2006 full year results roadshow presentation · this presentation contains forward looking...

TRANSCRIPT

1.

2006 Full Year Results2006 Full Year ResultsRoadshow PresentationRoadshow Presentation

22 February 200722 February 2007

2.

A$6.41/bbl 3%Reported A$643m 16%

Sales Revenue$2,769m 12%

0500

1000150020002500

2004 2005 2006

$2,144m 17%

0

1000

2000

3000

2004 2005 2006

Strong Operating PerformanceStrong Operating Performance

0

20

40

60

80

2004 2005 2006

0

200

400

600

800

2004 2005 2006

Production

2P ReservesProduction Costs/bblNPAT

EBITDAX

6

6.2

6.4

6.6

6.8

2004 2005 2006

0200400600800

1000

2004 2005 2006

61.0 mmboe 9%

mm

boe

mm

boe

A$m

A$m

A$/b

blA$

m

819 mmboe 6%

6.0

Underlying A$683m 7%

3.

Banjar Panji IncidentBanjar Panji Incident

• Santos 18% non-operated interest

• Mud flow commenced May 2006

• Response effort managed by a

National Mitigation Team

• Financial impact remains uncertain

4.

14% Increase in Contingent Resources14% Increase in Contingent Resources

Over 2.2 billion Over 2.2 billion boeboe of contingent resourceof contingent resource

Australia OnshoreAustralia Onshore733 mmboe733 mmboe

• Evans Shoal• Caldita/Barossa• Petrel/Tern• Reindeer

PNGPNG363 mmboe363 mmboe

• Hides• Barikewa• Elevala

AsiaAsia117 mmboe117 mmboe

• Hiu Aman• Wortel• Blackbird/ Dua• Swan

• Fairview• Roma

Australia OffshoreAustralia Offshore1,025 mmboe1,025 mmboe

5.

A Portfolio of Growth BusinessesA Portfolio of Growth Businesses

2.2. Eastern Australian gasEastern Australian gas

1.1. Cooper Basin oilCooper Basin oil

3.3. Western Australian oil and gasWestern Australian oil and gas

5.5. Asian growthAsian growth

4.4. LNG projectsLNG projects

6.

Santos competitive advantageSantos competitive advantage

Cooper Basin OilCooper Basin Oil

High value opportunityHigh value opportunity

Oil prices higher for longer

Ability to execute low cost program

Over 700 mmbbl original oil in place

Positive 2006 results

Utilising modern rigs and proven technology to increase recovery factors

Largest onshore Australian oil acreage position: 27,000km2

Doubling program in 2007

Unique capabilities, knowledge, infrastructure and short cycle time

7.

2006 2006 PlanPlan

20072007TargetTarget

2006 results above expectations

% % ChangeChange

Cooper Basin Oil Cooper Basin Oil –– 2006 Results2006 Results

Wells 100 108 8% 190

Success Rate 75% 79% 4% 75%

2P Reserves added (mmbbl) 7 15 114% 17

Initial rate per well (bbl/d) 120 156 30% 160

Capex $170m $186m 9% $330m

Full-cycle F&D Cost (A$/bbl) 18 22 22% 22

2006 Actual2006 Actual

8.

Significant near and medium term production impactSignificant near and medium term production impact

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Actual Projected

Bar

rels

per

day

(S

anto

s sh

are)

Base

Cooper Basin Oil Cooper Basin Oil –– Production OutlookProduction Outlook

2004 2005 2006 2007 2008 2009 2010

9.

Eastern Australian GasEastern Australian Gas

Gas demand growing strongly, PNG gas project suspended

Largest acreage operator in Otway/Sorell Basins

Otway Basin now a major gas producing area

CSG emerging to fill market demand

Gas is a low carbon emission fuel

Established leading position in CSG

Large uncontracted gas position, demonstrated contracting capability

Increasing gas demand and price

Strong market growthStrong market growth Santos is well positionedSantos is well positioned

10.

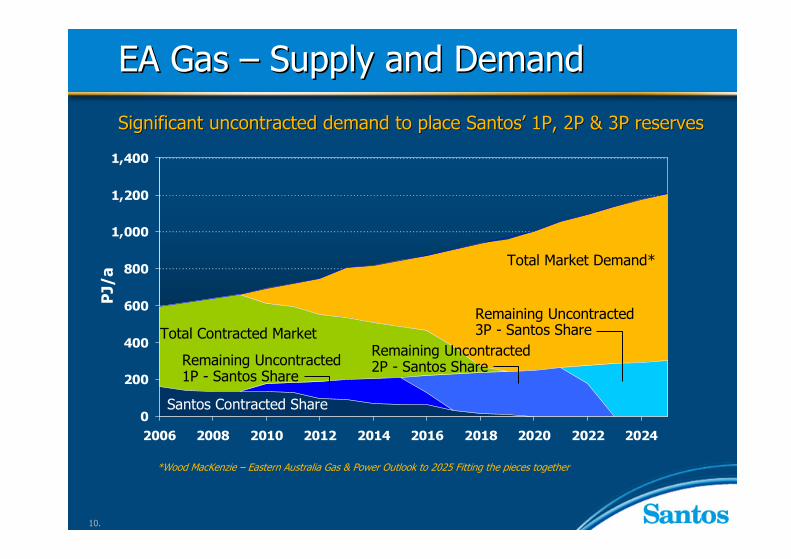

Significant uncontracted demand to place SantosSignificant uncontracted demand to place Santos’’ 1P, 2P & 3P reserves1P, 2P & 3P reserves

EA Gas EA Gas –– Supply and DemandSupply and Demand

0

200

400

600

800

1,000

1,200

1,400

2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

*Wood MacKenzie – Eastern Australia Gas & Power Outlook to 2025 Fitting the pieces together

Total Market Demand*

Santos Contracted Share

Remaining Uncontracted 1P - Santos Share

Remaining Uncontracted 2P - Santos Share

Remaining Uncontracted 3P - Santos Share

PJ/

a

Total Contracted Market

11.

0 100

kilometres• Strong competitive advantages

- Highest quality acreage

- Industry leading capability

- Existing infrastructure

- Largest onshore operator

Material CSG legacy asset establishedMaterial CSG legacy asset established

EA Gas EA Gas –– CSG BusinessCSG Business

LegendSantos acreageExtent of Surat/Bowen BasinsSantos CSG projectsOther producing CSG projectsGas pipeline

Oil pipeline

LegendSantos acreageExtent of Surat/Bowen BasinsSantos CSG projectsOther producing CSG projectsGas pipeline

Oil pipeline

Moranbah

EmeraldBowen

Basin

MahaloMouraDawson ValleyMungiQld

FairviewSpring Gully

Roma Shallow Gas (CSG)

Surat Basin

NSW

Roma

TardrumScotia/Peat

Moonie

Toowoomba

Kogan Nth

BrisbaneBrisbane

MaryboroughMaryborough

BundabergBundaberg

GladstoneGladstoneRockhamptonRockhampton

ScotiaScotia

FairviewFairview

RomaRoma

12.

0

50

100

150

200

2006 2007 2008 2009 2010 2011 2012

TJ/d

ay

Scotia Fairview

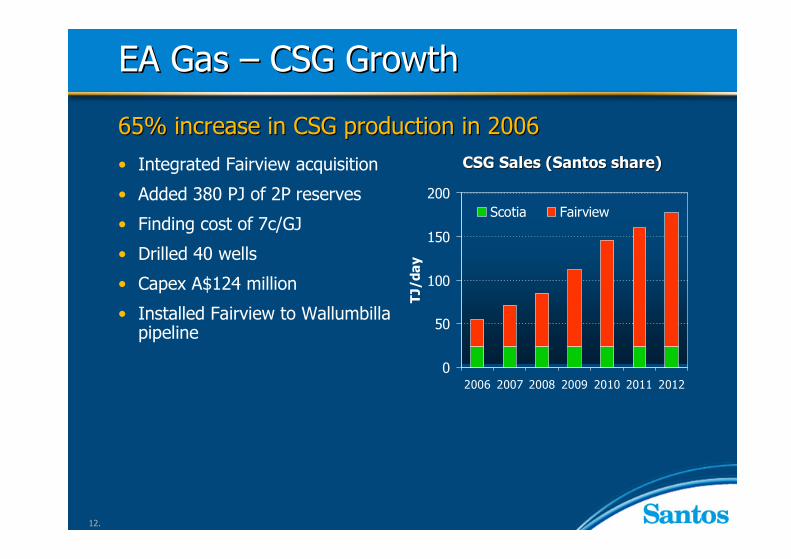

• Integrated Fairview acquisition

• Added 380 PJ of 2P reserves

• Finding cost of 7c/GJ

• Drilled 40 wells

• Capex A$124 million

• Installed Fairview to Wallumbilla pipeline

65% increase in CSG production in 200665% increase in CSG production in 2006CSG Sales (Santos share)CSG Sales (Santos share)

EA Gas EA Gas –– CSG GrowthCSG Growth

13.

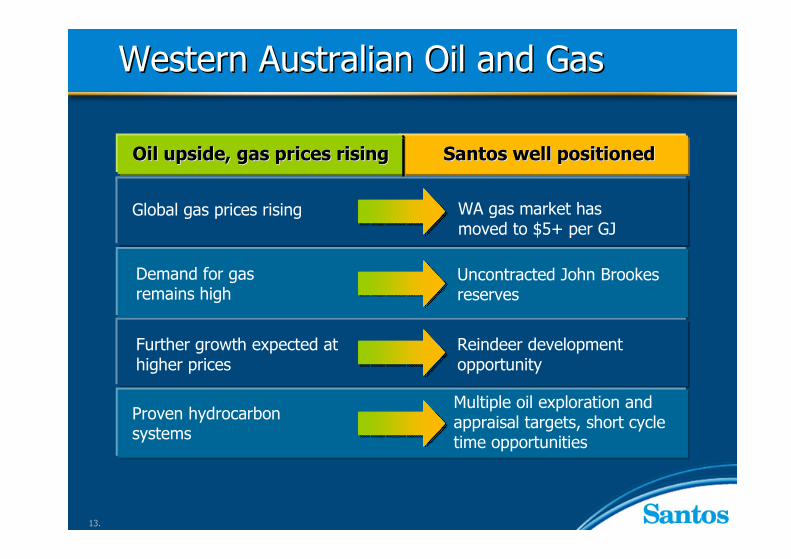

Western Australian Oil and GasWestern Australian Oil and Gas

Oil upside, gas prices risingOil upside, gas prices rising Santos well positionedSantos well positioned

Global gas prices rising

Reindeer development opportunity

Further growth expected at higher prices

Demand for gas remains high

Uncontracted John Brookes reserves

WA gas market has moved to $5+ per GJ

Proven hydrocarbon systems

Multiple oil exploration and appraisal targets, short cycle time opportunities

14.

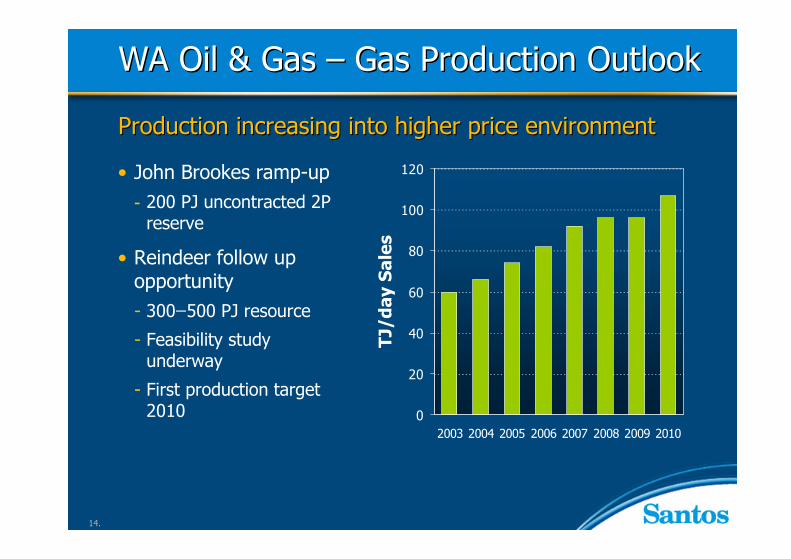

WA Oil & Gas WA Oil & Gas –– GasGas Production OutlookProduction Outlook

Production increasing into higher price environmentProduction increasing into higher price environment

• John Brookes ramp-up- 200 PJ uncontracted 2P

reserve

• Reindeer follow up opportunity- 300 ̶ 500 PJ resource

- Feasibility study underway

- First production target 2010 0

20

40

60

80

100

120

2003 2004 2005 2006 2007 2008 2009 2010

TJ/d

ay S

ales

15.

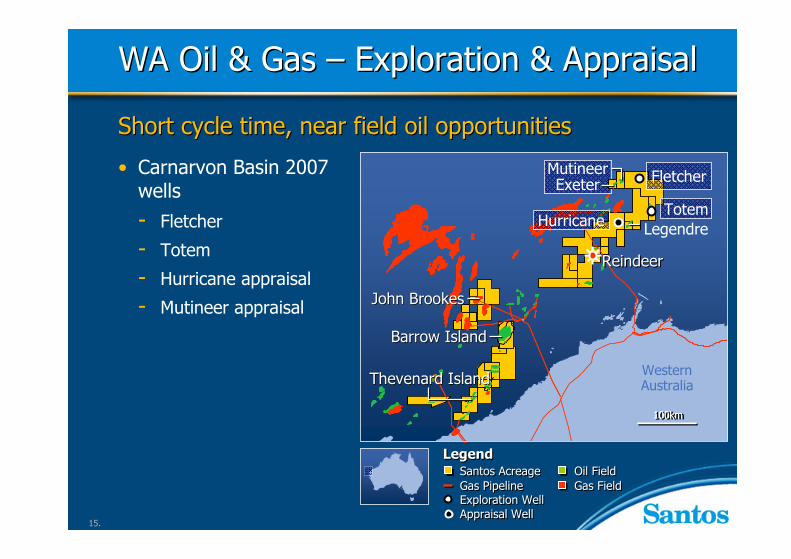

WA Oil & Gas WA Oil & Gas –– Exploration & AppraisalExploration & Appraisal

Short cycle time, near field oil opportunities Short cycle time, near field oil opportunities

• Carnarvon Basin 2007 wells- Fletcher

- Totem

- Hurricane appraisal

- Mutineer appraisalWesternAustralia

WesternAustralia

100km100km100km100km

ReindeerReindeer

Fletcher

Hurricane

MutineerExeter

John BrookesJohn Brookes

LegendSantos Acreage Oil FieldGas Pipeline Gas FieldExploration WellAppraisal Well

LegendSantos Acreage Oil FieldGas Pipeline Gas FieldExploration WellAppraisal Well

Barrow IslandBarrow Island

Thevenard IslandThevenard Island

LegendreTotem

16.

Santos well positionedSantos well positionedFavourable LNG dynamicsFavourable LNG dynamics

Booming demand for LNG

Hides field critical to PNG LNGPNG LNG

Large gas resources a prerequisite

Darwin LNG expansion

Significant contingent resource positions with quality assets

Multiple LNG opportunities

Santos 40% interest in 8+ tcf of resources

LNG ProjectsLNG Projects

17.

• ExxonMobil progressing evaluation of LNG development including Hides field- 5 to 6.5 mtpa LNG plant

- First cargos target 2012-2013

- Santos share 6+ mmboe pa

• Other Santos resources- 43% and operator of Barikewa

- 50% and operator of Elevala

• In total – 363 mmboe contingent resource in PNG

LNG the focus for PNG gas resourcesLNG the focus for PNG gas resources

LNG Projects LNG Projects -- PNGPNG

PRL 9

PDL 3

Papua New GuineaPDL 1PRL 5

SE Gobe

Barikewa

LegendSantos AcreageOil FieldGas FieldOil Pipeline

LegendSantos AcreageOil FieldGas FieldOil Pipeline

Hides

Elevala

MarineTerminal

ProposedLNG Facility

18.

• Material acreage position

• Appraisal ongoing

• 8+ tcf resource

• Aligned with ConocoPhillips

• 3.5 to 6 mtpa train

• First cargos 2013+

Santos well positioned for Darwin second trainSantos well positioned for Darwin second train

LNG Projects LNG Projects -- DarwinDarwin

00 100100

KilometresKilometres

LegendSantos Acreage Gas FieldGas Pipeline

LegendSantos Acreage Gas FieldGas Pipeline

DarwinDarwin

SunriseSunriseAbadiAbadi

CalditaCalditaEvans ShoalEvans Shoal

BarossaBarossa

PetrelPetrel

TernTern

Santos (Op) 40%Shell 50%Osaka Gas 10%

Santos 40%ConocoPhillips (Op) 60%

DLNG1Santos 10.6%ConocoPhillips (Op) 56.7%

19.

Asian GrowthAsian Growth

Santos has a quality portfolioSantos has a quality portfolioHigh growth potentialHigh growth potential

Focussed, long termvision required for success

Blackbird, Dua oil discoveries, Swan gas field, active exploration program

2006 new country entry to Vietnam

Development, production and exploration in Indonesia

Quality acreage captured

Maleo gas project online, Oyong startup 2Q 2007, Kutei

Strategy focus on Asia, USA business for sale

Indian entry, Kyrgyzstan acreage extension, Vietnam new block

20.

Two oil discoveries, with follow-on opportunitiesTwo oil discoveries, with followTwo oil discoveries, with follow--on opportunitieson opportunities

• Blackbird and Dua oil discoveries

• Accelerating seismic into Q1 2007, drilling into Q4 2007

• Commencing development planning

• Swan gas field development potential

• Northern block secured

25km

Blackbird oil discovery

LegendSantos acreage Gas fieldOil Field Gas Pipeline

Dua oil discoveryDuaDua oil discoveryoil discovery

Asian Growth Asian Growth -- VietnamVietnam

Swan gas fieldSwan gas field

12 PSC

21.

Core business positioned for growthCore business positioned for growthCore business positioned for growth

• Oyong Q2 2007 start-up

• Wortel gas discovery- Development planning

underway

• Jeruk development studies ongoing

• Kutei Basin- Exploration/appraisal wells

subject to deep water rig availability

0 250

kilometres

East JavaBasin

East JavaBasin

KuteiBasinKuteiBasin

Wortel

Kalimantan

East Java

Asian Growth Asian Growth -- IndonesiaIndonesia

Oyong

Maleo

LegendSantos acreage Oil pipeline Oil field Gas pipelineGas field

22.

• Attractive frontier basin

• Work program- 1 exploration well

- 2D and 3D seismic

- Estimated cost A$90m

• Emerging market with sound energy fundamentals

High potential regionHigh potential regionHigh potential region

0 100

kilometres

Ganges-BrahmaputraDelta

Ganges-BrahmaputraDelta

Kolkata

India Bangladesh

India

LegendSantos AcreageGas Field

LegendSantos AcreageGas Field

Burma

Asian Growth Asian Growth -- IndiaIndia

23.

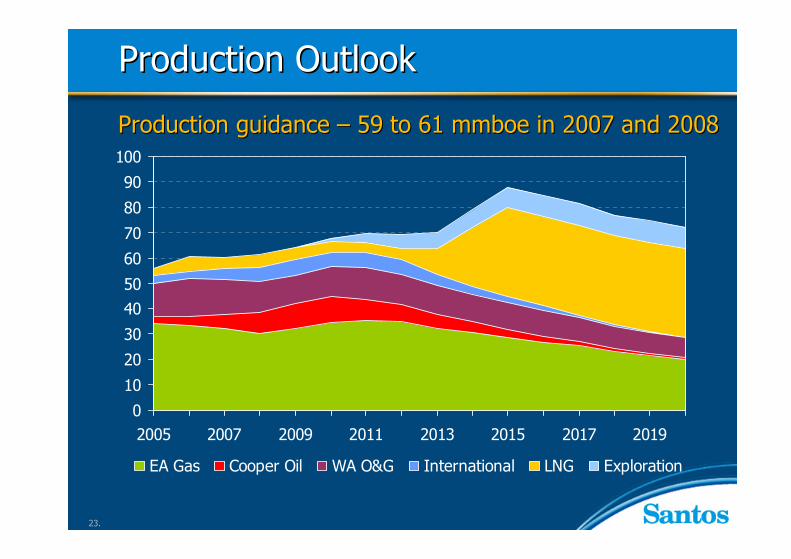

Production OutlookProduction Outlook

Actual Outlook

Production guidance Production guidance –– 59 to 61 59 to 61 mmboemmboe in 2007 and 2008in 2007 and 2008

0

10

20

30

4050

60

70

80

90

100

2005 2007 2009 2011 2013 2015 2017 2019

EA Gas Cooper Oil WA O&G International LNG Exploration

24.

SummarySummary

2. Eastern Australian gas

1. Cooper Basin oil

3. Western Australian oil and gas

5. Asian growth

4. LNG projects

• CSG new legacy asset• Flexibility through hub strategy• Positioned for increasing demand

• Large scale, low risk opportunity• Unique competitive advantage• Acreage and infrastructure

• Increasing gas production into higher price environment

• Near field exploration and appraisal

• Darwin LNG expansion• PNG LNG using Hides gas

• Regional expansion focus

25.

Reference SlidesReference Slides

26.

Cooper Basin Oil 2006 ProgramCooper Basin Oil 2006 Program

108 wells drilled with 79% success rate108 wells drilled with 79% success rate

SouthAustralia

Queensland

Oil PipelineGas Pipeline

Oil PipelineGas Pipeline

LegendSantos AcreageOil FieldGas Field

LegendSantos AcreageOil FieldGas Field

Rest of QldWells drilled 16Yanda 11Challum 3Wackett 1Currambar 1

Success 94%

ATP299PWells drilled 76

Success 75%

SAWells drilled 16JALBU 11 PEL114 3Derrilyn 2

Success 81%

MoombaMoomba

BalleraBalleraJacksonJackson

27.

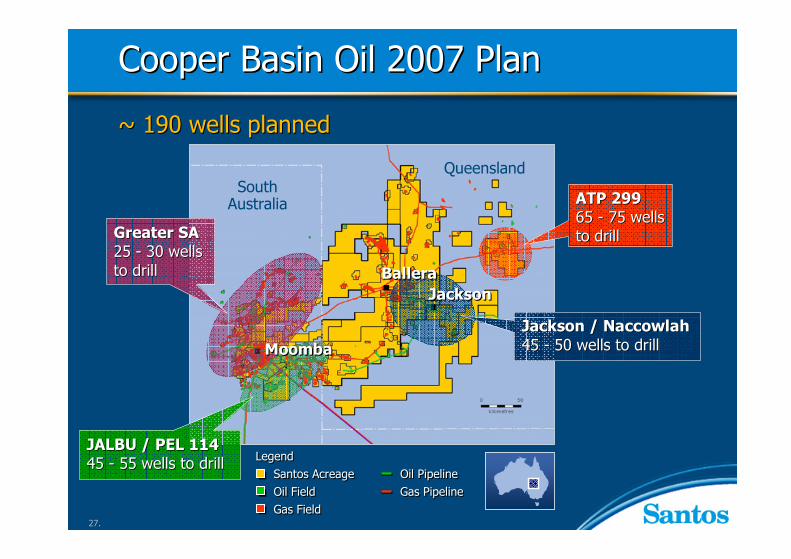

Cooper Basin Oil 2007 PlanCooper Basin Oil 2007 Plan

~ 190 wells planned~ 190 wells planned

SouthAustralia

Queensland

Jackson / NaccowlahJackson / Naccowlah45 45 -- 50 wells to drill50 wells to drill

ATP 299ATP 29965 65 -- 75 wells75 wellsto drillto drill

Oil PipelineGas Pipeline

Oil PipelineGas Pipeline

LegendSantos AcreageOil FieldGas Field

LegendSantos AcreageOil FieldGas Field

Greater SAGreater SA25 25 -- 30 wells 30 wells to drillto drill

JALBU / PEL 114JALBU / PEL 11445 45 -- 55 wells to drill55 wells to drill

MoombaMoomba

BalleraBalleraJacksonJackson

28.

Cooper Basin Oil Cooper Basin Oil -- WaterfloodingWaterflooding

• Without pressure support, an oil reservoir can have recovery factors less than 10% of oil-in-place

• Injection of water into the reservoir provides pressure support (drive) and “sweeps” the oil towards the producing wells

Water injection

Oil Production

ProductionRate

Time

Waterflood, pressuresupport

No pressuresupport, naturalfield decline

29.

Q1 0750OilEgyptRAD 2X

Q4 0737.5OilVietnamFalcon

Q4 07100OilEgyptSEJ-1

Q4 0733OilHoutmanCharon

Q3 0740.5Oil/GasEast JavaEJ-1

Q2 07 22.6OilDampierCharm-1

Q2/Q3 0733.3OilDampierFletcher-1

Q2 0766GasCooperMontegue

Q2 07 33.3OilDampierTotem-1

Q2 0731.3OilDampierHurricane-2

Q1 0750OilSurat/BowenStitch

Q1 0753.8OilSurat/BowenMahogany

%100 - 25050 -1000 – 50

TimingSantos InterestUpside Resource Potential (mmboe)TargetBasin / AreaWell Name

2007 Forward Exploration Schedule2007 Forward Exploration Schedule

The exploration portfolio is constantly being optimised therefore the above program may vary as a result of rig availability, drilling outcomes and as new prospects mature

30.

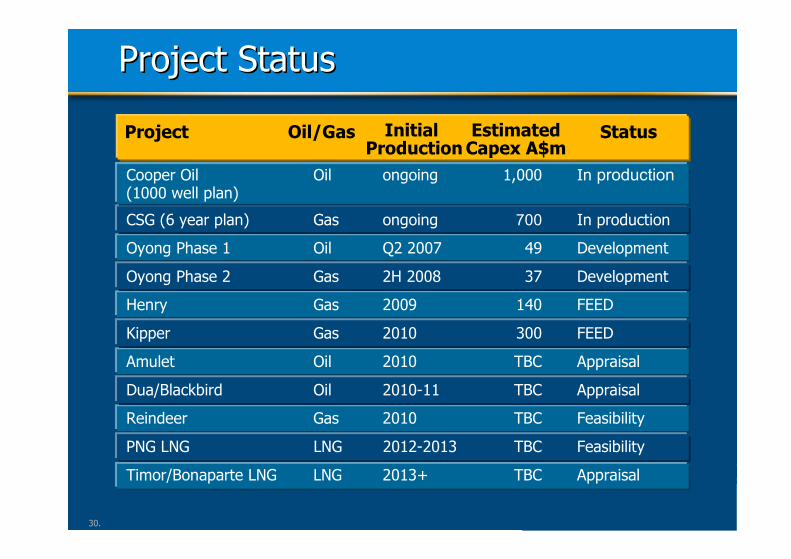

Project StatusProject Status

Project Oil/Gas EstimatedCapex A$m

StatusInitial Production

Cooper Oil Oil ongoing 1,000 In production(1000 well plan)

CSG (6 year plan) Gas ongoing 700 In production

Oyong Phase 1 Oil Q2 2007 49 Development

Oyong Phase 2 Gas 2H 2008 37 Development

Henry Gas 2009 140 FEED

Kipper Gas 2010 300 FEED

Amulet Oil 2010 TBC Appraisal

Dua/Blackbird Oil 2010-11 TBC Appraisal

Reindeer Gas 2010 TBC Feasibility

PNG LNG LNG 2012-2013 TBC Feasibility

Timor/Bonaparte LNG LNG 2013+ TBC Appraisal

31.

Disclaimer & Important NoticeDisclaimer & Important Notice

This presentation contains forward looking statements that are sThis presentation contains forward looking statements that are subject to ubject to risk factors associated with the oil and gas industry. It is belrisk factors associated with the oil and gas industry. It is believed that the ieved that the expectations reflected in these statements are reasonable, but texpectations reflected in these statements are reasonable, but they may hey may be affected by a range of variables which could cause actual resbe affected by a range of variables which could cause actual results or ults or trends to differ materially, including but not limited to: pricetrends to differ materially, including but not limited to: price fluctuations, fluctuations, actual demand, currency fluctuations, geotechnical factors, drilactual demand, currency fluctuations, geotechnical factors, drilling and ling and production results, gas commercialisation, development progress,production results, gas commercialisation, development progress,operating results, engineering estimates, reserve estimates, losoperating results, engineering estimates, reserve estimates, loss of market, s of market, industry competition, environmental risks, physical risks, legisindustry competition, environmental risks, physical risks, legislative, fiscal lative, fiscal and regulatory developments, economic and financial markets condand regulatory developments, economic and financial markets conditions in itions in various countries, approvals and cost estimates.various countries, approvals and cost estimates.

All references to dollars, cents or $ in this document are to AuAll references to dollars, cents or $ in this document are to Australian stralian currency, unless otherwise stated.currency, unless otherwise stated.