1 november 11, 2009 sony pictures entertainment mid range plan

TRANSCRIPT

1

November 11, 2009

SONY PICTURES ENTERTAINMENT

MID RANGE PLAN

2

Agenda

• Executive Summary• State of the Business

• SPE Divisional Details

o Motion Pictures o Home Entertainmento Domestic Televisiono International Televisiono Digital Production

• Financial Summary

• Closing

• Q & A

3

Executive Summary

4

Executive Summary

• Demand for our core product remains high

o 2009 YTD domestic box office revenues are up 5.3% from the same period in 2008

o U.S. Home Entertainment transactions are up 4% for the first half of 2009 vs. 2008

• Furthermore, we are still on track to meet our FYE10 EBIT target of $480 million

o However, $285 million of FYE10 EBIT is forecasted to come from asset sales

o This excludes approximately $66 million of incremental restructuring costs related to an in-process overhead reduction initiative

5

Executive Summary

• FYE10 has been subject to a number of challenges

o A decline in DVD sales due to the shift from sell thru to rental

o An adverse economic climate

o Lack of TV product in Syndication

o Continued investment in SPA – steady state not reached until FYE12

o Significantly lower margins and increased competition for direct-to-video product

6

Executive Summary

• Unfortunately, these challenges will continue to impact us throughout the MRP period, and most significantly in FYE11

• Our EBIT target for FYE11 is $300 million, excluding $15 million of restructuring costs

o If not for significant cost savings initiatives our EBIT for FYE11 would be closer to break-even

• Our Net Cash Flow target for FYE11 is break-even

o This cash flow target is very aggressive due to significant production spending for upcoming tentpole films in Columbia such as Spider-Man 4 and Men in Black III, the ramp-up of films within Sony Pictures Animation and higher spending per title for Screen Gems films

7

Executive Summary

• New company-wide initiative to reduce overhead by $100m

• Reducing theatrical and home entertainment marketing

• Restructured motion picture talent deals reducing upfront fees

• Cut TV production spend significantly, reducing our near-term commitment in Network TV

In order to minimize the impact to our operating results and cash flow, a number of major steps are

being undertaken

8

Executive Summary

• Significantly reduced our capital investments

• Driving mass market adoption of Blu-ray to mitigate the impact of the decline in DVD

• Continuing to expand our networks and international television production operations

• Pursuing new market segments in our traditional businesses (e.g., through new window strategies)

In order to minimize the impact to our operating results and cash flow, a number of major steps are

being undertaken

9

State of the Business

10

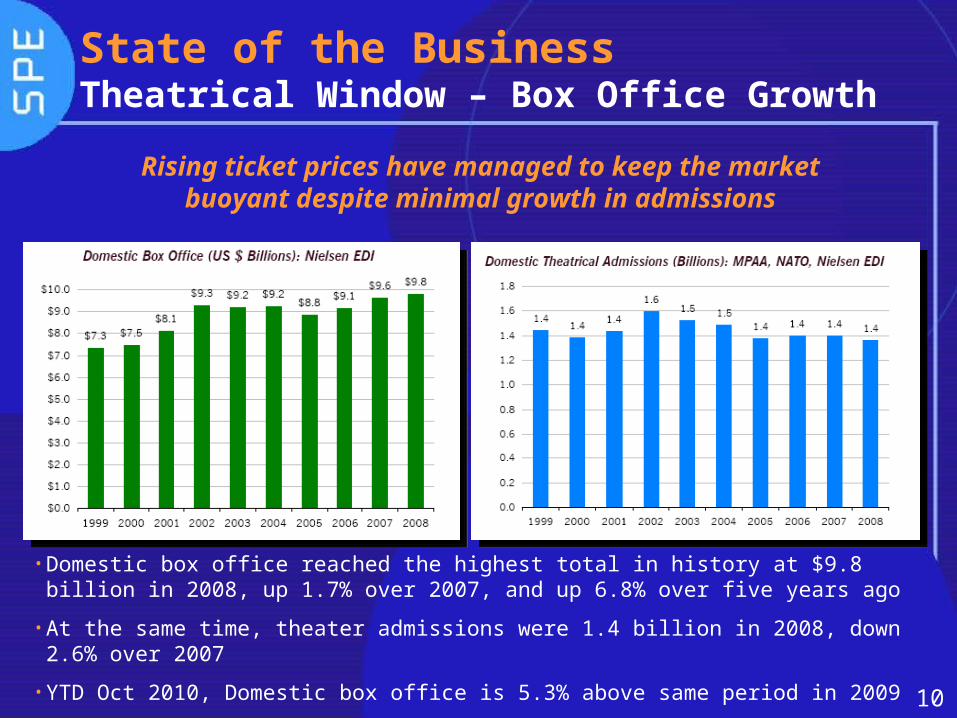

State of the BusinessTheatrical Window – Box Office Growth

Rising ticket prices have managed to keep the market buoyant despite minimal growth in

admissions

•Domestic box office reached the highest total in history at $9.8 billion in 2008, up 1.7% over 2007, and up 6.8% over five years ago

•At the same time, theater admissions were 1.4 billion in 2008, down 2.6% over 2007

•YTD Oct 2010, Domestic box office is 5.3% above same period in 2009

11

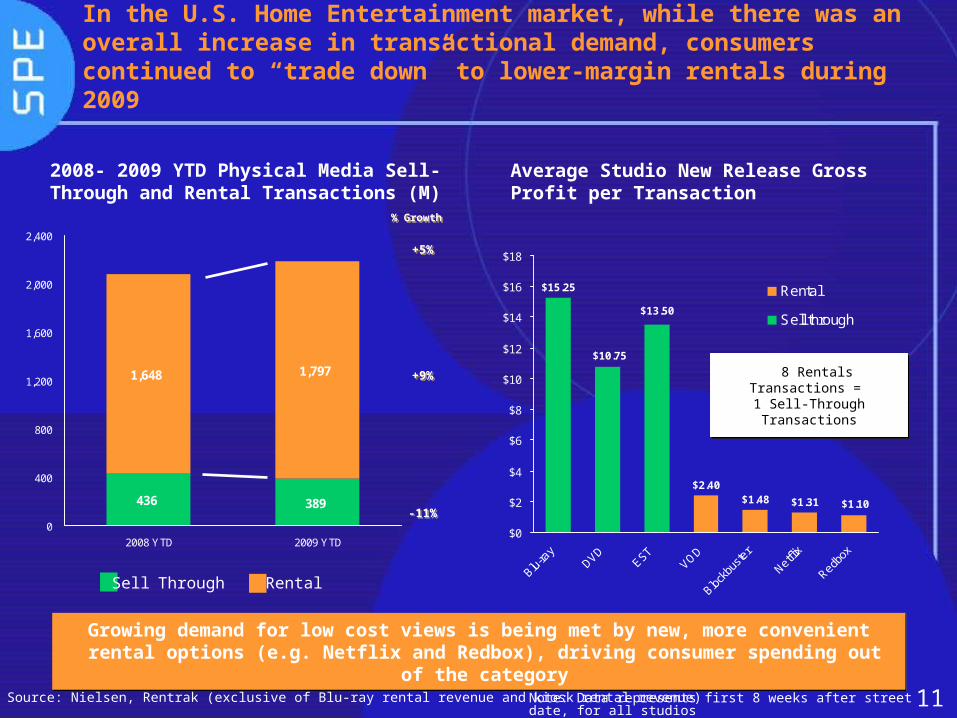

In the U.S. Home Entertainment market, while there was an overall increase in transactional demand, consumers continued to “trade down” to lower-margin rentals during 2009

Source: Nielsen, Rentrak (exclusive of Blu-ray rental revenue and kiosk rental revenue)

% Growth

% Growth

+5%+5%

+9%+9%

-11%-11%

2008- 2009 YTD Physical Media Sell-Through and Rental Transactions (M)

Growing demand for low cost views is being met by new, more convenient rental options (e.g. Netflix and Redbox), driving consumer spending out of

the category

Growing demand for low cost views is being met by new, more convenient rental options (e.g. Netflix and Redbox), driving consumer spending out of

the category

$15.25

$10.75

$13.50

$1.10$1.31$1.48$2.40

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

Blu-ra

yDVD

ESTVOD

Blockb

uste

r

Netflix

Redbox

Rental

Sell through

Average Studio New Release Gross Profit per Transaction

8 Rentals Transactions = 1 Sell-Through Transactions

8 Rentals Transactions = 1 Sell-Through Transactions

Sell Through Rental

Note: Data represents first 8 weeks after street date, for all studios

436 389

1,7971,648

0

400

800

1,200

1,600

2,000

2,400

2008 YTD 2009 YTD

12

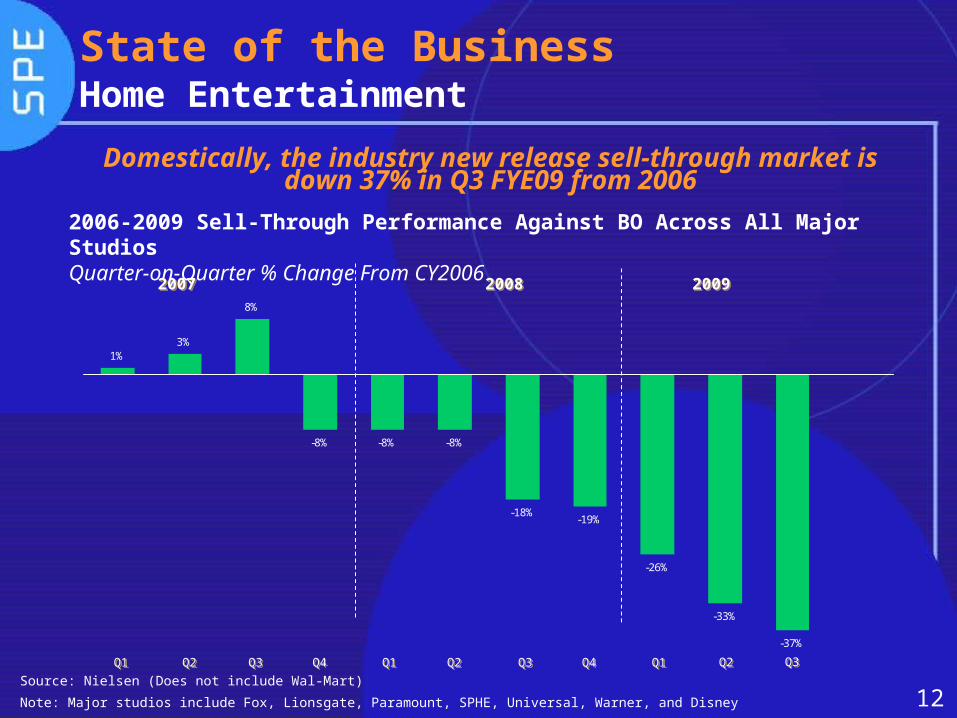

1%3%

8%

-8% -8% -8%

-18%-19%

-26%

-33%

-37%

State of the BusinessHome Entertainment

2006-2009 Sell-Through Performance Against BO Across All Major StudiosQuarter-on-Quarter % Change From CY2006

20072007 20082008 20092009

Source: Nielsen (Does not include Wal-Mart)

Note: Major studios include Fox, Lionsgate, Paramount, SPHE, Universal, Warner, and Disney

Domestically, the industry new release sell-through market is down 37% in Q3 FYE09 from 2006

Q1Q1 Q3Q3 Q4Q4 Q1Q1 Q2Q2 Q3Q3 Q4Q4 Q1Q1Q2Q2 Q2Q2 Q3Q3

13

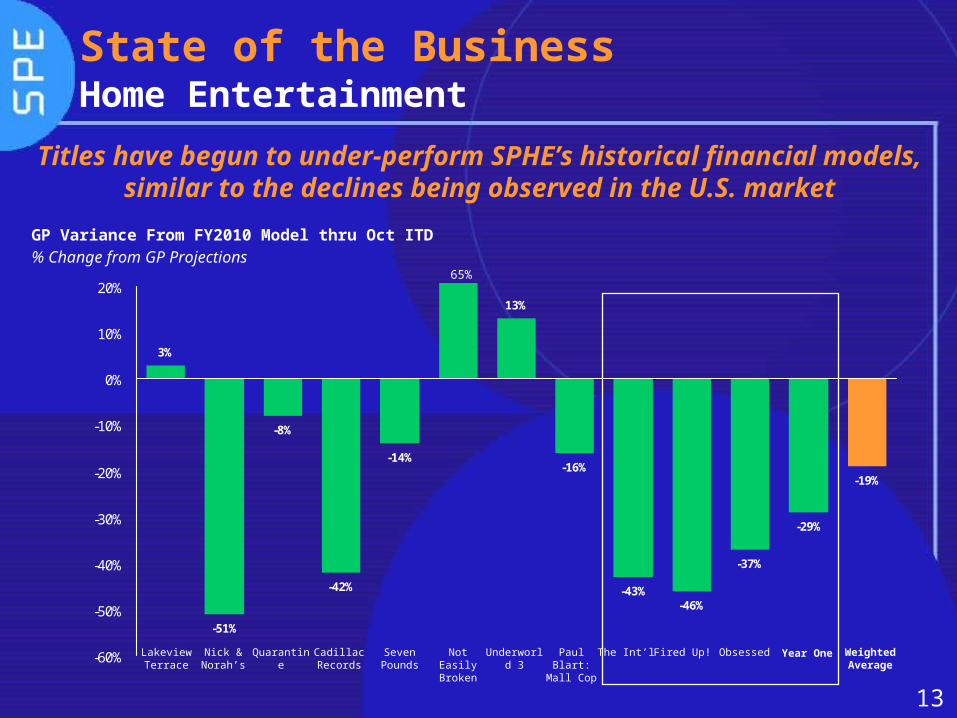

3%

-51%

-8%

-42%

-14%

13%

-16%

-43%-46%

-37%

-29%

-19%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

State of the BusinessHome Entertainment

Titles have begun to under-perform SPHE’s historical financial models, similar to the declines being observed in

the U.S. marketGP Variance From FY2010 Model thru Oct ITD% Change from GP Projections

Lakeview Terrace

Nick & Norah’s

Quarantine Cadillac Records

Seven Pounds

Not Easily Broken

Underworld 3

Paul Blart: Mall Cop

The Int’l Fired Up! Obsessed WeightedAverage

65%

Year One

14

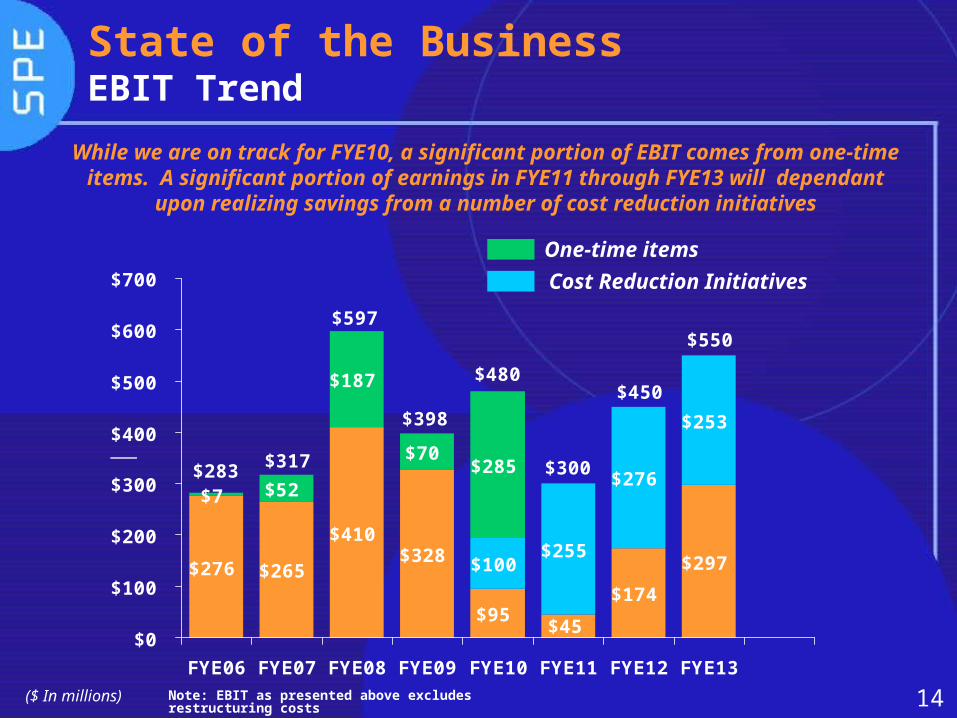

State of the BusinessEBIT Trend

$276 $265

$410$328

$95$174

$297$100$255

$276

$253

$7 $52

$187

$70$285

$45

$550

$450

$300

$480

$398

$597

$317$283

$0

$100

$200

$300

$400

$500

$600

$700

FYE06 FYE07 FYE08 FYE09 FYE10 FYE11 FYE12 FYE13

($ In millions)

One-time items

Cost Reduction Initiatives

While we are on track for FYE10, a significant portion of EBIT comes from one-time items. A significant portion of earnings in FYE11

through FYE13 will dependant upon realizing savings from a number of cost reduction initiatives

Note: EBIT as presented above excludes restructuring costs

15

State of the BusinessActions Already in Process to Improve EBITActions already taken in several areas will benefit

EBIT during the MRP

• Continued expansion of the Networks portfolio is yielding strong benefitso Total EBIT from Networks reaches $257 million in FYE13,

more than double the amount to be realized in FYE10o Our India networks are projected to realize $47.8 million of

earnings by FYE13

• Growing new contento Acquisitions of 2waytraffic and Embassy Row have

provided the foundation of a strong light entertainment business for SPE

o 2waytraffic profit contribution reaches $33 million by FYE13

16

State of the BusinessCost Reduction Initiatives

FYE11 includes $255 million of cost savings resulting from a number of initiatives

• New Company-wide initiative to reduce overhead by $100 milliono Initiative will focus on the reduction of headcount (both

filled and open positions), reduction of temporary employee expenses and other controllable costs

• $115 million reduction of marketing expense

o $100 million of theatrical marketing ($25 million not yet allocated to specific titles)

o $15 million of home entertainment marketing

• $40 million cost savings within Domestic Television

17

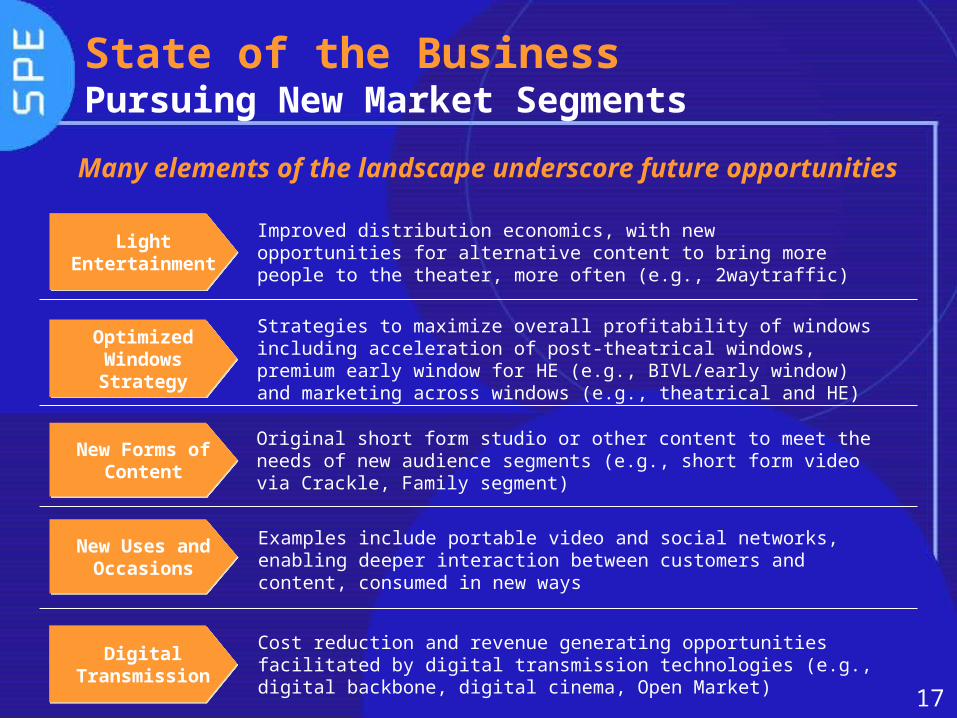

Light Entertainment

Light Entertainment

Improved distribution economics, with new opportunities for alternative content to bring more people to the theater, more often (e.g., 2waytraffic)

Strategies to maximize overall profitability of windows including acceleration of post-theatrical windows, premium early window for HE (e.g., BIVL/early window) and marketing across windows (e.g., theatrical and HE)

Optimized Windows Strategy

Optimized Windows Strategy

Original short form studio or other content to meet the needs of new audience segments (e.g., short form video via Crackle, Family segment)

New Forms of Content

New Forms of Content

Examples include portable video and social networks, enabling deeper interaction between customers and content, consumed in new ways

New Uses and Occasions

New Uses and Occasions

State of the BusinessPursuing New Market Segments

Cost reduction and revenue generating opportunities facilitated by digital transmission technologies (e.g., digital backbone, digital cinema, Open Market)

Digital Transmission

Digital Transmission

Many elements of the landscape underscore future opportunities

18

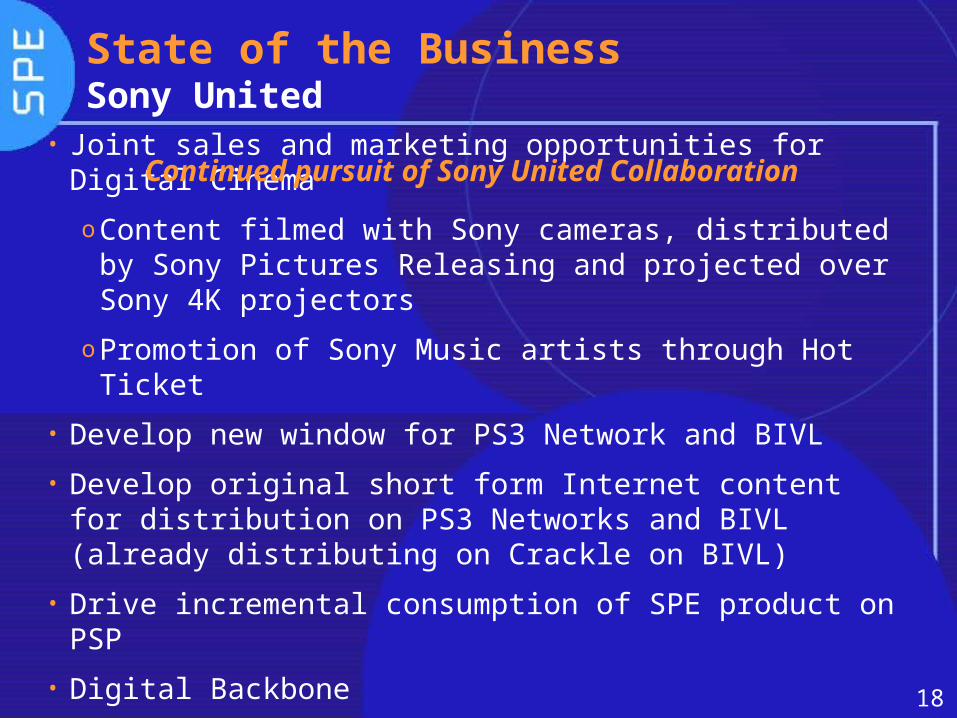

• Joint sales and marketing opportunities for Digital Cinema

oContent filmed with Sony cameras, distributed by Sony Pictures Releasing and projected over Sony 4K projectors

oPromotion of Sony Music artists through Hot Ticket

• Develop new window for PS3 Network and BIVL

• Develop original short form Internet content for distribution on PS3 Networks and BIVL (already distributing on Crackle on BIVL)

• Drive incremental consumption of SPE product on PSP

• Digital Backbone

State of the BusinessSony United

Continued pursuit of Sony United Collaboration

19

Divisional DetailsMotion PicturesMotion Pictures

20

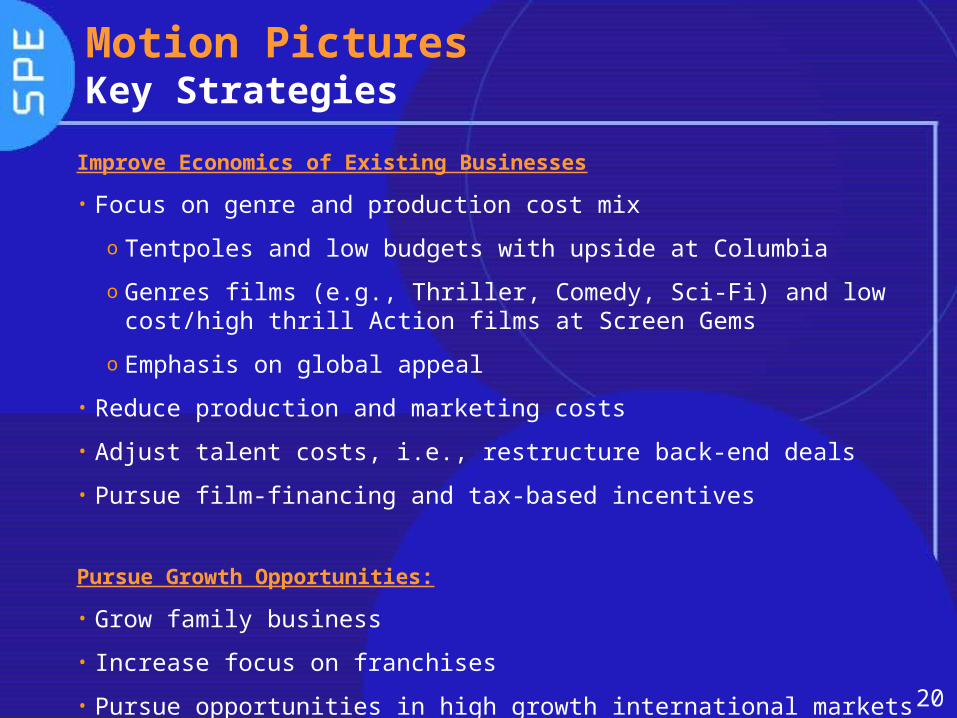

Improve Economics of Existing Businesses

• Focus on genre and production cost mix

o Tentpoles and low budgets with upside at Columbia

o Genres films (e.g., Thriller, Comedy, Sci-Fi) and low cost/high thrill Action films at Screen Gems

o Emphasis on global appeal

• Reduce production and marketing costs

• Adjust talent costs, i.e., restructure back-end deals

• Pursue film-financing and tax-based incentives

Pursue Growth Opportunities:

• Grow family business

• Increase focus on franchises

• Pursue opportunities in high growth international markets

Motion PicturesKey Strategies

21

$35 $36 $37 $39 $41

$50 $51 $54$57

$61

2009 2010 2011 2012 2013

United States International

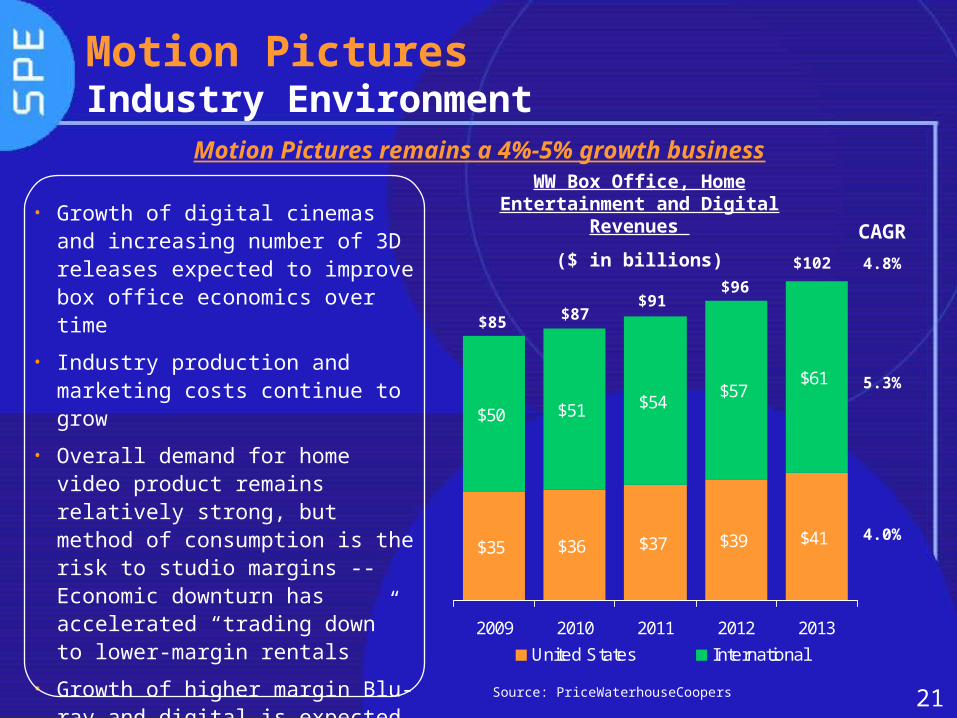

Motion PicturesIndustry Environment

CAGR

5.3%

4.0%

4.8%$102

$96$91

$87$85

WW Box Office, Home Entertainment and Digital

Revenues

($ in billions)

Source: PriceWaterhouseCoopers

• Growth of digital cinemas and increasing number of 3D releases expected to improve box office economics over time

• Industry production and marketing costs continue to grow

• Overall demand for home video product remains relatively strong, but method of consumption is the risk to studio margins -- Economic downturn has accelerated “trading down” to lower-margin rentals

• Growth of higher margin Blu-ray and digital is expected to only partially offset economic erosion from the decline of DVD

Motion Pictures remains a 4%-5% growth business

22

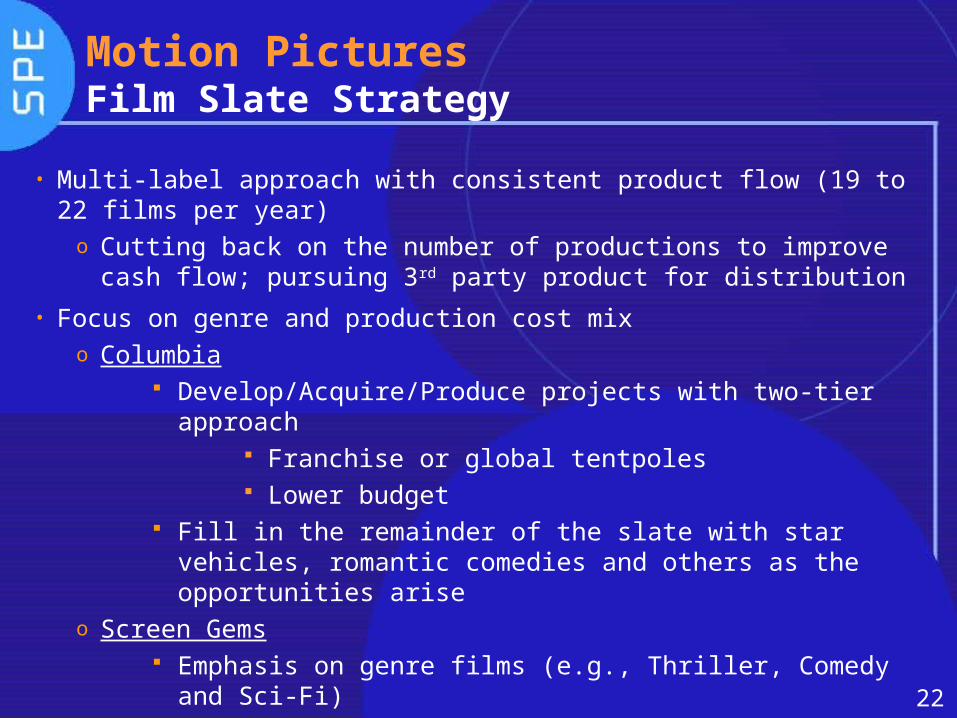

Motion PicturesFilm Slate Strategy

• Multi-label approach with consistent product flow (19 to 22 films per year)

o Cutting back on the number of productions to improve cash flow; pursuing 3rd party product for distribution

• Focus on genre and production cost mixo Columbia

Develop/Acquire/Produce projects with two-tier approach Franchise or global tentpoles Lower budget

Fill in the remainder of the slate with star vehicles, romantic comedies and others as the opportunities arise

o Screen Gems Emphasis on genre films (e.g., Thriller, Comedy and Sci-

Fi) Produce budget sensitive films (e.g., contained action,

lower talent deals) to maximize profitability

23

Motion PicturesFranchise Opportunities

• Numerous titles are in negotiation or active development with an eye toward production in the next few years

Masters of the Universe Spider-Man Men in Black Venom Ghostbusters Total Recall Goosebumps Bad Boys Ultraman Sinbad XXX Zombieland Mall Cop Pineapple Express

• “Talent Franchises/Brands” such as Will Smith and Adam Sandler offer additional opportunities

24

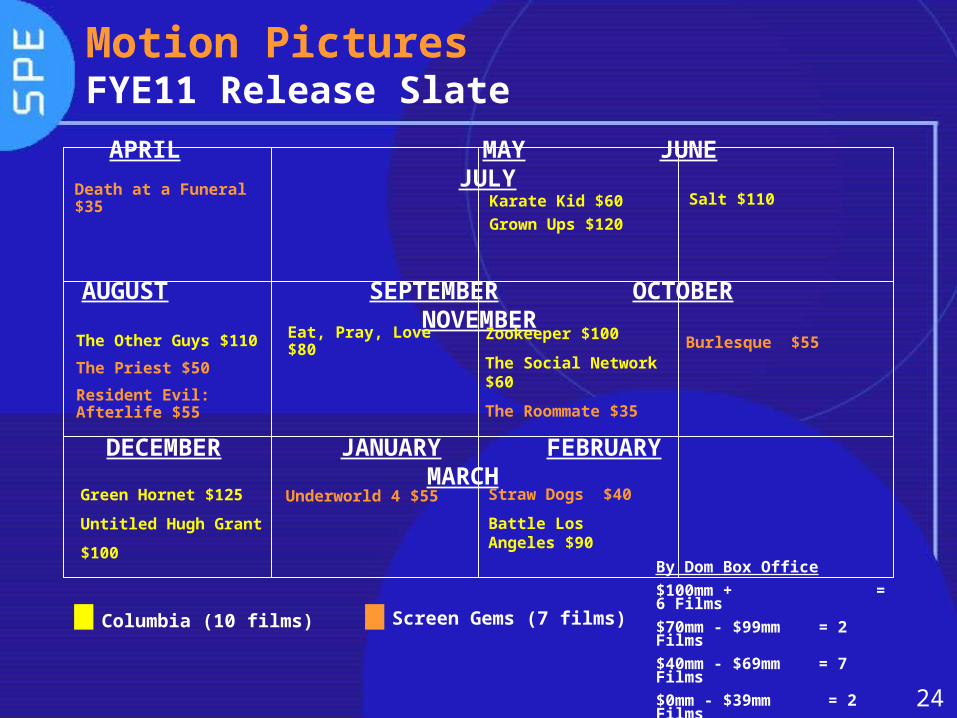

APRIL MAY JUNE JULY

DECEMBER JANUARY FEBRUARY MARCH

AUGUST SEPTEMBER OCTOBER NOVEMBER

Zookeeper $100

The Social Network $60

The Roommate $35

Karate Kid $60

Grown Ups $120

Salt $110

The Other Guys $110

The Priest $50

Resident Evil: Afterlife $55

Green Hornet $125

Untitled Hugh Grant

$100By Dom Box Office

$100mm + = 6 Films

$70mm - $99mm = 2 Films

$40mm - $69mm = 7 Films

$0mm - $39mm = 2 Films

Motion PicturesFYE11 Release Slate

Straw Dogs $40

Battle Los Angeles $90

Death at a Funeral $35

Screen Gems (7 films)

Underworld 4 $55

Burlesque $55Eat, Pray, Love $80

Columbia (10 films)

25

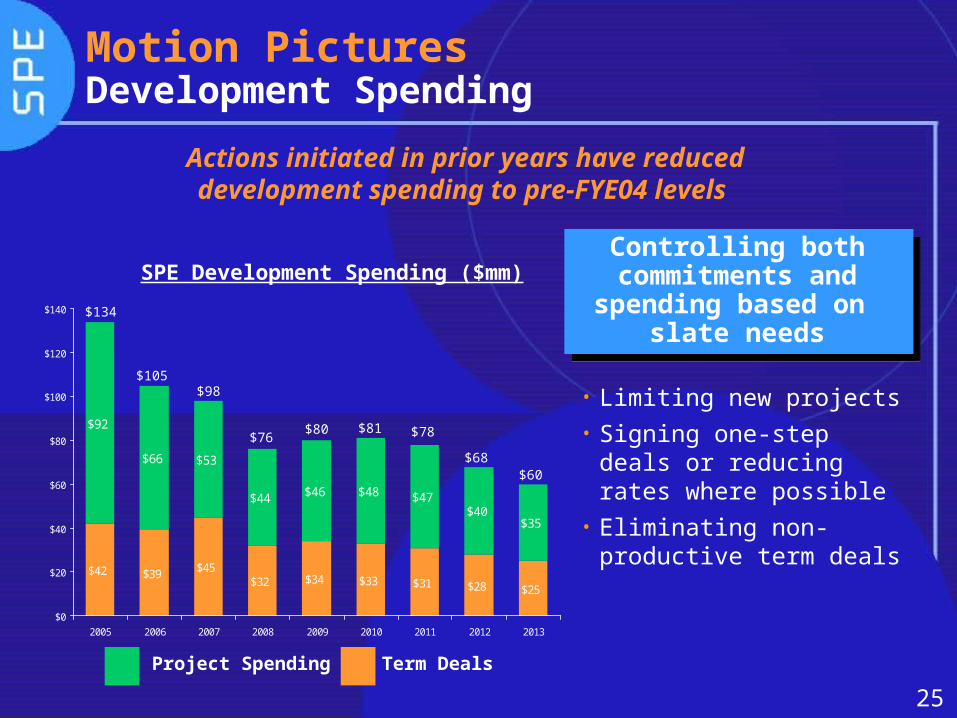

$42 $39 $45$32 $34 $33 $31 $28 $25

$92

$66 $53

$44 $46 $48 $47$40

$35

$0

$20

$40

$60

$80

$100

$120

$140

2005 2006 2007 2008 2009 2010 2011 2012 2013

Motion PicturesDevelopment Spending

Project Spending Term Deals

• Limiting new projects• Signing one-step deals or

reducing rates where possible

• Eliminating non-productive term deals

Controlling both commitments and

spending based on slate needs

SPE Development Spending ($mm)

$98

$134

$76

$105

$80 $81 $78

Actions initiated in prior years have reduceddevelopment spending to pre-FYE04 levels

$68$60

26

Motion PicturesReduce Production Costs

• Negotiating post break back-end deals and reduced upfront fees for talent

o All 6 films committed in FYE10 have been post cash break deals

o Have successfully reduced upfront compensation and renegotiated backend deals prior to starting principal photography (e.g., Spider-Man 4, How Do You Know, Green Hornet)

• Monitoring global incentives to capitalize on the opportunities to lower production cost

• Exploitation of tax-based incentives on a worldwide basis will save approximately $87mm on FYE11 releases

o All but 3 films on FYE11 calendar will receive a tax incentive of some sort

• Work closely with Physical Production to generate cost efficiencies and minimize cost overruns

27

MEDIA• Continuing to capitalize on global economic downturn and market softness to achieve greater media cost savings

•Upfront negotiations varied by outlets, yielding a 4% average rate reduction

•Adjusted Sony Media Mix to maximize exposure to our target audiences using less advertising dollars

• Maintained integrity of added value promotions with significantly reduced dollar volume

Motion PicturesMarketing and Distribution Spend

Strategy for Achieving Cost Savings

28

BASICS•Eliminate teaser campaigns where possible

•Negotiate flat fee deals with creative vendors

•Consolidate vendors globally to reduce production / distribution costs

•Expand digital distribution of TV spots, eliminating production and shipping of thousands of tapes

•Eliminate large premieres; have smaller parties when we do have these events, and limit travel expenses

•Eliminate junkets where possible and collaborate with other studios for shared junkets to reduce costs

Motion PicturesMarketing and Distribution Spend

Strategy for Achieving Cost Savings

29

• Target 5 to 6 lower budget titles per year

• 2 action/thrillers, 2 thriller/horrors, 2 comedies or other

• Producing films which are budget sensitive (e.g., contained action, lower talent deals) to maximize profitability

• Target audiences from the outset (e.g., young, urban, wide-appeal with an name cast or international appeal)

• Continue to opportunistically co-produce films with strategic partners (e.g., Constantin, Lakeshore, Vertigo and others)

• Continue to produce existing franchises (e.g., Underworld and Resident Evil) along with creating new franchises (e.g., Legion, Priest, and Skank Robbers)

• Explore full slate co-financing opportunities

Motion PicturesScreen Gems

Improve margins on new releases through a continued emphasis

on genre films coupled with a new focus on action films

30

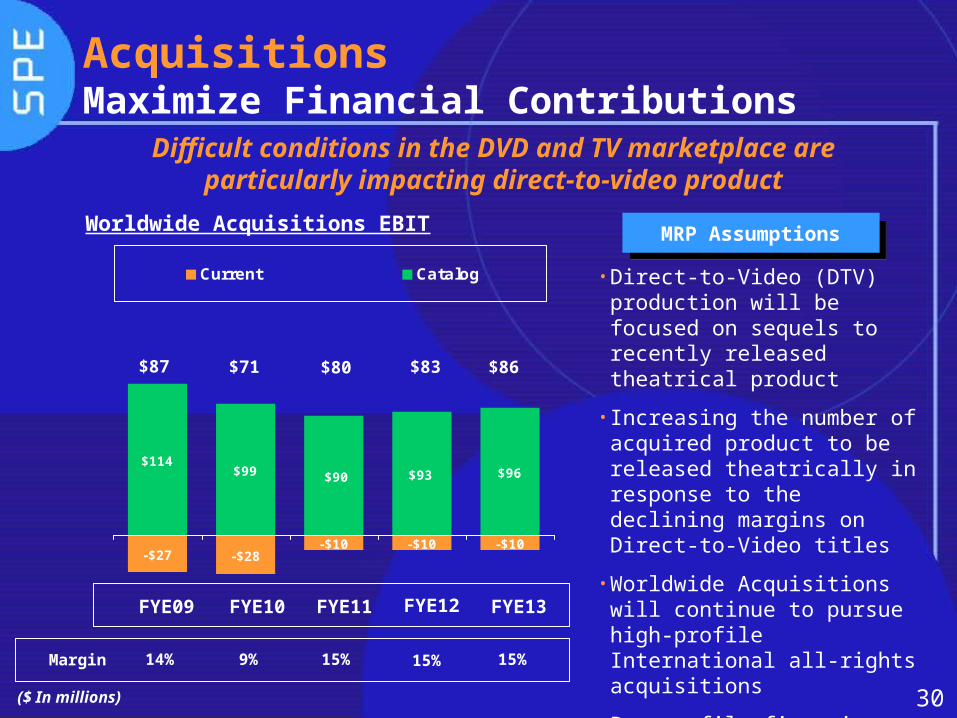

MRP Assumptions

AcquisitionsMaximize Financial Contributions

•Direct-to-Video (DTV) production will be focused on sequels to recently released theatrical product

• Increasing the number of acquired product to be released theatrically in response to the declining margins on Direct-to-Video titles

•Worldwide Acquisitions will continue to pursue high-profile International all-rights acquisitions

•Pursue film financing opportunities

Difficult conditions in the DVD and TV marketplace are particularly impacting direct-to-video product

-$27 -$28-$10 -$10 -$10

$114$99 $96$93$90

Current Catalog

Worldwide Acquisitions EBIT

$86$80$71$87 $83

FYE09 FYE10 FYE11 FYE13FYE12

($ In millions)

Margin 14% 9% 15% 15%15%

31

Motion Pictures Digital Cinema

Rollout Update• 14,000 digital screens estimated to be installed worldwide by

the end of 2010 with 21,000 projected by 2011

• Tighter access to capital has made it difficult for deployment entities to gain financing for the installation of the digital screens; accordingly, exhibitors worldwide have begun to explore self-financing for the deployment of digital equipment

• The push for 3D content continues to drive the rollout of digital installations

• Digital 3D is now the standard of at least 14 3D feature releases from Hollywood slated for next year (SPE will be releasing Resident Evil 4 in August 2010)

32

Divisional DetailsHome EntertainmentHome Entertainment

33

Improve Economics of Existing Business• Blu-ray: Drive mass market adoption to encourage consumers

to “trade up” to HD• Organization: Rationalize global organizational structure

Pursue Growth Opportunities• Retail Expansion: Maximize channel placement to create

impulse occasions • Product Innovation: Lead industry in new video formats and

releasing strategies

Pursue Sony United Collaboration• Commercial: Continue collaboration with SEL & SCE on

sales/marketing initiatives• Back Office: Consolidate operations across Sony divisions,

e.g., SPHE, SME, DADC

Home EntertainmentKey Strategies

34

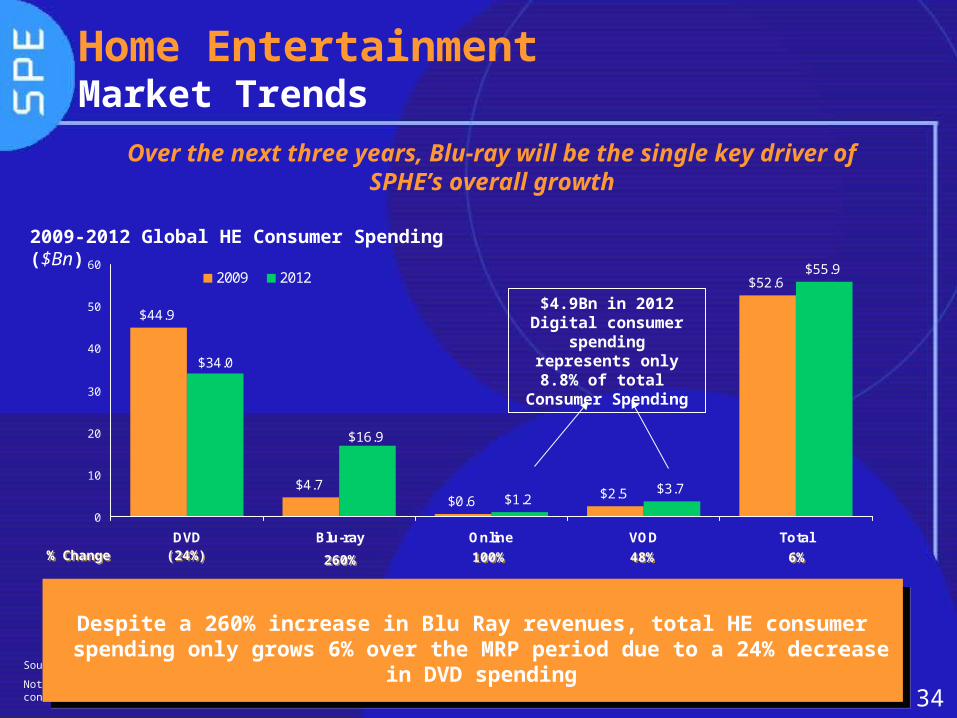

Over the next three years, Blu-ray will be the single key driver of SPHE’s overall growth

$44.9

$4.7$0.6

$2.5

$52.6

$1.2$3.7

$55.9

$16.9

$34.0

0

10

20

30

40

50

60

DVD Blu-ray Online VOD Total

2009 2012

2009-2012 Global HE Consumer Spending ($Bn)

% Change% Change (24%)(24%) 260%260% 100%100% 48%48% 6%6%

Source: Screen Digest,( July 2009)

Notes: VOD/PPV - total on-demand movie consumer revenues / On-line - transactional movie retail and rental download consumer revenues

Despite a 260% increase in Blu Ray revenues, total HE consumer spending only grows 6% over the MRP period due to a 24% decrease

in DVD spending

Despite a 260% increase in Blu Ray revenues, total HE consumer spending only grows 6% over the MRP period due to a 24% decrease

in DVD spending

Home EntertainmentMarket Trends

$4.9Bn in 2012 Digital consumer

spending represents only 8.8% of total

Consumer Spending

35

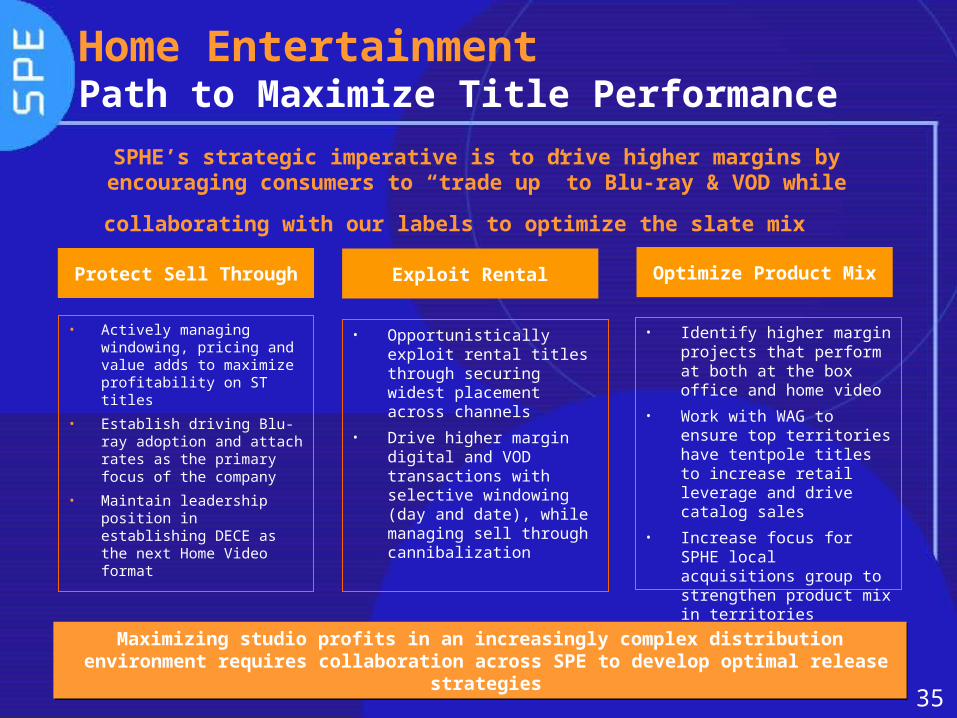

Protect Sell Through Exploit Rental Optimize Product Mix

SPHE’s strategic imperative is to drive higher margins by encouraging consumers to “trade up” to Blu-ray & VOD while

collaborating with our labels to optimize the slate mix

• Opportunistically exploit rental titles through securing widest placement across channels

• Drive higher margin digital and VOD transactions with selective windowing (day and date), while managing sell through cannibalization

• Actively managing windowing, pricing and value adds to maximize profitability on ST titles

• Establish driving Blu-ray adoption and attach rates as the primary focus of the company

• Maintain leadership position in establishing DECE as the next Home Video format

• Identify higher margin projects that perform at both at the box office and home video

• Work with WAG to ensure top territories have tentpole titles to increase retail leverage and drive catalog sales

• Increase focus for SPHE local acquisitions group to strengthen product mix in territories

Maximizing studio profits in an increasingly complex distribution environment requires collaboration across SPE to develop optimal release strategies

Maximizing studio profits in an increasingly complex distribution environment requires collaboration across SPE to develop optimal release strategies

Home EntertainmentPath to Maximize Title Performance

36

Home EntertainmentSummary of Home Entertainment Contribution

Actions

$830 $826$1,041

$1,141

$206 $248

$261 $173

$215$219

$53$46

$41

$245$255

$40

FYE10 FYE11 FYE12 FYE13

New & Recent Flow / Library Acq TV

$1,655$1,542

Worldwide HE Contribution

($ In millions)

$1,293$1,350

Aggressive steps must be taken to grow contributions in the current market

• HE is projecting to grow Flow/Library during the MRP period at a 7.4% CAGR despite retail space constraints and pricing pressures

o Flow/Library year-over-year growth is projected at 20% in FYE10/FYE11 driven by digital and blu-ray

o Digital Flow/Library is expected to grow by 64%, 29% and 17% in FYE11, FYE12 and FYE13, respectively; Blu-ray Flow/Library is expected to grow by 63%, 9% and 15% in FYE11, FYE12, and FYE13, respectively

• The $215m increase in New & Recent in FYE12 is driven by Spider-Man 4

37

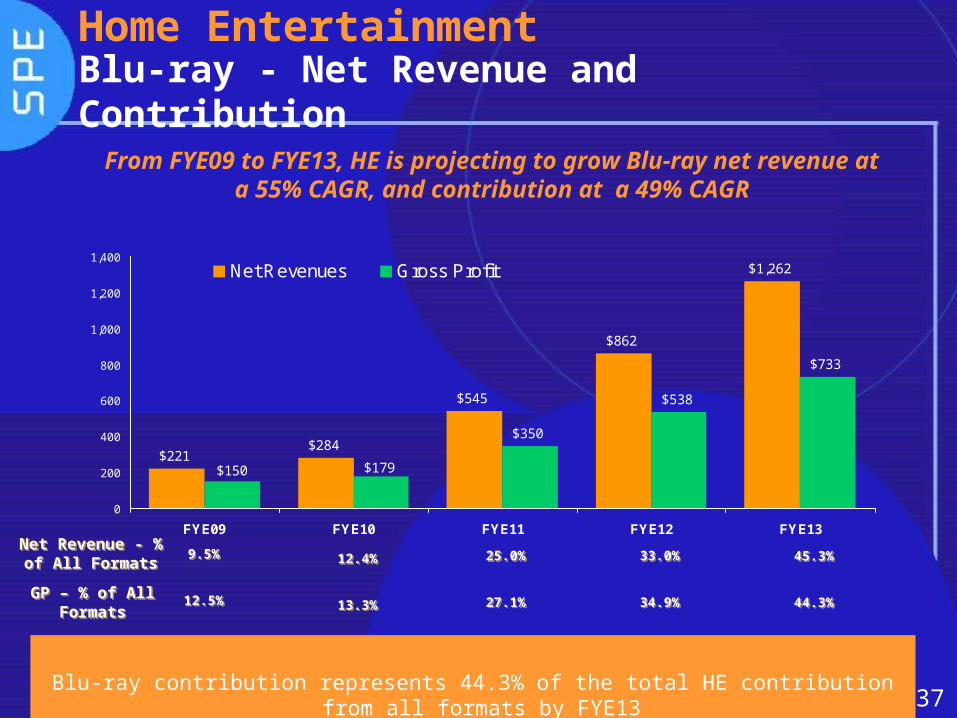

From FYE09 to FYE13, HE is projecting to grow Blu-ray net revenue at a 55% CAGR, and contribution at a 49%

CAGR

$221$284

$545

$862

$1,262

$350

$538

$733

$179$150

0

200

400

600

800

1,000

1,200

1,400

FYE09 FYE10 FYE11 FYE12 FYE13

Net Revenues Gross Profit

GP – % of All Formats

GP – % of All Formats

12.5%12.5% 13.3%13.3% 27.1%27.1% 34.9%34.9% 44.3%44.3%

Blu-ray contribution represents 44.3% of the total HE contribution from all formats by FYE13

Home EntertainmentBlu-ray - Net Revenue and Contribution

Net Revenue - % of All Formats

Net Revenue - % of All Formats 9.5%9.5% 12.4%12.4% 25.0%25.0% 33.0%33.0% 45.3%45.3%

38

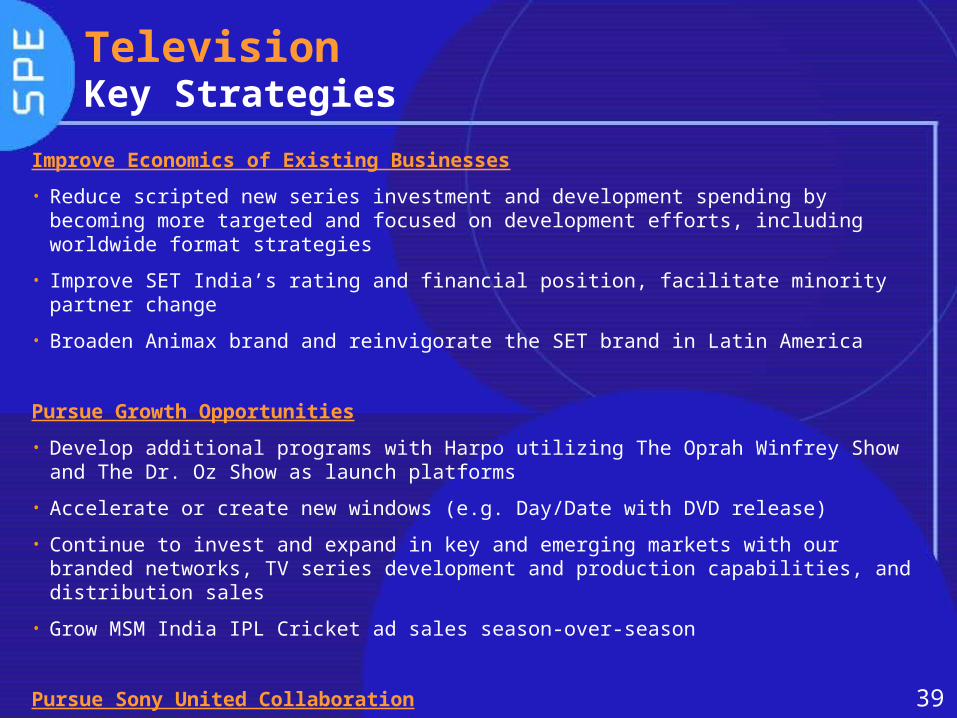

Divisional DetailsTelevisionTelevision

39

Improve Economics of Existing Businesses

• Reduce scripted new series investment and development spending by becoming more targeted and focused on development efforts, including worldwide format strategies

• Improve SET India’s rating and financial position, facilitate minority partner change

• Broaden Animax brand and reinvigorate the SET brand in Latin America

Pursue Growth Opportunities

• Develop additional programs with Harpo utilizing The Oprah Winfrey Show and The Dr. Oz Show as launch platforms

• Accelerate or create new windows (e.g. Day/Date with DVD release)

• Continue to invest and expand in key and emerging markets with our branded networks, TV series development and production capabilities, and distribution sales

• Grow MSM India IPL Cricket ad sales season-over-season

Pursue Sony United Collaboration

• Become the primary ad sales organization across Sony brand and platforms

• Utilize development, production and programming expertise to create content for PS3

TelevisionKey Strategies

40

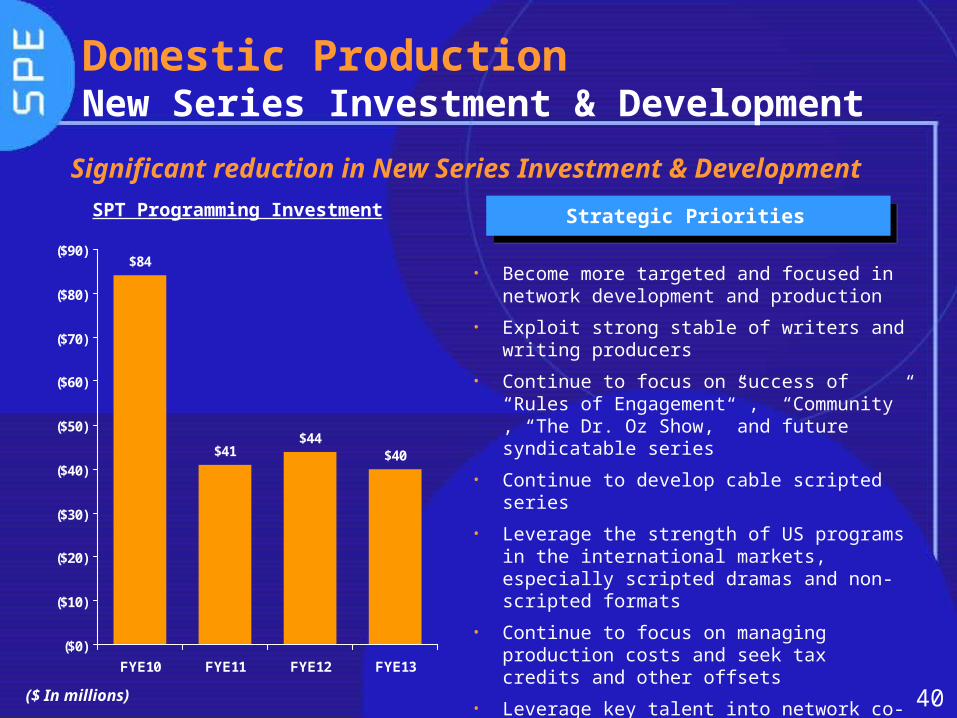

Domestic ProductionNew Series Investment & Development

• Become more targeted and focused in network development and production

• Exploit strong stable of writers and writing producers

• Continue to focus on success of “Rules of Engagement” , “Community” , “The Dr. Oz Show,” and future syndicatable series

• Continue to develop cable scripted series

• Leverage the strength of US programs in the international markets, especially scripted dramas and non-scripted formats

• Continue to focus on managing production costs and seek tax credits and other offsets

• Leverage key talent into network co-productions from the development stage

• Launch future shows with Harpo

SPT Programming Investment

($ In millions)

Strategic Priorities

$84

$41$44

$40

($0)

($10)

($20)

($30)

($40)

($50)

($60)

($70)

($80)

($90)

FYE10 FYE11 FYE12 FYE13

Significant reduction in New Series Investment & Development

41

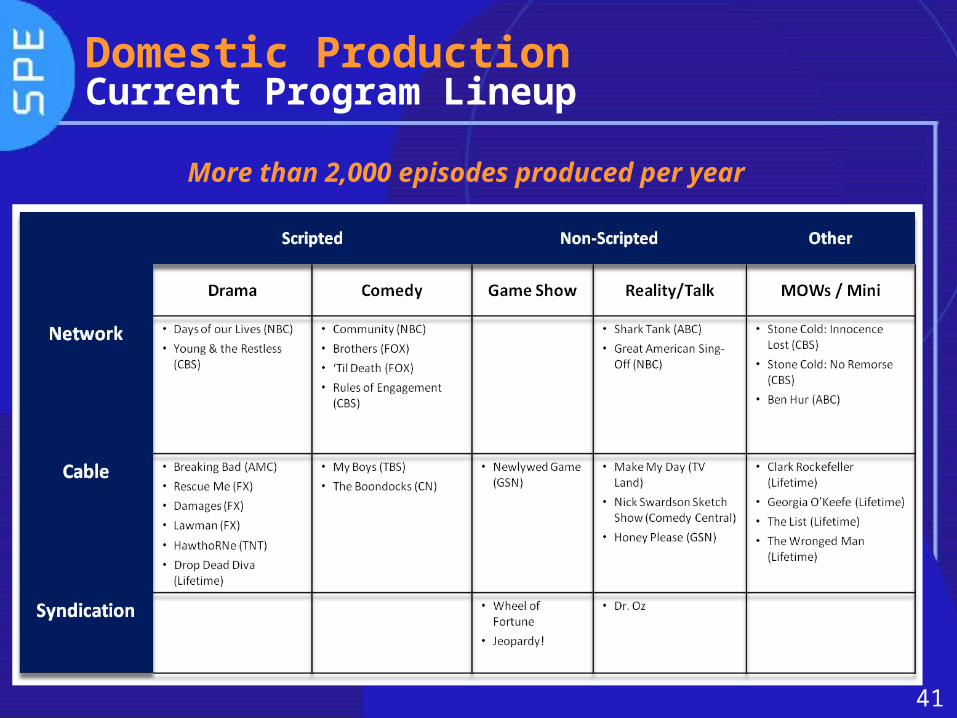

Domestic ProductionCurrent Program Lineup

More than 2,000 episodes produced per year

42

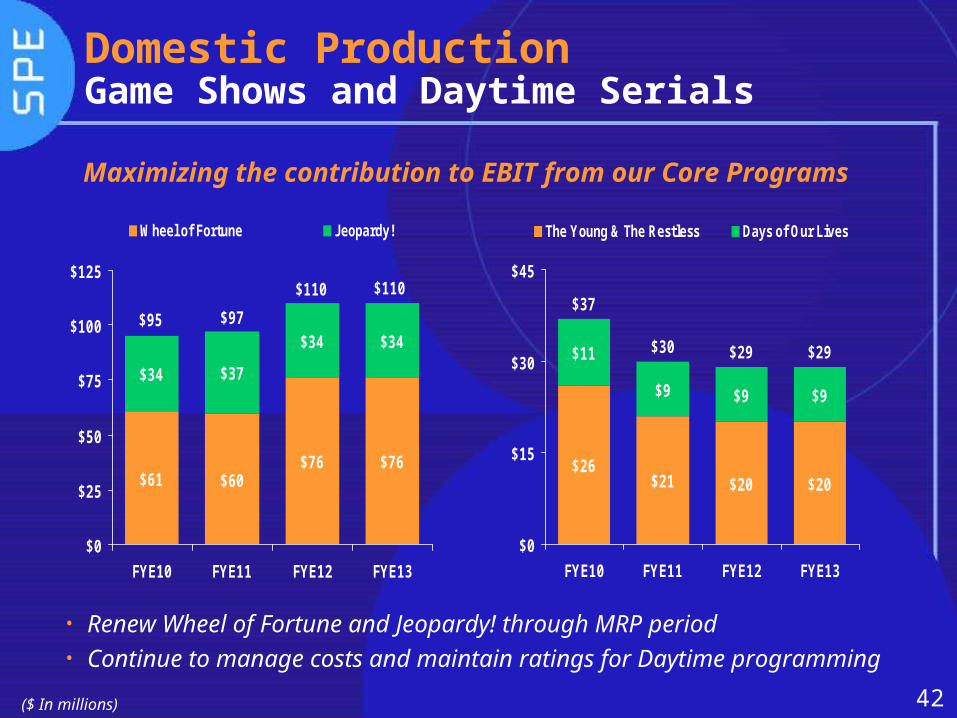

• Renew Wheel of Fortune and Jeopardy! through MRP period• Continue to manage costs and maintain ratings for Daytime

programming

Domestic ProductionGame Shows and Daytime Serials

($ In millions)

$26$21 $20 $20

$11

$9 $9 $9

$37

$30 $29 $29

$0

$15

$30

$45

FYE10 FYE11 FYE12 FYE13

The Young & The Restless Days of Our Lives

$61 $60$76 $76

$37

$34 $34

$34

$110 $110

$97 $95

$0

$25

$50

$75

$100

$125

FYE10 FYE11 FYE12 FYE13

Wheel of Fortune Jeopardy!

Maximizing the contribution to EBIT from our Core Programs

43

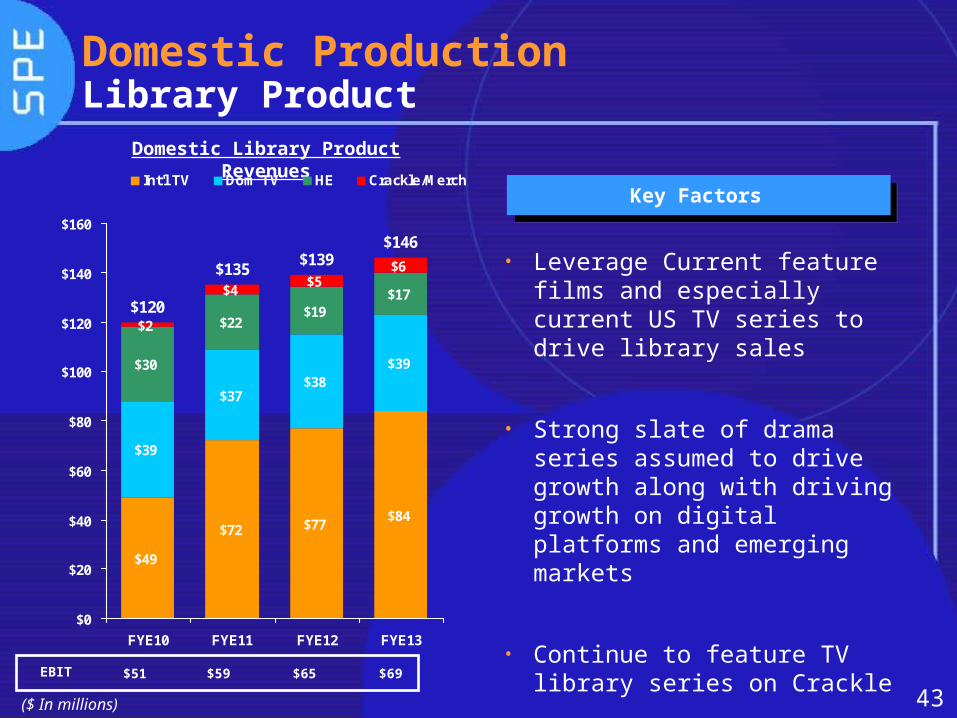

Domestic ProductionLibrary Product

• Leverage Current feature films and especially current US TV series to drive library sales

• Strong slate of drama series assumed to drive growth along with driving growth on digital platforms and emerging markets

• Continue to feature TV library series on Crackle

Domestic Library Product Revenues

($ In millions)

Key Factors

$51 $59 $65 $69EBIT

$49

$72 $77$84

$39

$37$38

$39$30

$22$19

$17

$2

$4$5

$6

$120

$135$139

$146

$0

$20

$40

$60

$80

$100

$120

$140

$160

FYE10 FYE11 FYE12 FYE13

Int'l TV Dom TV HE Crackle/Merch

44

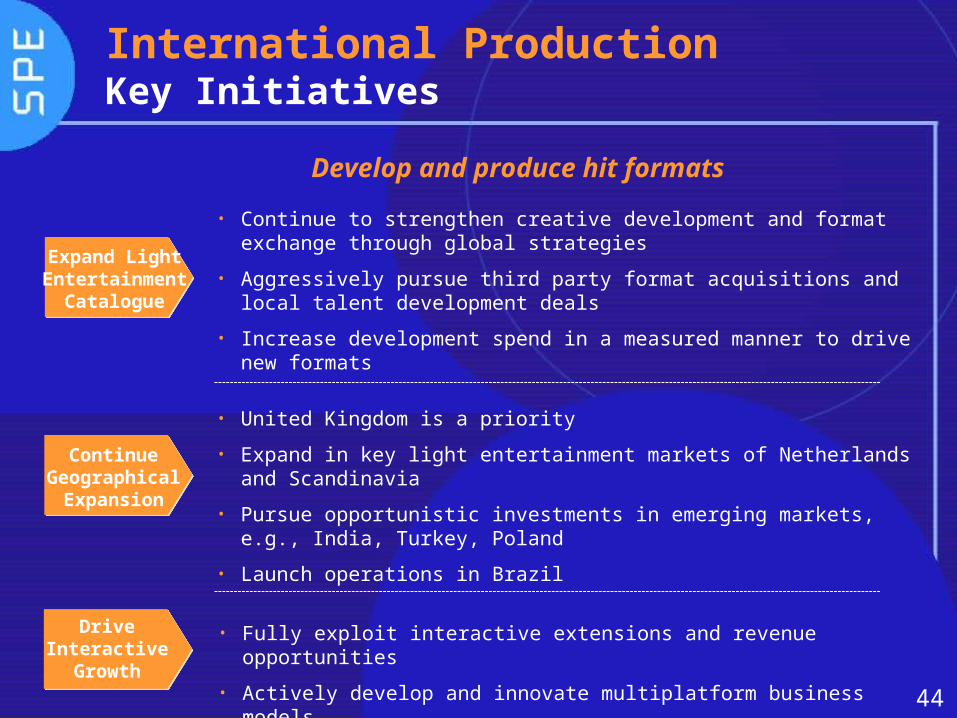

Expand Light Entertainment

Catalogue

International ProductionKey Initiatives

Continue Geographical

Expansion

Drive Interactive

Growth

• Continue to strengthen creative development and format exchange through global strategies

• Aggressively pursue third party format acquisitions and local talent development deals

• Increase development spend in a measured manner to drive new formats

• United Kingdom is a priority

• Expand in key light entertainment markets of Netherlands and Scandinavia

• Pursue opportunistic investments in emerging markets, e.g., India, Turkey, Poland

• Launch operations in Brazil

• Fully exploit interactive extensions and revenue opportunities

• Actively develop and innovate multiplatform business models

Develop and produce hit formats

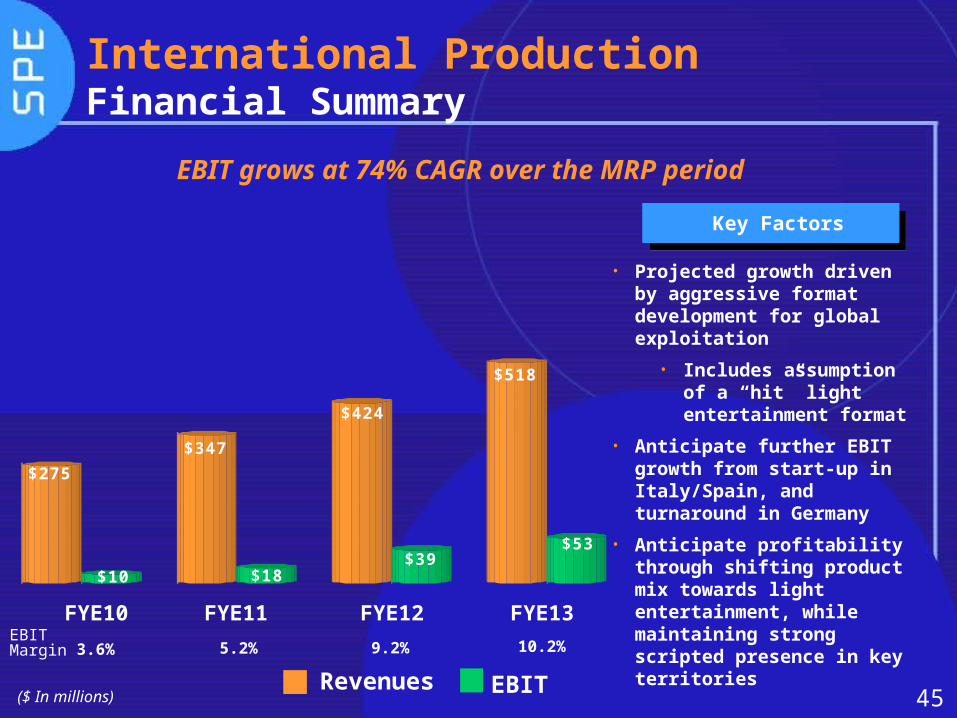

45EBITRevenues

FYE11 FYE12 FYE13FYE10

($ In millions)

International ProductionFinancial Summary

• Projected growth driven by aggressive format development for global exploitation

• Includes assumption of a “hit” light entertainment format

• Anticipate further EBIT growth from start-up in Italy/Spain, and turnaround in Germany

• Anticipate profitability through shifting product mix towards light entertainment, while maintaining strong scripted presence in key territories

Key Factors

$275

$10

$347

$18

$424

$39

$518

$53

EBIT grows at 74% CAGR over the MRP period

3.6% 5.2% 9.2% 10.2%EBIT Margin

46($ In millions)

International Production2waytraffic - Financial Summary

Revenues grow at 40% CAGR over the MRP

$24$36

$46

$196

$162

$111

$72

$18$33

$22$7$1

FYE10 FYE11 FYE12 FYE13

Revenues

Profit Contribution

EBITDA

• Although financial performance is less than expected, the structure of the purchase of 2waytraffic has allowed expected investment returns to remain very near originally expected

• The acquisitions of 2waytraffic and Embassy Row have provided the foundation of a strong light entertainment business for SPE

• 2waytraffic owns one of the most successful game show formats, “Who Wants to Be a Millionaire” on which the President of Embassy Row serves as Executive Producer

• Embassy Row and 2waytraffic are co-developing SPE’s library formats as well as formats acquired or created by the other (e.g. Make My Day, Newlywed Game, Sing Off, Shark Tank)

47

Domestic Distribution / Ad SalesMarket Environment

Distribution -

• Market conditions create an opportunity to expand our first-run business

o Although local stations are facing economic challenges, they still have an appetite for quality programming

o Competitive product in the marketplace has declined

• Cable networks increasingly shifting programming dollars to original content, creating downward pressure on prices for acquired film and TV product

• Cable and Satellite are requiring day-and-date commitments to secure premium shelf space and marketing

Ad Sales -

• Recessionary economy is contributing to a weaker advertising market

• 09/10 season upfront sales experienced price declines and lower volume, future seasons expected to slowly rebound

• Digital ad market continues to grow; however, rate of growth slows through future years

48

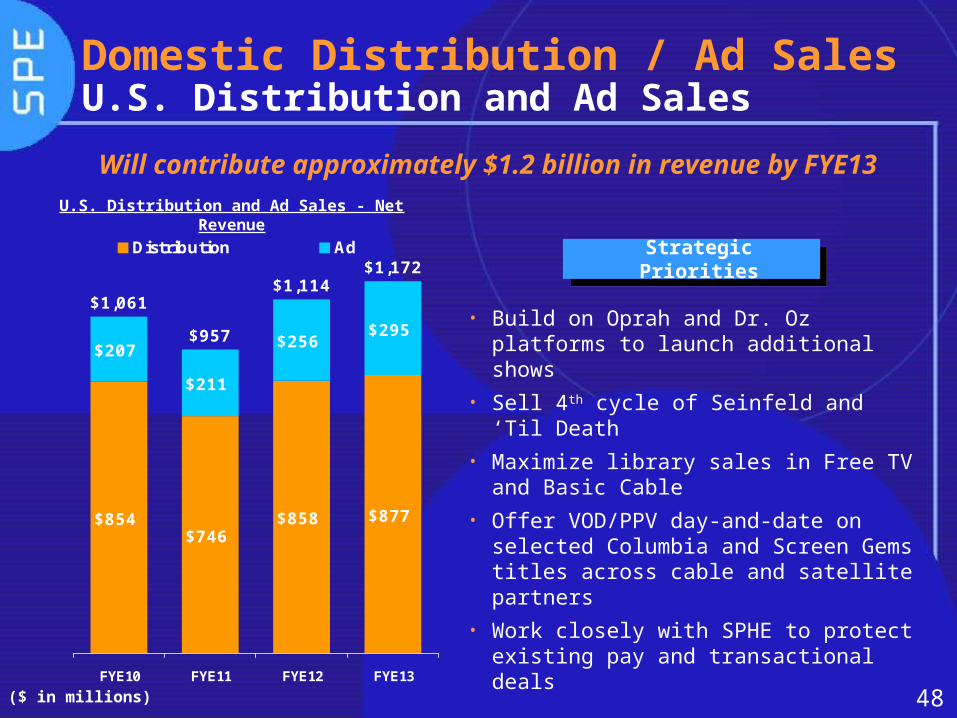

• Build on Oprah and Dr. Oz platforms to launch additional shows

• Sell 4th cycle of Seinfeld and ‘Til Death• Maximize library sales in Free TV and

Basic Cable• Offer VOD/PPV day-and-date on

selected Columbia and Screen Gems titles across cable and satellite partners

• Work closely with SPHE to protect existing pay and transactional deals

($ in millions)

Domestic Distribution / Ad SalesU.S. Distribution and Ad Sales

Will contribute approximately $1.2 billion in revenue by FYE13

U.S. Distribution and Ad Sales - Net Revenue

$854$746

$858 $877

$207

$211

$256$295

$1,061

$957

$1,114$1,172

FYE10 FYE11 FYE12 FYE13

Distribution AdStrategic Priorities

49

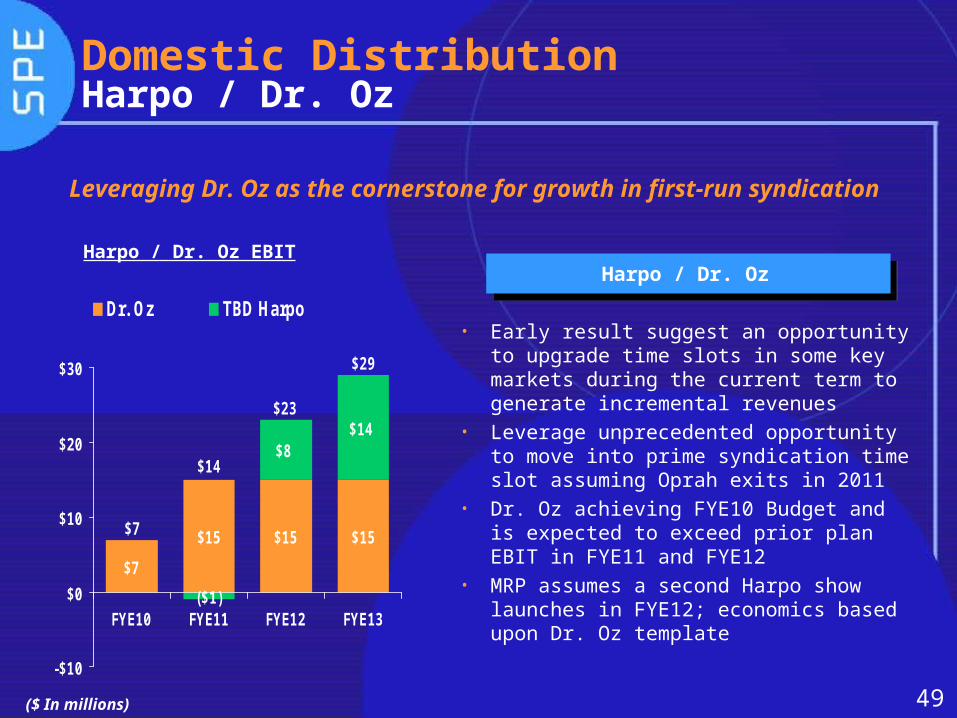

Leveraging Dr. Oz as the cornerstone for growth in first-run syndication

Domestic DistributionHarpo / Dr. Oz

• Early result suggest an opportunity to upgrade time slots in some key markets during the current term to generate incremental revenues

• Leverage unprecedented opportunity to move into prime syndication time slot assuming Oprah exits in 2011

• Dr. Oz achieving FYE10 Budget and is expected to exceed prior plan EBIT in FYE11 and FYE12

• MRP assumes a second Harpo show launches in FYE12; economics based upon Dr. Oz template

Harpo / Dr. Oz

($ In millions)

Harpo / Dr. Oz EBIT

$15 $15

($1)

$8$14

$15

$7

$29

$23

$14

$7

-$10

$0

$10

$20

$30

FYE10 FYE11 FYE12 FYE13

Dr. Oz TBD Harpo

50

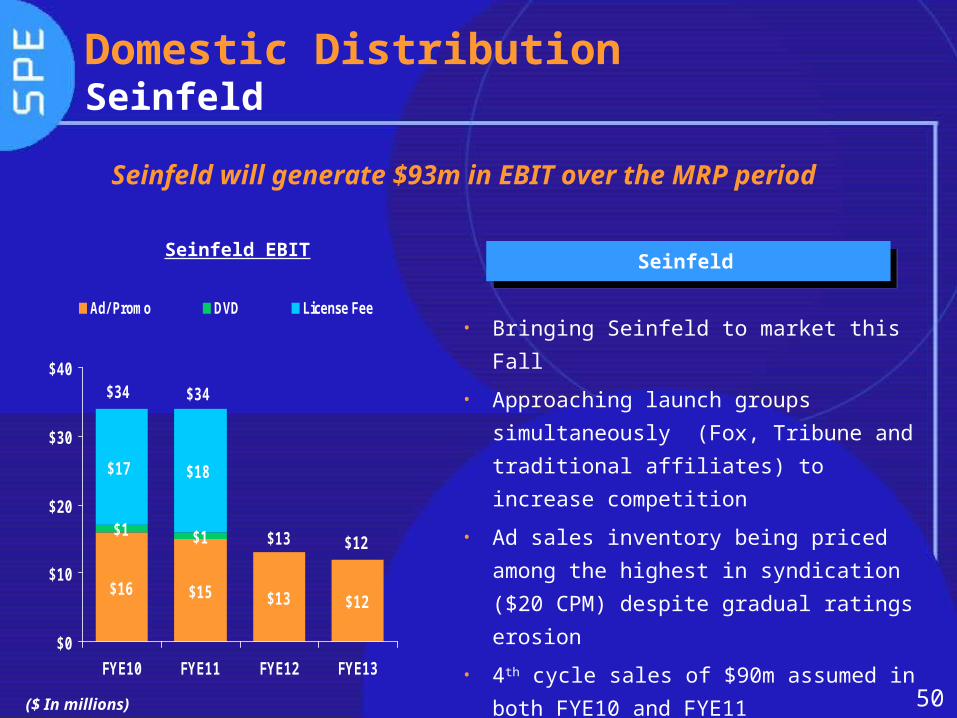

Seinfeld will generate $93m in EBIT over the MRP period

Domestic DistributionSeinfeld

• Bringing Seinfeld to market this Fall

• Approaching launch groups

simultaneously (Fox, Tribune and

traditional affiliates) to increase

competition

• Ad sales inventory being priced among

the highest in syndication ($20 CPM)

despite gradual ratings erosion

• 4th cycle sales of $90m assumed in both

FYE10 and FYE11

Seinfeld

($ In millions)

Seinfeld EBIT

$16 $15 $13 $12

$1 $1

$18$17

$12$13

$34$34

$0

$10

$20

$30

$40

FYE10 FYE11 FYE12 FYE13

Ad/ Promo DVD License Fee

51

International DistributionMarket Environment

• More cautious and targeted investments by broadcasters due to global recessionary environment

• One-hour dramas have become key differentiator for studios to secure top dollar feature film and TV output deals

• Local language products are growth drivers (e.g., telenovelas for Latin America, TV dramas, local sitcoms and soaps for Russia/CIS and Asian features)

• Proliferation of channels across an increasingly fragmented customer base diminishes ability to drive large deals

• Low single digit growth (2-3%) is expected in key markets in the next year(1), with some economic recovery increasing growth modestly starting in FYE12

(1) Source: Price Waterhouse Coopers 2009-2013 Global Entertainment and Media report.

52

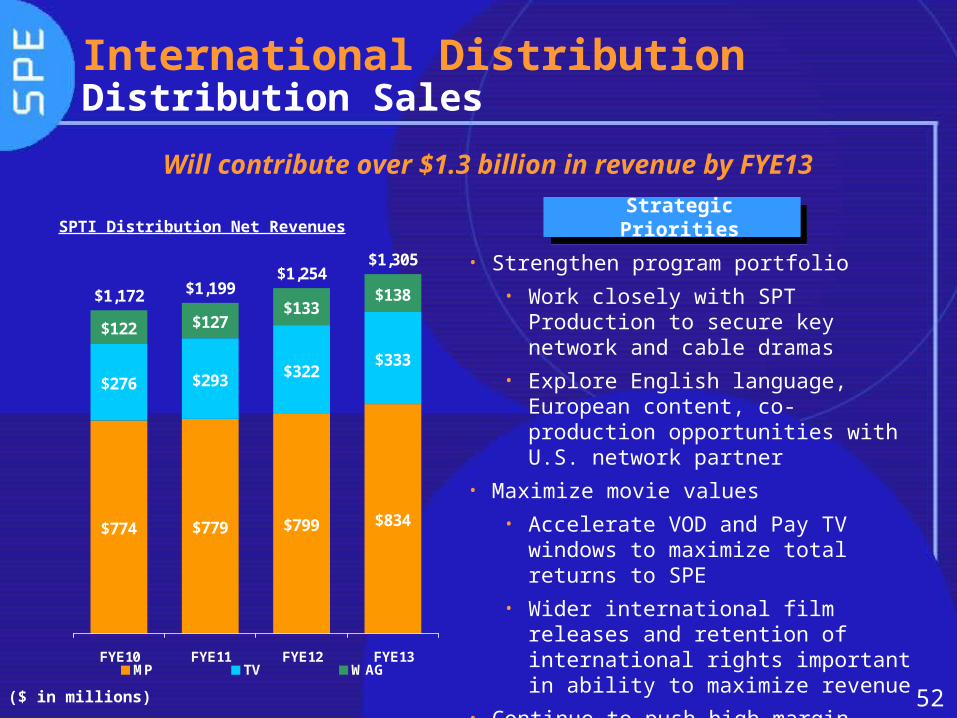

• Strengthen program portfolio• Work closely with SPT Production to

secure key network and cable dramas

• Explore English language, European content, co-production opportunities with U.S. network partner

• Maximize movie values• Accelerate VOD and Pay TV

windows to maximize total returns to SPE

• Wider international film releases and retention of international rights important in ability to maximize revenue

• Continue to push high-margin library sales

• Expand SPT’s presence in select emerging markets, e.g., Middle East, Africa

($ in millions)

International DistributionDistribution Sales

Will contribute over $1.3 billion in revenue by FYE13

SPTI Distribution Net Revenues

$834 $799$779 $774

$333$322 $293$276

$138$133

$127 $122

$1,172 $1,199$1,254

$1,305

FYE10 FYE11 FYE12 FYE13MP TV WAG

Strategic Priorities

53

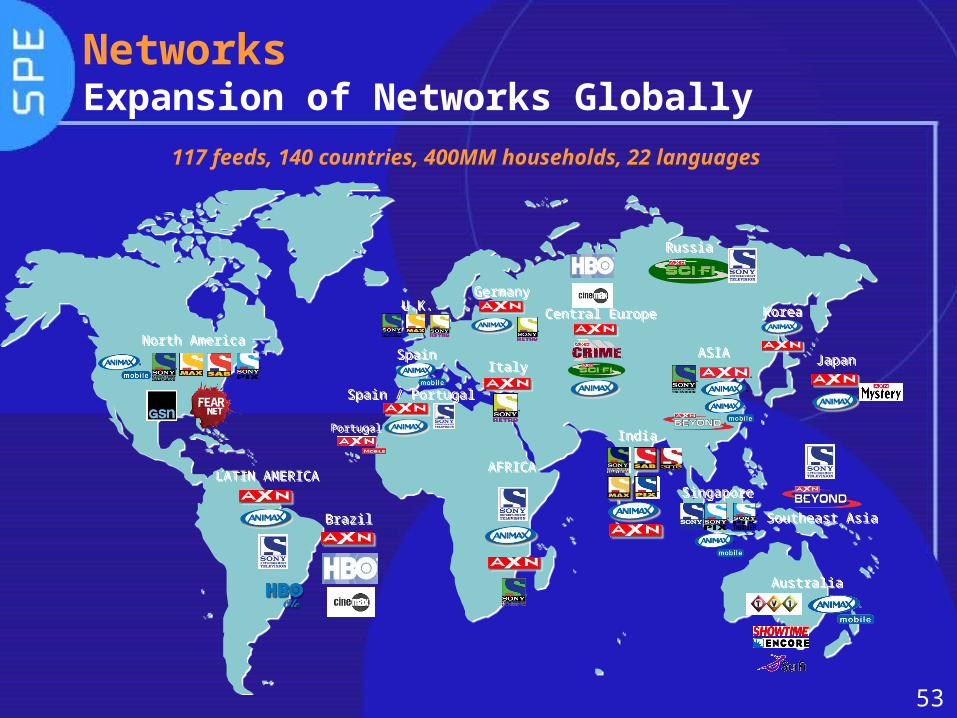

NetworksExpansion of Networks Globally

KoreaKorea

LATIN AMERICALATIN AMERICA

Central EuropeCentral Europe

North AmericaNorth America

BrazilBrazil

SpainSpain

Spain / PortugalSpain / Portugal

RussiaRussia

SingaporeSingapore

AFRICAAFRICA

Southeast AsiaSoutheast Asia

JapanJapanASIAASIA

AustraliaAustralia

U.K.U.K.

IndiaIndia

GermanyGermany

ItalyItaly

PortugalPortugal

117 feeds, 140 countries, 400MM households, 22 languages

54

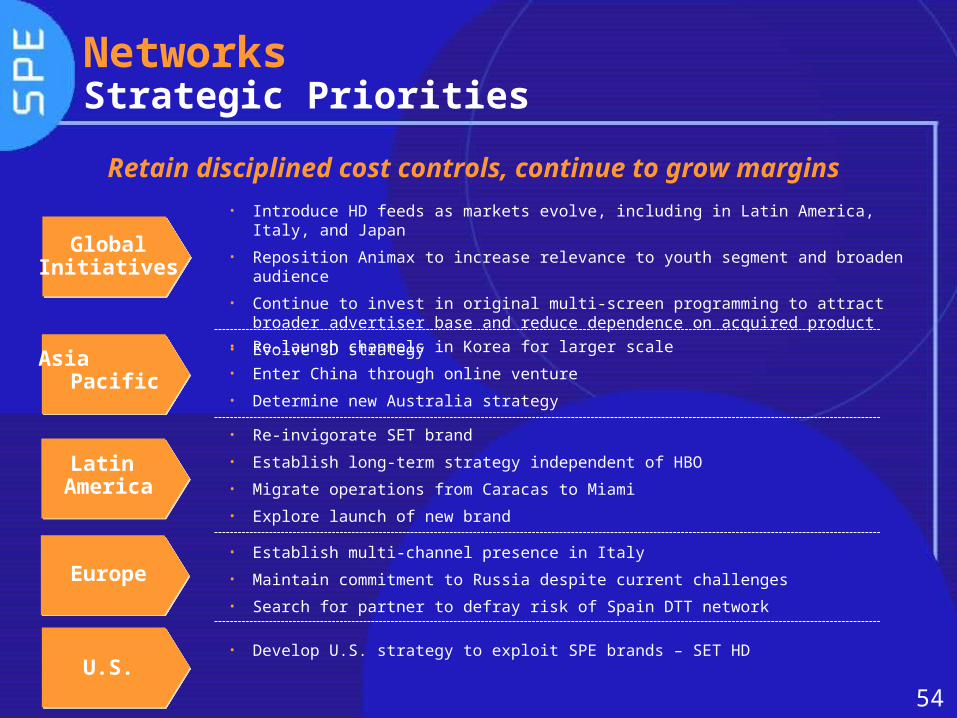

Global Initiatives

Latin America

Europe

U.S.

• Re-launch channels in Korea for larger scale

• Enter China through online venture

• Determine new Australia strategy

• Re-invigorate SET brand

• Establish long-term strategy independent of HBO

• Migrate operations from Caracas to Miami

• Explore launch of new brand

• Establish multi-channel presence in Italy

• Maintain commitment to Russia despite current challenges

• Search for partner to defray risk of Spain DTT network

• Develop U.S. strategy to exploit SPE brands – SET HD

Asia Pacific

• Introduce HD feeds as markets evolve, including in Latin America, Italy, and Japan

• Reposition Animax to increase relevance to youth segment and broaden audience

• Continue to invest in original multi-screen programming to attract broader advertiser base and reduce dependence on acquired product

• Evolve 3D strategy

Retain disciplined cost controls, continue to grow margins

NetworksStrategic Priorities

55

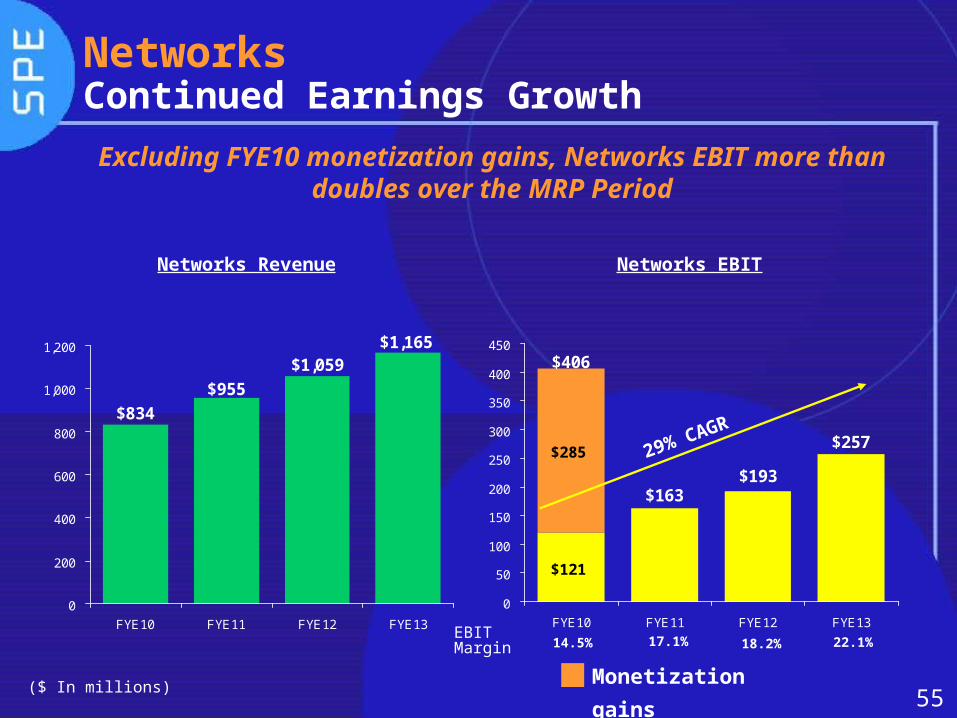

NetworksContinued Earnings Growth

Excluding FYE10 monetization gains, Networks EBIT more than doubles over the MRP Period

($ In millions)

Networks Revenue Networks EBIT

Monetization

gains

$1,165$1,059

$955

$834

0

200

400

600

800

1,000

1,200

FYE10 FYE11 FYE12 FYE13

$121

$285$257

$193$163

$406

0

50

100

150

200

250

300

350

400

450

FYE10 FYE11 FYE12 FYE13

29% CAGR

14.5% 17.1% 18.2% 22.1%EBIT Margin

56

$12$17

$27

$40

($11)($6)

$1

$12

($15) ($12)($8)

$0($ In millions)

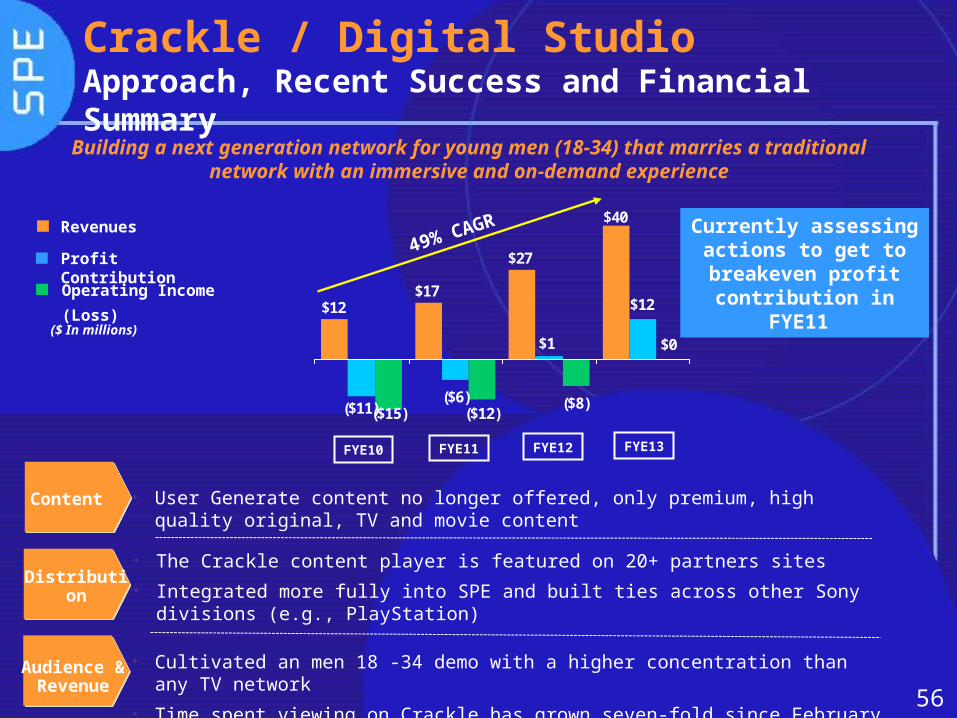

Crackle / Digital StudioApproach, Recent Success and Financial Summary

FYE11 FYE12 FYE13FYE10

Audience & Revenue

Distribution

• User Generate content no longer offered, only premium, high quality original, TV and movie content

• The Crackle content player is featured on 20+ partners sites

• Integrated more fully into SPE and built ties across other Sony divisions (e.g., PlayStation)

• Cultivated an men 18 -34 demo with a higher concentration than any TV network

• Time spent viewing on Crackle has grown seven-fold since February ‘09

Content

Building a next generation network for young men (18-34) that marries a traditional network with an immersive and on-demand experience

Revenues

Operating Income

(Loss)

Profit Contribution

49% CAGR Currently assessing

actions to get to breakeven profit contribution in

FYE11

57

Divisional DetailsDigital ProductionDigital Production

58

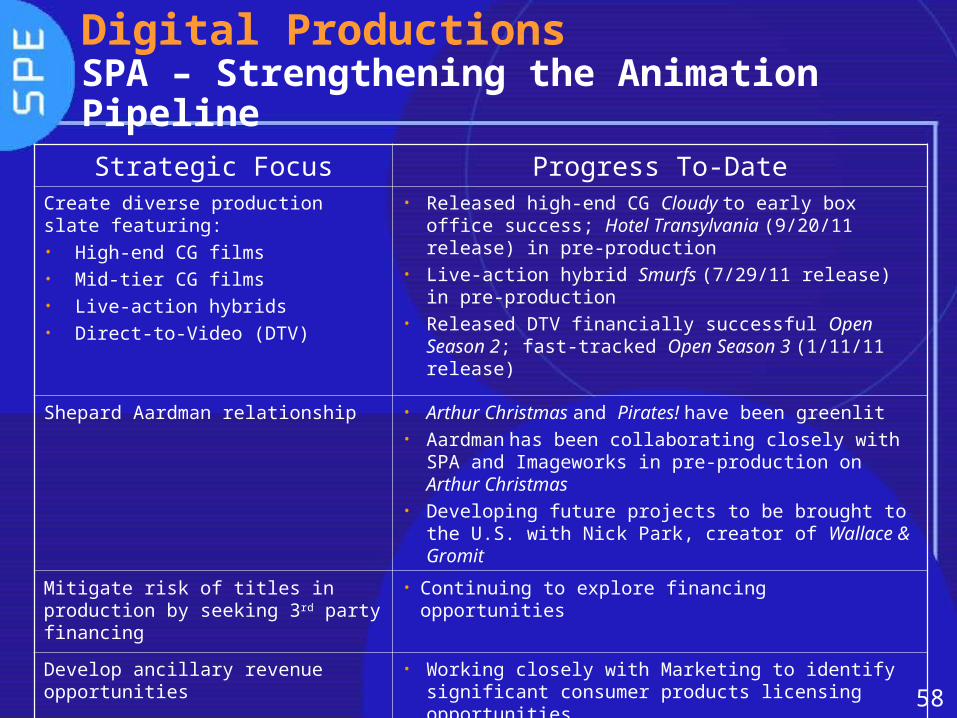

Strategic Focus Progress To-DateCreate diverse production slate featuring:• High-end CG films• Mid-tier CG films• Live-action hybrids• Direct-to-Video (DTV)

• Released high-end CG Cloudy to early box office success; Hotel Transylvania (9/20/11 release) in pre-production

• Live-action hybrid Smurfs (7/29/11 release) in pre-production

• Released DTV financially successful Open Season 2; fast-tracked Open Season 3 (1/11/11 release)

Shepard Aardman relationship • Arthur Christmas and Pirates! have been greenlit• Aardman has been collaborating closely with SPA

and Imageworks in pre-production on Arthur Christmas

• Developing future projects to be brought to the U.S. with Nick Park, creator of Wallace & Gromit

Mitigate risk of titles in production by seeking 3rd party financing

• Continuing to explore financing opportunities

Develop ancillary revenue opportunities

• Working closely with Marketing to identify significant consumer products licensing opportunities

Digital ProductionsSPA – Strengthening the Animation Pipeline

59

Digital ProductionsSPA - Capitalizing on Franchise Opportunities

• Even modestly successful theatrical CG animated films can become profitable franchises

• As a result of the strong performance of the direct-to-video (DTV) release of Open Season 2, profitability of the Open Season franchise is approximately $40m (10% margin)

o An additional $8m of gross profit anticipated from the from the DTV release of Open Season 3 in January 2011

• DTVs can also be opportunistically released theatrically overseas, which also enhances their home entertainment performance

• Cloudy with a Chance of Meatballs is the next property to be considered for DTV or theatrical release

60

Digital ProductionsImageworks

• Dependable source of digital animation and VFX expertise

o All services provided internally are at ‘net cost’

• Becoming more price competitive

o Reducing overall labor costs further through minimizing artist gap time

o Simplifying production technology and standardizing software tools

o Continuing to shift work to satellites in tax and cost advantaged areas (New Mexico and India)

o Non-billable costs to decrease by a 38.6% CAGR over the period from FYE08 through FYE13

• Using 3rd party work as a means to reduce SPA and Columbia production cost

o Strengthen relationships with large studio clients – Disney and Warner Bros.

61

Financial Summary

62

Financial SummaryOverview

• EBIT, excluding restructuring costs and FYE10 asset sales, grows to $550m by FYE13, a 41% CAGR, despite

o Lower contribution from the Home Entertainment marketo Continued margin pressures on acquisition producto Overall recessionary environment

• EBIT margin improves to 6.1% by FYE13• $255m of cost reduction initiatives included in FYE11• Breakeven Net Cash Flow currently assumed for FYE11

o Will require a significant reduction in motion picture production spending as well as other action items that are currently being evaluated

o Excludes $15m of incremental restructuring costs for overhead reductions initiatives

• Net Cash flow improves to $100m and $200m in FYE12 and FYE13, respectively

63

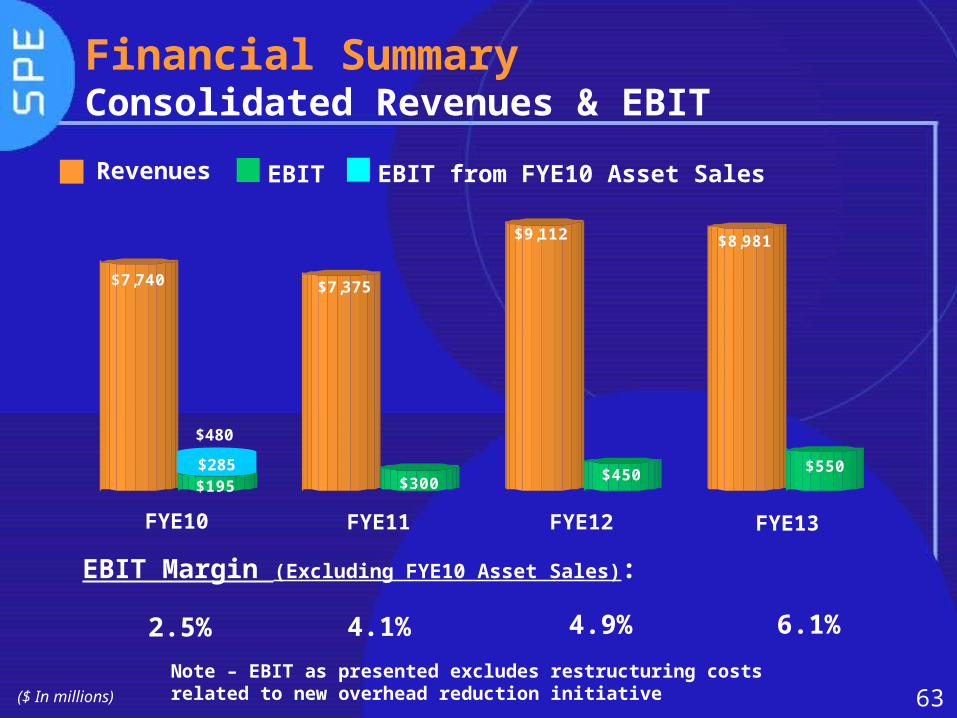

Financial SummaryConsolidated Revenues & EBIT

($ In millions)

FYE10 FYE11 FYE12 FYE13

EBIT Margin (Excluding FYE10 Asset Sales):

2.5% 4.1% 4.9% 6.1%

$7,740

$195

$7,375

$300

$9,112

$450

$8,981

$550$285

$480

EBITRevenues EBIT from FYE10 Asset Sales

Note – EBIT as presented excludes restructuring costs related to new overhead reduction initiative

64

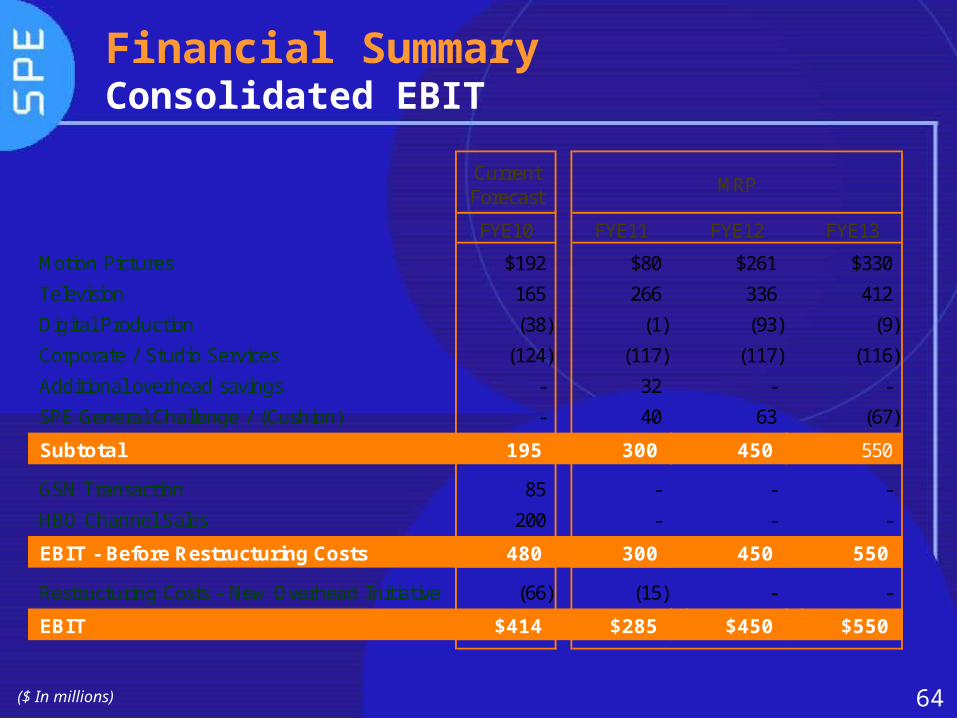

Financial Summary Consolidated EBIT

($ In millions)

Current Forecast

MRP

FYE10 FYE11 FYE12 FYE13

Motion Pictures $192 $80 $261 $330

Television 165 266 336 412

Digital Production (38) (1) (93) (9)

Corporate / Studio Services (124) (117) (117) (116)

Additional overhead savings - 32 - -

SPE General Challenge / (Cushion) - 40 63 (67)

Subtotal 195 300 450 550

GSN Transaction 85 - - -

HBO Channel Sales 200 - - -

EBIT - Before Restructuring Costs 480 300 450 550

Restructuring Costs - New Overhead Initiative (66) (15) - -

EBIT $414 $285 $450 $550

65

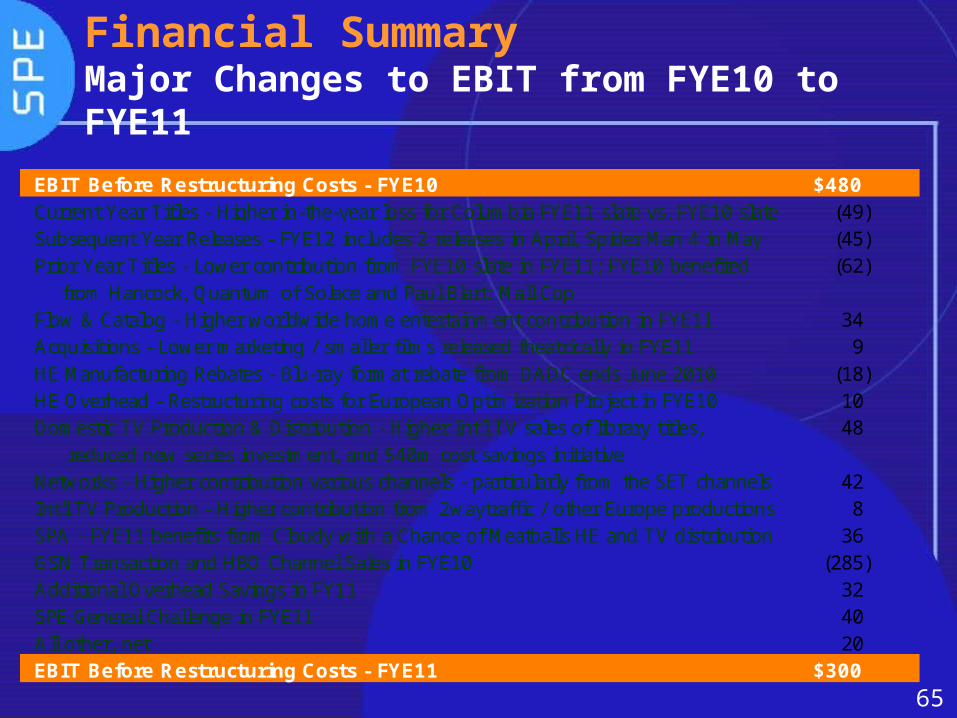

Financial Summary Major Changes to EBIT from FYE10 to FYE11

EBIT Before Restructuring Costs - FYE10 $480Current Year Titles - Higher in-the-year loss for Columbia FYE11 slate vs. FYE10 slate (49) Subsequent Year Releases - FYE12 includes 2 releases in April, Spider Man 4 in May (45) Prior Year Titles - Lower contribution from FYE10 slate in FYE11; FYE10 benefited (62)

from Hancock, Quantum of Solace and Paul Blart: Mall CopFlow & Catalog - Higher worldwide home entertainment contribution in FYE11 34 Acquisitions - Lower marketing / smaller films released theatrically in FYE11 9 HE Manufacturing Rebates - Blu-ray format rebate from DADC ends June 2010 (18) HE Overhead - Restructuring costs for European Optimization Project in FYE10 10 Domestic TV Production & Distribution - Higher Int'l TV sales of library titles, 48

reduced new series investment, and $40m cost savings initiativeNetworks - Higher contribution various channels - particularly from the SET channels 42 Int'l TV Production - Higher contribution from 2waytraffic / other Europe productions 8 SPA - FYE11 benefits from Cloudy with a Chance of Meatballs HE and TV distribution 36 GSN Transaction and HBO Channel Sales in FYE10 (285) Additional Overhead Savings in FY11 32 SPE General Challenge in FYE11 40 All other, net 20 EBIT Before Restructuring Costs - FYE11 $300

66

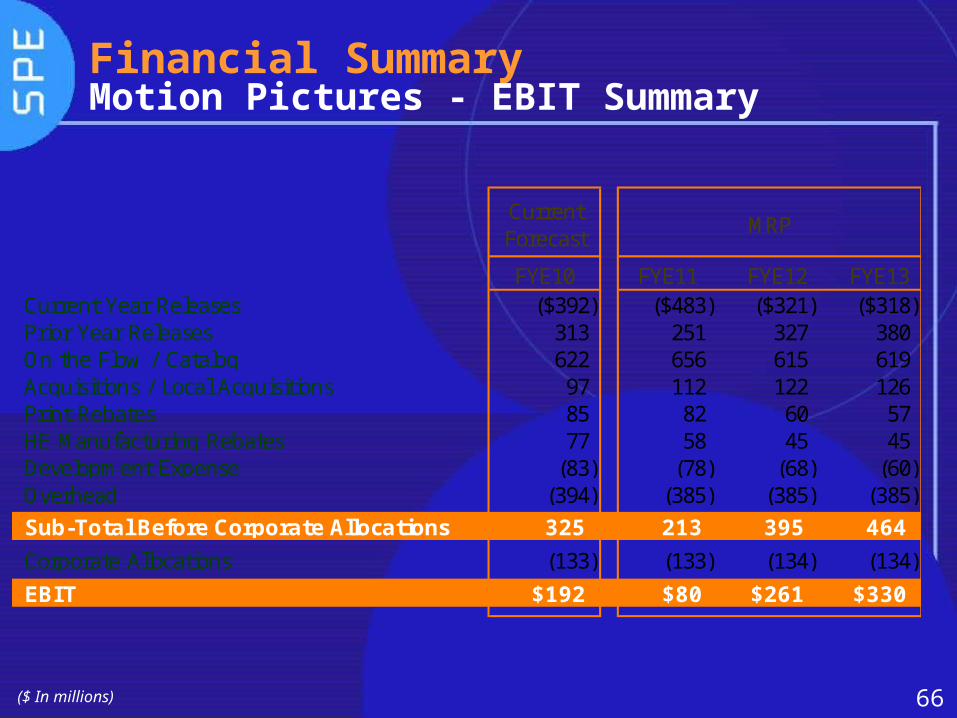

Financial SummaryMotion Pictures - EBIT Summary

($ In millions)

Current Forecast

MRP

FYE10 FYE11 FYE12 FYE13Current Year Releases ($392) ($483) ($321) ($318)Prior Year Releases 313 251 327 380 On the Flow / Catalog 622 656 615 619 Acquisitions / Local Acquisitions 97 112 122 126 Print Rebates 85 82 60 57 HE Manufacturing Rebates 77 58 45 45 Development Expense (83) (78) (68) (60) Overhead (394) (385) (385) (385)

Sub-Total Before Corporate Allocations 325 213 395 464

Corporate Allocations (133) (133) (134) (134)

EBIT $192 $80 $261 $330

67

Financial SummaryTelevision - EBIT Summary

($ In millions)

Current Forecast

MRP

FYE10 FYE11 FYE12 FYE13

Daytime Series / Game Shows $131 $128 $141 $139Third Party Distribution 35 35 15 12 Catalog Product 51 59 65 69Network, Cable & First Run Syndication (1) 6 23 24 Development (29) (25) (25) (25) Crackle / Digital Studio (15) (12) (8) - ENCORE Bonus 48 48 48 48 Earnings challenge 19 40 35 22 Overhead / Other (71) (61) (55) (51)

Domestic TV Production & Distribution 168 218 239 238

Networks 121 163 193 257 International Production 10 18 39 52 International Distribution (54) (53) (54) (54)

Sub-Total Before Corporate Allocations 245 346 417 493

Corporate Allocations (80) (80) (81) (81)

EBIT $165 $266 $336 $412

68

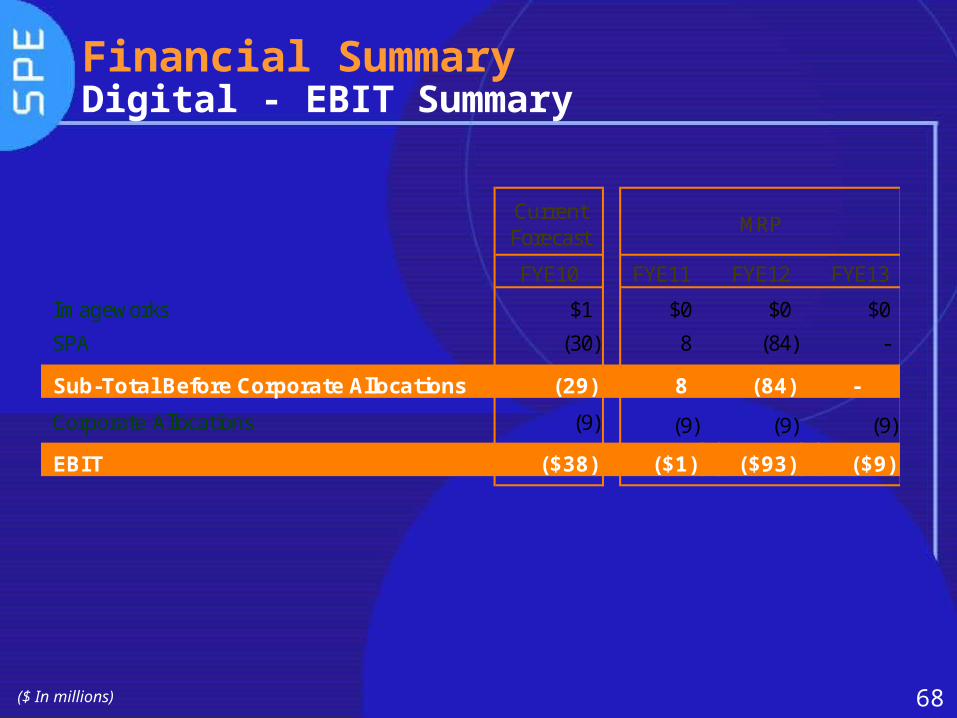

Financial SummaryDigital - EBIT Summary

($ In millions)

Current Forecast

MRP

FYE10 FYE11 FYE12 FYE13

Imageworks $1 $0 $0 $0

SPA (30) 8 (84) -

Sub-Total Before Corporate Allocations (29) 8 (84) -

Corporate Allocations (9) (9) (9) (9)

EBIT ($38) ($1) ($93) ($9)

69

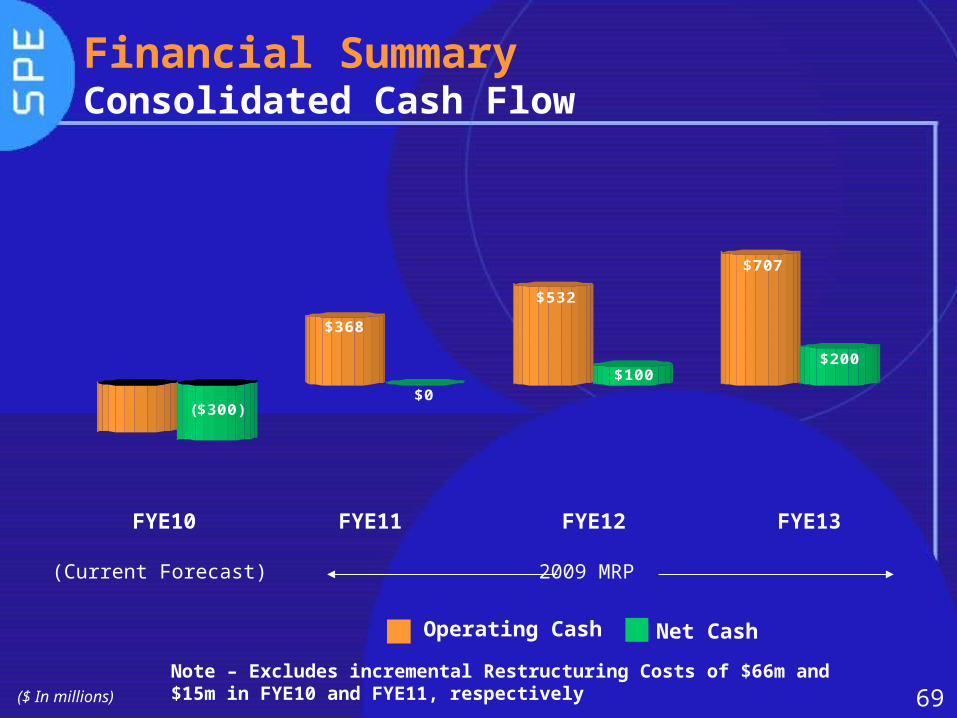

Financial SummaryConsolidated Cash Flow

FYE10 FYE11 FYE12 FYE13

(Current Forecast) 2009 MRP

Operating Cash Net Cash

($ In millions)

($300)

$368

$0

$532

$100

$707

$200

($260)

Note – Excludes incremental Restructuring Costs of $66m and $15m in FYE10 and FYE11, respectively

70

Closing

71

Closing Summary

FYE11 will continue to suffer from the same

challenges we are experiencing in the current

fiscal year. However, we are committed to act

upon the strategies we have outlined for your

today to mitigate the short term impacts while

positioning ourselves for improved profitability and

positive cash flow in FYE12 and FYE13

72