2 highlights of year 2005 positive economic outlook and indicators for africa g8 adopts the...

TRANSCRIPT

2

Highlights of Year 2005

Positive economic outlook and indicators for Africa

G8 adopts the Multilateral Debt Relief Initiative

Mr. Donald Kaberuka assumes office as the seventh elected

President of the Bank Group in September

Constitution of a Presidential Task Force on Institutional Reform

Bank policies and mix of products are amended to better address the

needs of member countries

Launch of first Botswana Pula denominated bond under the local

currency initiative

3

Table of Contents

11 African Economic Outlook

Bank Financial Profile33

Capital Market Activities44

22 Bank Group’s Activities and Road Ahead

4

The combination of the positive economic outlook and greater attention from the international community should result in progress towards achieving the Millennium Development Goals in Africa

11 African Economic Outlook

5

3.5%

4.0%

4.9%

5.2%

4.6%

3%

4%

4%

5%

5%

6%

2001 2002 2003 2004 2005

Drivers

Macroeconomic stability – Debt relief – Continued global expansion

Africa’s 2005 real GDP growth rate exceeded 4.5% for the third consecutive year

18 countries achieved GDP 18 countries achieved GDP growth rates growth rates above 5above 5 %%

Average per regionAverage per region

Central Africa: Central Africa: 4.8% 4.8%North Africa:North Africa: 4.8% 4.8%East Africa: East Africa: 5.6% 5.6% Southern Africa: 5.0%Southern Africa: 5.0%West Africa: West Africa: 4.4% 4.4%

Real GDP Growth

6

-5%

-2%

1%

4%

7%

10%

13%

2001 2002 2003 2004 2005

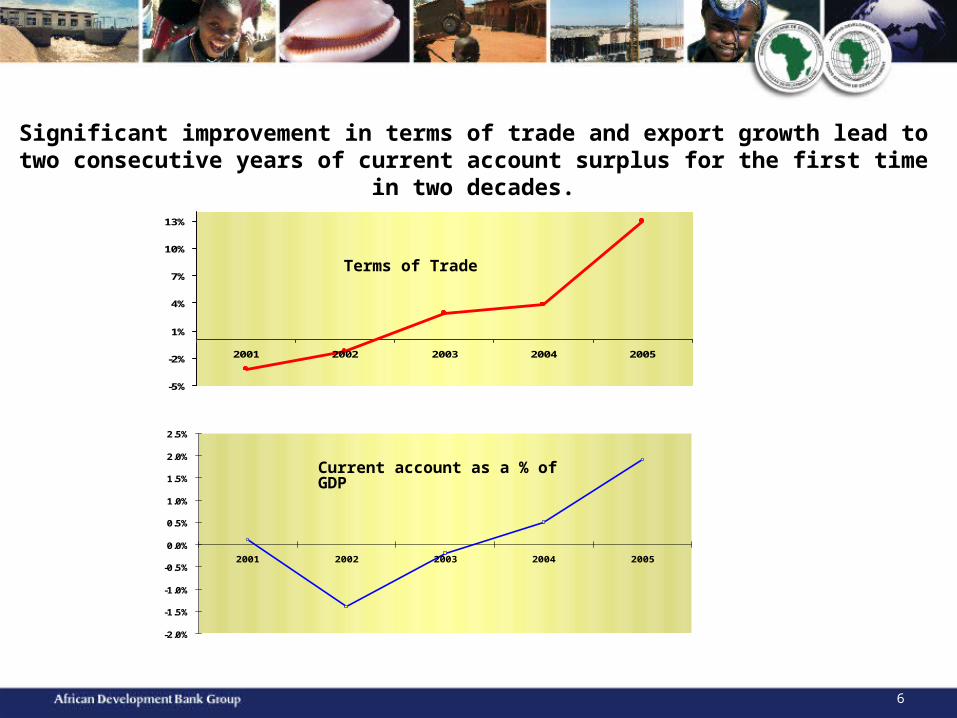

Significant improvement in terms of trade and export growth lead to two consecutive years of current account surplus for the first time in two decades.

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2001 2002 2003 2004 2005

Terms of Trade

Current account as a % of GDP

7

Improved export performance and debt relief measures have contributed to a steady decline in debt service

53.3% 52.9%

48.3%

42.4%

35.7%

30%

40%

50%

60%

2001 2002 2003 2004 2005

17.8%

14.9%

13.8%

12.0%

10.6%

10%

15%

20%

2001 2002 2003 2004 2005

Debt Service Ratio Debt / GDP

8

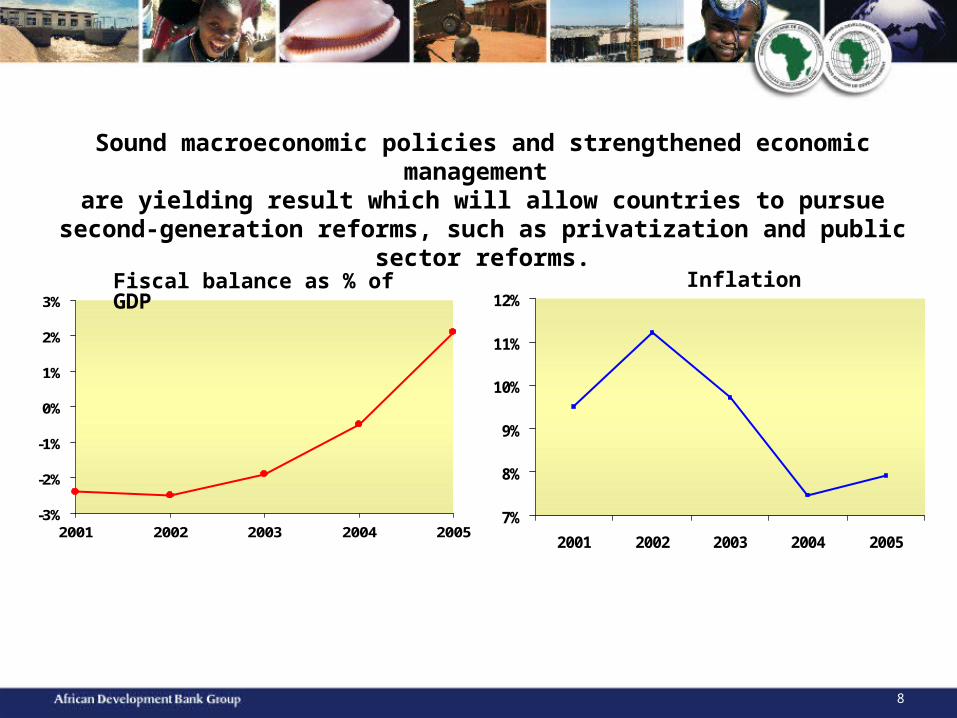

Sound macroeconomic policies and strengthened economic management are yielding result which will allow countries to pursue second-generation

reforms, such as privatization and public sector reforms.

7%

8%

9%

10%

11%

12%

2001 2002 2003 2004 2005

-3%

-2%

-1%

0%

1%

2%

3%

2001 2002 2003 2004 2005

InflationFiscal balance as % of GDP

9

G8 SUMMIT ON POVERTYG8 SUMMIT ON POVERTY

Fight against disease Fight against disease and hunger: and hunger:

Bono, Clinton & GatesBono, Clinton & Gates

Commission for Commission for AfricaAfrica

1.1. Eradicate extreme poverty Eradicate extreme poverty and hungerand hunger

2.2. Achieve universal Achieve universal primary educationprimary education

3.3. Promote gender equality Promote gender equality and empower womenand empower women

4.4. Reduce child mortalityReduce child mortality

5.5. Improve maternal healthImprove maternal health

6.6. Combat HIV/AIDS, malaria Combat HIV/AIDS, malaria and other diseasesand other diseases

7.7. Ensure environmental Ensure environmental sustainabilitysustainability

8.8. Develop a global Develop a global partnership for partnership for developmentdevelopment

Multilateral Debt Relief Initiative

Still, only few African countries will achieve the MDGs by 2015 even if all existing commitments to increase aid are honoured.

African Infrastructure African Infrastructure ConsortiumConsortium

In 2005, the spotlight of world development agenda was firmly on Africa

Millennium Millennium Development GoalsDevelopment Goals

10

22 Bank Group’s Activities and Road Ahead

In 2005, the Bank continued to build on its achievements and to reposition itself for greater effectiveness and efficiency in the delivery of its mandate

11

Access to ADB window

Access to ADF window

Access to ADB and ADF windows

Providing impetus to Africa’s development through the three windows of the ADB Group

Bank Group Vision

“The African Development

Bank is the premier financial

development institution of

Africa dedicated to

combating poverty and

improving the lives of the

people of the continent and

engaged in the task of

mobilizing resources toward

the economic and social

progress of its regional

member countries”

12

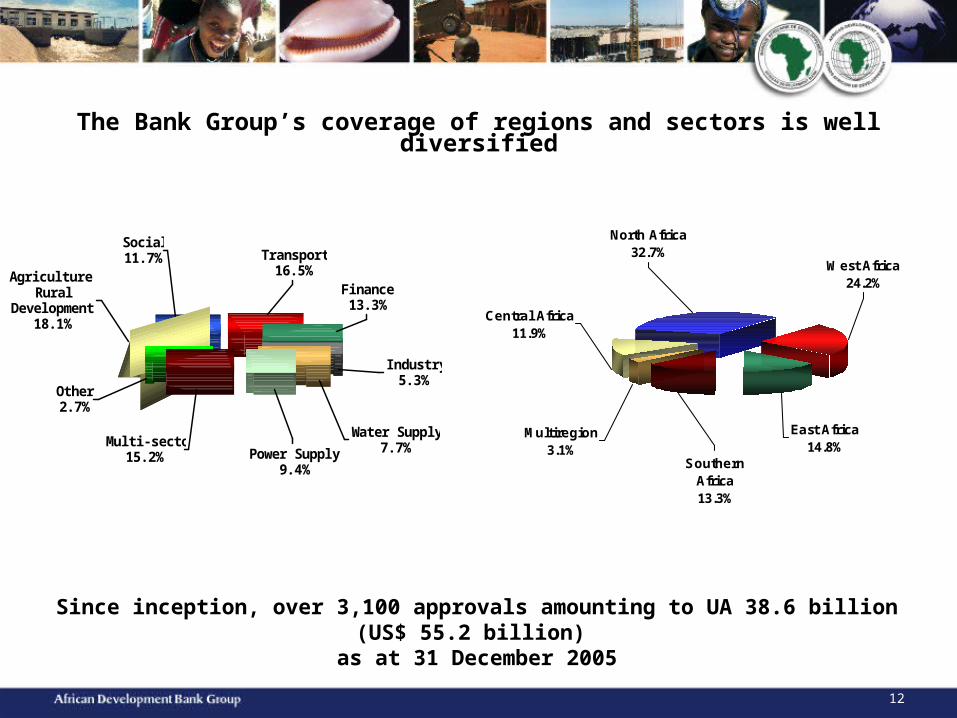

The Bank Group’s coverage of regions and sectors is well diversified

Agriculture & Rural

Development18.1%

Finance13.3%

Transport16.5%

Social11.7%

Other2.7%

Multi-sector15.2% Power Supply

9.4%

Water Supply7.7%

Industry5.3%

Since inception, over 3,100 approvals amounting to UA 38.6 billion (US$ 55.2 billion) as at 31 December 2005

Central Africa11.9%

Southern Africa13.3%

Multiregion3.1%

North Africa32.7%

West Africa24.2%

East Africa14.8%

13

The Bank Group’s approvals reflect customized assistance

24 out of 33 eligible African countries already benefit from debt relief under enhanced HIPC initiative

0

500

1,000

1,500

2,000

2,500

3,000

2001 2002 2003 2004 2005

ADB ADF HIPC NTF

In UA million

US$ 3.3 billion

US$ 4.3 billion

US$ 2.6 billion

US$ 2.8 billion

US$ 3.0 billion

14

The Bank’s Middle Income Countries Initiative in 2005 further increased the attractiveness of the ADB window

COMPETITIVE PRICINGCOMPETITIVE PRICINGCommitment fees eliminated for new sovereign

guaranteed loansLending spread decreased from 0.5% to 0.4%Market risk premium eliminated for fixed rate loans

Commitment fees eliminated for new sovereign guaranteed loans

Lending spread decreased from 0.5% to 0.4%Market risk premium eliminated for fixed rate loans

ENVIRONMENTAL IMPACTENVIRONMENTAL IMPACT

TECHNICAL ASSISTANCETECHNICAL ASSISTANCE

MIC Trust Fund amount increased from UA 1 million (US$ 1.43 million) to UA 16 million (US$ 22.87 million)

Ceiling per project raised to UA 600,000 (US$ 857,562) from UA 100,000 (US$ 142,927)

MIC Trust Fund amount increased from UA 1 million (US$ 1.43 million) to UA 16 million (US$ 22.87 million)

Ceiling per project raised to UA 600,000 (US$ 857,562) from UA 100,000 (US$ 142,927)

Loan-processing procedures streamlinedLoan-processing procedures streamlined

15

Manufacturing0.90%Others

1.00%

Oil & Gas13.90%

Infrastructure12.20%

Infrastructure Funds8.70%

Finance55.20%

Mining6.10%

Tourism2.00%

192 199

164180

241

270

306

255 257

206

0

50

100

150

200

250

300

350

2001 2002 2003 2004 2005

Approvals in UA million Approvals in US$ million

Development of a vibrant and competitive private sector across Africa is a strategic priority for the Bank

Loans30.0%

Private & Quasi-Equity0.8%

Equity Funds 9.3%

Guarantee0.7% Lines of

Credit53.6%

Enclave Projects

5.6%

Sector Distribution Product Type

Private sector strategy focus on Creating a conducive business environment Strengthening financial systems Improving infrastructure through Public-Private

Partnerships Promoting development of trade and

small-and-medium scale enterprises

Cumulative approvals: UA 1.17 billion (US$ 1.67 billion)

16

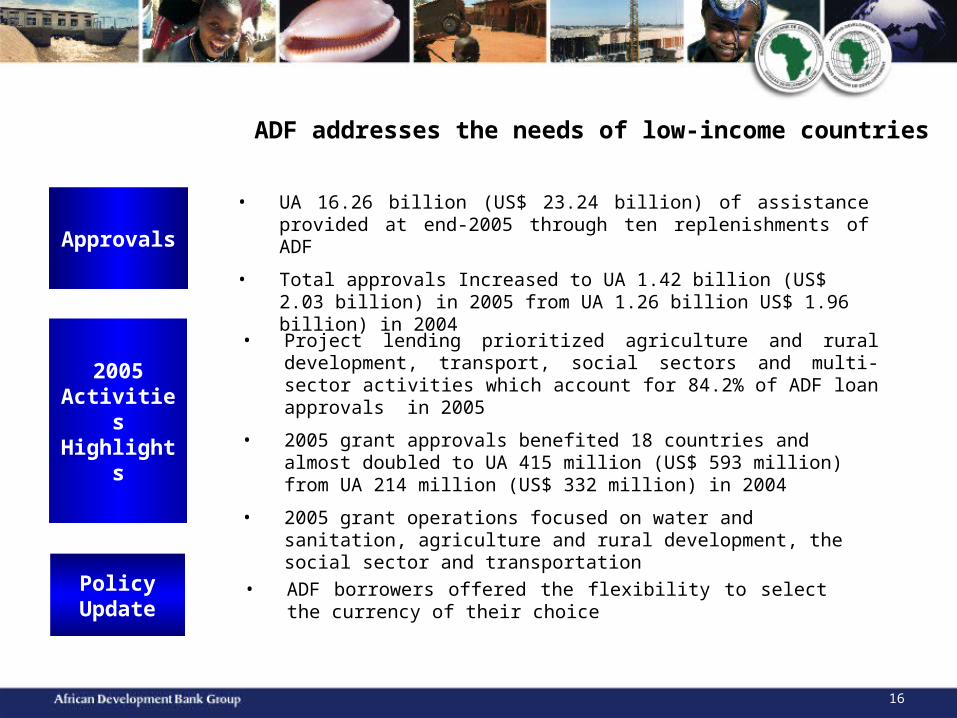

ADF addresses the needs of low-income countries

• ADF borrowers offered the flexibility to select the currency of their choice

Policy Update

2005 Activities Highlights

• Project lending prioritized agriculture and rural development, transport, social sectors and multi-sector activities which account for 84.2% of ADF loan approvals in 2005

• 2005 grant approvals benefited 18 countries and almost doubled to UA 415 million (US$ 593 million) from UA 214 million (US$ 332 million) in 2004

• 2005 grant operations focused on water and sanitation, agriculture and rural development, the social sector and transportation

Approvals

• UA 16.26 billion (US$ 23.24 billion) of assistance provided at end-2005 through ten replenishments of ADF

• Total approvals Increased to UA 1.42 billion (US$ 2.03 billion) in 2005 from UA 1.26 billion US$ 1.96 billion) in 2004

17

Through co-financing and partnership, the Bank Group enhances the resources and expertise mobilised for Africa

• From 1967 to 2005, the Bank participated in 852 co-financing operations, amounting to UA 84.2 billion (US$ 120.4 billion).

• In 2005, 19 operations for UA 3.2 billion (US$ 4.6 billion) were co-financed compared to 31 operations for UA 2.9 billion (US$ 4.4 billion) in 2004.

47.7%

6.7%

18.6%

0.6% 9.5% 1.2%

15.7%

Multisector Energy Sector Environment

Finance Transportation Agricultural Sector

Social Sector

Sector Distribution in 2005

18

The Multilateral Debt Relief Initiative launched in 2005 aims to complement the HIPC debt relief process

• HIPC debt relief is projected to substantially lower debt stocks and debt ratios for most HIPC beneficiaries

• 14 countries had reached completion point at end - 2005, 11 are at decision point and 7 are at pre-decision point

• The G8 Summit in July 2005 proposed that the ADF, IDA and IMF provide 100% irrevocable debt stock cancellation for countries that reach the completion point under the enhanced HIPC initiative

• 33 of the 42 eligible countries are in Africa

• Underlying Principles: Irrevocability and additionality of debt relief as well as preservation of the financial integrity of ADF and IDA

• Based on debt outstanding and disbursed at December 31, 2004, as the cut-off date, and January 1, 2006, as the implementation date, the cost of canceling the ADF debt of the 33 potential beneficiaries, after HIPC relief, is estimated at UA 5.84 billion (US$9.06 billion) in nominal terms.

• Donors will make new contributions to match, “dollar-for-dollar”, foregone principal and service charge payments based on an agreed burden sharing

Heavily Indebted

Poor Countries

Initiative

Heavily Indebted

Poor Countries

Initiative

Multilateral

Debt Relief

Initiative

Multilateral

Debt Relief

Initiative

19

The Bank Group continues to champion vital initiatives on the continent

Global statistics initiative to meet the demand for reliable regular and comparable data, and to strengthen statistical capacity in the continent leading to increased investor confidence and private capital flows. In 2005, under the supervision of the Bank, 48 RMCs started monthly data collection, providing the Bank with the monthly price data of available goods and services for 853 products.

Conceived by the Bank to assist countries emerging from conflicts to clear their arrears, re-engage with development partners and become fully reintegrated in the international community. At end 2005, the arrears of Burundi and the Republic of Congo have been cleared

through this facility.

Bank selected in 2005 to host the Secretariat of the African Infrastructure Consortium for which NEPAD is lead infrastructure agency.Took part in all support missions in 2004 and 2005 to launch APRM in nine countries and the actual peer review missions in Ghana, Rwanda and Kenya.

Rural Water Supply and Sanitation Initiative: (RWSSI) was launched by the Bank in 2004 to provide safe water and basic sanitation to 80% of the rural populations in Africa by 2015. It is a USD 14.2 billion initiative to be financed by ADF, donors, government resources and beneficiaries. At end 2005, 8 RWSSI programs and 2 studies were approved.

African Water Facility: This USD 600 million facility seeks to strengthen water resource management in the continent. At end 2005, donor countries had pledged EUR 9.9 million in financial support. The Bank has committed EUR 1.8 million over 3 years.

Post-Conflict Country Facility

Water Initiatives

20

Strengthen the Bank’s operations

with renewed country focus and greater

delegation to regional offices

Adapt the Bank’s structure to enable it to fulfill its mandate better

Invest in Bank Staff and improve business and

administration processes

Deepen the Bank’s research capacity

TASK FORCE ON

INSTITUTIONAL REFORM

The Bank continues to build on the strong foundation laid by past reforms to serve its regional members more effectively

21

The Bank’s decentralization process is well under way

Algeria

Angola

Burkina Faso

Cameroon

Chad

DRC

Ghana

Kenya

Malawi

Morocco

Rwanda

Sierra Leone

Sudan

Zambia

Offices Logistically Operational

Egypt

Ethiopia

Gabon

Nigeria

Madagascar

Mali

Mozambique

Senegal

Tanzania

Uganda

Offices Planned/

Work-in Progress 25 Offices to be established before the end

of 2006

Countries covered would represent approx. 89% of the Bank’s current portfolio

Strengthening institutional capabilities, ensuring greater development and making the Bank more client-responsive

Field offices expected to strengthen country dialogue, country portfolio performance and project implementation

25 Offices to be established before the end of 2006

Countries covered would represent approx. 89% of the Bank’s current portfolio

Strengthening institutional capabilities, ensuring greater development and making the Bank more client-responsive

Field offices expected to strengthen country dialogue, country portfolio performance and project implementation

22

The Bank’s robust financial position bolsters its ability to deliver on its development mandate

Bank Financial Profile33

23

The Bank enjoys strong shareholder support for its development mandate

Netherlands NorwayPortugalSpainSwedenSwitzerlandUK

Canada USA

Europe 21%

AlgeriaAngolaBeninBotswanaBurkina FasoBurundiCameroonCape VerdeCentral Afr. Rep.ChadComorosCongoCôte d’Ivoire D. R. CongoDjiboutiEgyptEquatorial

NamibiaNigerNigeriaRwandaS. Tome & PrincipeSenegal SeychellesSierra LeoneSomaliaSouth AfricaSudanSwazilandTanzaniaTogo TunisiaUgandaZambiaZimbabwe

Africa 60%

Americas 11%

AustriaBelgiumDenmarkFinlandFranceGermanyItaly

Middle East 0.7%

Kuwait Saudi Arabia

IndiaJapan

Asia7.3%

ChinaKorea

Argentina Brazil

GuineaEritreaEthiopiaGabonGambiaGhanaGuineaGuinea BissauKenyaLesothoLibyaMadagascarMalawiMaliMauritaniaMauritiusMoroccoMozambique

24

The ADB’s strong financial condition protects its bondholders

* Not restated. The Bank defines “usable capital” as the sum of paid-in capital, reserves, and callable capital of countries rated double-A and above

57.6%60.3%61.6%

47.9%51.2%

0%

50%

100%

2001* 2002* 2003* 2004 2005

Debt / Usable Capital* Policy Limit

LeverageLeverage

25

Growing reserves and stable earnings enhance the Bank’s risk bearing capacity…

221144178189125

1,5081,465

1,266

2,2662,187

2001* 2002* 2003* 2004** 2005

Net Income Total Reserves

In UA million

* These figures have not been restated. Net income figures exclude the IAS 39 adjustment.**The total amount transferred to reserves on 1 January 2005 due to the application of the IFRS changes was UA 700.18 million.

2005Net incomeUS$ 316 million

ReservesUS$ 3,239 million

26

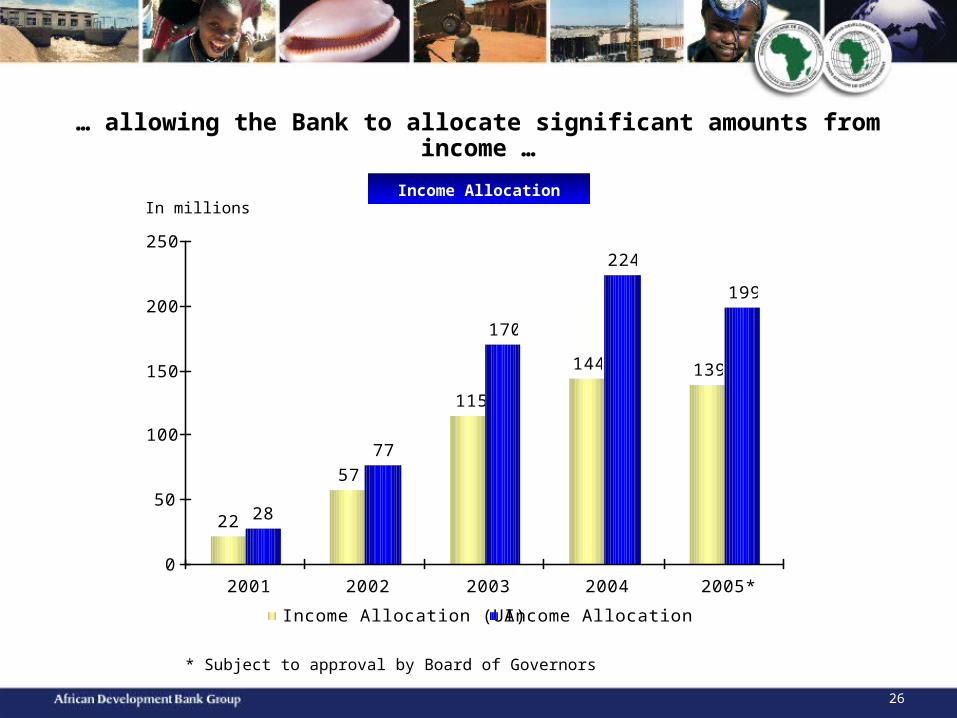

… allowing the Bank to allocate significant amounts from income …

22

57

115

144 139

28

77

170

224

199

0

50

100

150

200

250

2001 2002 2003 2004 2005*

Income Allocation (UA) Income Allocation (US$)

In millions

* Subject to approval by Board of Governors

Income Allocation

27

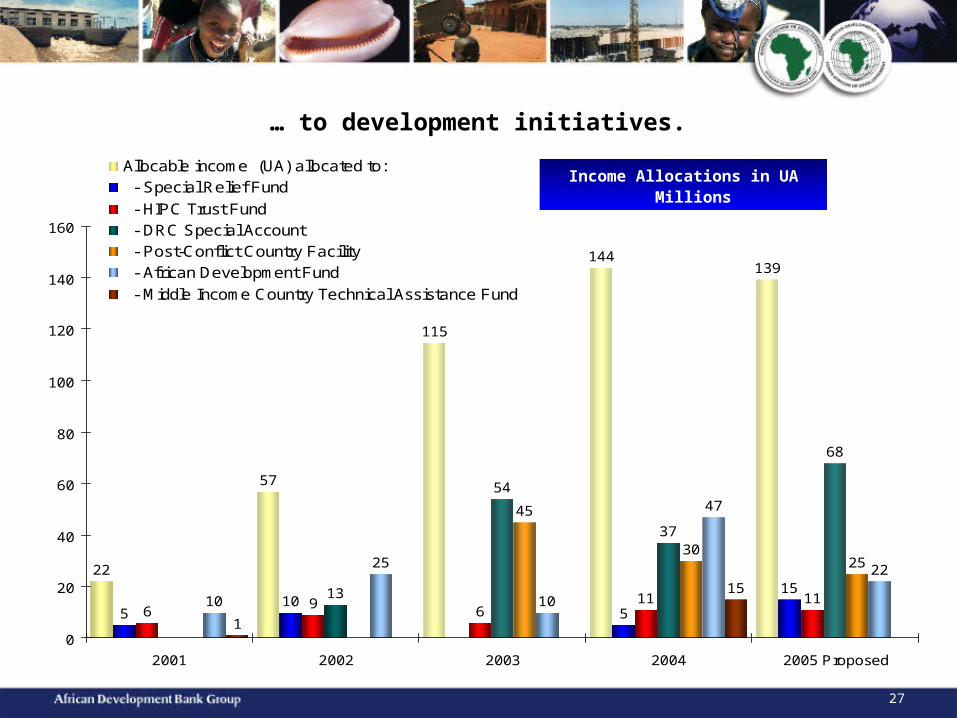

… to development initiatives.

22

57

115

144139

510

5

15

69

611 1113

54

37

68

45

3025

10

25

10

47

22

1

15

0

20

40

60

80

100

120

140

160

2001 2002 2003 2004 2005 Proposed

Allocable income (UA) allocated to: - Special Relief Fund

- HIPC Trust Fund - DRC Special Account - Post-Conflict Country Facility - African Development Fund

- Middle Income Country Technical Assistance Fund

Income Allocations in UA Millions

28

The Bank’s exceptional risk bearing capacity reinforces its ability to operate in a challenging environment

1,948 1,983 2,023 2,066 2,112

2,187 2,266

1,2661,5071,465

494469491

0

1,000

2,000

3,000

4,000

5,000

2001 2002 2003 2004 2005

Paid-in capital Reserves Loan loss provisions

Uses of risk capital

In UA million

Based on the effects of the revised IFRS, effective 1 January 2005, the nature of loan loss provisions has changed from ‘general’ to ‘specific’; accordingly, loan loss provisions represent a reduction in the exposure to the relevant country, not a source of risk capital. Therefore, the main components of the Total Risk Capital are Paid-in Capital and Reserves.

Unused risk capital49%

Sovereign portfolio

45%

Treasury2%

Non-sovereign portfolio

4%

As of 31 December 2005As of 31 December 2005

2005 Risk capital

Paid-in capital: US 3,018 million

Reserves: US$ 3,239 million

2005 Risk capital

Paid-in capital: US 3,018 million

Reserves: US$ 3,239 million

Risk capital

29

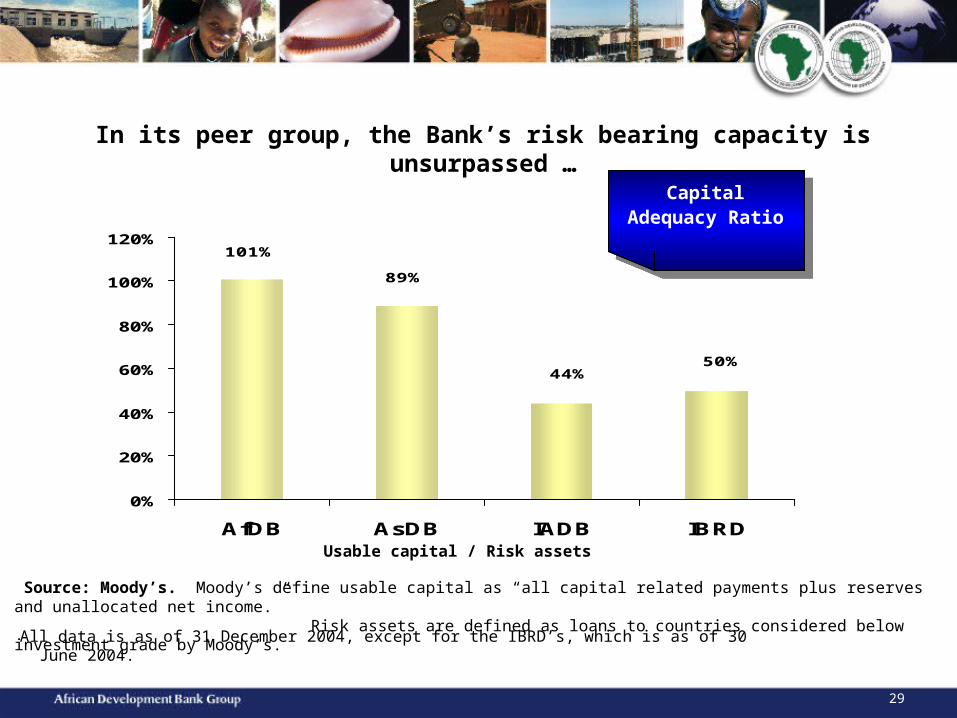

In its peer group, the Bank’s risk bearing capacity is unsurpassed …

101%

89%

44%50%

0%

20%

40%

60%

80%

100%

120%

AfDB AsDB IADB IBRDUsable capital / Risk assets

Source: Moody’s. Moody’s define usable capital as “all capital related payments plus reserves and unallocated net income.” Risk assets are defined as loans to countries considered below investment grade by Moody’s.

All data is as of 31 December 2004, except for the IBRD’s, which is as of 30 June 2004.

Capital Adequacy Ratio

Capital Adequacy Ratio

30

… and the Bank’s concentration risk is the lowest

86%

165%

191%

137%

0%

50%

100%

150%

200%

250%

ADB AsDB IADB IBRD

5 largest exposures to equitySource: Fitch

All data is as of 31 December 2004, except for the IBRD’s, which is as of 30 June 2004.

Concentration Ratio

Concentration Ratio

31

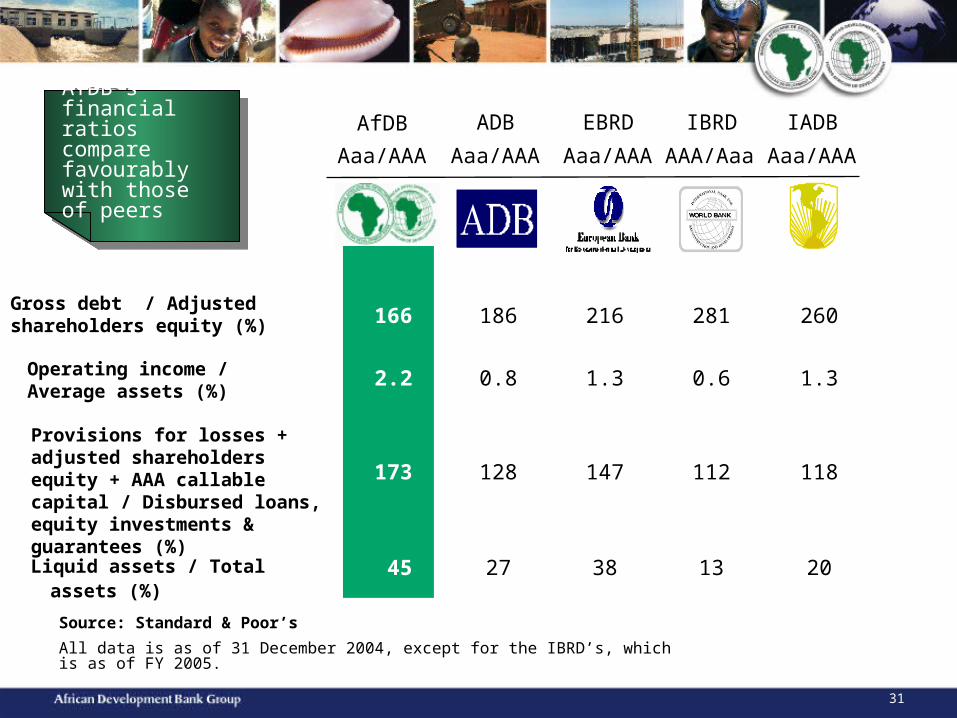

Aaa/AAA Aaa/AAA Aaa/AAA AAA/Aaa Aaa/AAA

AfDB ADB EBRD IBRD IADBAfDB’s financial ratios compare favourably with those of peers

AfDB’s financial ratios compare favourably with those of peers

Provisions for losses + adjusted shareholders equity + AAA callable capital / Disbursed loans, equity investments & guarantees (%)

Gross debt / Adjustedshareholders equity (%)

Operating income / Average assets (%)

Liquid assets / Total assets (%)

166 186 216 281 260

2.2 0.8 1.3 0.6 1.3

173 128 147 112 118

45 27 38 13 20

Source: Standard & Poor’s

All data is as of 31 December 2004, except for the IBRD’s, which is as of FY 2005.

32

CAPITAL MARKET ACTIVITIES44

The Bank is a flexible and responsive issuer in the capital markets

33

The Bank’s borrowing strategy enables it to provide cost-effective resources to African countries

ZAR 1.6%

USD 44.2%

BWP 0.6%

CAD 11.0%

CHF 2.6%

JPY 30.9%

GBP 1.0%

AUD 2.9%

EUR 5.0%HKD 0.1%

SEK 0.0%

Public bond issues in the Global, Euro and domestic markets

Private placements including structured notes

Loans Unlimited Global Debt Issuance Facility Euro 1 billion Commercial Paper

UA 5,940 million (US$ 8,490 million) as of 31 December 2005

Raise cost effective resources to on-lend to clients

Flexible in order to address investor needs Responsive to market trends Develop and nurture a well diversified investor

base Maintain a regular presence in the public

international markets

Public Issues 51.5%Private

Placements 24.4%

Uridashi 21.9%

Loans 2.3%

Instruments and debt programsInstruments and debt programs Funding StrategyFunding Strategy

Currency distribution and structure of the outstanding portfolioCurrency distribution and structure of the outstanding portfolio

34

The Bank maintains a constant presence in the global debt market

Americas 43%

Europe 15%

Asia 40%

Middle East & Africa 2%

2003 – USD 1,000 million Global 2003 – USD 1,000 million Global – – 3.25% due 20083.25% due 2008

2004 – USD 500 million Global – 3.75% due 20102004 – USD 500 million Global – 3.75% due 2010

2005 – USD 500 million Global – 4.50% due 20092005 – USD 500 million Global – 4.50% due 2009

Fund Managers

27%

Corporates 1%

Central Banks 48%

P ension Funds 5%

Insurance Companies

8%

Banks 11%

Investors – by TypeInvestors – by Type Investors – by GeographyInvestors – by Geography

35

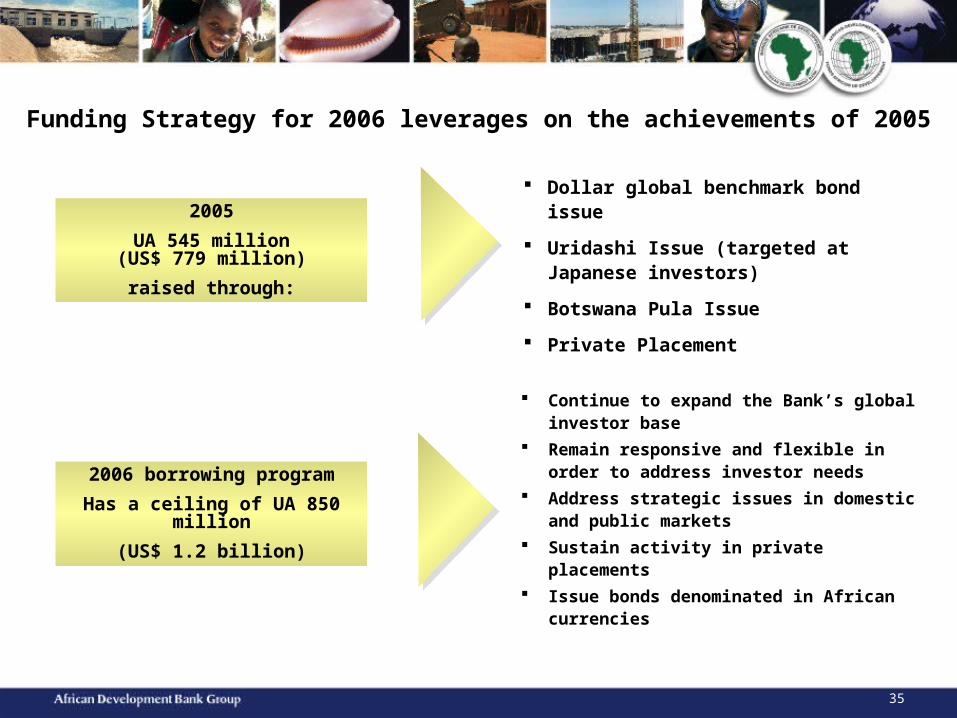

Funding Strategy for 2006 leverages on the achievements of 2005

Dollar global benchmark bond issue

Uridashi Issue (targeted at Japanese investors)

Botswana Pula Issue

Private Placement

2005

UA 545 million (US$ 779 million)

raised through:

Continue to expand the Bank’s global investor base

Remain responsive and flexible in order to address investor needs

Address strategic issues in domestic and public markets

Sustain activity in private placements

Issue bonds denominated in African currencies

2006 borrowing program

Has a ceiling of UA 850 million

(US$ 1.2 billion)

36

Building on success in African currencies

The Bank is monitoring issuance possibilities in several other African currencies

IFR Comments

“ … the transaction … represented the first true Eurobond in the currency….”

“… good demand from European institutions with the paper quickly sold out, primarily on the back of the chunky 10% coupon and the positive economic story that has emerged from Botswana since independence in 1966.”

EUROWEEK Comments

“AfDB defies pessimists to launch clearable pula Eurobond”

“The African Development Bank … priced the first Botswana pula Eurobond that will be fully clearable in the currency.”

IFR Comments

“The African Development Bank (AfDB) last week opened the door to the Tanzanian shilling market with a US$10m one-year currency-linked bond …”

EUROWEEK Comments

“AfDB introduces new market with synthetic Tanzanian shilling bond”

“The African Development Bank has become the first supranational borrower to issue a bond linked to the Tanzanian shilling”

BOTSWANAPULA ISSUE

BWP 300 million 10% due 12 January 2007

BOTSWANAPULA ISSUE

BWP 300 million 10% due 12 January 2007

TANZANIAN SHILLING ISSUE

USD 10 million linked to TZS11.8% due 20 February 2007

TANZANIAN SHILLING ISSUE

USD 10 million linked to TZS11.8% due 20 February 2007

37

The Bank enjoys the highest credit rating

Strong Support from Member Countries

Healthy Capital Position

Excellent LiquidityPreferred Creditor Status

Prudent Financial Management

Franchise Value

Quality of Management

38

APPENDIX

39

ADB: Summary financial information

In UA million

Net Income

Reserves

Paid in Capital*** net of CEAS

Subscribed Capital

Approvals

Assets

2001 2002 2003 2004 2005

987 1,068 746 1,520 869

8,873 8,197 10,034 10,792 11,601

21,491 21,510 21,564 21,597 21,636

1,770 1,803 1,866 1,920 1,967

1,266 1,465 1,508 2,187** 2,266

125* 189* 178* 144 221

* These figures have not been restated. Net income figures exclude the IAS 39 adjustment. **The total amount transferred to reserves on 1 January 2005 due to the application of the IFRS changes was UA 700.18 million.***Paid-in Capital excludes non-convertible currencies and non-negotiable notes

40

ADB: Statement of income and expenses (UA million)

YEARS ENDED 31 DECEMBER 2005 2004 2003 2002 2001

OPERATIONAL INCOME AND EXPENSESIncome from loans 324.23 323.11 325.46 414.82 447.82Income from investments 155.37 123.57 99.77 74.01 121.32Total operational income 479.60 446.68 425.23 488.83 569.14 Interest and amortized issuance costs (217.12) (197.08) (219.59) (258.69) (349.45) Unrealized loss/(gains) fair valued borrowings and related derivatives (30.77) (7.70) (81.65) 37.20 82.30 Unrealized gain/(loss) derivatives on non fair valued borrowings 7.22 (10.35)

Provision for loan losses 13.85 (53.86) 21.51 (3.49) (53.80)Net operational income 252.78 177.69 145.51 263.86 248.20

OTHER EXPENSES, netAdministration expenses 155.69 142.20 109.32 81.82 73.99Management fees (114.02) (104.59) (77.55) (59.50) (52.19)Administration expenses - net (41.67) (37.61) (45.14) (32.27) (30.35)Other income 15.72 7.40 2.61 1.25 1.40Depreciation (7.10) (6.42) (5.57) (5.51) (5.88)Provision for equity investments 0.75 3.31 (1.68) (0.06) (5.62)Loss/(gain) on exchange (0.74) (0.84) 0.98 (1.20) (0.09)

Translation gains and losses 1.58Total other expenses, net (31.46) (34.16) (48.80) (37.79) (40.54)

Net income 221.32 143.53 96.71 226.07 207.66

2004 has been restated

41

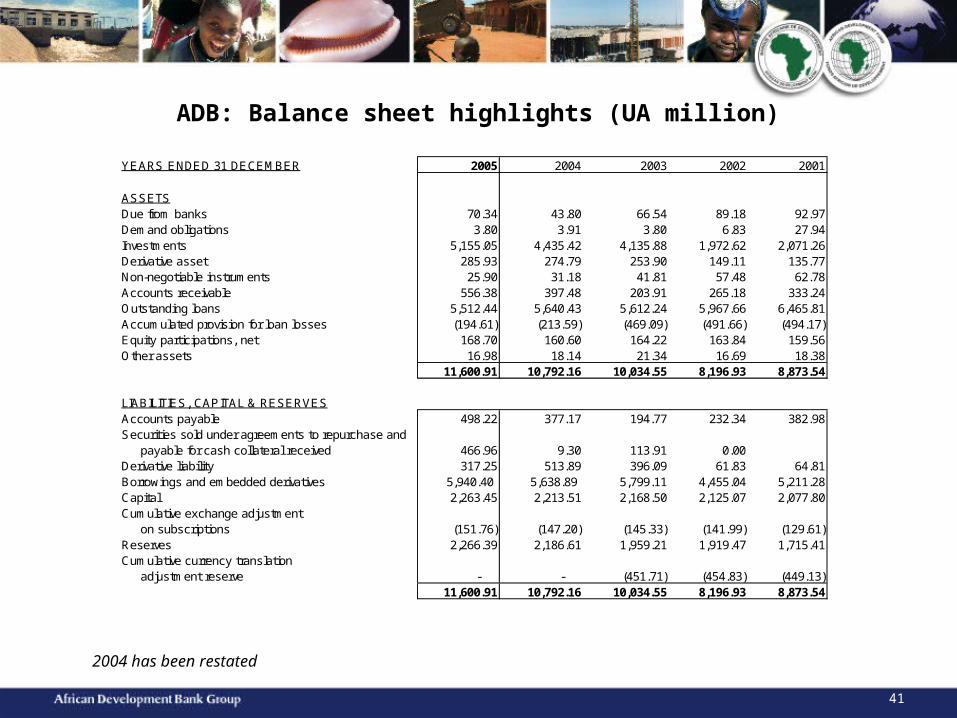

ADB: Balance sheet highlights (UA million)

YEARS ENDED 31 DECEMBER 2005 2004 2003 2002 2001

ASSETSDue from banks 70.34 43.80 66.54 89.18 92.97Demand obligations 3.80 3.91 3.80 6.83 27.94Investments 5,155.05 4,435.42 4,135.88 1,972.62 2,071.26Derivative asset 285.93 274.79 253.90 149.11 135.77Non-negotiable instruments 25.90 31.18 41.81 57.48 62.78Accounts receivable 556.38 397.48 203.91 265.18 333.24Outstanding loans 5,512.44 5,640.43 5,612.24 5,967.66 6,465.81Accumulated provision for loan losses (194.61) (213.59) (469.09) (491.66) (494.17)Equity participations, net 168.70 160.60 164.22 163.84 159.56Other assets 16.98 18.14 21.34 16.69 18.38

11,600.91 10,792.16 10,034.55 8,196.93 8,873.54

LIABILITIES, CAPITAL & RESERVESAccounts payable 498.22 377.17 194.77 232.34 382.98Securities sold under agreements to repurchase and payable for cash collateral received 466.96 9.30 113.91 0.00Derivative liability 317.25 513.89 396.09 61.83 64.81Borrowings and embedded derivatives 5,940.40 5,638.89 5,799.11 4,455.04 5,211.28Capital 2,263.45 2,213.51 2,168.50 2,125.07 2,077.80Cumulative exchange adjustment on subscriptions (151.76) (147.20) (145.33) (141.99) (129.61)Reserves 2,266.39 2,186.61 1,959.21 1,919.47 1,715.41Cumulative currency translation adjustment reserve - - (451.71) (454.83) (449.13)

11,600.91 10,792.16 10,034.55 8,196.93 8,873.54

2004 has been restated

42

More information on the Bank Group is available at www.afdb.org

Financial and Operational Analysis

Documentation for Debt Programs

Rating Agencies Reports

Financial Products for Borrowers

Exchange Rates

Annual Report

Financial Information in Japanese for investors is NOW available at www.afdb-org.jp