2008 general meeting assemblée générale 2008 toronto, ontario 2008 general meeting assemblée...

TRANSCRIPT

2008 General MeetingAssemblée générale 2008

Toronto, Ontario

2008 General MeetingAssemblée générale 2008

Toronto, Ontario

Canadian Institute

of Actuaries

Canadian Institute

of Actuaries

L’Institut canadien desactuaires

L’Institut canadien desactuaires

Contract Classification

Jim Doherty

November 2008

Jim Doherty

November 2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Agenda

• Contract Classification

• A few odds and ends

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

• Contract classification defines the accounting treatment.– i.e. How the liability will be measured on the balance sheet

• Financial Instruments – IAS 39– Amortized Cost or Fair Value

• Insurance Contracts – IFRS 4– Existing accounting measurement

• Discretionary Participation Financial Instruments– Existing accounting measurement

Contract classification

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

• The most significant impacts expected– Financial Instruments (Investment contracts)

– Unbundling of contracts (embedded derivatives)

Contract classification

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

IFRS• Measurement

• Current C GAAP - insurance enterprise level• IFRS 4 - at the contract level• Requires contracts to be classified

– Insurance contracts (IFRS 4)

– Financial Instruments (IAS 39 – IAS 32)

– Service Contracts (IAS 18)

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Definition of an insurance contract• A contract under which one party (the insurer)

accepts significant insurance risk from another party (the policyholder) by agreeing to compensate the policyholder if a specified uncertain future event (the insured event) adversely affects the policyholder.

IFRS 4 Appendix A

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

• Insurance risk is risk, other than financial risk, transferred from the holder of a contract to the issuers

• Financial risk is the risk of a possible future change in one or more of a specified interest rate, financial instrument price, … or other variable– provided in the case of a non-financial variable, that the

variable is not specific to a party to the contract.

• If both financial risk and significant insurance risk are present, contract is classified as insurance.

IFRS 4 Appendix A

Insurance Risk

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

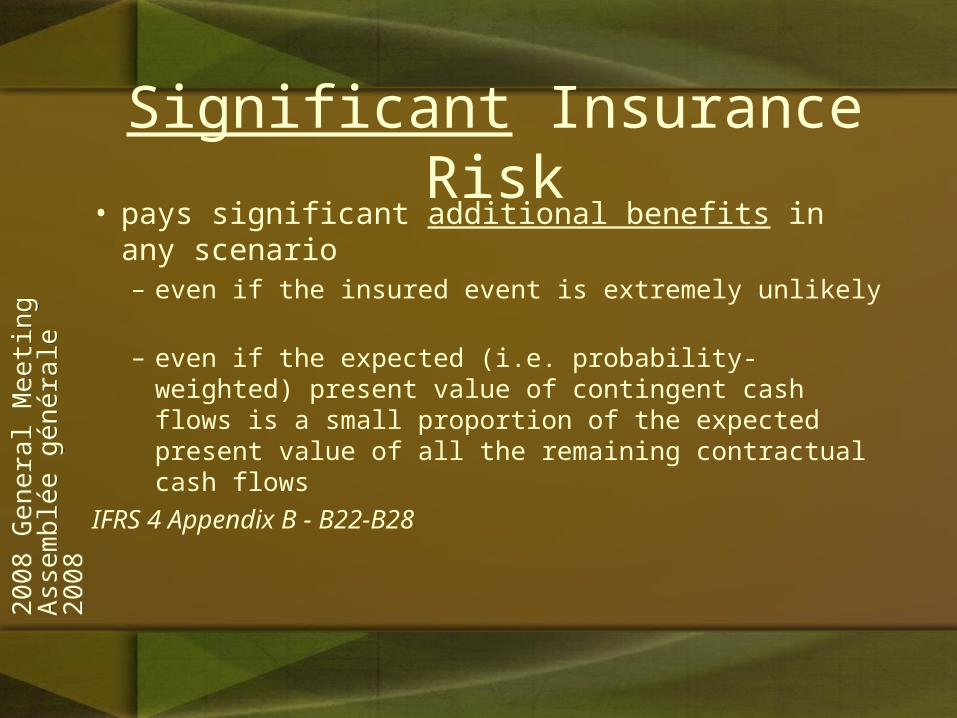

Significant Insurance Risk• pays significant additional benefits in any scenario

– even if the insured event is extremely unlikely

– even if the expected (i.e. probability-weighted) present value of contingent cash flows is a small proportion of the expected present value of all the remaining contractual cash flows

IFRS 4 Appendix B - B22-B28

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

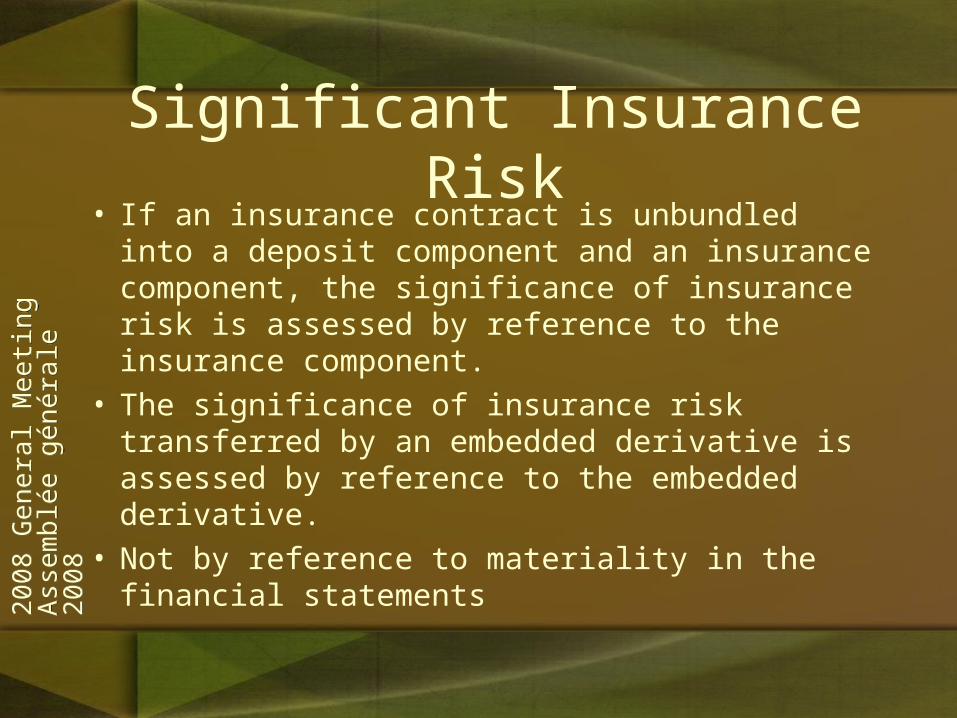

Significant Insurance Risk• If an insurance contract is unbundled into a

deposit component and an insurance component, the significance of insurance risk is assessed by reference to the insurance component.

• The significance of insurance risk transferred by an embedded derivative is assessed by reference to the embedded derivative.

• Not by reference to materiality in the financial statements

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Significant insurance risk• Additional benefits include

– Payments contingent on insurance risk• Term insurance

– timing risk• Whole life contract (payment known, timing unknown) has

additional benefits• Contract where death benefit is equivalent to maturity benefit (if

the maturity benefit is adjusted for time value of money) does not have additional benefits

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

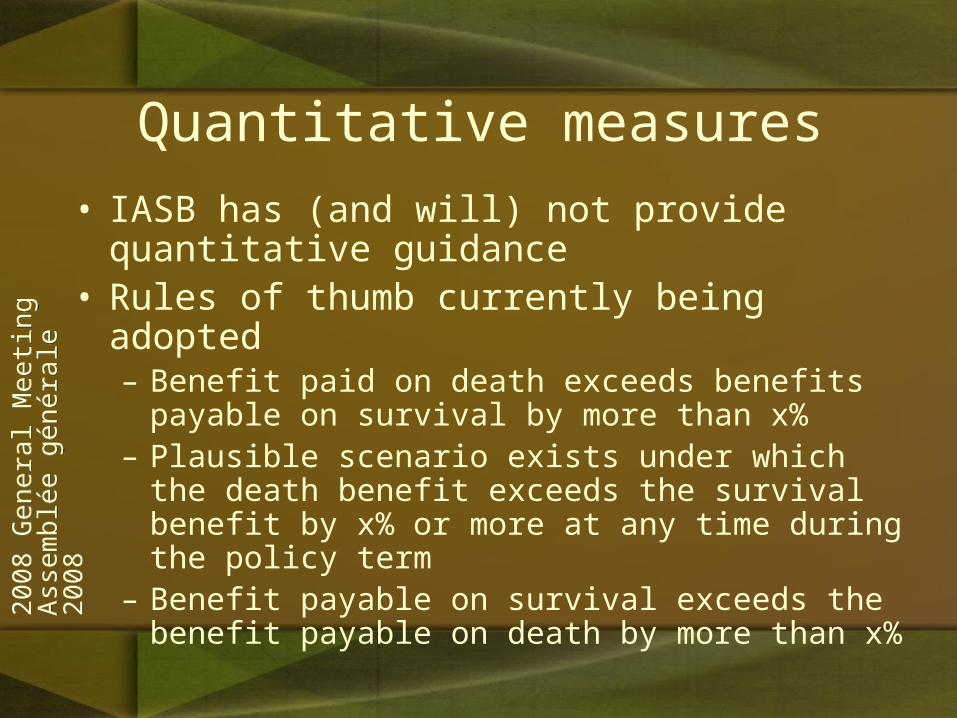

• IASB has (and will) not provide quantitative guidance

• Rules of thumb currently being adopted– Benefit paid on death exceeds benefits payable on survival

by more than x% – Plausible scenario exists under which the death benefit

exceeds the survival benefit by x% or more at any time during the policy term

– Benefit payable on survival exceeds the benefit payable on death by more than x%

Quantitative measures

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Significant Insurance Risk• Document your definition of significant

– This is your value for “x%”

– And the quantitative measures used

• Obtain concurrence of auditor• Apply consistently across all contracts

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Contract Classification• Tends to be a more complicated issue for Life and

Health Insurance – a number of products may have been created primarily

for investment purposes

• However, due to the somewhat liberal definitions in IFRS 4– most Life & Health Insurance contracts are expected to

meet the insurance contract threshold

– but an insurer still needs to conduct an analysis of it’s contracts!

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Contract Classification• Remember that the classification is at a contract

level and not at a product level.– Contracts entered into simultaneously with the same

policyholder count as one contract

• Classification is done as at the date of inception

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Contract Classification• Homogeneous blocks

– Contracts may be classified homogeneously on materiality grounds

– Relatively homogeneous book known to consist of contracts that all transfer insurance risk

– need not examine each contract

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Contract Classification• Depends on the facts and circumstances of

the contract terms• Document these and the rationale for the

conclusion reached– Particularly for complex products or where

judgement was required

• Obtain auditor concurrence

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Classification flowchart

Is there significantinsurance risk present

in the contract?

Is there adeposit component to the

contract? If so, is the deposit componentindependent of the insurance

cash flows?

Are any elements ofthe benefit driven by discretionary

participation

Insurancefeatures present

in contract

Classified as aninvestment contract

Deposit component

Yes

No

Insurance and depositcomponents of contract must, ifnot recognised, be unbundled

and valued separately

Yes

No

Insurancecomponent

Product is an InvestmentContract without discretionary

participation features

Product is anInsurance Contract

Product is an InvestmentContract with discretionary

participation featuresYes

No

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Life Insurance

Individual Insurance

Annuities

Group Insurance

Term Par Universal Life

Variable Universal

Life

Life Contingent Payout

Annuities

Fixed Payout Annuity

Fully Insured

Plan

Experience Rated Refund

Administrative Services Only

Insurance Not InsuranceBifurcation or TBD?

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Individual Insurance• Term Insurance• Whole Life• T 100• CI• DI• LTC• Riders

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Individual Insurance• UL

• VUL

• VL

• Index Linked

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Group L&H• Health• LTD• Life• Affinity• ASO• ERR• Hold Harmless agreements

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Payout Annuities• Life

• Settlement

• Structured Settlement

• Fixed

• Index Linked

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Seg Funds / VA• Group

• Individual

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

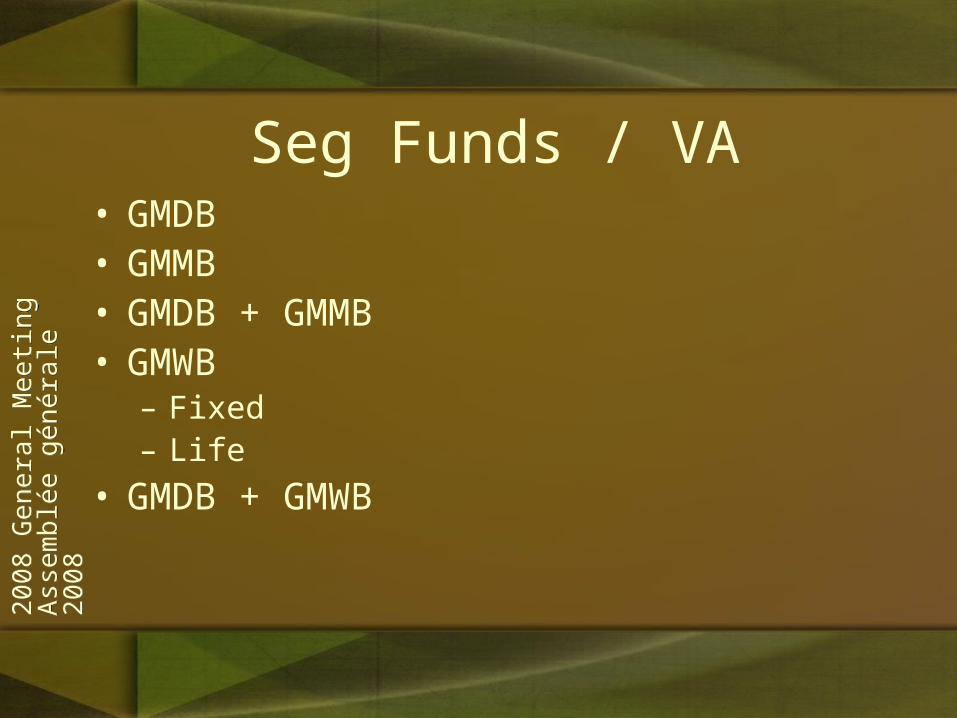

Seg Funds / VA• GMDB• GMMB• GMDB + GMMB• GMWB

– Fixed– Life

• GMDB + GMWB

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Seg Funds / VA• Normally a return of a % of premium on a unit-

linked contract would classify the contract as insurance. – IFRS requires only a single scenario for the contract to

be insurance.

• A situation where this may be questioned is if the fund is cash or bonds (depending on duration)

• Need to determine if there really is a chance that the death benefit would become significant.

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Seg Funds / VA• GMDB combined with GMMB

– Paragraph B27 • additional benefits can be the requirement to pay

benefits earlier

• if the insured event occurs earlier and

• the payment is not adjusted for the time value of money

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

An aside• Seg funds are on balance sheet – one line for the

assets and one for the liabilities • Treasury shares

– where the segregated funds hold shares of the insurance company

– these will probably have to be eliminated from the asset side as treasury shares, but kept on the liability side

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Deferred Annuities• Individual

– Annuitization benefit on a guaranteed basis– No MV adjustment on death

• Group– Deposit Administration

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

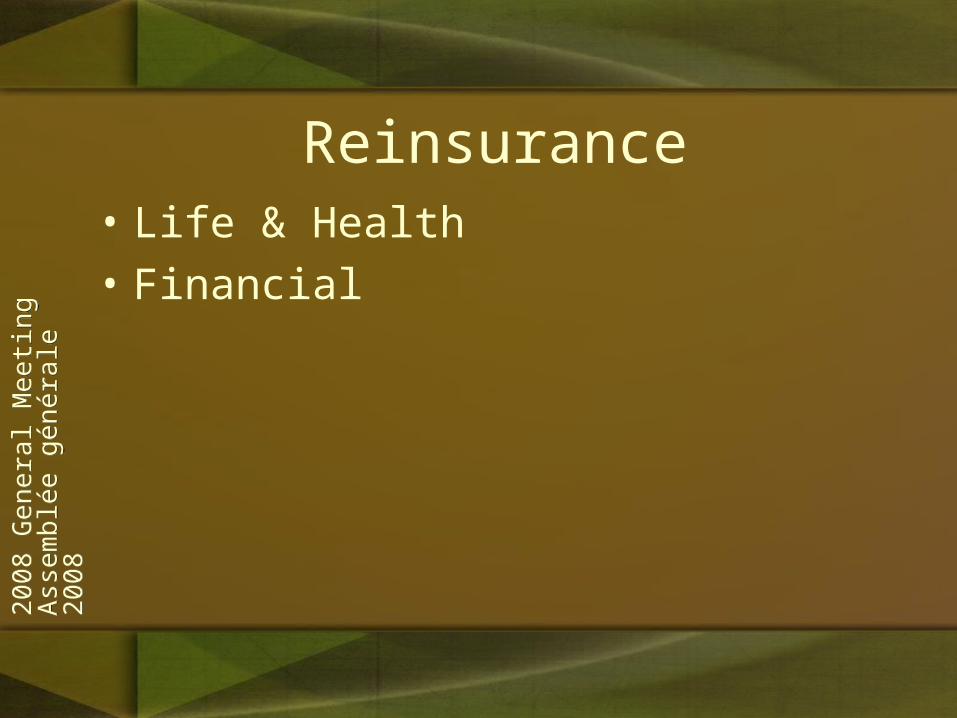

Reinsurance• Life & Health

• Financial

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

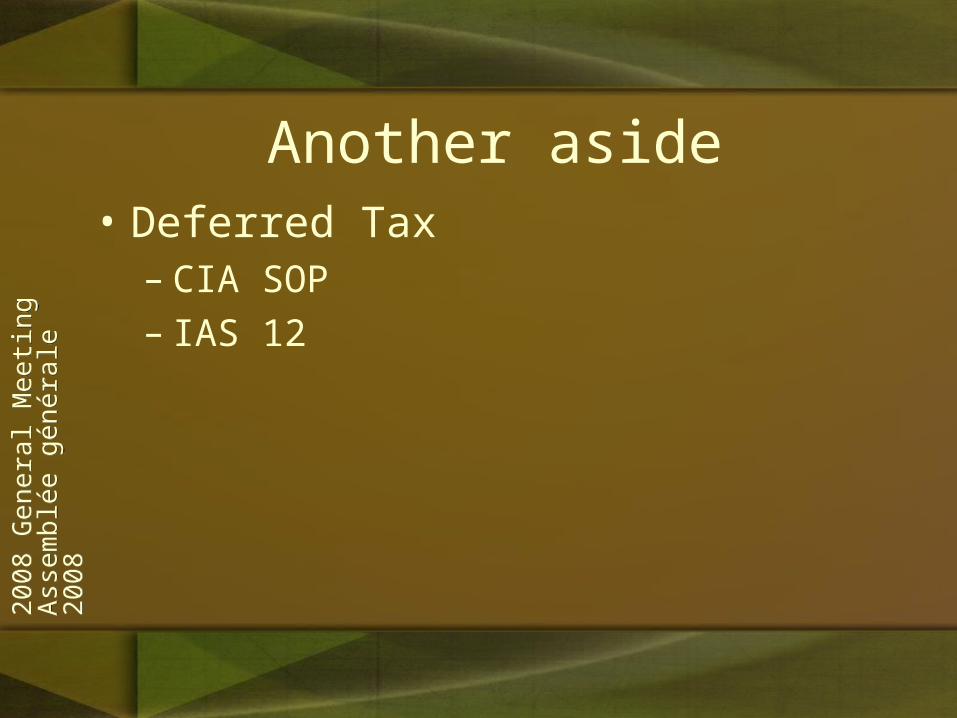

Another aside• Deferred Tax

– CIA SOP– IAS 12

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Contract Classification• IBNR • Claims in the course of payment• Dividends / Premiums / Proceeds on Deposit• Advance Premiums

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

Contract Classification• Facts and circumstances

• Document these and the rationale for the conclusion reached– Particularly for complex contracts or where

judgement was required

• Obtain auditor concurrence

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

And another aside• If the contract is a financial instrument and

measured at amortized cost under IAS 39• Need to check for embedded derivatives

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

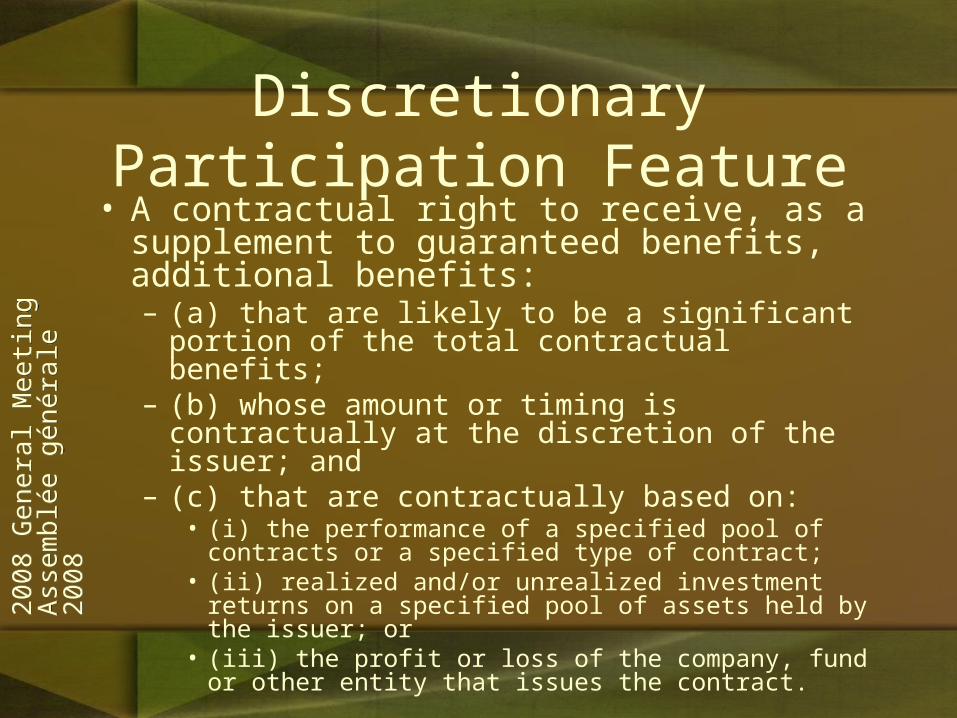

Discretionary Participation Feature• A contractual right to receive, as a supplement to

guaranteed benefits, additional benefits:– (a) that are likely to be a significant portion of the total

contractual benefits;– (b) whose amount or timing is contractually at the

discretion of the issuer; and– (c) that are contractually based on:

• (i) the performance of a specified pool of contracts or a specified type of contract;

• (ii) realized and/or unrealized investment returns on a specified pool of assets held by the issuer; or

• (iii) the profit or loss of the company, fund or other entity that issues the contract.

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

2008

Gen

eral

Mee

ting

Ass

embl

ée g

énér

ale

2008

IAS 39• If a Financial Instrument has a discretionary

participation features (DPF)– The whole contract is valued using IFRS 4. – If the deposit element can be separated, then it may be

accounted for under IAS 39 - but this is at the choice of the insurance company

– There are requirements to check that the liability held is at least as big as that which would be held under IAS 39.

Questions

2008 General MeetingAssemblée générale 2008

Toronto, Ontario

2008 General MeetingAssemblée générale 2008

Toronto, Ontario

Canadian Institute

of Actuaries

Canadian Institute

of Actuaries

L’Institut canadien desactuaires

L’Institut canadien desactuaires