12-1 copyright 2007 mcgraw-hill australia pty ltd ppts t/a fundamentals of corporate finance 4e, by...

TRANSCRIPT

12-1Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Chapter Twelve

Current Investment Decisions

12-2Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

12.1 The Investments Involved

12.2 The Operating Cycle and the Cash Cycle

12.3 Some Aspects of Short-term Financial Policy

12.4 The Cash Budget

12.5 A Short-term Financial Plan

Summary and Conclusions

Chapter Organisation

12-3Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Chapter Objectives• Understand the components of the operating cycle

and the cash cycle.• Explain the key issues in a firm’s short-term

financial policy.• Understand and apply the inventory model.• Prepare a cash budget.

12-4Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

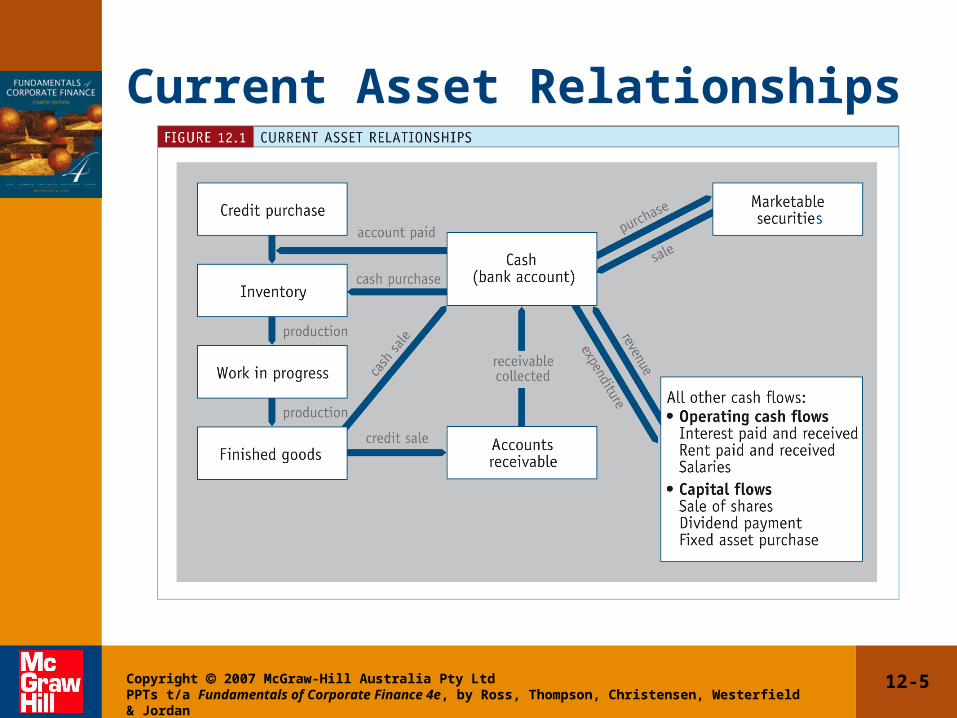

Current Investment Decisions• Involve the administration of the company’s current

assets (cash and marketable securities, receivables and inventory), and the financing needed to support these assets.

• Problems in using discounted cash flow techniques to evaluate these decisions:– identification of all relevant cash inflows and outflows– determining the size and timing of these cash flows– determining the correct discount rate.

12-5Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Current Asset Relationships

12-6Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

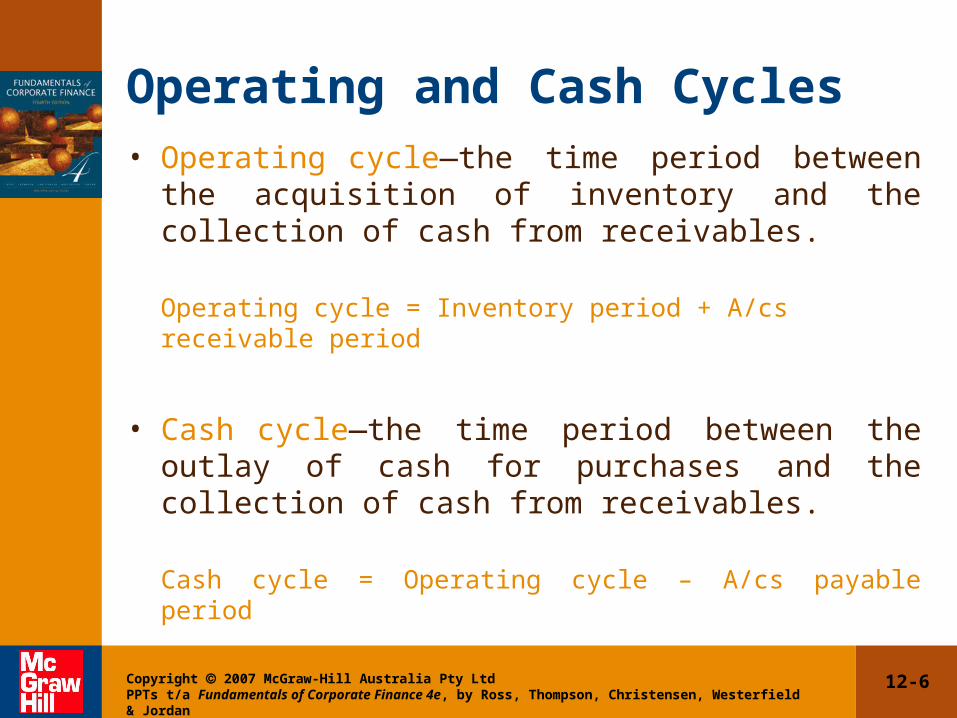

Operating and Cash Cycles• Operating cycle—the time period between the

acquisition of inventory and the collection of cash from receivables.

Operating cycle = Inventory period + A/cs receivable period

• Cash cycle—the time period between the outlay of cash for purchases and the collection of cash from receivables.

Cash cycle = Operating cycle – A/cs payable period

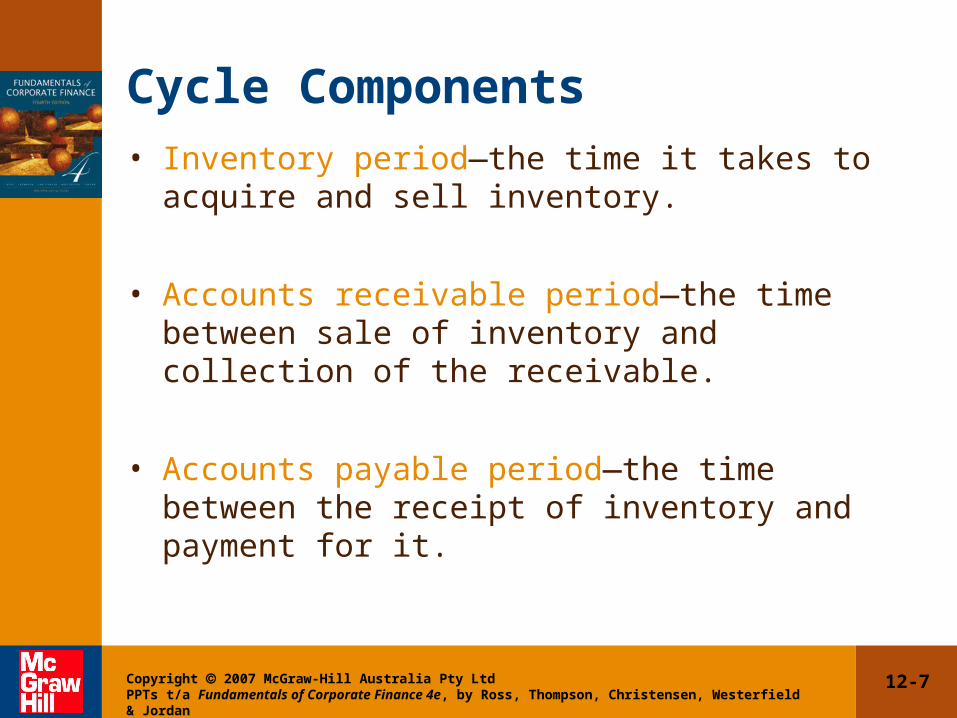

12-7Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Cycle Components• Inventory period—the time it takes to acquire and sell

inventory.

• Accounts receivable period—the time between sale of inventory and collection of the receivable.

• Accounts payable period—the time between the receipt of inventory and payment for it.

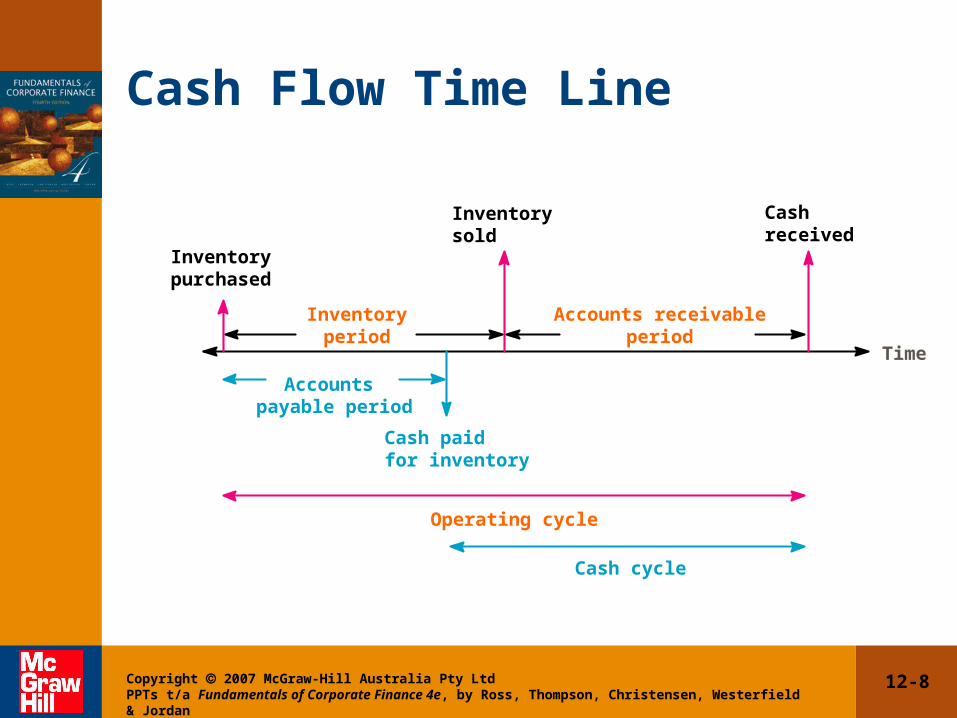

12-8Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Cash Flow Time Line

Accounts receivableperiod

Cashreceived

Time

Inventorysold

Inventorypurchased

Inventoryperiod

Accounts payable period

Cash paid for inventory

Operating cycle

Cash cycle

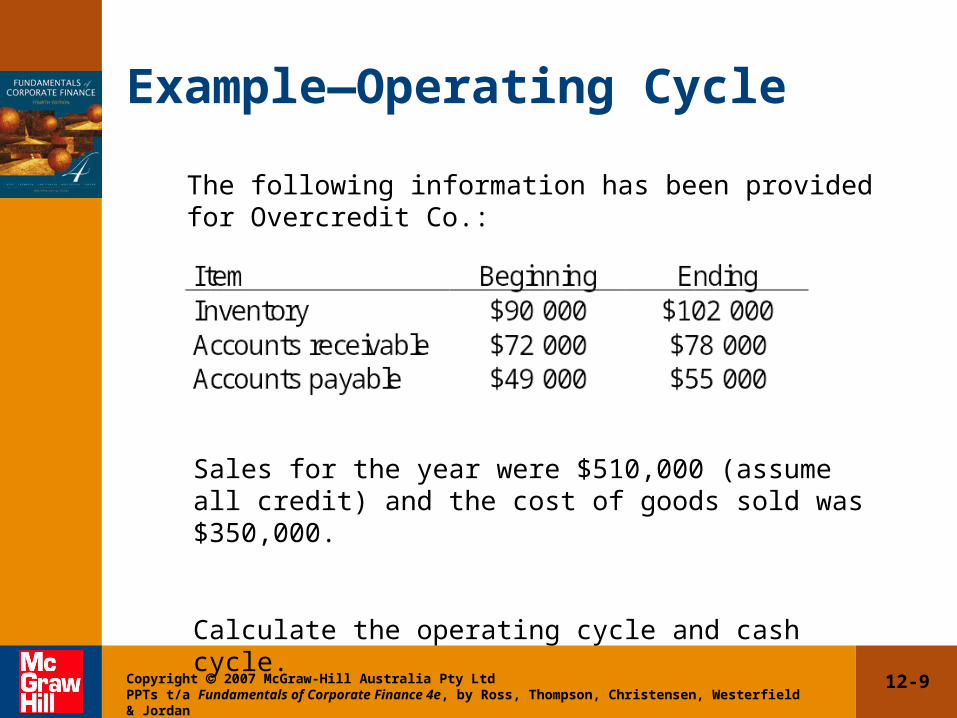

12-9Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Example—Operating Cycle

The following information has been provided for Overcredit Co.:

Sales for the year were $510,000 (assume all credit) and the cost of goods sold was $350,000.

Calculate the operating cycle and cash cycle.

12-10Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Example—Operating Cycle

days100times653

365

turnoverInventory

365periodInventory

times6532

00010200090000350

inventory Avg.

COGSturnoverInventory

.

.

a) Find the inventory period:

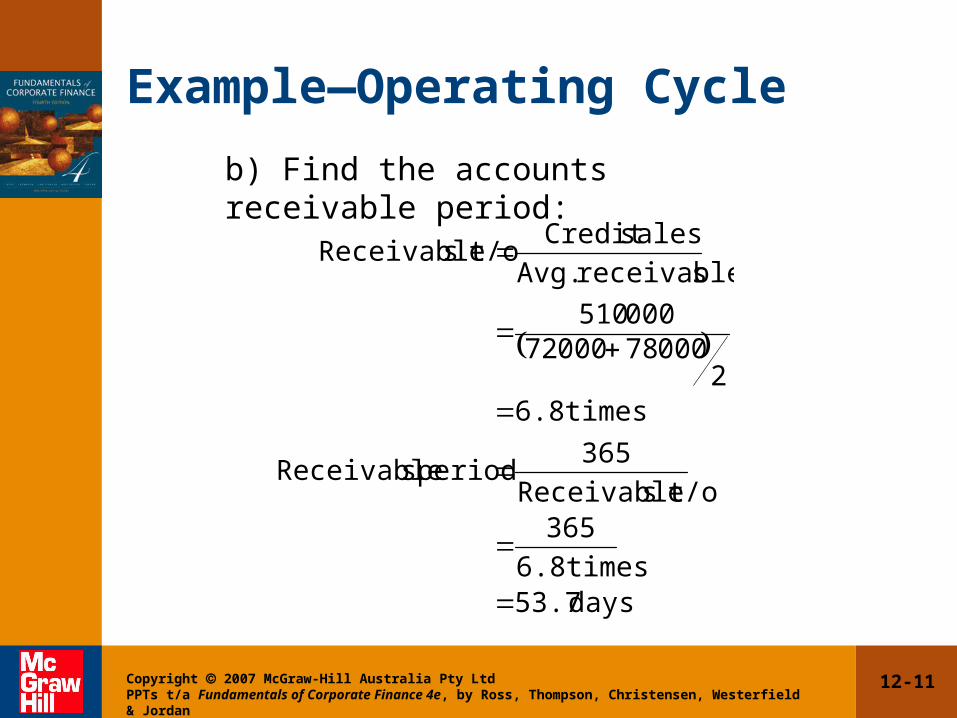

12-11Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Example—Operating Cycle

days 53.7 times6.8

365

t/osReceivable

365 period sReceivable

times6.8 2

000 78 000 72000 510

sreceivable Avg.

salesCredit t/osReceivable

b) Find the accounts receivable period:

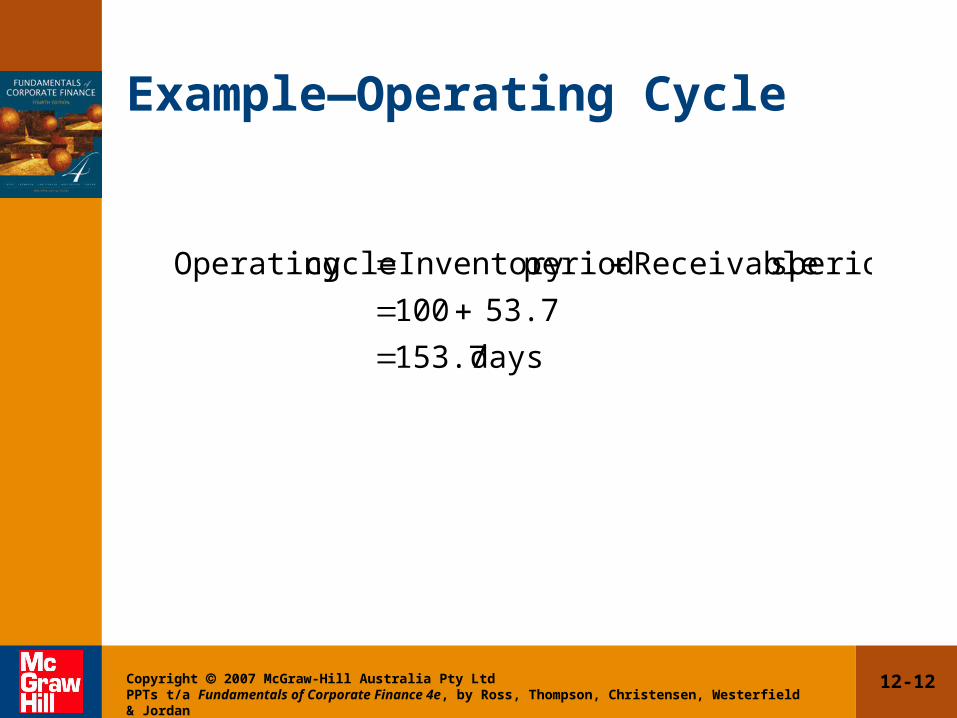

12-12Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Example—Operating Cycle

days 153.7

53.7100

period sReceivableperiodInventory cycle Operating

12-13Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

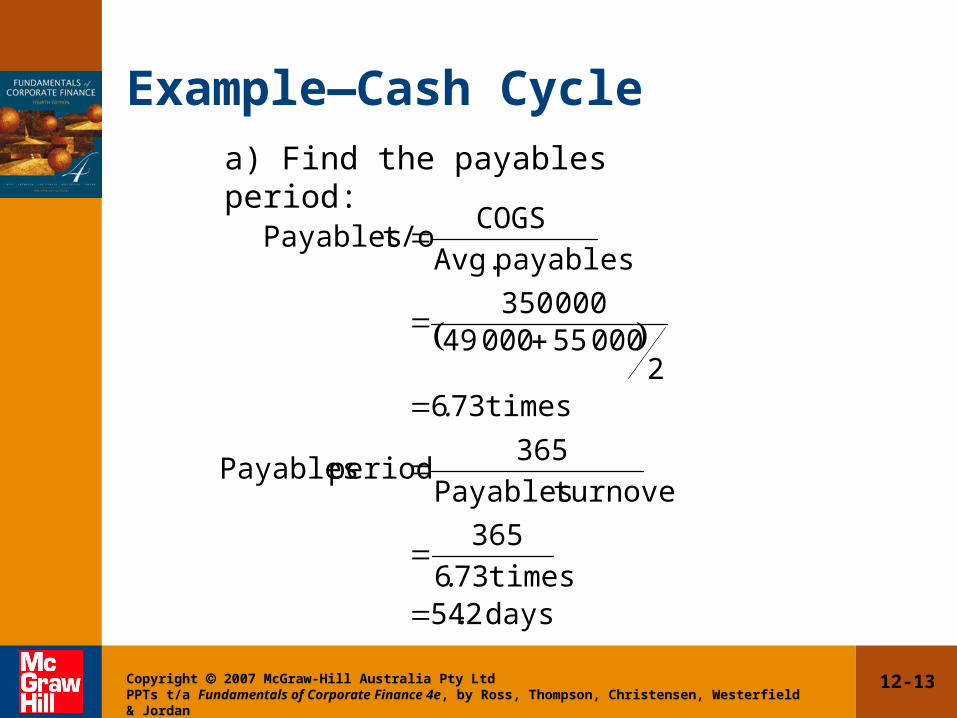

Example—Cash Cycle

days254times736

365

turnoverPayables

365period Payables

times7362

0005500049000350

payables Avg.

COGS t/oPayables

. .

.

a) Find the payables period:

12-14Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

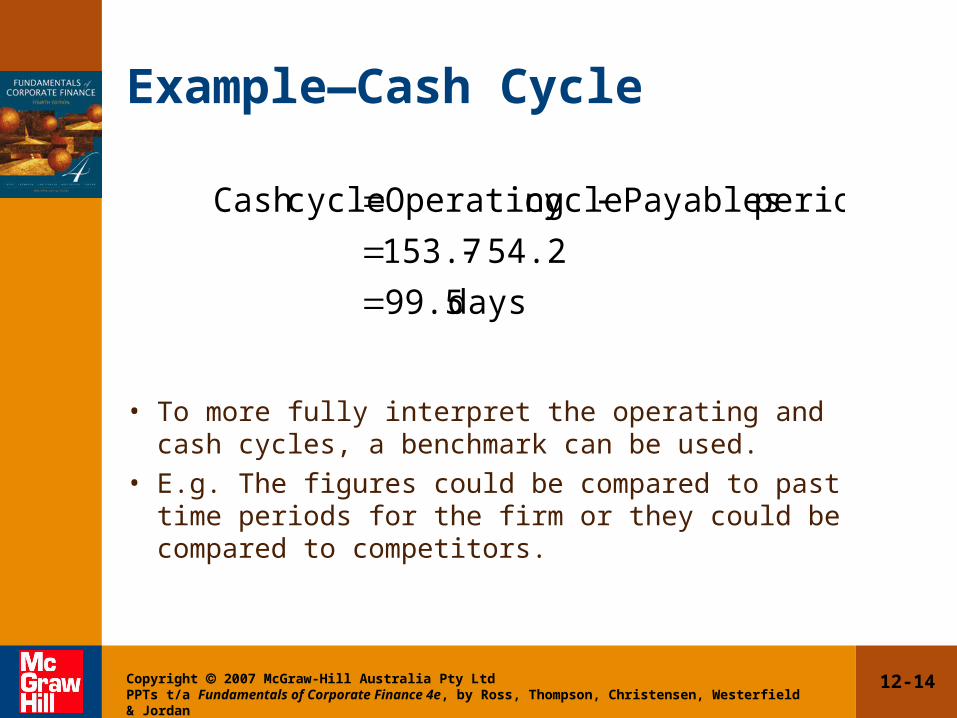

Example—Cash Cycle

days 99.5

54.2 153.7

period Payables cycle Operating cycleCash

• To more fully interpret the operating and cash cycles, a benchmark can be used.

• E.g. The figures could be compared to past time periods for the firm or they could be compared to competitors.

12-15Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Short-term Financial Policy• Size of investments in current assets

− Flexible policy—maintain a high ratio of current assets to sales

− Restrictive policy—maintain a low ratio of current assets to sales.

• Financing of current assets

− Flexible policy—less short-term debt and more long-term debt − Restrictive policy—more short-term debt and less long-term debt

12-16Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Size of the Firm’s Investment in Current Assets

• The size of the firm’s investment in current assets is determined by its short-term financial policies.

• Flexible policy actions include:– keeping large cash and securities balances

– keeping large amounts of inventory

– granting liberal credit terms.

• Restrictive policy actions include:– keeping low cash and securities balances

– keeping small amounts of inventory

– allowing few or no credit sales.

12-17Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

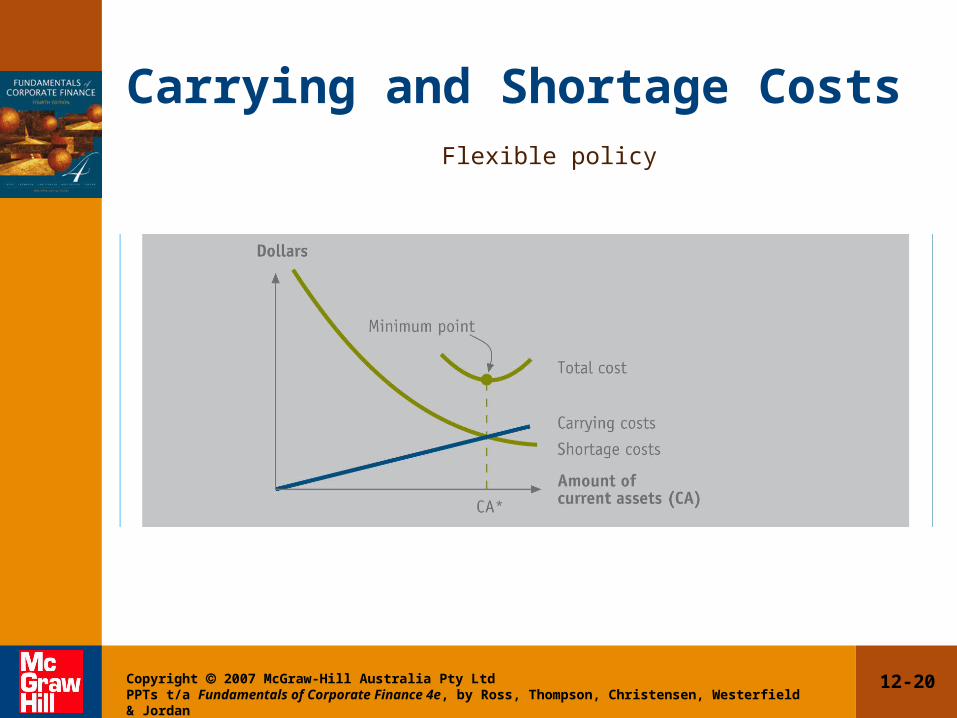

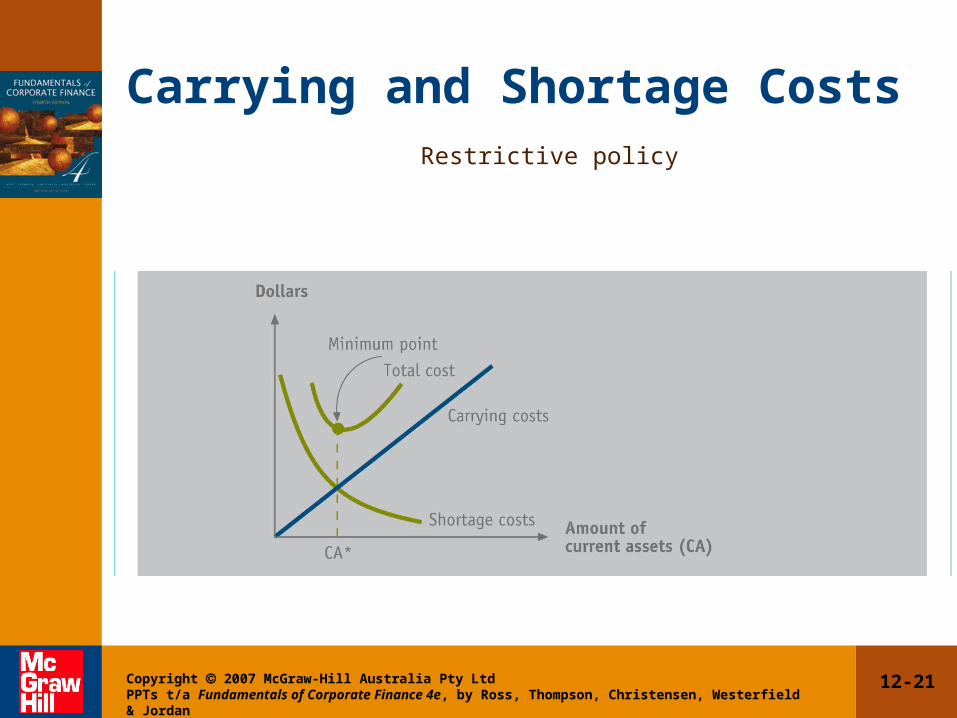

Costs of Investments• Need to manage the trade-off between carrying costs

and shortage costs.

• Carrying costs increase with the level of investment in current assets, and include the costs of maintaining economic value and opportunity costs.

• Shortage costs decrease with increases in the level of investment in current assets, and include trading costs and the costs related to being short of the current asset. For example, sales lost as a result of a shortage of finished goods inventory.

12-18Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

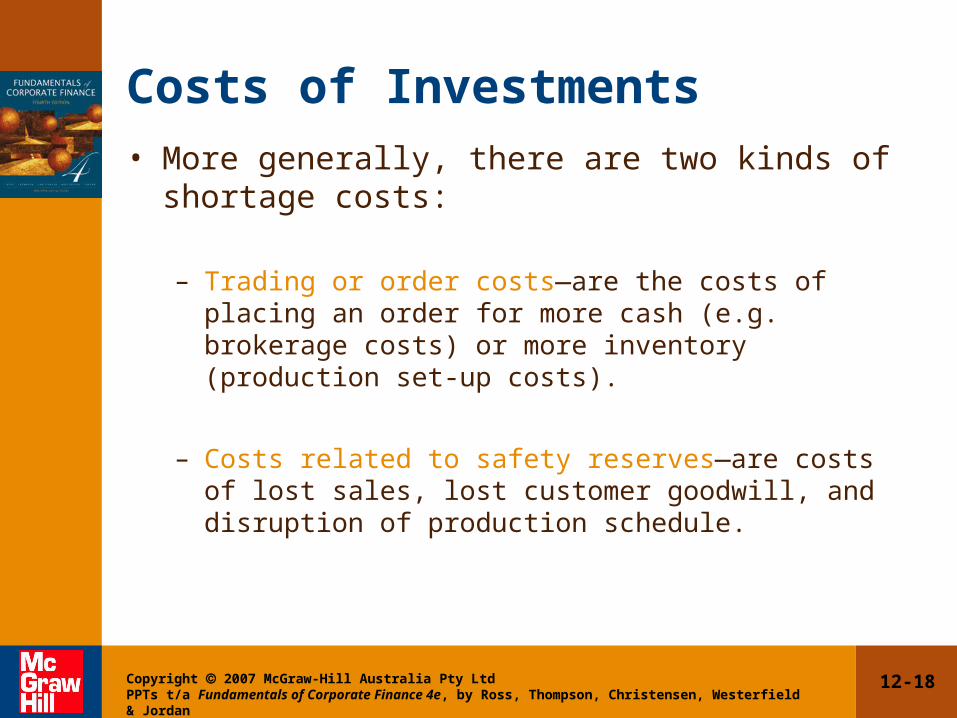

Costs of Investments • More generally, there are two kinds of shortage

costs:

– Trading or order costs—are the costs of placing an order for more cash (e.g. brokerage costs) or more inventory (production set-up costs).

– Costs related to safety reserves—are costs of lost sales, lost customer goodwill, and disruption of production schedule.

12-19Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Carrying and Shortage CostsShort-term financial policy: the optimal investment in current assets

12-20Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Carrying and Shortage CostsFlexible policy

12-21Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Carrying and Shortage CostsRestrictive policy

12-22Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

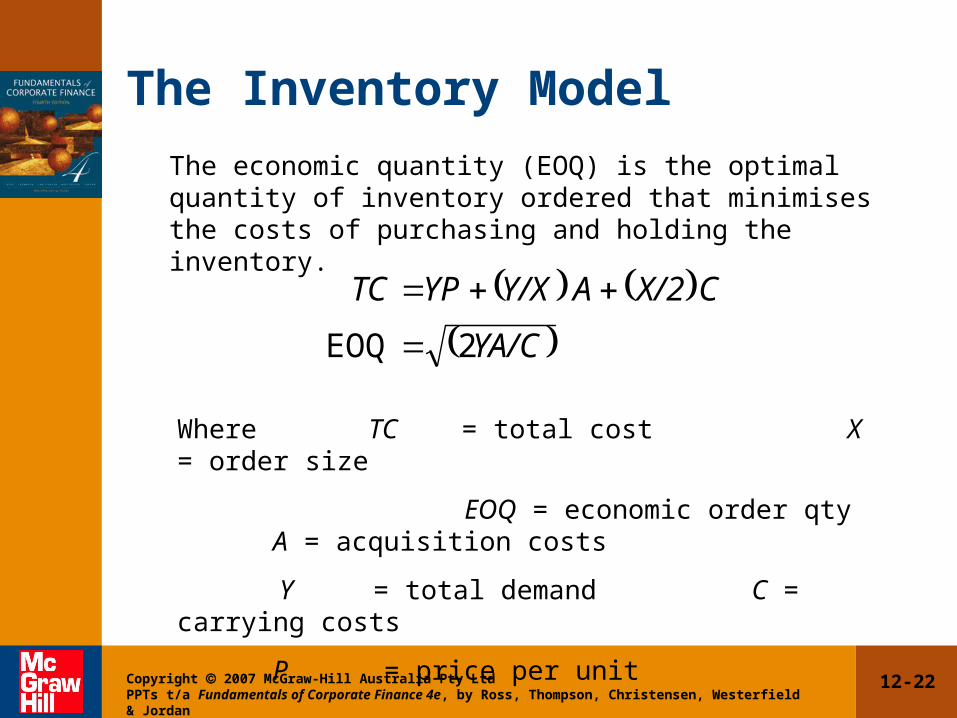

The Inventory Model

YA/C

C X/2 A Y/X YP TC

2EOQ

The economic quantity (EOQ) is the optimal quantity of inventory ordered that minimises the costs of purchasing and holding the inventory.

Where TC = total cost X = order size

EOQ = economic order qty A = acquisition costs

Y = total demand C = carrying costs

P = price per unit

12-23Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

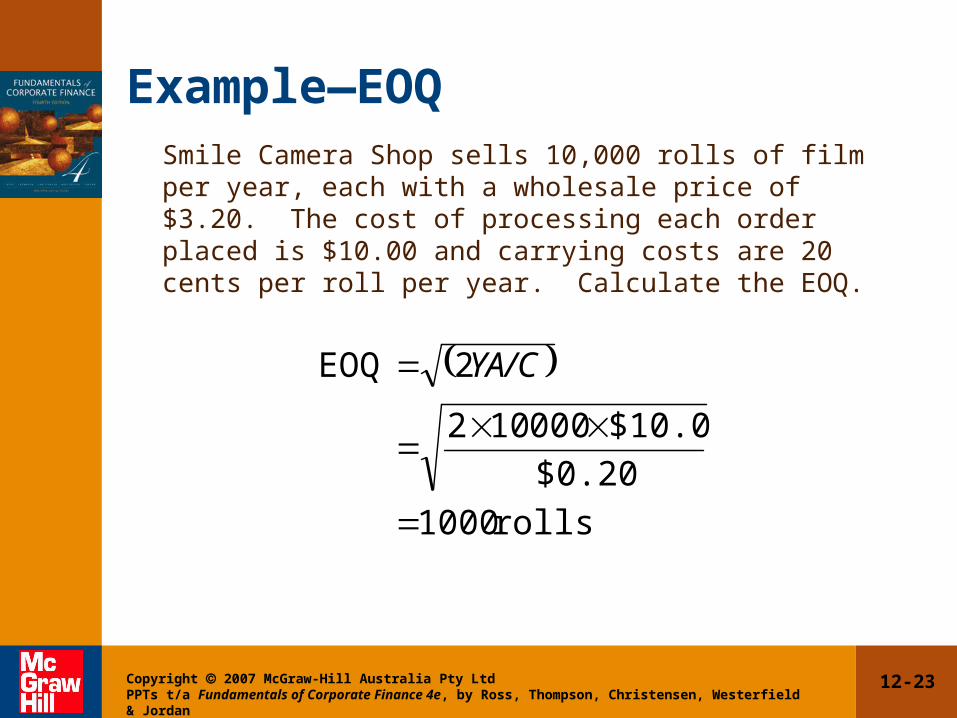

Example—EOQ Smile Camera Shop sells 10,000 rolls of film per year, each with a wholesale price of $3.20. The cost of processing each order placed is $10.00 and carrying costs are 20 cents per roll per year. Calculate the EOQ.

rolls 1000

$0.20

$10.00000 102

2EOQ

YA/C

12-24Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

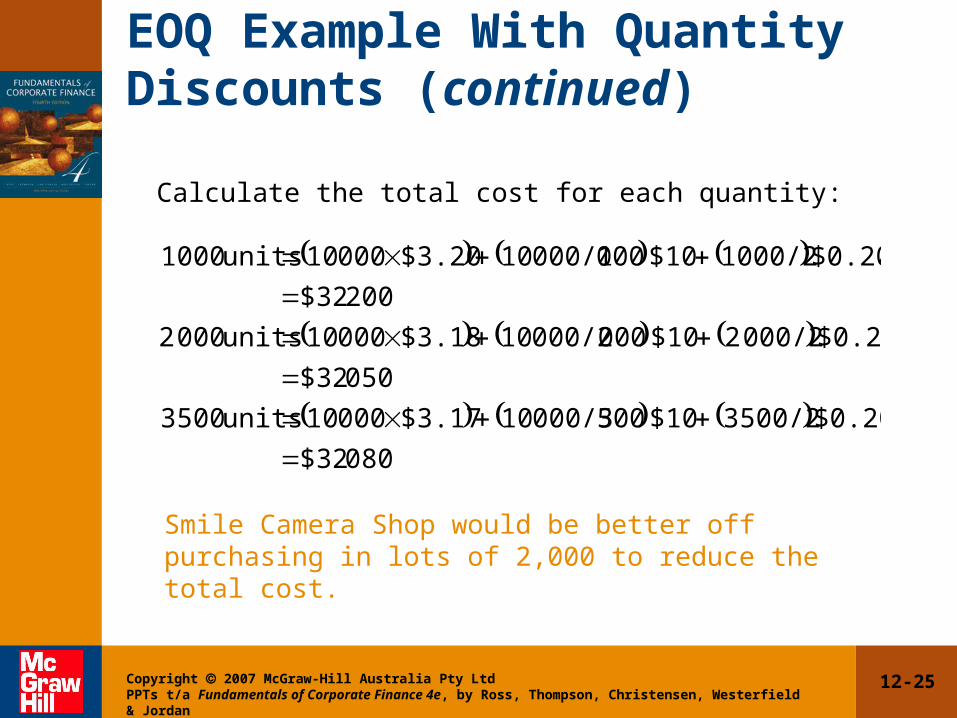

EOQ Example With Quantity Discounts

Smile Camera Shop is offered a 2-cent-per-roll discount if 2,000–3,500 rolls of film are ordered, and a 3-cent-per-roll discount if more than 3,500 rolls are ordered at a time. Determine the optimal order quantity.

12-25Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

EOQ Example With Quantity Discounts (continued)

080 $32

$0.20 500/2 3 $10 500 000/3 10 $3.17 000 10 units 500 3

050 $32

$0.20 000/2 2 $10 000 000/2 10 $3.18 000 10 units 000 2

200 $32

$0.20 000/2 1 $10 000 000/1 10 $3.20 000 10 units 000 1

Calculate the total cost for each quantity:

Smile Camera Shop would be better off purchasing in lots of 2,000 to reduce the total cost.

12-26Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Stock Out Costs• Costs of stock outs are the profits lost because the

firm is out of a particular product.

• Lead time is the time it takes from placing an order to the receipt of the inventory.

• Safety stock is the additional inventory held when demand is uncertain so as to reduce the probability of a stock out.

12-27Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

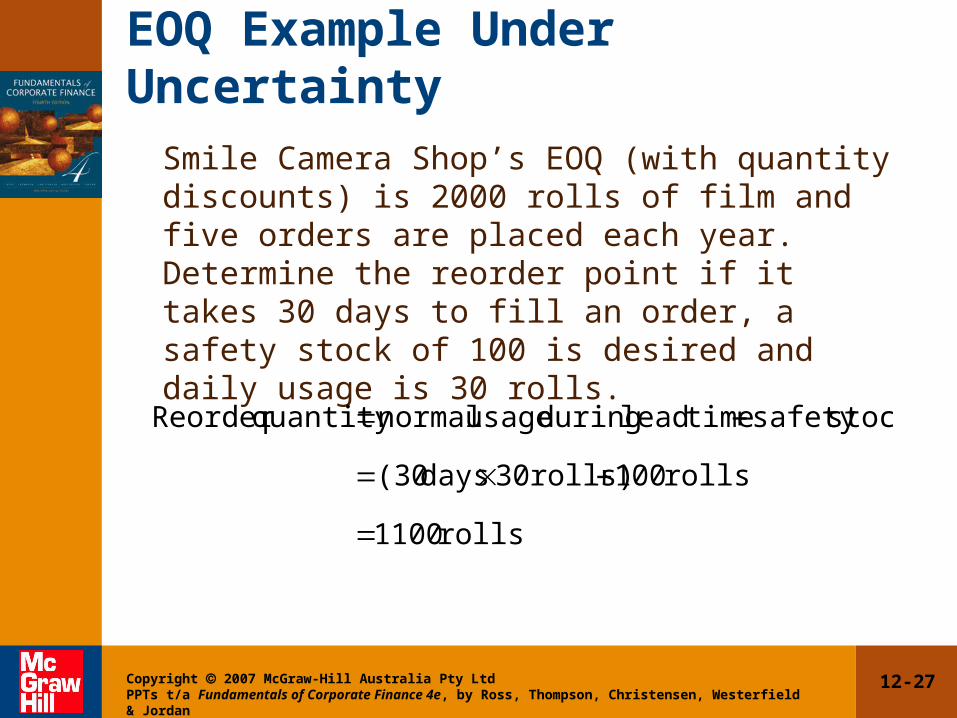

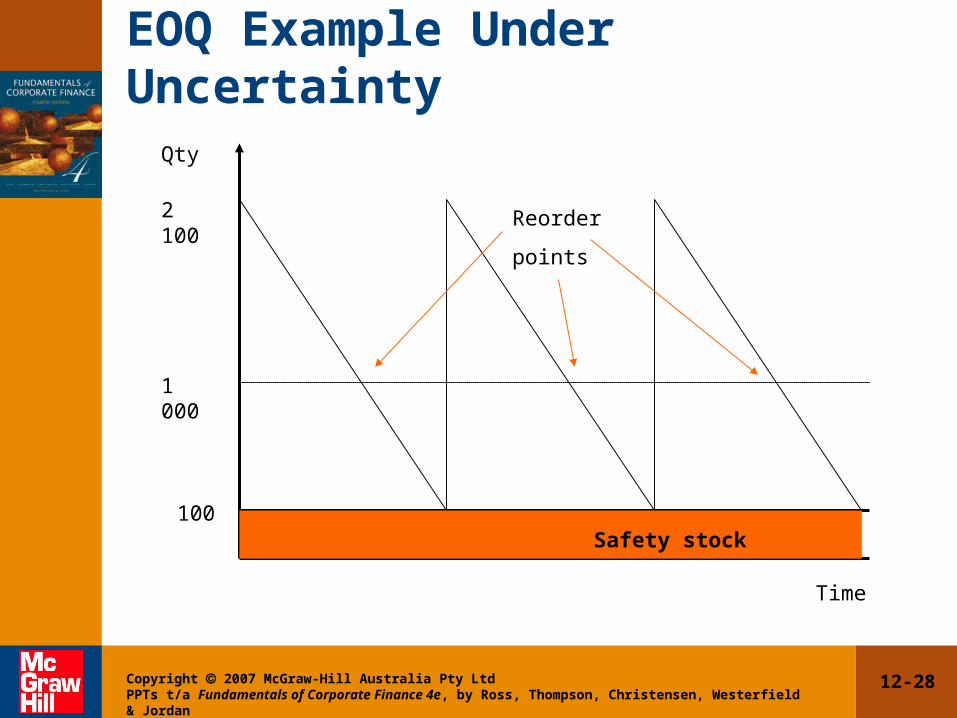

EOQ Example Under UncertaintySmile Camera Shop’s EOQ (with quantity discounts) is 2000 rolls of film and five orders are placed each year. Determine the reorder point if it takes 30 days to fill an order, a safety stock of 100 is desired and daily usage is 30 rolls.

rolls 1100

rolls 100rolls) 30days (30

stocksafety timelead during usage normalquantityReorder

12-28Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Qty

2 100

1 000

100

Time

Reorder

points

Safety stock

EOQ Example Under Uncertainty

12-29Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Just-in-Time (JIT)• Just-in-time (JIT) is a system for managing demand-

dependent inventories that minimises inventory holdings.

• JIT simply means that the purchaser receives the goods just in time to use the goods in the production process (e.g. a motor vehicle manufacturer) which in turn reduces the carrying cost of inventory.

• Acquisition costs are also minimised as next period’s production requirements are always known to the supplier.

12-30Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Cash Budget• A forecast of cash receipts and disbursements over

the next short-term planning period.

• Primary tool in short-term financial planning.

• Helps determine when the firm should experience cash surpluses and when it will need to borrow to cover working-capital costs.

• Allows a firm to plan ahead and begin the search for financing before the money is actually needed.

12-31Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Example—Cash Budget• Projected sales for the first six months of 2006:

Jan. $130 000 Apr. $140 000

Feb. $125 000 May $155 000

Mar. $145 000 Jun. $145 000

• Analysis of collection of accounts receivable:– collected in month of sale 20%

– collected in month following sale 60%

– collected in second month following sale20%

• Actual sales for November and December were $125 000 and $120 000 respectively.

12-32Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Example—Cash Budget (continued)• Wages and other expenses are 30 per cent of total

monthly sales.• Purchases are 50 per cent of the month’s estimated

sales, all paid for in the month of purchase.• Monthly interest payments are $15 000 (interest rate

is 1.5 per cent per month).• An annual dividend of $60 000 is payable in March.• The beginning cash balance is $30 000.• The minimum cash balance is $20 000.

12-33Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Cash Collections

12-34Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Cash Disbursements

12-35Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

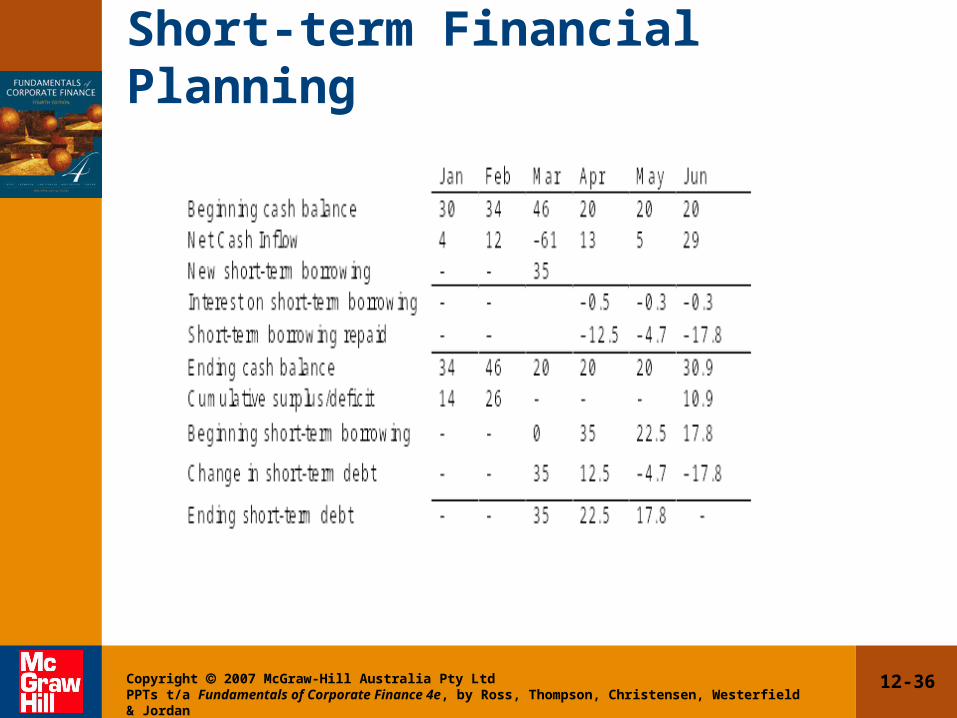

Cash Budget

12-36Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Short-term Financial Planning

12-37Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Fundamentals of Corporate Finance 4e, by Ross, Thompson, Christensen, Westerfield & Jordan

Summary and Conclusions• Decisions about current assets are interdependent. A

firm needs to establish its level of cash while considering the amount of inventory it should purchase and the level of accounts receivable.

• The objective of managing current assets is to find the optimal trade-off between carrying costs and shortage costs.

• The level of inventory that should be purchased to minimise carrying and shortage costs is called the economic order quantity (EOQ).

• The cash budget tells the financial manager what borrowing is required or what lending will be possible in the short-run.