1 file · web viewtwinning project fiche. 1. basic information. 1.1. programme: enpi ap 2008 1.2....

TRANSCRIPT

TWINNING PROJECT FICHE

1. Basic Information

1.1. Programme: ENPI AP 2008

1.2. Twinning Number: MD10/ENP-PCA/FI/07

1.3. Title:Strengthening Public Financial Management in the Republic of Moldova

1.4. Sector: DAC 15111 – Public Finance Management

1.5. Beneficiary country: Republic of Moldova

2. Objectives

2.1. Overall ObjectiveTo improve the management of public financial control in the Republic of Moldova in line with internationally recognized standards and European best practices.

2.2. Project purposeTo support the Ministry of Finance to improve the Public Internal Financial Controls.

2.3. Contribution to the EU - Moldova Action PlanThe EU-Moldova ENP Action Plan is a political document laying out the strategic objectives of the cooperation between Moldova and the EU. Its implementation will help fulfil the provisions in the Partnership and Cooperation Agreement and will encourage and support the further integration of Moldova into European economic and social structures.

The ENP Action Plan identifies priority areas for cooperation on financial control and related matters. Among others, it aims to promote sound management and control of public finance, including development of a strategy and policy paper for public internal financial control system, establishment of a legislative framework and gradual harmonization with the internationally agreed standards and EU best practices for the control and audit of public income, expenditure, assets and liabilities. External audit is another area for cooperation under the ENP AP, to ensure the establishment and adequate functioning of an independent Supreme Audit Institution in line with the internationally accepted and EU best practice external audit standards (INTOSAI standards – International Organization of Supreme Audit Institutions).”The EU Moldova action plan recognises that there is a need for gradual harmonisation with international standards when implementing PIFC. The activities in the twinning proposal are a logical extension of this gradual implementation as noted in the background and justification for the project below.

3. Description

3.1. Background and justification:

The traditional system of Financial Management; changes required and being implemented under PIFC and related activities. The traditional system of Financial Control

The following paragraphs describe the traditional financial control system in Moldova against which the PIFC model of financial control is being introduced as part of Public Financial Management Programme. Traditionally in the Republic of Moldova the role and functions of public sector managers have been defined in terms of the obligations of officials to implement activities in accordance with the established legal framework (this includes the laws established by Parliament and the regulations issued by the Government as a whole and by each ministry).

1

In the area of financial control, the ex-ante checks that an official is required to make before passing expenditure for payment or processing the receipt of funds were explicitly defined and regulated in law. The system then required ex post controls – an independent assessment of whether managers have applied the law correctly. This was done through a programme of external control (known as financial revision) undertaken by financial controllers reporting to an independent central unit (FCRS) or by controllers at the Court of Accounts. Under this system financial controllers have powers to impose penalties and sanctions on officials that have not administered activities in accordance with the law. The financial controllers, however, are not required to consider the economy, efficiency and effectiveness of the way the law has been applied.

Financial revision work is undertaken cyclically at all public entities in Moldova from central Ministries and Agencies receiving financing directly from the state budget, to lower level entities operating by the State and by Local Administrations. External Control/ Financial Revision work was until very recently undertaken by three institutions – the Court of Accounts (the public authority of the State that controls the formation, management and use of the public financial resources and management of public property); the Financial Control and Revision Service of the Ministry of Finance – the state control body which, within the scope of its competence, controls the economic and financial activity of institutions, enterprises and organizations (regardless of their form of property and type of activity) which use resources from the national public budget; and the Centre for Combating Economic Crime and Corruption, which, under certain circumstances, is empowered to carry of financial revisions.

In general the Court of Accounts has been responsible for external control work at first level budget holders (Ministries and Agencies) and the FCRS has been responsible for external control of all third level entities (local authorities). The control of budget entities at the second level (de-concentrated ministry departments operating locally and subordinate agencies) has been shared between the two institutions through a coordination of work plans. In the traditional system therefore, the responsibility for internal control was split between managers who process budgetary disbursements and receipts and financial controllers who check ex-post that these actions have complied with the law.

The main changes by implementing PIFCThe fundamental change, promoted by PIFC, is that managers will in future have the responsibility for all aspects of internal control (both ex ante and ex post) and are to be held accountable for the manner in which the FMC system operates in the delivery of effective public services. Internal audit units, reporting to the head of a public entity will be responsible for evaluating the effectiveness of the FMC system, but the responsibility for its implementation will remain with the management of the entity.

PIFC requires: The development of new procedures for Financial and Managerial Control (FMC) reflecting the

principle of accountability;

The creation of a new function of internal audit operating in a decentralised manner.

Creation of a system where the process of change and the implementation of new systems are overseen (or harmonised) through a central unit or units – a Central Harmonisation Unit.

The principles underlying PIFC reflect current best practice in public administration. A key feature of modern public management systems is that these are much more complex than in the past. Consequently, the responsibilities of public sector managers need to be defined in terms of the explicit goals/objectives of the policies that they are expected to implement, rather than a narrow definition of the laws that public sector managers are required to implement. In effect, managers are expected to address the economy, efficiency and effectiveness of their activities as well as ensuring legal compliance. And this cannot be done unless clear objectives are established at all levels of public administration.

Under PIFC, Managers will be given greater freedom and flexibility in the way they implement their objectives. But this managerial freedom must be balanced by the notion of accountability - that managers are held to account for the achievement of objectives (and not only for the compliance with the legal framework).

2

Progress in implementing PIFC In January 2008 the Government approved a strategy for the development of PIFC which was subsequently replaced by a new Strategy as approved by the Government on the 2nd of July 2010. The PIFC strategy has been progressively implemented in the following way1:

The legal basis for the implementation of PIFC has been established through an amendment to the Budget System and Budget Process Law (law no 172/XVI, 10 July 2008) and the law on local public administration (436/XVI, 28 December 2006). See annex 4.

A Central Harmonisation Unit (CHU) has been created. The unit began work as part of the FCRS and was subsequently transferred to the Ministry of Finance. The unit reports directly to one of the Vice-Ministers. The CHU is responsible for both FMC and Internal Audit and has a staff of 5 people against a complement of 7 posts.

The regulatory and normative framework for internal audit has been created through the adoption of National Internal Audit Standards, Code of Ethics and Audit Charter in December 2007 and the development, pilot testing and promulgation of the Methodological Norms for Internal Audit Implementation in the Public Sector, governing the implementation of internal audit in the Republic of Moldova (December 2008).

The regulatory and normative framework for FMC has been developed through the adoption a full set of Internal Control standards in June 2009 and the development of an FMC toolkit of guidance for implementation. The toolkit covers: general guidance on FMC, the general control environment setting objectives, identification and mapping of business processes; risk management, control activities. Certain sections of the FMC Toolkit are in the process of finalisation as at 2010.

As of April 2010, 33 internal audit units have been created. However, 10 of these units exist in name only and have no staff assigned; 6 units have staff but are still in the process of establishing the IA function; and 8 of the internal audit units that have been staffed have been assessed by the CHU as carrying out financial revision. In total therefore there are only 9 units which have been staffed and are carrying out internal audit work. There is therefore still a considerable distance to travel before Internal Audit units are fully effective.

The CHU has developed a detailed training strategy for PIFC. The strategy proposes a modular scheme for certification and training for internal auditors and financial controllers and the development of training modules in close collaboration with the Academy of Economic Studies and the Academy of Public Administration. The CHU will require additional staff to oversee the strategy effectively.

Various formal and on the job training has been carried out.

The CHU have also developed in liaison with the contractor responsible for component 3 of the PFMP on the development one-week training courses in FMC and Internal Audit. This has included a train the trainers course.

A draft PIFC law has been developed for presentation to the Parliament (May 2010)

A PIFC development strategy for the period 2010-2013 has been circulated to all relevant central agencies for comments and review in advance of submission to Government in April 2010. The strategy proposes the further pilot implementation of FMC in central and local public administrations and structured support to internal audit units.

In summary, by the middle of 2010, the MOF will have established and promulgated the legal and regulatory framework for the implementation of PIFC across Moldova. In addition there will be an agreed training strategy to support PIFC implementation and developed training courses and supporting material in the main areas of training required. The challenge from 2010 onwards is to develop a programme of support linked to the planned transformation of organisational structures and functions (internal audit and FMC) required to implement the PIFC concept in full.

1 Situation as per July – August 2010.

3

3.2. Linked activities

Three related development activities are relevant to this twinning proposal: Public Financial Management Project

Capacity Building at the Court of Accounts

Public Administration Reform.

Support to the implementation of PIFC as part of the Public Financial Management Project. The Ministry of Finance has received support for the implementation of PIFC since August 2007 through a technical assistance project Public Financial Management Project supported through a World Bank Trust Fund.

The four components of the PFMP are: Component 1 Budget Planning and Execution System deals with budget planning and system

execution by improving medium term expenditure policies, modernizing budget classification and introducing a single chart of accounts for public sector as well as by implementing an integrated Financial Management Information System.

Component 2 Internal Control and Audit deals with the development of an internal control and audit system within government in accordance with the best international practices and standards.

The internal control and audit component has three sub-components: 2A Establishing the normative and legal framework for Internal Control and Audit

2B Transformation of Financial (compliance) control into internal audit;

2C Expanding the Internal Audit system to Line Ministries and Selected Sub-national Entities.

Component 3 Training Capacity in Financial Management and Training deals with the institutionalisation of training capacity, developing and training public servants in 18 modules related to Financial management.

Component 4 Project management monitoring and evaluation.

The timescale for implementation of the project’s results was three years and support was provided through short-term inputs of international experts. The consultants involved consistently questioned the ambitious timescale for the full transformation bearing in mind the lack of a long-term technical advisor. Reasonable progress has been achieved on component 2A during the course of the project in establishing the legal and regulatory framework for internal control and internal audit; in pilot testing audit and financial control methodologies; and in developing a forward training strategy. However the ambitious plans for full transformation of financial control to internal audit and expansion of internal audit to selected line ministries and selected sub-national entities under components 2B and 2C have not been achieved.

The ministry of Finance has agreed an extension of the existing technical assistance project to provide further training and support to PIFC over the period June 2010 – June 2011. This will include a range of further training and support activities in the area of FMC and Internal Audit.

Capacity Building at the Court of AccountsThe Court of Accounts is benefiting from a range of technical support provided (a) through a World Bank Multi Donor Trust Fund and (b) through a bilateral support from the Swedish National Audit Office. This technical assistance is helping the Court to implement a five year development strategy to transform the Court from an External Financial Control institution to and External Audit institution. The four pillars of the strategy concern: institutional strengthening - including the development of a new legal framework; investment in audit related information technology and the establishment of better business

4

management processes; Profession building – developing, pilot testing and implementing a new methodological framework for external audit involving financial IT and performance audits; Developing People – introducing a range of new people management practices designed to recruit retain and motivate and audit workforce; and securing greater impact from its work – focusing on increasing the effectiveness of the Court’s relationships with Parliament, clients and the media.

As defined by the European Union, PIFC does not concern the activities of the external auditor of the state budget, even though external audit is a key feature of public financial management. Nevertheless it is important for the CHU to be aware of the developments in external audit and how changes in audit practices (in particular the move away from External Financial Control to External Audit) impact the control environment. During the course of the PFMP project the CHU has maintained close working relations with the COA and this has resulted for example in the sharing of audit methodologies and the realisation of shared training opportunities, particularly in relation to performance audit.

Public Administration Reform project

FMC is to be implemented in line with international standards for internal control, (namely the standards promoted through the COSO model) which takes a holistic view of the internal control system. Certain internal control standards relate to the promotion of the internal (control) environment – the tone at the top; as well the development of Human Resource policies and practices that ensure the recruitment and retention of suitably qualified staff. The standards also promote the need for staff to be competent to undertake control related activities.

With support from a Public Administration Reform project funded by a World Bank Multi Donor Trust Fund, the Government is also implementing a major programme of public sector reform. Two areas of this reform programme are directly relevant to FMC.

The development and implementation of a process of strategic planning across central public authorities. As part of this process the central public authorities have developed Institutional Development Plans, which for the first time provide a clear statement of their strategic and lower level objectives. One of the key principles of FMC is the need for public entities to develop clear strategic and operational objectives.

The development of a new Law on Civil Service which promotes the introduction of modern human resource management practices in all public authorities. A key feature of FMC is for managers to ensure the appointment of competent staff to undertake control activities. Managers also need to promote a culture of continuous professional development of staff. The CHU is working closely with the Public Administration Reform and PFM Projects. The forward work programme of the CHU identifies related developments in Public Sector reform and the need to maintain suitable contacts with the entities responsible for this programme of change.

3.3. Results

The mandatory results to be achieved by the project are:1. Enhanced capacity of the Central Harmonisation Unit to oversee the implementation of PIFC in

Moldova. 2. Legislative and normative framework updated. 3. Financial and Managerial (FMC) control strengthened. 4. Internal Audit Strengthened.

3.4. Activities (indicative)

Note: All activities are indicative and can be amended during the contract preparation based on the proposal made by the twinning partner.

Component 0 - General (indicative) In addition to the activities related to the four components (mandatory results), the project will also carry out the following:

5

0.1 Kick off meeting The first month of the project will be used to allow the installation of the Resident Twinning Advisor (RTA) in the Republic of Moldova. The RTA will have to be installed in his/her office within the beneficiary. She/he will be introduced to the BC stakeholders of the project and to his counterparts and staff. She/he will also hire an Assistant through an appropriate selection procedure.

A one-day kick-off meeting will be organized in the first month aiming at launching and presenting the project to the stakeholders, the media and the public at large. In order to guarantee large public information about the start of the project, the meeting will be concluded with a press conference and a press release.

Benchmarks: Stakeholders, media and public informed about the start and content of the project by start of Month 2.Resources: RTA, PL, translation, rent of premises.

0.2 Monthly MeetingsMonthly meetings will be held to discuss project progress and to solve any emerging problems. Monthly meetings will be attended by the RTA, representatives of the beneficiary institution, and as appropriate by the PAO / NCU and the EU Delegation.

0.3 Steering Committee MeetingsRegular steering Committee meetings to promote effective management and monitoring of project activities the Steering Committee (composition detailed under 6.3) will meet at least once every three months (first in month 3). Progress in the areas of the project’s interventions will be discussed with the beneficiary and the members of the Steering Committee.

0.4 Closing ConferenceA closing conference (wrap up meeting) will be held during the last two months of the project at which the results and impact of the project will be presented. The Conference will present recommendations for possible follow-up and lessons learned for similar projects to the beneficiary, the Moldovan Government, the civil society and other donors.

Benchmarks: Closing conference organized, recommendations and lessons learned formulated and discussed. Stakeholders, media and public informed about the results of the project at its end.

Resources: RTA, PL, translation, rent of premises.

Component 1 – Enhanced capacity of the Central Harmonisation Unit to oversee the implementation of PIFC in Moldova.

1.1 Establishment of and support to PIFC CouncilThis activity will assist the CHU to establish an effective PIFC Council, which addresses key strategic issues having impact on the implementation of PIFC. The draft PIFC Law envisages the creation of a new PIFC Council. The creation of a new cross-government entity to oversee the implementation of PIFC is a key step in the programme to both increase awareness and foster effective implementation across all the entities concerned. This activity covers both advice and guidance on the establishment of the Council and support to the CHU at the proposed meetings (minimum of one every six months) when the PIFC Council is establishing itself and its practical role. The practical experience of such consultative bodies in EU member states will be crucial in ensuring that the Council addresses issues at the right strategic level. The twinning partners will also consider how working level forums for Heads of Internal Audit and FMC champions should be integrated within the work of the PIFC Council.

Benchmark: PIFC Council established and operational.Resources: RTA, Short term experts and translation as appropriate.

6

1.2 Review of progress on PIFC strategy implementationUnder this activity the twinning partners will regularly review progress in implementing the present PIFC strategy, preparing as necessary modifications to forward plans for consideration and endorsement by the Steering Committee.

The PIFC strategy should be a living document because views of PIFC implementation will change over time. The expectation is that future plans as contained in the strategy will need to be kept under constant review and changed in the light of implementation experience.

Benchmark: PIFC Strategy implementation enhanced.Resources: RTA, Short term experts and translation as appropriate.

1.3 Preparation of an updated strategy for PIFC for the period 2013- 2016Under this activity the twinning partners will develop a new strategy for the future implementation of PIFC in the period 2013-2016. The strategy will incorporate the lessons drawn from the review of the earlier strategies and reflect new views on the development. A realistic timeframe for implementing PIFC is 7-10 years. There will therefore need to be a detailed plan for further implementation activity in the period 2013-2016.

Benchmark: PIFC Strategy for 2013-2016 prepared.Resources: RTA, Short term experts and translation as appropriate.

1.4. Develop a communication strategy to support the implementation of PIFC in Moldova.A strategy for the communication will be developed in order to support the implementation of PIFC. The strategy will outline what and how will be communicated to ensure that information is available to all involved in PIFC and Internal Audit. The strategy will ensure that information is consistently transmitted across the organisation and where appropriate outside.

As part of this activity, the twinning partners will consider the scope for enhancing the current web site to make the information more readily available to the target group. The partners will consider what information should be presented and in what format to increase transparency of the work of the CHU and the subjects that it is covering. The site should become the main legal and procedural repository for the country on the subject of PIFC and Internal Audit activities, which are both in the remit of the CHU.

Benchmark: Communication Strategy prepared and enhanced website design prepared.Resources: RTA, Short term experts and translation as appropriate.

Component 2 - Legislative and normative framework updated.

2.1. Review of the legal and regulatory framework for PIFCIn the course of this activity, a review of the legal and regulatory framework for PIFC will be carried out, in the light of the developments on EU best practices since the laws and regulations were adopted and development of proposals for changes in the legal and regulatory framework. Although no changes are envisaged at this stage, the activity makes provision for further (and probably minor) changes as considered necessary. The legal and regulatory framework is considered sufficient to implement PIFC. However, views both inside and outside the European Union on the best way forward are constantly evolving.Benchmark: Updated legal framework for PIFC, as appropriate.Resources: RTA, Short term experts and translation as appropriate.

2.2 Review of the “Methodological Norm” for FMC

7

Under this activity a review of the Operational Manual for FMC in the light of pilot activities will be undertaken and a revision of FMC standards and FMC toolkit will be carried out, as necessary. By the time this project starts, there will be significant experience based on the earlier pilot activities (undertaken by the PFMR project) in implementation of FMC. This experience will require further development of the legal framework and update of the “Methodological Norm” (manual), taking into consideration the experience of Moldova and other countries.

Benchmark: Updated FMC Manual and FMC toolkit. Resources: RTA, Short term experts and translation as appropriate.

2.3. Review of the operational manual for Internal Audit

The CHU has already developed and published a set of 18 methodological norms governing the application of internal audit standards in Moldova. In total the norms provide a range of guidance and advice for internal auditors (i.e. an audit manual) covering all the basic audit tasks. By design three advanced methodological norms concerning the audit of IT systems, sampling techniques and the role of the auditor in relation to fraud and corruption have yet to be produced and will be developed as part of activities 2.3 to 2.5.Benchmark: Operational Manual for Internal Audit developed Resources: RTA, Short term experts and translation as appropriate.

2.4. Develop a new methodological norm (guide) for IT systems audit. Under this activity, an additional methodological norm will be prepared to provide guidance for the audit of IT systems in order to establish their integrity. The methodological norm will cover all aspects of the audit of IT systems including the audit of both installation and application controls; advice on compliance testing of IT system controls; and the provision of detailed advice checklists for use by auditors who may be unfamiliar with controls in an IT environment

Benchmark: Methodological norm on IT systems audit issued.Resources: RTA, Short term experts and translation as appropriate.

2.5. Develop a new methodological norm (guide) on sampling techniques.

Under this activity, an additional methodological norm will be prepared to provide guidance for sampling techniques in order to facilitate the efficiency and effectiveness of audits by choosing the rights sampling method for the compliance or substantive test concerned. The methodological norm will cover: the situations where auditors need to sample test transactions; the benefits and drawbacks of judgement sampling, random sampling and statistical sampling; the basis theory underlying statistical sampling in audit environments (low and high error states, confidence levels, etc); practical advice on simple random sampling; and present suggested methods for Statistical Sampling (e.g. Monetary Unit Sampling, multi-location sampling).

Benchmark: Methodological norm on sampling techniques issued.Resources: RTA, Short term experts and translation as appropriate.

2.6. Develop a new methodological norm (Guide) about the role of the auditor in relation to fraud and corruption

Under this activity, an additional methodological norm will be prepared to provide guidance related to the role of the auditors in fraud detection and subsequent action to be taken. The methodological norm will cover the definition of fraud and corruption, the role and responsibilities of auditors in relation to fraud and corruption, the relationship with other entities responsible for investigating fraud and corruption, practical

8

guidance on the areas that are susceptible to fraud and corruption including checklist on red flag issues that are indicative of the risk of fraud and corruption.

Benchmark: Methodological norm on the role of auditors in fraud and corruption issued.Resources: RTA, Short term experts and translation as appropriate.

Component 3 - Financial and Managerial (FMC) control strengthened3.1 Review of FMC and Audit training and Training Needs Analysis (TNA).

A review of the effectiveness of training on the application of internal control standards and the FMC toolkit will be undertaken and proposals will be put forward for change as appropriate. As there is a close linkage between the FMC and Audit trainings, the review must take place in one exercise. Under this activity the twinning partners will review the effectiveness of training thus far provided with the aim of identifying any key critical gaps in training activities that could be addressed. In addition, there will be a TNA under this component that will identify needs that are currently not addressed in the training programme and therefore would not be identified by a training review.

Benchmark: Report on Training effectiveness and TNA. Resources: RTA, Short term experts and translation as appropriate.

3.2 Development of training materials related to FMC.

This activity will develop case study material for use in training activities using local Moldovan examples. The case studies should encompass: risk management; the documentation of systems and processes; defining objectives; and the range of control activities and their strengths and weaknesses.A constant request from staff attending training is that they can be provided with examples and case studies showing the application of key principles in a Moldovan context. Under this activity the twinning partners will develop a range of examples and exercises across the spectrum of FMC activity. The case study material will then be made available to both local trainers and STEs for use in training and pilot work as appropriate. Case study material, should encompass: (i) a bank of simple examples and (ii) more complex worked through exercises in the areas of: identifying processes; formulating objectives; identifying and documenting systems and processes; control activities; and risk management. The preparation of case study material will substantially enhance the effectiveness of the (mainly) lecture-based training already provided. Such material will also provide visiting experts with useful supporting material for use in on-the-job support of pilot implementation of FMC in selected entities.

Benchmark: Training materials including case studies prepared and ready for use.Resources: RTA, Short term experts and translation as appropriate.

3.3 Training of Trainers in new issues related to FMC

This activity will provide Training of Trainers on Financial Management Control to plug gaps in current training programmes or emerging issues as identified by the TNA. It is expected that the trainers employed by the Ministry of Finance will provide training to those who need it after they are trained in the particular subjects by the short-term experts. The subjects will be determined on the basis of the training review and the TNA. Benchmark: Trainers trained on FMC issues.Resources: RTA, Short term experts and translation as appropriate.

3.4 Pilot implementation of FMC at Central Level.

Under this activity the twinning partners will provide technical support to the pilot implementation of FMC

9

in two Central Public Administration Authorities (CPAAs). The Ministries/Agencies to be included in the pilots will be selected as part of the detailed work planning for the twinning project.

Work under the PFMP project has demonstrated the benefit of working closely with public entities who have the leadership, drive and desire to make a success of piloting FMC in advance of the wider implementation. For example, pilot implementation in the National Social Insurance House has been commended internationally as an example of the implementation of stronger financial management in a social insurance entity. Such pilot work will increase the CHU’s understanding of the obstacles to full implementation and generate FMC champions who can be used to great effect in the wider implementation of FMC expected in the second half of the twinning project.

Benchmarks: Analytical reports on the pilot implementation. Resources: RTA, Short term experts and translation as appropriate.

3.5 Pilot implementation of FMC at local authorities.

Under this activity two FMC pilots will be undertaken at two 2nd level local authorities (one municipality and one Rayon) to provide the CHU with a full understanding of what issues may arise at the local level. The challenges facing local public administrative authorities at the second level in the implementation of FMC may be different from those of CPAAs. This needs to be determined through pilot implementation.

Benchmark: Analytical reports on the pilot implementation. Resources: RTA, Short term experts and translation as appropriate.

3.6 Study tour related to FMCA study tour for 5 persons for 5 days (and interpreter) will be organised to an EU member state to study the implementation of Financial Management Controls in the member state. The study tour is to provide an opportunity for the participants involved in the current and previous pilot FMC activities to expand their knowledge of FMC by seeing the manner in which control systems help line ministries to deliver on their policy objectives. Benchmark: Study tour implemented. Resources: Tickets, per diem and translation as necessary.

3.7 Proposals for the monitoring of FMC implementation.

Under this activity the twinning partners will develop practical proposals as to how in the future the CHU will monitor the implementation of FMC across a number of different entities. One of the key roles of the CHU is to develop appropriate mechanisms and related performance indicators that will help it monitor the implementation of FMC across a number of government entities. The focus of CHU activities to date on FMC has inevitably been on the development of FMC methods and guidance but at some point it needs to consider how the impact will be measured in practice. Having prepared fully worked out monitoring proposals at the beginning of wider implementation will significantly strengthen the capacity of the CHU to oversee full implementation.

Benchmark: Proposal for a monitoring plan and methodology. Resources: RTA, Short term experts and translation as appropriate.

Component 4: Internal Audit Capacity Strengthened

4.1. Review of CHU monitoring arrangements

Under this activity the twinning partners will review the CHU monitoring arrangements for Internal Audit activities and develop proposals for improving monitoring and annual reporting arrangements, including specific advice on how CHU should evaluate the effectiveness of IA units. The CHU produced its first report

1

on progress in implementing internal audit in Moldova in April 2010. This was based mainly on the results of a questionnaire sent to all internal audit units though this does not seem to be the most appropriate methodology.

Benchmarks: Review report containing recommendations for improvement prepared. Resources: RTA, Short term experts and translation as appropriate.

4.2. Study tour for CHU staff to learn about internal audit

The study tour for 5 CHU staff for 5 days (+ interpreter) will examine in particular the process for developing guidance and monitoring implementation of internal audit work. None of the members of the CHU have had the opportunity to see at first hand a fully functioning central harmonisation unit. Inputs from international consultants can provide some of the needed techniques. But the opportunity to question first hand direct counterparts is now considered essential after more than 3 years of the development of this function in Moldova. As many member states have separate CHUs for FMC and Internal Audit this particular study tour will focus on an IA unit

Benchmark: Study tour implemented. Resources: RTA, Short term experts and translation as appropriate.

4.3. Develop options for certification of internal auditors

Under this activity the twinning partners will further develop policy options for a common certification process for public sector internal auditors in Moldova contained in the training strategy. The proposals should include a detailed cost-benefit analysis of any certification scheme recommended for implementation.The PIFC development strategy (and draft PIFC law) envisages the development of a new process of certification of internal audit staff. There are many options open to the CHU as to how to implement such a process and these are explored in the Training Strategy. Moreover some of these options, e.g. certification linked to some form of independent external assessment have clear costs attached to them.

Benchmark: Proposals for certification prepared and delivered to Government for further consideration.Resources: RTA, Short term experts and translation as appropriate.

4.4. Develop a programme of continuing professional education of internal auditors

Under this activity the twinning partners will develop an annual programme of continuing professional education of internal auditors that will include the delivery of a series of seminars and workshops on technical issues of relevance to internal audit staff.

Internal audit is a professional activity, which requires audit staff to maintain an up to date knowledge of developments in the profession. Although IA activity in Moldova has yet to become fully professional it is important that newly trained IA staff recognise the need for continuous professional education and take part in relevant refresher training and professional updates as appropriate. The programme will build on the earlier developed programme for initial certification, the TNA and be taken into account when developing the training material.

Benchmark: Programme for continuous education prepared and promoted. Resources: RTA, Short term experts and translation as appropriate.

4.5 Develop training material for internal audit training

This activity is expected to develop training material for the internal audit training and where appropriate the continued professional education. The training material will be based on the findings of the training review and the TNA and take the need for continued professional education into account. In addition to the material identified in the TNA and review, case study material should be prepared. The case study should encompass Planning the internal audit activity (strategic and annual work plans), planning IA missions, fieldwork, reporting and follow-up.

11

The intention is that the case study material is based on real examples but designed in such a way that model answers to exercises are used in later stages of training on the audit process so that participants understand the relationship between different elements of the process.

Benchmark: Training material prepared.Resources: RTA, Short term experts and translation as appropriate.

4.6. Delivery of Training of Trainers related to Internal Audit

Under this activity, Training of Trainers on Internal Audit will be carried out to plug gaps in current training programmes or emerging issues as identified by the TNA. It is expected that the trainers employed by the Ministry of Finance will provide training to those who need it after they are trained in the particular subjects by the short-term experts. The subjects will be determined on the basis of the training review and the TNA.

Benchmark: Trainers trained.Resources: RTA, Short term experts and translation as appropriate.

4.7. Preparation of internal audit strategy and work planning.

A key feature of modern internal audit is the development of a multi-annual and risk-based strategy for the IA unit, which is then used to prepare annual work plans. The activity will be an on the job training for the preparation of the audit plan based on the risk based strategy, this work plan will determine which entities will be audited in the pilot audits.

Benchmark: Internal Audit Strategy and Action Plan prepared. Resources: RTA, Short term experts and translation as appropriate.

4.8. On the job training by means of pilot audits

Under this activity the twinning partners will work with a minimum of eight internal audit units that has either been newly created or where “nominal” units created in the past but with no staff and now have new internal audit staff. For each unit the project will provide technical support to a minimum of one internal audit mission. (In one audit, the manual on IT audit will be tested). This activity builds on the experience of the PFMP, where pilot internal audits have proved to be a very successful means of on-the-job training for staff new to internal audit.

Benchmark: 8 pilot audits implemented and audit reports prepared. Resources: RTA, Short term experts and translation as appropriate.

4.9. Study tours for public sector internal auditors

Under this activity, two study tours will be conducted for 5 public sector internal auditors for 5 days, accompanied by an interpreter, focusing on strategic planning of audit work and the conduct of audit missions. The study tours will be staged, one in year 1 of the project and a second in year 2.

Internal Audit is a completely new activity in Moldova. It can thus be difficult for newly appointed heads of internal audit units to understand how their role and functions should evolve. The study tours will focus on strategic planning of internal audit work and the conduct of audit missions, providing the head and key staff of each IA unit undertaking pilot audits under activity 4.8 with an opportunity to see how an effective internal audit unit delivers results of benefit to senior managers. One member of the CHU will accompany the study tour participants to ensure that wider lessons from the study tour are disseminated to others.

Benchmark: Two study tours implemented. Resources: RTA, Short term experts and translation as appropriate.

1

3.5. Means\input from the MS Partner Administration:

3.5.1. Profile and tasks of the Project Leader

The Project Leader (PL) from the EU MS should be a senior civil servant or equivalent staff of a MS institution who works in the field relevant to this project and have been at five years in a management position within the institution. The PL will be responsible for achievement of project results, ensuring the activities for the co-operation and information exchange between EU MS side and Beneficiary side and ensuring that all the required support of the management and staff of the EU side are available. He will coordinate the Project Steering Committee (PSC) meetings on the EU MS side.

The PL shall devote a minimum of three working days per month in his home administration, with an on-site visit to the Republic of Moldova at least every 3 months to participate in the PSC meetings.

Profile

Qualification and skills University level education in economics, finance, audit or related field

Fluency in English. Command of Romanian and/or Russian is an asset

Good inter-personal and communication skills

Good management skills

General professional experience At least 10 years experience in Public Financial Management in the fields of FMC or Internal

Audit

Recent experience in a senior position in an institution responsible for Public Financial Management in an EU MS.

Experience in project management

Strong initiative, analytical and team working skills

Specific professional experience in financial management

Specific experience in the implementation of internal control systems in major government agencies, preferably from a coordination and/or harmonisation perspective

Knowledge of the process of internal audit.

Experience in preparation of major strategic documents

3.5.2. Profile and tasks of the RTA

Role and tasks

The RTA will be in charge of the day-to-day implementation of the Twinning project in the Republic of Moldova. S\he will coordinate the implementation of activities according to a predetermined work plan and liaise with the RTA counterpart in the Republic of Moldova. The RTA will be based at the Ministry of Finance of the Republic of Moldova.

RTA Secondment period: 24 months

Profile (indicative)

Qualification and skills University degree in a relevant discipline (Economics, accounting, PFM etc)

Fluency in English, good command of Russian and/or Romanian is an asset

Good PC literacy (Word, Excel, PowerPoint)

1

Good inter-personal and communication skills

Good management skills

Strong writing skills

General professional experience At least 3 years experience working in Public Financial Management, 5 years is considered to

be an asset.

Recent experience in a senior position in a state institution\mandated body responsible for the implementation of Financial and Managerial Controls, preferably involving some form of central oversight and/or harmonisation of standards, practices and guidelines.

Prior experience of working in an advisory role with a transition country that has implemented PIFC will be an asset

Strong initiative, analytical and team working skills

Experience in preparation of major strategy and policy documents in the area of public financial management and the related legal framework

3.5.3. Profile and tasks of the short-term experts

A pool of short term experts is required to implement the activities as outlined above covering the following indicative subjects as identified in the indicative activities:

Institutional Development and workflow analysis Strategic Planning Training and curriculum development Financial Management Controls Internal Audit IT audit Sampling techniques for auditors Preparation of Manuals Communication

Tasks of medium and short-term experts:

Terms of reference for short-term experts will be elaborated by PL/RTA at the work plan preparation stage. The exact number of STEs per activity should be agreed during the contract negotiation process.

Indicative General Profile of the Short Term expertsQualifications and skills:

University degree the appropriate field (as indicated above) Excellent command of written and spoken English. Knowledge of Romanian / Russian can be considered an asset Good inter-personal and communication skills.

General professional experience: At least 5 years of professional experience in the relevant field, 8 years experience is considered to

be an asset. Experience in PHARE/ENPI-East countries

3.5.4. Profile and Tasks of the RTA Assistant

The profile and tasks of the RTA assistant will be specified by the RTA and RTA counterpart. The recruitment procedure will follow the provisions of the EC manual section 5.9. RTA assistant.

1

4. Institutional FrameworkThe beneficiary institution is the Central Harmonisation Unit of the Ministry of Finance (MoF) of Moldova.The Central Harmonisation Unit was established in 2006 as one of the units of the Financial Control and Revision Service. In September 2008 the CHU was transferred to the Ministry of Finance. The CHU reports to a Vice Minister of Finance. The organisational structure of the Ministry of Finance is provided at Annex 6.The project is not expected to lead to any change in the institutional structure of the Ministry or the CHU.

5. Budget The maximum estimated indicative budget for the project is EUR 1.500.000. The beneficiary will provide in-kind contribution in the form foreseen in the Twinning manual.

6. Implementation Arrangements

6.1. The Implementing AgencyThe Implementing Agency responsible for tendering, contracting and accounting is the Delegation of the European Union to the Republic of Moldova.

Responsible person: Mr. Oleg HIRBUPosition: Project Manager, Delegation of the European Union to the Republic of

Moldova

Address: 12 Kogalniceanu Street

MD-2001 Chisinau, Republic of Moldova

Tel.: + 373 22 505 210

Fax: + 373 22 272 622

E-mail: [email protected]

The Programme Administration Office (PAO) will support the Twinning project implementation process together with the Delegation of the European Union to the Republic of Moldova:

Responsible person: Ms. Oxana DRAGUTA

Position: Senior Consultant, State Chancellery of the Government of Moldova, Division for Policy, Strategic Planning and External Assistance

Address: Piata Marii Adunari Nationale, 1

MD-2033 Chisinau

Tel: +373 22 250 465

Fax: +373 22 250 259

E-mail: [email protected]

6.2. Main counterpart in BC

Beneficiary Ministry of Finance, Directorate of Harmonisation of PIFC system (“CHU”)

1

institution:

BC Project Leader: Mr. Ion SIRBU

Position: Head of Directorate of Harmonisation of PIFC system (“CHU”)Ministry of Finance

Address: Cosmonautilor 7/406

MD-2005, Chisinau, Republic of Moldova

+373 22 226359

E-mail: [email protected]

RTA Counterpart: Mr. Petru BABUCI

Position: Head of Financial Management and Control Harmonization DivisionMinistry of Finance

Address: Cosmonautilor 7/406

MD-2005, Chisinau, Republic of Moldova

+373 22 226359

E-mail: [email protected]

6.3. Contracts

There will be one twinning contract with a selected Member State or consortium of Member States with duration of 24 Months.

6.4. Project Steering Committee

A Project Steering Committee (PSC) will be established for the control and supervision of the project activities and mandatory results. The Steering Committee will meet at regular intervals and will submit by the end of the meeting (as recorded in the meeting minutes) and approval/non approval of the project reports. Official minutes of the PSC meetings will be kept in English and distributed to all parties within 15 days after PSC meeting.

7. Implementation Schedule (indicative)

7.1 Launching of the call for proposal (date)November 2010

7.2 Start of project activities (date) September 2011

7.3 Project completion (date)November 2013

1

7.4 Duration of the implementation period (number of months)24 Months

8. SustainabilityThe Ministry of Finance is a permanent structure of the Government of Moldova and the twinning contract is a part of an ongoing restructuring of the MoF, which includes the establishment of a PIFC mechanism. Therefore, the results of the project will be sustainable.

9. Crosscutting Issues

EnvironmentNone

Poverty ReductionThe ultimate goal of the project is to strengthen accountability and in turn the managerial control of all public expenditure programmes including those programmes that address poverty. More effective internal control will reduce waste and inefficiency increasing resources available for programme activities.

Equal opportunityParticipation will be open to both female and male personnel. Records of staff participating in training and other project activities will reflect this statement. The gender structure within the public authorities, entities and bodies on state and local level where are the majority of procurement purchases is well balanced. This enables fair male/female deployment in the execution of the project itself.

Good Governance and Human rights

The project supports good governance by establishing better management control processes that facilitate the accountability of ministers for their expenditure programmes.

10. Conditionality and sequencingThere are no conditionalities.

1

ABBREVIATIONSBC Beneficiary Country

CHU Central Harmonisation Unit of the Ministry of Finance – a central unit established to fulfil the harmonization requirements of PIFC

COA Court of Accounts of the Republic of Moldova

COSO The Committee of Sponsoring Organizations of the Treadway Commission – a entity that has prepared a range of standards/principles for internal control that are now widely accepted as international best practice.

CPAA Central Public Administrative Authority - as defined in the law on Government comprising 16 Ministries and 8 central agencies

EU European Union

FMC Financial Management and Control – one of the elements of PIFC referring to all the systems and processes put in place to ensure that management achieves their objectives.

FCRS Financial Control and Revision Service of Moldova – an entity carrying out financial revisions.

IA Internal Audit – an organizational unit created within a public sector entity to carry out internal audit work in line within international standards

IC Internal Control – defined within PIFC as FMC plus IA.

IFAC International Federation of Accountants – an international standard setting body.

IIA Institute of Internal Auditors – a recognised internal audit standard setting body.

INTOSAI International Organisation of Supreme Audit Institutions

IT Information Technology

LPAA Local Public Administrative Authority – an organizational unit at the local level

MNIAPS Methodological Norms for Internal Audit on the Public Sector in Moldova

MS Member State

PEFA PEFA (Public Expenditure & Financial Accountability) is a partnership between the World Bank, the European Commission, the UK's Department for International Development, the Swiss State Secretariat for Economic Affairs, the French Ministry of Foreign Affairs, the Royal Norwegian Ministry of Foreign Affairs, and the International Monetary Fund.PEFA aims to support integrated and harmonized approaches to assessment and reform in the field of public expenditure, procurement and financial accountability.Assessments based on PEFA methodology have been carried out in Moldova once every 2-3 years, the most recent in July 2008.

PFM Public Financial Management – a generic description of the legal framework, processes and institutions required to manage the public finances effectively

PFMP Public Financial Management Programme – a project established through a multi donor trust fund to improve public financial management in Moldova

PIFC Public Internal Financial Control – a concept developed by the European Union to encompass Internal Audit (IA) and Financial Management Controls (FMC) and a process of central harmonization.

PI Performance Indicator

PL Project Leader (Member State or Beneficiary Country)

STE Short Term Expert

TNA Training Needs Analysis

ANNEXES TO PROJECT FICHE

1. Logical Framework Matrix in standard format2. Indicative Implementation Chart 3. Extract from the PIFC development strategy outlining the PIFC Concept in Moldova4. Legal and normative framework5. References to Government Strategies6. Organisational structure of the Ministry of Finance

ANNEX 1 - LOGFRAME PLANNING MATRIX

Project name and number:

Strengthening Public Financial Management in Moldova

Programme name and number: ENPI annual Programme 2008

Total budget: EUR 1.500.000

Overall objective Objectively verifiable indicators Sources of Verification

To improve the management of public financial control in the Republic of Moldova in line with internationally recognized standards and European best practices.

Improved PEFA scores for FMC and IA. Increased willingness to provide budget support to Moldova

PEFA evaluations, Donor correspondence related to budget support.

Project purpose Objectively verifiable indicators Sources of Verification Assumptions

To support the Ministry of Finance to improve Public Internal Financial Controls

Reduced number of corruption / fraud cases due to poor FMC.

Improved ranking in the TI corruption perception Index. (currently 89)

PEFA indicators specific for FMC and internal audit improved in comparison to the last PEFA assessment

Audit Reports

CHU reports

Reports from the Anti Corruption Agency

Transparency international Corruption Perception Index

PEFA reports

Political will to implement FMC and Internal Audit as required

Staff level in CHU is sufficient for the task and there are no significant changes in staff.

Results Objectively verifiable indicators Sources of Verification Assumptions

1. Enhanced capacity of the Central Harmonisation Unit to oversee the implementation of PIFC in Moldova.

2. Legislative and Normative framework updated.

3. Financial and Managerial (FMC) control strengthened.

Internal controls and audit process are risk based and reflect clear coordination from CHU. Draft legislation is put forward for Government ConsultationPEFA score on indicator 18,19,20 are improved from “b” to “a”

PEFA assessment reportsGovernment reports on the consultation of legislationWebsite of CHU enhancedInternal Audit ReportsAnnual Report of the CHUInterviews with staff.

Enabling environment for change remains in place.

Political will to implement FMC and Internal Audit as required

Audited entities are prepared to

4. Internal Audit Capacity Strengthened. PEFA score on indicator 21 improved from “c+” to “b”Staff of budget organisations have better understanding of importance and methods of PIFC

provide sufficient staff to support experts

Sufficient technical expertise and managerial capacity to support the activities

Activities Means Assumptions

Component 1: Enhancement of the capacity of the Central Harmonisation Unit to oversee the implementation of PIFC in Moldova

1.1 Establishment of and support to PIFC Council 25 Man Days Short term experts PIFC Council not already in existence when twinning project commences

1.2 Review of progress on PIFC strategy implementation

20 Man Days Short term experts Staff is available to participate in the review, PIFC strategy contains sufficient benchmarks to enable monitoring.

1.3 Preparation of an updated strategy for PIFC for the period 2013- 2016

20 Man Days Short term experts Political will to continue PFM reform is present

1.4 Develop a Communication Strategy to support PIFC implementation in Moldova

40 Man Days Short term experts Means to implement the strategy can be made available. Web developers are available to work with the content developers.

Component 2: Update of the legislative and normative framework

2.1 Review of the legal and regulatory framework for PIFC

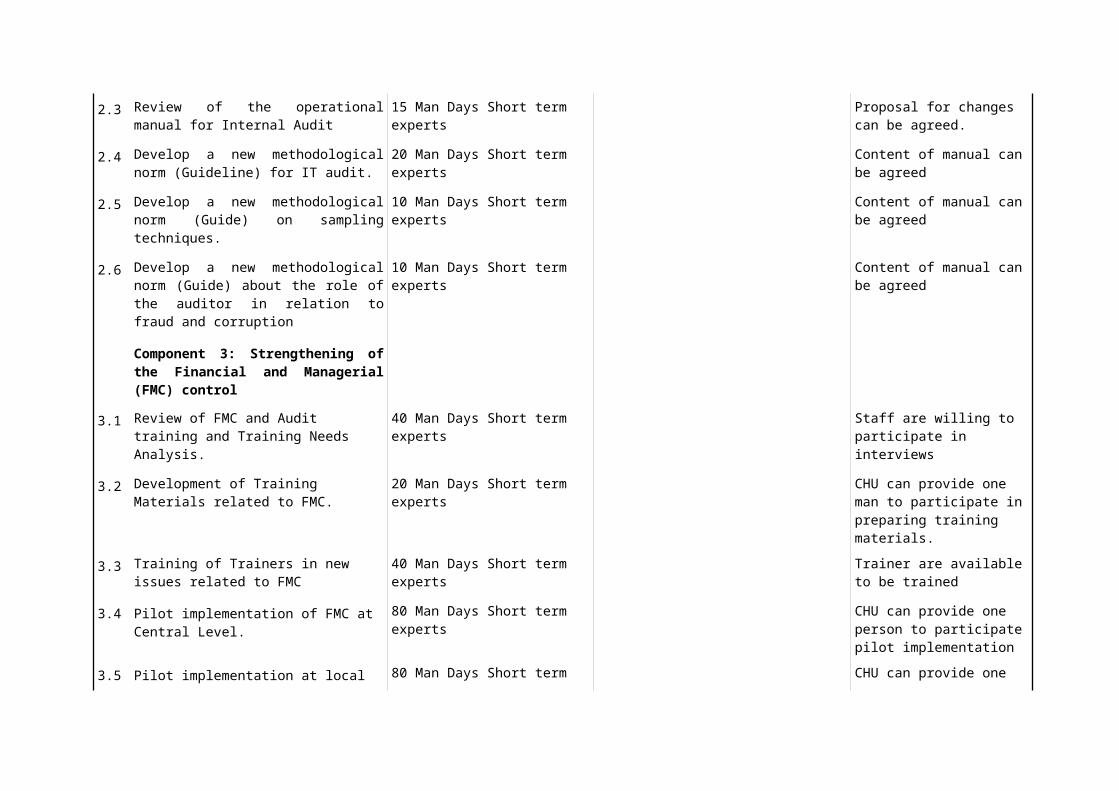

20 Man Days Short term experts Proposal for changes can be agreed.

2.2 Review of the “Methodological Norm” for FMC

20 Man Days Short term experts Proposal for changes can be agreed.

2.3 Review of the operational manual for Internal Audit

15 Man Days Short term experts Proposal for changes can be agreed.

2.4 Develop a new methodological norm (Guideline) for IT audit.

20 Man Days Short term experts Content of manual can be agreed

2.5 Develop a new methodological norm (Guide) on sampling techniques.

10 Man Days Short term experts Content of manual can be agreed

2.6 Develop a new methodological norm (Guide) about the role of the auditor in relation to fraud and corruption

10 Man Days Short term experts Content of manual can be agreed

Component 3: Strengthening of the Financial and Managerial (FMC) control

3.1 Review of FMC and Audit training and Training Needs Analysis.

40 Man Days Short term experts Staff are willing to participate in interviews

3.2 Development of Training Materials related to FMC.

20 Man Days Short term experts CHU can provide one man to participate in preparing training materials.

3.3 Training of Trainers in new issues related to FMC

40 Man Days Short term experts Trainer are available to be trained

3.4 Pilot implementation of FMC at Central Level. 80 Man Days Short term experts CHU can provide one person to participate pilot implementation

3.5 Pilot implementation at local authorities. 80 Man Days Short term experts CHU can provide one person to participate pilot implementation

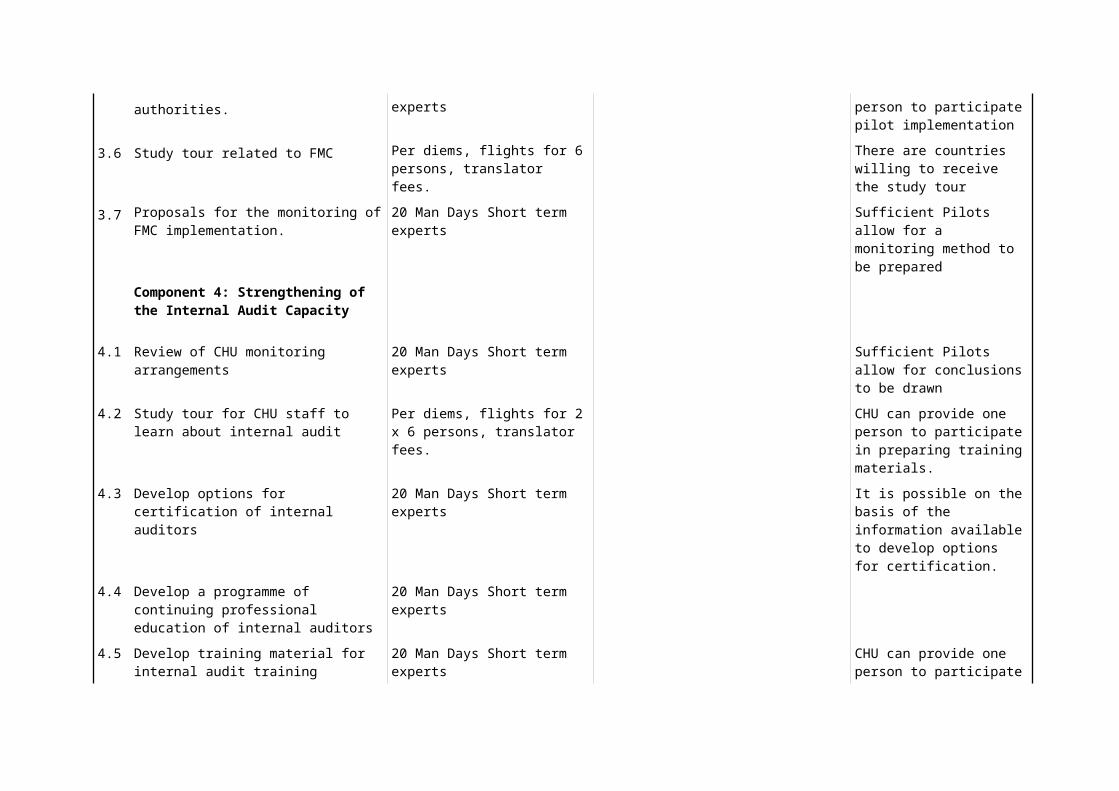

3.6 Study tour related to FMC Per diems, flights for 6 persons, translator fees.

There are countries willing to receive the study tour

3.7 Proposals for the monitoring of FMC implementation.

20 Man Days Short term experts Sufficient Pilots allow for a monitoring method to be prepared

Component 4: Strengthening of the Internal Audit Capacity

4.1 Review of CHU monitoring arrangements 20 Man Days Short term experts Sufficient Pilots allow for conclusions to be drawn

4.2 Study tour for CHU staff to learn about internal audit

Per diems, flights for 2 x 6 persons, translator fees.

CHU can provide one person to participate in preparing training materials.

4.3 Develop options for certification of internal auditors

20 Man Days Short term experts It is possible on the basis of the information available to develop options for certification.

4.4 Develop a programme of continuing professional education of internal auditors

20 Man Days Short term experts

4.5 Develop training material for internal audit training

20 Man Days Short term experts CHU can provide one person to participate in preparing training materials.

4.6 Delivery of Training of Trainers related to Internal Audit

40 Man Days Short term experts Trainers are available to be trained

4.7 Preparation of internal audit strategy and work planning.

20 Man Days Short term experts Sufficient information is available for the strategic planning.

4.8 On the job training by means of pilot audits 80 Man Days Short term experts Audited institutions are willing to actively participate in the exercise.

4.9 Study tours for public sector internal auditors Per diems, flights for 6 persons, translator fees.

ANNEX 2 - Preliminary Implementation PlanningMonth 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

Component 0

0.1 Kick off Meeting x

0.2 Steering Committee meetings x x x x x x x

0.3 Monthly meeting x x x x x x x x x x x x x x x x x x x x x x

0.4 Wrap up Meeting x

Final Payment x

Component 1: Enhancement of the capacity of the Central Harmonisation Unit to oversee the implementation of PIFC in Moldova

1.1. Establishment of and support to PIFC council x x x x

1.2 Review of progress on PIFC strategy implementation x x x x x x x

1.3 Preparation of an updated strategy for PIFC for the period 2013- 2016 x x x x

1.4Develop a Communication Strategy to support PIFC implementation in Moldova

x x x x

Component 2: Update of the legislative and normative framework

2.1Review of the legal and regulatory framework for PIFC x

2.2Review of the “Methodological Norm” for FMC x

2.3Review of the operational manual for Internal Audit x

2.4Develop a new methodological norm (Guideline) for IT audit. x

2.5Develop a new methodological norm (Guide) on sampling techniques. x

2.6Develop a new methodological norm (Guide) about the role of the auditor in relation to fraud and corruption

x

ANNEX 2 - Preliminary Implementation PlanningComponent 3: Strengthening Financial and Managerial Control

3.1Review of FMC and Audit training and Training Needs Analysis. x x

3.2 Development of Training Materials related to FMC. x

3.3Training of Trainers in new issues related to FMC x

3.4 Pilot implementation of FMC at Central Level. x x x x x x

3.5 Pilot implementation of FMC at local authorities. x x x x x x

3.6 Study tour related to FMC x

3.7Proposals for the monitoring of FMC implementation. x

3.8Study tour to examine the monitoring of the implementation of FMC in one member state

x

Component 4: Strengthening of the Internal Audit Capacity

4.1 Review of CHU monitoring arrangements x

4.2 Study tour for CHU staff to learn about internal audit x

4.3 Develop options for certification of internal auditors x

4.4Develop a programme of continuing professional education of internal auditors

x

4.5 Develop training material for internal audit training x x

4.6 Delivery of Training of Trainers related to Internal Audit x x

4.7 Preparation of internal audit strategy and work planning. x x

4.8 On the job training by means of pilot audits x x x x x x x x

4.9 Study tours for public sector internal auditors x x

ANNEX 3

Extract from the PIFC Development strategy– The conceptual model for PIFC in Moldova.

5. CONCEPTUAL MODEL

◦ Public internal financial control

▪ PIFC as defined by the EU has three distinct elements represented by the formula:

PIFC = FMC + Internal Audit + Central Harmonization Unit

▪ The relationship of PIFC to the traditional concept of internal control is defined as:

Internal Control = FMC + Internal Audit

◦ Centralized Harmonization - the design and implementation of PIFC

▪ The responsibility for the design and implementation of PIFC in Moldova will rest with the Ministry of Finance. The Ministry of Finance has the role to develop and implement the state policy in the field of public finances and is responsible for determining the nature of changes in public financial management required and the pace at which those changes are to be implemented.

▪ The CHU from the Ministry of Finance will:

Monitor the implementation of Public Internal Financial Control Concept;

Develop and submit proposals on amending and completing the legal framework in the area of public internal financial control;

Develop regulatory acts on the organization of FMC and internal audit in the public sector, including standards, methodological norms, instructions, guidelines, recommendations and other regulatory acts;

Monitor and evaluate the implementation of the internal audit and FMC in the public sector;

Evaluate internal audit activity and FMC system functionality in the public sector;

Develop the Annual Consolidated Report on Public Internal Financial Control and subsequently the Ministry of Finance submits it to the Government;

Organize and/or deliver training in the area of financial management and control, and training and professional certification of internal auditors of the public sector;

Harmonize the regulatory framework in the area of PIFC with the best practices.

▪ Reporting directly to the Minister of Finance the CHU is a structural subdivision responsible for coordinating the process of transformation from the existing system of control to a new PIFC system. In effect, the role of the CHU is to manage a change process that will directly impact on all the managers and staff in the public sector

▪ As a change agent, the CHU has five strategic objectives:

To identify what changes are needed to current systems of financial management and control to promote better managerial accountability in line with PIFC principles, setting and prioritizing

actions required by reference to the likely benefits, implementation costs and risks;

To persuade managers at all levels of the need for, and benefits of, the change to PIFC, including the introduction of internal audit;

To train public servants in the area of PIFC and provide specific training on FMC and internal audit in the public sector which meets the needs of end-users;

To support managers across the public sector in the implementation of PIFC by giving timely and relevant ad hoc advice: by producing regulations and methodological guidelines that are clear and easy to understand; and by updating the Ministry of Finance web-site devoted to PIFC, etc.;

To monitor the implementation of PIFC across the public sector through continuous recording of progress achieved, periodic evaluation of actions and reporting on this progress achieved.

◦ Financial management and control

▪ Concept and definition

The conceptual model for the implementation of FMC in the Republic of Moldova is reflected in the National Internal Control Standards in the public sector. The standards establish the main areas where action is required to implement FMC across the public sector.

Financial management and control is defined as a system planned and executed by the governing and administration persons and other staff in accordance with the regulatory framework and the applied regulations to provide a reasonable assurance that the public funds are used in a legal, ethical, transparent, economic, efficient and effective way for the fulfilment of the entity’s objectives.

The manager of the entity organizes the financial management and control system, with the purpose of providing reasonable assurance that the entity’s objectives will be achieved through:

effective and efficient operations;

compliance with legislation and applicable regulations;

safety and optimization of assets and liabilities;

reliability and integrity of information.

The first category addresses entity's basic objectives, including performance goals. The second category relates to complying with those laws and regulations to which the entity is subject. The third category relates to safeguarding public funds against losses, wrong usage and prejudices caused by squanders, abuse, deficient management, errors, fraud and irregularities. The fourth category deals with the preparation of reliable financial statements and other financial data. These distinct but overlapping categories address different needs and allow a directed focus to meet the separate needs.

▪ Main components of FMC system

FMC is implemented based on the international internal control framework that consists of five interrelated components (see p. 5.3.2.2). These components are derived from the way management runs an activity, and are integrated with the

management process but do not replace this one. Although the components apply to all public entities, small and mid-size institutions may implement them differently than large ones. The internal control procedures of a small entity may be less formal and less structured, yet a small entity can still have an effective FMC system.

The National Internal Control Standards in the public sector cover the same five broad areas that include:

Control environment – this sets the tone of an organization, influencing the internal control consciousness of its staff.

Performance and Risk Management – this covers the need to establish objectives for operational systems and to identify the risks that may impact their achievement.

Control Activities – these are the policies and procedures that help ensure management directives are carried out.

Communication and information – this covers the information that must be identified, captured and communicated in a form and timeframe that enables people to carry out their responsibilities.

Monitoring and Evaluation – this covers the process for assessing the quality of the FMC system's performance over time.

There is a direct relationship between the four categories of objectives (paragraph 5.3.1.3), which are what an entity strives to achieve, and the five components (paragraph 5.3.2.2), which represent what is needed to achieve the objectives. All components are relevant to each category of objectives.

▪ Limitations in FMC – the concept of reasonable assurance

FMC provides reasonable assurance that an entity achieves its strategic and operational objectives in an efficient and effective way, produces reliable financial and performance information; manages the assets and liabilities in a safe and optimal way, and acts in compliance with relevant legislation.

The achievement of objectives will be affected by limitations inherent in FMC system. These include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of simple error or mistake. Additionally, internal control procedures can be circumvented by the collusion of two or more people, as well by the unwillingness of the management to follow the procedures. Another limiting factor is that the design of a FMC system must reflect the fact that there are resource constraints, and the benefits of internal control procedures must be considered relative to their costs.

Hence, the FMC system does not guarantee the achievement of those four categories of general objectives (p. 5.3.1.3) and does not influence the Government policy changes or economic situation – factors that influence the performance of a public entity.

▪ Responsibility for FMC implementation

The primary responsibility for the implementation of FMC lies with the head of the public entity. More than any other individual, the head of the entity sets the "tone at the top" that affects the integrity and ethics and other factors of a positive control environment. In a large public entity, the manager fulfils this duty by providing

leadership and direction to operational managers and monitoring their activity. Operational managers, in their turn, assign responsibility for establishment and implementation of more specific internal control policies and procedures to the personnel. In a smaller entity, the influence of the manager is usually more direct.

FMC is, to some degree, the responsibility of every employee in an entity and therefore should be an explicit or implicit part of everyone's job description. All employees produce information used in FMC system or take other actions needed to perform the internal control procedures. Also, all personnel should be responsible for communicating upward problems in operations, non-compliance with the Code of Ethics, or other violations of policy or legal and regulatory framework in force.

◦ Internal Audit

▪ Definition of internal audit

The National Internal Audit Standards (NIAS) define internal audit as an independent and objective activity that:

helps the entity to secure a certain level of control over its operations, provides guidance regarding the enhancement of its operations and contributes to the creation of added value;

helps the entity to meet its objectives, by assessing, through a systematic and methodical approach, the risk management, control and corporate governance processes, with proposals of improving their effectiveness.

Internal Audit is further defined by the NIAS to encompass two types of audit missions where:

Assurance mission – is an objective review of the probative elements, carried out in order to provide the entity with independent assessment of the risk management, control or corporate governance processes;

Consulting mission – covers consulting activities or other consultancy-related services, provided to the requiring entity to help the management meet its objectives (provide value added and improve the functioning of the entity), whose nature and scope are agreed in advance with the entity.

▪ 5.4.2.1. Internal audit organization and operation

The Internal Audit is organized through an internal audit unit established within the organizational structure of the public entity, if this one is a central special public administration authority or local public administration authority of the second level or of Balti municipality that has its own Internal Audit Charter.

The internal audit units of central and local public authorities perform internal audit of subordinated entities.

The public entity, that does not fall under the scope of p. 5.4.2.1, has the right to establish an internal audit unit.

The public entity, subordinated to central and local public authorities, that does not fall under the scope of p. 5.4.2.1, has the right to establish an internal audit unit with the approval of the hierarchically superior body.

The internal audit unit is established within the approved staffing limits of the

public entity, being directly subordinated and directly reporting to the entity’s manager.

The manager of entity shall officially inform the Central Harmonization Unit from the Ministry of Finance on the establishment of the internal audit unit within the public entity.

The head of the internal audit unit is responsible for reporting to the management of the entity they audit:

(i) any cases where there is evidence of suspected fraud and corruption; and

(ii) any areas identified of high risk of fraud and corruption where no specific cases have been previously identified.

The manager of the entity is responsible for passing any cases of suspected fraud and corruption to the Centre for Combating Economic Crime and Corruption.

ANNEX 4

Legislative Framework Regarding Public Internal Financial Control