1 introduction to sepa - ibm · pdf fileintroduction to sepa swg fss 2 enterprise payments...

TRANSCRIPT

© 2002 IBM Corporation

SWG FSS

Verena MICHEL

Introduction to SEPA

SWG FSS

© 2006 IBM Corporation2Enterprise Payments Platform - vm

As of today, different ‘types of payments’ coexist

They facilitate and support the transactions executed by the different economic

actors

– for the payment of the price of goods and services

– for the repayment of a debt.

The payments can take different forms :

- cash payment

- payment using a specific payment media : cheque, card, transfer

These payments represent very large volumes :

e.g. 16 billion transactions = 19000 billion € in France during 2006

- electronic payment (prepaid electronic burse)

SWG FSS

© 2006 IBM Corporation3Enterprise Payments Platform - vm

The European Central Bank is driving the standardisation of payments through the Single Euro Payments Area (SEPA) initiative

� SEPA vision: “…citizens can make payments throughout the whole area from a single bank account, using a single set of payment instruments, as easily and as safely as in the national context today” (ECB: Towards a Single Euro Payments Area, 3rd Progress Report, p4)

� Unique standard for electronic payment initiation and reconciliation (ECB: op cit, p5)

� “By 2010 transformation of infrastructures fully underway either by conversion of national infrastructures into pan-European infrastructures (no parallel domestic and

cross-border systems) or their elimination” (Ms G. Tumpel-Gugerell, ECB Board Member, 09/2004)

� Directive proposal by the Commission on Payment Services in the Internal Market (New Legal Framework) issued 1 December 05:

“Member states shall require the payer’s payment service provider to

ensure that….the amount ordered is credited to the payee’s account

at the latest at the end of the first working day following the point in

time of acceptance. However, up to 1 January 2010 …. may agree on

a period no longer than 3 days”

For more information see :

http://www.europeanpaymentscouncil.org

SWG FSS

© 2006 IBM Corporation4Enterprise Payments Platform - vm

EPCs vision of the Single Euro Payments Area

SEPA will work as a single

domestic payments market

in which citizens and

economic actors will be

able to make payments as

easily and inexpensively

as in their hometown.

This means a commitment

of all involved parties,

including users of payment

services and supportive

public authorities.

It will also require the

completion of the

proposed Payment

Services Directive, which

is intended to provide a

harmonised legal

environment.

Extract of the European Payment Council webpage

SWG FSS

© 2006 IBM Corporation5Enterprise Payments Platform - vm

Extensive change across all participants

� EPCDefine schemes and charging conventions

Define PEACH framework

Define and implement certification procedures

� 25 National Banking / Payment AssociationsDecision and timetable / transition on adoption of SEPA-compliant

schemes

Decision on clearing infrastructures: fold into PEACH, merge, wind down

Review legal / contractual frameworks

� 8,000 BanksTransition to SEPA schemes: standards, operating procedures,

access network(s)

Process changes

Lower cost of transaction

Customer education

� 2 million Corporate customers and government agencies

Transition to SEPA schemes: standards, operating procedures

Credit transfers (salary payment)

Direct Debits (customer payments)

Return messages

Link to finance systems

Review banking relationships outside home member state

� Service providers, operators, etcDefine role and services within and/or outside PEACH

Transition to SEPA schemes: standards, operating procedures,access network(s)

� MerchantsChanges to terminals

SWG FSS

© 2006 IBM Corporation6Enterprise Payments Platform - vm

• the regulatory rules need to be harmonised

• 70% of the payments (percentage of the card payments, direct debits and credit transfers

done in EURO) are concerned

•an important message transformation effort has to be delivered by all the economic actors, as

EPC has defined standard message formats based on XML ISO 20022

• at a first stage in the Euro zone (13 countries by January 1, 2008)

• at a second stage in the 25 European countries plus : Iceland, Liechtenstein, Norway and

Switzerland

•le large majority of the banks declared their intention to comply with the SEPA rules and

launch SEPA format transformation and payment system renewal projects by january 2008

•The other industries and the administrations will also need to adapt their billing and payments

systems to the SEPA formats

Direct SEPA impacts

SWG FSS

© 2006 IBM Corporation7Enterprise Payments Platform - vm

SEPA Timeline

� CT scheme

� DD scheme

� Cards framework

� CSM framework

� Legal framework

� Security requirements

� National products

� Sepa products

� Infra processes both

� Gradual market-driven migration

� Roll-out preparation

� Testing

SWG FSS

© 2006 IBM Corporation8Enterprise Payments Platform - vm

SEPA means new schemes and new processing infrastructures

Different methodologies have been

adopted for :

1. Credit Transfers and Direct

Debits got new Electronic

Transfer Schemes (ETS)

Key deliverables : SCT and

SDD Rulebooks which detail

core and basic services to

enable a common level of

service to users in a

predictable timeframe

2. Card payments will get their

schemes adapted

Key deliverable : SCF states

how issuers, acquirers, card

schemes and operators must

adapt their current operations

to comply to SEPA

SWG FSS

© 2006 IBM Corporation9Enterprise Payments Platform - vm

SEPA Credit Transfer (SCT) processing

• In general no important difference

to current transfer processing

• Not all types of existing credit transfers will

be replaced by SCT. The actors need to

ensure coexistence of the new with the

existing schemas

• The main required changes of the bank’s

processes are related to

•the coexistence of different schemas

•the SEPA payments must apply the

SEPA schemas

•new / additional Clearing and Settlement

actors are entering the market

•The format choice given to the

customers for issuing their payment

orders cf : Making SEPA a Reality, EPC066-06 version 1.3, page 39

SWG FSS

© 2006 IBM Corporation10Enterprise Payments Platform - vm

SEPA Direct Debit (SDD) Processing

cf : Making SEPA a Reality, EPC066-06 version 1.3, page 40

• Currently important differences exist between

the countries related to the mandate

processing

• The transposition of the Directive into country

law is not completed (impacts cross country

DD)

• The main changes of the bank’s processes

are related to :

•mandate handling process wich will need

to be reviewed and evt. rebuilt

•different schemas might coexist for some

time (country focused and cross country)

• Same clearing and settlement actors as SCT

• Same changes related to format and schema

changes as SCT

SWG FSS

© 2006 IBM Corporation11Enterprise Payments Platform - vm

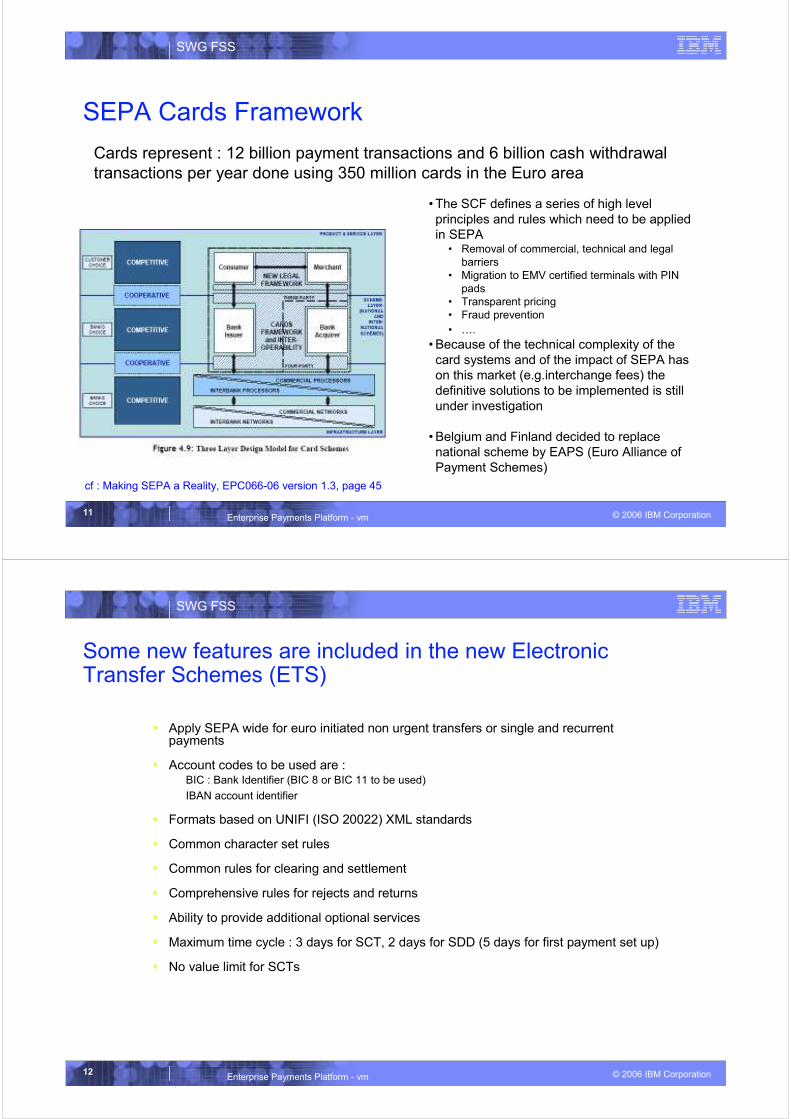

SEPA Cards Framework

cf : Making SEPA a Reality, EPC066-06 version 1.3, page 45

• The SCF defines a series of high level

principles and rules which need to be applied

in SEPA • Removal of commercial, technical and legal

barriers

• Migration to EMV certified terminals with PIN

pads

• Transparent pricing

• Fraud prevention

• ….

• Because of the technical complexity of the

card systems and of the impact of SEPA has

on this market (e.g.interchange fees) the

definitive solutions to be implemented is still

under investigation

• Belgium and Finland decided to replace

national scheme by EAPS (Euro Alliance of

Payment Schemes)

Cards represent : 12 billion payment transactions and 6 billion cash withdrawal

transactions per year done using 350 million cards in the Euro area

SWG FSS

© 2006 IBM Corporation12Enterprise Payments Platform - vm

Some new features are included in the new Electronic Transfer Schemes (ETS)

� Apply SEPA wide for euro initiated non urgent transfers or single and recurrent payments

� Account codes to be used are : BIC : Bank Identifier (BIC 8 or BIC 11 to be used)

IBAN account identifier

� Formats based on UNIFI (ISO 20022) XML standards

� Common character set rules

� Common rules for clearing and settlement

� Comprehensive rules for rejects and returns

� Ability to provide additional optional services

� Maximum time cycle : 3 days for SCT, 2 days for SDD (5 days for first payment set up)

� No value limit for SCTs

SWG FSS

© 2006 IBM Corporation13Enterprise Payments Platform - vm

Banks need to transform their processes and systems and create value-added services

� Impact on retail business of banksPressure from monolines will increase

International players are aggressively building scale via acquisition (e.g. BNP Paribas bid for BNL in Italy)

Innovative new services will be brought “cross-border”

Increased competition for high-net-worth clients as new services launched aimed at “residences abroad” clientele

Move to D+1, also for cross-border payments, versus D+2 or D+3 which are common today (proposed EU Payments Directive)

� Impact on payments will be significant – a threat and an opportunityGlobal Corporations like Philips currently hold many accounts with local banks to facilitate payments to employees and local suppliers

They will want to use one format to make payments across all geographies

Going forward, they could close down out-of-home country accounts and push them to a large bank in home country – or a “foreign” global bank

Global banks like Citibank, HSBC , etc., are also targeting the small and medium corporations and are investing in “payment engines” which will serve both the large and SME corporation

� As a consequence, Banks will need to develop value-added services to compensate for profit erosion

� Pan European Clearing Houses (PE-ACH) are competing for market shares

SWG FSS

© 2006 IBM Corporation14Enterprise Payments Platform - vm

A business process layer and a data model have been provided by EPC to enforce the standards (rulebooks)

� The Logical data model provides the correspondence between the Rulebooks and the UNIFI messages for :

– Customer to bank (C2B) space – initiation phase of Credit Transfer or DD ireti

– Bank to bank (B2B) space – clearing and settlement phaseDirect Debit collectionInterbank Payment Dataset for SCT

– Status/return/reject eventsAttn : requires exact copy of all the attributes of the rejected,… Dataset

– Reversal eventsApplicable only to SDD for reversal of the collection by the creditor

– Bank to customer space (B2C) – information on the collection or transfer information

� This information is delivered through :

– SDD Rulebook reference

– SCT Rulebook reference

– UNIFI message formats*

– ISO20022 element definition

*UNIFI : Universal Financial Industry message scheme, published by ISO20022

SWG FSS

© 2006 IBM Corporation15Enterprise Payments Platform - vm

Extract of the SCT Rulebook availableat EPC:

High level message usage and content for business users

SWG FSS

© 2006 IBM Corporation16Enterprise Payments Platform - vm

Extract of the SCT Documentation available at Unifi

SWG FSS

© 2006 IBM Corporation17Enterprise Payments Platform - vm

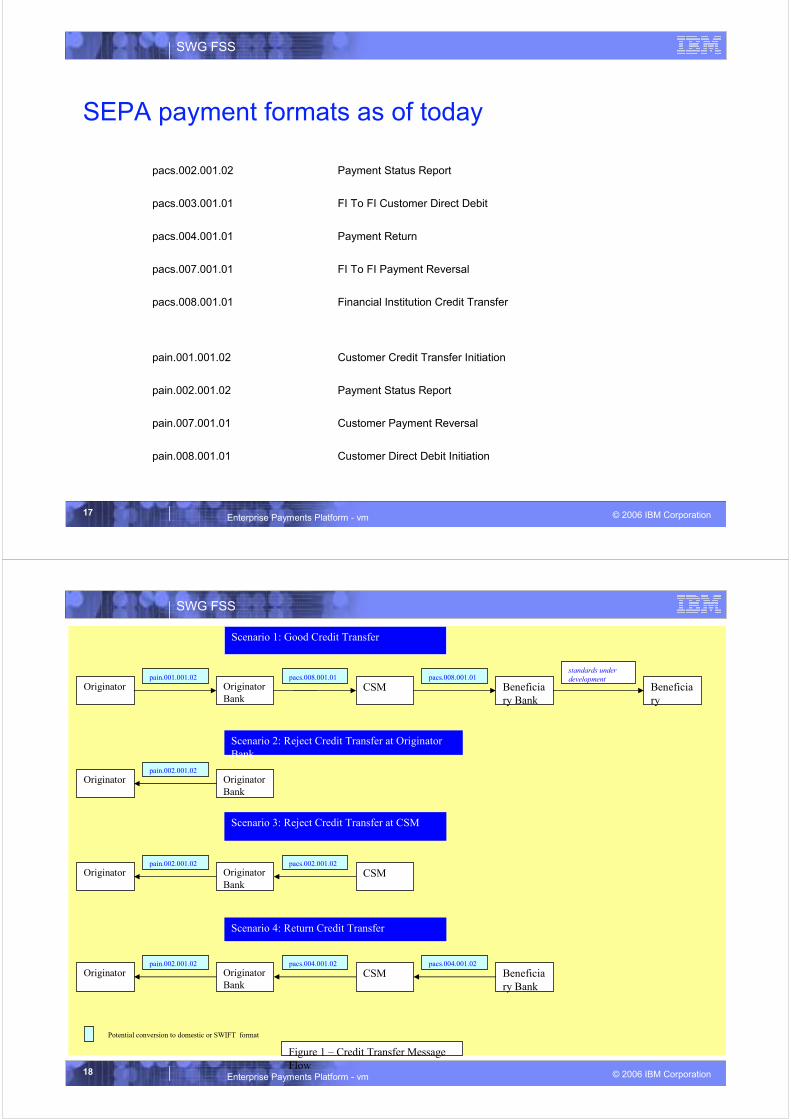

SEPA payment formats as of today

Customer Direct Debit Initiationpain.008.001.01

Customer Payment Reversalpain.007.001.01

Payment Status Reportpain.002.001.02

Customer Credit Transfer Initiationpain.001.001.02

Financial Institution Credit Transferpacs.008.001.01

FI To FI Payment Reversalpacs.007.001.01

Payment Returnpacs.004.001.01

FI To FI Customer Direct Debitpacs.003.001.01

Payment Status Reportpacs.002.001.02

SWG FSS

© 2006 IBM Corporation18Enterprise Payments Platform - vm

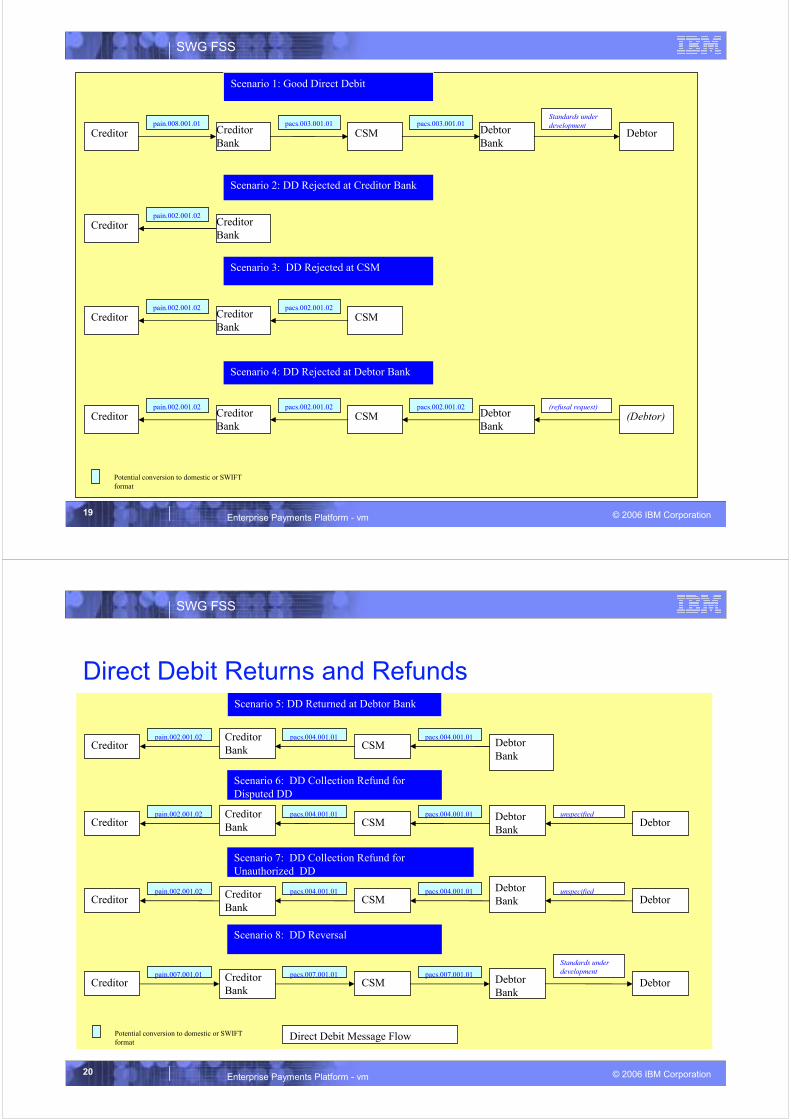

Originator Originator

BankCSM Beneficia

ry Bank

pain.001.001.02 pacs.008.001.01 pacs.008.001.01

Scenario 1: Good Credit Transfer

Originator Originator

Bank

pain.002.001.02

Scenario 2: Reject Credit Transfer at Originator

Bank

Originator Originator

BankCSM

pain.002.001.02

Scenario 3: Reject Credit Transfer at CSM

pacs.002.001.02

Originator Originator

BankCSM Beneficia

ry Bank

pain.002.001.02

Scenario 4: Return Credit Transfer

pacs.004.001.02 pacs.004.001.02

Beneficia

ry

standards under

development

Potential conversion to domestic or SWIFT format

Figure 1 – Credit Transfer Message

Flow

SWG FSS

© 2006 IBM Corporation19Enterprise Payments Platform - vm

Creditor Creditor

BankCSM Debtor

Bank

pain.008.001.01 pacs.003.001.01 pacs.003.001.01

Scenario 1: Good Direct Debit

Creditor Creditor

Bank

pain.002.001.02

Scenario 2: DD Rejected at Creditor Bank

Creditor Creditor

BankCSM

pain.002.001.02

Scenario 3: DD Rejected at CSM

pacs.002.001.02

Creditor Creditor

BankCSM Debtor

Bank

pain.002.001.02

Scenario 4: DD Rejected at Debtor Bank

pacs.002.001.02 pacs.002.001.02

Debtor

Standards under

development

(Debtor)

Potential conversion to domestic or SWIFT

format

(refusal request)

SWG FSS

© 2006 IBM Corporation20Enterprise Payments Platform - vm

Direct Debit Returns and Refunds

CreditorCreditor

Bank CSM Debtor

Bank

pain.002.001.02 pacs.004.001.01 pacs.004.001.01

Scenario 5: DD Returned at Debtor Bank

Creditor CSMDebtor

Bank

pain.002.001.02

Scenario 6: DD Collection Refund for

Disputed DD

Creditor CSMDebtor

Bankpain.002.001.02

Scenario 7: DD Collection Refund for

Unauthorized DD

Creditor CSM Debtor

Bank

pain.007.001.01

Scenario 8: DD Reversal

pacs.007.001.01 pacs.007.001.01

Debtor

Debtor

Debtor

Potential conversion to domestic or SWIFT

format

unspecified

unspecified

pacs.004.001.01pacs.004.001.01

pacs.004.001.01pacs.004.001.01

Standards under

development

Direct Debit Message Flow

Creditor

Bank

Creditor

Bank

Creditor

Bank

SWG FSS

© 2006 IBM Corporation21Enterprise Payments Platform - vm

For more information

� EPC : http://www.europeanpaymentscouncil.eu/index.cfm

� UNIFI formats : http://www.iso20022.org/

SWG FSS

© 2006 IBM Corporation22Enterprise Payments Platform - vm

The SEPA SEPA Data model*

� Describes the business processes and communication

needs (data sets and attributes) between parties. Defined in

the SCT and in the SDD Rulebook which focus on the B2B

space (only C2B minimum requirements are defined)

� Defines a solution which meets the business needs.

Structures data in a data flow containing logical messages

and complements the Rulebooks linking the data sets and

attributes to the message formats and elements defined in

the Physical Layer

� Provides the physical layer based on UNIFI Direct Debit

and Credit Transfer XML standards based on UNIFI

(ISO20022) XML and complemented by Implementation

Guidelines

Mandatory in the B2B space

Business Process Layer

Logical Data Layer

Physical Data Layer

*Published by the EPC (Doc: EPC029-06 version 2.2, 13 December 2006)

Has been defined as a 3 layer model :

SWG FSS

© 2006 IBM Corporation23Enterprise Payments Platform - vm

The banks are rising to the challenge

� European Payments Council (EPC):Have published SEPA Cards Framework and Rule Books for SEPA Credit Transfers and SEPA Direct Debits, for final approval 1Q06

Banks will be ready to offer these services to customers by Jan 2008

For Jan 2010: “confident that a critical mass will exist and that SEPA will be irreversible”

� Italy, Spain and Luxemburg committed quickly to transition to SEPA standards

� EBA announces "Multi-purpose Pan-European Direct Debit service" (M-PEDD) with 59 banks, live mid-2007

� European ACHs jostling for position

� Consolidation of infrastructures viewed as inevitable

� Preparation of a transition period of 4 to 5 yearswhich implies the management of the coexistence of the existing systems with SEPA

� UK reacts launching ‘UK Faster Payments initiative’