1 impact 2020 the future and how it will affect design firms worldwide american insurance and design...

TRANSCRIPT

1

IMPACT 2020The Future and How It Will Affect Design Firms Worldwide

AMERICAN INSURANCE

AND DESIGN

CONFERENCE 2015

March 25, 2015

Salt Lake City, Utah

Frank A. Stasiowski, FAIA

Copyright 2015 by PSMJ Resources, Inc. All rights reserved

2

IMAGINE………

3

What If ………?????

4

But 1st…A Brief Look at History….

5

3 Monumental Turning Points for ALL Design Professionals……...

1. The Onslaught of Liability Fear and Insurance……..

2. From “Value” to “Time” Compensation….The FTC Decision……..

3. The great “AUTOCAD” giveaway………

6

So where are we today ????

7

Some Headlines This Morning…

DOW Leaps to Record Highs…..…but Can it Last ???

February New Home starts biggest # in 7 years….

Crippling Blackouts paralyze South Africa…..

New Home Building gets Big Lift in February…..

Retirement WORRY is highest in 23 Years…..

Two Americans aboard downed Alpine jet……..

Today’s Teens want No Part of Huge School Loan Debt…..

Ukraine to STOP buying Russian gas next month…….

Heinz-Kraft deal announced….

March Madness will Waste Millions of Employee Hours….

7

8

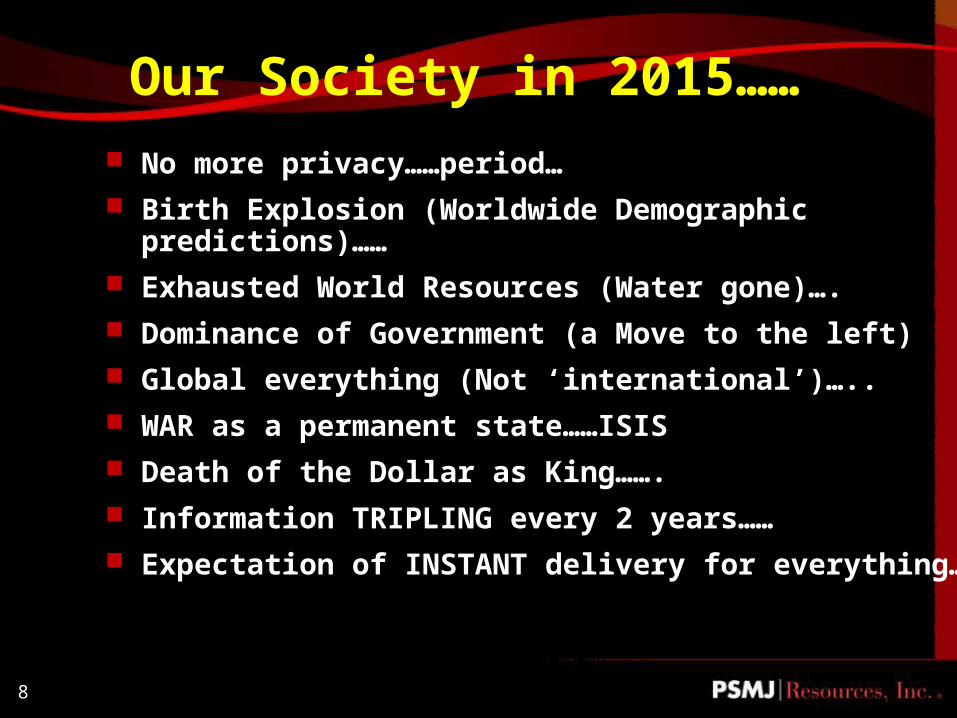

Our Society in 2015…… No more privacy……period… Birth Explosion (Worldwide Demographic

predictions)…… Exhausted World Resources (Water gone)…. Dominance of Government (a Move to the left) Global everything (Not ‘international’)….. WAR as a permanent state……ISIS Death of the Dollar as King……. Information TRIPLING every 2 years…… Expectation of INSTANT delivery for everything….

9

Did you know 2.0......????

9

http://www.youtube.com/watch?v=pMcfrLYDm2U

10

Three 2020 Mega-Forces and What They Mean to You…

11

Megaforce #1:Slower Global Growth

12

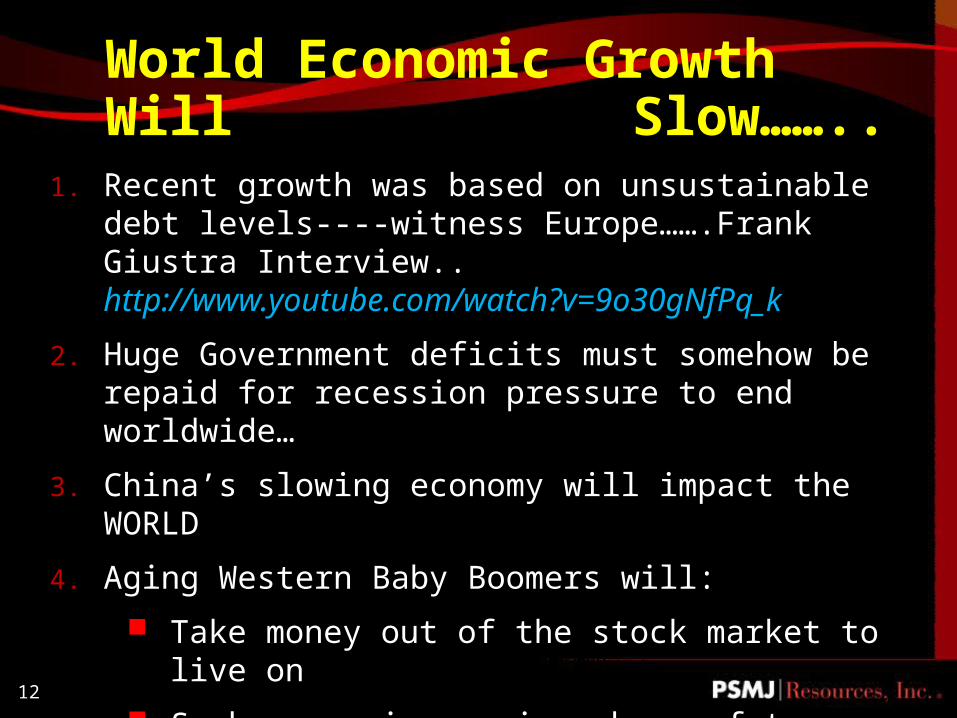

World Economic Growth Will Slow……..

1. Recent growth was based on unsustainable debt levels----witness Europe…….Frank Giustra Interview.. http://www.youtube.com/watch?v=9o30gNfPq_k

2. Huge Government deficits must somehow be repaid for recession pressure to end worldwide…

3. China’s slowing economy will impact the WORLD

4. Aging Western Baby Boomers will:

Take money out of the stock market to live on

Suck up an increasing share of tax revenues

13

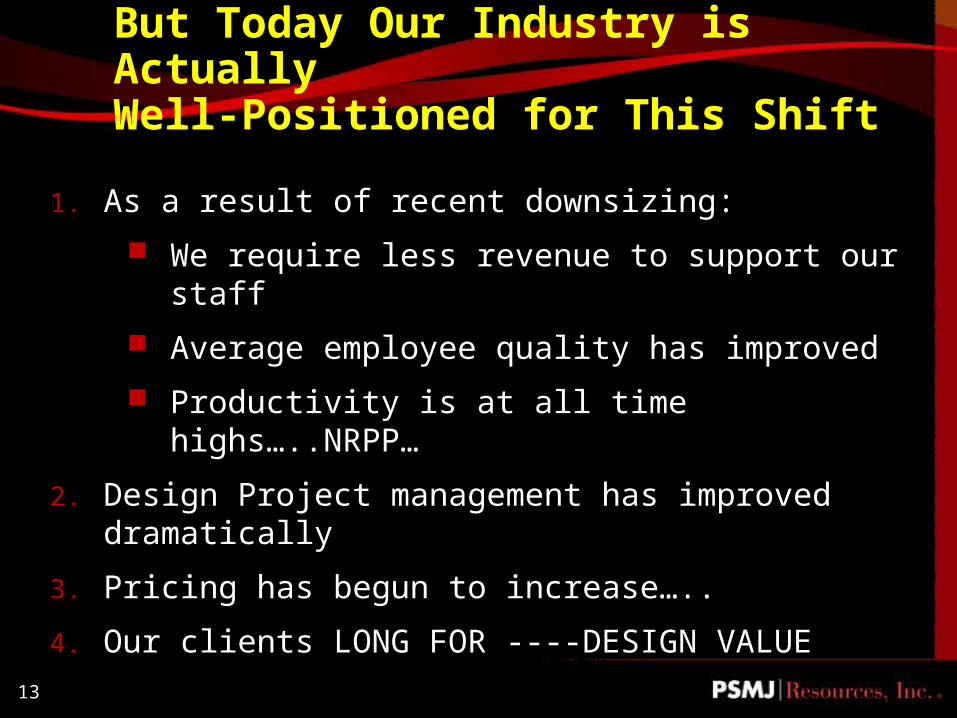

But Today Our Industry is Actually Well-Positioned for This Shift

1. As a result of recent downsizing:

We require less revenue to support our staff

Average employee quality has improved

Productivity is at all time highs…..NRPP…

2. Design Project management has improved dramatically

3. Pricing has begun to increase…..

4. Our clients LONG FOR ----DESIGN VALUE

14

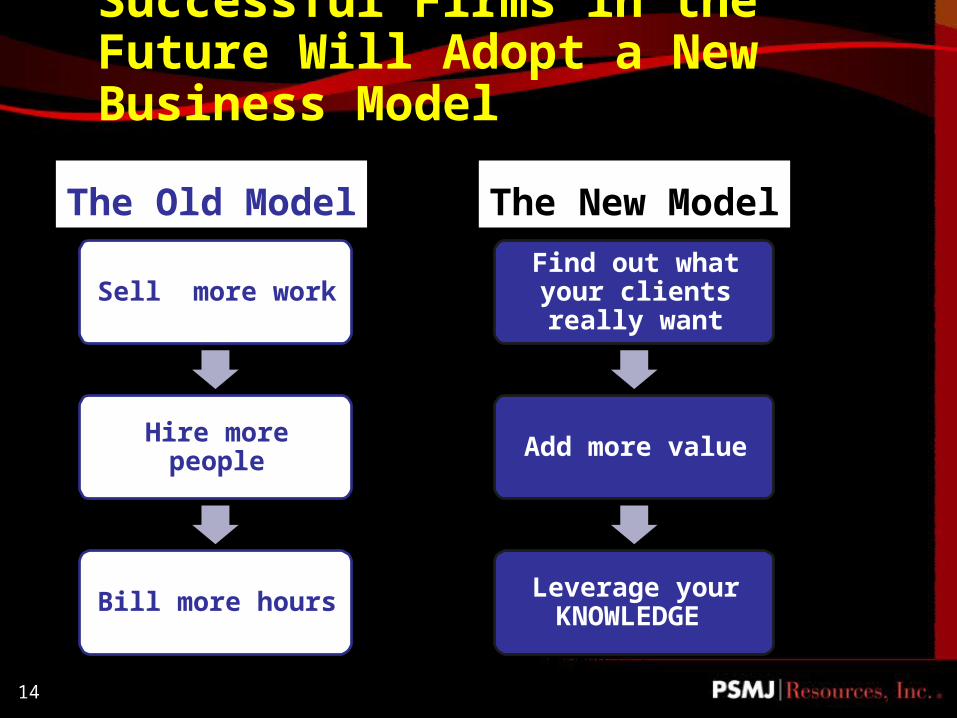

Successful Firms in the Future Will Adopt a New Business Model

The Old Model

Sell more work

Hire more people

Bill more hours

The New Model

Find out what your clients really want

Add more value

Leverage your KNOWLEDGE

15

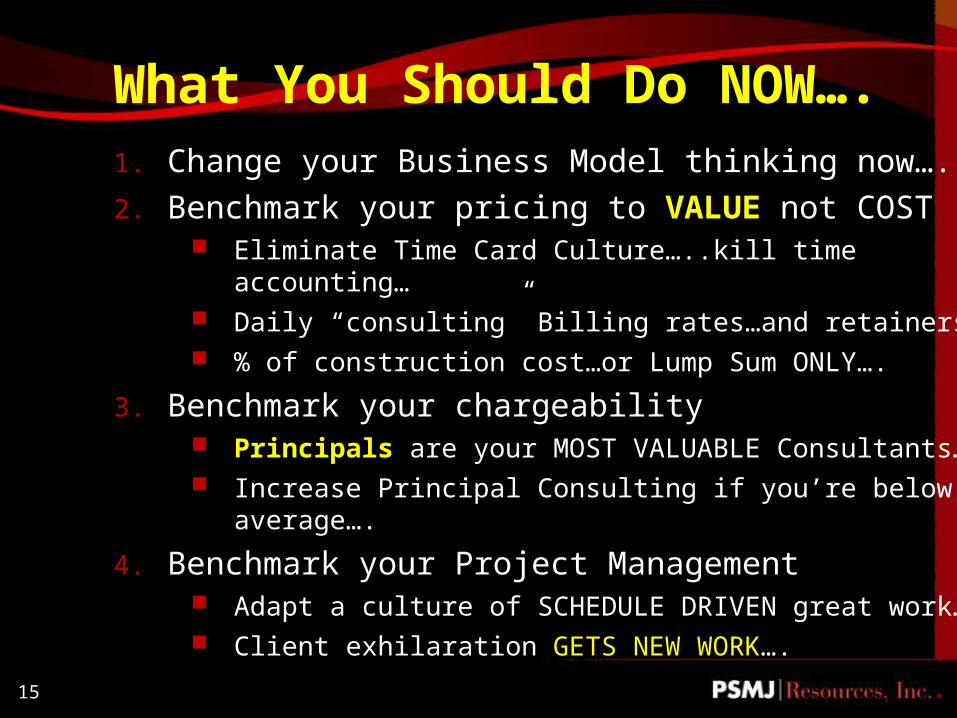

What You Should Do NOW….1. Change your Business Model thinking now….

2. Benchmark your pricing to VALUE not COST Eliminate Time Card Culture…..kill time accounting… Daily “consulting” Billing rates…and retainers… % of construction cost…or Lump Sum ONLY….

3. Benchmark your chargeability Principals are your MOST VALUABLE Consultants… Increase Principal Consulting if you’re below average….

4. Benchmark your Project Management Adapt a culture of SCHEDULE DRIVEN great work… Client exhilaration GETS NEW WORK….

16

Megaforce #2:The Retiring Baby Boomers

17

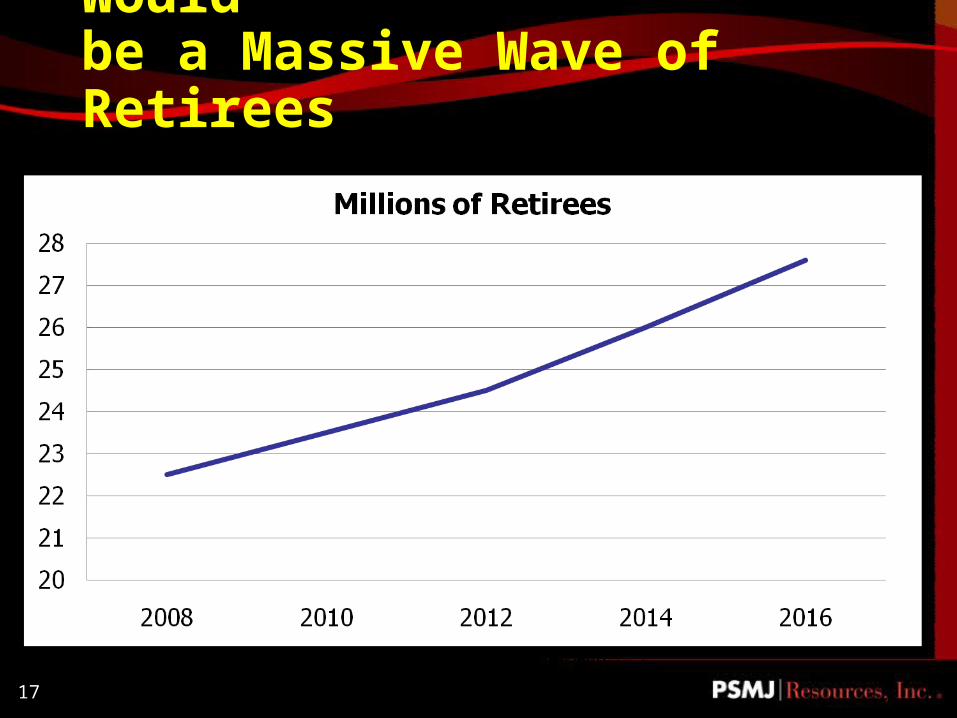

It Looked Like There Would

be a Massive Wave of Retirees

18

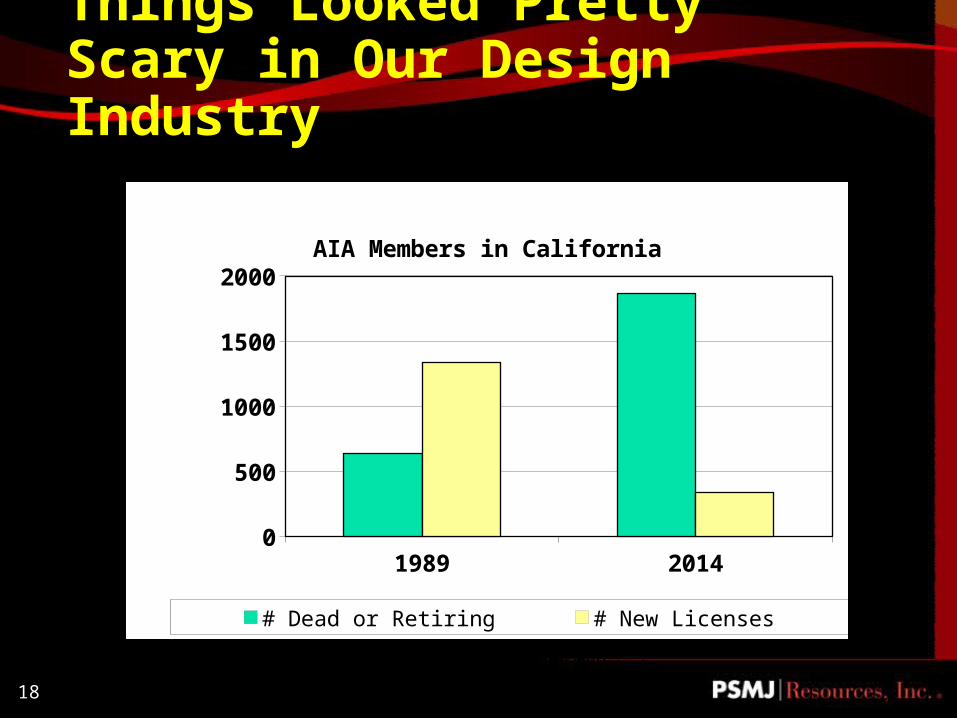

Things Looked Pretty Scary in Our Design Industry

1989 20140

500

1000

1500

2000AIA Members in California

# Dead or Retiring # New Licenses

19

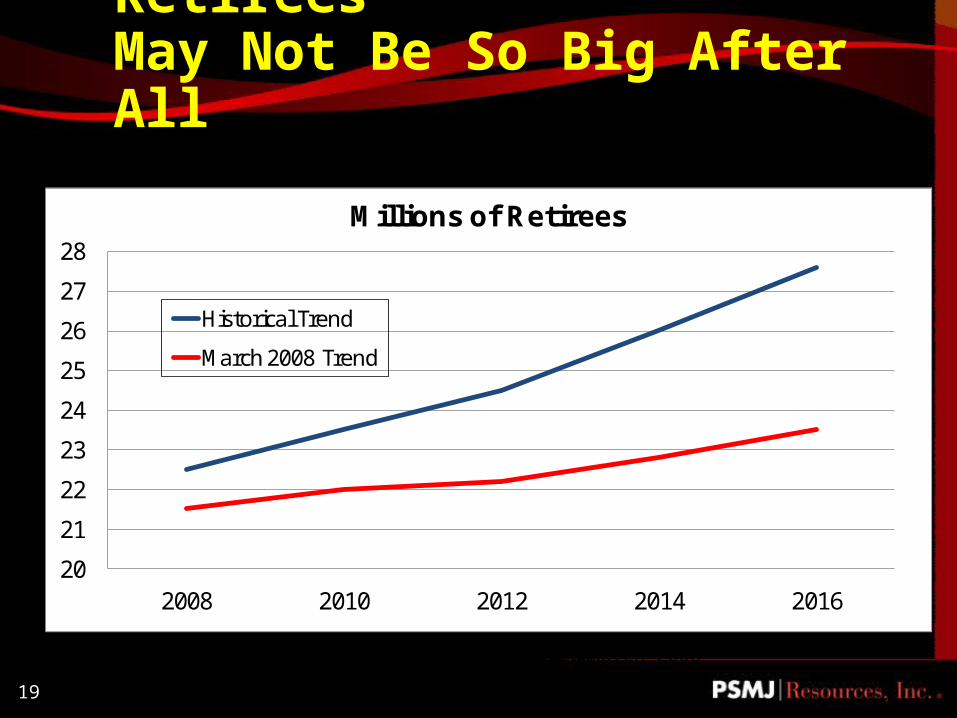

…But That Wave of Retirees May Not Be So Big After All

20

21

22

23

24

25

26

27

28

2008 2010 2012 2014 2016

Millions of Retirees

Historical Trend

March 2008 Trend

Source: The Coyne Partnership, March 2008

20

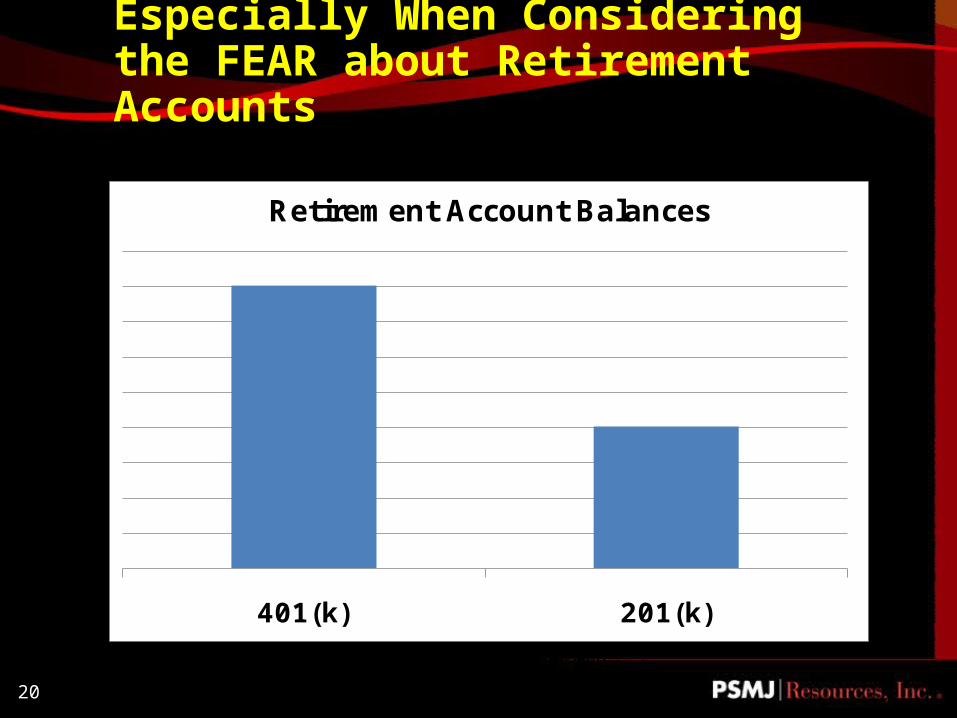

Especially When Considering the FEAR about Retirement Accounts

401(k) 201(k)

Retirement Account Balances

21

What You Should Do NOW…

1. Team retirees with college students…..

2. More Independent Contractors…….

3. Look at “partial retirees” as a way to balance your workload……..

4. Start signing up retirees as “casual” employees………

5. Locate offices in areas with lots of retirees……..

22

Megaforce #3:The Surge in Ownership Transition

23

Mass Exodus of Senior Principals May Be Delayed…

1. Leading edge of baby-boomers now hitting a YOUNG age 65…………..

2. Many are founders or senior principals with lots of stock that has lost value since 2005……….

3. Few have developed long-term ownership transition plans and really want to stay…….

4. Even fewer have developed the next generation of leaders…………..

5. Result will be many failed ownership transitions…...

6. There will also be many more acquisitions…….

24

What Should You Do?

1. Formalize and document your firm’s thought leadership and institutional knowledge ASAP.

2. Create a Financial Capitalization model for a 10-year ownership transition plan tied to Growth expectations.

3. Start a formal leadership development program that captures 25 year olds now. If you already have one, put it into higher gear.

4. If you don’t have enough time for an internal transition, position your firm for a successful external merger. (For an outline of a “Marketability Assessment,” e-mail me at [email protected]

25

Demographics Drives our World......

25

As a Species we humans are predictable in how we impact the food chain…..

26

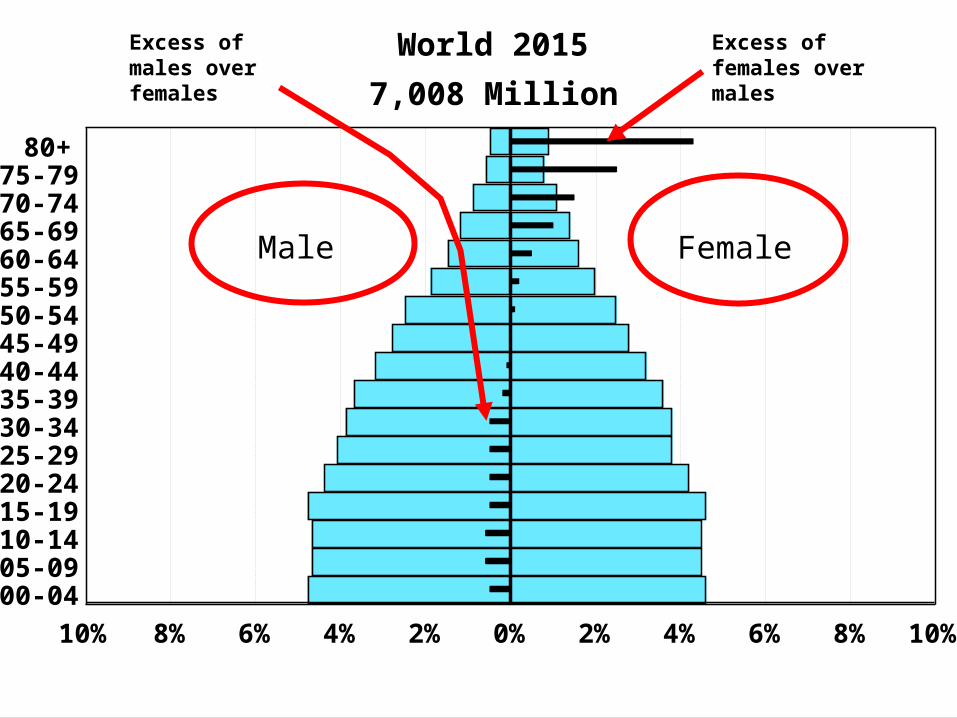

World 2015

7,008 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 2% 4% 6% 8% 10%

FemaleMale

Excess of males over females

Excess of females over males

27

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

India 20151,080 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

China 20151,306 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Italy2015 58 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Japan 2015127 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Mexico 2015106 Million

Russia 2015143 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

United States 2015298 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Canada 201533 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Iran 201568 Million

28

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

World 20157,009 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

More Developed Countries 20151,210 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Less Developed Countries 20155,841 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Near East 2015191 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Latin America and the Caribbean 2015555 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Western Europe 2015396 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Central Africa 2015891 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

South America 2015371 Million

80+75-7970-7465-6960-6455-5950-5445-4940-4435-3930-3425-2920-2415-1910-1405-0900-04

0%2%4%6%8%10% 0% 2% 4% 6% 8% 10%

FemaleMale

0 5 10-5-10

Northern Africa 2015159 Million

29

0

1

2

3

4

5

0 10 20 30 40 50 60 70 80 90 100

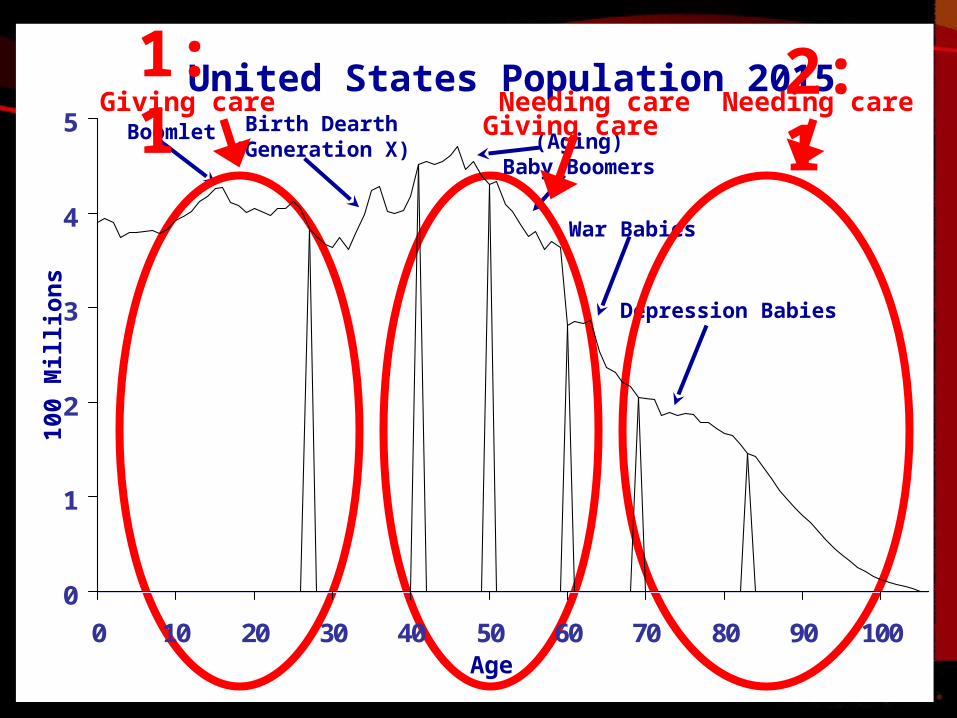

United States Population 2015

Depression Babies

(Aging)Baby Boomers

Boomlet Birth Dearth(Generation X)

War Babies

100

Mi l

l io n

s

Age

Giving care

2:1Needing careNeeding care

1:1Giving care

30

With this DATA How Does the Immediate Future Look for Design Firms Worldwide ???

Results of PSMJ’s Quarterly Market Forecast for Q3 2010( 538 Firms Reporting)

31

A Few Overall 2015 Trends….

31

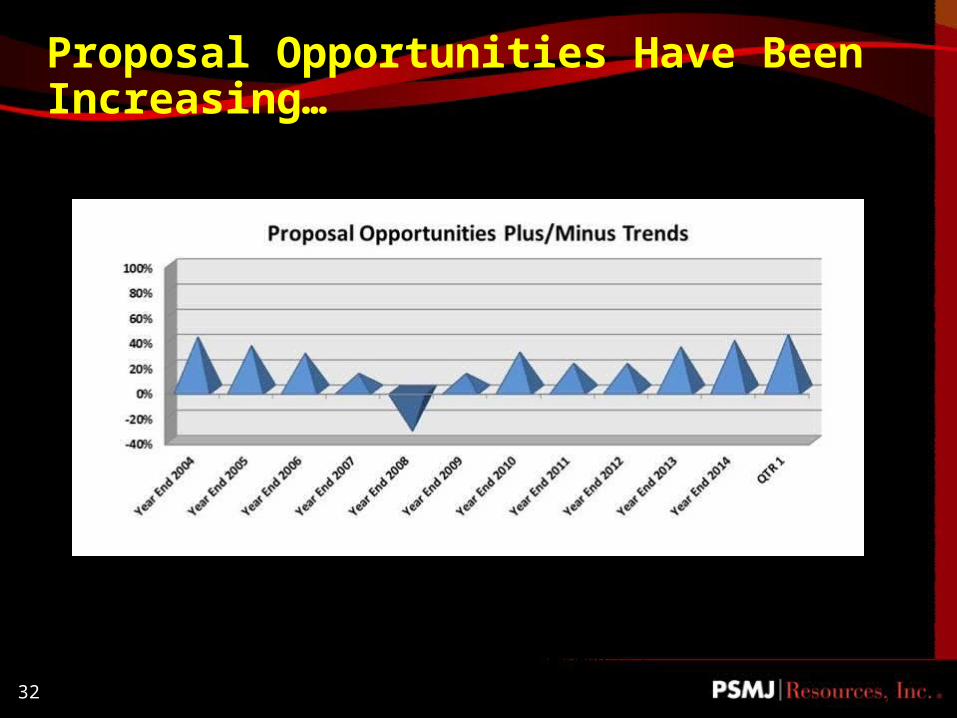

32

Proposal Opportunities Have Been Increasing…

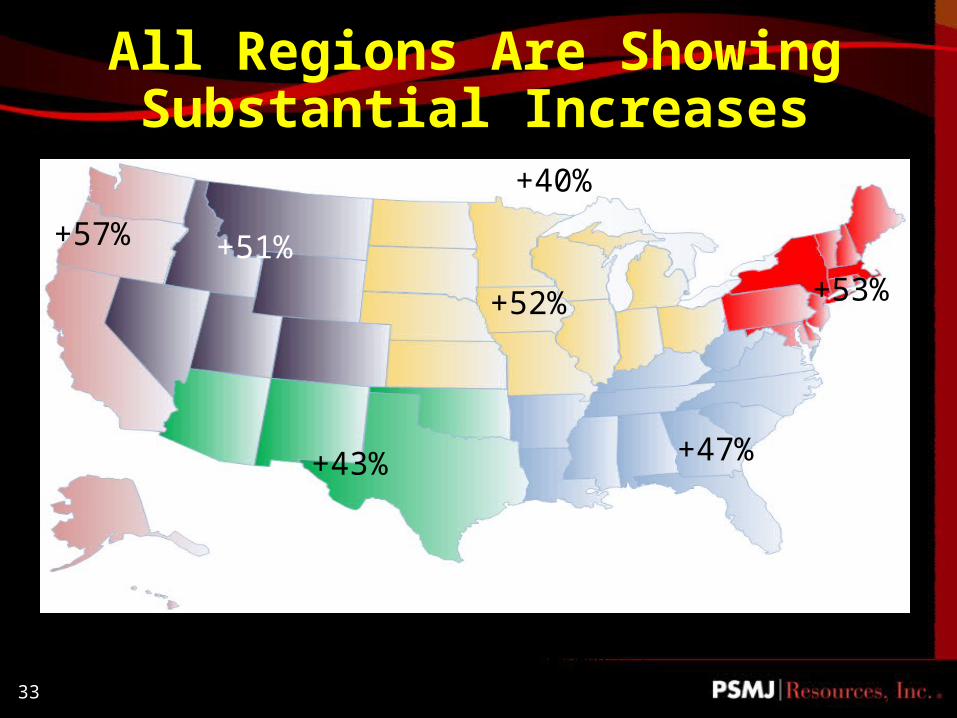

33

All Regions Are Showing Substantial Increases

+53%

+47%

+52%

+43%

+51%+57%

+40%

34

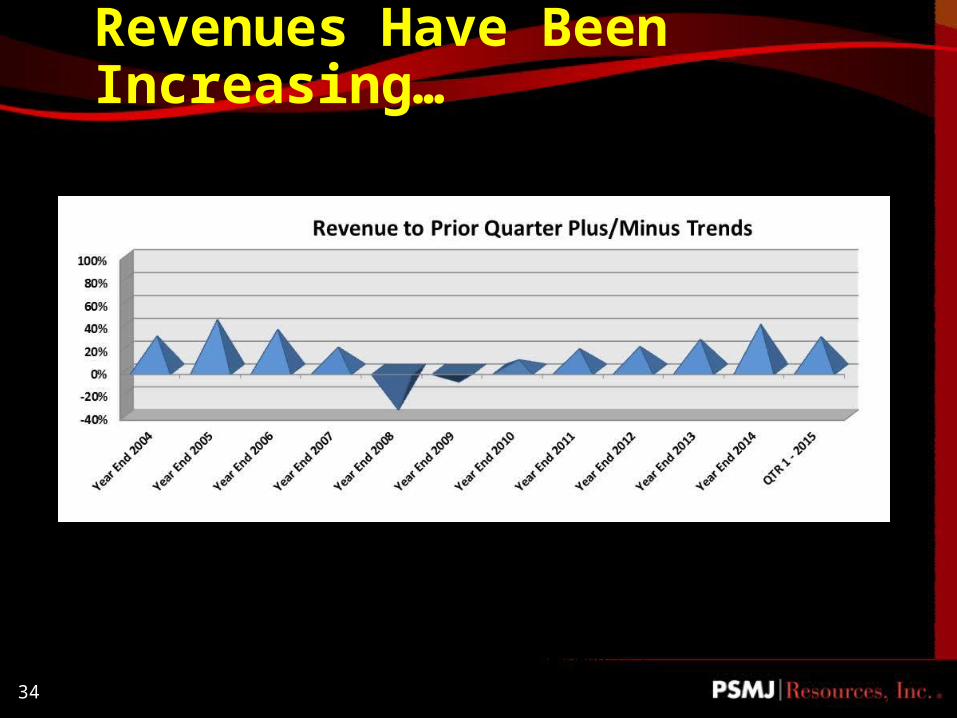

Revenues Have Been Increasing…

35

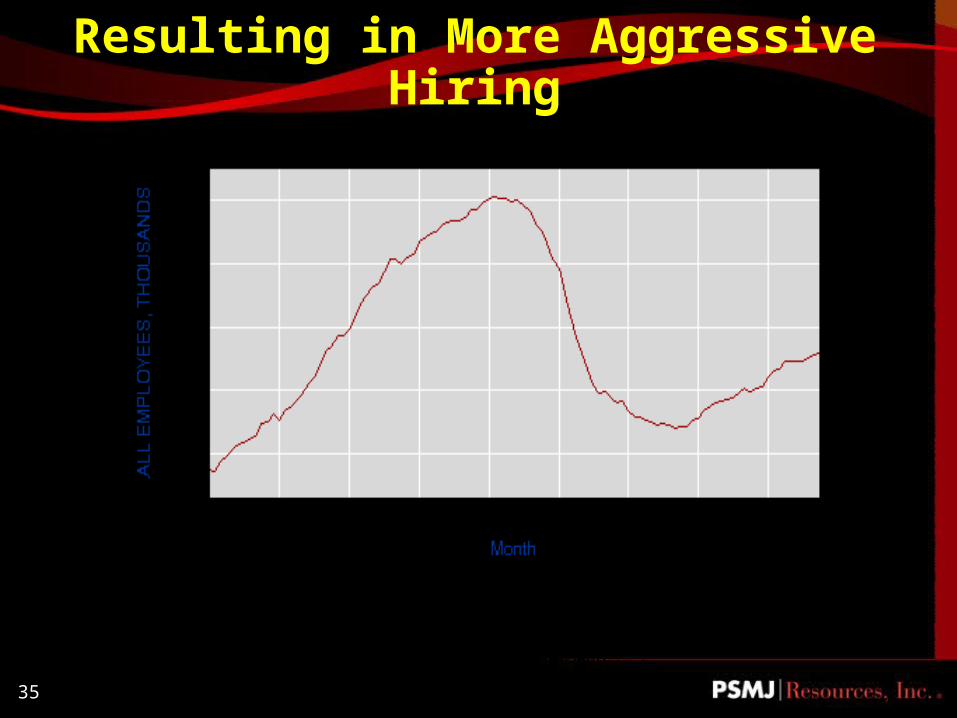

Resulting in More Aggressive Hiring

Source: U.S. Department of Labor

36

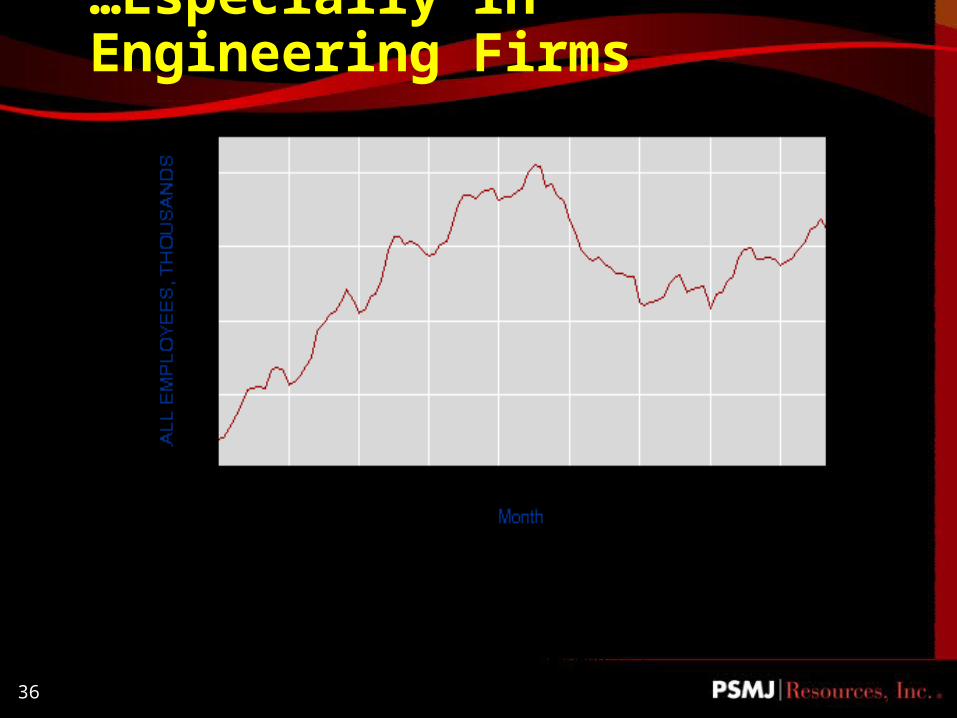

…Especially in Engineering Firms

Source: U.S. Department of Labor

37

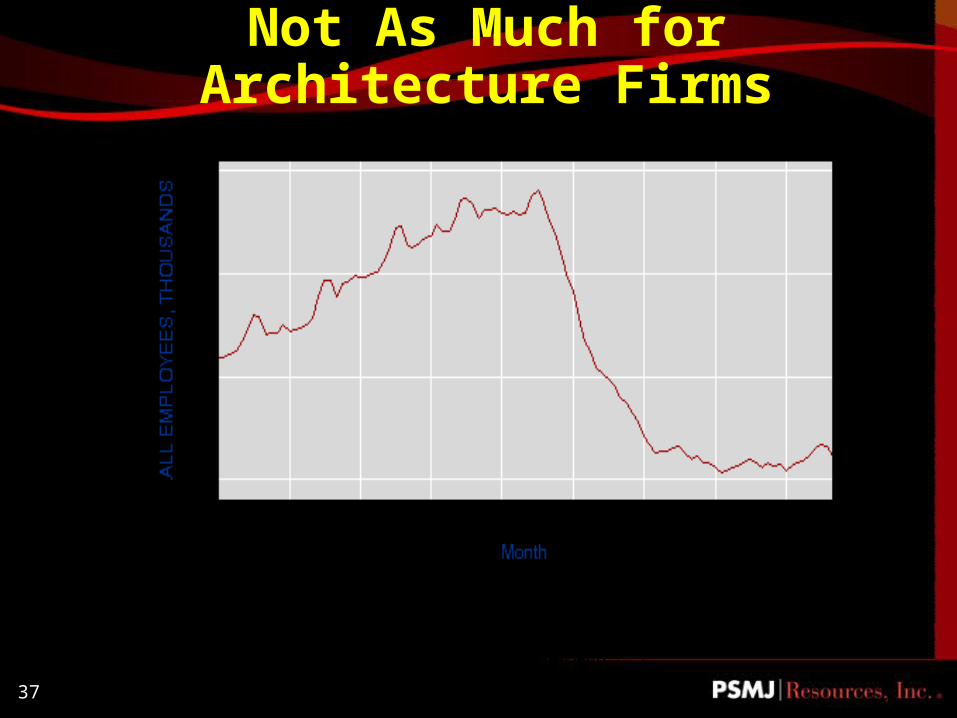

Not As Much for Architecture Firms

Source: U.S. Department of Labor

38

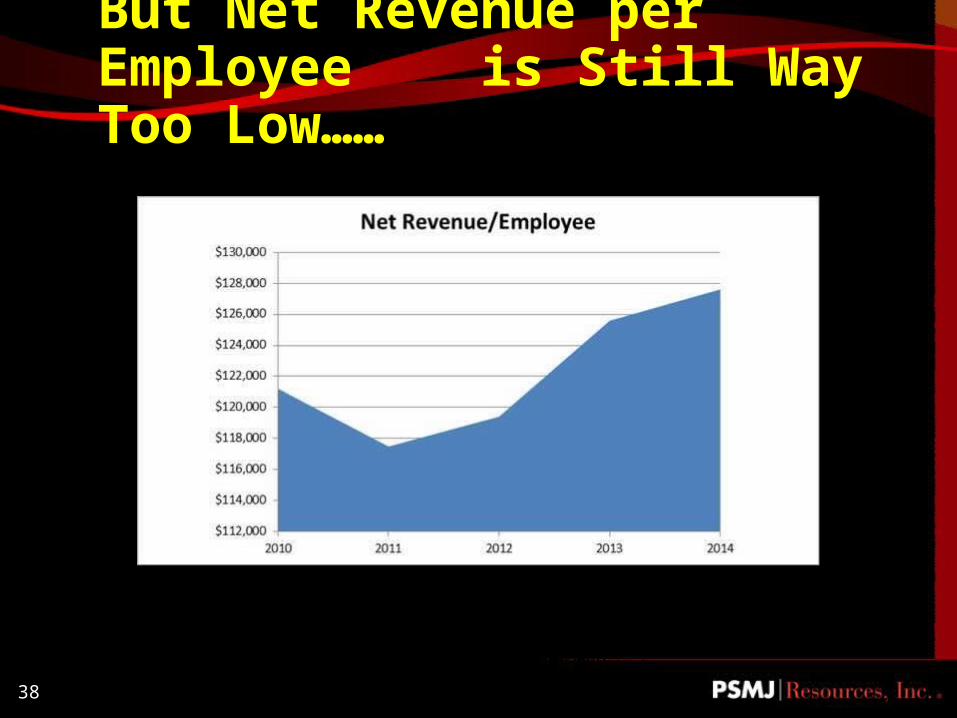

But Net Revenue per Employee is Still Way Too Low……

39

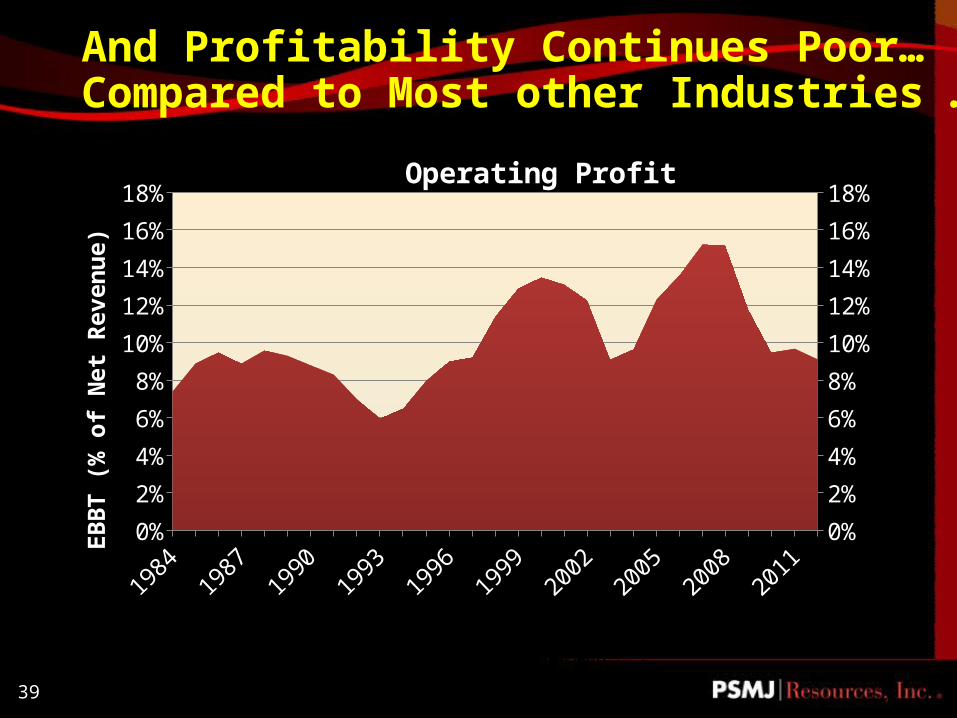

And Profitability Continues Poor…Compared to Most other Industries …..

19841986

19881990

19921994

19961998

20002002

20042006

20082010

20120%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%Operating Profit

EBBT

(% o

f Net

Rev

enue

)

40

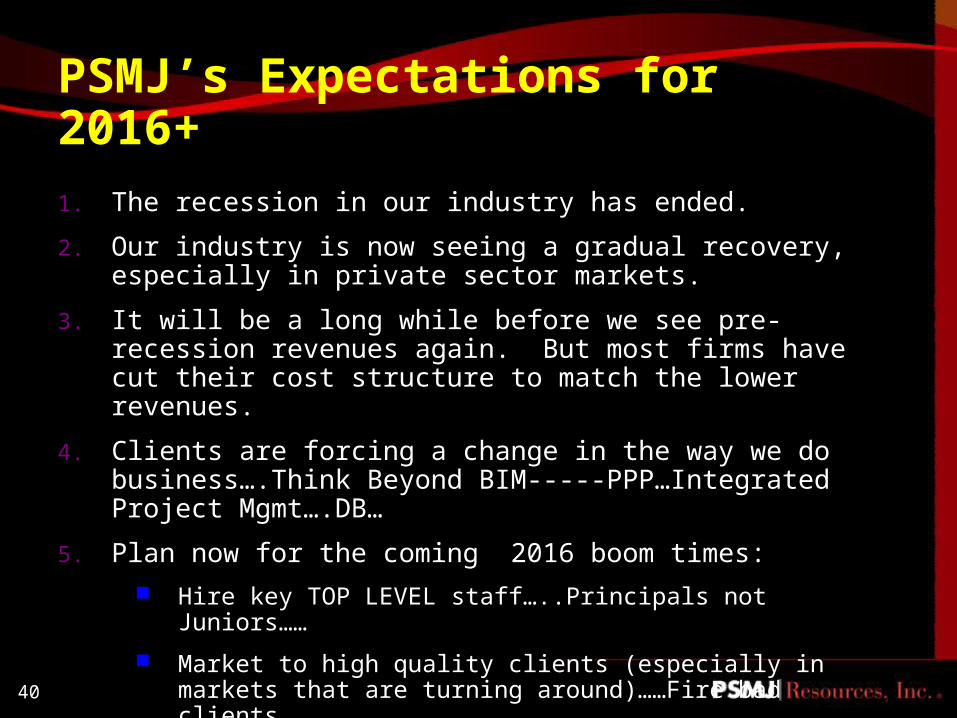

PSMJ’s Expectations for 2016+1. The recession in our industry has ended.

2. Our industry is now seeing a gradual recovery, especially in private sector markets.

3. It will be a long while before we see pre-recession revenues again. But most firms have cut their cost structure to match the lower revenues.

4. Clients are forcing a change in the way we do business….Think Beyond BIM-----PPP…Integrated Project Mgmt….DB…

5. Plan now for the coming 2016 boom times: Hire key TOP LEVEL staff…..Principals not Juniors……

Market to high quality clients (especially in markets that are turning around)……Fire bad clients….

Make acquisitions now before prices for firms increase dramatically

41

Now Let’s IMAGINE ….

the Bold New 2020 and Beyond Future for Our Profession…..

42

43

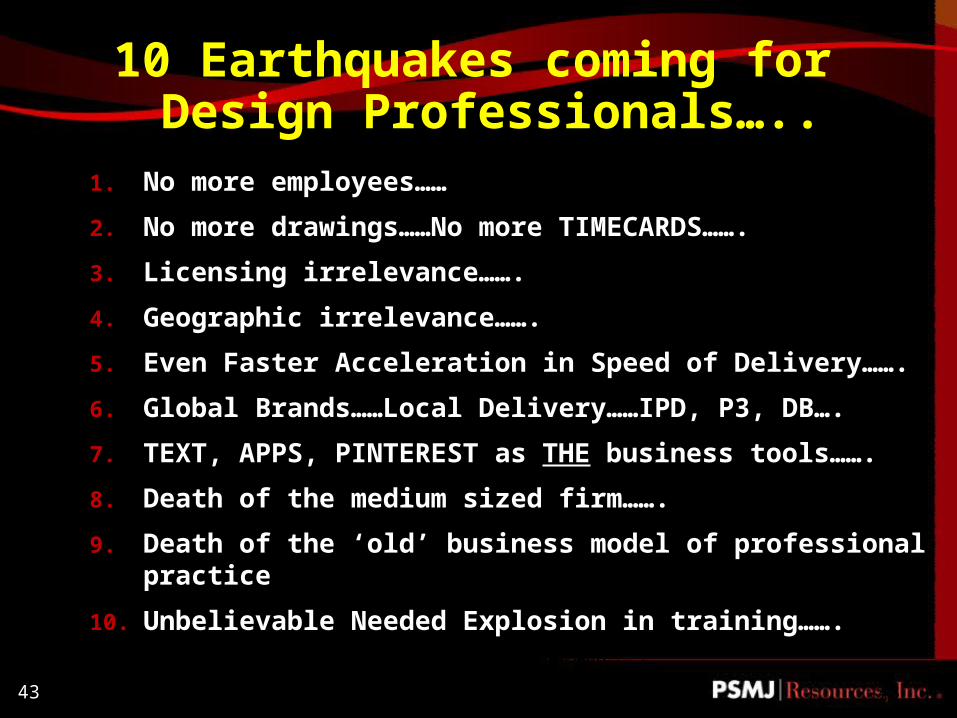

10 Earthquakes coming for Design

Professionals…..1. No more employees……

2. No more drawings……No more TIMECARDS…….

3. Licensing irrelevance…….

4. Geographic irrelevance…….

5. Even Faster Acceleration in Speed of Delivery…….

6. Global Brands……Local Delivery……IPD, P3, DB….

7. TEXT, APPS, PINTEREST as THE business tools…….

8. Death of the medium sized firm…….

9. Death of the ‘old’ business model of professional practice

10. Unbelievable Needed Explosion in training…….

43

44

Could this be YOUR Biggest Opportunity in Decades ?????

44

45

Some Tough Questions Moving Forward……..

46

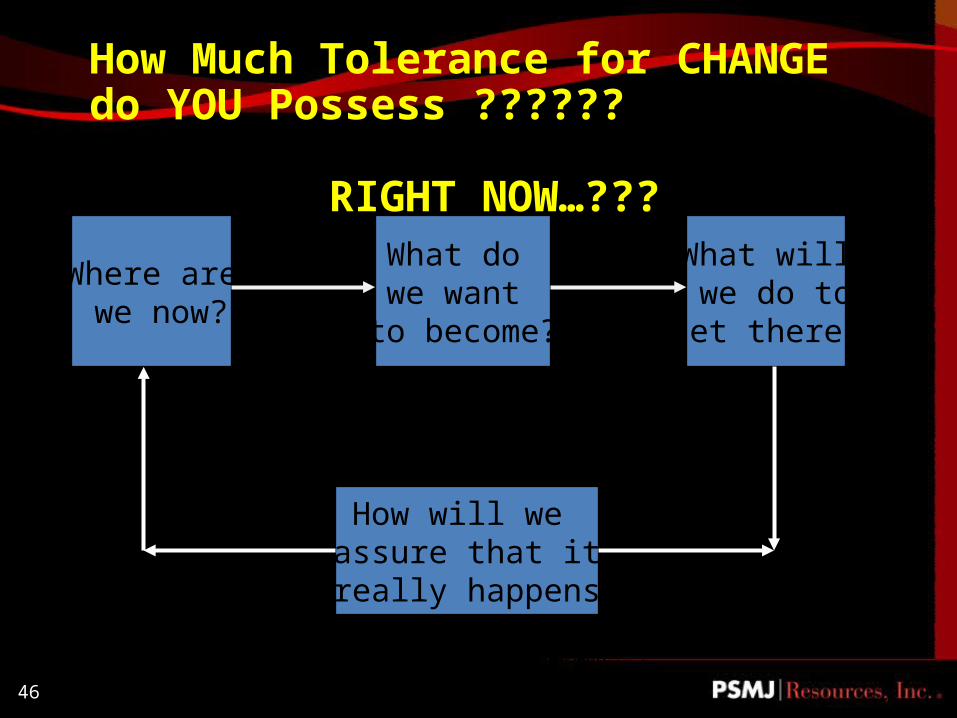

How Much Tolerance for CHANGE do YOU Possess ??????

RIGHT NOW…???

Where are we now?

What do we want

to become?

What will we do toget there?

How will we assure that it

really happens?

47

Imagine……………. What does 2020 really look like for YOU personally?? Are you Ready ???

48

Purpose….What are YOU here for ?

49

What are the Principles That DRIVE

you…..???

50

What are Your Immediate Tasks………???

51

Do you have the PASSION to Shake the Trees or Will You FOLLOW the Leemings ???

52

Can You Really Embrace CHANGE IN every facet of your approach to…..?

Marketing

Growth

Project Delivery

Design for Value

Human Resources

IT

Finance

Leadership Transition

Capitalization

Acquisitions

Global Culture

Business Model

53

9 Urgent Actions you must take right now…….

Adapt a CULTURE of permanent change…… Restructure how you are capitalized….. Embrace technological new ideas BEFORE your

competitors….. Share your Intellectual Capital FREELY….. Build a network of knowledge you can tap fast.. Control your clients through speed of delivery…. Price and contract what you do in a brand new way…. Treasure and Build Your Relationships…… Embrace RISK….It is the LIFEBLOOD of CHANGE….

54

Remember……

“Change always brings bold new opportunities…..be vigilant !!!! Think GLOBALLY!!! And most

importantly….Do it even faster…..!!!!!”

--Frank A. Stasiowski, FAIA

55

Bold Thoughts ?? Questions?? or Mind Blowing Comments Please !!

Call or connect with PSMJ Resources, Inc. at 617-965-0055 or

www.psmj.com

To contact Frank: Phone: 617/965-0055 E-mail: [email protected]

To contact Kate Allen re: PSMJ Survey Data: Phone: 303-549-8782 E-mail: [email protected]

For a copy of this Presentation, please email….. [email protected]

NOW….it’s up to you…..