2009 commercial real estate report€¦ · 2009 commercial real estate report ... future trends....

TRANSCRIPT

2009 Commercial Real Estate ReportCedar Rapids | Iowa City / Coralville | Cedar Falls / Waterloo

Welcome

NAI Iowa Realty Commercial is excited to present our Tenth Annual Commercial Real Estate Report. This report is an in-depth analysis of commercial real estate in the Greater Cedar Rapids area. Surveys are distributed annually for office, warehouse, retail and investment properties. We gathered facts and figures on over 1,600 properties; our most comprehensive survey to date. We then applied our own analysis to the data to more accurately determine the area’s activity and better predict future trends.

Data is an essential component of any facilities or investment decision. At NAI Iowa Realty Commercial, we believe that a comprehensive analysis is an important aspect of advising our clients so they are able to make wise, profitable choices.

Unfortunately, as our office was flooded June 12, 2008, we were unable to save our survey results and publish our trends magazine for the year. The report this year is a great testimony to the strength and cooperation of our area landlords and commercial property owners that took time to help us rebuild and update our data. This report is up to date through mid-year of 2009 and reflects the market impacts of the floods and the economy. Thank you for your review of this report and/or your contribution. Should you have any questions or comments, please contact me at 319-378-6781 or [email protected]

Thank you, Kirk Hiland Managing Broker, NAI Iowa Realty Commercial

Tenth Annual Commercial Real Estate Report

The information contained in this report is believed to be reliable, but not guaranteed. Reproduction of this publication, in whole or in part, is prohibited without permission of NAI Iowa Realty Commercial.

Peggy Slaughter Fred Miehe, CCIM Matt MieheTom DaltonRandy Miller

Cedar Rapids

Todd Barker, MBAAaron Saylor Josh Seamans Jeremy TiptonJoanne Stevens, CCIM

Bob Holland, CCIM, SIORScott Byers, CCIM,

SIORKirk Hiland Dave Drown, CCIM, SIOR Jim Lamb Adam GibbsVan Miller

NAI Iowa Realty Commercial Agents

Iowa City / Coralville Cedar Falls / Waterloo

Rod Eiklenborg

3

NAI Iowa Realty Commercial

Our team features specialists in nearly every aspect of commercial real estate, and we hold individual accreditations with CCIM, SIOR, MCR, ALC and GRI. Our affiliation with NAI gives us access to markets across the world. With over 3,700 brokers in 270 offices worldwide, we have vast resources at our fingertips; a global perspective combined with local expertise.

We are Iowa’s largest and most experienced commercial real estate company. Recently, we were cited as the 46th highest volume producing commercial real estate company in the Midwest, and the only firm in the state that made the list. From local investor to corporate America, we have the market information, contacts, experience and insight to meet diverse needs.

NAI Iowa Realty Commercial has office locations throughout the state of Iowa (Cedar Rapids, Waterloo, Iowa City and Des Moines). Widely acknowledged as the leader in Iowa

commercial real estate, our branches are able to service Cedar Rapids, Marion, Hiawatha, Waterloo/Cedar Falls, Iowa City/Coralville, North Liberty, Muscatine, Dubuque, the Quad Cities and all surrounding communities. In conjunction with a sister office in West Des Moines, we also provide extensive coverage in central Iowa.

Locally, our associates have over 350 combined years of experience in:

• Site Selection

• Buyer, Seller, Landlord and Tenant Representation

• Land Development: Retail Centers, Industrial/Warehouse and Office Property

• Project Management

• Property and Lease Management

• Mergers, Acquisitions and Divestitures

• Business Brokerage

Investment

Where We Are

Despite an unprecedented national economic debacle and the fourth largest natural disaster to ever hit the United States, the Eastern Iowa investment market has remained strong and steady. Area real estate investments have never been looked on as glamorous in comparison to the Sun Belt and coasts. But, while the bubble blew apart in these areas, our properties have not only maintained their values but shown their typical steady growth.

Eastern Iowa is fortunate to have strong locally owned and controlled financial institutions which buttress the major lenders that have a strong and increasing presence in our market. The majority of our investment opportunities are in the Ten Million Dollar and under range and this niche fits well with local lenders with knowledge of the real property and in many cases the investors.

Up until mid-2008, area real estate investment was experiencing a strong influx of investors from the coasts, many of them Tenants in Common (TIC) purchasers and similar syndications. These investors have now dried up with the loss of their equity positions, properties and financing structures (Collateralized Mortgage Backed Securities, Interest Only, etc.) and are probably out of our picture for the time being. However, the projects they invested in have maintained their values and continue to be good, viable commercial investments. We anticipate in the next few years that we will have some of these properties available again, not through any fault of the properties themselves, but rather because of borrower’s deficiencies in other markets.

NAI Iowa Realty Commercial is uniquely positioned to handle these through our affiliation with NAI which is now on a national and international basis assisting several major lenders in disposition of REO properties and the fact that we handled many of these major transactions initially.

Where We’re Going

The big plus to investment real estate these days is that interest rates are remaining in the same low range. With rates ranging between 5½ and 6½ percent interest, real estate investment still makes good sense for a long term hold.

Underwriting has tightened in that:

• Down payments have edged up to the 25-30 range

• Non-recourse loans have gone the way of the Carrier Pigeon

• Appraisals are receiving increased scrutiny and

• Capitalization rate expectancies have moved up

In today’s market, even national, Class A tenants are receiving scrutiny and an increase in capitalization basis points that were unheard of previously. The low cap sales dependent to a great extent on hopes of value increase are dying away.

Our area investment market today has strength, stability and growth. Inventories of properties for sale are limited because we have not experienced the national downturn in our area real estate market and many of the investor/owners recognize a good position when they see one. Owners and investors have to recognize that we are in a new economy with different lending rules, different expectations of and from tenants, and unfortunately, ever-increasing government control of lending, ownership and use.

Reminders:

Owner/investors, in order to maintain and grow their commercial real estate position, must:

• Be proactive on property taxes

• Be prepared to refinance into longer term fixed money should they sense an upturn in inflation

• Recognize the ramifications of changes in capital gains taxes that may (probably will) take place

• Be available and responsive to tenants to maintain occupancy

4

Central Business District

The Flood. Those two words changed the complexion of the Central Business District forever. Complete destruction and devastation of all first floor, basement and in some cases second floor areas. Both sides of the river, hundreds of thousands of square feet to rebuild, replace and/or remove.

What stage is the Central Business District at and where is it headed?

Our survey showed that well over 90 percent of the office building owners either were or planned on returning their buildings to their previous use. The majority of tenants previously officed in downtown have returned to the downtown especially those on the floors that weren’t flood impacted. First floor office space has been slower to return as rebuild has taken longer in these spaces. New tenants will most likely be the users of these first floor spaces, i.e. a Health and Fitness Center will tenant much of the first floor of the Higley Building.

The question of heating has been a stumbling block as the “City” steam system formerly provided by Alliant Utilities is phased out. Building owners are looking to private gas or electric boiler systems for their needs and with this will come an increase in expense to cover the increased cost of these systems. Landlords and tenants will have a major negotiation point in leases as for the most part the former system was very inexpensive and usually billed out as part of the base rent. This will lead to rents effectively increasing and brings suburban rents into competition with the CBD whereas before they were higher across the board for all classes of office space. Another factor in play is the parking expense and tenants are looking closely at that versus the free parking in the suburban market.

Government, long the major player in the downtown CBD is, with one exception, taking an extensive look at rebuilding and moving back to existing space.

The exception to this is the Federal Government with its new Courthouse and Federal Office facility. Long in the planning, the inundation of the existing antiquated facility along First St. SE, advanced the funding process on the new $140 million plus facility now under construction along Eighth Avenue SE.

City government is still in the planning process as to whether they will relocate or return to the island. Likewise the planned intermodal facility is looking for a site as well as the Library, the Central Fire Station and several other City Departments. The commitment to the downtown is strong and these facilities as they develop will add a new look and resurgence to the Central Business District.

Suburban Office

As CBD office tenants fled their flood ravaged buildings, the suburban market experienced a vacancy rate next to nothing. To the credit of suburban Landlords, prices were fair and leases were designed to fit the tenant need and plans for the future. As offices return to the CBD and things settle, our survey shows that the average vacancy rate across the board for all classes of space seems to have stabilized at 10%. Certainly better than major metropolitan areas throughout the United States and much better than former Iowa hot spots such as West

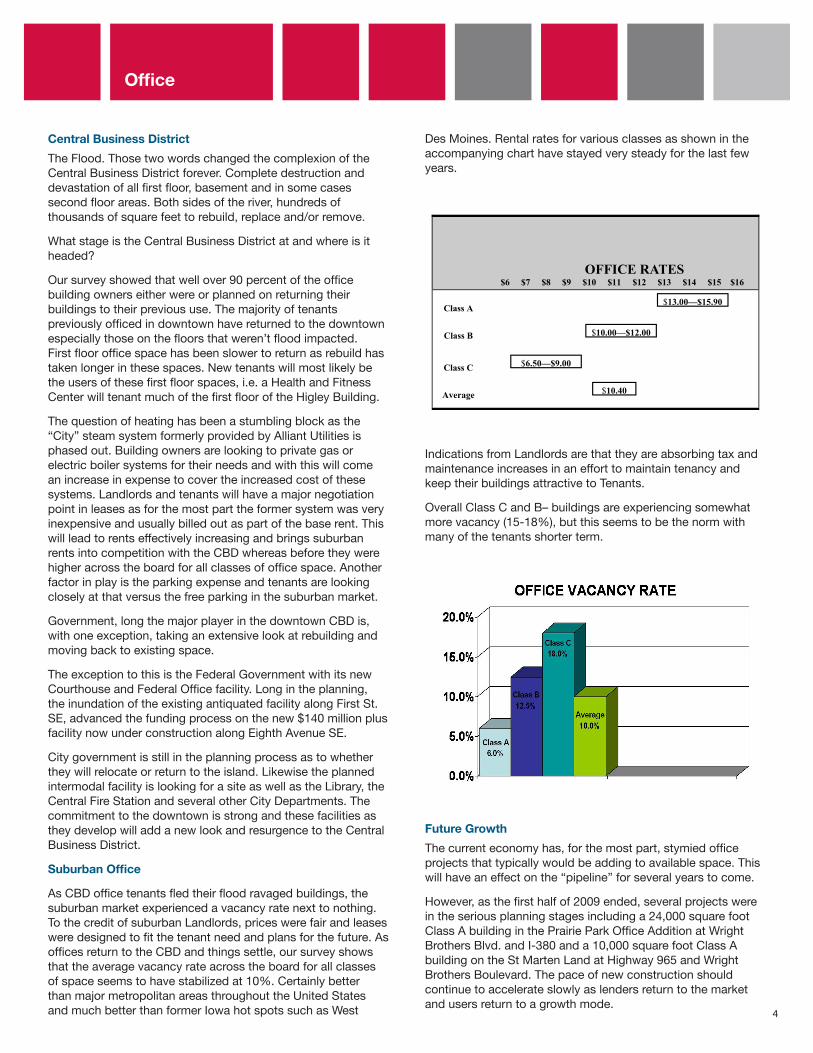

Des Moines. Rental rates for various classes as shown in the accompanying chart have stayed very steady for the last few years.

Suburban Office

As CBD office tenants fled their flood ravaged buildings, the suburban market experienced a vacancy rate next to nothing. To the credit of suburban Landlords, prices were fair and leases were designed to fit the tenant need and plans for the future. As offices return to the CBD and things settle, our survey shows that the average vacancy rate across the board for all classes of space seems to have stabilized at 10%. Certainly better than major metropolitan areas throughout the United States and much better than former Iowa hot spots such as West Des Moines. Rental rates for various classes as shown in the accompanying chart have stayed very steady for the last few years.

Indications from Landlords are that they are absorbing tax and maintenance increases in an effort to maintain tenancy and keep their buildings attractive to Tenants.

OFFICE RATES $6 $7 $8 $9 $10 $11 $12 $13 $14 $15 $16

Class A

Class B

Class C

Average

$13.00—$15.90

$10.00—$12.00

$6.50—$9.00

$10.40

Indications from Landlords are that they are absorbing tax and maintenance increases in an effort to maintain tenancy and keep their buildings attractive to Tenants.

Overall Class C and B– buildings are experiencing somewhat more vacancy (15-18%), but this seems to be the norm with many of the tenants shorter term.

Future Growth

The current economy has, for the most part, stymied office projects that typically would be adding to available space. This will have an effect on the “pipeline” for several years to come.

However, as the first half of 2009 ended, several projects were in the serious planning stages including a 24,000 square foot Class A building in the Prairie Park Office Addition at Wright Brothers Blvd. and I-380 and a 10,000 square foot Class A building on the St Marten Land at Highway 965 and Wright Brothers Boulevard. The pace of new construction should continue to accelerate slowly as lenders return to the market and users return to a growth mode.

Office

5

Retail Recap

As the National economy plunged, Retail in the corridor remained strong and viable. Major news was the bankruptcy of General Growth, long a player in the corridor area and the current owner of Coral Ridge Mall in Coralville. While this shocked major players and markets around the country, it was business as usual at Coral Ridge with very high occupancy and sales.

Elsewhere in Coralville at Holiday Road and Highway 965, Gordman’s; Michaels; Petco and Bed, Bath and Beyond anchor a power strip that has but a few pad sites left.

In Iowa City, Sycamore Mall which sold to California investors in late 2008 continues to experience high occupancy and shows a good example of a successful turnaround situation.

Cedar Rapids has leaned down its retailing which has actually helped occupancies and market areas.

Westdale Mall, in foreclosure prior to the Floods of 2008, was given a short breath of life when County and City offices moved to the property on an emergency basis. Apparently, as time goes on these government offices will move out and the mall will once again be an albatross waiting for an investor/developer to take it from the lender and do a redevelopment. Citizens will debate for years why the county and city did not look seriously at purchasing and rebuilding this into a government facility.

Nevertheless, the mall still anchored by Younkers and JC Penney remains available with no new prospects in site. One bright spot is the purchase of the former “Big Lots” building and adjoining land at the Northeast corner of the Mall property. Developers are said to have several prospects for restaurants and retail on the site after razing the existing buildings. This might be the start of something good for the area.

Across town retail has remained strong with Lindale Mall being the longtime anchor. Flanking Lindale, Market Place on First is full and growing with the addition of Ginsberg Jewelers on an outlying pad site. Lindale Crossings at First Ave. and Collins Rd. has experienced some minor vacancy with a few small spaces being vacated by local retailers. Collins Road Square recently purchased by a group of Texas investors is filling space with about 27,000 square feet left to go. Northland Square is full, but will be looking to backfill the Barnes and Noble Bookstore space as they transition to Lindale Mall. The former K’s Merchandise, a 100,000+ square foot big box has now undergone a change in use and is leased to Rockwell Collins.

The old standby of Cedar Rapids, Town and Country Shopping Center, the first center of its’ kind built in the United States currently has about a 96 % occupancy.

Retail

6

Industrial & Warehouse

The demand for warehousing increased considerably in the period after the floods of 2008. A combination of business and Government backfilled most of the dry space that was either for lease or for sale.

Warehouse rates have remained relatively stagnant for the past several years as new demand was met by build-to-suit developers and many landlords have held the line on rents as property taxes have driven up the triple net costs for tenants. The major warehousing for the Cedar Rapids Metro area resides on the southwest side of Cedar Rapids (see chart) and these warehouses have held rents fairly steady in a range from $4.00 to $4.65 per square foot for several years. Vacancy in this area runs about 5.30 %, the lowest in Cedar Rapids and second only to Marion, which has a very tight market at about 2.3% vacancy (see chart).

Metro area warehousing has had little new construction and the only major building currently under construction is 110,000 square feet on Mann Road SW. 248,000 square feet on 20th Ave. SW remains on the market after the former tenants vacated. These comprise the two largest boxes left on the Southwest side, without current occupants. Additional space may become open

as two buildings along Highway 30 currently housing Cooper Tire, may become available.

Coralville has 410,000 square feet of warehouse at I-80 and Commerce Drive that has been available as Proctor and Gamble have transitioned into their own warehouse facilities.

Despite a few large boxes, corridor warehousing has remained strong. Pro-active Landlords have been able to keep their buildings filled and demand continues for good grade warehousing. The economy and consumer demand for locally produced goods are the factors that will come into play this year for our larger warehouse spaces. Flexibility to tenant need will be a major factor in filling space.

Our industrial market has taken some major blows with the loss of Midland Forge, Terex and Cryovac. These facilities will need a major re-work and rehab to attract new industry. Most likely major redevelopment with a new use will be the end game for these properties.

Industrial & Warehouse

$6.50 $6.04

$4.65

$6.00 $5.25

$0.00$1.00$2.00$3.00$4.00$5.00$6.00$7.00

NE SE NW/SW MAR/HIA AVERAGE

WAREHOUSE RATES (Average Rent/Square Foot)

NESENW/SWMAR/HIAAVERAGE

Industrial and Warehouse

The demand for warehousing increased considerably in the period after the floods of 2008. A combina-tion of business and Government backfilled most of the dry space that was either for lease or for sale.

Warehouse rates have remained relatively stagnant for the past several years as new demand was met by build-to-suit developers and many landlords have held the line on rents as property taxes have driven up the triple net costs for tenants. The major warehousing for the Cedar Rapids Metro area resides on the southwest side of Cedar Rapids (see chart) and these warehouses have held rents fairly steady in a range from $4.00 to $4.65 per square foot for several years. Vacancy in this area runs about 5.30 %, the low-est in Cedar Rapids and second only to Marion, which has a very tight market at about 2.3% vacancy. (see chart)

Metro area warehousing has had little new construction and the only major building currently under con-struction is 110,000 square feet on Mann Road SW. 248,000 square feet on 20th Ave. SW remains on the market after the former tenants vacated. These comprise the two largest boxes left on the Southwest side, without current occupants. Additional space may become open as two buildings along Highway 30 currently housing Cooper Tire, may become available.

Coralville has 410,000 square feet of warehouse at I-80 and Commerce Drive that has been available as Proctor and Gamble have transitioned into their own warehouse facilities.

Despite a few large boxes, corridor warehousing has remained strong. Pro-active Landlords have been able to keep their buildings filled and demand continues for good grade warehousing. The economy and consumer demand for locally produced goods are the factors that will come into play this year for our larger warehouse spaces. Flexibility to tenant need will be a major factor in filling space .

Our industrial market has taken some major blows with the loss of Midland Forge, Terex and Cryovac. These facilities will need a major re-work and rehab to attract new industry. Most likely major redevel-opment with a new use will be the end game for these properties.

13.60%

10.22%

5.20%

2.00%

7.80%

0.00%2.00%4.00%6.00%8.00%

10.00%12.00%14.00%

NE SE NW/SW MAR/HIA OVERALL

VACANCY

NESENW/SWMAR/HIAOVERALL

7

Cedar Falls Waterloo

The Cedar Valley market continues to grow with strong, steady, sustained growth. The market is absorbing office and industrial vacancies.

• Fortune 500 company Grainger Inc., has moved into its new 41,000 sq. ft. call center at Country Club Business Center in Waterloo. The new site allows for expansion in the future. The construction project has a valuation of $5.2 million.

• VGM spinoff plans to utilize a historic downtown Waterloo building that once housed one of the city’s oldest businesses. Healthcare Quality Association of Accreditation, or HQAA is a spin-off of the VGM Group, specializing in accreditation in the home medical equipment industry.

• Target Distribution completed a 400,000 sq. ft. refrigeration distribution facility expanding on its 1.4 million sq. ft. facility in the Cedar Falls Industrial Park. It is a $35 million project totaling $80-$90 million including equipment with at least 100 new employees.

• Isle of Capri completed a $175 million casino in Waterloo for a June 1, 2008 opening. At ground breaking it was a $70 million project. Isle of Capri has significantly improved the amenities and design making it a $175 million project.

• New construction in the commercial/office/industrial section continues. Waterloo and Cedar Falls have seen numerous new and expanded professional office buildings and industrial facilities.

• The Cedar Valley’s medical community is worth noting with Allen Memorial Hospital’s planned expansion, its most expensive in history. They will invest $47M in a Cardiac Care and Emergency Room.

Population (2008)

Waterloo 66,662 Cedar Falls 38,059 Evansdale 5,056

Total 109,777

Unemployment Rate (June 2009)

Waterloo / Cedar Falls 4.7%

Commercial Property Rates*

Rent/SF Year Vacancy Property Low High Rate

Downtown Office (Prime) $6.25 $11.00 9.0%

Suburban Office (Prime) $8.00 $13.25 5.0%

Industrial Bulk Warehouse $3.00 $5.25 2.0%

Retail $7.00 $20.00 12.5%

*Rental rates include estimated taxes, insurance and maintenances.

NAI Global is one of the world’s leading providers of commercial real estate services. We bring together people and resources wherever needed to deliver outstanding results for our clients.

NAI At A Glance

350 Offices 45 Countries 5,000 Professionals $40 Billion Annual Transaction Volume

About NAI Global

Cedar Valley At A Glance

116 Third Street SECedar Rapids, Iowa 52401tel 319-363-2337fax 319-365-9833

220 Ridgeway Ave., Suite 100Waterloo, Iowa 50701tel 319-233-9999fax 319-291-7130

327 Second Street, Suite 201Coralville, Iowa 52241tel 319-354-0989fax 319-887-6565

www.iowacommercial.com

Individual Memberships