111 chapter 17: domestic and international dimensions of monetary policy 1 econ 151 – principles...

TRANSCRIPT

111

Chapter 17: Domestic and International Dimensions of Monetary Policy

1

ECON 151 – PRINCIPLES OF MACROECONOMICS

Materials include content from Pearson Addison-Wesley which has been modified by the instructor and displayed with permission of the publisher. All rights reserved.

What’s So Special About Money? The demand for money, what people wish to

holdPeople have certain motivation that causes them to

want to hold money balances.There is a demand for money by the public,

motivated by several factors. Transactions demand Precautionary demand Asset demand

17-2

What’s So Special About Money? (cont'd) Money Balances

Synonymous with money, money stock, and money holdings

Transactions Demand

Holding money as a medium of exchange to make payments

The level varies directly with nominal GDP.

17-3

What’s So Special About Money? (cont'd) Precautionary Demand

Holding money to meet unplanned expenditures and emergencies

Asset Demand

Holding money as a store of value instead of other assets such as certificates of deposit, corporate bonds, and stocks

17-4

What’s So Special About Money? (cont'd) The demand for money curve

Assume the amount of money demanded for transactions purposes is proportionate to income

Precautionary and asset demand are determined by the opportunity cost of holding money (the interest rate).

17-5

Figure 17-1 The Demand for Money Curve

17-6

The Demand for Money Curve

17-7

Quantity of Money

Inte

rest

Rat

e

Md

• When the interest rate rises the opportunity cost of holding money increases and the quantity of money demanded falls

• The location of Md is determined by the level of income

Q1

Br2

Ar1

Q2

The Tools of Monetary Policy

The Fed seeks to alter consumption, investment, and aggregate demand as a whole by altering the rate of growth of the money supply.

17-8

The Tools of Monetary Policy (cont'd) The Fed has three tools at its disposal as part

of its policymaking action.

Open market operations

Discount rate changes

Reserve requirement changes

17-9

The Tools of Monetary Policy (cont'd) Open market operations

Fed purchases and sells government bonds issued by the U.S. Treasury

At first, there is some equilibrium level of interest rate (and bond prices).

An open market operation must cause a change in the price of bonds.

17-10

Figure 17-2 Determining the Price of Bonds, Panel (a)

17-11

Contractionary Policy• Fed sells bonds• Supply of bonds increases• Bond prices fall

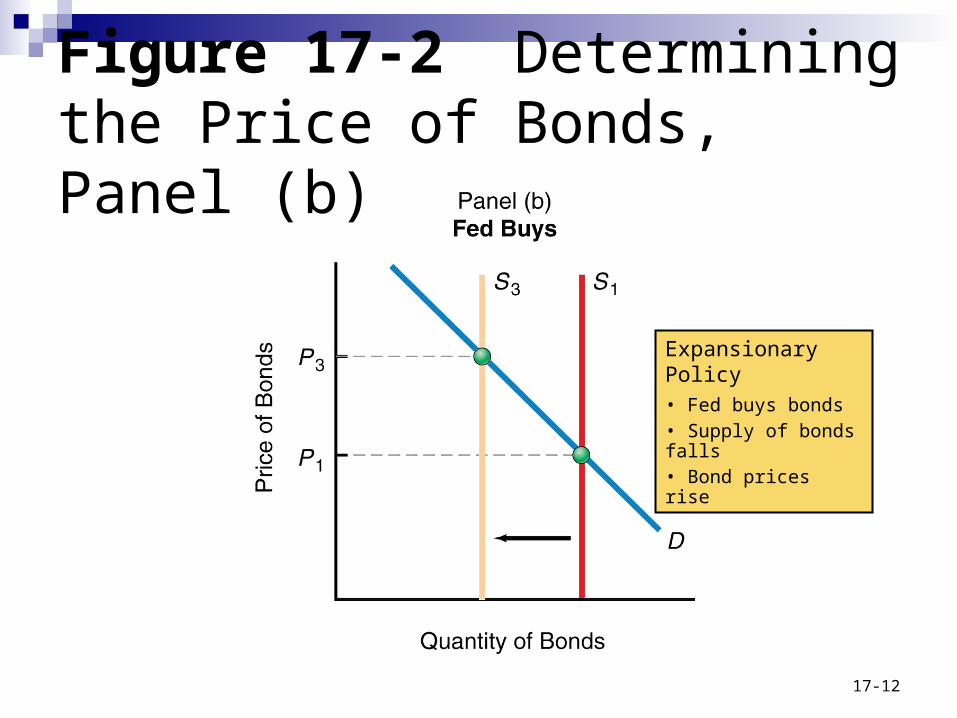

Figure 17-2 Determining the Price of Bonds, Panel (b)

17-12

Expansionary Policy• Fed buys bonds• Supply of bonds falls• Bond prices rise

The Tools of Monetary Policy (cont'd) Relationship between the price of existing

bonds and the rate of interestThere is an inverse relationship between the price

of existing bonds and the rate of interest.

17-13

The Tools of Monetary Policy (cont'd) Example

You pay $1,000 for a bond that pays $50/year in interest.

17-14

Bond yield =$50

$1,000= 5%

Now suppose you pay $500 for the same bond.

Bond yield =$50

$500= 10%

The Tools of Monetary Policy (cont'd) The market price of existing bonds (and all

fixed-income assets) is inversely related to the rate of interest prevailing in the economy.

17-15

The Tools of Monetary Policy (cont'd) Changes in the difference between the discount

rate and the federal funds rateThe discount rate is generally kept at 1 percentage

point above the market-determined federal funds rate.

Increasing (decreasing) the discount rate increases (decreases) the cost of borrowed funds for depository institutions that borrow reserves.

17-16

The Tools of Monetary Policy (cont'd) Changes in the reserve requirements

An increase (decrease) in the required reserve ratio

Makes it more (less) expensive for banks to meet reserve requirements

Reduces (expands) bank lending

17-17

Effects of an Increase in The Money Supply (cont'd) Direct effect

Aggregate demand rises because with an increase in the money supply, at any given price level people now want to purchase more output of real goods and services.

17-18

Effects of an Increase in The Money Supply (cont'd) Indirect effect

Not everybody will necessarily spend the newfound money on goods and services.

Some of the money gets deposited, so banks have higher reserves (and they lend the excess out).

17-19

Effects of an Increase in The Money Supply (cont'd) Indirect effect

Banks lower rates to induce borrowing. Businesses engage in investment. Individuals consume durable goods (like housing and autos).

Increased loans generate an increase in aggregate demand.

More people are involved in more spending (even those who didn’t get money from the helicopter!).

17-20

Graphing the Effects of an Expansionary Monetary Policy Assume the economy is operating at less than

full employment

Expansionary monetary policy can close the recessionary gap.

Direct and indirect effects cause the aggregate demand curve to shift outward.

17-21

Figure 17-3 Expansionary Monetary Policy with Underutilized Resources

17-22

• The recessionary gap isdue to insufficient AD

• To increase AD, use expansionary monetary policy

• AD increases and real GDP increases to full employment

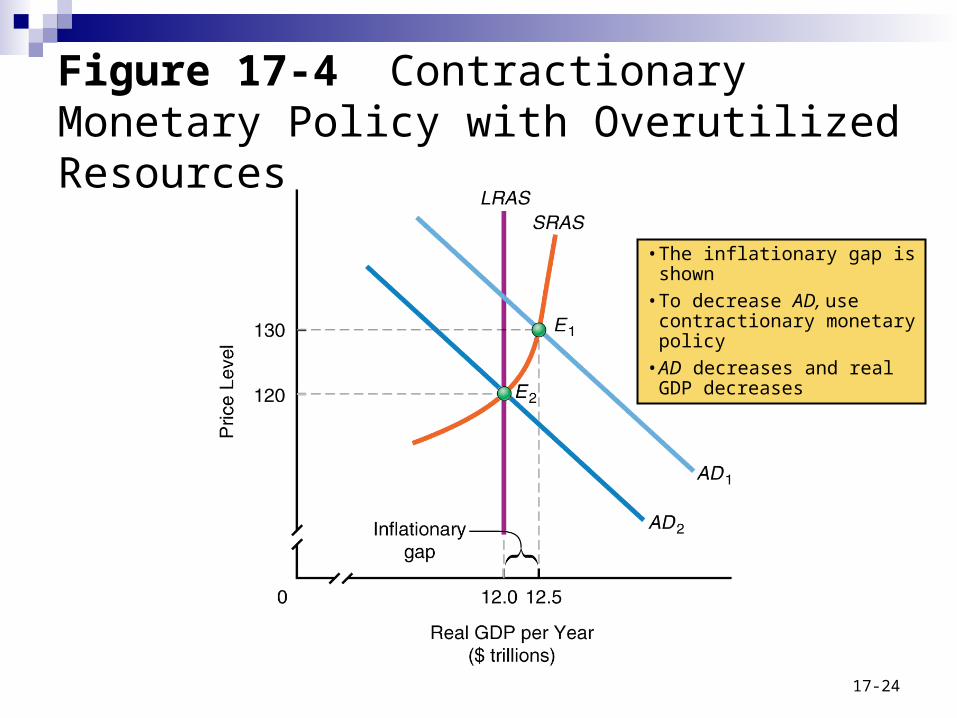

Graphing the Effects of Contractionary Monetary Policy Assume there is an inflationary gap

Contractionary monetary policy can eliminate this inflationary gap.

Direct and indirect effects cause the aggregate demand curve to shift inward.

17-23

Figure 17-4 Contractionary Monetary Policy with Overutilized Resources

17-24

•The inflationary gap is shown

•To decrease AD, use contractionary monetary policy

•AD decreases and real GDP decreases

Open Economy Transmission of Monetary Policy So far we have discussed monetary policy in a

closed economy.

When we move to an open economy, monetary policy becomes more complex.

17-25

Open Economy Transmission of Monetary Policy (cont'd) The net export effect

Impact of expansionary (contractionary) monetary Lower (higher) interest rates Financial capital flows out of (into) the United States Demand for dollars will decrease (increase) International price of dollar goes down (up) Foreign goods look more (less) expensive in

United States Net exports increase (decrease) and imports fall (go up)

17-26

Open Economy Transmission of Monetary Policy (cont'd) Globalization of international

money markets

Global money markets reduce the Fed's ability to control the rate of growth in the money supply.

Foreign entities can influence both the supply of and demand for U.S. dollars.

Their actions can reinforce or offset the Fed strategy.

17-27

Monetary Policy and Inflation

Most theories of inflation relate to the short run and the price index in the short run can fluctuate due toOil price shocks, labor union strikes

In the long run, there is a more stable relationship between growth in the money supply and inflation.

17-28

Monetary Policy and Inflation (cont'd) Simple supply and demand analysis can be used

to explain Why the price level rises when the money supply is

increased

If the supply of money expands relative to the demand for money It takes more units of money to purchase given

quantities of goods and services (i.e., the price level has risen)

17-29

Monetary Policy and Inflation (cont'd) The Equation of Exchange

The formula indicating that the number of monetary units times the number of times each unit is spent on final goods and services is identical to the price level times real GDP

17-30

MsV = PY

Monetary Policy and Inflation (cont'd) V = Income Velocity of Money

The number of times per year the dollar is spent on final goods and services; equal to the nominal GDP divided by the money supply.

17-31

Monetary Policy and Inflation (cont'd) The equation of exchange and the quantity

theory: MSV = PY

MS = actual money balances held by nonbanking public

V = income velocity of money; the number of times, on average per year, each monetary unit is spent on final goods and services

P = price level or price index

Y = real GDP per year17-32

Monetary Policy and Inflation (cont'd) The equation of exchange as

an identity

Total funds spent on final output MsV equals total funds received PY

The value of goods purchased is equal to the value of goods sold

MsV = PY = nominal GDP

17-33

Monetary Policy and Inflation (cont'd)

Assume: V is constantY is stable

Increases in Ms must be matched by equal increases in the price level

17-34

MsV = PY

Quantity Theory of Money and Prices

The hypothesis that changes in the money supply lead to proportional changes in the price level

Figure 17-5 The Relationship Between Money Supply Growth Rates and Rates of Inflation

17-35

Monetary Policy in Action: The Transmission Mechanism Recall we talked about the direct and indirect

effects of monetary policy.Direct effect: implies increase in money supply

causes people to have excess money balances.

Indirect effect: occurs as people purchase interest-bearing assets, causing the price of such assets to go up.

17-36

Figure 17-6 The Interest-Rate-Based Money Transmission Mechanism

17-37

Figure 17-7 Adding Monetary Policy to the Aggregate Demand–Aggregate Supply Model, Panel (a)

17-38

At lower rates, a larger quantity of money will be demanded

Figure 17-7 Adding Monetary Policy to the Aggregate Demand–Aggregate Supply Model, Panel (b)

17-39

The decrease in the interest rate stimulates investment

Figure 17-7 Adding Monetary Policy to the Aggregate Demand–Aggregate Supply Model, Panel (c)

17-40

The increase in investment shifts the AD curve to the right

Fed Target Choice: Interest Rates or Money Supply? It is not possible to stabilize the money supply and

interest rates simultaneously.

The Fed has often sought to achieve an interest rate target.

There is a fundamental tension between targeting interest rates and controlling the money supply.

The Fed, in the short run, can select an interest rate or a money supply target but not both.

17-41

Figure 17-8 Choosing a Monetary Policy Target

17-42

If the Fed selects re, it

must accept Ms

If the Fed selects M’s,

it must allow the interest rate to fall

Fed Target Choice: Interest Rates or Money Supply? (cont'd) The Fed, in the short run, can select

an interest rate or a money supply target but not both.

17-43

Fed Target Choice: Interest Rates or Money Supply? (cont'd) Choosing a policy target

Money supply When variations in private spending occur

Interest rates When the demand for (or supply of) money

is unstable Interest rate targets are preferred

17-44

The Way Fed Policy is Currently Implemented At present the Fed announces an interest rate

target.

The rate referred to is the federal funds rate of interest.

Or, the rate at which banks can borrow excess reserves from each other.

17-45

The Way Fed Policy is Currently Implemented (cont'd) If the Fed wants to raise “the” interest rate, it

engages in contractionary open market operations.

Fed sells more Treasury securities than it buys, thereby reducing the money supply.

This tends to boost “the” rate of interest.

17-46

The Way Fed Policy is Currently Implemented (cont'd) Conversely, if the Fed wants to decrease “the”

rate of interest, it engages in expansionary open market operations.

Fed buys more Treasury securities, increasing the money supply.

This tends to lower “the” rate of interest.

17-47

The Way Fed Policy is Currently Implemented (cont'd) FOMC Directive

A document that summarizes the Federal Open Market Committee’s general policy strategy

Establishes near-term objectives for the federal funds rate and specifies target ranges for money supply growth

17-48

The Way Fed Policy is Currently Implemented (cont'd) Trading Desk

An office at the Federal Reserve Bank of New York charged with implementing monetary policy strategies developed by the FOMC

17-49

50505050

Chapter 17: Domestic and International Dimensions of Monetary Policy

50

ECON 151 – PRINCIPLES OF MACROECONOMICS

Materials include content from Pearson Addison-Wesley which has been modified by the instructor and displayed with permission of the publisher. All rights reserved.