2004 annual report - interceramic...

TRANSCRIPT

2004Annual Report

and Oklahoma City, Oklahoma as well as started work onprojects for additional company-owned stores in rapidly growingareas such as Denver, Colorado and Sacramento, California.Company-owned distribution in important markets makes sensein Mexico as well, and during 2004 we acquired our franchiseesin a number of key cities, including Monterrey, Saltillo, San LuisPotosi, Mexicali, Tampico and Chihuahua.

With net sales of US $341.2 million, we set yet anothercompany record, growing by 11.3 percent over sales of US$306.4 million in 2003. Our gross margin improved as well, upto 35.7 percent for the year compared to 2003, when it wasalmost a full percentage point lower. Operating expenses as apercentage of sales increased slightly and at 6.7 percent, ouroperating margin was identical to that of last year. On the backof higher overall sales, operating income still was up nicely over2003, increasing by 11.3 percent to US $22.8 million from US$20.5 million. Earnings before interest, taxes, depreciation andamortization (“EBITDA”) for 2004 posted a substantial increaseover 2003, and at US $41.0 million was 13.3 percent greaterthan EBITDA of US $36.2 million recorded last year. As ourborrowing costs have decreased over the past few years andour results have improved, we have been much less pinched bydebt, and our debt service coverage ratio at the end of 2004was 7.2 times, compared to 5.7 at the end of 2003. Late in 2004we started work on a refinancing of our long-term debt in orderto take advantage of our improving financial condition and loweravailable rates. This transaction was completed in early January2005, and not only stretched out our maturities to amortize thedebt over five years, but also further reduced our borrowingcost.

In Mexico, sales for 2004 were up by 10.8 percent over 2003 on5.8 percent more product sold. As we completed the acquisitionof a number of our most important franchise stores over thecourse of the year, a much larger percentage of our sales inMexico are coming through the subsidiaries. During 2005 weshould feel the full effect of these acquisitions, and expect ourMexican sales to show good growth over the year. In the UnitedStates market the company achieved excellent sales growth, up12.0 percent in 2004 over 2003. We also moved more productin the United States over the course of the year, selling 10.4percent more tile than we did in 2003. Overall, we maintainedthe same basic split of sales between Mexico and the U.S.market that we have had for the past few years, with about 56percent of all group sales taking place in Mexico.

For Interceramic, 2004 was a momentous year. Along withsignificant improvement in our financial results over the prioryear, the year saw a number of other positive achievements.Perhaps first among them was the celebration of Interceramic's25 year anniversary. The long journey from a modest brick plantin Chihuahua, Mexico to four massive, state-of-the-artmanufacturing facilities and distribution covering all of NorthAmerica has been both astonishing and rewarding. In MexicoInterceramic has unparalleled name recognition as a very wellrespected, top-of-the-market brand, and our reputation hasbeen steadily growing in the United States and Canada as well.During 2004, we closed another successful stock offering,resulting in US $43.7 million in new equity for the company.Most of this we have invested in a new floor tile manufacturingfacility in Mexico which should start production in the secondquarter of this year. The new facility will employ the absolutelatest in ceramic tile manufacturing technology, and allow us toproduce about 25 percent more of our highest quality floor tileat lower costs and with more flexibility.

The year also saw Interceramic invest further in distributioninfrastructure. In the United States, we opened a brand-new“Interceramic Tile and Stone Gallery” store in the fast growingSan Diego, California market. We also moved to new, larger andmore prominent facilities in Houston, Texas, Atlanta, Georgia

Letter to Shareholders

1

Our results from the fourth quarter of 2004 present a sharplypositive contrast in almost every respect against the fourthquarter of 2003. Fourth quarter 2004 sales of US $90.4 millionwere 18 percent greater than sales of US $76.6 million in thefourth quarter of 2003 and, boding well for 2005, operatingincome was up a whopping 47.6 percent in the fourth quarter of2004 over the fourth quarter of last year-from US $3.1 million toUS $4.5 million. EBITDA showed a healthy increase as well, up29.5 percent to US $9.3 million from US $7.2 million in the sameperiod last year.

While 2004 was a good year here at Interceramic, we areexpecting even better things for 2005. With a new plant comingon line, burgeoning company-owned distribution and US $182million of equity behind us, we begin the year with theinfrastructure and financial strength to move us even furtherforward. As always, we thank our investors, our customers andour employees for their continued support.

Oscar E. Almeida ChabreChairman of the Board

2

Letter to Shareholders

In today's world, Companies which are committed to thedevelopment of society must go beyond the economic realmand the creation of jobs. Companies today are facing theenormous task of integration into the global market place, notonly by facing competition, but also by striving to be sociallyresponsible companies.

Promoting and generating better living conditions and providinggrowth opportunities are part of our corporate culture as carriedout by each and every member of our company.

At Interceramic we have focused our efforts on four majorareas:

• Improving the quality of life of our partners and collaborators,

• Preserving and improving the environment,• Conducting all of our actions, decisions and

relationships in an ethical manner, and,• Making concrete contributions towards the

sustainable development of the communities where we operate.

Obtaining the 2005 Distinction as an “Empresa SocialmenteResponsable” (Socially Responsible Company) implies not onlythat at Interceramic we are aware of the importance of activelyparticipating in the communities where we operate, but that wefurther tailor our support with plans and programs whichproduce sustainable development without creating adependancy.

Social responsibility is a central characteristic of each and everyone of the members of the Interceramic Family and we areconvinced that by working responsibly and living by ourdistinctive core values of quality, innovation and service, we canpositively impact our partners and collaboratos as well as ourcommunities.

Socially Responsible Company

3

Apart from meeting with Management and with the external,independent auditors, the Audit Committee undertook thefollowing activities:

Based on the discussions which took place betweenManagement and the independent auditors, the disclosuresmade on the financial statements report, the statements madeby Management to this Auditors Committee, and the report ofthe independent auditors, this Audit Committee recommendedto the Board of Directors that the consolidated financialstatements for the year ended December 31, 2004 bepresented for approval at the Annual Shareholders Meeting totake place on April 26, 2005.

C.P. HUMBERTO VALLES HERNANDEZPRESIDENT

The Management of Internacional de Cerámica, S.A. de C.V. isresponsible for the internal controls of all of the internalprocesses of the company, including the preparation andfinalization of all of the company's financial information.Mancera, S.C. (Member of Ernst & Young Global), as theexternal auditors of Internacional de Cerámica, S.A. de C.V., isresponsible for the examination of the annual consolidatedfinancial statements, in accordance with generally acceptedaccounting principles, and further must prepare a report as tosaid financial statements detailing the financial situation of thecompany, also in compliance with generally acceptedaccounting principles in Mexico, and, also, through areconciliation note, with the generally accepted accountingprinciples in the Unites States. The Audit Committee watchesover and supervises these processes and also recommends tothe Board of Directors, for its approval, the office of independentaccountants to be used as the external auditors for theCompany.

As part of this vigilance process, the Committee meets with thecompany's Management and with the external independentauditors, for the purpose of discussing the effectiveness of theinternal controls which are applied to the operations andfinancial processes of the company, as well as to evaluate theaccounting policies and practices and the results derived fromthe annual audits.

Report of the Audit Committeefor the year ended December 31, 2004

4

•It was in agreement with and ratified the selection ofMancera, S.C., as the external auditor for Internacionalde Cerámica, S.A. de C.V., so it could examine theCompany's consolidated financial statements andsubsequently prepare and finalize a report, same whichshall be presented for approval at the AnnualShareholders Meeting to take place on April 26, 2005.•The consolidated financial statements for the yearended December 31, 2004 were reviewed anddiscussed with the Board of Directors and with theexternal auditors. •Discussions were held with the independent auditorsregarding the auditing of the consolidated financialstatements of Internacional de Cerámica, S.A. de C.V.,specifically as to the depth and reach of the audit, anyobservations to be made, and the results derived fromthe auditing process. •The economic independence and related criteria for theindependent auditors was reviewed and evaluated. •All transactions which the company undertook withrelated parties were reviewed and evaluated, and adetermination was made that said transactions were nomore or less favorable to the company as if thosetransactions would have taken place with any othersupplier or party.

Board of Directors

5

Chairman of the BoardOSCAR E. ALMEIDA CHABRE

Chief Executive OfficerVICTOR D. ALMEIDA GARCIA

SecretaryNORMA ALMEIDA DE CHAMPION

Directors

ALFREDO HARP CALDERONI Vicepresident of Foundation Alfredo Harp Helú, A.C.DAVID KOHLER Group President, Kitchen and Bath Group, Kohler Co.FEDERICO TERRAZAS TORRES Chairman, Grupo Cementos de Chihuahua, S.A. de C.V.SYLVIA ALMEIDA President, Corporación Administrativa y Técnica, S.A. de C.V.DIANA E. ALMEIDA DirectorPATRICIA ALMEIDA DirectorMARK BLAUGRUND President, RECON Real Estate Consultants, Inc.HUMBERTO VALLES HERNANDEZ Retired Member of Mancera S.C., member of Ernst & Young GlobalCARLOS ELIAS TERRAZAS Chairman, Comercial Corporativa del Norte, S.A. de C.V.

Directors elected by Series D Shareholders

AUGUSTO O. CHAMPION Chairman, Arquitectura Habitacional e Industrial, S.A. de C.V.SERGIO MARES DELGADO President, Grupo Futurama

Statutory Auditor

AMERICO DE LA PAZ DE LA GARZA Partner of Mancera, S.C. member of Ernst & Young Global

Last twelve years

6

EBITDA(Million of nominal US Dollars)

Debt Service(Times)

Net Debt to EBITDA(Times)

85.4

80.8

43.6 66

.4 86.4 94.6 11

7.3 14

8.0

170.

6

169.

1

171.

8

190.

443.6

54.9

64.4

87.5 96

.3 108.

2 118.

0 111.

8 117.

4

130.

9

134.

6 150.

8

129.

0

135.

7

108.

0

153.

9 182.

7 202.

8

235.

3 259.

8 288.

0

300.

0

306.

4

341.

2

93 94 95 96 97 98 99 00 01 02 03 04

Mexico International

32.9

49.2

62.2

76.0 83

.1

95.1 10

7.2

111.

0

106.

3 121.

6

51.6

50.9

36%

35%37

%

37%

37%

35%

37%

34%

32%

31%

38%

39%

93 94 95 96 97 98 99 00 01 02 03 04

20.6

19.5

8.6

22.0

28.4

36.6

34.3 40

.1

46.7

43.2

36.2 41

.0

93 94 95 96 97 98 99 00 01 02 03 04

2.0

2.8

0.8 1.

5 1.9 2.

4

2.4 2.

8

3.6

4.4

5.7

7.2

93 94 95 96 97 98 99 00 01 02 03 04

4.2

6.3

16.0

6.6

5.2

4.1

4.2

3.2

2.7

2.7 3.4

2.8

93 94 95 96 97 98 99 00 01 02 03 04

Net Sales(Million of nominal US Dollars)

Gross Profit and Margin(Million of nominal US Dollars)

INTERNACIONAL DE CERÁMICA, S.A. DE C.V. AND SUBSIDIARIES

Consolidated Financial Statements

As of December 31, 2003 and 2004and For the years ended

December 31, 2002, 2003 and 2004with report of Independent Auditors

7

Contents

8

Report of Independent Auditors 1

Consolidated Financial Statements

Consolidated Balance Sheets 2Consolidated Statements of Income 4Consolidated Statements of Changes in Stockholders´ Equity 5Consolidated Statements of Changes in Financial Position 6Notes to Consolidated Financial Statements 7

Consolidated Financial Statements

9

INTERNACIONAL DE CERÁMICA, S.A. DE C.V. AND SUBSIDIARIES

Consolidated Balance Statements

(Thousands of Constant Mexican pesos ( Ps.) as of December 31, 2004)

Consolidated Financial Statements

10

2004

Ps. 196,271

369,37042,78621,701

( 18,039)415,818

1,101,59426,047

1,739,730

7,616

4,292,710( 1,814,333)

2,478,377

51,282102,423

Ps. 4,379,428

2003

Ps. 53,420

325,27649,92234,817

( 22,615)387,400

985,74423,733

1,450,297

8,051

3,726,781( 1,669,278)

2,057,503

-93,010

Ps. 3,608,861

2004Thousands ofU.S. dollars

$ 17,477

32,8913,8101,932

( 1,606)37,027

98,0942,319

154,917

678

382,254( 161,561)

220,693

4,5679,121

$ 389,976

AssetsCurrent assets:

Cash and cash equivalents

Accounts receivable:TradeRelated parties Other accounts receivableLess: allowance for doubtful accounts

Inventories, netPrepaid expensesTotal current assets

Investment in affiliated companies

Property, plant and equipmentAccumulated depreciation

GoodwillOther assets

Total assets

See accompanying notes to consolidated financial statements.

December 31,

Consolidated Financial Statements

11

2004

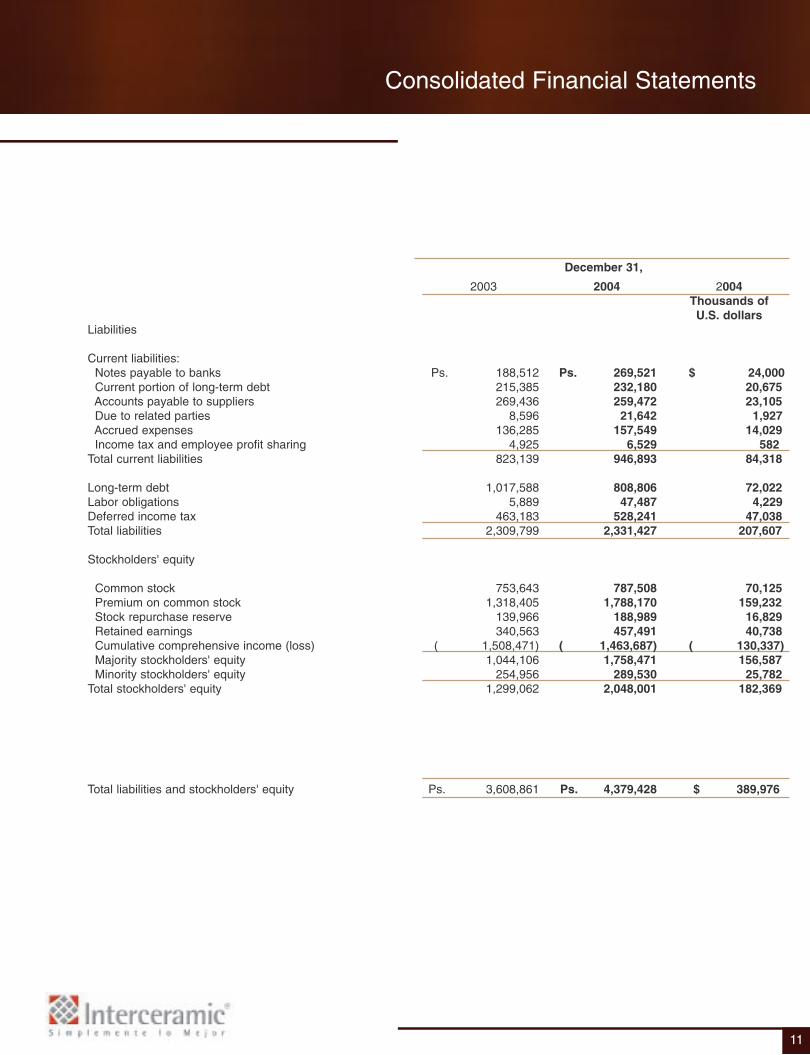

Ps. 269,521 232,180259,47221,642

157,5496,529

946,893

808,80647,487

528,2412,331,427

787,5081,788,170

188,989457,491

( 1,463,687)1,758,471

289,5302,048,001

Ps. 4,379,428

2003

Ps. 188,512215,385269,436

8,596136,285

4,925823,139

1,017,5885,889

463,1832,309,799

753,6431,318,405

139,966340,563

( 1,508,471)1,044,106

254,9561,299,062

Ps. 3,608,861

Liabilities

Current liabilities:Notes payable to banksCurrent portion of long-term debtAccounts payable to suppliersDue to related partiesAccrued expensesIncome tax and employee profit sharing

Total current liabilities

Long-term debtLabor obligationsDeferred income taxTotal liabilities

Stockholders' equity

Common stock Premium on common stockStock repurchase reserveRetained earningsCumulative comprehensive income (loss)Majority stockholders' equityMinority stockholders' equity

Total stockholders' equity

Total liabilities and stockholders' equity

December 31,

2004Thousands ofU.S. dollars

$ 24,00020,67523,105

1,92714,029

58284,318

72,0224,229

47,038207,607

70,125159,232

16,82940,738

( 130,337)156,587

25,782182,369

$ 389,976

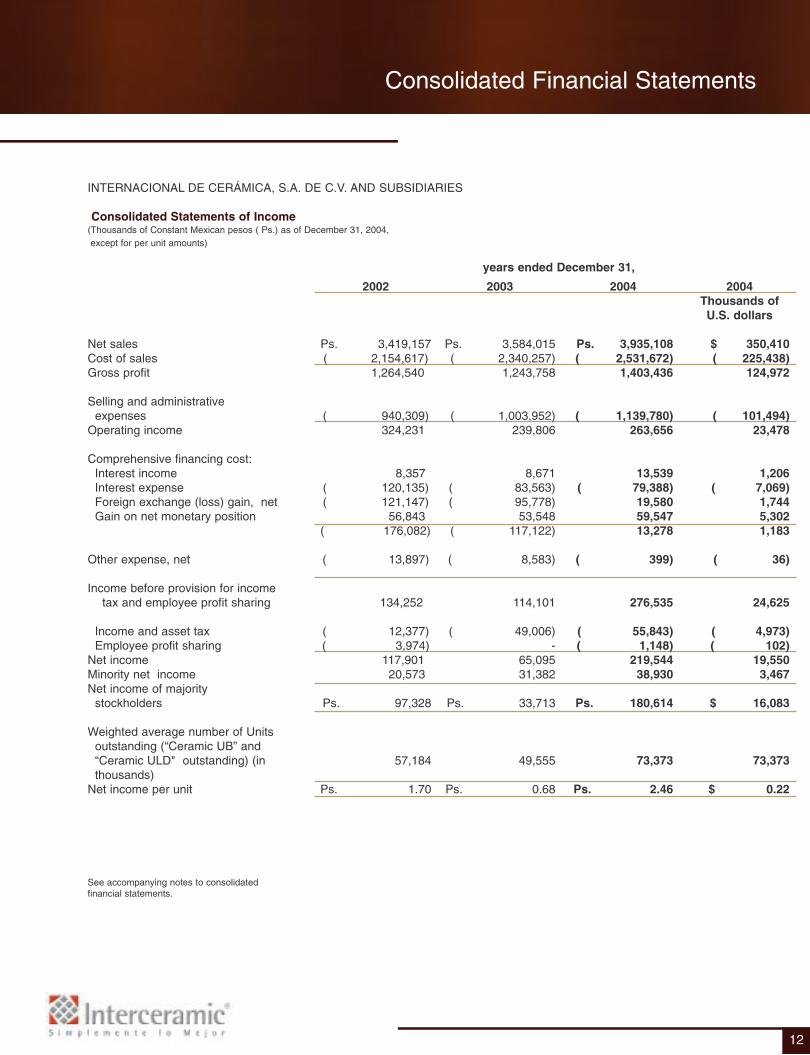

Net salesCost of salesGross profit

Selling and administrativeexpenses

Operating income

Comprehensive financing cost:Interest incomeInterest expenseForeign exchange (loss) gain, netGain on net monetary position

Other expense, net

Income before provision for income tax and employee profit sharing

Income and asset tax Employee profit sharing

Net income Minority net incomeNet income of majority

stockholders

Weighted average number of Unitsoutstanding (“Ceramic UB” and “Ceramic ULD" outstanding) (in thousands)

Net income per unit

See accompanying notes to consolidatedfinancial statements.

INTERNACIONAL DE CERÁMICA, S.A. DE C.V. AND SUBSIDIARIES

Consolidated Statements of Income(Thousands of Constant Mexican pesos ( Ps.) as of December 31, 2004,except for per unit amounts)

Consolidated Financial Statements

12

2004

Ps. 3,935,108( 2,531,672)

1,403,436

( 1,139,780)263,656

13,539( 79,388)

19,58059,54713,278

( 399)

276,535

( 55,843)( 1,148)

219,54438,930

Ps. 180,614

73,373

Ps. 2.46

2004Thousands ofU.S. dollars

$ 350,410( 225,438)

124,972

( 101,494)23,478

1,206( 7,069)

1,7445,3021,183

( 36)

24,625

( 4,973)( 102)

19,5503,467

$ 16,083

73,373

$ 0.22

2003

Ps. 3,584,015( 2,340,257)

1,243,758

( 1,003,952)239,806

8,671( 83,563)( 95,778)

53,548( 117,122)

( 8,583)

114,101

( 49,006)-

65,09531,382

Ps. 33,713

49,555

Ps. 0.68

2002

Ps. 3,419,157( 2,154,617)

1,264,540

( 940,309)324,231

8,357( 120,135)( 121,147)

56,843( 176,082)

( 13,897)

134,252

( 12,377)( 3,974)

117,90120,573

Ps. 97,328

57,184

Ps. 1.70

years ended December 31,

Consolidated Financial Statements

13

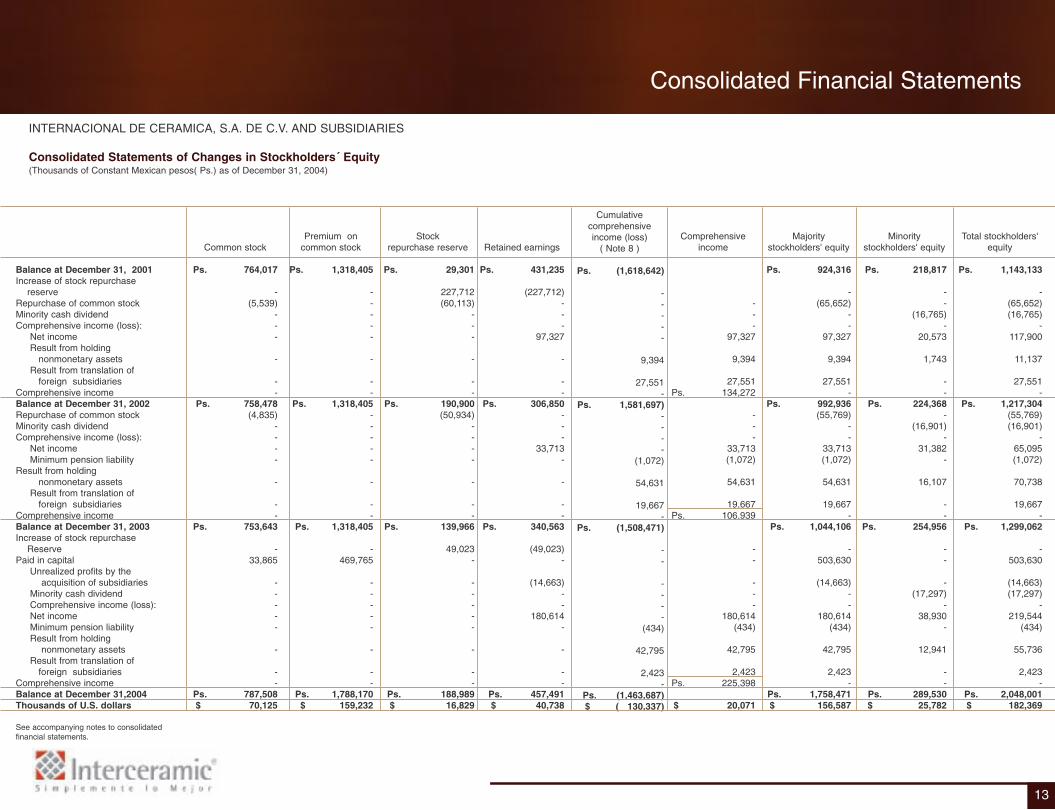

INTERNACIONAL DE CERAMICA, S.A. DE C.V. AND SUBSIDIARIES

Consolidated Statements of Changes in Stockholders´ Equity(Thousands of Constant Mexican pesos( Ps.) as of December 31, 2004)

Premium oncommon stock

Ps. 1,318,405

-----

-

--

Ps. 1,318,405-----

-

--

Ps. 1,318,405

-469,765

-----

-

--

Ps. 1,788,170$ 159,232

Common stock

Ps. 764,017

-(5,539)

---

-

--

Ps. 758,478 (4,835)

----

-

--

Ps. 753,643

-33,865

-----

-

--

Ps. 787,508$ 70,125

Stock repurchase reserve

Ps. 29,301

227,712(60,113)

---

-

--

Ps. 190,900(50,934)

----

-

--

Ps. 139,966

49,023-

-----

-

--

Ps. 188,989$ 16,829

Retained earnings

Ps. 431,235

(227,712)---

97,327

-

--

Ps. 306,850---

33,713-

-

--

Ps. 340,563

(49,023)-

(14,663)--

180,614-

-

--

Ps. 457,491$ 40,738

Cumulativecomprehensiveincome (loss)

( Note 8 )

Ps. (1,618,642)

-----

9,394

27,551 -

Ps. 1,581,697) ----

(1,072)

54,631

19,667 -

Ps. (1,508,471)

--

----

(434)

42,795

2,423-

Ps. (1,463,687) $ ( 130,337)

Comprehensiveincome

---

97,327

9,394

27,551Ps. 134,272

---

33,713(1,072)

54,631

19,667Ps. 106,939

--

---

180,614(434)

42,795

2,423Ps. 225,398

$ 20,071

Majoritystockholders' equity

Ps. 924,316

-(65,652)

--

97,327

9,394

27,551-

Ps. 992,936 (55,769)

--

33,713(1,072)

54,631

19,667-

Ps. 1,044,106

-503,630

(14,663)--

180,614(434)

42,795

2,423-

Ps. 1,758,471$ 156,587

Minoritystockholders' equity

Ps. 218,817

--

(16,765)-

20,573

1,743

--

Ps. 224,368-

(16,901)-

31,382-

16,107

--

Ps. 254,956

--

-(17,297)

-38,930

-

12,941

--

Ps. 289,530$ 25,782

Total stockholders'equity

Ps. 1,143,133

-(65,652)(16,765)

-117,900

11,137

27,551-

Ps. 1,217,304 (55,769)(16,901)

-65,095(1,072)

70,738

19,667-

Ps. 1,299,062

-503,630

(14,663)(17,297)

-219,544

(434)

55,736

2,423-

Ps. 2,048,001$ 182,369

Balance at December 31, 2001Increase of stock repurchase

reserve Repurchase of common stockMinority cash dividendComprehensive income (loss):

Net incomeResult from holding

nonmonetary assetsResult from translation of

foreign subsidiariesComprehensive incomeBalance at December 31, 2002Repurchase of common stockMinority cash dividendComprehensive income (loss):

Net incomeMinimum pension liability

Result from holding nonmonetary assets

Result from translation of foreign subsidiaries

Comprehensive incomeBalance at December 31, 2003Increase of stock repurchase

ReservePaid in capital

Unrealized profits by the acquisition of subsidiaries

Minority cash dividendComprehensive income (loss):Net incomeMinimum pension liabilityResult from holding

nonmonetary assetsResult from translation of

foreign subsidiariesComprehensive incomeBalance at December 31,2004Thousands of U.S. dollars

See accompanying notes to consolidatedfinancial statements.

INTERNACIONAL DE CERÁMICA, S.A. DE C.V. AND SUBSIDIARIES

Consolidated Statements of Changes in Financial Position(Thousands of Constant Mexican pesos ( Ps.) as of December 31, 2004)

Consolidated Financial Statements

14

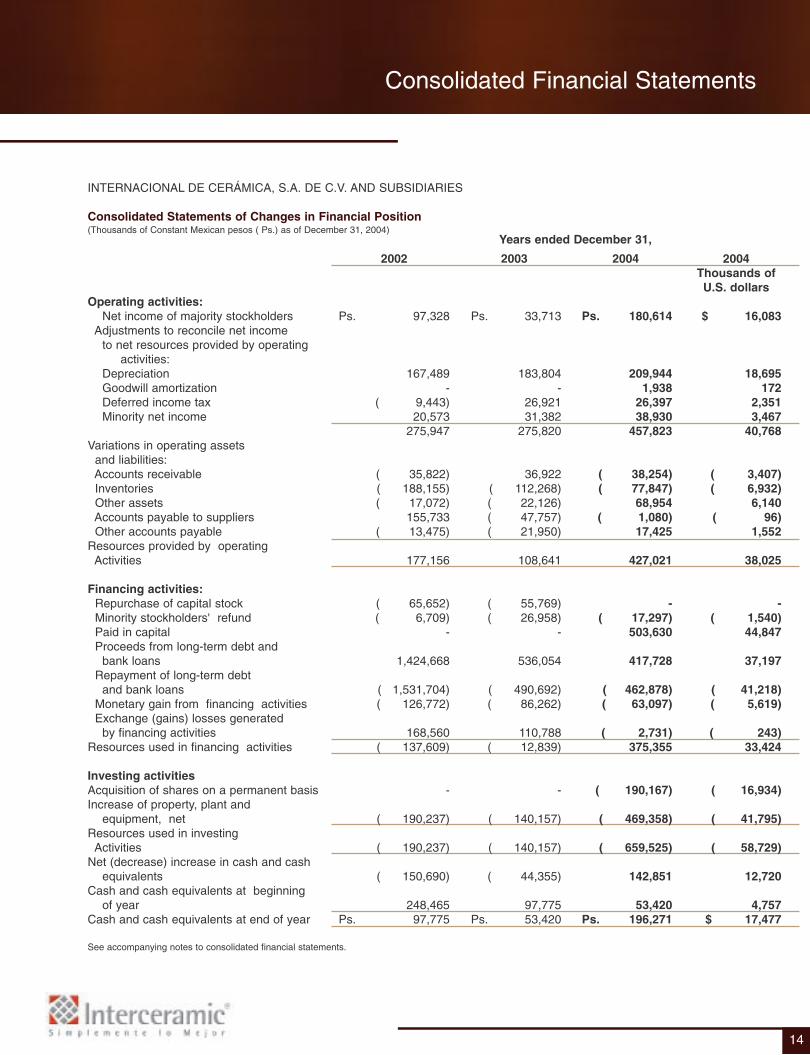

Operating activities:Net income of majority stockholders

Adjustments to reconcile net incometo net resources provided by operating

activities:DepreciationGoodwill amortizationDeferred income taxMinority net income

Variations in operating assetsand liabilities:Accounts receivableInventoriesOther assetsAccounts payable to suppliersOther accounts payable

Resources provided by operating Activities

Financing activities:Repurchase of capital stockMinority stockholders' refundPaid in capitalProceeds from long-term debt and

bank loansRepayment of long-term debt

and bank loansMonetary gain from financing activitiesExchange (gains) losses generated

by financing activitiesResources used in financing activities

Investing activitiesAcquisition of shares on a permanent basis Increase of property, plant and

equipment, netResources used in investing

ActivitiesNet (decrease) increase in cash and cash

equivalentsCash and cash equivalents at beginning

of yearCash and cash equivalents at end of year

See accompanying notes to consolidated financial statements.

2004

Ps. 180,614

209,9441,938

26,39738,930

457,823

( 38,254)( 77,847)

68,954( 1,080)

17,425

427,021

-( 17,297)

503,630

417,728

( 462,878)( 63,097)

( 2,731) 375,355

( 190,167)

( 469,358)

( 659,525)

142,851

53,420Ps. 196,271

2004Thousands ofU.S. dollars

$ 16,083

18,695172

2,3513,467

40,768

( 3,407)( 6,932)

6,140( 96)

1,552

38,025

-( 1,540)

44,847

37,197

( 41,218)( 5,619)

( 243)33,424

( 16,934)

( 41,795)

( 58,729)

12,720

4,757$ 17,477

2003

Ps. 33,713

183,804-

26,92131,382

275,820

36,922( 112,268)( 22,126)( 47,757)( 21,950)

108,641

( 55,769)( 26,958)

-

536,054

( 490,692)( 86,262)

110,788 ( 12,839)

-

( 140,157)

( 140,157)

( 44,355)

97,775Ps. 53,420

2002

Ps. 97,328

167,489 -

( 9,443) 20,573

275,947

( 35,822)( 188,155)( 17,072)

155,733( 13,475)

177,156

( 65,652)( 6,709)

-

1,424,668

( 1,531,704)( 126,772)

168,560 ( 137,609)

-

( 190,237)

( 190,237)

( 150,690)

248,465Ps. 97,775

Years ended December 31,

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31,2004 and thousands of U.S. dollars ( $), except for number ofshares and units, minimum dividend per share, market valueper unit and exchange rates, which are stated in pesos (Ps.))

1. Description of the business and significant accountingpolicies

Description of the business

Internacional de Ceramica, S.A. de C.V. (“Interceramic”), itssubsidiaries, Recubrimientos Interceramic, S.A. de C.V.(“Recubrimientos”) and Interceramic, Inc., which is located inGarland, Texas, are all engaged in the manufacture andmarketing of ceramic floor and wall tiles, the extraction of clayfor the manufacture of ceramic tiles and marketing of bathroomfurniture. The other subsidiaries, which are listed below in the “Basis of consolidation”, are engaged primarily in the marketingof ceramic tiles and in the manufacture and marketing ofadhesives in the Mexico City and Guadalajara metropolitanareas and in the United States. Interceramic and itssubsidiaries are hereinafter referred to collectively as the“Company.”

Significant accounting policies

The consolidated financial statements of the Company havebeen prepared in Mexican pesos (“Ps.”) in accordance withaccounting principles generally accepted in Mexico (“MexicanGAAP”).

The significant accounting policies and practices followed in thepreparation of the consolidated financial statements aredescribed below:

a) Basis of consolidation

The consolidated financial statements include the accounts ofInterceramic and all of its subsidiaries. All materialintercompany balances and transactions have been eliminatedin consolidation. The subsidiaries included in the consolidatedfinancial statements are as follows, along with correspondingownership:

Ownership interest atDecember 31,

(*) In March 2004, Holding de Franquicias Interceramic, S.A. deC.V., acquired stock of Distribucion Interceramic, S.A. de C.V.,and of Interacabados de Occidente, S.A. de C.V., at book value.

(**) In March 2004, Interacabados del Centro, S.A. de C.V.,changes its name to Holding de Servicios Interceramic S.A. deC.V., and it currently owns 100% of the capital of Materiales enProceso, S.A. de C.V., and Servicios AdministrativosInterceramic, S.A. de C.V.

Consolidated Financial Statements

15

Adhesivos y Boquillas Interceramic, S. de R.L. de C.V.

Distribución Interceramic, S.A. de C.V.

Holding de Franquicias Interceramic, S.A. de C.V.

Holding de Servicios Interceramic, S.A. de C.V.

(antes Interacabados del Centro, S.A. de C.V. )

Interacabados de Occidente, S.A. de C.V.

Interceramic Holding, Inc.

Interceramic de Occidente, S.A. de C.V.

Interceramic Trading Co.

Materiales en Proceso, S.A. de C.V.

Operadora Interceramic de México, S.A. de C.V.

Recubrimientos Interceramic, S.A. de C.V.

Servicios Administrativos Interceramic, S.A. de C.V.

2003

51.00

100.00

-

100.00

100.00

100.00

100.00

100.00

100.00

100.00

50.01

100.00

2004

51.00

(*)

100.00

100.00

(*)

100.00

100.00

100.00

(**)

100.00

50.01

(**)

Consolidated Financial Statements

16

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31,2004 and thousands of U.S. dollars ( $), except for number ofshares and units, minimum dividend per share, market valueper unit and exchange rates, which are stated in pesos (Ps.))

1. Description of the business and significant accountingpolicies (continued)

a) Basis of consolidation (continued)

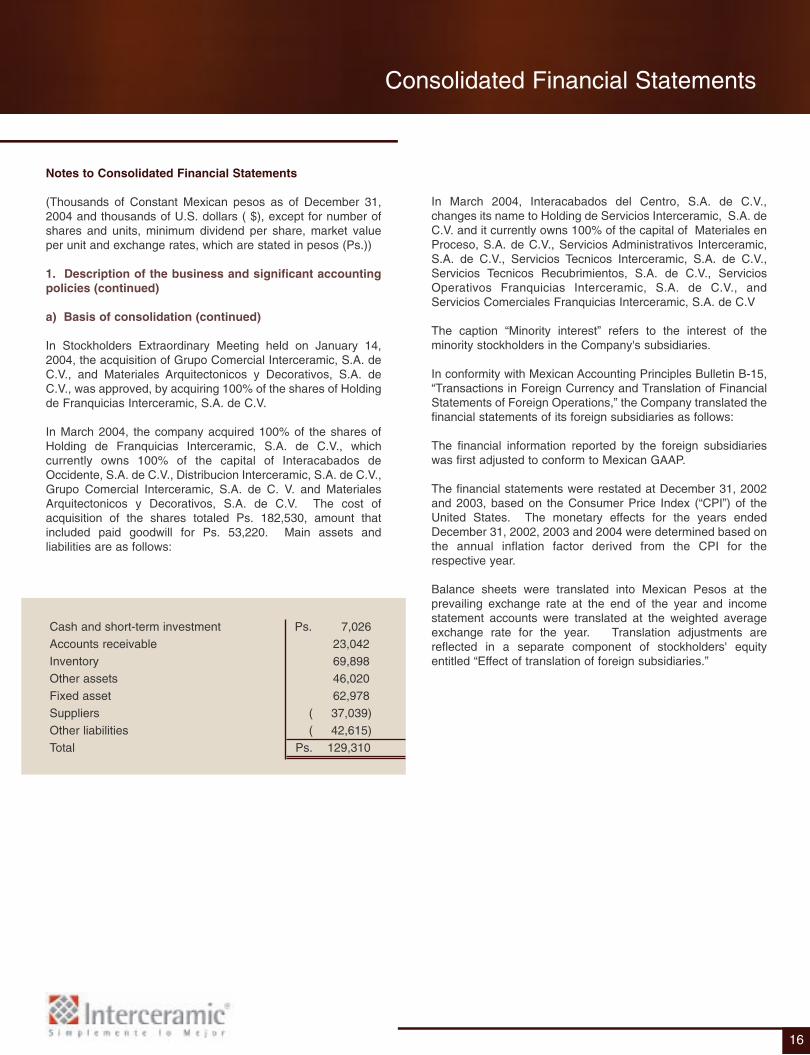

In Stockholders Extraordinary Meeting held on January 14,2004, the acquisition of Grupo Comercial Interceramic, S.A. deC.V., and Materiales Arquitectonicos y Decorativos, S.A. deC.V., was approved, by acquiring 100% of the shares of Holdingde Franquicias Interceramic, S.A. de C.V.

In March 2004, the company acquired 100% of the shares ofHolding de Franquicias Interceramic, S.A. de C.V., whichcurrently owns 100% of the capital of Interacabados deOccidente, S.A. de C.V., Distribucion Interceramic, S.A. de C.V.,Grupo Comercial Interceramic, S.A. de C. V. and MaterialesArquitectonicos y Decorativos, S.A. de C.V. The cost ofacquisition of the shares totaled Ps. 182,530, amount thatincluded paid goodwill for Ps. 53,220. Main assets andliabilities are as follows:

In March 2004, Interacabados del Centro, S.A. de C.V.,changes its name to Holding de Servicios Interceramic, S.A. deC.V. and it currently owns 100% of the capital of Materiales enProceso, S.A. de C.V., Servicios Administrativos Interceramic,S.A. de C.V., Servicios Tecnicos Interceramic, S.A. de C.V.,Servicios Tecnicos Recubrimientos, S.A. de C.V., ServiciosOperativos Franquicias Interceramic, S.A. de C.V., andServicios Comerciales Franquicias Interceramic, S.A. de C.V

The caption “Minority interest” refers to the interest of theminority stockholders in the Company's subsidiaries.

In conformity with Mexican Accounting Principles Bulletin B-15,“Transactions in Foreign Currency and Translation of FinancialStatements of Foreign Operations,” the Company translated thefinancial statements of its foreign subsidiaries as follows:

The financial information reported by the foreign subsidiarieswas first adjusted to conform to Mexican GAAP.

The financial statements were restated at December 31, 2002and 2003, based on the Consumer Price Index (“CPI”) of theUnited States. The monetary effects for the years endedDecember 31, 2002, 2003 and 2004 were determined based onthe annual inflation factor derived from the CPI for therespective year.

Balance sheets were translated into Mexican Pesos at theprevailing exchange rate at the end of the year and incomestatement accounts were translated at the weighted averageexchange rate for the year. Translation adjustments arereflected in a separate component of stockholders' equityentitled “Effect of translation of foreign subsidiaries.”

Cash and short-term investment

Accounts receivable

Inventory

Other assets

Fixed asset

Suppliers

Other liabilities

Total

Ps. 7,026

23,042

69,898

46,020

62,978

( 37,039)

( 42,615)

Ps. 129,310

Consolidated Financial Statements

17

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31,2004 and thousands of U.S. dollars ($), except for number ofshares and units, minimum dividend per share, market valueper unit and exchange rates, which are stated in pesos (Ps.))

1. Description of the business and significant accountingpolicies (continued)

Consolidated financial statements as of December 31, 2002and 2003 are presented in constant currency at December 31,2004, using a common restatement factor determined based onthe weighted average net sales. Such factors were 1.0682 and1.0465, respectively.

b) Estimates in financial statements

The preparation of consolidated financial statements inconformity with generally accepted accounting principlesrequires management to make estimates and assumptions thataffect the reported amounts of assets and liabilities anddisclosures of contingent assets and liabilities at the date of theconsolidated financial statements and the amounts of revenuesand expenses during the reporting periods. Actual results coulddiffer from these estimates.

c) Concentration of risk

The Company distributes its products through Company-ownedand independent franchise locations in Mexico. The Companydistributes its products in the United States and Canada mainlythrough its network of wholly-owned Interceramic Tile and StoneGalleries ( ITS) stores and a network of 79 independentdistributors with a combined total of 180 locations. On a regularbasis, the Company assesses the credit worthiness of itscustomers and distributors and typically obtains personalguarantees or liens to secure amounts due from its customersand distributors. No single customer represented more than 5%of the Company's consolidated net sales.

d) Recognition of the effects of inflation

The Company recognizes the effects of inflation on financialinformation as required by Mexican Accounting PrinciplesBulletin B-10, “Accounting Recognition of the Effects of Inflationon Financial Information.” Consequently, the amounts shown inthe accompanying financial statements and in these notes areexpressed in thousands of constant pesos as of December 31,2004.

Certain concepts and procedures required by the application ofBulletin B-10 are explained below:

- The Company follows the specific-cost method to restate itsinventories.

-Imported machinery and equipment was restated based on therate of inflation in the country of origin and the prevailingexchange rate at the balance sheet date. Machinery andequipment of domestic origin was restated based on theMexican National Consumer Price Index (NCPI).

-At December 31, 2003 and 2004 stockholder's equity accountswere restated by using a common restatement factor, whichwas determined based on NCPI.

-The gain or loss on net monetary position represents theeffects of inflation, as measured by the NCPI, on the Company'smonetary assets and liabilities. During inflationary periods,losses are incurred by holding monetary assets, whereas gainsare realized by holding monetary liabilities. The net monetaryeffect is included in the consolidated statements of income aspart of the “comprehensive financing cost.”

-The deficit from restatement of stockholders' equity consistsprincipally of the initial cumulative monetary position result andthe cumulative deficit from holding non-monetary assets. The(loss) gain from holding non-monetary assets represents theamount by which the (decrease) increase in the specific valueof assets was (lower) higher than the rate of inflation.

e) Cash and short-term investments

Cash and short-term investments are mainly represented bybank deposits on immediately available cash instruments withmaturities not exceeding 90 days, and they are presentedvalued at their acquisition cost plus outstanding accruedinterest. Their total is similar to their market value.

f) Estimate for doubtful accounts

The estimate of doubtful accounts is determined based on aseniority assessment and a qualitative review of accountsreceivable. Total estimate also contemplates assessment ofhistoric losses for bad credits, as well as the review of theeconomic environment in which the company operates. InMexico, a part of Company sales are made though a network ofindependent dealers where recovery of accounts receivable isassured and another part of sales is carried out thoughsubsidiary franchises where most of the sales are in cash and,therefore, not giving way to significant doubtful accounts.

Consolidated Financial Statements

18

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31,2004 and thousands of U.S. dollars ($), except for number ofshares and units, minimum dividend per share, market valueper unit and exchange rates, which are stated in pesos (Ps.))

1. Description of the business and significant accountingpolicies (continued)

f) Estimate for doubtful accounts (continued)

In the U.S.A., the estimate for doubtful accounts is based on anumber of factors that include, among others, the assessmentof losses due to unrecoverable credits that occurred in prioryears, experience, the review of specific balances of certainaccounts and the economic conditions of the environment inwhich the company operates.

g) Inventories and cost of sales

Inventories are recorded initially at acquisition or productioncost and then restated to reflect replacement cost, which is notin excess of market value.

Cost of sales represents the estimated replacement cost at thetime sales were realized, expressed in constant pesos at theend of the year.

The reserve for obsolete and slow-moving inventories isdetermined based on an evaluation of the Company'sinventories, an historical loss rate and a number of qualitativefactors such as aging, discontinued lines of products and slowmoving inventories.

h) Investment in shares of affiliated companies

Investments in companies in which the Company has anownership interest of between 10% and 50% and for which theCompany exercises significant influence, are accounted forusing the equity method. Investments in companies in which theCompany has an ownership interest of less than 10% arerecorded at cost and restated for changes in the NCPI.

i) Property, plant and equipment

Machinery coming from abroad, as well as the amount ofacquisitions of the year were restated based on inflation of thecountry of origin on assets and translated into pesos byapplying the rate of exchange in force as of the date of thefinancial statements.

-At December 31, 2003 and 2004, approximately 93% and 91%of machinery and equipment were restated based on specificfactors and 7% and 9% were restated based on the NCPI.

-Depreciation is computed on the restated values, using thestraight-line method based on the estimated useful lives of theassets as determined periodically by management based ontechnical studies.

j) Impairment of long-lived assets

Beginning January 1st., 2004, the Company adopted thedispositions of Bulletin C-15 “Impairment of long -lived assetsand their disposition,” issued by the Mexican Institute of PublicAccountants on March 2003.

Said Bulletin establishes that when impairment signs in thevalue of long-standing assets exist, recovery value of theseassets should be determined by obtaining the sales price of saidassets and the use value. When recovery value is lower thannet book value , the difference is recognized as a loss due toimpairment. The adoption of this rule had no significant effectseither on the results or on the financial position of the Company.

k) Intangible assets

Beginning January 1st., 2003, the Company adopted thedispositions of Bulletin C-8 “Intangible Assets” issued by theMexican Institute of Public Accountants. This Bulletinestablishes, among other aspects, that only development costsof a project should be capitalized if they comply with the criteriadefined for recognition as assets; pre-operating costs notidentified as development should be recorded as an expense ofthe year y intangible assets considered with an indefinite life arenot amortized, but rather its fair value is subject to impairmenttests. The effects of applying this Bulletin were not significantfor the Company.

l) Goodwill

Goodwill represents the difference between acquisition cost andfair value of net assets acquired at the date of acquisition. It isrestated by applying the NCPI and it is amortized by thestraight-line method, over a 20-year period.

Beginning 2005, this goodwill is no longer amortized and it willbe subject only to impairment tests.

Consolidated Financial Statements

19

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31,2004 and thousands of U.S. dollars ($), except for number ofshares and units, minimum dividend per share, market valueper unit and exchange rates, which are stated in pesos (Ps.))

1. Description of the business and significant accountingpolicies (continued)

m) Exchange differences

Transactions in foreign currency are recorded at the exchangerate at the time of the transactions. Exchange differences aredetermined from the date of the transactions to the time ofsettlement or valuation at the balance sheet date and arecharged or credited to income.

n) Labor obligations

Beginning January 2004, the Company implemented a pensionplan in addition to that granted by the Mexican Social SecurityInstitute. The Company decided to anticipate the effects ofbulletin D-3 referring to the new subject “Remuneration at theend of the labor relationship.” The effects of both the newpension plan and the effect of recognizing compensations areshown in Note 7.

The costs of pensions, compensations, and seniority premiumsare recognized periodically based on calculation performed byindependent actuaries by means of the projected unit creditmethod, using net financial hypothesis net of inflation, inconformity with guidelines established in Bulletin D-3 “LaborObligations,” issued by the Mexican Institute of PublicAccountants.

The Federal Labor Law establishes the obligation to makecertain payments to personnel who no longer works for theCompany under certain circumstances. At December 31,2003, compensations to personnel are recorded under incomeof the year when payment occurs.

o) Income taxes and employee profit sharing

Deferred income taxes are recognized for all temporarydifferences between balance sheet components for financialand tax reporting purposes, using enacted income tax rates.

The Company periodically evaluates the possibility ofrecovering deferred tax assets and if necessary, adjusts therelated valuation reserve.

Employee profit sharing is a statutory obligation payable toemployees that is determined in accordance with the provisionsof both Mexican labor and income tax laws.

In conformity with Bulletin D-4, deferred employee profit sharingis recognized only on temporary differences determined in thereconciliation of current year net income for financial and taxreporting purposes, provided there is no indication that therelated liability or asset will not be realized in the future.

Current year employee profit sharing is charged to results ofoperations and represents a current liability due and payable ina period of less than one year.

Current year income tax is charged to results of operations andrepresents the tax liability due and payable in less than oneyear.

p) Revenue recognition

The Company recognizes revenue when goods are shippedand invoiced. Revenue from retail operations is recognized,generally, at the point of sale. Returns and allowances areestimated and accrued based on historical results.

q) Net income per unit

Net income per unit is determined on the basis of the weightedaverage number of units issued and outstanding. Units arecomprised of two common shares that are traded together asone unit. A “UB” unit is comprised of two Series “B” Shares anda “ULD” unit is comprised of one Series “L” Share and oneSeries “D” Share. After December 2004, units were separatedremaining only series “B” and series “D” shares.

r) Comprehensive income (loss)

Comprehensive income consists of net income or loss for theyear plus those items that are reflected directly in stockholders'equity and that do not constitute capital contributions,reductions or distributions such as deficit from restatement ofstockholders' equity, effect of translation of foreign subsidiariesand deferred taxes allocated to stockholders' equity.

s) Reclassifications

Certain amounts in the 2002 and 2003 consolidated financialstatements have been reclassified to conform to the 2004presentation.

Consolidated Financial Statements

20

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

2. Related parties

In the normal course of business, the Company has transactions with related parties and affiliated companies. Affiliated companies arethose in which the Company's principal stockholders have significant equity interests or control of management. The main transactionswith these companies consist of ceramic tile purchases for resale in Mexico and in the United States. Such transactions are negotiatedon terms and prices that management believes are comparable to similar transactions with non-related customers.

During the years ended December 31, 2002, 2003 and 2004, the Company had the following transactions with related parties:

Sales of ceramic tile:Affiliated companiesGrupo Comercial Interceramic, S.A. de C.V.Materiales Arquitectónicos y Decorativos, S.A. de C.V.

Joint venture:Dal-Tile International, Inc.

Inventory purchases:Stockholders

Kohler, Co.

Joint ventureCustom Building Products, Inc.

Fees paid for administrative servicesand other items:

Affiliated companies:Arquitectura Habitacional e Industrial, S.A. de C.V.Corporacion Administrativa y Tecnica, S.A. de C.V.Corporacion Aerea Cencor, S.A. de C.V.

2004

Ps. --

108,333Ps. 108,333

Ps. 91,550

6,187Ps. 97,737

Ps. 57,48437,55510,495

Ps. 105,534

2003

Ps. 182,11387,110

88,758Ps. 357,981

Ps. 101,414

17,365Ps. 118,779

Ps. -36,59910,196

Ps. 46,795

2002

Ps. 193,86981,316

108,342Ps. 383,527

Ps. 91,785

7,526Ps. 99,311

Ps. -37,64810,544

Ps. 48,192

Sales to join venture partners consist of ceramic tiles sold in the United States.

Purchases from stockholders and Joint ventures consist of bathroom fixtures and adhesives related products to be resold in Mexico.

Fees paid for administrative services relate to management consulting, use of computer systems, maintenance of equipment, air taxiservices and construction of a new plant provided by related companies.

3. Inventories

Inventories at December 31, 2003 and 2004 consisted of the following:

The reserve for obsolete and slow-moving inventories is Ps. 68,426 and Ps. 90,054 at December 31, 2003 and 2004, respectively, andhas been deducted from finished goods and raw materials and supplies.

Finished goodsWork in processRaw materials and suppliesMerchandise in transit

2004

Ps. 898,19741,51196,57965,307

Ps. 1,101,594

2003

Ps. 825,07834,62293,64632,398

Ps. 985,744

Consolidated Financial Statements

21

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

2. Related parties (continued)

An analysis of amounts due to and from related parties at December 31, 2003 and 2004 is as follows:

Trade receivables:Grupo Comercial Interceramic, S.A. de C.V.Materiales Arquitectónicos y Decorativos, S.A. de C.V.Dal-Tile International, Inc.ExecutivesOthers

Accounts payable:Custom Building Products, IncKohler, Co.Others

2004

Ps. - -

27,92514,479

382Ps. 42,786

Ps. 1,41920,024

199Ps. 21,642

2003

Ps. 21,9279,462

18,333-

200Ps. 49,922

Ps. 4237,404

769Ps. 8,596

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

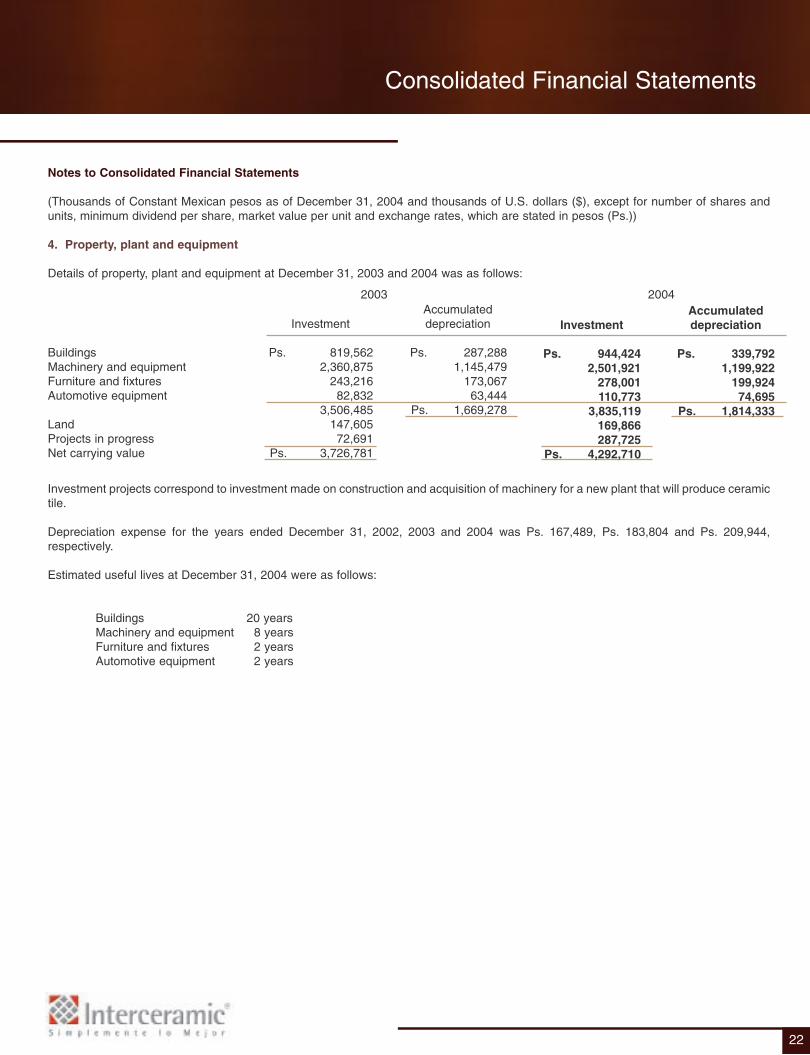

4. Property, plant and equipment

Details of property, plant and equipment at December 31, 2003 and 2004 was as follows:

Investment projects correspond to investment made on construction and acquisition of machinery for a new plant that will produce ceramictile.

Depreciation expense for the years ended December 31, 2002, 2003 and 2004 was Ps. 167,489, Ps. 183,804 and Ps. 209,944,respectively.

Estimated useful lives at December 31, 2004 were as follows:

Buildings 20 yearsMachinery and equipment 8 yearsFurniture and fixtures 2 yearsAutomotive equipment 2 years

Consolidated Financial Statements

22

BuildingsMachinery and equipmentFurniture and fixturesAutomotive equipment

LandProjects in progressNet carrying value

Accumulateddepreciation

Ps. 287,2881,145,479

173,06763,444

Ps. 1,669,278

Investment

Ps. 819,5622,360,875

243,21682,832

3,506,485147,60572,691

Ps. 3,726,781

Accumulateddepreciation

Ps. 339,7921,199,922

199,92474,695

Ps. 1,814,333

Investment

Ps. 944,4242,501,921

278,001110,773

3,835,119169,866287,725

Ps. 4,292,710

2003 2004

Consolidated Financial Statements

23

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

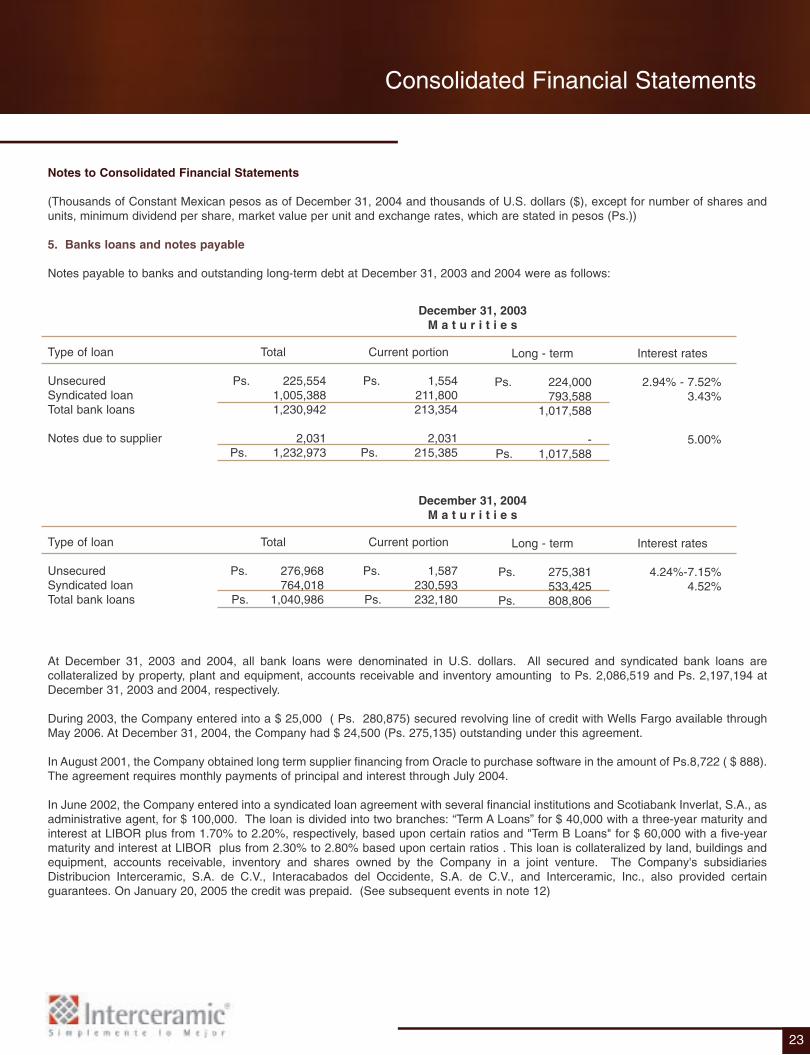

5. Banks loans and notes payable

Notes payable to banks and outstanding long-term debt at December 31, 2003 and 2004 were as follows:

At December 31, 2003 and 2004, all bank loans were denominated in U.S. dollars. All secured and syndicated bank loans arecollateralized by property, plant and equipment, accounts receivable and inventory amounting to Ps. 2,086,519 and Ps. 2,197,194 atDecember 31, 2003 and 2004, respectively.

During 2003, the Company entered into a $ 25,000 ( Ps. 280,875) secured revolving line of credit with Wells Fargo available throughMay 2006. At December 31, 2004, the Company had $ 24,500 (Ps. 275,135) outstanding under this agreement.

In August 2001, the Company obtained long term supplier financing from Oracle to purchase software in the amount of Ps.8,722 ( $ 888).The agreement requires monthly payments of principal and interest through July 2004.

In June 2002, the Company entered into a syndicated loan agreement with several financial institutions and Scotiabank Inverlat, S.A., asadministrative agent, for $ 100,000. The loan is divided into two branches: “Term A Loans” for $ 40,000 with a three-year maturity andinterest at LIBOR plus from 1.70% to 2.20%, respectively, based upon certain ratios and "Term B Loans" for $ 60,000 with a five-yearmaturity and interest at LIBOR plus from 2.30% to 2.80% based upon certain ratios . This loan is collateralized by land, buildings andequipment, accounts receivable, inventory and shares owned by the Company in a joint venture. The Company's subsidiariesDistribucion Interceramic, S.A. de C.V., Interacabados del Occidente, S.A. de C.V., and Interceramic, Inc., also provided certainguarantees. On January 20, 2005 the credit was prepaid. (See subsequent events in note 12)

Type of loan

UnsecuredSyndicated loanTotal bank loans

Current portion

Ps. 1,587230,593

Ps. 232,180

Total

Ps. 276,968764,018

Ps. 1,040,986

Interest rates

4.24%-7.15%4.52%

Long - term

Ps. 275,381533,425

Ps. 808,806

December 31, 2004M a t u r i t i e s

Type of loan

UnsecuredSyndicated loanTotal bank loans

Notes due to supplier

Current portion

Ps. 1,554211,800213,354

2,031Ps. 215,385

Total

Ps. 225,5541,005,3881,230,942

2,031Ps. 1,232,973

Interest rates

2.94% - 7.52%3.43%

5.00%

Long - term

Ps. 224,000793,588

1,017,588

-Ps. 1,017,588

December 31, 2003M a t u r i t i e s

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

5. Bank loans and notes payable (continued)

During 2004, the Company contracted four revolving credit lines with Bancomer, Banorte, Banamex and Scotiabank Inverlat for theamount of $ 7,000, $ 8,000, $ 6,000 and $ 5,000, respectively. Maturity dates are January 31, 2005, January 14, 2005, January 13,2005 and January 14, 2005 respectively. At December 31, 2004, lines for $ 24,000 (Ps. 269,521) have been exercised.

At December 31, 2004, future maturities of long-term debt were as follows:

The Syndicated loan and outstanding bank loan agreements establish certain obligations and restrictive covenants with respect to certaintransactions including, the payment of cash dividends, mergers and combinations, the disposal of fixed assets, information reportingrequirements and others. In addition, the Company is required to maintain certain financial ratios. At December 31, 2004, the Companywas in compliance with all of its obligations and restrictions established by these agreements.

6. Foreign currency position

The Company had the following U.S. dollar denominated assets and liabilities at December 31, 2003 and 2004:

Dollar denominated assets and liabilities were translated to Mexican pesos using the interbank rates at December 31, 2003 and 2004 ofPs. 11.235 and Ps. 11.230 per U.S. dollar, respectively. The exchange rate at February 14, 2005 was Ps. 11.162 per U.S. dollar.

Foreign currency denominated sales during the years ended December 31, 2002, 2003 and 2004 were Ps. 1,491,637 ($130,781), Ps.1,574,280 ($ 134,647) and Ps. 1,740,786 ($ 150,844), respectively (calculated using the Interbank Rate at the end of each month), andrepresented 43.63%, 43.93% and 44.24 % of total net sales, respectively.

Most of the Company's machinery and equipment is imported, primarily from Italy and Spain.

During the years ended December 31, 2002, 2003 and 2004, the Company imported inventory and machinery and equipment into Mexicototaling $ 29,690, $ 47,788, and $52,429 respectively.

Current assets

Current liabilities Long-term liabilitiesTotal liabilitiesNet short position

Consolidated Financial Statements

24

Maturities20062007

Maturities20062007200820092010

Before prepaymentPs. 527,952

280,854

Ps. 808,806

With newsyndicated credit

amountPs. 67,380

202,140336,900539,040202,140

Ps. 1,347,600

2004$ 41,158

65,75872,022

$ 137,780$ ( 96,622)

2003$ 50,464

48,73486,553

$ 135,287$ ( 84,823)

December 31,

Consolidated Financial Statements

25

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

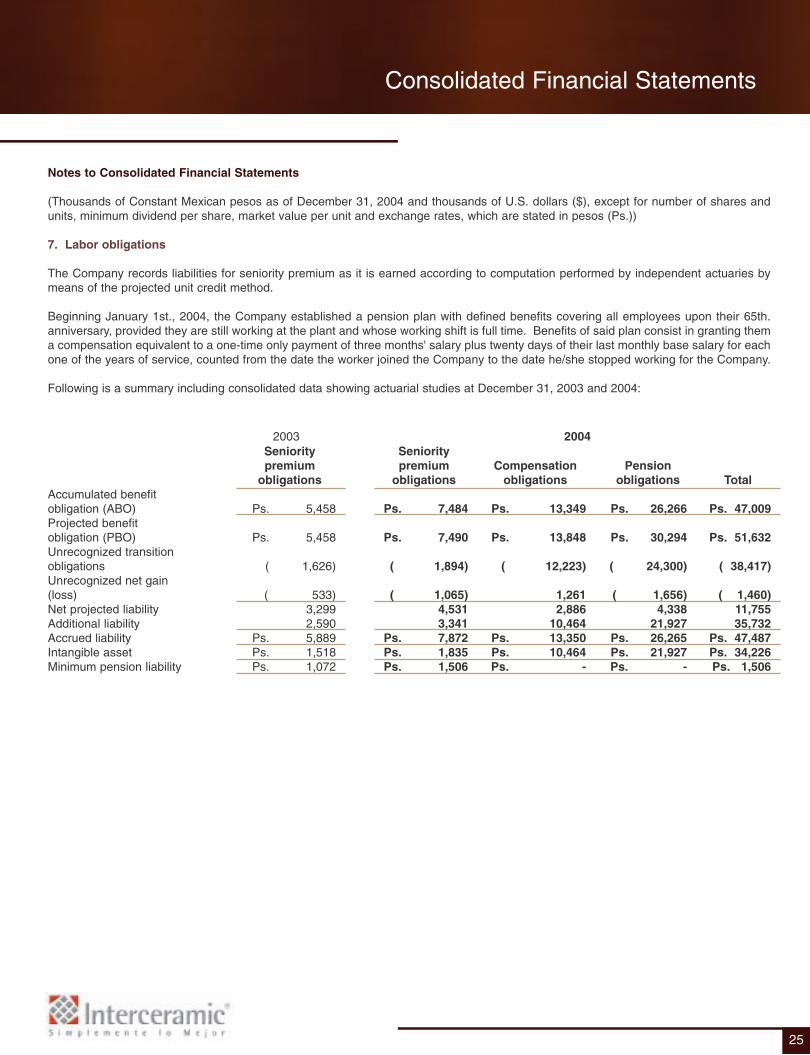

7. Labor obligations

The Company records liabilities for seniority premium as it is earned according to computation performed by independent actuaries bymeans of the projected unit credit method.

Beginning January 1st., 2004, the Company established a pension plan with defined benefits covering all employees upon their 65th.anniversary, provided they are still working at the plant and whose working shift is full time. Benefits of said plan consist in granting thema compensation equivalent to a one-time only payment of three months' salary plus twenty days of their last monthly base salary for eachone of the years of service, counted from the date the worker joined the Company to the date he/she stopped working for the Company.

Following is a summary including consolidated data showing actuarial studies at December 31, 2003 and 2004:

Accumulated benefitobligation (ABO)Projected benefit obligation (PBO)Unrecognized transitionobligationsUnrecognized net gain (loss)Net projected liability Additional liabilityAccrued liabilityIntangible assetMinimum pension liability

Senioritypremium

obligations

Ps. 5,458

Ps. 5,458

( 1,626)

( 533)3,2992,590

Ps. 5,889Ps. 1,518Ps. 1,072

Senioritypremium

obligations

Ps. 7,484

Ps. 7,490

( 1,894)

( 1,065)4,5313,341

Ps. 7,872Ps. 1,835Ps. 1,506

Compensationobligations

Ps. 13,349

Ps. 13,848

( 12,223)

1,2612,886

10,464Ps. 13,350Ps. 10,464Ps. -

Pensionobligations

Ps. 26,266

Ps. 30,294

( 24,300)

( 1,656)4,338

21,927Ps. 26,265Ps. 21,927Ps. -

Total

Ps. 47,009

Ps. 51,632

( 38,417)

( 1,460)11,75535,732

Ps. 47,487Ps. 34,226Ps. 1,506

2003 2004

Consolidated Financial Statements

26

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

7. Labor obligations (continued)

The components of the net periodic pension cost during the years ended December 31, 2002, 2003 and 2004 were as follows:

The transition liability is being amortized over a period of 21 years.

The significant assumptions considered in determining the net periodic pension cost during the years ended December 2002, 2003 and2004 were:

The Company's subsidiary located in the United States has a defined contribution savings plan covering substantially all its employees.Total contributions for the years ended December 31, 2002, 2003 and 2004 were approximately Ps. 3,034 ( $279), Ps. 2,927 ( $249) andPs. 3,099 ( $ 276), respectively.

Change in benefit obligation:Net liabilities projected to January 1st 2004Liabilitites at January 1st 2004

subsidiary franchises acquired:

Cost of pension:Service costInterest cost

Expected fund returnAmortization of transition liabilityAmortization of actuarial lossesCurtailment losses Inflation effectsNet periodic pension cost

Benefits paid by the Company Adjustment for actual amount expensed Net liabilities projected to December 31st. 2004

Senioritypremium

obligations

Ps. 3,690

-

725263

- 80

( 10) 332

( 48) 1,342

( 1,420)

-

Ps. 3,612

Senioritypremium

obligations

Ps. 3,612

-

730293

- 97

( 9) -

( 133)978

( 1,323)

32

Ps. 3,299

Senioritypremium

obligations

Ps. 3,299

549

844323

( 6) 94 5 -

1951,455

( 602)

( 170)

Ps. 4,531

Compensationobligations

Ps. -

-

1,739536

- 499

- -

1122,886

-

-

Ps. 2,886

Pension Planobligations

Ps. -

-

2,0051,174

- 992

- -

1674,338

-

-

Ps. 4,338

Total

Ps. 3,299

549

4,5882,033

( 6) 1,585

5 -

4748,679

( 602)

( 170)

Ps. 11,755

2002 2003 2004

Discount rateRate of pay increasesEffect of inflation

20045.50%1.50%4.00%

20035.50%2.50%5.00%

20025.50%2.50%5.00%

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

8. Stockholders´ equity

The Company's capital stock is variable with a fixed minimum of Ps. 227,955 (Ps. 8,000 nominal).

The Company's capital stock consists of two series of shares (B and D).

Series “B” shares are common registered shares with no par value and full voting rights. They may be freely subscribed, and for a periodof ten years, ending in December 7, 2004, they will be represented by common units, each consisting of two series “B” shares (traded as“Ceramic UB”).

Series “L” registered shares have limited voting rights with no par value and they may be freely subscribed. They are represented for aperiod of ten years by common units, each consisting of a series “D” share and a series “L” share. During this ten-year period, ending inDecember 2004, each series “L” share may only be traded together with a series “D” share (traded as “Ceramic ULD”).

Series “D” shares are preferred registered shares with limited voting rights, without par value and until December 31, 2004 they arerepresented by limited voting units, each consisting of one Series “D” share and one Series “L” Share and may only be traded togetheras a unit (traded as “Ceramic ULD”). The Series “D” shares are entitled to a minimum annual preferred dividend of Ps. 0.025 per share.In any given period in which no minimum preferred dividend is declared or it is paid only partially, such dividend or the unpaid amountshall accumulate for future periods. The accumulated minimum preferred dividends at December 31, 2003 and 2004 is Ps. 6,298 andPs. 7,040.

In December 2004, the Series “L” shares were convert to Series “B” shares, and thereafter, the Series “L” shares will cease to exist as aclass of Company's capital stock, and all voting and other rights previously applicable to holders of Series “L” shares will no longer exist,other than to the extent rights may be available under the Bylaws to holders of Series “B” shares. After December 2004 the Series “D”shares will retain their minimum preferred dividend and limited voting rights.

An analysis of the authorized and outstanding capital stock as of December 31, 2003 and 2004 is as follows:

2003 2004Number of Number of

Consolidated Financial Statements

27

Series"B""D""L"

Units"Ceramic UB""Ceramic ULD"

Shares57,906,63219,646,72019,646,72097,200,072

124,571,150

Units28,953,31619,646,720

-48,600,03662,285,575

Shares129,785,37832,878,746

-162,664,124162,800,072

Units-----

Number of outstanding sharesNumber of authorized shares

Consolidated Financial Statements

28

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

8. Stockholders´ equity (continued)

b) Until before December 2004, the company had established a Stock Option Plan, according to which hundreds of Company employeesand executives could receive options from time to time during their term to buy a number of Limited Vote Units for the eligible employeeas established by the Board Committee.

All shares distributed under this plan were issued and acquired by a trust expressly established for that purpose. Acquisitions made bythe Trust were funded by contributions made by the Company.

During 2004, all employees and executives decided to buy from the Trust all the units to which they were entitled, according to the plan.At the time of the acquisition, all employees had earned said right. At December 31, 2004, therefore, the Trust was cancelled, the totalamount of acquisitions made from the Trust totaled 1,154,700 Series “B” shares and 1,154,700 Series “D” shares, limited vote units, forthe amount of $14,473. At December 31, 2003, the Trust balance amounted to 1,203,000 limited vote units, totaling $14,579.

c) During 2004, the Company increased the reserve for repurchase of share for $ 49,023 and during 2003, it repurchased the followingshares:

d) In conformity with the Mexican Corporations Act, at least 5% of net income of each year must be allocated to increase the legal reserve.This practice must be continued until the legal reserve reaches 20% of capital stock issued and outstanding. As of December 31, 2004,the Company has a legal reserve of Ps. 37,682 that is included in retained earnings.

e) An analysis of cumulative comprehensive income (loss) at December 31, 2002, 2003 and 2004 is as follows:

Series“B”“L”“D”

Units"Ceramic UB""Ceramic ULD"

Shares5,272,3981,785,1401,785,1408,842,678

Units2,636,1991,785,140

-4,421,339

Shares----

Units----

2003 2004Number of Number of

Cumulative effect of deferred income taxesMinimum pension liabilityDeficit from restatement of stockholders' equityEffect of translation of foreign SubsidiariesCumulative comprehensive income (loss)

2004

Ps. ( 334,850)( 1,506)(1,230,565)

103,234Ps. (1,463,687)

2004Thousands ofU.S. dollars

$ ( 29,817) ( 134)( 109,578)

9,192$ ( 130,337)

2003

Ps. ( 334,850)( 1,072)( 1,273,360)

100,811Ps. ( 1,508,471)

2002

Ps.( 334,850)-

( 1,327,961)81,114

Ps.( 1,581,697)

Consolidated Financial Statements

29

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

9. Income taxes, asset tax and employee profit sharing

a) Interceramic and its subsidiaries in Mexico are each subject to the payment of income and asset tax. The Company's U.S. subsidiariesare subject to state and federal taxes income. These taxes are computed by Interceramic and each subsidiary separately and each filesits own tax return.

An analysis of income and asset tax expense for the years ended December 31, 2002, 2003 and 2004 is as follows:

b) An analysis of the deferred tax liabilities (assets) at December 31, 2003 and 2004 is as follows:

A valuation allowance has been recorded due to the uncertainly of realizing a portion of the Company's tax loss and assets carryforwards,primarily from its operations in the United States.

Current income tax and asset taxDeferred income tax expense (benefit)

2004Ps. 29,446

26,397Ps. 55,843

2003Ps. 22,082

26,924Ps. 49,006

2002Ps. 21,821

( 9,444)Ps. 12,377

Deferred tax liabilitiesInventoriesFixed assetsForeign subsidiaries deferred tax liabilities and

effect of translation

Deferred tax assetsAllowance for doubtful accountsProvisionsTax loss carryforwardsAsset tax paid in prior years

Less: valuation allowanceNet deferred income tax liabilities

2004

Ps. 187,373 385,248

21,751594,372

1,08021,654

293,29441,602

( 357,630)

291,499Ps. 528,241

2003

Ps. 183,578367,562

43,577594,717

89610,563

370,57152,452

( 434,482)

302,948Ps. 463,183

Consolidated Financial Statements

30

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

9. Income taxes, asset tax and employee profit sharing (continued)

c) The portion of deferred income taxes attributable to the excess of indexed costs over replacement cost and the effect of translation offoreign subsidiaries have an effect on deferred income taxes charged to income for the years ended December 31, 2002, 2003 and 2004as analyzed below:

(1) Since current tax legislation recognizes partially the effects of inflation on certain items that give rise to deferred taxes, the current yearnet monetary effect on such items has been reclassified in the statement of income from result from the monetary position result todeferred income tax expense of the year.

d) A review of the main items that in 2002, 2003, and 2004 originated a difference between income tax computed at the current tax rateof 35%, 34%, and 33%, respectively, and the provision recorded by the Company for income tax and asset tax is as follows:

Change in deferred income tax liabilitiesLess:

Effect of inflation, net monetary effect (1)Opening balance of deferred tax by adquired

franchisesChange in deferred income taxes

recorded in deficit from restatementof stockholders' equity

Change in deferred income taxesrecorded in effect of translation of foreign subsidiaries

Deferred income tax expense (benefit) includedin statements of income

2004Ps. 65,058

29,923

( 29,978)

( 16,654)

( 21,952)

Ps. 26,397

2003Ps. 100,929

18,843

-

( 69,879)

( 22,972)

Ps. 26,921

2002Ps. 11,318

21,162

-

( 30,925)

( 10,998)

Ps. ( 9,443)

Income before provision for income tax andemployee profit sharing Tax computed over income before income taxand employees profit sharing (35%, 34% and33%, respectively)

Inflationary effects Non-deductible expensesOtherChange in valuation allowanceCost of income tax at current rate Effect of change in income tax rates Net income tax expenseEffective rate

2004

$ 276,535

$ 91,256

( 3,220)8,663

14,983 5,023

116,705( 60,862)$ 55,843

42%

2003

$ 114,101

$ 38,795

( 595)3,8081,7105,876

49,594( 588)

$ 49,00643%

2002

$ 134,252

$ 46,990

( 185)14,022

42 ( 32,983)

27,886( 15,509)

$ 12,37720%

Consolidated Financial Statements

31

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

9. Income taxes, asset tax and employee profit sharing (continued)

Beginning on January 1, 2002, gradual decrease of one percentage point for each year beginning from 2003 was approved, until the 32%rate is reached in 2005. However, in December 2004, a gradual decrease has been approved again to lower the Income Tax rate. During2005, the rate will be 30%, 29% for 2006, and 28% from 2007and thereafter. The effects of this change represented a benefit in incomeof the year for Ps. 60,862.

e) The company has fiscal losses that according to the income tax law effective in Mexico may be amortized against fiscal incomegenerated over the first ten years. Fiscal losses may be restated following certain procedures established by law.

The Company has in excess Asset Tax in prior years over Income Tax due, which according to the applicable law may be recoveredthrough income generated over the next ten years. Receivable Asset Tax may be restated through certain procedures established in saidlaw. In 2002, 2003, and 2004, Interceramic did not make any payment for Asset Tax since it exercised the immediate deduction optionof investments on fixed assets. Some subsidiaries paid Asset Tax for $ 5,955, $ 5,244 and $ 1,558, for years 2002, 2003, and 2004,respectively.

An analysis of the available tax loss carryforwards and recoverable asset tax for the Company's Mexican subsidiaries at December 31,2004, restated for inflation, is as follows:

Interceramic, Inc., the Company's US subsidiary, has net operating loss carryforwards for federal income tax purposes, which if not utilizedto offset future taxable income, will expire at various dates as summarized below:

Year of tax loss or payment of asset tax

19971998199920002001200220032004

Tax losscarryforwards

Ps. -7,17234,9119,747211

7,584551,41318,695

Ps. 629,733

Year ofexpiration

20072008200920102011201220132014

Recoverableasset tax

Ps. 7,7643,9465,7935,6646,2645,5155,098 1,558

Ps. 41,602

Year of tax loss199619971998199920002001

Tax losscarryforwards

Ps. 25,171140,21825,24817,45067,89531,000

Ps. 306,982

Year ofexpiration

201120172018201920202021

Consolidated Financial Statements

32

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

9. Income taxes, asset tax and employee profit sharing (continued)

At December 31, 2002, 2003 and 2004, the Company had the following equity account balances for income tax purposes:

Beginning in 1999 and through 2001, the Income Tax law allowed the option of deferring payments of part of income taxes due duringthose years. Deferred of said tax and related income is controlled through the Reinvested Net Fiscal Account (“CUFINRE”). Earningsdistributed in excess of fiscal balances from CUFINRE and CUFIN, will be subject to enacted corporative income tax rate. EffectiveJanuary 1st., 2002, the above-mentioned option of deferring a portion of income tax, was eliminated.

10. Industry segment information

Financial information by geographical area is as follows:

200220032004

Balance of Net TaxProfit Account

(“CUFIN”)Ps. 100,810Ps. 120,418Ps. 229,229

Balance of RestatedContribute

Capital Account (“CUCA”)Ps. 2,045,279Ps. 1,849,312Ps. 1,944,717

Reinvested Net FiscalAccount

(“CUFINRE”)Ps. 20,784Ps. 1,824Ps. 2,102

Net sales:General customersInter-area transfers

Interest expense, net ofmonetary effectNet income DepreciationCapital expendituresTotal assets Long-lived assets:Property, plant and

equipmentOther assets

Mexico

Ps. 2,036,875920,164

Ps. 2,975,039

Ps. (68,635)Ps. 22,530Ps. 117,516Ps. 159,570Ps. 4,160,709

Ps. 1,615,645721,789

Ps. 2,337,434

United States

Ps. 1,382,2829,963

Ps. 1,392,245

Ps. 5,343Ps. 93,605Ps. 49,973Ps. 30,667Ps. 900,637

Ps. 318,1695,160

Ps. 323,329

Eliminations andother adjustments

Ps. -(930,127)

Ps. (930,127)

Ps. -Ps. (18,807)Ps. -Ps. -Ps. (1,637,943)

Ps. -(649,711)

Ps. (649,711)

Consolidated

Ps. 3,419,157-

Ps. 3,419,157

Ps. (63,291)Ps. 97,328Ps. 167,489Ps. 190,237Ps. 3,423,403

Ps. 1,933,81477,238

Ps. 2,011,052

As of for the year ended December 31, 2002

Consolidated Financial Statements

33

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

10. Industry segment information (continued)

Net sales:General customersInter-area transfers

Interest expense, net ofmonetary effectNet income DepreciationCapital expendituresTotal assets Long-lived assets:Property, plant and

equipmentOther assets

Mexico

Ps. 2,099,349850,753

Ps. 2,950,102

Ps. (27,029)Ps. 23,894Ps. 133,796Ps. 122,208Ps. 4,249,407

Ps. 1,754,229768,332

Ps. 2,522,561

United States

Ps. 1,484,66647,373

Ps. 1,532,039

Ps. (2,987)Ps. 7,620Ps. 50,008Ps. 17,949Ps. 887,422

Ps. 303,27411,618

Ps. 314,892

Eliminations andother adjustments

Ps. -(898,126)

Ps. (898,126)

Ps. -Ps. 2,199Ps. -Ps. -Ps. (1,527,967)

Ps. -(680,407)

Ps. (680,407)

Consolidated

Ps. 3,584,015-

Ps. 3,584,015

Ps. (30,016)Ps. 33,713Ps. 183,804Ps. 140,157Ps. 3,608,862

Ps. 2,057,50399,543

Ps. 2,157,046

As of for the year ended December 31, 2003

Net sales:General customersInter-area transfers

Interest expense, net ofmonetary effectNet income DepreciationCapital expendituresTotal assets Long-lived assets:Property, plant and

equipmentOther assets

Mexico

Ps. 2,294,0461,578,873

Ps. 3,872,919

Ps. ( 19,579)Ps. 177,807Ps. 158,653Ps. 380,358Ps. 4,999,243

Ps. 2,197,581955,720

Ps. 3,153,301

United States

Ps. 1,641,062-

Ps. 1,641,062

Ps. ( 262)Ps. 20,805Ps. 51,291Ps. 22,738Ps. 904,856

Ps. 280,7965,020

Ps. 285,816

Eliminations andother adjustments

Ps. -( 1,578,873)

Ps. ( 1,578,873)

Ps. -Ps. (17,998)Ps. -Ps. -Ps. ( 1,524,671)

Ps. -( 850,701)

Ps. ( 850,701)

Consolidated

Ps. 3,935,108-

Ps. 3,935,108

Ps. ( 19,484)Ps. 180,614Ps. 209,944Ps. 403,096Ps. 4,379,428

Ps. 2,478,377110,039

Ps. 2,588,416

As of for the year ended December 31, 2004

Consolidated Financial Statements

34

Notes to Consolidated Financial Statements

(Thousands of Constant Mexican pesos as of December 31, 2004 and thousands of U.S. dollars ($), except for number of shares andunits, minimum dividend per share, market value per unit and exchange rates, which are stated in pesos (Ps.))

10. Industry segment information (continued)

Geographical sales by customer location is as follows:

(*) A small part of these sales did not occur in the United States.

11. Commitments and contingencies

The Company has entered into rental agreements for office space, manufacturing facilities, and equipment used in its operations undernon-cancelable operating leases. A summary of future minimum lease payments under these agreements at December 31, 2004 is asfollows:

Rental expense incurred under operating leases for the years ended December 31, 2002, 2003 and 2004 was Ps.57,527, Ps. 97,983 andPs. 110,353, respectively.

Under certain lease agreements the respective monthly lease payments will increase annually in accordance with the NCPI.

b) The Company is party to various claims, legal actions, and complaints arising in the ordinary course of business. In the opinion ofmanagement and the Company's independent lawyers, all such matters are without merit or are of such nature, or involve such amounts,that an unfavorable disposition would not have a material effect on the financial position or results of operations of the Company.

c) Derived from the construction of the new plant, which will be used to manufacture ceramic tile, operations are expected to start in May2005, the company has entered into contracts with Arquitectura Habitacional e Industrial, S.A. de C.V., to invest approximately Ps.84,217on the construction work, of which the amount of Ps. 52,155 had been invested at December 31, 2004. This amount has already beenrecorded as investment projects under fixed assets.