1. - open repositoryarizona.openrepository.com/arizona/bitstream/10150/602141/1/tb244.pdf · and...

TRANSCRIPT

Laser Leveling and Farm Profits

Item Type text; Book

Authors Daubert, John; Ayer, Harry

Publisher College of Agriculture, University of Arizona (Tucson, AZ)

Rights Copyright © Arizona Board of Regents. The University of Arizona.

Download date 16/07/2018 11:36:52

Link to Item http://hdl.handle.net/10150/602141

:t;; Ml

V sLtiFv" w+ 0tie.a-:. Vi.l. MUgaee{..

Re'vA'a,:hit =' a.:^. `rr++t.r T o , -.. .. .... . i .i ..: w'-u'+ssari:: _ `:r+w ` .i» : :. .rt' -

''.y' . « 's

ti /c° .."6.° ähpg..qg... .a FA.d w,s84;.0 . ° . . ".,tn$' ; nb.... o «ie: :,;. . . ...

` y+':y`,. awt^e .+.,.-.. t ¿ v .:Æ9r"ëLiEjç .,,, '.{.21a,á° C°" ''di' ". `5 r`a t C,w.

A °R4.A N...,k AtS+Ai Y

' }n.w',...'..,a ;jua«b . «nWU.h:.. ,a.. .,-á-.e+.t.' .. .".r.:6. {, ep '1.. 'iP"r$+°.,r.' vAR"OP1. `¡y, 1. reYeN' ¡p ,I=..l.

.^s' TM RAw ot:. .''. .r..°+f." .a. ,:rA',A+ ,,"." ?.e"'AW' u.r . t,.."j....:.

. ".E

'gf r:..,.z}.;,r"," ;gJw.° ' : i ti^. "ti:; .

EV;'-9ow ..C..°!+a.^^'+.rz..;p+s. a" .t^a w: :..a.w.e,. "` . . ..... "1: . . . ' .. " M" ..G eiY:'.

;-"A44a. ..., s: ca t;ä a, . '

:lc.hf Daubert and Harry Ayer

Technical Bulletin Number 244 Agricultural Ex.periamenl Station, College of Agriculture

The trniversil:y of Ari.zonai.

and Natural Resource Economics Division

Economic Research Service United States Department of Agriculture

Tucson, Arizona o June 1982

Laser Levelin g and Farm Profits

John Daubert and Harry Ayer

Technical Bulletin Number 244 Agricultural Experiment Station, College of Agriculture

The University of Arizona and

Natural Resource Economics Division Economic Research Service

United States Department of Agriculture Tucson, Arizona June 1982

John Daubert is an assistant professor of agricultural economics, University of Arizona, and Harry Ayer is an agricultural economist, Natural Resource Economics Division, ERS, USDA, and adjunct professor of agricultural economics, University of Arizona. (Cover design by Mark Lynham)

Acknowledgements

The Natural Resource Economics Division, Economic Research Service, U.S. Depart-

ment of Agriculture and the University of Arizona's Agricultural Experiment Station and

the Department of Agricultural Economics, College of Agriculture, provided support for

this research. We appreciate the assistance of the following persons who provided information used

in our analysis: Robert Abels, Steven Jones, and Carl Pacek of the Soil Conservation Ser-

vice; Allan Halderman, Scott Hathorn, Jr. and Walter Hinz of the University of Arizona; Pedro Gonzales of the Agricultural Stabilization and Conservation Service; and Walter Parsons of the Arizona Department of Water Resources and the Soil Conservation Ser-

vice.

We also thank those who commented on an earlier draft of this report: Robert Abels of the Soil Conservation Service; Wilford Gardner, Allan Halderman, Scott Hathorn, Jr. and Walter Hinz of the University of Arizona; James Croghan of the Agricultural Stabili- zation and Conservation Service; Walter Parsons of the Arizona Department of Water

Resources and Soil Conservation Service; and John Hostetler of the Economic Research Service.

Introduction

According to the 1980 Groundwater Act, irrigated agri-

culture in Arizona faces increasingly strict water use regula-

tions. While water conservation is an important goal in arid

Arizona, farmers must typically make significant economic sacrifices if they are to reduce water use. Most technologies to conserve water on the farm require large initial capital costs for structures and equipment. Other non -structural water conservation strategies, specifically those involving exotic low water use crops, can also be expensive, since

those crops currently produce less net farm income corn-

pared with net returns from irrigated cotton, alfalfa, and small grain. Fortunately, several new irrigation systems, in-

cluding level basins, sprinkler, drip, and others, help Arizo- na farmers conserve water and may increase farm profits. The following analysis focuses only on the profitability of laser leveling. Given current water supply, water cost, and water law in Arizona, laser leveling is profitable on many farms. But, before investing in laser leveling, the farmer should compare the potential net gain from alternative technologies.

Farmers can use laser -leveling technology' to 1) smooth the slope of their existing furrow irrigation system, i.e.,

1The technology of laser leveling is described by Hinz and Halder- man: "The laser beam is transmitted from a rotating command post generating a light plane on the level or at predetermined grade. A receiver is mounted on a mast attached to a scraper. The signal

laser plane to slope, or 2) dead level their fields to make a

level border irrigation system. Both laser -leveling invest- ments conserve water by improving irrigation application efficiencies -reducing runoff and deep percolation. Laser leveling may also increase farm profits. Farmers who use less water will lower water costs and may increase crop rev-

enues, since laser leveling can improve crop yields through better water distribution over the field.

Even with water cost savings and yield benefits, some farm- ers may find that laser -leveling investments are too expensive. To encourage laser leveling, the cost -sharing program of the Agricultural Stabilization and Conservation Service (ASCS)

and accelerated tax depreciation reduce private investment costs. Even though the incentive programs make investment favorable on more farms, the current programs limit the max- imum per year cost -share payment and tax deduction and therefore may slow the rate at which farmers laser level their farms. Some farmers will find that laser leveling only a few acres per year over many years is more profitable than laser leveling the whole farm immediately.

keeps the scraper blade on the desired grade by operating hydraulic control valves automatically. Results obtained have been within plus or minus five hundredths (.05) of a foot. This is greater ac- curacy than can be obtained with traditional land leveling methods.

Laser beam land leveling equipment includes: (1) tractor, (2) drag scraper, (3) laser command post, receiver and control box, and (4) hydraulic valve, pump, hose and connections."

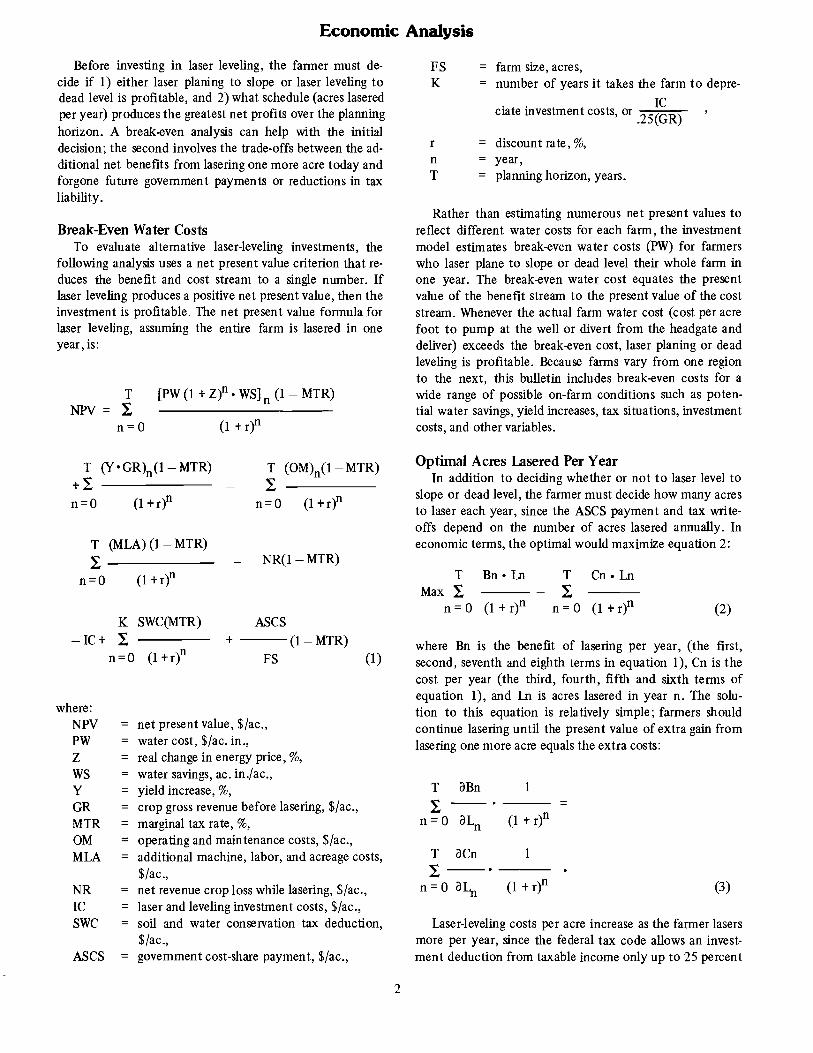

Economic Analysis

Before investing in laser leveling, the farmer must de-

cide if 1) either laser planing to slope or laser leveling to dead level is profitable, and 2) what schedule (acres lasered per year) produces the greatest net profits over the planning horizon. A break -even analysis can help with the initial decision; the second involves the trade -offs between the ad- ditional net benefits from lasering one more acre today and forgone future government payments or reductions in tax liability.

Break -Even Water Costs To evaluate alternative laser -leveling investments, the

following analysis uses a net present value criterion that re-

duces the benefit and cost stream to a single number. If laser leveling produces a positive net present value, then the investment is profitable. The net present value formula for laser leveling, assuming the entire farm is lasered in one year, is:

T [PW (1 + Z)n WS] (1 - MTR) NPV =

n=0 (l +r)n

T (Y GR)n(1 - MTR) + n=0 (l +r)n

T (MLA) (1- MTR) - n=0 (1+r)n

K SWC(MTR)

-IC+ I n=0 (l+r)n

where: NPV =

PW = Z= WS = Y= GR =

MTR =

OM =

MLA =

NR =

IC

SWC =

ASCS =

T (0M)n(1- MTR)

- n=0 (l+r)n

- NR(1- MTR)

ASCS

+ (1- MTR)

FS (1)

net present value, $ /ac., water cost, $ /ac. in., real change in energy price, %,

water savings, ac. in. /ac., yield increase, %,

crop gross revenue before lasering, $ /ac., marginal tax rate, %,

operating and maintenance costs, $ /ac., additional machine, labor, and acreage costs, $ /ac., net revenue crop loss while lasering, $ /ac., laser and leveling investment costs, $ /ac., soil and water conservation tax deduction, $ /ac., government cost -share payment, $ /ac.,

2

FS =

K =

r =

n =

T =

farm size, acres, number of years it takes the farm to depre-

ciate investment costs, or .25(GR)

discount rate, %,

year, planning horizon, years.

Rather than estimating numerous net present values to reflect different water costs for each farm, the investment model estimates break -even water costs (PW) for farmers who laser plane to slope or dead level their whole farm in one year. The break -even water cost equates the present value of the benefit stream to the present value of the cost stream. Whenever the actual farm water cost (cost per acre foot to pump at the well or divert from the headgate and deliver) exceeds the break -even cost, laser planing or dead leveling is profitable. Because farms vary from one region to the next, this bulletin includes break -even costs for a

wide range of possible on -farm conditions such as poten- tial water savings, yield increases, tax situations, investment costs, and other variables.

Optimal Acres Lasered Per Year In addition to deciding whether or not to laser level to

slope or dead level, the farmer must decide how many acres to laser each year, since the ASCS payment and tax write - offs depend on the number of acres lasered annually. In economic terms, the optimal would maximize equation 2:

T Bn Ln T Cn Ln Max E E

n=0 (l+r)n n=0 (1+r)n (2)

where Bn is the benefit of lasering per year, (the first, second, seventh and eighth terms in equation 1), Cn is the cost per year (the third, fourth, fifth and sixth terms of equation 1), and Ln is acres lasered in year n. The solu- tion to this equation is relatively simple; farmers should continue lasering until the present value of extra gain from lasering one more acre equals the extra costs:

T ôBn 1

n=0 âLn (1 + r)n

T aCn 1

n=0 aLn (1 + r)n (3)

Laser -leveling costs per acre increase as the farmer lasers more per year, since the federal tax code allows an invest- ment deduction from taxable income only up to 25 percent

of gross farm income in the year the farmer takes the de-

duction. Investment costs which exceed the 25 percent limit may be deducted from succeeding years' taxable in-

come, again subject to the same 25- percent rule. Deduc- tions which must be carried forward represent a real cost - the opportunity cost of money. The farmer could have

earned interest on the money invested but not deducted from income taxes. The model determines whether the added water savings and yield benefits from laser leveling one more acre exceed the opportunity cost of the interest forgone on money not deducted from taxable income. If

the opportunity cost of laser leveling an additional acre is

less than the benefits, then more is leveled, and vice versa. Similarly, laser -leveling benefits can vary with the num-

ber of acres the farmer levels. The ASCS cost -share program typically pays 50 percent of investment costs, up to a max-

imum of $3,500 per year. Once the farmer receives $3,500, cumulative ASCS benefits can increase only by laser level- ing less this year and more in future years. The model com- pares the water savings plus yield benefits from laser level- ing more now with the present value of forgone future ASCA payments.

Laser Leveling Benefits and Costs Benefits

Water Savings Benefits (PWWS). Arizona farms with ex-

pensive irrigation water will receive the greatest benefit from laser leveling. The effective water costs (PW), dollars per acre

inch of water to pump or divert and deliver, varies greatly in

Arizona. On farms using wells, PW depends on the lift, fuel

prices, pump efficiency, and on -farm irrigation delivery ef-

ficiencies. The cost of surface water varies with the user or

ditch fee and delivery efficiency. The basic data for water

cost comes from Arizona Cooperative Extension crop and

pump water budgets [Hathom and co- authors] .

The amount of water saved (WS) depends upon the crop

consumptive water use and the change in irrigation field ef-

ficiency after laser leveling. Farmers who dead level their fields can increase application efficiency from 50 -65 percent on traditional slope- furrow systems to 85 -90 percent. Laser

planing to slope improves application efficiency from 50 -65

percent to 60-70 percent [Parsons] . Specific farm efficien-

cy improvements will depend on initial field efficiency, ex-

isting irrigation system, and soil texture, but they should fall within those ranges.

This study uses Erie, et. al. to indicate consumptive use

by crops in the Mesa, Arizona area and the Blaney - Criddle

method to estimate consumptive use in other locations, plus the above range of efficiency improvements to esti-

mate water use savings from laser leveling. Given con-

sumptive water use for cotton, wheat, sorghum, and alfalfa

in the Mesa area of 41, 26, 25, and 74 acre inches per acre,

respectively, the water savings for laser planing to slope

range from five to 15 acre inches per acre, while the water savings for dead leveling range from 10 to 30 acre inches per acre. For example, if cotton consumptive use of water is 41 acre inches and initial field efficiency is 60 percent, then the total water application needed to reach the crop is

68 acre inches (41 ac. in. - .60). Assuming field efficiency

increases to 85 percent, total water needed per acre is 48

inches (41 ac. in. - .85), a reduction of 20 acre inches per acre. Savings for other crops, and for situations in which more than one crop is harvested within a year (double cropping), are computed in a similar fashion.

The expected increase in energy prices (Z) can also af-

fect water savings benefits. Lasering becomes more profit-

3

able when the price for energy inputs needed to pump or

divert water increases faster than the general farm inflation rate. Winter 1980 -81 projections of electricity price over

the next 10 years [Data Resources, Inc.] indicate that the nominal price of electricity will increase approximately 10 percent per year through 1990. The 10 percent price increase is about the same as the projected rate of general inflation. Projected price increases are expected to level

out, relative to inflation, primarily as a result of a decrease in the proportion of electric utilities which use natural gas

and petroleum as fuel sources. Some areas of Arizona may experience either a greater

increase in the price of fuel or an increase in pumping costs due to declining well yields or lift depths. Therefore, the break -even analysis assumes, first, that the nominal rate of increase in the unit cost of water is 10 percent, the same as

the model's general inflation rate, and, second, that unit water costs increase at 13 percent. Even those assumptions may understate future energy price increases for some Ari-

zona irrigators. Some irrigators using low priced electricity from utilities which buy their electricity from federal hy- droelectric sources at rates established by long -term con- tracts may experience a substantial increase in electricity prices when the contracts begin to expire in 1987.

Yield Increase Benefits (Y GR). Lasere d fields uniformly distributing water over the crop may increase yields (Y). No data are available on yield increase resulting from lasering, but estimates of extension agents and others familiar with lasered farms suggest that after two years yields may in- crease from zero to over 10 percent for laser planing to slope and zero to 30 percent for dead leveled fields [Parsons] .

Gross farm incomes are estimated using a range of cotton prices, yields and farm acreages. The price of cotton fiber ranged from $ß0 to $1 per pound (in 1981 dollars) between 1973 and 1981. Fiber yields in 1980 varied from 600 to 1,000 pounds per acre, depending upon the county, but average yield for most of Arizona exceeded 900 pounds. Based on these data, the analysis uses gross income of $700 per acre.

If added yield significantly increases harvesting costs, they should be subtracted from gross income. Our analysis assumes harvesting costs do not increase.

Costs Investment Costs (IC). Total investment costs may include

removing and replacing existing ditch systems for dead level irrigation systems, major earth moving from high to low spots, erosion control structures, and laser beam operations. For specific farm conditions and locations, costs of dead level- ing may exceed 25% of the cost of irrigated land in Arizona.

The cost to remove old and install new ditches will de- pend upon the length, location and elevation of old and new ditches. Assuming that concrete -lined ditches cost $3 -$5 per foot (October 1981), and that the farmer re-

places all ditches, ditching costs are approximately $350 per acre [Parsons] . Since Arizona farmers save some

ditches, the cost of removing and adding ditches for laser - leveled fields is about $100 per acre [Abels] .

Custom earth movers currently charge $.35 to $.45 per cubic yard. For a dead -level field, farmers must move from 400 to 1,000 cubic yards per acre, depending on initial slope, while farmers who laser plane to the exist- ing slope may move 150 to 450 cubic yards per acre. In addition, fields with initial grades of .6 percent or greater require chiseling to loosen subsoil, and up to 20 tons per acre of steer manure to replace topsoil. Chiseling costs $16 per acre, and steer manure approximately $5 per ton.

Other first year costs for some dead -level fields include the installation of erosion control structures at $900 per 10 -acre block, check gates costing $300 each to service 20 to 40 acres, and one flume costing $350 for each farm.

Parsons estimates initial investment costs of dead level-

ing of $400, $500 and $600 per acre would apply to 25, 50 and 25 percent, respectively, of the irrigated land in Arizona, and that laser planing initial investment costs are

$100 to $200 per acre. These costs are used in the sensitivi- ty analysis.

Operation and Maintenance Costs (OM). Annual touch- up is recommended on both lasered and non -lasered fields, but lasered fields require special attention each three to five years. The special laser touch -up costs approximately $50 per acre. The break -even analysis assumes that the farmer touches up lasered fields every five years at $50 per acre.

Net Crop Revenue Forgone While Laser Leveling (NR). Net crop revenue forgone while lasering depends upon the crop sacrificed. Usually, laser leveling is scheduled during the small -grain segment of a crop rotation. Budget data in- dicate that in Maricopa, Pima, Pinal and Yuma Counties, for wheat prices near $7.50 per hundredweight and sor- ghum near $6 per hundredweight, the farm returns over total variable costs sacrificed during lasering ranged from $14 to $235 per acre in 1980. The analysis assumes a loss of $150 per acre return over total variable cost.

Machine, Labor, and Acreage Costs for Dead Leveled Fields (MLA). Farmers who change from furrow irrigation to a basin system generally incur added machinery costs, extra irrigation labor cost, and acreage losses. The break - even analysis includes a 12 percent or $26 per acre in- crease in machine cost resulting from the added turning

4

time, a $7 per acre increase in labor costs resulting from fre- quent switching of water from one basin to the next, and a three percent or $4 per acre decrease in long -run net reve- nues resulting from a three percent acreage loss for ad- ditional roads and canals.

Economic Time and Tax Factors Planning Horizon (T). The planning horizon is the ex-

pected life of laser -leveled fields. In some cases the bene- fits and costs from laser leveling continue indefinitely, since periodic touch -up leveling should prevent deteriora- tion. At the other extreme, the benefits and costs of laser leveling may terminate in a very few years if the land is

sold for subdivision development. The break -even analysis uses three planning horizons: 10, 25 and 50 years. Short planning horizons are appropriate for farmland that is ex- pected to go out of crop production or if new water -saving technology makes laser leveling obsolete. Long planning horizons are appropriate if the farmer expects to continue farm production or if the farm is sold to another farmer, since laser leveling, with periodic touch -up, should have an infinite life.

Real Rate of Discount (r). The real after -tax rate of dis-

count is the inflation -free rate at which the investor dis- counts future incomes or costs (Le., the individual's time preference for present or future income streams). In a per- fectly functioning economy the interest an investor is

willing to pay for an investment loan in an inflation -free economy would equal the real discount rate. Estimates from time periods when inflation was very low suggest a rate of 3 -5 percent, but some farmers may wish to dis- count the future more. The two rates used in the analysis, five percent and 10 percent, are equivalent to 10 and 20 percent before -tax discount rates for farmers in a 50 -per- cent tax bracket.

Marginal Tax Rate (MTR). The marginal tax bracket of the investor affects both net benefits and net costs of laser leveling. The marginal tax rate is a combination of federal and state rates and approximately equals:

Federal Tax Rate (1 -State Tax Rate) + State Tax Rate (1- Federal Tax Rate).

In Arizona, where the maximum state rate is eight percent, the marginal tax rate is only slightly less than the federal rate.

Nearly all farmers in Arizona are in the 35- percent feder- al tax bracket or higher. Consider a 300 -acre cotton farm in Pinal County, using wells with a 575 -foot lift. Given Hath- orn, Little, and Stedman 1980 budget reports and $32 per pound cotton prices, the net returns per acre above all variable costs, ownership costs, and a management fee, were $132; total farm profits, before taxes, were $39,600. From the 1980 personal income tax schedule, a person fil- ing a joint return with a $34,000 income and four deduc- tions would be in the 35- percent bracket.

Some farmers may exceed the 50% maximum tax rate.

Since no data are available on the distribution of farms in different tax brackets, the analysis assumes that if personal farm incomes are higher than those of the 50- percent tax bracket, farms will incorporate, and thus fall into the 48% tax bracket. The break -even analysis investigates ef-

fects of a 35- and 50- percent tax bracket.

Federal Incentive Programs The Agricultural Stabilization and Conservation Ser-

vice (ASCS) cost -share program promotes laser leveling by lowering water conservation investment costs. De- pending on the cost -sharing arrangement, the program reimburses the farmer for a percentage of investment

costs, up to a total farm limit per year. ASCS payments in Arizona often cover 50% of investment costs up to $3,500 per year maximum.

Federal laws, enacted in 1968, indirectly encourage water conservation investment by lowering the farmer's tax liability [Internal Revenue Service] . The soil and water conservation depreciation allowance lets farmers depreciate their laser leveling investment. This depreciation program is

different from others, since the deduction depends on the farm gross income, rather than asset life. The 1980 law lets farmers depreciate their investment up to 25 percent of gross farm income per year.

Is Laser Leveling Profitable? Break -even Results Break -even water costs are estimated for laser planing

to slope and to dead level assuming that (1) the ASCS pay- ments end after the initial investment and (2) the farmer lasers the whole farm in the first year. The results indicate that both laser planing to slope and dead leveling are often profitable. The choice between laser leveling to slope or dead leveling will depend on characteristics of a particu- lar farm. Our example farm has:

farm size (FS) = 500 acres, gross farm income (GR) _ $700 /acre, marginal tax rate (MTR) = 35 %,

real discount rate (r) = 5 %,

real increase in energy prices (z) = 0 %,

net revenue crop loss (NR)_ $150 /acre, dead level investment costs (IC) _ $600 /acre, laser planing to slope investment costs (IC) _ $200 /acre, operation and maintenance costs (OM) _ $50 /acre every

5 years, added machine, labor, and lost acreage costs (MLA) _

$37 /acre, ASCS payment (ASCS)_ $3,500 /year, dead level water savings (WS) =10 ac. in. /ac., laser planing to slope water savings (WS)= 10 ac. in. /ac., dead level yield increase (Y) = 10 %,

laser planing to slope yield increase (Y) = 3 %, and time horizon (T) = 25 years.

The break -even water cost (cost to divert or pump plus deliver) is $13 per acre foot for laser planing to slope and $17 per acre foot for dead leveling. Farms with similar characteristics should laser level if the farm water cost exceeds the break -even water price. Appendix A shows how to calculate break -even water costs for different conditions. Farms with different benefit and cost characteristics should laser plane to slope or dead level if the farm water cost exceeds the break -even water costs presented in Tables 1

and 2. Farmers who find both planing to slope and dead level-

ing profitable should choose the alternative with the great- est difference between the break -even cost and the farm water costs. For example, a farmer with current water costs of $45 per acre foot, laser- planing -to -slope investment costs

5

equal to $200 per acre, a real price of pumping increasing at three percent per year, water savings equal to 10 acre inches per year, a 25 -year planning horizon, and a zero yield increase, has water costs which exceed the break - even cost of water by $15 ($45 per acre foot actual water cost minus $30 per acre foot break -even cost from Table 1). For dead leveling, suppose the same farmer determines that investment costs are $400 per acre, the real price of fuel increases at an annual rate of three percent, water savings equal 20 acre inches per acre, there is a 25 -year planning horizon, and yields will increase by five percent. From Table 2, the break -even cost is $21 per acre foot, or $24 below the actual water cost. Under these condi- tions, even though both investments are profitable, dead leveling is preferred to laser planing to slope.

The sensitivity analysis of the break -even costs shows that potential yield benefits, water savings, investment costs, pumping cost inflation, and the planning horizon significantly affect break -even water costs. Even a three percent increase in yield substantially alters the break - even water cost when water savings are relatively low (for either laser planing to slope or dead leveling), but at higher water savings the yield effect is greatly reduced. Large yield increases, of say five percent for laser planing and 15 percent for dead leveling, can justify investment even with- out any water savings (break -even cost equals zero). Un- fortunately, experts disagree on just how much yields may increase.

Large water savings also lower break -even costs. Laser leveling reduces water applications from five to 30 acre inches per acre by increasing field efficiency on flood irri- gated fields. The effect of greater water savings on break - even prices is particularly important when yield increases are small.

Initial investment costs in Arizona generally range from $100 to $200 per acre for laser planing to slope and $400 to $600 for dead leveling. As investment costs increase within these ranges, the break -even price increases sharply if yields don't increase, but often only marginally if yields do increase.

The sensitivity analysis indicates that a three percent

Table 1. Break -Even Water Costs for Laser Planing to Slope: Different Investment Costs, Fuel Price Changes, Water Savings, Time Horizons, and Crop Yield Benefits; Arizona, 1980/81 a

$100 /ac IC 0% Z

5 ac in WS

10T 25T 50T 10 ac in WS

10T 25T 50T 15 ac in WS

10T 25T 50T

3% Z 5 ac in WS

10T 25T 50T 10 ac in WS 15 ac in WS

10T 25T 50T 10T 25T 50T

%Y $ /acft

0 86 62 55 44 32 38 30 22 18 76 45 31 39 24 16 27 16 10 1 67 43 36 34 22 18 25 16 12 60 33 21 31 18 11 21 12 7 3 35 9 2 18 5 1 12 4 1 30 7 1 15 4 1 10 3 0 5 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

5 ac in WS 10T 25T 50T

0% Z 10 ac in WS

10T 25T 50T

$200 / ac IC

15 ac in WS 10T 251 50T

3% Z 5 ac in WS

10T 25T 50T 10acinWS 15acinWS

10T 25T 50T 10T 25T 50T

%Y $ /acft

0 115 76 65 58 39 32 40 27 22 100 57 38 52 30c 19 35 20 13 1 96 60 48 49 31 24 33 21 16 84 43 29 43 22 14 29 16 10 3 61 24 14 31 13b 7 21 9 5 54 18 8 27 9 4 19 7 3 5 36 0 0 18 0 0 12 0 0 24 0 0 12 0 0 8 0 0

a IC is investment cost per acre, Z is the percentage increase in the real price of pumping, WS is the acre inches of water saved per acre, T is the planning horizon in years, and Y is the percentage increase in yield.

bBreak -even water cost for the example farm.

cBreak -even water cost for the example choice between laser leveling to slope and dead leveling.

Table 2: Break -Even Water Costs for Dead Leveling: Different Investment Costs, Fuel Price Changes, Water Savings, Time Horizons, and Crop Yield Benefits; Arizona, 1980/81.a

$100 / ac IC 0%Z 3%Z

10acinWS 20acinWS 30acinWS 10acinWS 20acinWS 30acinWS 10T 25T 50T 10T 25T 50T 10T 25T 50T 10T 25T 50T 10T 25T 50T 10T 25T 50T

%Y $ /acft

0 130 97 89 65 48 44 43 32 30 114 72 53 57 36 26 38 24 18 1 120 89 79 60 44 40 40 30 26 106 65 47 53 32 23 35 22 16 3 103 72 62 52 36 31 34 24 21 91 53 37 46 27 19 30 18 12 5 86 55 46 43 28 23 29 18 15 77 41 28 38 21c 14 24 14 9

10 44 13 4 22 7 2 15 4 1 40 9 2 20 5 1 13 3 1

14 11 0 0 6 0 0 4 0 0 10 0 0 5 0 0 3 0 0

$00 / ac IC 0%Z 3%Z

10 ac in WS 20 ac in WS 30 ac in WS 10 ac in WS 20 ac in WS 30 ac in VVS 10T 25T 50T 10T 25T 50T 10T 25T 50T 10T 25T 50T 10T 25T 50T 10T 25T 50T

%Y $/acft

0 169 120 106 84 60 53 56 40 35 150 89 62 75 44 31 50 30 21 1 160 110 96 80 55 48 53 37 32 142 82 56 70 41 28 47 27 19 3 144 94 79 72 47 40 48 31 26 127 70 47 63 35 24 42 23 16 5 127 78 64 64 39 32 42 26 21 112 58 37 56 29 19 37 19 12

10 85 35 20 43 17b 10 28 12 7 74 25 12 37 13 6 25 8 4 14 52 14 0 26 1 0 17 1 0 46 1 0 23 1 0 15 0 0

aAbbreviations are defined in footnote a in Table 1.

bBreak -even water cost for the example farm.

cBreak -even water cost for the example choice between laser leveling to slope and dead leveling.

6

increase in the real price of fuel, in comparison with a zero percent change, will lower the break -even cost significant- ly if no yield increases are expected. Break -even costs are usually $5 to $25 less with future increases in energy prices.

The planning horizon can have a substantial impact on break -even costs for both planing to slope and dead level- ing. The results indicate that for a relatively short planning period, 10 years, lasering is profitable where water savings are medium to high (10 inches or above for planing to slope and 20 inches or above for dead leveling) or yield increases are moderate or above (three percent for planing to slope and five percent for dead leveling).

Summarizing the data of Tables 1 and 2, two findings stand out. First, the break -even costs for water, even for dead leveling, are often lower than the current cost per acre foot to pump and deliver water on many Arizona farms. Ac- cordingly, laser leveling will often be profitable. Second, the decision to dead level or laser plane to slope depends on the yield benefit and water savings. Laser planing to slope will tend to be more profitable than dead leveling when project- ed water savings and yield benefits are small for both in- vestments. Individual farmers who expect large water sav-

ings or yield benefits from dead leveling, as shown in the earlier example, may find dead leveling more profitable.

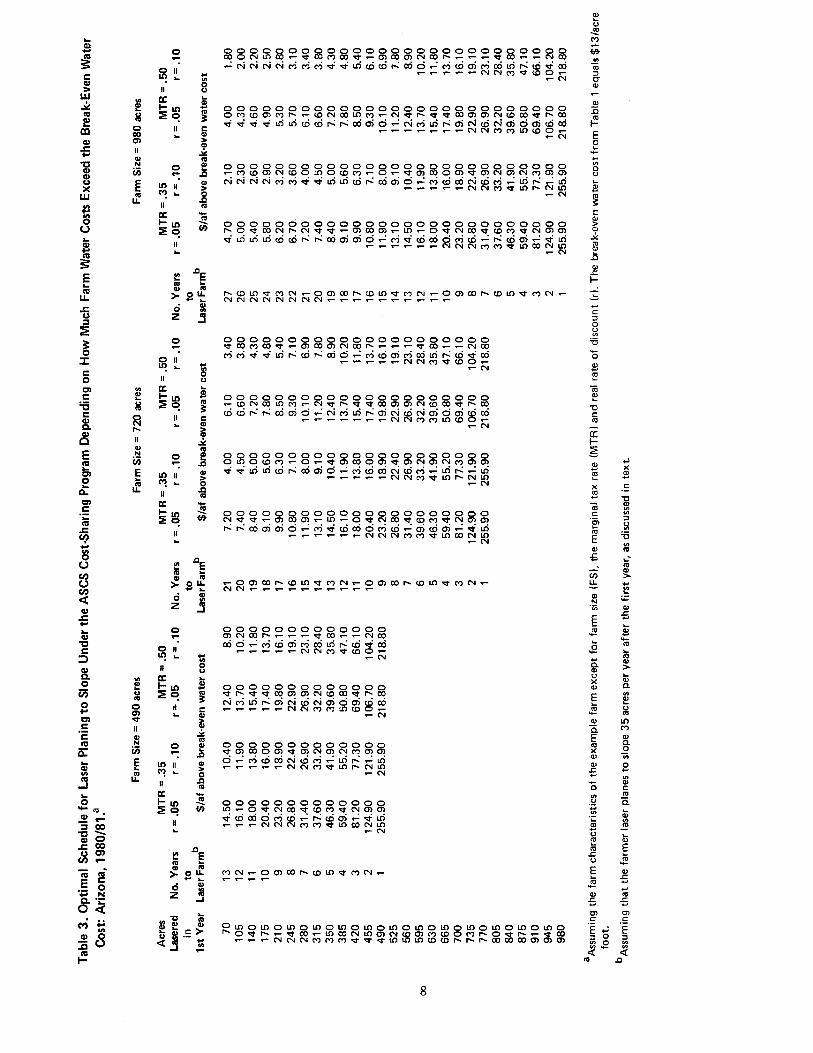

Optimal Acreage to Laser per Year In addition to deciding whether or not to laser, the farm-

er must decide how many acres to laser each year. Since ASCS payments and tax write -offs depend on the number of acres laser leveled per year, the farmer whose water costs exceed the break -even cost must determine an optimal laser leveling schedule. The optimal number of acres to laser each year will depend on whether or not ASCS payments are continued. Although ASCS payments for conservation have been a mainstay of federal farm programs for many years, their continuance is subject to annual congressional appro- priations. Current administration and congressional pres- sures to reduce federal expenditures have increased the un- certainty of many government programs.

Continuing ASCS Payments Assuming that the ASCS cost -share program will con-

tinue, some farms will require ASCS payments if the bene- fits from laser leveling are to outweigh the costs, while the benefits on other farms will outweigh the costs without ASCS payments. Farms which require ASCS payments to make lasering profitable receive the greatest net benefits by annually leveling that number of acres which maximizes their ASCS payments. If the yearly maximum ASCS pay- ment is $3,500, there is a 50 -50 cost -share program, dead leveling costs $600 per acre, and laser planing to slope costs $200 per acre, then the optimal number of acres to dead level each year is:

$3,500 = 12 acres,2 h($600/ac)

while the optimal number of acres lasered to slope each year is:

$3,500 1/2($200 /ac)

- 35 acres.

2For dead level fields the optimal number of lasered acres per year may equal 25, because field size considerations may outweigh economic parameters.

7

For this farm, it is assumed that benefits without the ASCS payments are less than costs. Lasering less than the 12 or 35 acres per year fails to take full advantage of the maxi- mum $3,500 ASCS payment, while lasering more reduces the number of payments.

Some Arizona farmers will find that lasering is profitable even without the ASCS payment. For these farmers, the

optimal sequencing occurs when the present value of future ASCS payments given up by lasering more today equals the net benefit of lasering one more acre. The optimal amount to laser per year will occur somewhere between the number of acres which just exhausts the maximum annual ASCS payment (12 for dead leveling and 35 for laser planing to slope) and the farm size, and depends upon the same

factors which affect the break -even water cost. For illustra- tive purposes, the example farmer would dead level 25 acres per year for 20 years if the farm water cost just equalled the $17 per acre foot break -even water cost, or laser to slope 35 acres per year for 13 years if the farm water cost just equalled the $13 per acre foot break -even water cost. If the farm cost per acre foot exceeds the dead level break - even cost by $5 per acre foot, the farmer should dead level 50 acres in the first year and 25 acres per year for 18 years. Laser scheduling for different tax brackets, discount rates, and farm sizes are shown for laser planing to slope in Table 3 and for dead leveling in Table 4.

In general, the ASCS cost -sharing program slows the rate at which farmers laser level. Without the program, farms having a water cost equal to or greater than the break -even water cost could profitably laser level their whole farm im- mediately. With the program, farmers should save part of the farm for future laser leveling. For example, suppose a farm has water costs equal to $30 per acre foot, a break - even cost of $13 per acre foot, a farm size of 490 acres, a marginal tax rate of .50, a real rate of discount of five per- cent, and other characteristics of the example farm. Actual water costs are $17 per acre foot above the break -even cost. If the farmer is laser planing to slope, Table 3 indicates that between 140 and 175 acres should be planed the first year and that 35 acres per year should be laser planed each year for nine to 10 years thereafter. A faster schedule fails to take full advantage of the ASCS cost -sharing program.

i CO

R

C CD :a w Y co

Y m a)

15 N cd.)

X W

CIS

h 8 V d CO

E co

=L

E C _ O Q) c_

.O

C a A)

CZ

E CO

E

y t1 CD C

,= Co?

,,, ,

V GO

(,) N < t a+

_ co O. O

(03

.2 cm C

ev d se

Ñ .3 i O m

CO

L o 0) V C)

CO v- CC

O ++ N

y Q M H ..CÌ

ÿ . N O Op O II w N Cñ

E . to

LL

1A

E 8

R II

a) N ÿ

CO

LL

w s-

Cr p

m N

CA

m

LL

0 e-

II . ÿ

II CO)

m` I- U) m g O 3

il C m

w O i T. d

U7 ' m

II > M. p

II to

c m F O ` : p

11

b.

ß E

i OLL + .

z Si

o r ly

N ii o CC L 1- ,r¿0

II C m

L d

O 0 I- ß I w

Cl i D II m

CO

r2O V3

II.

L.

o i E d co

} +O+LL

d my

tq Z J p

' IL

ÿ II u cc ,, 1-LO +m+

:E 3

!y m

CO o m e-

.y4

C'; I., Q 11 ß cc w 1.-- 111 4! ,O (ß

H .

w 9E co .- m co i, r i o vmi z 3

CO

d c} Q w

^

O O O O O O O O O O O O O O O O O O O O O O co co O O O CO O N U) CO .- er O M CO er N- O oo O N CO h r- r- r- d co r- )-- N 0 r- NNNN MMMCrCrU)000hcX)O'-MCDOÑÑMCrC0O00

r- N

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 O M co O co h r- Cp N CO LO M N et h Cr Cr co co O N C0 co Cn c co Ct Cr Cr Cr ui LOCDOODOOCVMLOhOÑÑMMU)cDOÑ

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 00 0 0 0 0 0 0 0 0 0 0 rMCDONCDOOOCOM- O.-Cr0 OOCrONONc")OO NNNNMMa CrUiUicÇ)1.c0010.-MGO0OL1fOM LOh l0 NNMCr LOhÑ LD .- N

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 hOCrcONhNerTr.-OCOO.-LOr-OV'NcOTr(DMd'NOO Ni ui ui UicD(OI I`hoOOOOMCtcOcOOML0.-1cD0) V LO NNNMMTrLOccLO N

hCOLOetMN 0000hC0U)CtMNr-0000hCDU)erMNr- N N N N N N N N

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Cr 0 M CO CF r O 0 O N 00 h - a- - Cr o0 -.- N c0 MC'iCf CCL.C)r.:cÓfcOÓr-MCDÓriÓui r-:cÒcÓ NNMV UD

r N

Ooo000000000000000000 .- cONCOLOM Nrrher veD00N00erCheO COOhcoOÓr-NMLOhONÑMC)COCD00

N- CV

00000 0000000000000000 O LC) OCDM r'Or- erOCOOO V ONONMD1O1 CrtOLt7f0h0o00a-MCD00ÑÑM.YIOhNIO

N

Ooo000000000000000oppO Nererr-Oc00)r-LOr-OCtNODetCDCMetNO)O) I1`o000OrMV Cflo00MCDOjCOO Ti ui r- 4-. . r- r- r- N N N M M et LO CO N LO

r- N

ÑÑ00ht0lOCt MN.-00)00hCOLOetMNr-

Ñ O O O CD CD 00 _O r: O Ñ

MOr-MCOOMOLf)hcOC<c0 NNMCrCOO N

0000000000000 et hCrCr0OON0ooenco NMLOiONtON000CCpp0 NNMMLO000.- N

0 0 0 0 0 0 0 0 0 0 0 0 0 V 00000 Ct ONONMOO O r MCOONCDCi ui r: LO NNMU)hÑ

0000000000000 LOrOCrNCOCOMerN00 ¡00OMOr-I:COOi Ni ui N N N M M Cr U) co U) N

MN 00OohCOU)CrMNr-

L.O O LO _O LO co OO O LO O LO O LO O U) O LO O U) O OO O U) _O LO O ó0 et h er0 U)ODNtOONCpOMCOOMhO h 0 r r-r-NNNMMMetCfLOL.c)LO000Dhhh000c00O

c0

M

if).

H

7 6 m

m . N

E

O w ++

° VO

,- ..

d > m Y ÿ .1:-)

m

H

- c = o Ñ =p

Ó .,..

T.

10

O 1cc

CC 1- 2 m

X CO

C 'pl

m E

m .s

_, (n LL

m

ti E

w

w

d v w E

w m Q. E m

axi

y u

= m 15 CO ` s v E 10

w .

C E *' O O ÿ O

@a

+%

w C

13

Ñ CD

=p

Os p

m m >

+

m

co

CO m > et O

;U

co V LO c+)

m tZ

Ñ O

m

M

O. . vmi

m

m

Oo ` .1-

co

+ 1/ CO

H CO c

E O Ñ

..

Tab

le 4

. O

ptim

al S

ched

ule

for

Dea

d Le

velin

g U

nder

the

AS

CS

Cos

t -S

harin

g P

rogr

am D

epen

ding

on

How

Muc

h T

he A

ctua

l F

arm

Wat

er C

ost

Exc

eeds

The

Bre

ak -E

ven

Wat

er C

ost;

Ariz

ona,

198

0/81

Far

m S

ize

= 4

90 a

cres

F

arm

Siz

e =

720

acr

es

Far

m S

ize

= 9

80 a

cres

Acr

es

Lase

red

in

1st

Yea

r

No.

Yea

rs

to

Lase

r F

arm

MT

R =

.35

MT

R =

.50

r =

.05

r =

.10

r =

.05

r =

.10

b $

/af a

bove

bre

ak-e

ven

wat

er c

ost

No.

Yea

rs

to

b La

ser F

arm

=.3

5 M

TR

=.5

0 r =

.05

r =

.10

r =

.05

r =

.10

$ /af

abo

ve b

reak

-eve

n w

ater

cos

t

No.

Yea

rs

to

b La

ser

Far

m b

MT

R =

.35

MT

R =

.50

r =

.05

r =

.10

r =

.05

r =

.10

abov

e br

eak -

even

wat

er c

ost

50

19

5.00

3.

00

4.30

2.

60

29

2.60

1.

00

2.10

.9

0 39

1.

30

.40

1.10

.3

0 10

0 17

5.

90

3.80

5.

00

3.20

27

2.

80

1.26

2.

40

1.10

37

1.

50

.50

1.30

.4

0 15

0 15

7.

10

4.80

6.

00

4.10

25

3.

20

1.60

2.

60

1.30

35

1.

70

.60

1.40

.5

0 20

0 13

8.

70

6.20

7.

40

5.30

23

3.

70

1.90

2.

70

1.60

33

1.

90

.70

1.60

.6

0 25

0 11

10

.80

8.30

9.

20

7.10

21

4.

20

2.40

3.

70

2.00

31

2.

20

.80

1.85

.7

0 30

0 9

13.9

0 11

.30

11.3

0 9.

60

19

5.00

3.

00

4.30

2.

60

29

2.60

1.

00

2.10

.9

0 35

0 7

18.8

0 16

.10

16.1

0 13

.80

17

5.90

3.

80

5.00

3.

20

27

2.80

1.

26

2.40

1.

10

400

5 27

.70

25.1

0 23

.70

21.5

0 15

7.

10

4.80

6.

00

4.10

25

3.

20

1.60

2.

60

1.30

45

0 3

48.6

0 46

.30

41.6

0 40

.00

13

8.70

6.

20

7.40

5.

30

23

3.70

1.

90

2.90

1.

60

500

1 15

3.20

15

3.20

13

1.00

13

1.00

11

10

.80

8.30

9.

20

7.10

21

4.

20

2.40

3.

70

2.00

55

0 9

13.9

0 11

.30

11.3

0 9.

60

19

5.00

3.

00

4.30

2.

60

600

7 18

.80

16.1

0 16

.10

13.8

0 17

5.

90

3.80

5.

00

3.20

65

0 5

27.7

0 25

.10

23.7

0 21

.50

15

7.10

4.

80

6.00

4.

10

700

3 48

.60

46.3

0 41

.60

40.0

0 13

8.

70

6.20

7.

40

5.30

75

0 1

153.

20

153.

20

131.

00

131.

00

11

10.8

0 8.

30

9.20

7.

10

800

9 13

.90

11.3

0 11

.30

9.60

85

0 7

18.8

0 16

.10

16.1

0 13

.80

900

5 27

.70

25.1

0 23

.70

21.5

0 95

0 3

48.6

0 46

.30

41.6

0 40

.00

1000

1

153.

20

153.

20

131.

00

131.

00

a A

ssum

ing

the

farm

cha

ract

eris

tics

for

the

exam

ple

farm

exc

ept

for

FS

, M

TR

and

r

(as

defin

ed i

n T

able

3).

The

bre

ak -e

ven

cost

fro

m T

able

2 e

qual

s $1

7 /a

f.

bAss

umin

g th

at t

he f

arm

er l

aser

lev

els

at l

east

25

acre

s pe

r ye

ar.

In A

rizon

a, f

arm

ers

seld

om l

aser

le

vel

field

s le

ss t

han

25 a

cres

due

to

the

cost

s as

soci

ated

with

sm

alle

r fie

lds.

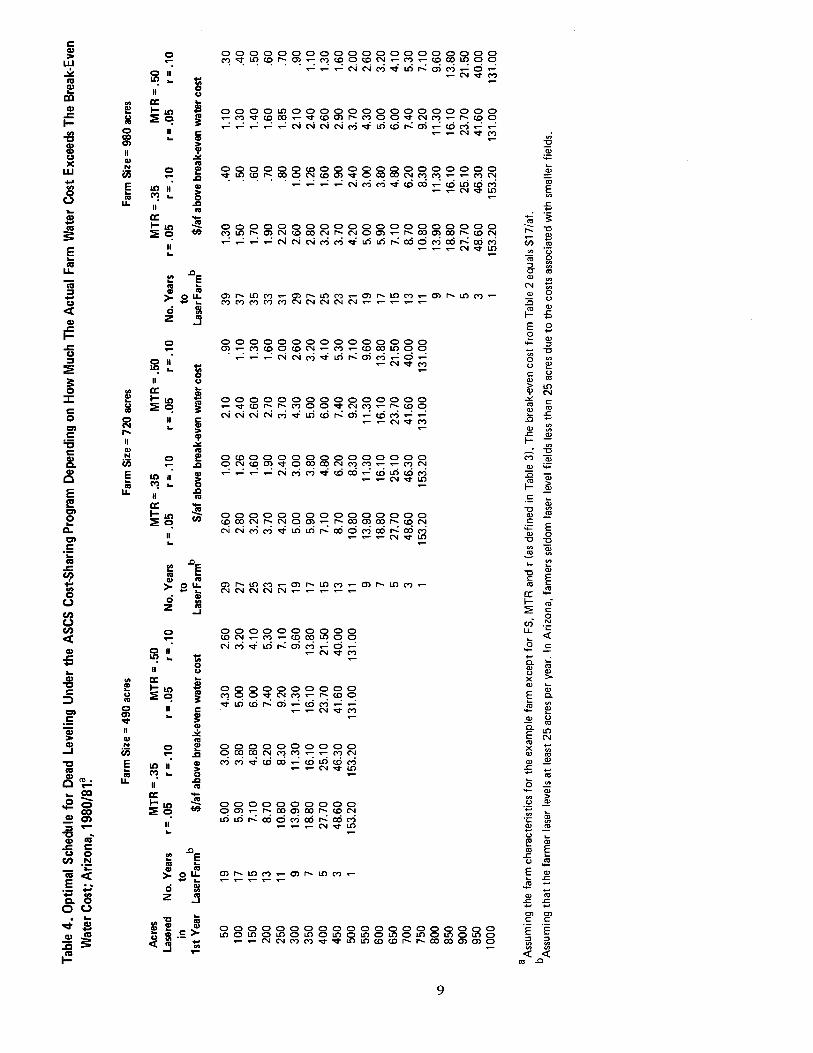

Termination of ASCS Payments The final scheduling decision involves how many acres

per year should be dead leveled if ASCS cost - sharing pro- grams are expected to stop after one year. Without future ASCS payments, the cost of dead leveling additional acre-

age will eventually increase as the tax code forces farmers to spread the deduction from taxable income into future years. For example, the maximum amount a farmer with $700 per acre gross income can deduct in one year is $175 per acre. If investment costs equal $600 per acre the farmer can deduct $175 per acre per year for three years and $75 per acre in the fourth year, while the farmer with $400 per acre investment costs can deduct $175 per acre for two years and $50 per acre in the third year from taxable income. This situation seldom applies to laser planing to slope because of the small initial investment costs relative to the maximum amount a farmer can depreciate under the program.

The optimal number of acres to dead level depends on the farm water cost, investment cost, gross farm income,

farm size, the marginal tax rate, and the real rate of discount (Table 5). For the example 500 -acre farm, the optimal num- ber of acres to dead level each year varies from 145 to 500, depending on how much the farm water costs per acre foot exceed the break -even water cost from Table 2 ($17 per acre foot).

Increases in yield from the assumed 10 percent will

change the break -even water costs, as shown in Table 2, but do not change the numbers of Table 5, which shows the amount above the break -even water cost needed before the farmer should laser more. Different farm sizes or gross farm income will not change the decision rule with respect to the difference between farm water cost and the break -even water cost, but will change the optimal number of acres to laser each year. Different marginal tax or discount rates change the decision rule governing the difference between farm water cost and break -even costs, but not the acres dead leveled each year. Lower or higher investment costs change both the water cost, break -even cost difference and the acres to be dead leveled decision points.

Table 5. Optimal Dead Leveling Schedule Assuming ASCS Payments End After One Year: Arizona, 1980/81.

Parameter Change

Example Farma

Farm Size = 700 ac

Gross Income per Acre = $500 /ac

Marginal Tax Rate = 50%

Real Discount Rate = 10%

Investment Cost = $400 /ac

Farm Water Cost ($ / ac ft) Optimal Acres Lasered (ac / yr)

FWC= 17 b to 17+9 FWC = 17 + 10 to 17 + 19 FWC = 17 + 20 to 17 + 29 FWC= 17 + 30 or greater

FWC = 17 to 17 + 9 FWC= 17+10to 17+19 FWC= 17+20to 17+29 FWC = 17 + 30 or greater

FWC=17to17+9 FWC = 17 + 10 to 17 + 19 FWC = 17 + 20 to 17 + 29 FWC= 17 +30 to 17+39 FWC=17+40to 17+49

FWC= 17 to 17+14 FWC= 17+15to 17+30 FWC= 17+31 to 17+45 FWC = 17 + 46 or greater

FWC= 17 to 17 + 19 FWC = 17 + 20 to 17 + 36 FWC = 17 + 37 to 17 + 52 FWC = 17 + 53 or greater

FWC = 7 to +7 FWC = 7 + 8 to 7 + 13 FWC = 7 + 14 or greater

alnvestment costs are $600 /ac the marginal tax 500 ac, and FWC is farm water cost.

bBreak -even water price from Table 2.

145 290 435 500

204 408 612 700

104 208 312 416 500

145 290 435 500

145 290 435 500

219 438 500

rate is 35 %, the real discount rate is 5 %, gross income is $7001ac farm size is

Conclusions In addition to conserving water, laser leveling either to

slope or dead level is often a profitable investment in Ari- zona, since farm water costs often exceed break -even costs. However, as shown in the analysis, a number of factors sig-

nificantly affect profitability and individual farmers need to

10

check profitability given conditions on their particular farms. Our estimates suggest that laser planing to slope is

probably more profitable than dead leveling when yield and water savings benefits are small for both investments, but that individual farm characteristics, especially the expected

yield increase, may make dead leveling the preferred invest-

ment alternative on some farms. Even in cases where farm-

land goes out of production in 10 years, there are many circumstances when lasering, either to slope or basin level,

is profitable. How fast the farmer lasers also affects the return from

laser leveling. The optimal number of acres to laser per year depends upon yield increases, farm water costs, farm sizes,

investment costs, gross farm income, and the marginal tax rate. Of particular interest is the effect of the ASCS cost - share program. Although the ASCS program makes lasering more profitable, it may slow the pace at which farmers should laser. Since the ASCS program limits the annual pay- ment to an individual farm to $3,500 per year, farmers tak- ing advantage of the program enhance profits by laser level- ing over several rather than a few years.

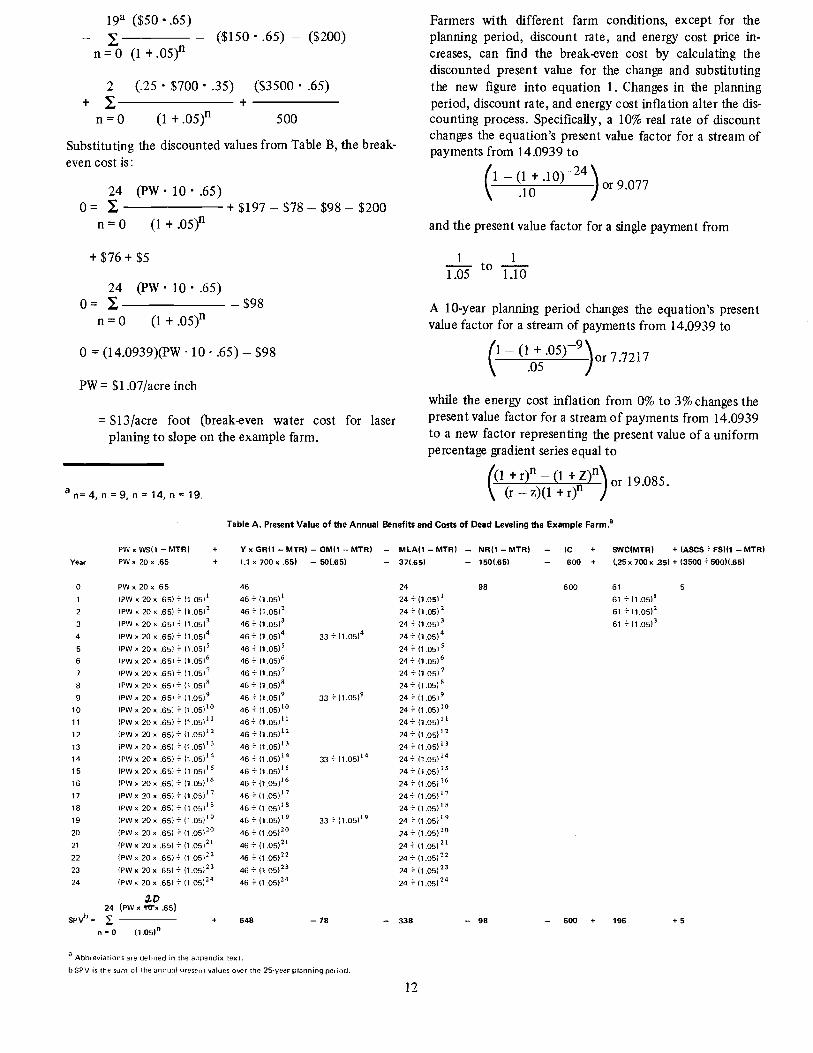

Appendix 1 Calculation of the Break -Even Water Costs

Any water user can estimate break -even water costs for dead leveling or laser planing to slope on a particular farm using equation 1 on page 2. The break -even water cost (PW)

equates the present value of the benefits from laser leveling the whole farm in one year to the present value of the costs. For example, solving equation 1 for PW using the characteristics on the example farm in the text (farm size (FS) = 500 acres, gross farm income (GR) _ $700 /acre, marginal tax rate (MTR) = 35 %, real after tax discount rate (r) = 5 %, net revenue crop loss (NR) _ $150 /acre, dead leveling investment costs (IC) _ $600 /acre, operation and maintenance costs (OM) _ $50 /acre every five years, ASCS payment (ASCS) _ $3,500 /year, water savings (WS) = 20 acre inches /acre, yield increase (Y) = 10 %, time horizon (T) = 25 years,a and additional machine, labor and acreage costs for dead leveling (MLA) _ $37 /acre):

24 0=

n=0

19b

n = 4

(PW 20 .65) 24 (10% $700 .65)

(1 +.05)n

($50 .65)

+

n=0 (1 +.05)"

24 ($37 .65)

(1 + .05)" n = 0 (1 + .05)"

3 (25$700.35) - ($150 .65) - ($600) + E

n = 0 (1 + .05)"

($3,500 .65)

500

Substituting the discounted present values from Table A

into the equation:

+

a This time horizon assumes that the benefits and costs accrue to the farmer at the beginning of each year. While we recognize that in the first year the farmer will probably pay investment costs approx- imately eight months before harvesting the crop, this assumption simplifies the calculations with only an insignificant loss in accuracy.

bn = 4, n = 9, n = 14, and n = 19.

11

24 PW20.65 0 = E + $648 - $78 - $338

n=0 (1 +.05)n

-$98- $600 +$196+ $5.

Simplifying and solving for PW:

0

0

=

=

24 1 (PW 20 .65)

20 .65) - $265

- $265

n=0 (1+.05)"

(14.0939)c (PW

PW = $1.45 /acre inch

= $17 /acre foot (break -even water cost for dead leveling example farm).

To estimate the break -even water cost for laser planing to slope on the example farm, simply substitute the appro- priate lasering costs and benefits into the formula. Laser planing to slope saves less water (10 acre inches /acre), pro- duces smaller yield benefit (3 %), has lower investment cost ($200 /acre), and has no MLA costs. All other farm charac- teristics are the same as in the preceding example. For laser planing to slope, equation (1) is:

24 (PW 10.65) 24 (3%$700.65) 0= +

n = 0 (1 + .05)" n = 0 (1 + .05)"

c 24 1 1 - (1 + .051-24

n 11+.051n .05 - 14.0939

is the discount factor determining the present value of $1 received annually at the end of each year for 25 years, and equals 14.0939. For additional information concerning discounting, present values, and tables of discount factors see Alpin, et. al.

19a ($50 .65) - ($150 .65) - ($200)

n = 0 (1 + .05)n

2 (.25 $700 .35) ($3500 .65) + +

n = 0 (1 + .05)n 500

Substituting the discounted values from Table B, the break - even cost is:

24 (PW 10 .65) 0 = + $197 - $78 - $98 - $200

n = 0 (1 + .05)n

+ $76 + $5

24 (PW 10 .65) 0 = $98

n=0 (1+.05)n

0 = (14.0939)(PW 10 .65) - $98

PW = $1.07 /acre inch

= $13 /acre foot (break .even water cost for laser planing to slope on the example farm.

an= 4, n= 9, n = 14, n = 19.

Farmers with different farm conditions, except for the planning period, discount rate, and energy cost price in- creases, can find the break -even cost by calculating the discounted present value for the change and substituting the new figure into equation 1. Changes in the planning period, discount rate, and energy cost inflation alter the dis- counting process. Specifically, a 10% real rate of discount changes the equation's present value factor for a stream of payments from 14.0939 to

(1 - (1 + .10) -241 or 9.077

.10 J

and the present value factor for a single payment from

1.05 to 1.10

A 10 -year planning period changes the equation's present value factor for a stream of payments from 14.0939 to

(i - (1 + .05) -91 J or 7.7217

.05

while the energy cost inflation from 0% to 3% changes the present value factor for a stream of payments from 14.0939 to a new factor representing the present value of a uniform percentage gradient series equal to

(1 + on - (1 + Z)n or 19.085. r -z(l+r

Table A. Present Value of the Annual Benefits and Costs of Dead Leveling the Example Farm .a

Year

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

PW x WS(1 - MTR) +

PWx20x.65 +

PWx20x.65 (PW x 20 x .65)+11.0511

(PW x 20 % ,65) - (1.05)2

(PW x 20 x .65)+11.05)3

(PW x 20x.651+(1.0514 (PW x 20 x .651+ (1.0515

IPW x 20 x .651+ (1.05)6

(PW x 20 x .65) + (1.05)7

(PW x 20 x .651+ (1.0518

(PW x 20 x .65)+ i1.0519

(PW x 20x.651+(1.05110 (PW x 20 x .65)+(1.051L1

(PW x 20 x .651+ (1.05112

(PW x 20x .651+(1.05113

(PW x 20 x .651+ (1,05114

(PWx20x.651+11.05)15 (PW x 20 x .65) + 11.05)16

IPW x 20 x .651+ (1.05)17

IPWx20x.651-11.05178 (PW x 20 x .651+11.051'9

IPW x 20 x .65) + 11.05)20

(PW x 20 x .651+ (1.05121

(PW x 20 x .65)+ (1.05)22

(PW x 20 x 651+ (1.05)23

(PW x 20 x .65) + (1.05124

Y x GR(1 - MTR) - OM11 - MTR)

1.1 x 700 x .65) - 50(.65)

46

46+ (1.05)1

46 +(1.05)2 46- (1.05)3

46 + (1.05)4 33 -(1.05)4 46- (1.05)5

46 + (1.05)6

46 -(1.05)' 46 + (1.05)8

46 - (1.0519 33 +11.0518

46=(1.05)10 46+(1.05)1' 46 -(1.05)12 46+ (1.05)13

46-(1.05)14 33 =11.051'4 46- 11.05)'5

46 +11.05)16

46+(1.05)17 46=(1.O51'ß 46 + (1.0511 9 33 +11.05)19

46 + (1.05)20

46 +(1.05)21 46 +(1.05)22 46 + (1.05)23

46 -(1.05)24

SPVb=

D 24 (PW x YO`x .65)

E n = 0 (1.051"

+ 648 - 78

a Abbreviations are defined in the appendix text.

b SPV is the sum of the annual present values over the 25 -year planning period.

- MLA(1 - MTR) - NR(1 - MTR) - IC + SWC(MTR) + (ASCS+FS)l1 - MTR)

- 37(95) - 150(95) - 600 + (,25x 700x .35) + (3500+500)(.65)

24

24 +11.0511

24- (1.05)2

24 -(1.0513 24+ (1.05)4

24-(1.05)5 24+11.05)6 24-(1.0517 24 + (1.0518

24+(1.0519 24+11.05110

24+ (1.05)1

24+(1.05)t2 24+(1.0511á

24+ (1.05)14

24+(1.05115

24+11.05)16 24 :- (1.05)12

24+(1.05)78 24+(1.05)19 24+(1.05120 24 + (195)21

24+ (1.05122

24+(1.O5)2á

24 +11.05)24

98 600 61

61 - (1.05)1

61 + (1.0512

61 -(1.05)3

5

- 338 - 98 - 600 + 196 + 5

12

Table B. Present Value of the Annual Benefits and Costs of Laser Planing to Slope on the Example Farm .a

Year

0

1

PW x WS11 - MTR)

PIN x10x.65

PWx10x.65 (PW x 10 x 651+ (1.051'

Y x GR (1 - MTR)

(.03 x 700 x .65) -

14

14 -(1.05)1

- OM11 -MTR) 501.65)

- NR(1 -MTR) - 150(.65)

98

- IC

_ 200

200

+

+

SWC(MTR)

(.25x 700 x 35)

61

16 _ (1.0511

+

+

(ASCS-FS111 -MTR) 13500 _ 500)4.651

5

2 (PW x 10x.65)T(1.0512 14=(1.0512

3 (PW x 10x .65)-(1.051 14-(1.051 4 (PW x 10 x .65) + (1 .050 14 -: (1.050 33+ (1.0514

5 ( P W x 10 x .65) -(1.0515 14 -(1.0515

6 (PIN x 10x.651-11.050 14-(1.051 7 (PW x 10 x .651-(1.05)7 14-11.0517

8 (PW x 10x.651-(1.0518 14-11.05)8 9 (PW x 10x.65)-(1.0519 14-(1.0519 33- (1.0514

10 IPW x 10x.651-(1.05110 14-(1.051° 11 (PW x 10x.65) -(1.05111 14-(1.05111

12 (PW x 10 x .651-(1.05112 14-(1.05)12 13 (PWx10x.65)-(1.05113 14-(1.05113 14 (PWx 10x.651-(1.05114 14-(105)14 33- (1.0514

15 (PW x 10x.651-(1 05115 14-11.05115

16 (PW x 10 x .65) - (1.051'6 14 - (1 .05116

17 (PWx 10x.65) S- (1.05)17 14-11.0517 18 (PW x 10x.651-(1.05)18 14-11.05118 19 (PW x 10x.651-(1.05119 14-(1.05)19 33 -(1.05)4 20 (PW x 10x.65)-(1.05120 14-11.05120

21 (PW x 10x.65)-(1.05)21 14- (1.05(21

22 (PW x 10x.651 - (1.05)22 14=(1.05)22 23 (PWx 10x.651 - (1.05123 14- (1.05)22

24 (PW x 10x.651 - (1.05)24 14- 11.05)24

24 (PW x 10 x .651

SPVb = 197 - 78 - 98 - 200 + 76 + 5

n = 0 (1.051n

a Abbreviations are defined in the appendix text.

b SPV is the sum of the annual present values over the 25 -year planning period,

References Ables, Robert, Soil Conservation Technician, Soil Conservation Ser-

vice, Buckeye, Arizona, personal communication, January 1981. Aplin, R. D., G. L. Carley and C. P. Francis, Capital Investment

Analysis, Grid Publishing, Inc., Columbus, Ohio, 1977. Arizona Groundwater Management Study Commission, "Final

Report" State of Arizona, June 1980. Data Resources, Inc., "U.S. Long -Term Review, Winter 1980 -81,"

1981. Erie, L. J., Orrin F. French and Karl Harris, Consumptive Use of

Water by Crops in Arizona, Technical Bulletin 169, Agricul- tural Experiment Station, University of Arizona, Tucson, Ari- zona, September 1965.

Hathorn, Scott, Jr., "Arizona Pump Water Budgets, Pinal County, 1981," Cooperative Extension Service, The University of Ari- zona, Tucson, Arizona, January 1980.

Hathorn, Scott, Jr., Donald R. Howell and James R. Haylitt, "1980 Arizona Field Crop Budgets, Yuma County," Cooperative Ex- tension Service, The University of Arizona, Tucson, Arizona, January 1980.

13

Hathorn, Scott, Jr., James Little and Sam Stedman, "1980 Arizona Field Crop Budgets, Pinal County," Cooperative Extension Ser- vice, The University of Arizona, Tucson, Arizona, January 1980.

Hathorn, Scott, Jr. and Larry Sullivan, "1980 Arizona Field Crop Budgets, Cochise County," Cooperative Extension Service, The University of Arizona, Tucson, Arizona, January 1980.

Hinz, Walter W. and Allan D. Halderman, "Laser Beam Land Level- ing Costs and Benefits," Bulletin Q114, Cooperative Extension Service, The University of Arizona, Tucson, Arizona, November 1978.

Internal Revenue Service, Farmer's Tax Guide, Publication 225, Revised October 1980.

Pachek, Carl E., Conservation Agronomist, Soil and Water Conserva- tion Service, Phoenix, Arizona, personal communications, March 1981.

Parsons, Walter, Irrigation Water Management Specialist, Soil Conservation Service, Tucson, Arizona, personal communication, January 1981.