1 finance 7311 corporate financial planning. 2 financial planning l long-run corporate objectives...

TRANSCRIPT

1

FINANCE 7311FINANCE 7311

CORPORATE FINANCIAL PLANNING

2

FINANCIAL PLANNINGFINANCIAL PLANNING

Long-Run CORPORATE OBJECTIVES Maximize the Value of the Firm

Sub-objectives (INCREASE MARKET SHARE)

STRATEGIES (STEPS) SPECIFIC ACTION PLAN SWOT ANALYSIS; 4 P’S

– (PRICE STRATEGY)

3

Financial Planning, cont.Financial Planning, cont.

PERFORMANCE MEASUREMENTOJBECTIVE; SPECIFICWERE GOALS ACHIEVED?

(% MARKET SHARE)

BUSINESS PLAN => FINANCIAL PLANOperating & marketing strategies underlie a

financial plan

4

USES OF FINANCIAL PLANUSES OF FINANCIAL PLAN

PROJECTION OF FINANCIAL NEEDS Financial implications of corporate

strategies

PERFORMANCE MEASUREMENT A benchmark which reflects strategies

5

FINANCIAL MODELFINANCIAL MODEL

EQUATIONS A = D + E End Balance = Beg. Bal. + Add - Subtract

PARAMETERS Tax rate; NWC requirements

DECISION VARIABLES Investment; Financing

6

COMPONENTSCOMPONENTS

PRO-FORMA FINANCIAL STMTS CASH BUDGET SPECIFIC BUDGETS

Production Personnel Marketing; distribution Capital

7

PRO-FORMA B/S & I/SPRO-FORMA B/S & I/SSTEP 1: SALES FORECAST

Historical data Growth (size of pie & piece of pie) Capabilities (prod., mgmt, distrib.)

STEP 2: OTHER INFORMATION? YES ==> Use it Capital spending; Debt Schedule; ETC.

8

Pro-Forma’s, cont.Pro-Forma’s, cont.

NO => Does Account Vary With Sales? NO ==> SAME BALANCE AS LAST YEAR YES ==> PERCENTAGE OF SALES

PERCENTAGE OF SALES APPROACH

Increase account by % change in sales Keeps acct/sales ratio constant Ratio analysis from before helpful

9

% OF SALES EXAMPLE% OF SALES EXAMPLE

Last Year Sales: 10,000 Last Year Acct. Rec. 1,000 Forecast Sales Growth: 20% Forecast Sales: 10,000 X 1.2 = 12,000 Forecast Acct. Rec. 1,000 X 1.2 = 1,200 OR: 1,000/10,000 X 12,000 = 1,200

10

% of SALES - COMMENTS% of SALES - COMMENTS

Method of Last ResortAssets / Sales ratio is optimalAssumes Full CapacityAssumes Assets / Sales relation is linear

Economies of Scale Less than full capacity Sales decreases

11

Pro-Forma F/S, cont.Pro-Forma F/S, cont.STEP 3: EXTERNAL FINANCING

NEED

Balance Sheet Does Not Balance Plug is the Financing Need May use Cash or Debt as a Plug

STEP 4: B/S & I/S RELATIONS Net Income and Retained Earnings Depreciation Expense and Accumulated Depreciation Interest Expense and Debt

12

Pro-Forma F/S, cont.Pro-Forma F/S, cont.

STEP 5: WHAT-IF ANALYSIS Use well-planned spreadsheet Put variables in separate cells

PRO-FORMA EXAMPLE: SAMPLE APPAREL COMPANY

13

CASH BUDGETCASH BUDGET

Projection of future cash flowsPerformance benchmarkUseful for seasonal companies

More specific information

Provides same ‘financing’ need as pro-forma financial statements

14

Cash Budget, cont.Cash Budget, cont.

STEP 1: Obtain a Sales Forecast Weekly, Monthly, etc.

STEP 2: Project Amount & Timing of Cash Inflows

Primarily collection of sales How do we estimate timing? What are other inflows?

15

Cash Budget, cont.Cash Budget, cont.

STEP 3: Project amount & timing of cash outflows

Purchases Labor Capital Expenditures Dividends & interest Other Expenses

16

Cash Budget, cont.Cash Budget, cont.

STEP 4: NET CASH FLOWSTEP 5: FINANCING NEED/SURPLUS NET CASH FLOW

+ BEGINNING CASH = ‘ENDING’ CASH - DESIRED CASH = FINANCING NEED (= B/S PLUG)

17

GROWTHGROWTH

SOURCE OF SALES GROWTH: QUANTITY PRICE COMBINATION OF BOTH

QUANTITY INDUSTRY GROWTH (Pie) MARKET SHARE GROWTH (Piece of Pie)

18

Two Growth RatesTwo Growth Rates

INTERNAL GROWTH RATE

Rate of growth without resorting to external funds

∆ Assets = ∆ Equity ∆ Equity = Net income x retention ratio IGR = ROA x r The above computes ROA using BEGINNING

assets

19

IGR exampleIGR example

Wal-Mart 1994: ROA = 13.9%Income = $1.02 : Dividends = $0.13IGR = 13.9% x .8725 = 12.3%Suppose expected growth is 23%=> 10% will have to be financed

externally10% x 16,800MM = $1.68MM financing

need

20

Sustainable Growth RateSustainable Growth Rate

No external equity issuedDebt issued such that D/E is constant

What happens to D/E with IGR?

Want %∆ in equity = %∆ in debt ==> SGR = ROE x r Note: ROE is computed using

BEGINNING equity

21

Sustainable Growth, cont.Sustainable Growth, cont.

DuPont: ROE x r = Profitability x turnover x leverage x r Management choices: Squeeze more sales $ out of existing assets Squeeze more income out of existing sales $ Retain more earnings in the firm Be willing to accept more leverage Settle for less growth

22

GROWTH & FIRM VALUEGROWTH & FIRM VALUE

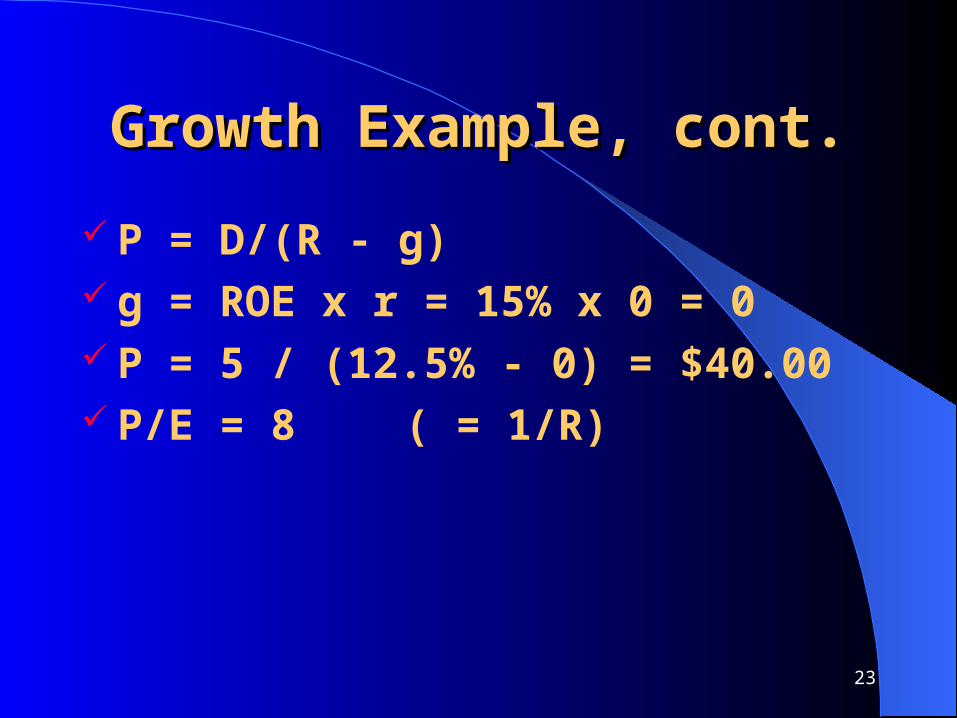

Growth should be Value Enhancing EXAMPLE: Suppose EPS = $5.00 R = 12.5% (Investors’ required return) ROE = 15% r = 0 (No reinvestment)

23

Growth Example, cont.Growth Example, cont.

P = D/(R - g) g = ROE x r = 15% x 0 = 0 P = 5 / (12.5% - 0) = $40.00 P/E = 8 ( = 1/R)

24

Growth Example, cont.Growth Example, cont.

Now, suppose r=60% (reinvest 60%) g = ROE x r = 15% x 60% = 9% D = 40% x 5.00 = $2.00 P = 2 / (12.5% - 9%) = $57.14 P/E = 11.43 Growth has increased Price and P/E!

25

Growth example, cont.Growth example, cont.

Suppose r = 60% as before ROE = 10% g = 10% x 60% = 6% P = $2 / (12.5% - 6%) = $30.77 P/E = 6.2 Growth has decreased both price and P/E! Growth creates Value when: ROE > R