©2003 thomson/south-western 1 chapter 19 – decision making under uncertainty slides prepared by...

TRANSCRIPT

©2003 Thomson/South-Western 1

Chapter 19 –Chapter 19 –

Decision Decision Making Under Making Under UncertaintyUncertainty

Slides prepared by Jeff Heyl, Lincoln UniversitySlides prepared by Jeff Heyl, Lincoln University©2003 South-Western/Thomson Learning™

Introduction toIntroduction to Business StatisticsBusiness Statistics, 6e, 6eKvanli, Pavur, KeelingKvanli, Pavur, Keeling

©2003 Thomson/South-Western 2

Two Basic QuestionsTwo Basic Questions

What are the possible actions What are the possible actions (alternatives) for this problem?(alternatives) for this problem?

What is it about the future that What is it about the future that affects the desirability of each affects the desirability of each action?action?

©2003 Thomson/South-Western 3

TermsTerms Descriptions of the future: states of Descriptions of the future: states of

naturenature The state of nature items are outcomes.The state of nature items are outcomes.

The key distinction between an action and a The key distinction between an action and a state of nature is that the action is taken is state of nature is that the action is taken is under your control, whereas the state of under your control, whereas the state of nature that occurs is strictly a matter of nature that occurs is strictly a matter of chance.chance.

The payoff is the result of an action (A) an The payoff is the result of an action (A) an a state of nature (S)a state of nature (S)

©2003 Thomson/South-Western 4

Payoff TablePayoff Table

States of NatureStates of Nature

ActionAction SS11 SS22 SS33 …… SSnn

AA11 1111 1212 1313 …… 11nn

AA22 2121 2222 2323 …… 22nn

AA33 3131 3232 3333 …… 33nn

AAkk kk11 kk22 kk33 …… knkn

Table 19.1Table 19.1

©2003 Thomson/South-Western 5

Conservative (Minimax) Conservative (Minimax) StrategyStrategy

The action chosen is that action that The action chosen is that action that under the under the worstworst conditions produces the conditions produces the lowest “loss”lowest “loss”

The opportunity loss, LThe opportunity loss, Lijij, is the difference , is the difference

between the payoff for action I and the between the payoff for action I and the payoff for the action that would have the payoff for the action that would have the largest payoff under the state of nature jlargest payoff under the state of nature j

©2003 Thomson/South-Western 6

Minimax StrategyMinimax Strategy

Construct an opportunity loss table by Construct an opportunity loss table by using the maximum payoff for each state using the maximum payoff for each state of natureof nature

Determine the maximum opportunity loss Determine the maximum opportunity loss for each actionfor each action

Find the minimum value of the Find the minimum value of the opportunity losses found in step 2; the opportunity losses found in step 2; the corresponding action is the one selectedcorresponding action is the one selected

©2003 Thomson/South-Western 7

The Gambler (Maximax) The Gambler (Maximax) StrategyStrategy

The Maximax strategy is to choose The Maximax strategy is to choose that action having the largest that action having the largest

possible payoffpossible payoff

©2003 Thomson/South-Western 8

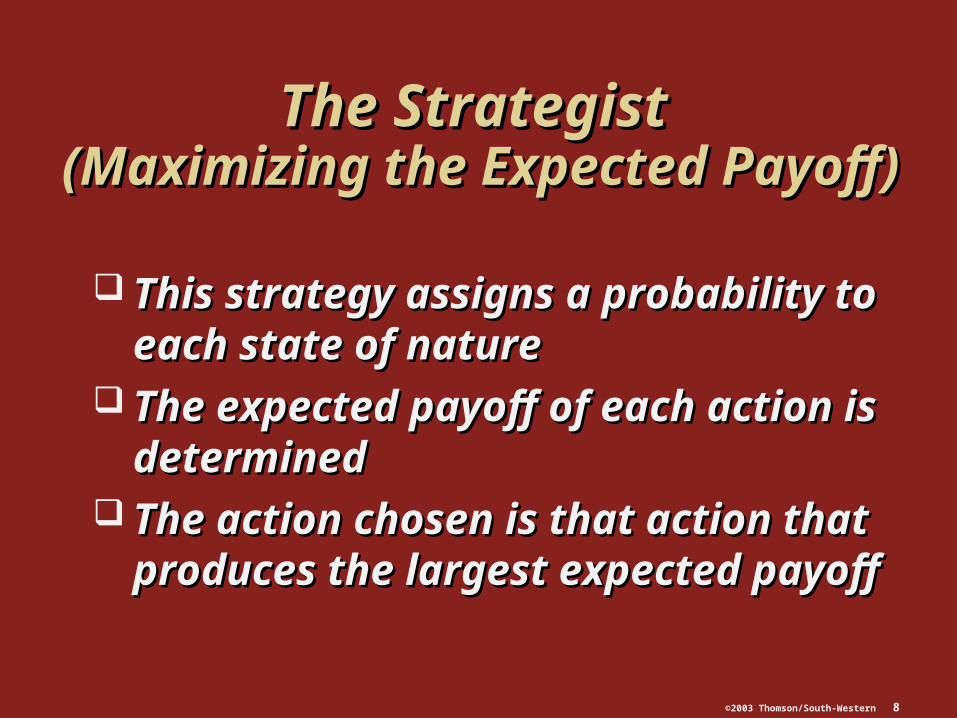

The Strategist The Strategist (Maximizing the Expected Payoff)(Maximizing the Expected Payoff)

This strategy assigns a probability to This strategy assigns a probability to each state of natureeach state of nature

The expected payoff of each action is The expected payoff of each action is determineddetermined

The action chosen is that action that The action chosen is that action that produces the largest expected payoffproduces the largest expected payoff

©2003 Thomson/South-Western 9

Sailtown ExampleSailtown Example

Average Interest RateAverage Interest Rate

Amount OrderedAmount Ordered Increases (Increases (SS11)) Steady (Steady (SS22)) Decreases (Decreases (SS33))

50 (50 (AA11)) 1515 1515 1515

75 (75 (AA22)) 2.52.5 22.522.5 22.522.5

100 (100 (AA33)) -10-10 3030 3030

150 (150 (AA44)) -35-35 55 4545

Table 19.1Table 19.1

©2003 Thomson/South-Western 10

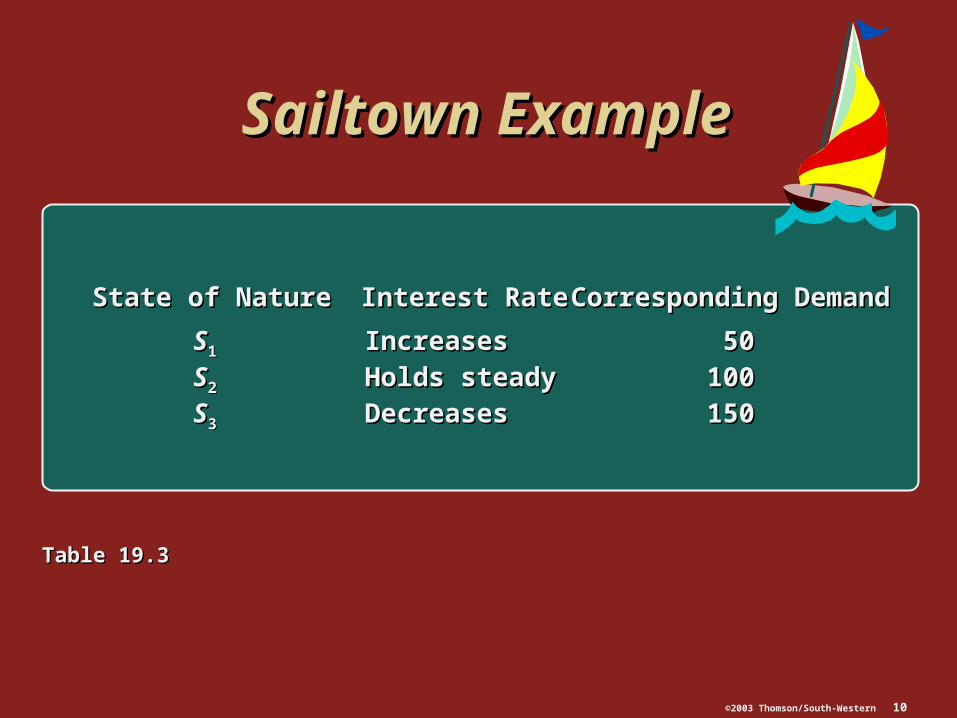

Sailtown ExampleSailtown Example

Table 19.3Table 19.3

State of NatureState of Nature Interest RateInterest Rate Corresponding DemandCorresponding Demand

SS11 IncreasesIncreases 5050

SS22 Holds steadyHolds steady 100100

SS33 DecreasesDecreases 150150

©2003 Thomson/South-Western 11

Sailtown ExampleSailtown Example

Revenue forRevenue for Loss Due toLoss Due toActionAction Boats SoldBoats Sold Returned BoatsReturned Boats Net PayoffNet Payoff

AA11 50 • $15,00050 • $15,000 0 • 5000 • 500 = $0= $0 $15,000$15,000

AA22 50 • $15,00050 • $15,000 25 • 50025 • 500 = $12,00= $12,00 $2.500$2.500

AA33 50 • $15,00050 • $15,000 50 • 50050 • 500 = $25,000= $25,000 -$10,000-$10,000

AA44 50 • $15,00050 • $15,000 100 • 500100 • 500 = $50,000= $50,000 -$35,000-$35,000

Table 19.4Table 19.4

©2003 Thomson/South-Western 12

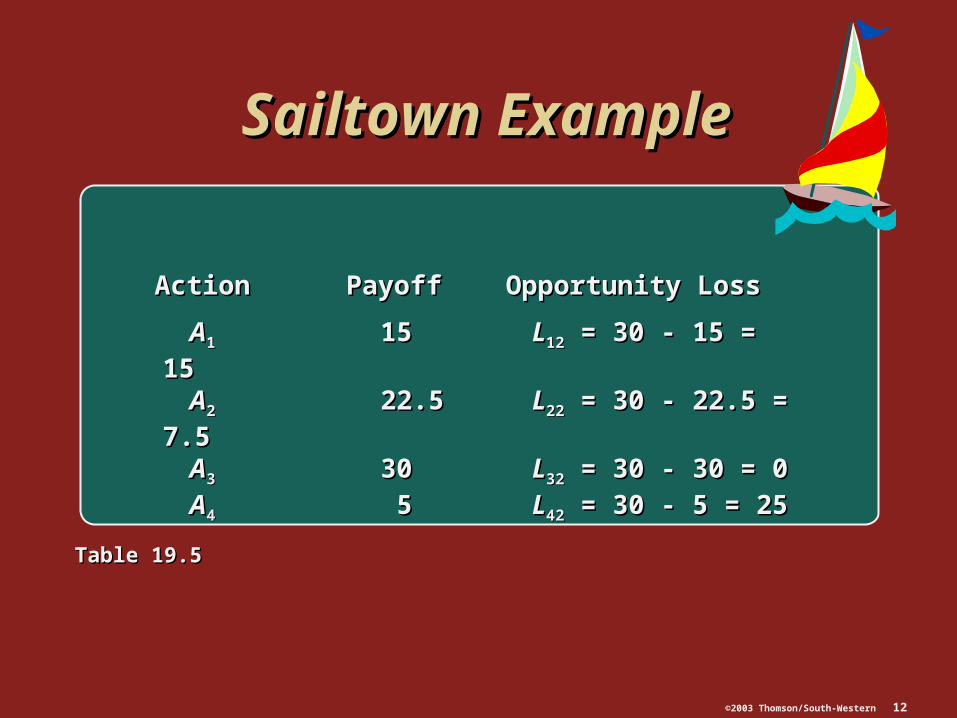

Sailtown ExampleSailtown Example

ActionAction PayoffPayoff Opportunity LossOpportunity Loss

AA11 1515 LL1212 = 30 - 15 = 15 = 30 - 15 = 15

AA22 22.522.5 LL2222 = 30 - 22.5 = 7.5 = 30 - 22.5 = 7.5

AA33 3030 LL3232 = 30 - 30 = 0 = 30 - 30 = 0

AA44 55 LL4242 = 30 - 5 = 25 = 30 - 5 = 25

Table 19.5Table 19.5

©2003 Thomson/South-Western 13

Sailtown ExampleSailtown Example

ActionAction PayoffPayoff Opportunity LossOpportunity Loss

AA11 1515 LL1212 = 45 - 15 = 30 = 45 - 15 = 30

AA22 22.522.5 LL2222 = 45 - 22.5 = 22.5 = 45 - 22.5 = 22.5

AA33 3030 LL3232 = 45 - 30 = 15 = 45 - 30 = 15

AA44 4545 LL4242 = 45 - 5 = 0 = 45 - 5 = 0

Table 19.6Table 19.6

©2003 Thomson/South-Western 14

Sailtown ExampleSailtown Example

Table 19.7Table 19.7

State of NatureState of Nature

ActionAction SS11 SS22 SS33

AA11 00 1515 3030

AA22 12.512.5 7.57.5 22.522.5

AA33 2525 00 1515

AA44 5050 2525 00

©2003 Thomson/South-Western 15

Sailtown ExampleSailtown Example

State of NatureState of Nature ProbabilityProbability

SS11: Interest rate increases: Interest rate increases PP((SS11) = .3) = .3

SS22: Interest rate remains unchanged: Interest rate remains unchanged PP((SS22) = .2) = .2

SS33: Interest rate decreases: Interest rate decreases PP((SS33) = .5) = .5

Table 19.10Table 19.10

©2003 Thomson/South-Western 16

Sailtown ExampleSailtown Example

ActionAction Expected PayoffExpected Payoff

AA11: Order 50 sailboats: Order 50 sailboats (15)(.3) + (15)(.2) + (15)(.5) = 15(15)(.3) + (15)(.2) + (15)(.5) = 15

AA22: Order 75 sailboats: Order 75 sailboats (2.5)(.3) + (22.5)(.2) + (22.5)(.5) = 16.5(2.5)(.3) + (22.5)(.2) + (22.5)(.5) = 16.5

AA33: Order 100 sailboats: Order 100 sailboats (-10)(.3) + (30)(.2) + (30)(.5) = 18(-10)(.3) + (30)(.2) + (30)(.5) = 18

AA44: Order 150 sailboats: Order 150 sailboats (-35)(.3) + (5)(.2) + (45)(.5) = 13(-35)(.3) + (5)(.2) + (45)(.5) = 13

Table 19.11Table 19.11

©2003 Thomson/South-Western 17

Sailtown ExampleSailtown Example

Table 19.16Table 19.16

Expected PayoffExpected Payoff

PP((SS11)) PP((SS22)) PP((SS33)) AA11 AA22 AA33 AA44

.4.4 .2.2 .4.4 1515 14.514.5 1414 55

.4.4 .3.3 .3.3 1515 14.514.5 1414 11

.4.4 .1.1 .5.5 1515 14.514.5 1414 99

.5.5 .2.2 .3.3 1515 12.512.5 1010 -3-3

.5.5 .1.1 .4.4 1515 12.512.5 1010 11

.3.3 .3.3 .4.4 1515 16.516.5 1818 99

.3.3 .2.2 .5.5 1515 16.516.5 1818 1313

©2003 Thomson/South-Western 18

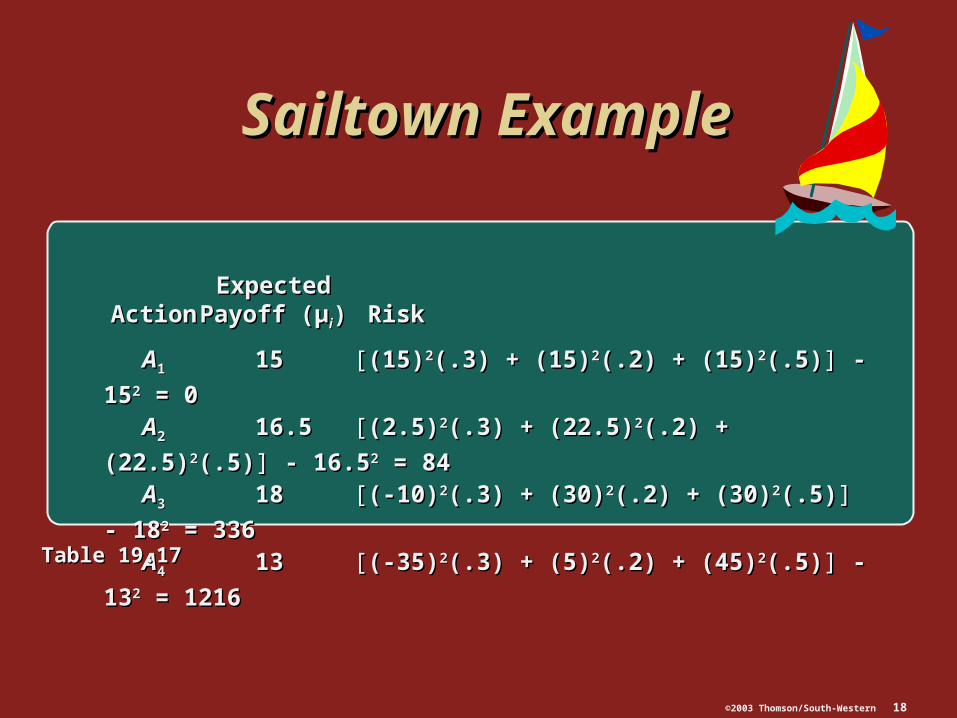

Sailtown ExampleSailtown Example

ExpectedExpectedActionAction Payoff (µPayoff (µii)) Risk Risk

AA11 1515 [[(15)(15)22(.3) + (15)(.3) + (15)22(.2) + (15)(.2) + (15)22(.5)(.5)]] - 15 - 1522 = 0 = 0

AA22 16.516.5 [[(2.5)(2.5)22(.3) + (22.5)(.3) + (22.5)22(.2) + (22.5)(.2) + (22.5)22(.5)(.5)]] - 16.5 - 16.522 = 84 = 84

AA33 1818 [[(-10)(-10)22(.3) + (30)(.3) + (30)22(.2) + (30)(.2) + (30)22(.5)(.5)]] - 18 - 1822 = 336 = 336

AA44 1313 [[(-35)(-35)22(.3) + (5)(.3) + (5)22(.2) + (45)(.2) + (45)22(.5)(.5)]] - 13 - 1322 = 1216 = 1216

Table 19.17Table 19.17

©2003 Thomson/South-Western 19

Sailtown ExampleSailtown Example

Figure 18.1Figure 18.1

©2003 Thomson/South-Western 20

UtilityUtility

Utility combines the decision Utility combines the decision maker’s attitude toward the payoff maker’s attitude toward the payoff and the corresponding risk of each and the corresponding risk of each alternativealternative

The utility value of a particular The utility value of a particular outcome is used to measure both outcome is used to measure both the attractiveness and the risk the attractiveness and the risk associated with this dollar amountassociated with this dollar amount

©2003 Thomson/South-Western 21

Utility ValueUtility Value

Step 1: Assign a utility value of Step 1: Assign a utility value of 00 to to the smallest payoff amount (the smallest payoff amount (minmin ) and ) and

a value of a value of 100100 to the largest ( to the largest (maxmax ) )

Step 2: The utility value for any payoff Step 2: The utility value for any payoff under consideration is found by under consideration is found by using:U(using:U(ijij) = P ) = P * 100* 100

©2003 Thomson/South-Western 22

UtilityUtility

Utility of 11,200Utility of 11,200

Uti

lity

Uti

lity

100100

5050

00

|

11,20011,200

|

40,00040,000ProfitProfit

Figure 18.2Figure 18.2

©2003 Thomson/South-Western 23

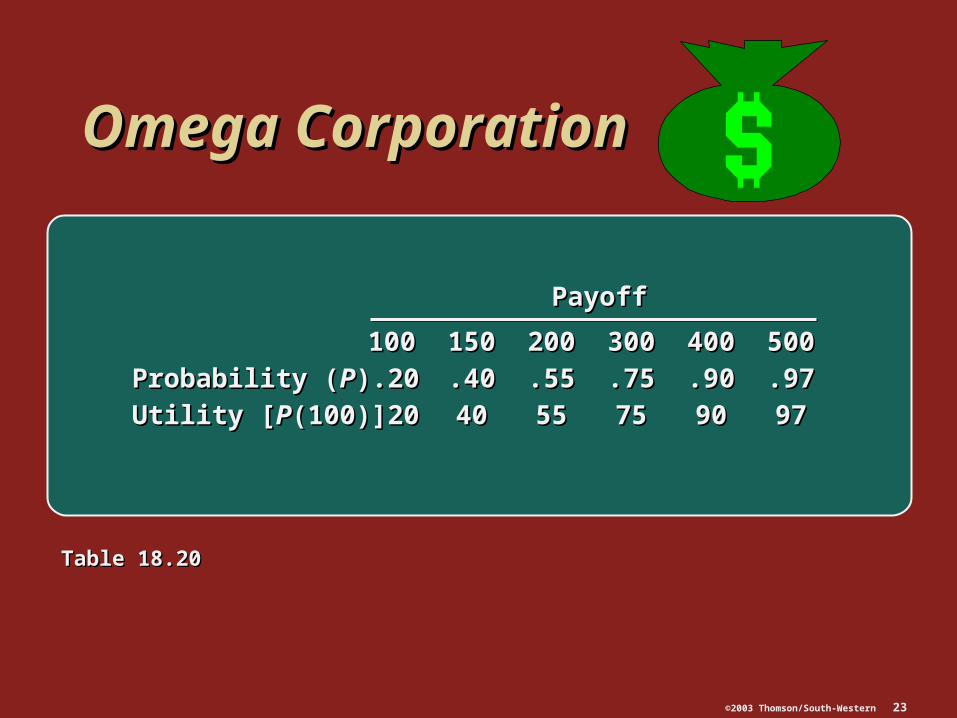

Omega CorporationOmega Corporation

PayoffPayoff

100100 150150 200200 300300 400400 500500

Probability (Probability (PP)) .20.20 .40.40 .55.55 .75.75 .90.90 .97.97

Utility [Utility [PP(100)](100)] 2020 4040 5555 7575 9090 9797

Table 18.20Table 18.20

©2003 Thomson/South-Western 24

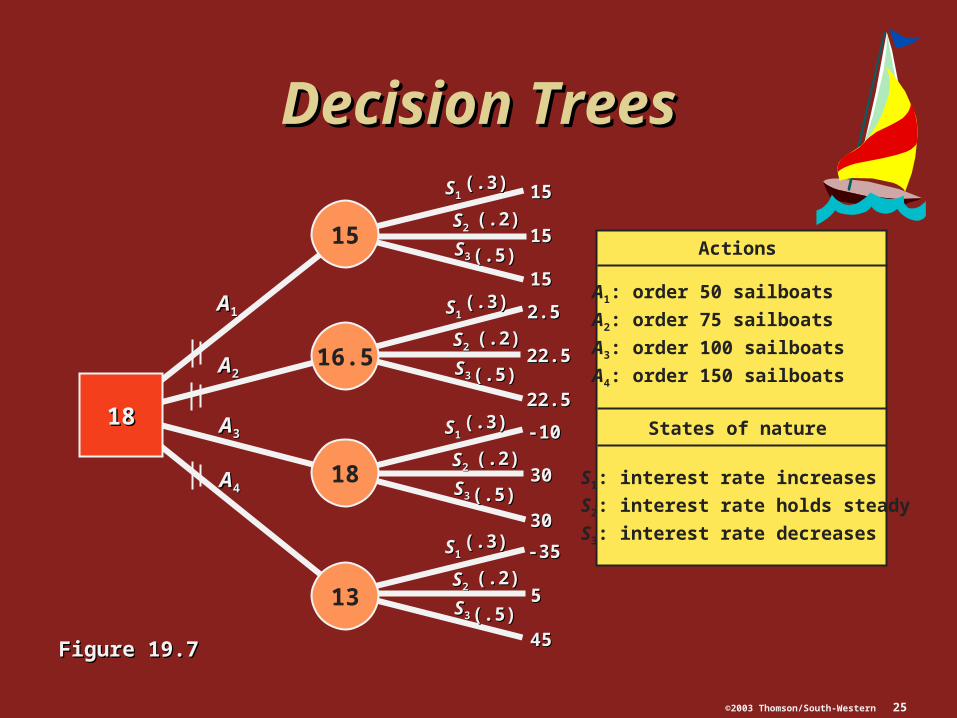

Decision Trees Decision Trees and Bayes’ Ruleand Bayes’ Rule

A decision tree graphically represents A decision tree graphically represents the entire decision problem, including:the entire decision problem, including: The possible actions facing the decision The possible actions facing the decision

makermaker The outcomes that can occurThe outcomes that can occur The relationships between the actions The relationships between the actions

and outcomesand outcomes

©2003 Thomson/South-Western 25

Decision TreesDecision Trees

1818

15

16.5

18

13

AA11

AA22

AA33

AA44

SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

1515

1515

1515

2.52.5

22.522.5

22.522.5

-10-10

3030

3030

-35-35

55

4545

Actions

States of nature

A1: order 50 sailboats

A2: order 75 sailboats

A3: order 100 sailboats

A4: order 150 sailboats

S1: interest rate increases

S2: interest rate holds steady

S3: interest rate decreases

Figure 19.7Figure 19.7

©2003 Thomson/South-Western 26

Decision Trees Decision Trees and Bayes’ Ruleand Bayes’ Rule

Bayes’ rule allows you to revise a Bayes’ rule allows you to revise a probability in light of certain probability in light of certain information that is providedinformation that is provided

PP((EEii||BB) = =) = =PP((EEii and and BB))

PP((BB))

iith pathth path

sum of pathssum of paths

©2003 Thomson/South-Western 27

Use of Bayes’ RuleUse of Bayes’ Rule

AA11

AA22

AA33

AA44

SS11

SS22

SS33

SS11

SS22

SS33

SS11

SS22

SS33

SS11

SS22

SS33

1515

1515

1515

2.52.5

22.522.5

22.522.5

-10-10

3030

3030

-35-35

55

4545

Actions

States of nature

A1: order 50 sailboats

A2: order 75 sailboats

A3: order 100 sailboats

A4: order 150 sailboats

S1: interest rate increases

S2: interest rate holds steady

S3: interest rate decreases

Figure 19.8Figure 19.8

©2003 Thomson/South-Western 28

Deriving the Posterior Deriving the Posterior ProbabilitiesProbabilities

Consultant predicts an increase (Consultant predicts an increase (II11))

Consultant predicts an increase (Consultant predicts an increase (II11))

Consultant predicts an increase (Consultant predicts an increase (II11))

.7.7

.4.4

.2.2

SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

Figure 19.9Figure 19.9

©2003 Thomson/South-Western 29

Resulting Decision TreeResulting Decision Tree

AA11

AA22

AA33

AA44

SS11

SS22

SS33

(.538)(.538)

(.205)(.205)

(.256)(.256)

(.538)(.538)

(.205)(.205)

(.256)(.256)

(.538)(.538)

(.205)(.205)

(.256)(.256)

(.538)(.538)

(.205)(.205)

(.256)(.256)

1515

1515

1515

2.52.5

22.522.5

22.522.5

-10-10

3030

3030-35-35

55

4545

SS11

SS22

SS33

SS11

SS22

SS33

SS11

SS22

SS33

15

8.45

-6.28

11.72

Consultant predictsConsultant predicts

an increase (an increase (II11))1818

Figure 19.10Figure 19.10

©2003 Thomson/South-Western 30

Completed Completed Decision Decision Tree for Tree for Sailtown Sailtown ProblemProblem

Figure 19.11Figure 19.11

AA11

AA22

AA33

AA44

SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

1515

1515

1515SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

2.52.5

22.522.5

22.522.5SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

-10-10

3030

3030SS11

SS22

SS33

(.3)(.3)

(.2)(.2)

(.5)(.5)

-35-35

55

4545

21.321.3

15

13

16.5

18

AA11

AA22

AA33

AA44

SS11

SS22

SS33

(.538)(.538)

(.205)(.205)

(.256)(.256)

1515

1515

15152.52.5

22.522.5

22.522.5-10-10

3030

3030-35-35

55

4545

1515

15

SS11

SS22

SS33

(.538)(.538)

(.205)(.205)

(.256)(.256)-6.28

SS11

SS22

SS33

(.538)(.538)

(.205)(.205)

(.256)(.256)

SS11

SS22

SS33

(.538)(.538)

(.205)(.205)

(.256)(.256)

11.72

8.45

AA11

AA22

AA33

AA44

20.7920.79

SS11

SS22

SS33

(.231)(.231)

(.385)(.385)

(.385)(.385)

1515

1515

1515

15

SS11

SS22

SS33

(.231)(.231)

(.385)(.385)

(.385)(.385)

-35-35

55

4545

11.16

SS11

SS22

SS33

(.231)(.231)

(.385)(.385)

(.385)(.385)

2.52.5

22.522.5

22.522.517.90

SS11

SS22

SS33

(.231)(.231)

(.385)(.385)

(.385)(.385)

-10-10

3030

3030

20.79

AA11

AA22

AA33

AA44

SS11

SS22

SS33

(.086)(.086)

(.057)(.057)

(.857)(.857)

1515

1515

15152.52.5

22.522.5

22.522.5-10-10

3030

3030-35-35

55

4545

35.8435.84

15

SS11

SS22

SS33

(.086)(.086)

(.057)(.057)

(.857)(.857)35.84

SS11

SS22

SS33

(.086)(.086)

(.057)(.057)

(.857)(.857)

SS11

SS22

SS33

(.086)(.086)

(.057)(.057)

(.857)(.857)

20.78

26.56

23.80

-2.5

NoNoadditional additional informationinformation

PurchasePurchaseadditionaladditionalinformationinformation

II11

II22

II33

(.35)(.35)

(.26)(.26)

(.39)(.39)

©2003 Thomson/South-Western 31

Deriving the Posterior Deriving the Posterior ProbabilitiesProbabilities

SS11

SS33

SS22

(.3)(.3)

(.2)(.2)

(.5)(.5)

(.7)(.7)

(.4)(.4)

(.2)(.2)II11

II11

II11

AA

Sum of branchesSum of branches = = PP((II11))

= .39= .39PP((SS11 | | II11) = .21/.39) = .21/.39 = .538= .538

PP((SS22 | | II11) = .08/.39) = .08/.39 = .205= .205

PP((SS33 | | II11) = .10/.39) = .10/.39 = .256= .256

1.01.0

SS11

SS33

SS22

(.3)(.3)

(.2)(.2)

(.5)(.5)

(.2)(.2)

(.5)(.5)

(.2)(.2)II22

II22

II22

AA

Sum of branchesSum of branches = = PP((II22))

= .26= .26PP((SS11 | | II22) = .06/.26) = .06/.26 = .231= .231

PP((SS22 | | II22) = .10/.26) = .10/.26 = .385= .385

PP((SS33 | | II22) = .10/.26) = .10/.26 = .385= .385

1.01.0

SS11

SS33

SS22

(.3)(.3)

(.2)(.2)

(.5)(.5)

(.1)(.1)

(.1)(.1)

(.6)(.6)II33

II33

II33

AA

Sum of branchesSum of branches = = PP((II33))

= .35= .35PP((SS11 | | II33) = .03/.35) = .03/.35 = .086= .086

PP((SS22 | | II33) = .02/.35) = .02/.35 = .057= .057

PP((SS33 | | II33) = .30/.35) = .30/.35 = .857= .857

1.01.0

Figure 19.12Figure 19.12