2009 foster business school cost accounting l.ducharme a review of cost terms and purposes chapter 2

Post on 19-Dec-2015

216 views

TRANSCRIPT

2009 Foster Business School Cost Accounting L.DuCharme

A Review of CostTerms and Purposes

Chapter 2

22009 Foster Business School Cost Accounting L.DuCharme

Outline

• Cost terminology– Cost object– Assignment– Direct vs. Indirect– Variable vs. Fixed– Drivers– Relevant range– Average cost

32009 Foster Business School Cost Accounting L.DuCharme

Outline (continued)

• Manufacturing companies vs. others

• Inventory vs. period costs

• Flow of Costs: T-accounts

• Prime & conversion costs

• Different costs for different purposes

42009 Foster Business School Cost Accounting L.DuCharme

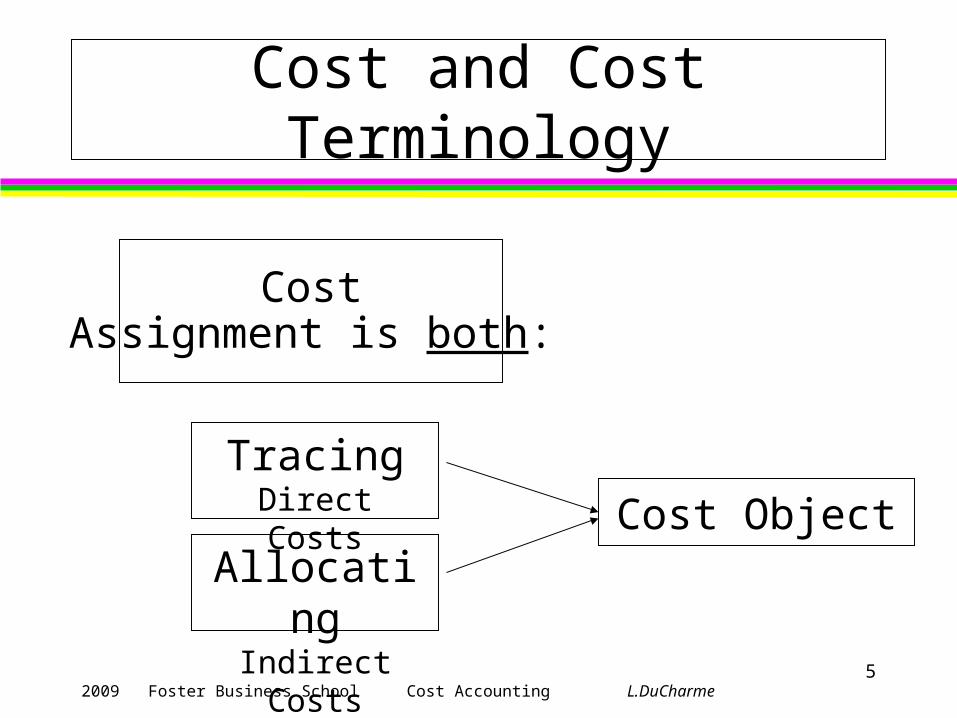

Cost and Cost Terminology

Cost is a resource sacrificed or forgone to achievea specific objective.

An actual cost is the cost incurred (a historical cost)as distinguished from budgeted costs.

A cost object is anything for which a separatemeasurement of costs is desired.

52009 Foster Business School Cost Accounting L.DuCharme

Cost and Cost Terminology

CostAssignment is both:

Cost ObjectTracing

Direct Costs

AllocatingIndirect Costs

62009 Foster Business School Cost Accounting L.DuCharme

Direct vs. Indirect costs

Distinguish between direct costsand indirect costs.

72009 Foster Business School Cost Accounting L.DuCharme

Direct and Indirect Costs

Direct CostsExample: Oak wood used to Mfg. of chairs.

Indirect CostsExample: salary of thePlant night watchperson.

COST OBJECT

Example: 50 Oak Chairs produced inMay.

82009 Foster Business School Cost Accounting L.DuCharme

Direct and Indirect CostsExample

Direct Costs:Maintenance Department $40,000Personnel Department $20,600Assembly Department $75,000Finishing Department $55,000

Assume that Maintenance Department costs areallocated equally among the production departments.

How much is allocated to each department?

92009 Foster Business School Cost Accounting L.DuCharme

Direct and Indirect Costs Example

Allocated$20,000

Maintenance$40,000

AssemblyDirect Costs

$75,000

FinishingDirect Costs

$55,000

$20,000

102009 Foster Business School Cost Accounting L.DuCharme

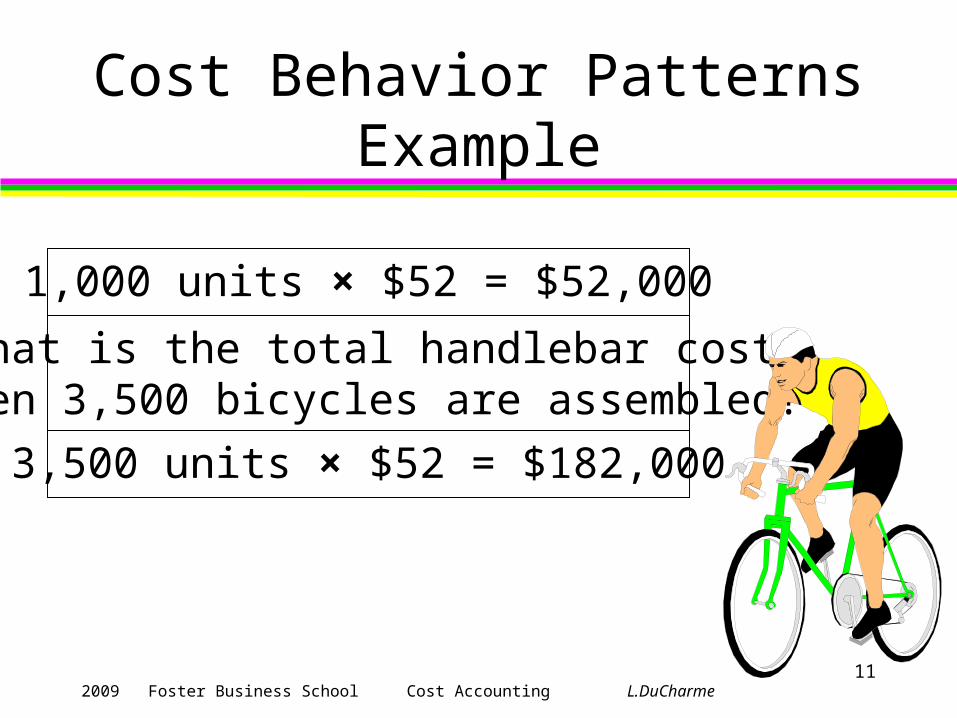

Cost Behavior Patterns Example

Bicycles by the Sea buys a handlebarat $52 for each of its bicycles.

What is the total handlebar cost when1,000 bicycles are assembled?

Variable vs. Fixed costs

112009 Foster Business School Cost Accounting L.DuCharme

Cost Behavior Patterns Example

1,000 units × $52 = $52,000

What is the total handlebar costwhen 3,500 bicycles are assembled?

3,500 units × $52 = $182,000

122009 Foster Business School Cost Accounting L.DuCharme

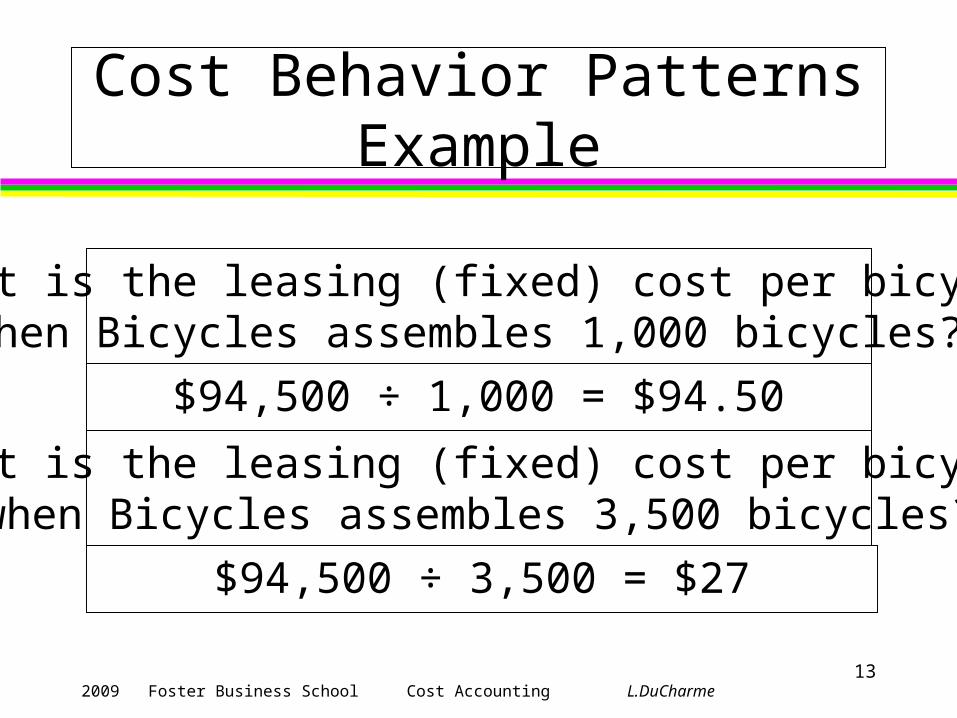

Cost Behavior Patterns Example

Bicycles by the Sea incurred $94,500 ina given year for the leasing of its plant.

This is an example of fixed costs withrespect to the number of bicycles assembled.

132009 Foster Business School Cost Accounting L.DuCharme

Cost Behavior Patterns Example

What is the leasing (fixed) cost per bicyclewhen Bicycles assembles 1,000 bicycles?

$94,500 ÷ 1,000 = $94.50

What is the leasing (fixed) cost per bicyclewhen Bicycles assembles 3,500 bicycles?

$94,500 ÷ 3,500 = $27

142009 Foster Business School Cost Accounting L.DuCharme

Cost Drivers

The cost driver of variable costs is the levelof activity or volume whose change causes

the (variable) costs to change proportionately.

The number of bicycles assembled is acost driver of the cost of handlebars.

152009 Foster Business School Cost Accounting L.DuCharme

Relevant Range Example

Assume that fixed (leasing) costs are $94,500for a year and that they remain the same for a

certain volume range (1,000 to 5,000 bicycles).

1,000 to 5,000 bicycles is the relevant range.

162009 Foster Business School Cost Accounting L.DuCharme

Relevant Range Example

020000400006000080000

100000120000

0 1000 2000 3000 4000 5000 6000

Volume

Fix

ed C

osts

$94,500

172009 Foster Business School Cost Accounting L.DuCharme

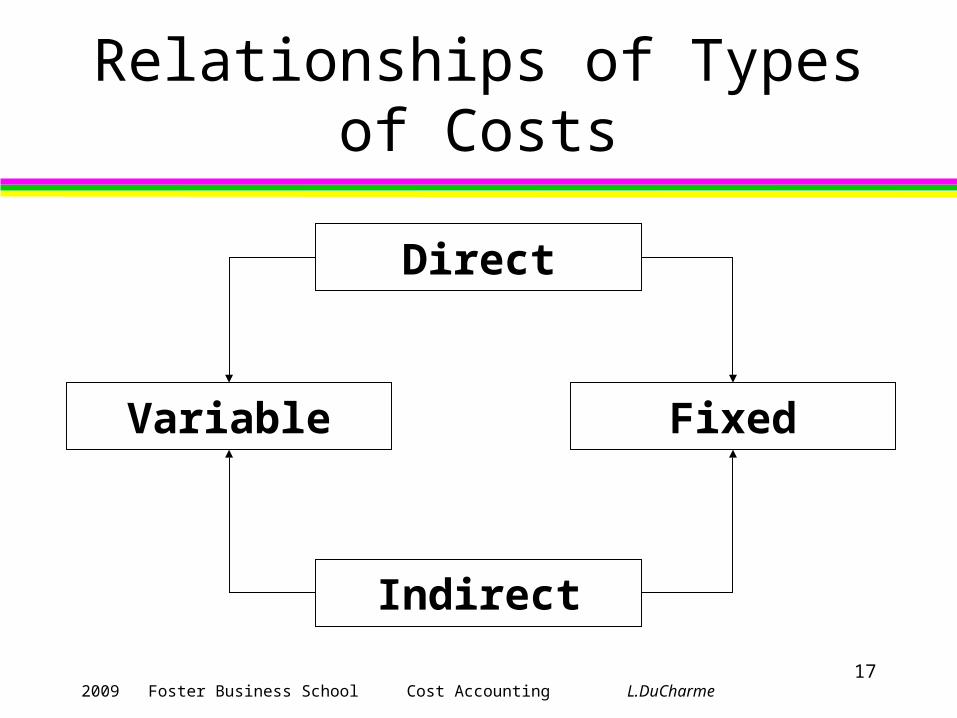

Relationships of Types of Costs

Direct

Indirect

Variable Fixed

182009 Foster Business School Cost Accounting L.DuCharme

“Average Costs”

Interpret unit costs cautiously.

192009 Foster Business School Cost Accounting L.DuCharme

Total Costs and Unit Costs Example

What is the unit cost (leasing and handlebars)when Bicycles assembles 1,000 bicycles?

Total fixed cost $94,500+ Total variable cost $52,000 = $146,500

$146,500 ÷ 1,000 = $146.50

202009 Foster Business School Cost Accounting L.DuCharme

Total Costs and Unit CostsExample

0

50000

100000

150000

200000

0 500 1000 1500

Volume

Tot

al C

osts

$94,500

$94,500 + $52x$146,500

212009 Foster Business School Cost Accounting L.DuCharme

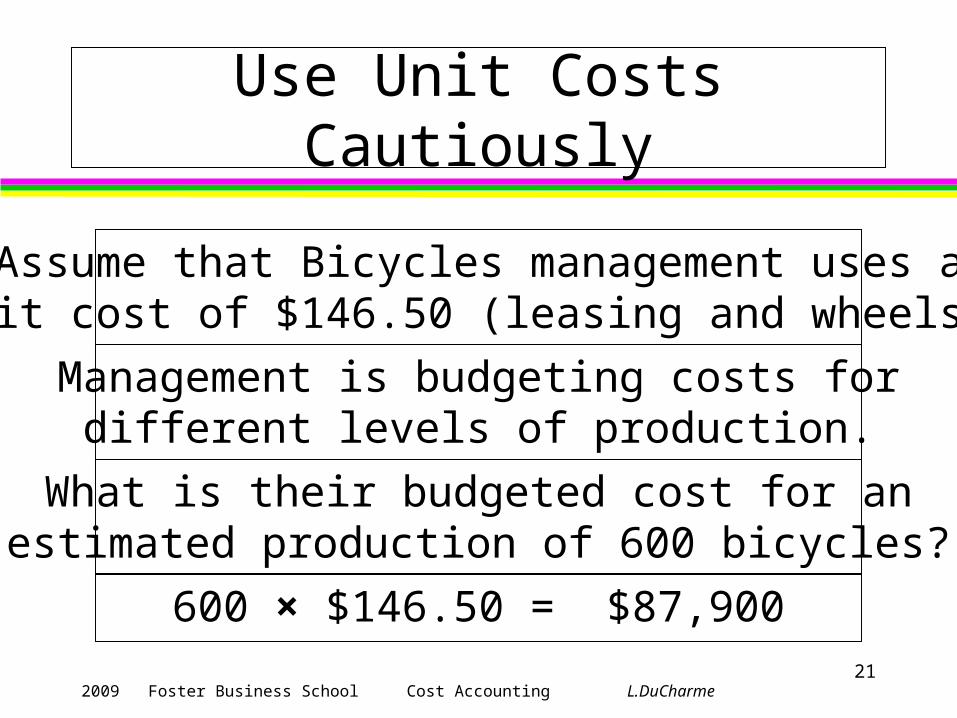

Use Unit Costs Cautiously

Assume that Bicycles management uses aunit cost of $146.50 (leasing and wheels).

Management is budgeting costs fordifferent levels of production.

What is their budgeted cost for anestimated production of 600 bicycles?

600 × $146.50 = $87,900

222009 Foster Business School Cost Accounting L.DuCharme

Use Unit Costs Cautiously

What is their budgeted cost for an estimatedproduction of 3,500 bicycles?

3,500 × $146.50 = $512,750

What should the budgeted cost be for anestimated production of 600 bicycles?

232009 Foster Business School Cost Accounting L.DuCharme

Use Unit Costs Cautiously

Total fixed cost $ 94,500Total variable cost ($52 × 600) 31,200Total $125,700

$125,700 ÷ 600 = $209.50

Using a cost of $146.50 per unit wouldunderestimate actual total costs if output

is below 1,000 units.

242009 Foster Business School Cost Accounting L.DuCharme

Use Unit Costs Cautiously

What should the budgeted cost be for anestimated production of 3,500 bicycles?

Total fixed cost $ 94,500Total variable cost (52 × 3,500) 182,000Total $276,500

$276,500 ÷ 3,500 = $79.00

252009 Foster Business School Cost Accounting L.DuCharme

Manufacturing vs. others

Distinguish among

manufacturing companies,

merchandising companies, and

service-sector companies.

262009 Foster Business School Cost Accounting L.DuCharme

Manufacturing

Manufacturing companiespurchase materials and components and

convert them into finished goods.

A manufacturing company must also develop,design, market, and distribute its products.

272009 Foster Business School Cost Accounting L.DuCharme

Merchandising

Merchandising companiespurchase and then sell tangible products

without changing their basic form.

282009 Foster Business School Cost Accounting L.DuCharme

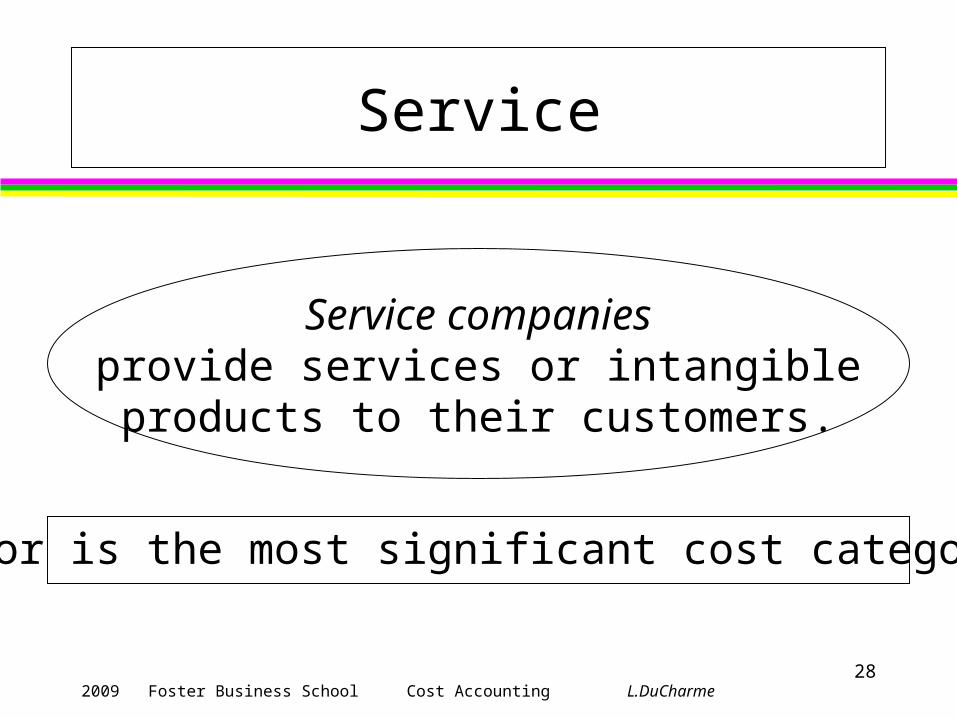

Service

Service companiesprovide services or intangibleproducts to their customers.

Labor is the most significant cost category.

292009 Foster Business School Cost Accounting L.DuCharme

Inventoriable Costs

Differentiate between

inventoriable costs

and period costs.

302009 Foster Business School Cost Accounting L.DuCharme

Types of Inventory

Manufacturing-sector companiestypically have one or more of the

following three types of inventories:

1. Direct materials inventory

2. Work in process inventory (work in progress)

3. Finished goods inventory

312009 Foster Business School Cost Accounting L.DuCharme

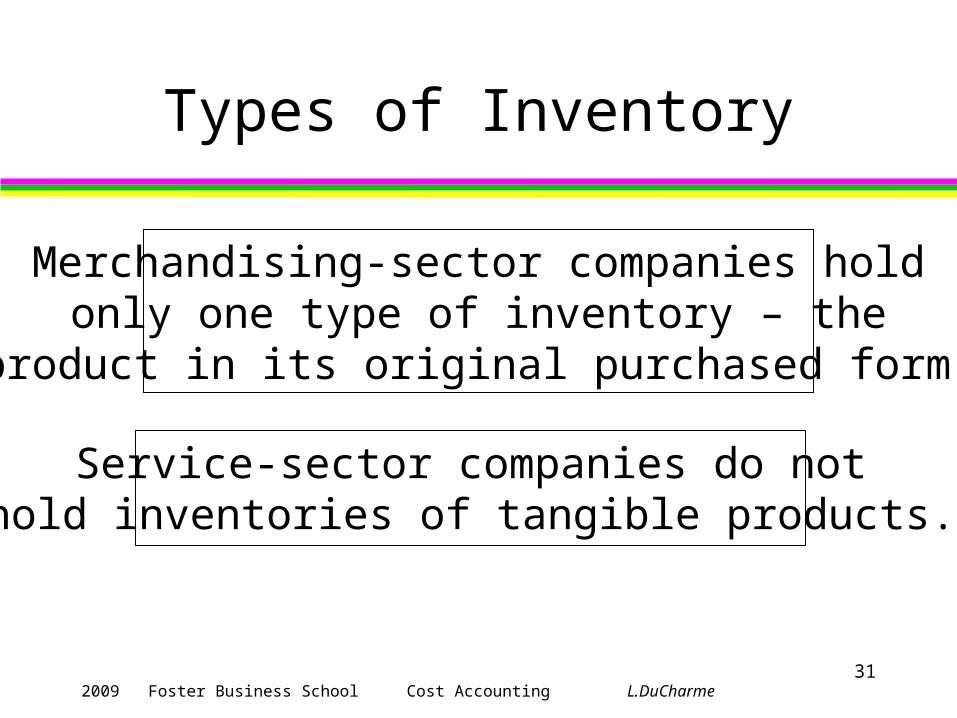

Types of Inventory

Merchandising-sector companies holdonly one type of inventory – the

product in its original purchased form.

Service-sector companies do nothold inventories of tangible products.

322009 Foster Business School Cost Accounting L.DuCharme

Classification ofManufacturing Costs

Direct materials costs

Direct manufacturing labor costs

Indirect manufacturing costs

332009 Foster Business School Cost Accounting L.DuCharme

Inventoriable Costs

Inventoriable costs (assets)…

become cost of goods sold…

after a sale takes place.

342009 Foster Business School Cost Accounting L.DuCharme

Period Costs

Period costs are all costs in the incomestatement other than cost of goods sold.

Period costs are recorded as expenses of theaccounting period in which they are incurred.

352009 Foster Business School Cost Accounting L.DuCharme

Flow of Costs

• T-account diagram (in class)

362009 Foster Business School Cost Accounting L.DuCharme

Prime Costs(all direct mfg. costs)

DirectMaterials

DirectLabor

PrimeCosts+ =

372009 Foster Business School Cost Accounting L.DuCharme

Conversion Costs(all mfg. cost except DM)

DirectLabor

ManufacturingOverhead+ =

ConversionCosts

IndirectLabor

IndirectMaterials Other

382009 Foster Business School Cost Accounting L.DuCharme

Different Costs?

Product costs are

computed in different ways

for different purposes/uses.

392009 Foster Business School Cost Accounting L.DuCharme

Many Meanings of Product Cost

A product cost is the sum of the costsassigned to a product for a specific purpose.

1. Pricing and product emphasis decisions

2. Contracting with government agencies

3. Preparing financial statements for external reporting under generally accepted accounting principles

2009 Foster Business School Cost Accounting L.DuCharme

End of Chapter 2That’s all Folks!