real estate and capital markets - rdhawan.com · trends in real estate capital markets ... equity...

TRANSCRIPT

Real Estate Forecasting Seminar February 21, 2007

Terry V. Grissom Ph.D.Professor Real Estate Department

Georgia State University Economic Forecast Center

& Person who sets inReal Estate Research Center

Real Estate and Capital Markets

Trends in Real Estate Capital MarketsSession Objectives:Participants will:• view relations of real estate & capital• Note changes in structure of real estate capital

market• Identify the effect of changing relationships on

risk and return options• Have option to consider strategies using our

insights• Develop an alternative way of thinking

Nature of Real Estate and CapitalAlternative Economic Tradition shows:

Real Estate ≡ Capital&

Real Estate ≠ Capital

A partial function of difference in:Risk ≠ Uncertainty

& Consideration of distributive factors

Structural Nature of Real Estate

Real Estate is alternatively categorized and perceived as:

• A Commodity• A factor of production • A Resource• An Asset Class

Operational Nature of Real Estate

Operational Essence of Real Estate

• Economic Location: SitusUse Succession (LUST)

• Collateral

Agricultural and Direct return to Physical Land

Income Allocated to Location and Accessibility

TransportationCosts

Site Rent

Basis of Real Estate Value: Basic Bid Rent Curve Model – defining Land Use Patterns by Trade-off

Location and Accessibility

Economic Edge of City0 Distance from City Core - CBD

Shift in Bid Rent Curve –due increase fuel cost

Agricultural and Direct return to Physical Land

Economic Edge of City

Income Allocated to Location and Accessibility

TransportationCosts

Site Rent

Impact of fuel costs: Demand Increase where Price Exceeds Income

Demand Increase at high price within income range

Site Rent

Quantity Loss due to Demand decline for undesirable/unavailable land

Demand decline and shift in trade-off of rent ( ) to transport cost

0 D

Basis of Real Estate Value: Basic Bid Rent Curve: Patterns of Trade-off of Site Rent and

Accessibility Vary with Land Use

TransportationCosts

Economic Edge of City

Income Allocated to Location and Accessibility

Office

Retail

Industrial

Residential

Agricultural and Direct return to Physical Land

Site Rent

0 D

TransportationCosts

Income Allocated to Location and Accessibility

Office

Industrial

Linking Economic Location to Capital : A Spatial Capital as Product

Real Estate as:• Space used over time• Situs Capital – Economic Location • Sustainable development –natural capital• Space and money as Capital• Real Estate as Capital Markets within

Spatial Markets• How to pull it all together and get there

Valuation: Cost Analysis and Asset FeasibilityRisk Measure from origins of a project at a location:

PotentialCost Market Revenue

[ Financing Options] [Operating Options][Operating Options] [ Financing Options]

Required Justified Investment Revenue Value

RR (JIV)

JIV-Cost & Rent SensitivityValue/CostPer SF GBA$200.00

$135.09

$123.30

$100.00

0 $ 10 $20 $30$18.27$12.43$13.00

RentNOI PGI

Income Productivity Range

Ro | JIV

Rc | Vc

η

JIV-Cost Comparison As Measure of RiskAlternative Risk Adjustment: • Value:

A. JIV/Cost = Profitability Index (PI):PI >1 go, PI =1, neutral, PI<1, no go

B. Probability of Ruin (δ = PI -1) • Income Elasticity:

(JIV/Cost -1)/(Mkt Rent/Required Rent-1)

• Rate/Return/Yield – Equity Shortfall Risk (ESR) or Roy’s Criterion (a hurdle rate);

JIV-Cost Comparison As Measure of RiskRoy’s Criterion (ESR):

E(Ri) - ϕ = ESR (π E(Ri) ≤ ϕ)σRi

Where: E(Ri) = expect return on asset (average)σRi = total risk to asset (market measures

can be used)ϕ = investor’s hurdle rate (required rate

of return)π = probabilityESR = equity shortfall rate

Functional Nature of Real Estate

Functional Essence of Real Estate:

Conversion of:

Space-time <====> Money-time

Repeat of Overview Essentials from Repeat of Overview Essentials from Underwriting and Risk PerspectivesUnderwriting and Risk Perspectives

The general principles of real estate finance, underwriting, investment and portfolio analysis are simplified as:

• Pain• Pleasure• Bail-out

Real Estate FinanceAs in general finance, the nature of real estate finance has evolved and changed over time.

Key changes have been in:• Nature of institutions and intermediaries• Participants and sources of capital• Real estate investment vehicles• Relationships to inflation and interest

contingencies• Change in risk exposures

Traditional Capital Market for Real Estate

Source Instrument Capital Intermediary

Savers

Investors

Pass Book

Life Policy

Banks

Thrifts

Insurance Co.

Positions of: Limited Exposures

Private Syndications

Lawyers

Accountants

Professional Intermediaries

Traditional Capital Market for Real Estate

Investment Intermediaries Capital Vehicle

Mortgage Brokers/Bankers Mortgages

Developers

BrokersEquities

Evolving Capital Market for Real EstateSource Instrument Capital Intermediary

Insurance Co.

ThriftsS-term Savers

Pass Book

Money Markets

CDs

Banks

Mortgage Conduits …

L-term Savers

Investors

Life Policy

Pension Funds

IRA/Keogh

Positions of: Limited Exposures

Employers

Public/Private SecuritiesPublic/Private Trusts ….

Equity Conduits .

Evolving Capital Market for Real Estate

Investment Intermediaries Capital Vehicle

Mortgages

…… Mortgage Conduits

Mortgage Brokers/Bankers

….. Public/Private Securities

….. Public/Private Trusts

…... Equity Conduits Equities

Blended Debt and Equity Vehicle

0

200

400

600

800

1000

1200

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98

Comparison of Debt and Equity Capital$B illions

Ye ars

D e bt

Equity

Sourc e : GSU R e al Estate ; Grissom

0

10

20

30

40

50

60

86 88 90 92 94 96 98 00 02 04 06

Life Co

Banks

Foriegn Inves tors

S&Ls

Traditional Equity Capital$ Billions

0

20

40

60

80

100

120

86 88 90 92 94 96 98 00 02 04 06

Pension Funds

EREITs

Emerging Equity Capital$ Billion

0

50

100

150

200

250

300

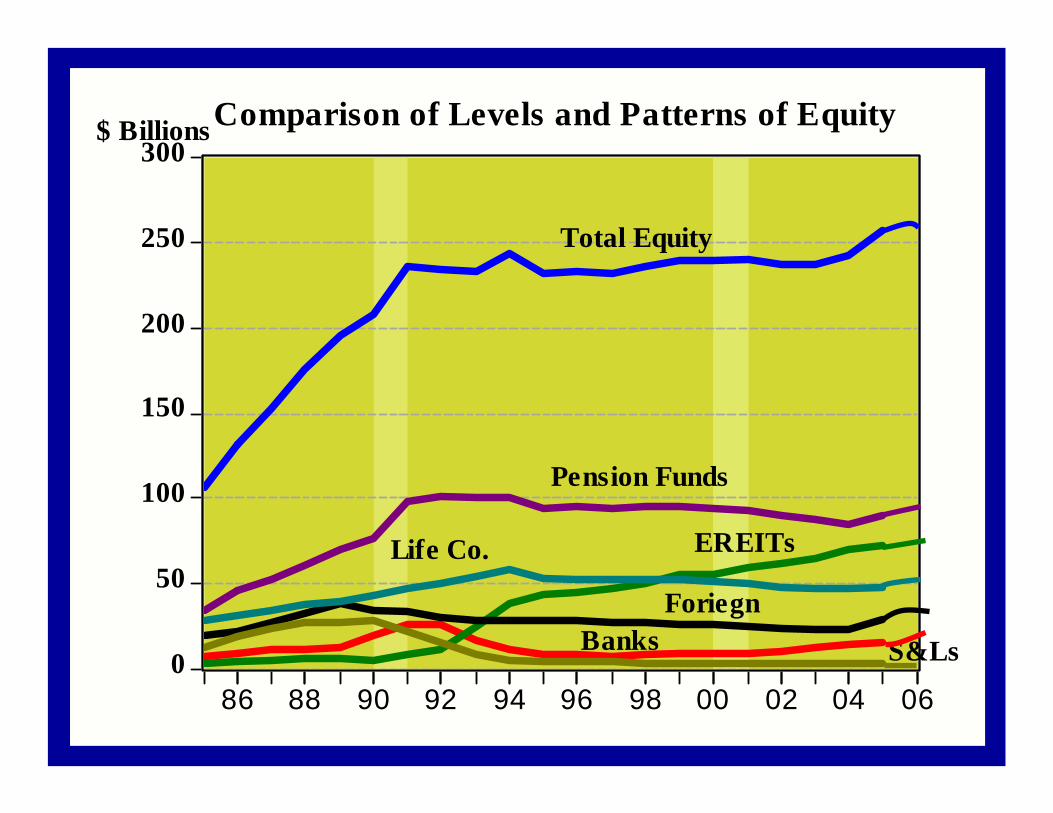

86 88 90 92 94 96 98 00 02 04 06

Total Equity

Pension Funds

Banks

EREITsLife Co.

Foriegn

S&Ls

Comparison of Levels and Patterns of Equity$ Billions

Equity Pie: 1995-6

Foreign Investors: 12.29%

REITs: 18.76%

Thrifts: 1.75% Banks: 3.42%

Life Co.: 23.21%

Pensions:40.56%

Equity Pie: 2005-6

Series1

Series1

Series1

Series1Series1

Series1

Thrifts: 1.08% Banks: 6.02%

REITs: 27.98%

Foreign Investors: 11.27%Life Co.: 18.66%

Pensions:34.98%

Banks: 6.02%

Pensions:34.98%

0

20

40

60

80

100

120

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98

Securitized Debt Capital Sources$Billions

MREITs

CMBSs

YearsSource: GSU Real Estate; Grissom

Interest RateInterest Rate Determinates: Classes of InflationDeterminates: Classes of Inflation

-.08

-.04

.00

.04

.08

.12

.16

50 55 60 65 70 75 80 85 90 95 00

Anticipate d Inflation

Actual Inflation

Unanticipate d Inflation

Infla tion Influences on C ost o f C apita lR ate s

-.05

.00

.05

.10

.15

.20

50 55 60 65 70 75 80 85 90 95

T o ta l R e turns a nd R e g im e s G N P , Inte re s t a nd T a x S pline T re ndsR e turns /R ate s

Ye ars

G N PG N P

Inte re s t

G N P

Inte re s t

Tax

Inte re s t

S ource : G S U, G ris s om & D e Lis leThis e xhibit s hows the s e gme nt e d s pline s or tre nd in thek e y caus al variable s impacting re al e s tate re turns ove r time .

R e al Es tateR e turns

-.04

.00

.04

.08

.12

.16

.20

50 55 60 65 70 75 80 85 90 95 00 05

Total Return Cycles and Long-term TrendTotal Return

Years

Total Return Series

Long-termTrend

57 Year Trend/CycleSource: Grissom, GSU:Data Sources: Ibbotson Associates and NCREIF data

-.04

.00

.04

.08

.12

.16

.20

50 55 60 65 70 75 80 85 90 95 00 05

Event and Return HistoryReturns

Years

KoreanWar

Creeping Inflation

KeynesianPolicy

Oil Crisis

Vietnam War

Oil Cris is

RepealBretton Woods

Disinter-mediation

Stagflation

M onetaryPolicy Supply-side

Reagonomics

Deregulation M CA

1981 TaxAct 1986 Tax

Act

Oil Concerns Oil Concerns

Gulf War

1993 TaxAct

Neo-Keynes ian

CommunistDevolution

1997 Tax Act

9-11 Event

ERISAFIRREA

TechnologyB ubble

Bust

CEO-SOBs

Comp. Conservatives

Source: Grissom, GSU

1991 FDICImprovement Act

General Real Estate Trends: Multiple Indices

- .0 8

- .0 4

.0 0

.0 4

.0 8

.1 2

.1 6

.2 0

8 6 8 8 9 0 9 2 9 4 9 6 9 8 0 0 0 2 0 4

I& A /N C R E IF

I& AN C R E IF

N C R E IF N C R E IF

I& AA C L I

A C L IN C R E IF

N R E I

N R E I

A C L IN C R E IF

N R E I

K YI

K YI

R E R C

A C L I

R E R C

C om p a r ison of A ltern a tive R etu rn s S er ie s :C on ver ted to In d ices

Tot

al R

etur

ns

Y ea r sS ou rce: G risso m G SU R ea l E tate C enter

Changes in Real Estate As Function of Capital Evolution

The changes:• More players: Increase flow of K to RE• Varying source of K• Increase instruments: Blended• Direct Real Estate: debt and equity• Indirect Real Estate: debt and equity

(securities or other derivatives)K = capital, RE = Real Estate

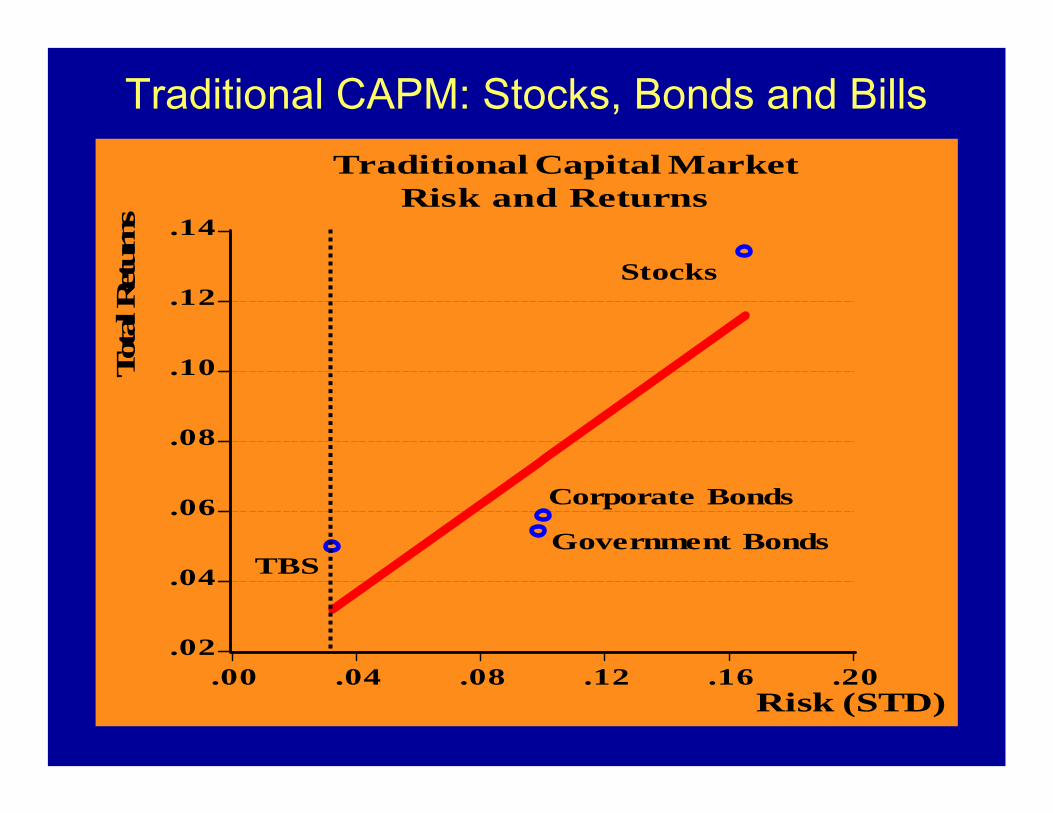

Traditional CAPM: Stocks, Bonds and Bills

.02

.04

.06

.08

.10

.12

.14

.00 .04 .08 .12 .16 .20

Traditional Capital Market Risk and Returns

TBS

Stocks

Corporate Bonds

Government Bonds

Tot

al R

etur

ns

Risk (STD)

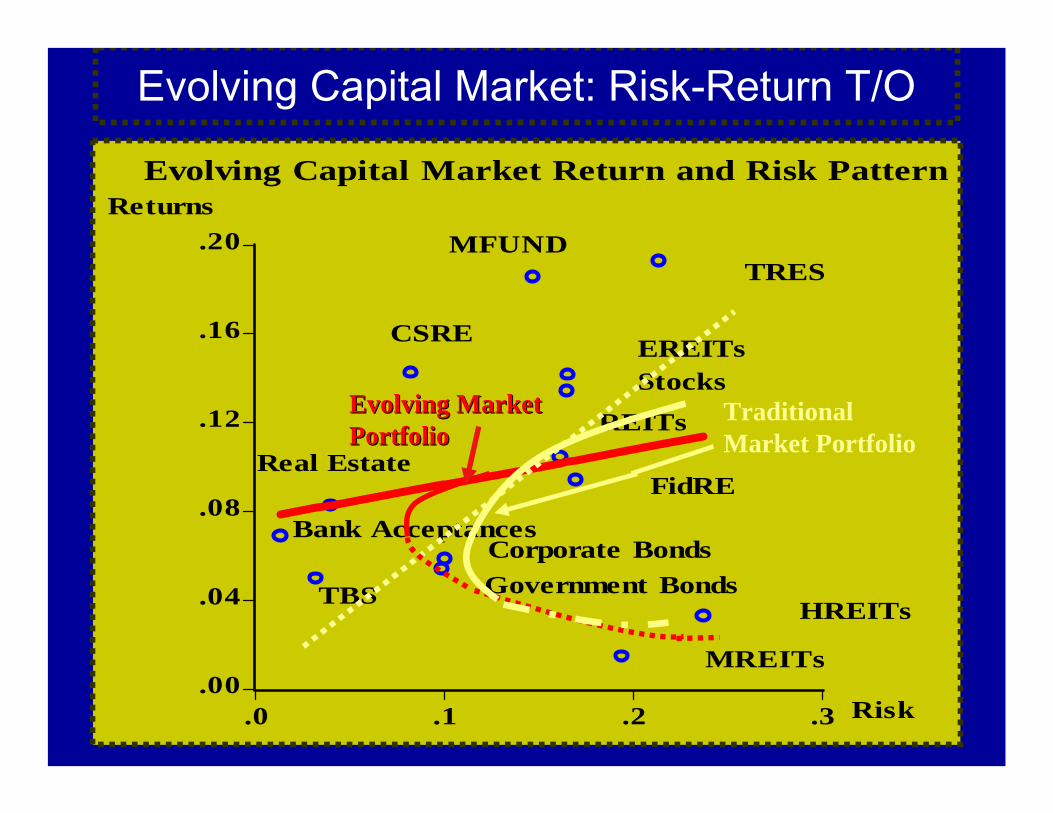

Evolving Capital Market: Risk-Return T/O

.00

.04

.08

.12

.16

.20

.0 .1 .2 .3

Evolving Capital Market Return and Risk Pattern

TBS

Bank AcceptancesCorporate BondsGovernment Bonds

MREITs

HREITs

Returns

Risk

Real EstateFidRE

EREITsStocks

REITs

CSRE

MFUNDTRES

Four Quadrant Strategy Private Public

Direct Eqty in Operating Cos. Commingled Funds Equity REITs

Equity Participating Interests Real Estate Securities Private Syndications Public Syndications Limited Partnerships RE Mutual Funds Co-investment Derivatives Development Development

Development Development Mortgages Mtg REITs Mortgage Pools Hybrid REITs

Debt Synthetic Leases Senior/Junior Positions Commingled Funds CMOs Participating Mtg Synthetic Leases Co-investment CMBSs

Enhanced Core Opportunistic -- Pools of partially defaulted loans, large broken deals, etc.

New Development

Core Agriculture

Fully Leased in the (concentration investment size Timber between $10-25 million) Office Retail Hotels, Healthcare, Industrial Mobile Home Parks Apartment

Modest Value Added - Traditional core properties with lease or rehab "challenges"

Equity in Private Real Estate Companies

Below - investment- grade CMBS

Equity in public real estate companies

Enhanced Core

The End!

Appendix

Extension of Real Estate, Direct and Indirect to International Asset Classes

International Real Estate Securities

The European Public Real Estate Association (EPRA):

• offers a global data base of securitized national market portfolios

• Data base allows the development of market models for both property and equity

• A characteristic line can also be developed per national portfolios

International Real Estate Securities

The EPRA data is a foundation for a market model per national asset/portfolio measures:•Market Model

E(Ri) = αi + βiM( RM) ± εi

• The beta parameter βiM reflects the sensitivity of the asset to market volatility

• αi reflects the return component not associatedwith the market

International Real Estate SecuritiesMarket Model enables a characteristic line for each asset/portfolio:

E(Ri) = βiM( RM) (+) αi + εi

Systematic Unsystematic

.0

.1

.2

.3

.4

.5

.6

.7

2 4 6 8 10 12 14 16 18 20 22 24

Diverification Impacts

Standard Deviationper Portfolio

Systematic Risk Portfolio Rankby Numberof Securities

Theoretical RiskTrend with Diversified Portfolios

.0

.1

.2

.3

.4

.5

.6

.7

2 4 6 8 10 12 14 16 18 20 22 24 26

Real Estate Securities Risk as f(n)

Equity Securities Risk as f(n)

Evans and Archer Naive Diversification ModelRisk

P(n)

International Real Estate Securities

EPRA

-.1

.0

.1

.2

.3

.4

.5

.6

.7

2 4 6 8 10 12 14 16 18 20 22

Real Estate Portfolio

GlobalEquity Portfolio

GlobalSystematic Risk

RiskDiversification: Asset Structure in Evan & Archer Model

P(n)

Equity Portfolio

Real Estate Systematic Risk

.0

.1

.2

.3

.4

.5

.6

2 4 6 8 10 12 14 16 18 20 22

Risky Asset Risk Spac e Ide ntity G rid

Real Estate Securities Risk:f(As set Structure)

Equitty Risk: f(Asset Structure).

Asset Secant

Risk

Ris kM agnitude

Traditional CAPM: Stocks, Bonds and Bills & R E

.04

.06

.08

.10

.12

.14

.00 .04 .08 .12 .16 .20

Traditional Capital Market Risk and ReturnTotal Returns

Stocks

Corporate Bonds

Government BondsTBS

CompositeReal Estate

AtlantaIndustrial

NationalIndustrial

Traditional CAPM: Stocks, Bonds and Bills

.02

.04

.06

.08

.10

.12

.14

.00 .04 .08 .12 .16 .20

Traditional Capital Market Risk and Returns

TBS

Stocks

Corporate Bonds

Government Bonds

Tot

al R

etur

ns

Risk (STD)

Evolving Capital Market: Risk-Return T/O

.00

.04

.08

.12

.16

.20

.0 .1 .2 .3

Evolving Capital Market Return and Risk Pattern

TBS

Bank AcceptancesCorporate BondsGovernment Bonds

MREITs

HREITs

Returns

Risk

Real EstateFidRE

EREITsStocks

REITs

CSRE

MFUNDTRES

Traditional Market Portfolio

Evolving Market Evolving Market PortfolioPortfolio

Evolving Capital Market: Risk-Return T/O

.00

.04

.08

.12

.16

.20

.0 .1 .2 .3

Evolving Capital Market Return and Risk Pattern

TBS

Bank AcceptancesCorporate BondsGovernment Bonds

MREITs

HREITs

Returns

Risk

Real EstateFidRE

EREITsStocks

REITs

CSRE

MFUNDTRES

O O

Table 4 Alternative Theories of Distribution

Traditional Contemporary Alternative Labor Labor: CAPITAL:

Entrepreneuership Real Capital: Technology Real Real

Financial Financial Capital: Land Real Entrepreneur Financial Labor Entrepreneurship Land Land

-.08

-.04

.00

.04

.08

.12

.16

.20

86 88 90 92 94 96 98 00 02 04

I&A/NCREIF

I&ANCREIF

NCREIF NCREIF

I&AACLI

ACLINCREIF

NREI

NREI

ACLINCREIF

NREI

KYI

KYI

RERC

ACLI

RERC

Comparison of Alternative Returns Series:Converted to Indices

Tota

l R

etur

ns

YearsSource: Grissom GSU Real Etate Center