2011aug10 documentation - rakesh alshi - wirc-icai.org documentation - rakesh alshi...documentation...

TRANSCRIPT

Doc

umen

tatio

n

Rak

esh

G. A

lshi

Aug

ust 2

011

Agenda

Introduction

Concept and deliverables

The approach

Post-completion

Takeaways

Introduction

Documentation

–W

hy t

ake t

he T

rouble

??

•Because you have to -i.e. legislation

(Sec 92D read with Rule 10D)

•To be prepared for a Transfer Pricing assessment

•As a contemporaneous record

•To demonstrate how pricing decisions were made

•To show that you did adopt arm

’s length principle

•To eliminate/ minimise penalties

Indian TP Regulations and OECD

recommendations

•Extensiveness of documentation process to be determ

ined

by prudent business management principles

•Greater the complexity & unusualness of the case, the more

significance will attach to documentation

•Key considerations:

•Nature and term

s of the transaction

•An outline of the business (financial or otherwise)

•Management strategy, market penetration strategies

•Organisation structure

•Ownership linkages within the group

•Factors influencing the setting of prices

•Special circumstances

•Business environment / trends –competition, technology, etc.

•Functions, assets, risks

Objectives

•At a high-level, objective or purpose of a documentation

can be viewed along a spectrum

•Significant differentiating aspects

•Not interchangeable but planning documentation can be

converted into compliance documentation

•Im

plementation aspects

Design and planning

documentation

Compliance

documentation

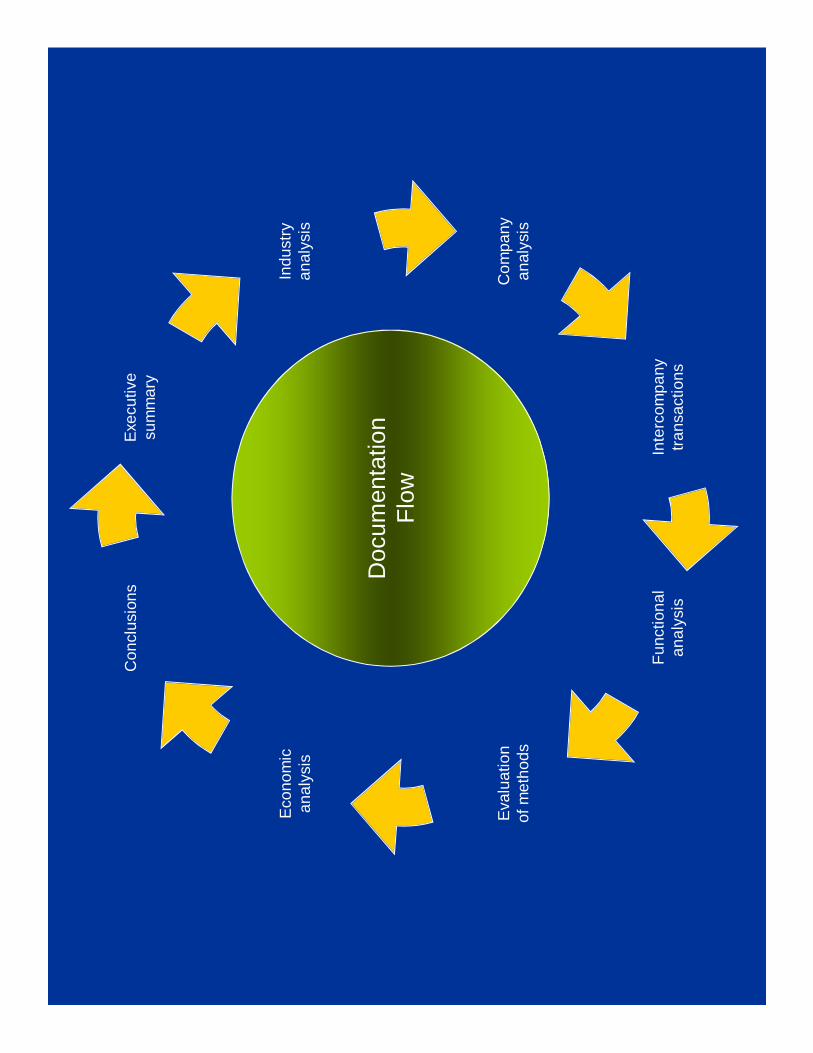

Documentation Flow

Exe

cutiv

esu

mm

ary

Indu

stry

anal

ysis

Com

pany

anal

ysis

Inte

rcom

pany

tran

sact

ions

Fun

ctio

nal

anal

ysis

Eva

luat

ion

of m

etho

ds

Eco

nom

ican

alys

is

Con

clus

ions

Doc

umen

tatio

nF

low

Sources

•Company inform

ation

•Financial statements

•Corporate entity structure charts

•TP policy

•Intercompany agreements

•Industry research

•Investment banker reports

•Market research, university studies, industry reports from government

agencies or industry bodies

•Websites

•Newspaper or journal articles

•Functional analysis

•Interviews

It’s important to connect all these and build a story!

The Approach

Getting started

Executive summary:

•Summarise key elements

•Objective

•Scope

•Conclusions

•Im

portant to first identify conclusions

one would like to reach based on facts

of each individual case

•Develop remainder of document to

reach those conclusions

•Each section leads to the next

•List conclusions a provide link to show

how those conclusions were reached

Indu

stry

Ana

lysi

s

Com

pany

Ana

lysi

s

Inte

rcom

pany

Tra

nsac

tions

Fun

ctio

nal A

naly

sis

Eva

luat

ion

of M

etho

ds

Eco

nom

ic A

naly

sis

Con

clus

ions

Industry analysis –what’s this?

•Provides reader with description of industry in which the

company 0perates

•Focus on those industry factors which have the greatest

effect on company’s profitability

•Listen to operational personnel as to which factors they

consider most important and review the research,

highlighting areas which are most supportive or

demonstrative of company’s case

•Make sure focus is on competitive conditions faced by the

company

Industry analysis –contents

Overview

Background

•Products

•Structure

•Market segmentation

Market overview –focus on relevant industry

and market trends

Main competitors –discuss where the company

falls within competitive makeup, compare

financial successes and failuresfir

st d

escr

ibe

broa

d pa

ram

eter

s, th

en fo

cus

in

mor

e de

tail

on th

e co

mpa

ny’s

ba

ckdr

op

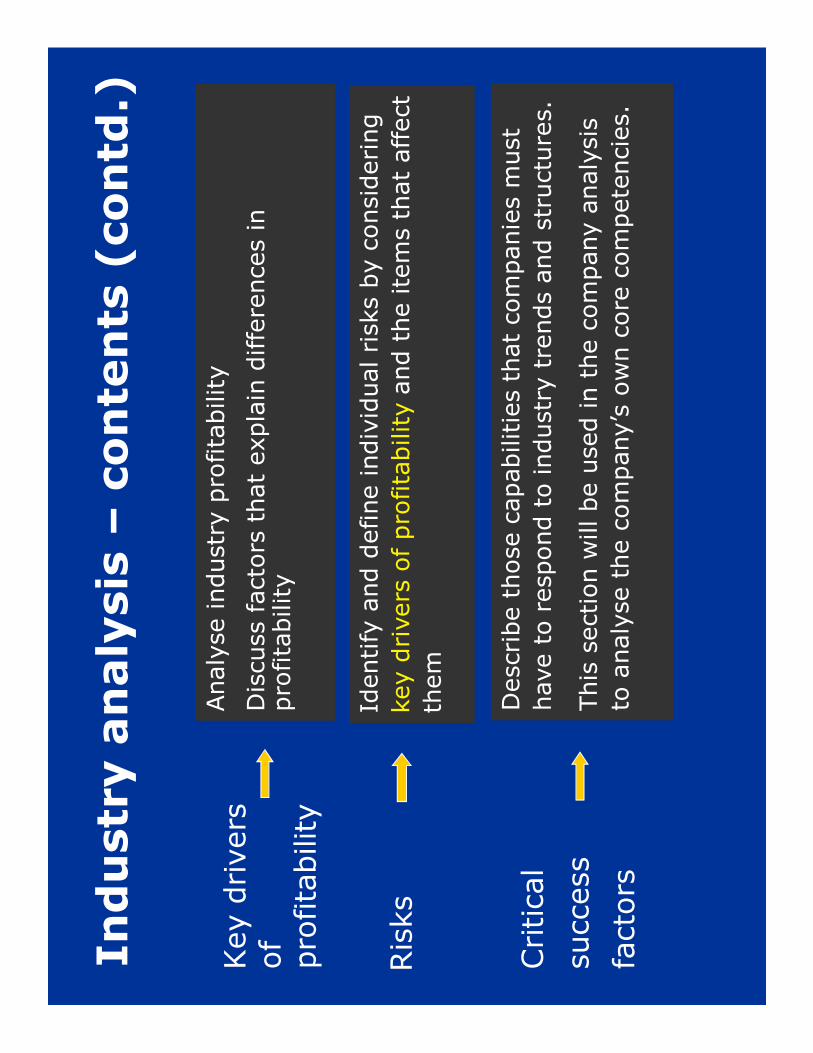

Industry analysis –contents (contd.)

Key drivers

of profitability

Analyse industry profitability

Discuss factors that explain differences in

profitability

Risks

Identify and define individual risks by considering

key drivers of profitabilityand the items that affect

them

Critical

success

factors

Describe those capabilities that companies must

have to respond to industry trends and structures.

This section will be used in the company analysis

to analyse the company’s own core competencies.

Industry analysis –contents (contd.)

Key

conclusions

for TP

Goal of this section is to set the stage for

future analyses

Aim at establishing a link between industry

analysis and what is to come later in the

report

Depends on what it is important to highlight

for the company

Summarise most important points for

influencing further conclusions

Company analysis –what’s this?

•Provides reader with a background of the company,

placed in the context of the transactions

•Prepared to understand legal & business structure /

operations of the company

•Objective is to describe the group’s:

•Competitive and corporate strategy

•Financial perform

ance

•Strengths and weaknesses (SWOT analysis?)

•Legal structure

•Make use of major points identified in industry analysis

Company analysis –contents

Background

•History

•Corporate strategy

•Vision / mission statement

Business overview

Financial perform

ance –

describe over time

Overview

Company analysis –contents

(contd.)

Core

competencies

Few skills that the company possesses to a greater

extent than most others (may be identified in

relation to industry critical success factors)

Discuss company’s strengths and weaknesses

relative to immediate competitors

Company’s profitability compared to its strategic

group / sector

Key

conclusions

for TP

Intercompany transactions –what’s

this?

•Provides a description of intercompany transactions

under review

•Pricing policy and intercompany agreements

•Aggregation of transactions

Intercompany transactions –

contents

List

transactions

Provides clarity on which transactions have been

analysed

Aggregation

of transactions

Discuss whether appropriate to consider

transactions one by one or on a grouped basis

(whole entity?)

TP policy

Describe the company’s TP policy document (if

any)

Term

s and conditions that apply to transactions

Intercompany agreements / contracts

Functional analysis –what’s this?

•Describes functions perform

ed, assets utilised & risks

borne by each transacting entity

•Analyses how company manages its core competencies,

critical success factors& risks

•Examines how conclusions reached in industry &

company analysestranslate into specific activities

undertaken by the company

•Basis for entity characterisation

Functional analysis –process flow

Org

anis

atio

n st

ruct

ure

a)M

anag

emen

t

b)O

pera

tions

c)S

uppo

rt

Rol

es &

Res

pons

ibili

ties

a)M

anag

er (

Tre

asur

y) –

resp

onsi

ble

for

hedg

ing

risks

b)S

taff

(Res

earc

h) –

resp

onsi

ble

for

spec

ific

task

s th

at fo

rm p

art o

f des

igni

ng

and

deve

lopi

ng n

ew p

rodu

cts

Act

iviti

es

a)T

reas

ury

incl

udes

cas

h an

d ris

k m

anag

emen

t, he

dgin

g, f

inan

cing

, fo

reca

stin

g an

d in

sura

nce

b)R

&D

incl

udes

gen

erat

ion

of

inno

vatio

ns,

prod

uct i

mpr

ovem

ents

, ad

vanc

es in

man

ufac

turin

g pr

oces

ses,

et

c.

Fun

ctio

ns

•T

reas

ury

•R

esea

rch

& D

evel

opm

ent

a)In

dust

ry

Ana

lysi

s

b)C

ompa

ny

Ana

lysi

s

c)In

ter-

com

pany

Tr

ansa

ctio

ns

Ass

ets

a) T

angi

bles

b) In

tang

ible

s

Ris

ks

Bus

ines

s fa

ctor

s th

at m

ay e

xpos

e co

mpa

ny t

o po

ssib

ility

of l

oss

/ dam

age

–m

arke

t ris

k, w

arra

nty

risk,

cre

dit r

isk,

etc

.

Fun

ctio

nal

Ana

lysi

s

Functional analysis –contd.

•Functions / Assets / Risks can be summarised by way of

a chart showing the contribution of each party

•Overview of economically relevant contributions made by

each entity, key perform

ance indicators and assets

contributed

•Summary of contributions helps in entity characterization

•Entity characterization important in finding out the

“simpler party”

•Simpler party typically leads to conclusion on choice of

tested party

Economic analysis –what’s this?

•Summarises evaluation of TP accepted methodology,

comparable search process and results of benchmarking

analysis

•Choice of most appropriate methodology is based on FAR

•Choice of tested party

•Which PLI should be applied?

•Core benchmarking consists of searches perform

ed on

databases to arrive at a list of comparable independent

companies

•PLI is applied to comparable companies’ financials

•Economic adjustm

ents may need to be perform

ed to

enhance comparability

Economic analysis –process flow

Ent

ity C

hara

cter

izat

ion

Cho

ice

of T

este

d P

arty

Fun

ctio

nal A

naly

sis

•F

unct

ions

•R

isks

•A

sset

s

Arm

’s le

ngth

ran

ge o

f res

ults

??

Eco

nom

ic A

naly

sis

•S

elec

tion

of M

ost A

ppro

pria

te M

etho

d

•B

ench

mar

king

Fin

anci

al A

naly

sis

•P

rofit

Lev

el In

dica

tor

•M

ultip

le y

ear

/ dat

a av

aila

bilit

y

Conclusions –what’s this?

•Provides the findings of each section of the report

•Analyzes how these conclusions were reached

•Comment on whether the objectives of the report have

been met

Post-completion

Post-completion

•Draft and implement TP policy and / or

intercompany agreement

•“Living” document

Takeaways

Takeaways

•Build a TP story

•Understand the issues

•Connect the dots / Make the complex

understandable

•Speak easy language

•Seek a fresh perspective

Takeaways

The R

evenue w

ill never u

ndersta

nd y

our

busin

ess a

s w

ell a

s y

ou -

but

if y

ou f

ail t

o

expla

in y

our b

usin

ess a

nd p

ric

ing in e

asy

“la

nguage”, you w

ill encounte

r o

ngoin

g

expensiv

e d

iffi

cult

ies.

Questions?

See

k a

fres

h p

ersp

ecti

ve a

nd

rin

g f

ence

th

e ri

sks

!!

Pre

sent

atio

n N

ame

(Vie

w /

Hea

der

and

Foo

ter)

33F

irm N

ame/

Lega

l E

ntity

and

Leg

al C

opy