108 finance and finance reporting (actuarrial)

TRANSCRIPT

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

13 April 2000 (pm)

Subject 108 — Finance and Financial Reporting

Time allowed: Three hours

INSTRUCTIONS TO THE CANDIDATE

1. Write your surname in full, the initials of your other names and yourCandidate’s Number on the front of the answer booklet.

2. Mark allocations are shown in brackets.

3. Attempt all 19 questions, beginning your answer to each question on aseparate sheet.

Graph paper is not required for this paper.

AT THE END OF THE EXAMINATION

Hand in BOTH your answer booklet and this question paper.

In addition to this paper you should have availableActuarial Tables and an electronic calculator.

Faculty of Actuaries108—A2000 Institute of Actuaries

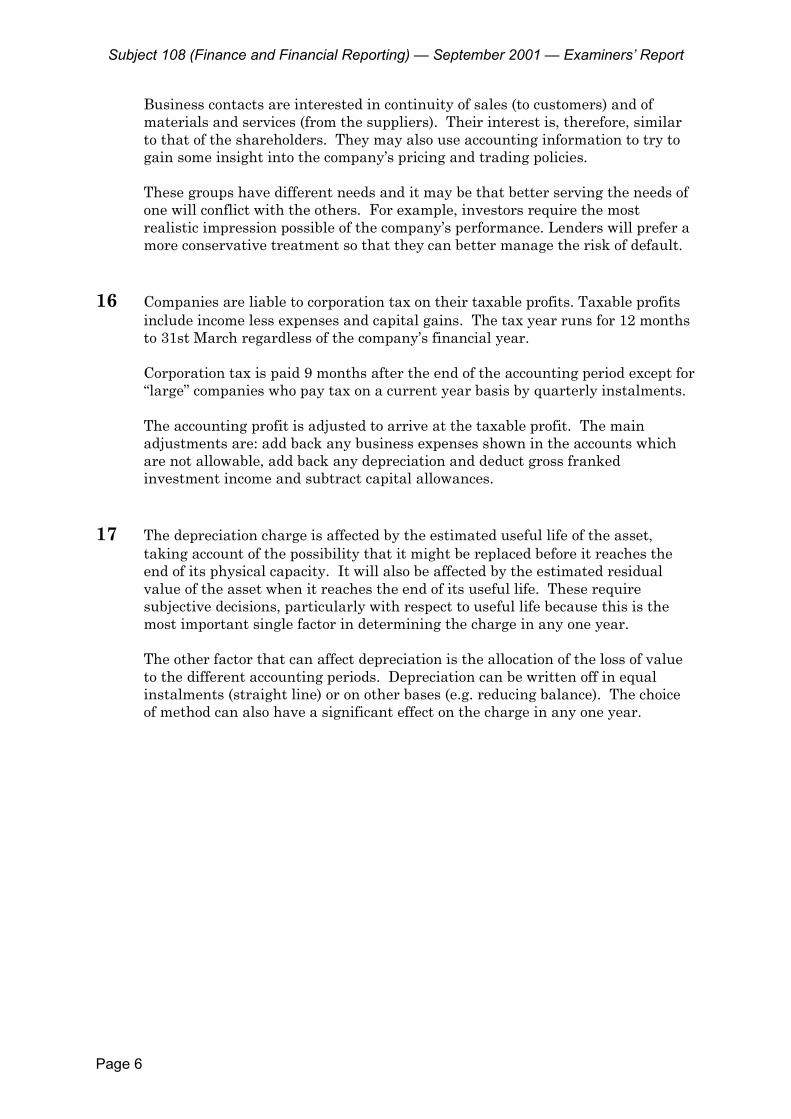

108—2

For questions 1–5 indicate in your answer booklet which one of the answers A, B, C or Dis correct.

1 In certain circumstances the Stock Exchange may grant a quotation for acompany even though the company is not making any new shares or existingshares available to the market.

This method of obtaining a quotation is known as:

A A placingB A tender issueC An introductionD A prospectus issue [2]

2 The following information relates to the ordinary shares of F plc:

Earnings per share 50pDividend cover 2.5 timesPublished dividendyield

3.2%

The price of F plc’s ordinary shares implied by the above data is:

A 78pB 625pC 1563pD 3906p [2]

108—3 PLEASE TURN OVER

The following information relates to questions 3 and 4.

X Ltd’s Balance sheet as at 31 December 1999 included the following items:

£ Total assets less current liabilities 125,000 9% Debentures (repayable 2004) 20,000

105,000

Ordinary shares of 50p each 50,000 10% Preference shares of £1 each 20,000 Reserves 35,000

105,000

3 X Ltd’s profit before interest and taxation for the year to 31 December 1999was £40,000.

X Ltd’s company’s Return on Capital employed for the year ended 31December 1999 is:

A 32%B 38%C 44%D 47% [2]

4 X Ltd’s interest cover is:

A 6.6 timesB 10.5 timesC 13.9 timesD 22.2 times [2]

108—4

5 A company’s ordinary shares have a current market price of £2. The companyis making a 2 for 5 rights issue at a price of £1.50.

What is the ex-rights price?

A £1.50B £1.74C £1.86D £2.60 [2]

In questions 6–10 one or more of the options may be correct. Answer in your booklet byselecting according to the following code:

A if I and II only are correctB if II and III only are correctC if I only is correctD if III only is correct

6 Which of the following assets are not intangible fixed assets?

I Research costsII Trade marksIII Development costs [2]

7 Which of the following is true:

I Depreciation adjustments are attempts to reflect the value of fixedassets in the balance sheet.

II Depreciation is an application of the matching concept.

III Depreciation is a measure of the wearing out or consumption of afixed asset over time. [2]

8 Which of the following statements about preference shares is correct?

I Preference shares carry fixed dividend rights.

II Preference dividends can be suspended if the directors decide that thecompany cannot afford to pay them.

III Preference shareholders never have any voting rights. [2]

9 An ordinary share may have a high dividend yield because:

I Dividend cover is high.II It is cheap.III Dividend growth prospects are poor. [2]

108—5 PLEASE TURN OVER

10 Chargeable gains on the disposal of the following assets are not subject tocapital gains tax:

I Any residential properties.II Private motor cars.III British government securities. [2]

11 The directors of Sawburn plc have decided to investigate ways in which theymight improve their management of short and medium term finance. Thecompany’s business involves irregular inflows and outflows of cash. Thedirectors have tended not to rely on bank overdraft in order to deal with cashshortages, preferring to use short fixed term loans instead. They are nowconsidering a change to this policy because of the greater flexibility ofoverdraft finance. They have decided that this might reduce finance costsbecause interest is only paid on overdrafts on the amount by which the accountis actually overdrawn.

Describe the factors that the directors should take into account in making thischange of policy and explain whether overdraft is likely to be the most suitableform of short term finance in these circumstances. Your answer should makeappropriate references to the alternatives to overdrafts. [8]

12 The directors of a company are planning to undertake a rights issue. Describethe factors that should be taken into account in deciding whether to have thisissue underwritten. [6]

13 Explain what is meant by the term “associate company” and explain howassociates are treated on consolidation. [4]

14 Discuss the proposition that ratio analysis is considered to be a useful methodof interpreting financial statements, although it has some limitations. [6]

15 A company intends to acquire a factory and £600,000 of plant and machinery.Explain the taxation implications of leasing these assets rather thanpurchasing them outright. [6]

16 Describe the main features of merchant banks and discuss their influence onthe financial markets. [6]

108—6

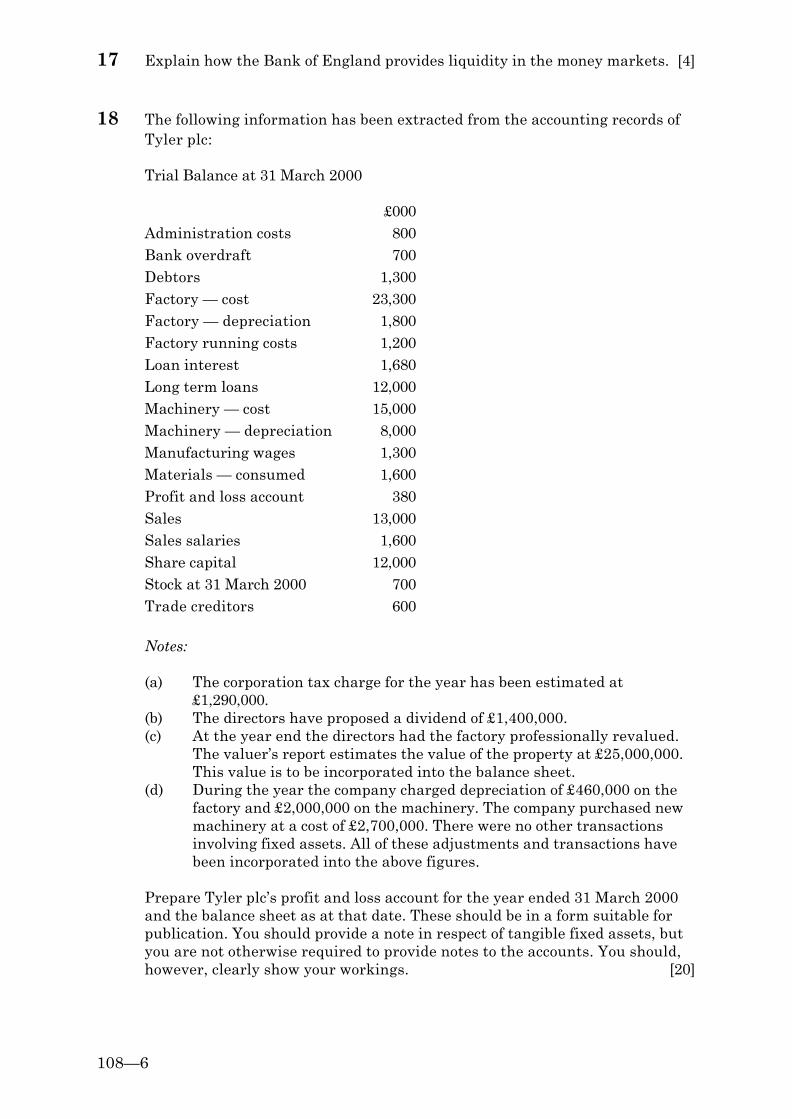

17 Explain how the Bank of England provides liquidity in the money markets. [4]

18 The following information has been extracted from the accounting records ofTyler plc:

Trial Balance at 31 March 2000

£000 Administration costs 800 Bank overdraft 700 Debtors 1,300 Factory — cost 23,300 Factory — depreciation 1,800 Factory running costs 1,200 Loan interest 1,680 Long term loans 12,000 Machinery — cost 15,000 Machinery — depreciation 8,000 Manufacturing wages 1,300 Materials — consumed 1,600 Profit and loss account 380 Sales 13,000 Sales salaries 1,600 Share capital 12,000 Stock at 31 March 2000 700 Trade creditors 600

Notes:

(a) The corporation tax charge for the year has been estimated at£1,290,000.

(b) The directors have proposed a dividend of £1,400,000.(c) At the year end the directors had the factory professionally revalued.

The valuer’s report estimates the value of the property at £25,000,000.This value is to be incorporated into the balance sheet.

(d) During the year the company charged depreciation of £460,000 on thefactory and £2,000,000 on the machinery. The company purchased newmachinery at a cost of £2,700,000. There were no other transactionsinvolving fixed assets. All of these adjustments and transactions havebeen incorporated into the above figures.

Prepare Tyler plc’s profit and loss account for the year ended 31 March 2000and the balance sheet as at that date. These should be in a form suitable forpublication. You should provide a note in respect of tangible fixed assets, butyou are not otherwise required to provide notes to the accounts. You should,however, clearly show your workings. [20]

108—7

19 The directors of Holt plc have introduced a formal system of investmentappraisal. Projects must have a positive net present value when discounted ata cost of capital determined in relation to their systematic risk. The board ispresently considering two unrelated projects. One is for an investment in aspeculative research project. This is fraught with potential problems becauseit is dependent on the successful application of a recent theoretical discoveryreported in the physics literature. Even if the technical problems can beovercome, there is a serious risk that another company will offer the principalscientists — who are the leading specialists in their field — more lucrativecontracts. The other project is a rather more predictable expansion of theproduction facilities for an existing product line which has a well establishedmarket.

The beta coefficient for the research project is 0.6 while that of the newproduction facilities is 1.3. The risk free rate is 3% and the risk premium is8%.

(a) Calculate the required rate of return for each of the projects. [4]

(b) Explain why it might be possible that an apparently risky project couldhave a lower required rate of return than that for a less volatile project.

[6]

(c) Explain whether company directors are likely to accept the logicunderlying the capital asset pricing model (CAPM) in practice whenthey are making investment decisions. [5]

(d) Outline alternative ways in which one might estimate the betacoefficient of a project. [5]

[Total 20]

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

April 2000

Subject 108 — Finance and Financial Reporting

EXAMINERS’ REPORT

! Faculty of Actuaries! Institute of Actuaries

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 2

1 C

2 B

3 -

4 -

5 C

6 C

7 B

8 A

9 B

10 -

There were three small errors in questions in order to ensure no student wasunfairly penalised for this the paper was marked out of 94 and the three questionswere discounted. The remaining questions were answered well.

11 The directors should consider the cost of the different types of finance available tothem. Clearly, it is desirable to use the cheapest source unless it has some otherdisadvantage. Different types of finance involve different levels of risk for thelender and that will tend to result in different rates of interest.

The other major issue is the risks created for the company. A source of financemight leave the company open to serious penalties if it is forced to default for anyreason. For example, a secured loan will tend to be relatively cheap but mightcreate serious problems for the company if the lender calls in the security.Furthermore, the company will have a limited borrowing capacity for any giventype of finance. Exhausting this might restrict its ability to deal with futureproblems.

Bank overdrafts do provide a flexible means of dealing with fluctuatingrequirements. Most loans commit the company to the payment of interestthroughout the agreed term of the loan. Early repayment might not be permittedby the agreement or could involve an additional charge. Overdraft facilities canbe agreed with the bank and then used and as and when the company requires.The company can borrow up to its overdraft limit for as short a period as itrequires the funding. Interest will be charged on a daily basis on the actualamount outstanding.

The rates of interest charged on overdrafts tend to be quite high and so it mightprove to be an expensive source of finance if the company is likely to be heavilyoverdrawn for a large proportion of the time. Term loans might prove cheaper inthis situation because of lower rates, even though there might be short periods ofcash surplus during which the company does not actually require the funding.

One disadvantage of using the overdraft facility is that the banks are likely toimpose a restriction on the maximum amount that they are willing to advance inthis manner. Having the capacity to borrow up to the limit at short notice couldbe useful if the company has an unexpected need for cash. If part of the facilityhas been used up in the course of normal operations then the company will bemore severely constrained.

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 3

There may be other sources of finance which would be more suitable for thecompany’s fluctuating needs. For example, debt factoring makes it possible toraise cash immediately after a sale has taken place. This has the advantage ofbringing in more cash at busier times when the company’s needs might begreater and could offer many of the benefits of overdraft without using up any ofthe actual overdraft facility.

This question was well answered by most candidates

12 The main advantage of underwriting a share issue is that there is no risk of thecompany being left with unsold shares. If the rights issue proves unattractive toshareholders then the company may have insufficient funds to finance the projectfor which the shares were being issued. It may prove difficult and expensive toraise additional long term finance by some other means.

The main disadvantage of underwriting the issue is that the company will haveto incur fees which may prove substantial. While this might be a worthwhileinvestment, it is desirable to minimise such costs wherever possible.

The rights issue is likely to prove successful if the new shares are sold at areasonable discount. While any discount is likely to make the shares attractive,the volatility of the stock market and of the company itself should be considered.If the share price is likely to move rapidly then the rights price could exceed themarket price, thereby making he new shares unattractive.

The extent to which the company can persuade the markets that the new fundswill be invested profitably will also have some bearing on the need for anunderwriter. If the company has a viable project then the share price could risein response to that information and that will make the issue even moreattractive. The company should discuss the likely market perception of theproject with independent experts such as the company’s merchant bankers.

This question was reasonably well answered by candidates

13 An associate company is one in which the holding company has an interest whichgrants it some influence, but not outright control. This is normally implied by aninvestment which exceeds 20% of share capital, but is less than 50%.

Associate companies are included in the consolidated profit and loss account byincluding the group’s share of their profits, regardless of whether those profitshave been distributed by way of dividend. The group share of net assets isincluded in the consolidated balance sheet.

The first part of this question was well answered however candidates had littleidea of how the associate should be treated in the consolidation as a result themarks were low.

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 4

14 Many figures in the financial statements are difficult to interpret in isolation. Forexample, it means very little to know how much profit a business made withouthaving some corresponding idea of the amount of capital that had to be investedin order to generate this income.

Ratios provide a basis for comparing related figures and for identifying issuesthat ought to be investigated. Management might, for example, monitor liquidityby calculating the current ratio and would deal with any deviation from theoptimal relationship – usually 2:1.

Trends in ratios can be particularly revealing. For example, a decreasing currentratio is normally a more worrying sign than a ratio which appears to be low inabsolute terms.

Ratios do have a number of drawbacks. For example, they can be distorted bywilful manipulation of the figures (e.g. window dressing or off-balance sheetfinancing). They can also omit crucial information such as contingent liabilityinformation.

This question was well answered

15 If the company purchases the assets then it will receive a writing downallowance on both the industrial buildings and the plant and machinery. Thismeans that the tax benefits of the investment will not be received immediatelyafter the investment takes place. Instead, the company will have to offset thecost against taxable profit in future years.

If the company borrows in order to finance the acquisition of the assets then itwill be able to claim tax on the interest payments.

Rental payments on property and lease payments on plant and machinery willattract immediate tax relief, with the taxable profit being reduced by theamounts of the cash flow in each year.

The company’s ability to enjoy the tax relief on writing down allowances isrelated to its ability to earn taxable profits. If the company is making a loss fortax purposes then it will receive no benefit from the additional writing downallowances. A lessor may be in a better position to take advantage of these reliefsand this may well be reflected in the rentals.

This question was quite well answered by the majority of candidates.

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 5

16 Merchant banks specialise in corporate finance. Their role is largely advisory.Typically, merchant banks will provide advice on the following types of matter:

1. bid or defence strategies in a takeover2. financial aspects of a merger3. investment projects4. raising capital

They also act as intermediaries in the issue of financial instruments:

1. issuing houses in share issues2. underwriters of new issues3. Eurobonds

Merchant banks also provide fund management services:

1. management of unit trusts, investment trusts and pension funds2. organisation of the Eurobond market

Merchant banks are active in the money markets:

1. as guarantors of bills of exchange2. as holders of Treasury bills and local authority bills

Occasionally, merchant banks provide finance to companies.

Candidates answered the first part of the question well but were unsure ofmerchant banks influence on the market.

17 The Bank of England acts in a supporting role for the various institutions thatare active in the short-term money markets, particularly the discount houses.

The discount houses provide short term finance by borrowing cash surpluses thatmight be available for as little as a few days and lending for a slightly longerperiod. This difference in maturity between their assets and liabilities can leavethem exposed to the risk of being unable to repay their debts.

The risk of default is avoided because the Bank of England will always providethe discount houses with support whenever they need it. This can take thefollowing forms:

1. The Bank will always be prepared to purchase Treasury or local authoritybills or bills of exchange from the discount houses in order to help themthrough a cash crisis.

2. The Bank will act as a lender of last resort provided the discount housesdeposit bills as security.

3. The discount houses can sell a bill of exchange to the Bank andsimultaneously agree to repurchase it at a later date.

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 6

This support is available because the discount houses are an important elementof the Bank’s mechanism for controlling short term interest rates. The discounthouses agree to buy the Treasury bills that the Bank sells at its weekly Treasurybill auctions.

This question was well answered by most candidates.

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 7

18 Tyler plc

Profit and loss account

for the year ended 31 March 2000

£000 £000

Turnover

Cost of sales - 4,100

Gross profit

Distribution costs - 1,600

Administrative expenses - 800

- 2,400

Operating profit

Interest payable - 1,680

Taxation - 1,290

Dividend - 1,400

Retained profit for the year

Retained profit brought forward

Retained profit carried forward 2,510

Tyler plc

Balance sheet as at 31 March 2000

£000 £000

Tangible fixed assets (note 1) 32,000

Current assets

Stock 700

Trade debtors 1,300

2,000

Creditors: amounts due within one year

Bank overdraft - 700

Trade creditors - 600

Taxation - 1,290

Proposed dividend - 1,400

- 3,990

Net current liabilities - 1,990

30,010

Long term liabilities - 12,000

18,010

Share capital 12,000

Revaluation reserve 3,500

Profit and loss 2,510

18,010

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 8

Note 1 Tangible fixed assets

FactoryMachinery

Total

£000 £000 £000

Cost at 31 March 1999 23,300 12,300 35,600

Additions - 2,700 2,700

Adjustment on revaluation 1,700 - 1,700

Cost at 31 March 2000 25,000 15,000 40,000

Depreciation at 31 March 1999 1,340 6,000 7,340

Charge for year 460 2,000 2,460

Adjustment on revaluation - 1,800 - - 1,800

Depreciation at 31 March 2000 - 8,000 8,000

Net book value at 31 March 2000 25,000 7,000 32,000

Net book value at 31 March 1999 21,960 6,300 28,260

Cost of sales

Factory running costs 1,200

Manufacturing wages 1,300

Materials consumed 1,600

4,100

This question was badly answered very few candidates produced a note forfixed assets and the formats were poor. Given that this is not one of the newtopics it was surprising how badly the question was answered.

19 (a) Required rate on the research project = 3+(8*.6) = 7.8%

Required rate on expansion = 3+(8*1.3) = 13.4%

(b) The total risk associated with an investment is not particularly importantin the context of a diversified portfolio. A significant proportion of the riskin most investments can be diversified away. In other words, factors suchas movements in exchange rates will have an adverse effect on someinvestments and a positive effect on others. The effect of investing in aportfolio is to reduce the overall volatility of the returns.

Risk can be separated into two components: systematic and unsystematic.Systematic risk is inherent in the political and economic environment andis common to all companies. For example, a change in energy prices willaffect all companies to some extent. Unsystematic risk is specific to thecompany. It encompasses a range of risks specific to the company such aschanges in market demand for its products, stability of industrialrelations, nature and location of its assets, and so on.

Subject 108 (Finance and Financial Reporting) — April 2000 — Examiners’ Report

Page 9

Systematic risk cannot be diversified away because it arises from factorswhich will have an effect on all companies. Thus, an increase in interestrates or oil prices is likely to have an adverse effect on all companies andwill depress returns from the market as a whole. Unsystematic risk canbe diversified away and, provided the investment is held in a properlydiversified portfolio, it can therefore be ignored.

It is possible that a highly speculative investment will not be affected bygeneral market conditions to any great extent. That means that it will nothave a high systematic risk. The volatility will, therefore, be due tounsystematic factors that can be diversified away. That, in turn, suggeststhat the investment may require a very low return.

(c) Company directors are in a rather different position from shareholders. Ashareholder can hold a diversified portfolio of investments and can,therefore, reduce the risks associated with a particular investment. Adirector will probably have only one principal employer and will,therefore, be motivated more by total risk.

This different perspective might be evidenced by a tendency to invest inrelatively safe projects. This is because a disaster might be rathercatastrophic for the board even though it would have relatively littleimpact on the shareholders.

Alternatively the board might be inclined to seek diversification for thecompany even though the shareholders can diversify for themselves.Given that diversification will have the effect of distracting managementfrom the core activities of the business, the overall effect will not be in theshareholders’ interests.

(d) One approach is to use the company’s own beta coefficient. That is onlyrelevant, however, if the project is subject to the same risks as thecompany as a whole.

Another approach is to use the beta of a company which is engaged in thesame line of business as the project.

A third possibility is to use historical data to estimate the betas ofindividual divisions or segments of the main company. These betas canthen be used as a surrogate for the coefficients of individual projectswhich fall within their scope.

This question was very badly done by most candidates. Many candidatescorrectly calculated the answer to part (a) and then demonstrated littleunderstanding of the theory required in the rest of the question. This is animportant area of finance and candidates should study the topic morecarefully.

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

14 September 2000 (pm)

Subject 108 — Finance and Financial Reporting

Time allowed: Three hours

INSTRUCTIONS TO THE CANDIDATE

1. Write your surname in full, the initials of your other names and yourCandidate’s Number on the front of the answer booklet.

2. Mark allocations are shown in brackets.

3. Attempt all 18 questions, beginning your answer to each question on aseparate sheet.

Graph paper is not required for this paper.

AT THE END OF THE EXAMINATION

Hand in BOTH your answer booklet and this question paper.

In addition to this paper you should have availableActuarial Tables and an electronic calculator.

Faculty of Actuaries108—S2000 Institute of Actuaries

108—2

For questions 1–4 indicate in your answer booklet which one of the answers A, B, C or Dis correct.

1 Which of the following statements is incorrect:

A Companies can issue ordinary shares below the par value.

B Ordinary shares normally offer a higher expected return than otherclasses of security.

C A company’s authorised share capital will be laid down in itsMemorandum of Association.

D An appropriate way of valuing ordinary shares is to find the present valueof the future dividend stream. [2]

2 One of G plc's employees developed a new product. This has just been patented.The development costs of this product were negligible, but the patent rights arealmost certainly worth many millions of pounds. Which accounting conceptwould prevent the company from recognising the value of this patent as a fixedasset in its balance sheet?

A Going concernB MaterialityC Money measurementD Prudence [2]

3 Which of the following is not true for a finance lease?

A The lease agreement has a primary period which covers all or most of theuseful economic life of the asset.

B The lessee is normally responsible for servicing and maintenance of theasset.

C The lease payments will appear in the profit and loss account as anexpense.

D The lessee records the leased asset as a fixed asset in its balance sheet.[2]

4 Which of the following best describes the effects of an increase in the riskcharacteristics of a project when evaluating its net present value?

A The discount rate increases and the net present value increases.B The discount rate increases and the net present value decreases.C The discount rate remains constant, but the net present value decreases.D The discount rate decreases and the net present value decreases.

[2]

108—3 PLEASE TURN OVER

In questions 5–10 one or more of the options may be correct. Answer in your booklet byselecting according to the following code:

A if I and II only are correctB if II and III only are correctC if I only is correctD if III only is correct

5 Companies who wish to raise finance by issuing sterling commercial paper haveto meet certain minimum standards. They must:

I be listed on the London Stock ExchangeII have a minimum level of net assets of £50mIII have a minimum level of share capital of £50m [2]

6 When choosing between two mutually exclusive projects, the internal rate ofreturn can give a misleading decision. Which of the following may be reasons forthis?

I Projects can have more than one rate of return.

II Internal rate of return ignores the rates of return available from otherprojects.

III Internal rate of return ignores the cost of capital. [2]

7 An increase in the value of a fixed asset due to revaluation would:

I increase the equity of a companyII make the balance sheet look strongerIII increase the profit of a company [2]

8 Which of the following would you normally expect to find in the external auditor’sreport to the shareholders:

I a certificate guaranteeing the truth and fairness of the financialstatements

II a statement that the directors were responsible for preparing the financialstatements

III a brief description of the work undertaken by the auditor prior to draftingthe report [2]

108—4

9 A company might carry out a rights issue at a deep discount:

I to reduce the share premium accountII to avoid misunderstandings by unsophisticated shareholdersIII to avoid having to pay underwriting costs [2]

10 Which of the following statements is true?

I Specific risk can be diversified away on a large, well spread portfolio.

II Systematic risk arises because of the volatility of the market as a whole.

III Diversification across a well diversified internationally-based portfolio willremove systematic risk entirely. [2]

11 Explain the shareholder value approach to project evaluation. [6]

12 X Plc is planning an expansion and requires £500,000 in order to do so. Thedirectors are unsure whether to finance this by debt or equity. Discuss thefactors they should take into account including any taxation implications. [8]

13 Describe the accounting standard setting process in the UK and explain whysuch a system is necessary. [8]

14 Describe the role life insurance offices play in the investment markets. [6]

15 Explain the taxation treatment of UK company dividends and also how frankedinvestment income is treated. [6]

16 Companies throughout the world raise finance by issuing Eurobonds. Describethe main characteristics of Eurobonds and briefly explain their popularity. [6]

108—5 PLEASE TURN OVER

17 The profit and loss accounts and balance sheets of two manufacturing companiesare shown below:

T Plc Y Plc£000 £000 £000 £000

Sales 600 700

Cost of sales 240 210

Gross profit 360 490

Selling expenses 54 84

Administrative expenses 60 35

114 119

Net profit 246 371

Taxation 64 100

182 271

Dividend 80 110

102 161

Retained profit b/fwd 106 230

208 391

T Plc Y Plc£000 £000 £000 £000

Fixed assets

Property - 500

Machinery 760 280

760 780

Current assets

Stock 48 26

Debtors 150 105

Bank 2 22

200 153

Current liabilities

Creditors (including Tax) 89 118

Net current assets 111 35

871 815

Share capital 663 424

Profit and loss 208 391

871 815

Compare these two companies in terms of their profitability and solvency.Explain which company appears to be the better managed in respect of each ofthese matters. You should support your answer with ratios. [20]

108—6

18 Z plc is a large, long established manufacturing company. The company isexpanding and the directors are keen to identify new ways in which they mightobtain the necessary finance. The finance director has warned that the companymust obtain most of this new funding from the sale of new shares. The companyhas borrowed very heavily in the past and the company's existing loanagreements require it to seek the permission of existing lenders before obtainingfurther debt.

Z plc is not quoted on the stock exchange. The family of the company’s foundersowns most of the company’s share capital. It is unlikely that these investors willbe able to invest the sums required to take advantage of the opportunities thatthe directors have identified. It has been suggested that the company might seeka stock exchange quotation.

(i) Explain the advantages and disadvantages to Z plc of issuing fresh sharecapital. [6]

(ii) Explain the advantages and disadvantages of obtaining a stock exchangequotation. [6]

(iii) Assuming that Z plc obtains a quotation, identify the most appropriatemethod by which the company might issue fresh share capital anddescribe the steps that are involved. Your answer should explain why youhave chosen this particular method. [8]

[Total 20]

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

September 2000

Subject 108 — Finance and Financial Reporting

EXAMINERS’ REPORT

Faculty of ActuariesInstitute of Actuaries

Subject 108 (Finance and Financial Reporting) — September 2000 — Examiners’ Report

Page 2

1 A2 C3 C4 B5 A6 C7 A8 B9 D10 A

Comment on Questions 1 to 10

There were no particular problems with the objective test questions, with most candidatesscoring a reasonable mark.

11 The shareholder value approach to project evaluation considers the net presentvalue of the project from the shareholder’s perspective.

In theory, investing in a positive NPV project will increase shareholders’ wealthby the amount of that NPV. In practice, this change will only occur if the marketis aware of the investment and agrees with management’s estimates of thepotential risks and rewards. It may be that the share price will not move in linewith expectations because the market is not convinced that the risk is justified oreven because the directors have withheld important information for the sake ofcommercial sensitivity.

The directors would essentially attempt to apply the same valuation models usedby outside analysts and advisers in an attempt to determine how theinformation that they intend to publish will impact the share price.

Comment on Question 11

Many candidates had clearly not understood that the shareholder value approach is aclearly defined technique for project evaluation. A large number of answers were clearlybased on a sensible guess as to what the technique might comprise.

12 The directors should consider the current level of gearing. If the company isalready heavily financed by debt then it will be difficult for the directors to justifyborrowing more.

The use of one form of finance can have implications for the risks, and thereforecosts, associated with the other. Issuing fresh debt will expose the existingshareholders to a greater risk of losing their investment if the company is forcedto default on its loans. This will mean that the cost of equity might increase.Issuing fresh equity creates a broader “buffer” between assets and liabilities forproviding lenders with collateral and that might reduce the cost of debt.

Subject 108 (Finance and Financial Reporting) — September 2000 — Examiners’ Report

Page 3

Debt finance is usually cheaper than equity and so the company should considerusing it wherever possible. The lower cost is partly because the debt holders aretaking much less of a risk when they purchase debt stock and are, therefore,willing to accept a lower rate of return.

The cost of debt is further reduced because interest is allowable as an expense fortax purposes, whereas dividends on shares is not.

It might be difficult to sell £500,000 of share capital without incurringdisproportionate issue costs. Raising debt can be rather more flexible. Thecompany could, however, get round this by issuing rather more than £500,000and using the additional sum raised to repay some of its existing debt.

Comment on Question 12

This question was generally answered well.

13 A body called the Financial Reporting Council (FRC) is responsible for thestandard setting process. The FRC concentrates on the management of theprocess and delegates the real work of developing standards to the AccountingStandards Board (ASB). The FRC’s contribution to the process is largelyrestricted to raising finance for the ASB and appointing its members.

The ASB develops documents called Financial Reporting Standards (FRSs).FRSs are intended to reduce the number of acceptable treatments for specificitems in the financial statements. One example of this is FRS 2 which deals withgroup accounts. This standard defines the relationship between holdingcompanies and their subsidiaries and establishes a standard approach to theirincorporation into consolidated financial statements.

A typical standard would be set in the following manner:

• ASB establishes a working party.• Working party drafts an exposure draft (ED).• ED published and comments invited.• Interested parties may ‘lobby’ in defence of their interests.• There may be one or more rounds of revision to the ED.• FRS issued.

This process involves considerable openness, but it also creates the risk of thestandards being influenced by the actions of lobbyists.

This system is necessary because there have been many controversies over thecorrect preparation of financial statements. These have led to problems with thecredibility of the profession. Standards also reduce processing and interpretationcosts for users because they can become more familiar with the specifictreatments adopted by all companies for particular items.

Subject 108 (Finance and Financial Reporting) — September 2000 — Examiners’ Report

Page 4

Comment on Question 13

Many candidates appeared to be writing everything that they knew about accounting inthe hope that this related to the question. The most common error was to write a detailedexplanation of the concepts underlying financial accounting, with no reference whatsoeverto the regulatory framework referred to in the question.

14 Life insurance companies are major institutional investors and, collectively, areamongst the very largest institutions.

The companies collect cash from policy holders and invest this in the long term.Policy holders will normally be offered the expectation of a future bonus based onthe profits of the company. This has the effect of requiring insurance companiesto seek out investment opportunities which both offer the prospect of maintainingthe real purchasing power of their deposits and also a realistic expectation ofcapital growth.

Insurance companies are also subject to a number of regulatory constraints onthe nature of their investments. These are partly attributable to the need tomaintain solvency margins in accordance with DTI regulations.

Comment on Question 14

This question was generally answered well.

15 Franked investment income (FII) is the grossed-up value of dividends paid by UKcompanies. The cash value of the dividend received is grossed up by the additionof a tax credit which is currently 10%.

The tax credit is a reflection of the fact that the dividend has been paid out ofprofits which have already been subject to corporation tax. Individuals who arebasic rate taxpayers will not normally pay any further tax on their FII. The FIIis added to their taxable income, but the tax credit will cancel the additional taxthat this would involve. Non taxpayers cannot, however, recover the tax creditwhich has been notionally withheld by the company. Higher rate taxpayers mayhave to pay some additional tax in order to satisfy their obligation to pay tax atthe higher rate.

Companies must also include their FII in their tax computation and will be liableto tax on it. This income will, however, be taxed at a flat rate of 20% regardlessof the rate of corporation tax to which the company is subject.

Comment on Question 15

This question was generally answered well.

Subject 108 (Finance and Financial Reporting) — September 2000 — Examiners’ Report

Page 5

16 Eurobonds are bonds which are issued outside of the company’s domicile. Thereis a thriving market in such arrangements. The fact that the stocks are tradedin a country in which the host government has no particular interest can meanthat they are not subject to any legal or tax regulations. This lack of regulationcan reduce issuing costs and the possibility of freedom from taxes can evenreduce the coupon rates of debts. Eurobonds tend to be traded through banksrather than recognised stock exchanges.

Eurobonds can be issued in almost any currency. They are redeemed at par withcoupon payments throughout the term of the bond. Almost all Eurobonds areunsecured. Eurobonds are bearer documents.

Most Eurobonds offer a fixed coupon rate, although some offer a variable couponrate.

Comment on Question 16

This question was generally answered well.

17

T plc Y plc

ROCE 246 28 % 371 46 %

871 815

Gross profit % 360 60 % 490 70 %

600 700

Selling / sales 54 9 % 84 12 %

600 700

Admin / sales 60 10 % 35 5 %

600 700

Current ratio 200 2.2 :1 153 1.3 :1

89 118

Acid test ratio 152 1.7 :1 127 1.1 :1

89 118

Y plc is the more profitable company because it has a higher return on capitalemployed. It appears to have achieved a higher return by virtue of three factors:

• It can generate a higher gross profit from every £ of sales. Either it is sellingat a higher margin or it can obtain goods at a lower cost price.

Subject 108 (Finance and Financial Reporting) — September 2000 — Examiners’ Report

Page 6

• Its sales appear to be supported by a higher spend on advertising. This hasenabled it to achieve higher sales despite having higher selling prices.

• It manages to spend less on administration.

Y plc also appears to have better managed working capital. At first glance, T plchas a “textbook” current ratio of 2:1. The company has a very high acid testratio, which appears to be due to very slow turnover of debtors. This means thatthe company has a great deal of finance tied up in non-productive assets. Theseare not necessarily available to meet short-term commitments.

Comment on Question 17

This question was generally answered well.

18 (i) Share capital is the most flexible form of finance. The payment ofdividend is entirely at the discretion of the directors. If the dividends arewithheld for any reason then the shareholders have no direct sanctionsagainst the company, other than the right to sell their shares on the openmarket.

Issuing fresh share capital also makes it easier to raise further finance byborrowing. This is because lenders are usually keen to see the companymaintain a sensible relationship between debt and equity. If the companyfails then the lenders must be repaid in full before the shareholdersreceive anything. If the shareholders have financed a large proportion ofthe share capital then this protects the lenders from the loss of theirprincipal.

Share capital tends to be a rather expensive form of finance. This isbecause shareholders bear a much higher risk than lenders. They have tobe rewarded with a substantial return in order to motivate them to acceptthis level of risk. In addition, the company does not receive any tax reliefon dividends whereas loan interest is tax deductible.

Issuing additional share capital will also tend to dilute the sense ofownership and control enjoyed by the present shareholders. They mightbe willing to forego the opportunity to expand if doing so would makethem accountable to outside shareholders.

(ii) A stock exchange quotation would provide a ready market for the sale ofshares. This would make it easier for the company to sell fresh shares onthe open market. It would also offer existing and future shareholders ameans of disposing of their shares.

The fact that an investment in the company could be liquidated moreeasily would make it a more attractive prospect, thereby reducing the costof finance.

Subject 108 (Finance and Financial Reporting) — September 2000 — Examiners’ Report

Page 7

The availability of a ready market means that market forces willdetermine an objective share price. This can be a useful piece ofinformation for shareholders and directors alike. There can be taxproblems associated with the gift of shares that cannot be easily valued.Knowing the share price makes it easier to calculate the cost of capital.

The stock exchange imposes strict regulations on the behaviour of quotedcompanies. The fact that a company is willing to accept this disciplineprovides further confidence for both shareholders and lenders and soshould have the effect of further reducing finance costs.

There are, of course, substantial transaction costs associated withobtaining a listing. Apart from professional fees and other direct costs, agreat deal of management time will be taken up.

The fact that the company’s shareholders can sell their shares easily onthe market might encourage them to take a short-term outlook. Thiscould make the company vulnerable to take-over bids.

(iii) The company ought to consider an offer for sale. This would involveselling new shares to the general public at a fixed price which wasdetermined by the directors. The advantage of this is that it raisesadditional capital at the same time as introducing the company to thestock exchange.

There is relatively little risk of this type of transaction going wrongbecause the company would sell the shares via an issuing house. Theissuing house would act as an intermediary between the company and thepublic. In the first instance, the issuing house would purchase the sharesfrom the company and then resell them to the public. This means thatthe company knows in advance how much the issue will generate becausethe issuing house is responsible for any lack of demand and will be leftholding any unsold shares.

The use of an issuing house also provides the company with a source ofexperience and advice in the selection of other professionals and in thecoordination of their various efforts.

Well before the offer for sale, the company will engage an issuing house.The issuing house will try to generate interest in the launch, e.g. bypublicising positive news that might be picked up by the financial press.

In the weeks before the launch, the issuing house will advise on the pricethat should be set. This will normally be a reasonably conservativefigure, if only because a higher issue price would involve a greater risk forthe issuing house and that might result in higher fees and premia.

The company is required to publish a prospectus, which is a formaldocument required by the stock exchange. This is a detailed documentcontaining a wealth of historical and forecast information, both financialand non-financial. This information will also be supported by a number of

Subject 108 (Finance and Financial Reporting) — September 2000 — Examiners’ Report

Page 8

assurances from the company’s external auditors. The prospectus willalso state the offer price for the shares.

The prospectus will be reproduced in at least one national newspaper andmay be distributed in other ways.

Anyone wishing to purchase shares can do so during the periodimmediately after the publication of the prospectus. Hopefully, the offerprice was set at a level that would encourage investment and the issuewill be over-subscribed. This means that the issuing house will have todecide on the most appropriate basis for the allocation of shares.

Finally, the successful applicants will receive letters of acceptance.Official trading on the stock exchange can take place on the day after theacceptance letters are posted.

Comment on Question 18

This question tended to be answered well in some parts, but not others. Parts (i) and (ii)were generally answered well, although there was very little attempt to relate answers tothe facts of the scenario. Part (iii) tended to generate a checklist of mechanisms for issuingshares instead of recommending one particular technique, as required by the question.

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

5 April 2001 (pm)

Subject 108 ó Finance and Financial Reporting

Time allowed: Three hours

INSTRUCTIONS TO THE CANDIDATE

1. Write your surname in full, the initials of your other names and yourCandidateís Number on the front of the answer booklet.

2. Mark allocations are shown in brackets.

3. Attempt all 18 questions. From question 11 onwards begin each answer on aseparate sheet.

Graph paper is not required for this paper.

AT THE END OF THE EXAMINATION

Hand in BOTH your answer booklet and this question paper.

In addition to this paper you should have availableActuarial Tables and an electronic calculator.

! Faculty of Actuaries108óA2001 ! Institute of Actuaries

108 A2001ó2

For questions 1ñ10 indicate in your answer booklet which one of the answers A, B, C or Dis correct.

1 C plc is to make a 3 for 5 rights issue at 120p. If the price of the shares on theday the allotment letters were posted was 140p, what price would you expect forthe shares ex-rights when dealings commence?

A 127.5pB 130pC 132.5pD 140p [2]

2 A key difference between the net present value technique and the internal rate ofreturn technique for capital budgeting is:

A that the net present value is easier to calculateB that they use different cash flowsC that they have different reinvestment rate assumptionsD that they are relevant to the shareholders [2]

3 Which of the following would NOT be included in a firmís capital structure?

A retained earningsB dividendsC capital surplusD convertible debentures [2]

4 Which of the following is NOT a current asset?

A stockB creditorsC debtorsD cash [2]

5 Which of the following is NOT a method of short term borrowing?

A commercial paperB bill of exchangeC factoringD leasing [2]

108 A2001ó3 PLEASE TURN OVER

6 Which of the following are limited companies NOT required to produce as aresult of the Companies Act?

A chairmanís reportB directorsí reportC balance sheetD auditorís report [2]

7 Which of the following is NOT a method of bringing a security to listing?

A an offer for saleB a scrip issueC an offer for subscriptionD an introduction [2]

8 A manufacturing companyís cash balances have run low. Which of the followingwould increase cash in the short term?

A press debtors for prompter paymentB pay creditors more quicklyC encourage sales staff to sell moreD delay the acquisition of a piece of manufacturing equipment [2]

9 Which of the following statements is NOT true of self-administered pensionfunds?

A a typical fund invests mainly in index linked giltsB most existing schemes are defined benefit schemesC all the schemes are responsible for their own investment strategyD almost all private sector schemes are funded [2]

10 Which of the following is NOT an intangible asset?

A development costsB patentsC investmentsD goodwill [2]

11 Explain the differences between an investment trust and a unit trust. [8]

12 Explain why a company would seek a Stock Exchange quotation. [8]

108 A2001ó4

13 Describe the different reports the external auditor can give when it is impossibleto express an unqualified opinion. [6]

14 Ordinary shares are the most important form of financial instrument used by UKcompanies.

(i) Describe the main characteristics of ordinary shares. [6]

(ii) Explain why ordinary shares are more marketable than loan capital. [2][Total 8]

15 Explain why pension funds have special regulations governing the form andcontent of their financial statements. [4]

16 Explain why a company might issue convertible securities instead ofstraightforward debt or equity. [6]

17 PQR plc is a pharmaceutical company. The companyís research department hasidentified a compound that can cure the common cold without any side effects.Unfortunately, the manufacture of this compound requires the company to investheavily in a high technology factory which will use a number of new techniques,some of which are unproven. The company will also need to recruit and retainthe services of a number of eminent scientists, each of whom is both vital to theproject and would be irreplaceable.

Financing this project will require the company to borrow heavily. The companyis unlikely to survive as an independent entity if it invests in this project and itfails. The directors have been advised that there is at least a 50% chance of acatastrophic failure.

The project has a beta of 0.5. The risk free rate is 3% and the equity riskpremium is 8%. The project offers an estimated return of 24%.

REQUIRED:

(a) Calculate the required rate of return for the project. [2]

(b) Explain how investing in this project would affect the wealth of PQR plcísshareholders. [5]

(c) Explain how an apparently risky project can have a relatively lowrequired rate of return. [7]

(d) Explain whether you believe that the directors of PQR plc will invest inthe project. [6]

[Total 20]

108 A2001ó5

18 MNO plc has a number of different business interests. The directors of MNO areinterested in identifying managers for promotion to senior positions. As part ofthis process, they are comparing the performance of two autonomous divisions,both of which purchase goods in bulk for resale to small retailers. Each divisionis responsible for a different part of the country, but is otherwise engaged in thesame line of business. The directors have prepared the following summaryfinancial statements from the companyís bookkeeping records:

Easterndivision

Westerndivision

Profit statements (year ended 31 December 2000) £000 £000

Sales 800 1,400 Cost of sales 320 490 Gross profit 480 910 Advertising and distribution 80 196 Administration 64 56 Operating profit 336 658 Interest 24 11 Net profit 312 647

Balance sheets (as at 31 December 2000) £000 £000

Fixed assets 1,000 1,200

Current assets Stock 51 57 Debtors 80 222 Bank 10 7

141 286 Current liabilities

Creditors 48 53 Working capital 93 233

Long term loans 200 100 893 1,333

Capital 893 1,333

(a) Compare the performance of the two divisions in terms of theirprofitability, liquidity and management of stock, debtors and creditors.Your answer should be supported by relevant ratios, although theseshould form only part of your analysis. [14]

(b) Describe the limitations of your analysis in (a), explaining why thedirectors should seek additional information before making a finaldecision about the suitability of either divisional management team forpromotion. [6]

[Total 20]

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

April 2001

Subject 108 ó Finance and Financial Reporting

EXAMINERSí REPORT

! Faculty of Actuaries! Institute of Actuaries

Subject 108 (Finance and Financial Reporting) ó April 2001 ó Examinersí Report

Page 2

Suggested answers:

1 C

2 A

3 B

4 B

5 D

6 A

7 B

8 A

9 A

10 C

Generally all Multiple Choice Questions were answered correctly with the majority ofcandidates scoring over 16.

11 Investment trusts are companies, most of which are listed on the StockExchange. Shares in investment trusts can be purchased and sold as for anyother quoted company.

Unit trusts are not companies, but are trusts in the strict legal sense. They cannot,therefore, be quoted on the Stock Exchange. Units can only be bought from and sold tothe management company which organises the trust.Investment trusts tend to specialise in investments in other companies, althoughsome invest in gilts, property and overseas companies.Unit trusts are far more heavily constrained and regulated in terms of what theycan invest in and they tend to restrict their investments to quoted securities.Investment trusts can borrow in addition to raising funds from investors. Unittrusts must rely on the sale of units for finance. This means that investmenttrusts can offer their shareholders the benefits of gearing whereas unit trustscannot.

Units in unit trusts are normally priced by taking the market value of the trustísunderlying assets and dividing by the number of units. The management chargesapplied for running the fund are paid for by an initial charge levied on the fundinvested. Shares in investment trusts are normally worth less than the marketvalue of the assets divided by the number of shares. The main reason for this is

Subject 108 (Finance and Financial Reporting) ó April 2001 ó Examinersí Report

Page 3

that the managers take an annual fee for their management charge and this hasthe effect of depressing the value of the shares relative to their underlying assets.

This question was answered very well with most candidates scoring very highmarks

12 A quotation will help to raise capital. If the company is quoted then it will be able tosell shares to a wide market and raise large sums cheaply. This is because thequotation will provide a free secondary market in the companyís shares.Providers of debt will lend more happily to a quoted company as they know that thecompany must comply with the Stock Exchange requirements on an ongoing basis.Shareholders will also benefit from the fact that the shares will have a readilyobservable market price which may be useful for tax purposes and also for portfoliomanagement. These advantages will also help the company to raise funds.The ease with which shares in quoted companies can be traded means thatshareholders have an easy exit route if they ever decide to sell their investment.The fact that they can do so means that they will feel far more secure when buyingshares.The ready availability of a market price means that the shares are far moreacceptable to employees if they are granted as part of a share option scheme. It willbe possible to attribute a value to the shares or options received.The fact that the shares are listed will also make them more readily available touse as the purchase consideration in a takeover situation. Shareholders of thetarget company will have a far clearer impression of the relative values of theshares being offered compared with the ones that they already hold.

Excellent answers by many candidates. Candidates who had studied the corereading found this question straightforward.

13 The most common form of qualified opinion is the ìexcept forî form. This isappropriate when the auditor has encountered a material disagreement over thefinancial statements or has been subject to a material uncertainty because thescope of the audit work has been restricted. The except for makes it clear that thefinancial statements give a true and fair view ìexcept forî the changes that wouldhave been necessary in order to correct for the disagreement or in response to theresolution of the uncertainty.

There are two more extreme forms of qualified opinion. Adverse opinions are usedwhen the auditor disagrees with the impression created by the financial statementsso violently that s/he is of the opinion that the financial statements do not give atrue and fair view. Disclaimers of opinion are given when the auditor is faced withsuch fundamental uncertainty that it is impossible to tell whether the financialstatements give a true and fair view. In this latter case, the auditor refuses toexpress an opinion.

In each of the cases described above, the auditor will describe the problems thathave led to the need for a qualified opinion and will make their implications clear

Subject 108 (Finance and Financial Reporting) ó April 2001 ó Examinersí Report

Page 4

to the readers. Then the report will clearly state the opinion, making use of one ofthe prescribed forms of qualification.

This question was the most poorly answered in the paper, clearly most candidateshad ignored this in the core reading. I would emphasis that all topics in the corereading are likely to be examined and it really pays to study all the areas.

14 Ordinary shareholders bear the risks and rewards of ownership. They are last tobe repaid in the event that the company fails. They may also receive little or nodividend at difficult times. On the other hand, they will also be entitled to all ofthe profits after tax and any preference dividend. They will normally be the onlyones entitled to vote at general meetings.

Ordinary shareholders will normally have a relatively volatile return from theirinvestment, but this will be compensated for by the possibility of unrestrictedopportunity for capital growth. If the company is a massive success then the shareholdersmay find that their stake increases in value beyond all recognition.

Ordinary shares are backed by real trading assets. This means that they offer ameasure of protection against inflation. This is reflected by the fact that, onaverage, ordinary shares have given a higher long term return than any otherinvestment.

Ordinary shares are normally irredeemable. Indeed, there are provisions that aredesigned to ensure that shareholders cannot have their capital returned.

Shareholders normally receive a dividend, although the amount of this will be atthe discretion of the directors. The amounts will be affected by the companyísperformance and also by the boardís desire to retain funds for future expansion.Ordinary shares tend to be marketable because there is an active secondarymarket in the shares of quoted companies. This is assisted by the fact that theshares tend to be issued in large, homogenous blocks, making the creation of amarket worthwhile. Other instruments are more likely to be issued in smaller,more fragmented tranches and so there is less scope for offering a liquidsecondary market.

Again answered well.

15 Pension funds offer a vehicle for investment, in exactly the same manner as anyother form of commercial entity. There are, however, significant features whichmakes their accounting principles different:

• Pensioners have far less scope for diversification in their pensions than in anyother type of investing activity. This means that they have to be keptinformed about the stewardship of their fund to reduce the risk of them beingleft exposed to the loss of their pensions.

Subject 108 (Finance and Financial Reporting) ó April 2001 ó Examinersí Report

Page 5

• Pension funds have very long term commitments to pensioners and mustdemonstrate that they are being managed for the long term.

• The loss of a pension may be far more serious than the loss of any other typeof investment. Pensioners may be far more vulnerable because they areunlikely to have the capacity to earn sufficient income to make up for anyloss.

These factors come together to create a need for members of a pension fund toreceive adequate accounting information to enable them to measure thestewardship and performance of the fund. The readers may be relativelyunsophisticated and require even greater protection than that offered to the readersof the financial statements of limited companies.

Most points mentioned by candidates , however little mention of accountinginformation in most answers.

16 Convertibles are attractive to issuers when it is felt that the price of the ordinaryshares is abnormally low. This might happen in the case of a start-up or a businesswhich is dealing with considerable temporary uncertainty. Issuing fresh sharesunder such circumstances would dilute the equity of existing shareholders. Therewill still be some dilution when the debentures are converted, but this willhopefully be less than would arise if the shares had been issued when the companywas at a transitional stage.

The company has to be reasonably confident that the share price is onlytemporarily depressed, otherwise the debenture holders would not convert. Inthat case the company would have to find cash in order to meet the redemption.Convertibles are essentially a means of raising equity during difficult periods. Theycan be preferable to straight loan stock because they are self-liquidating and can beissued at a slightly lower coupon rate. They might attract a particular group ofinvestors who are looking for a guaranteed short term income plus the possibility ofa capital gain at a later date.

This question was poorly answered, many candidates described convertibles butwere at a loss to suggest why companies might wish to issue them. It would bebeneficial if candidates could apply the core reading to different situations ratherthan simply memorising facts.

17 (a) The required rate of return is risk free rate + (beta x equity risk premium).Required rate of return = 3% + (0.5 x 8%) = 7%.

(b) Investing in this project would increase the shareholdersí wealth. Therequired rate of return, taking risk into account, is only 7%. The projectactually offers 24%. This means that the project has a positive net presentvalue (NPV) and the value of their shares will increase by the NPV of thisproject.The increase will, however, only occur if the stock market has sufficientinformation to form a view on its likely outcome. It must also agree withmanagementís evaluation of the project. If shareholders are less optimisticthan the board then the share price will not rise by as much.

Subject 108 (Finance and Financial Reporting) ó April 2001 ó Examinersí Report

Page 6

(c) The risks associate with investments are split into those that can bediversified away and those that cannot. The risks that can be diversifiedaway can be ignored because any rational investor will hold a broad portfolioof assets. Some of the investments will do badly but this will be compensatedby the fact that others will do well. Over the portfolio as a whole the investorshould expect to have a return that tends towards that offered by themarket as a whole.

If the portfolio has been well constructed, the only variation from marketreturns should be because of any deliberate structuring of the portfolio toleave the shareholder exposed to more or less of the risks faced by themarket as a whole. These risks cannot ever be diversified away because theyaffect all companies to some extent or another. For example, an increase ininterest rates will push down most share prices to some extent and so allinvestments will suffer.

Looking at PQR plcís project from the shareholdersí perspective, many of therisks are very specific to the investment. The risk that the technology willnot work or that the staff will leave can be countered by investing in asufficient spread of other securities to cancel the highs and lows on thisproject with those obtained from others. The project might not beparticularly sensitive to factors that affect the market as a whole and so itneed not require a high rate of return.

(d) In theory the directors should only be concerned with the shareholdersíwealth. That means that they should invest in this project because it has apositive NPV. The fact that it might threaten the companyís existence wouldnot matter because their portfolios will include some companies that will failand others that will thrive.

The directors cannot, however, diversify in quite the same manner. Most oftheir income will come from this one company and their personalreputations will be associated with its success or failure. They will,therefore, have a great deal to lose if they put the shareholdersí interestsfirst. The directors might also feel a moral responsibility towards the otheremployees to ensure that the company survives in order to keep them inemployment.

The directors might also be concerned that many investors will notappreciate the importance of planning their investments on a portfolio basis.They might criticise the directors for taking a risk that is, in fact, justified bythe returns offered. If they do not accept that many of the risks are specificto the project and can be diversified away they might accuse the directors ofmismanagement.

Part a was well answered , the remaining parts of the question were poorlyanswered, most candidates had learned facts but found it difficult to applythese to practical situations.

Subject 108 (Finance and Financial Reporting) ó April 2001 ó Examinersí Report

Page 7

18 (a)Eastern Western

Return on capital employed 312+24893+200

31 % 647+111333+100

46 %

Profit margin 336800

42% 6581,400

47%

Gross profit % 480800

60 % 9101400

65 %

Advertising I sales 80800

10% 1961400

14%

Administration / sales 64800

8% 561400

4%

Asset turnover 8001000

0.8 times 14001200

1.2 times

Current ratio 14148

2.9 times 28653

5.4 times

Quick ratio 141 ñ5148

1.9 times 286-5753

4.3 times

Stock turnover 51 x365 320

58 days 57 x 365 490

42 days

Debtors turnover 80800

37 days 2221400

58 days

Creditors turnover 48320

55 days 53490

39 days

Western has a higher return on capital employed. That is enough in itself toindicate that it is the more profitable of the two companies.Western appears to have spent more on advertising with a view to seeking ahigher selling price per unit. This may have contributed to a higher overallprofitability. The company has also managed to save considerably onadministration costs, spending only 4% of turnover as opposed to 8%. Finally,Western has managed to obtain a higher asset turnover.Western has also managed liquidity more effectively. The company has leanercurrent and quick asset ratios. Eastern appears to be heavily over invested inunproductive assets.Finally, Western also appears to have a better strategy for the management ofstock, debtors and creditors. It is turning stock over rapidly, thereby managingcash flows. It has managed to offer debtors a reasonable period of credit, possiblyjustifying its premium pricing policy. It is also paying creditors within a realisticperiod, thereby maintaining its credit rating.

(b)There is always a risk that accounting figures are not comparable. Theaccounting policies could be different or the companiesí accountants could havemade different estimates and assumptions.Western is also 50% larger in terms of turnover. That might make the companyappear to be more efficient, when it is actually enjoying economies of scale. Theseeconomies could mask an underlying weakness in management.There could be other structural reasons why Western enjoys greater success. Thecompany could, for example, sell to a different, more profitable market segment.Barriers to entry might make it impossible for Eastern to compete directly.

Well answered by most candidates.

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

11 September 2001 (pm)

Subject 108 ó Finance and Financial Reporting

Time allowed: Three hours

INSTRUCTIONS TO THE CANDIDATE

1. Write your surname in full, the initials of your other names and yourCandidateís Number on the front of the answer booklet.

2. Mark allocations are shown in brackets.

3. Attempt all 19 questions. From question 11 onwards begin each answer on aseparate sheet.

Graph paper is not required for this paper.

AT THE END OF THE EXAMINATION

Hand in BOTH your answer booklet and this question paper.

In addition to this paper you should have availableActuarial Tables and an electronic calculator.

! Faculty of Actuaries108óS2001 (15.2.01) ! Institute of Actuaries

108 S2001ó2

For questions 1ñ10 indicate in your answer booklet which one of the answers A, B, C or Dis correct.

1 Which of the following is subject to taxation in the UK?

A social security benefitsB winnings from gamblingC profits from an ISAD dividends from a UK company [2]

2 Which of the following statements is NOT true of investment trusts?

A an investment trust is a companyB they raise equity and debt capitalC they never invest in the shares of other UK companiesD most investment trusts are listed on the stock exchange [2]

3 When a firm announces a two-for-one scrip issue investors should expect that, (inthe absence of other new information):

A earnings per share will fall but the stock price will remain the sameB the stock price will fall but the earnings per share will remain the sameC both the earnings per share and the stock price will remain the sameD both the earnings per share and the stock price will fall [2]

4 The nominal value of a bond is received by the bondholder:

A at the time of purchaseB annuallyC whenever coupon payments are madeD at maturity [2]

5 The net present value method of capital budgeting assumes that cash flows arereinvested at:

A the firmís cost of capitalB the firmís dividend yieldC no rate ó they are not reinvestedD the rate of return of the project [2]

108 S2001ó3 PLEASE TURN OVER

6 The payback method can lead to the wrong decision being made because:

A it ignores income beyond the payback periodB the payback period is difficult to calculateC the returns in later years are uncertainD of the emphasis placed on the interest factor [2]

7 Which of the following changes in working capital will result in an improvementin a companyís net cash inflow from operating activities?

A increase in creditorsB increase in stockC increase in debtorsD decrease in other current liabilities [2]

8 The following ratios were calculated from the financial statements of G plc, amajor manufacturing company.

Stock turnover 12 daysDebtors turnover 42 daysCreditors turnover 46 days

For how long, on average, does G plc have cash tied up in any particular piece ofstock?

A 8 daysB 12 daysC 54 daysD 100 days [2]

108 S2001ó4

9 H plcís summary financial statements are as follows:

Profit and loss accountFor the year ended 31 March 2001 £000

Profit before tax and interest 2,000Interest (300)Taxation (500)

1,200Dividend (700)Retained for year 500Balance brought forward 4,700Balance carried forward 5,200

Balance sheetAs at 31 March 2001 £000

Total assets less current liabilities 35,200Long term loans (3,000)

32,200

Share capital 27,000Profit and loss account 5,200

32,200

Calculate H plcís return on capital employed.

A 3.7%B 4.3%C 5.7%D 7.4% [2]

10 Which of the following statements is NOT true of double taxation relief (DTR)?

A The UK has a double taxation agreement with many countries.

B The maximum offset is the rate of tax that would have been paid in theUK.

C DTR is available on revenue of a capital nature.

D DTR is only available on income received from abroad. [2]

11 Explain why the net present value criterion is superior to other methods ofinvestment appraisal. [6]

108 S2001ó5 PLEASE TURN OVER

12 Explain the influence of a central bank (e.g. the Bank of England) on thegovernment bond market. [6]

13 Explain how a companyís capital structure might influence its share price. [6]

14 Describe the role building societies play in investment markets. [4]

15 Discuss the interests of four user groups of financial statements and explain whysome of the groupsí interests may conflict. [8]

16 Explain how a companyís UK corporation tax liability is calculated and when itmust be paid. [6]

17 Describe the factors that must be determined when selecting a companyísdepreciation policy. [4]

18 D plc is in the process of making a 1 for 4 rights issue. The rights letters havejust been sent to shareholders. The company currently has 20m £1 shares inissue and the current market price is £4.50 per share.

The rights letter gives shareholders the right to buy their new shares for £3.50each. D plc plans to use the cash raised to build a major extension to its factory,thereby doubling production capacity.

The finance director has received an angry letter from a shareholder. Theshareholder complains that he cannot afford to invest in new shares. He is,therefore, likely to suffer a loss because the fact that the market will be floodedwith cheap shares will almost certainly decrease the value of his holding.

Required:

(a) Calculate the value at which the share price is likely to settle after therights issue. [2]

(b) Explain whether the shareholder's complaint is justified with particularreference to the difference between the rights price and the currentmarket price. [4]

(c) Explain whether the share price is likely to settle at the figure calculatedin (a) above. [4]

(d) Discuss the advantages and disadvantages of financing the extension byissuing loan stock. [5]

(e) Discuss the advantages and disadvantages of financing with a commercialmortgage. [5]

[Total 20]

108 S2001ó6

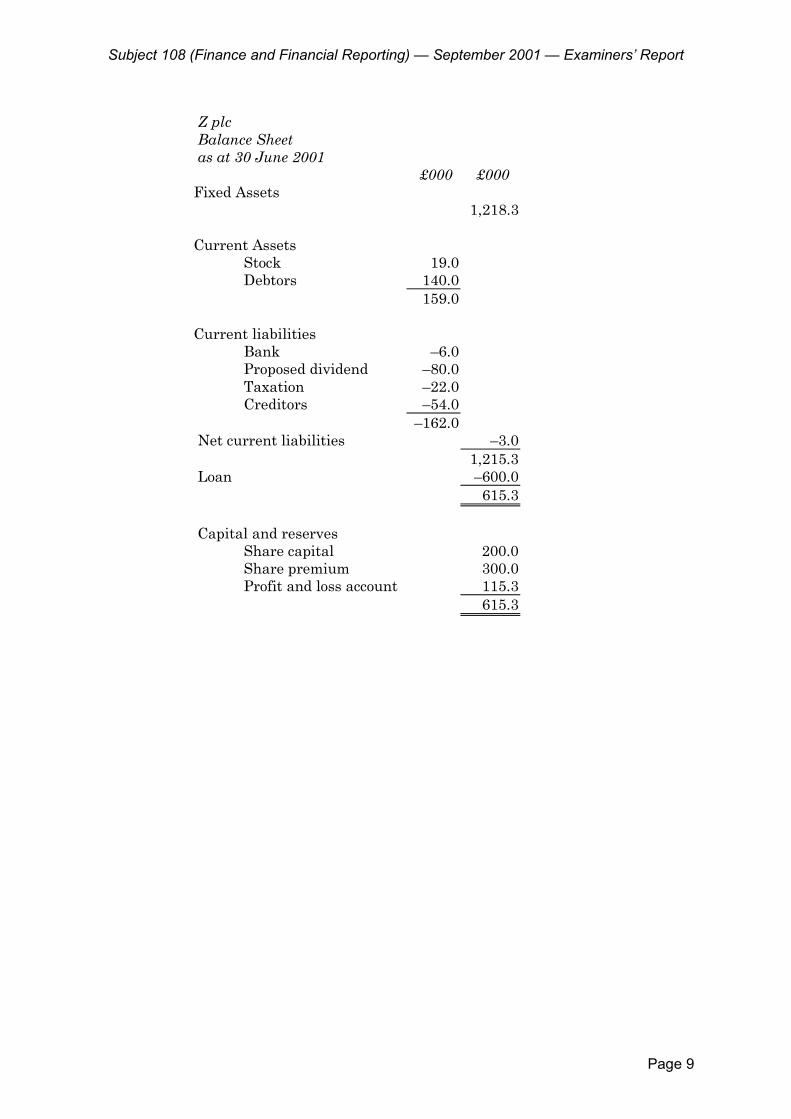

19 The following information has been extracted from the bookkeeping records of Zplc:

Z plc

Trial Balance as at 30 June 2001.

£000 £000 Administrative expenses 25 Advertising 200 Bank 6 Creditors 54 Debtors 140 Interest 120 Land and Buildings ó cost 983 Land and Buildings ó depreciation 45 Loan 600 Manufacturing overheads 35 Plant and Machinery ó cost 550 Plant and Machinery ó depreciation 150 Profit and loss as at 1 July 2000 180 Purchases 450 Sales 1,200 Share capital 200 Share premium 300 Stock as at 1 July 2000 18 Wages ó administrative staff 44 Wages ó distribution staff 30 Wages ó manufacturing 140

2,735 2,735

Notes:

(i) Closing stock was counted at the year end and was valued at £19,000.

(ii) Depreciation is to be charged on the following bases:

Factory ó 2% of costPlant and Machinery ó 25% of reducing balance

(iii) The directors have decided to pay a dividend of £80,000 for the year.

(iv) The corporation tax charge has been estimated at £22,000 for the year.

(a) Prepare Z plcís profit and loss account for the year ended 30 June2001 and its balance sheet as at that date. These should be in aform suitable for publication insofar as this is possible from theinformation provided. [15]

(b) Comment on any notable features of Z plcís dividend policy, asrevealed by your answer to (a) above. [5]

[Total 20]

Faculty of Actuaries Institute of Actuaries

EXAMINATIONS

September 2001

Subject 108 ó Finance and Financial Reporting

EXAMINERSí REPORT

! Faculty of Actuaries! Institute of Actuaries

Subject 108 (Finance and Financial Reporting) ó September 2001 ó Examinersí Report

Page 2

Examinerís Comments

Questions 1 to 10There were no particular problems with the objective test questions, with mostcandidates scoring a reasonable mark.

Question 11The only recurring problem with this question was a slight failure to answer thequestion. Many candidates described the shortcomings of various methods withoutexplaining whether they had been dealt with by net present value.