e. market participant assumptions independent of the reporting entity

Level 2: Observable inputs (pricing model)

Level 3: Unobservable i.e. reporting entity’s own assumptions (requires extensive disclosures)

Reporting entity may not ignore Level 1 and 2 information that is reasonably available without undue cost and effort

35

Risk• Inherent in valuation techniques• Fair value measurement must reflect

adjustment for risk– Assuming allowance for risk included in the exit

price

• Also reflect impact of restrictions on the sale or use of the asset– Assuming market participants would consider the

restriction when pricing the asset

36

How Could This Impact Insurers?

• Affirms previous statements– 115 Investments in Debt and Equity Securities– 133 Derivative Instruments and Hedging Activities– 107 Fair Value of Financial Instruments

(disclosures of)

• Clear application to accounting for invested assets but what about reserves/policy assets?

37

FASB Concept Stmt No. 6

• Elements of Financial Statements– Fair value measurement reflects current market

participant assumptions about the future inflows associated with an asset (increase in economic benefits) and future outflows associated with a liability (reduction in economic benefit)

• Implication that reserves must reflect future interest earnings and future service fees– Fair value will be the NPV of expected cash flows

under the policy or reinsurance agreement

38

Recording Discounted Reserves

• The commutation price, assuming a market for sale of the liability

• Will the IRS then require a discount to the fair value reserve amount, when calculating taxable income?

• Effective date of FIN 157 – Applies to financial statements issued for

fiscal years beginning after Nov. 2007

39

FIN 159

• Fair Value Option for Financial Assets and Liabilities

• Permits entities to choose to measure financial instruments at fair value.

• Objective: mitigate volatility in reported earnings ….without adoption of complex hedging provisions

40

FIN 159 does not apply to:

• Investment in subsidiary that entity is required to consolidate

• Interest in VIE• Employers’ and plans’ obligations for pension

and other post retirement benefits• Lease obligations• Deposit liabilities • Financial instruments that are component of

shareholder’s equity

41

FIN 159 does apply to:• Non-financial insurance contracts and

warranties that the insurer can settle by paying a third party to provide the goods and services

• The Fair Value Option permits the entity to choose to measure eligible items at fair value at specified election dates– Report unrealized gains and losses on items

for which the fair value option has been elected

42

The Fair Value Option

• Is applied to “entire instruments”, not to portions of instruments

• Is irrevocable

• Applies to entities with fiscal years beginning after Nov. 2007– Provided the entity has elected to apply the

provisions of FAS 157

43

Questions for the Panel Members?

44

Thank you

panel members for your participation today.

45

This program fulfills 1/3rd of the teleconference requirement for the completion of the Associate in Captive Insurance (ACI) designation.

It also counts as 100 minutes of continuing education (2 CPE credits) for CPAs via ICCIE’s certification through the National Association of State Boards of Accountancy (NASBA), as well as 2 continuing education credits for ACI designation recipients.