2012 doritos marketing plan

DESCRIPTION

Developing A Marketing PlanTRANSCRIPT

2013

Marketing Plan

Niko Vergis

12/12/12

Developing a Marketing Plan

2 | P a g e

Title Page … 1

Table of Contents… 2

Company Overview... 3 - 4

Market Summary… 4 -5

Demographic Overview… 5 – 7

Competition… 8 – 11

SWOT Analysis… 12

Marketing Objectives… 13 - 14

Key Strategies

Mission Statement

Marketing Strategy and Programs … 14 - 21

Budget/Calendar… 22

Advertisement… 23

Bibliography… 24

3 | P a g e

Doritos Company Overview

PepsiCo’s mission statement states, “Our mission is to be the world's premier consumer

Products Company focused on convenient foods and beverages. We seek to produce financial

rewards to investors as we provide opportunities for growth and enrichment to our employees,

our business partners and the communities in which we operate. And in everything we do, we

strive for honesty, fairness and integrity”. PepsiCo also have a vision on the company and I

states, “PepsiCo's responsibility is to continually improve all aspects of the world in which we

operate - environment, social, economic - creating a better tomorrow than today. “Our vision is

put into action through programs and a focus on environmental stewardship, activities to benefit

society, and a commitment to build shareholder value by making PepsiCo a truly sustainable

company.

Frito Lay is a sister company under PepsiCo and specifically creates sells and distributes

many kinds of potato chips. Frito lay is one of five companies under Pepsi-Cos belt, the band has

become public as a whole but not by itself. Frito Lay has been around for more than 75 years

and holds 79.6% of the potato chip and snack foods industry to date.

The revenue of Frito Lay over the last 3 years has steadily stayed around $16 Billion and

about $3 Billion of that is in North America. As for PepsiCo as a whole the revenue has reached

over $66.5 Billion. Frito Lay’s profits are not available to the public PepsiCo is, reaching a gross

profit of $35 Billion and a Net profit of $6.5 Billion. Frito Lay currently has 40,000 employees

worldwide and 3000 employees are in North America. In North America Frito has 7 important

executives Albert Carey as president, Nancy Loewe as Chief Financial officer, Justin Lambeth as

Secretary, and Leslie Keating- Randolph Melville-Jamie Montemayor- Anindita Mukherjee ass

4 | P a g e

as Senior Vice Presidents. The North American headquarters for Frito Lay is located in Dallas

Texas, while PepsiCo headquarters is located in New York, New York.

Market Summary

The "salty snack" industry includes potato chips, corn chips, tortilla chips, ready-to-eat

popcorn (except candy-coated), pork rinds, potato sticks, and extruded snacks such as cheese

puffs. According to the Snack Food Association, sales for snacks during 2011 totaled $24.6

billion. Frito-Lay was the undisputed champion of this industry category, with Tostitos, Ruffles,

Rold Gold, Fritos, Lay's, Cheetos, SunChips, and many more top sellers under its umbrella.

Potato chips and tortilla chips controlled the snack foods market. Doritos as of 2011, hold over

$5 billion of worldwide sales. 84 percent of American households eat potato chips, which had

one-third of the salty snacks market in the mid-2000s.

The dietary trend in the 2000s toward healthier eating did not affect the snack category of

foods as much as anticipated, as approximately one-third of the population regularly ate snacks

in place of a meal. Single-serve and other "on the go" packaging was lifting sales by catering to

the demands of a faster-paced lifestyle. Three-fourths of those who snack do so in the evenings.

In addition, snacks were becoming more healthful, with reductions in sugar and fat. New

labeling requirements in 2006 stipulated that nutritional labels must specify trans-fat content,

otherwise known as hydrogenated fats and oils, in grams. Industry leader Frito-Lay beat the rush

by including the line on its labels in 2003, well in advance of the deadline for compliance.

The salty snack foods industry has a unique structure, since Frito-Lay, a division of

PepsiCo, controlled about two-thirds of the total market share. Although the industry has some

elements of a monopoly (aggressive pricing and distribution policies among chip makers), the

5 | P a g e

regional presence of many large and small manufacturers keeps it highly competitive. Numerous

companies of varying size make up the snack industry. Many compete only on a regional level,

although some find it difficult to price their products competitively with the larger

manufacturers. Others, however, create a market niche, sometimes with a specialty product such

as kettle-style potato chips or baked chips sold through health food stores. If their products meet

with success among customers, the smaller makers can often charge higher prices than the

biggest manufacturers. Larger manufacturers are generally full-service snack companies – those

offering a full range of products, including potato chips, tortilla chips, and other salty snacks.

The smaller producers are more likely to specialize.

Total Consumption Framework

The main demographic of consumption for Doritos are younger bustling families with 6

or more children reaching 207 index which is over twice the consumption of the average

consumer. Second highest consumers are older bustling families with 6 or more children

reaching 189 index which is just under twice the consumption of the average consumer. As for

Affluent

Suburban

Spreads

Cosmopolitan

Centers

Young Transitionals

Any size HHs, No Children, < 35

Older Bustling Families

Large HHs with Children (6+), HOH 40+

Younger Bustling Families

Large HHs with Children (6+), HOH <40

Small Scale Families

Small HHs with Older Children 6+

Start-Up Families

HHs with Young Children Only < 6

TotalPlain Rural

Living

Modest

Working

Towns

Struggling

Urban Cores

Comfortable

Country

Total

Senior Couples

2+ person HHs, No Children, 65+

Empty Nest Couples

2+ person HHs, No Children, 55-64

Established Couples

2+ person HHs, No Children, 35-54

Senior Singles

1 person HHs, No Children, 65+

Independent Singles

1 person HHs, No Children, 35-64

116

71

49

10083 98 107 94 97 113

147

207

189

74

48

23

40 45 51 60 50 49

62 68 74 65 69 80

102 99 127 104 112 140

12 19 22 28 22 29

42 44 44 48 52 54

47 97 82 81 69 86

189 169 192 122 222 232

177 186 217 173 214 242

146 144 154 142 135 154

LifeStyle

BehaviorStage

108 79 117 138 122 148 118

6 | P a g e

the most consumption of Doritos within a lifestyle would be families in Plain Rural Living

reaching 113 index, and following that would be Comfortable Country life style reaching

107index. Looking at the percentages below shows that Midscale Working Towns purchase a

7.3% volume of Doritos. Following that are Moderate Blue-Collar Towns with a 6.8% volume.

Demographic Overview

%

VolumeIndex

16.6% 119

31.8% 116

28.4% 101

15.0% 84

8.3% 65

2.4% 77

3.6% 100

3.9% 89

3.0% 81

5.1% 115

4.8% 90

4.0% 124

4.5% 89

4.3% 81

4.0% 105

3.1% 95

4.2% 100

7.3% 119

4.9% 90

3.4% 95

3.2% 101

6.8% 122

4.3% 102

3.5% 91

3.2% 105

4.3% 92

4.5% 111

3.8% 132

4.1% 98

9.7% 113

17.1% 161

32.8% 193

40.5% 63 No Children

Struggling Rural Mix

Struggling Backroad Living

Age of Oldest Child

Age Under 6

Age 6 - 11

Age 12 - 17

Moderate Blue-Collar Towns

Moderate Country Living

Struggling Urban Mix

Struggling Small City Mix

Struggling Minipolitan

Struggling Country Living

Midscale Minipolitan

Midscale Fringe Towns

Midscale Working Towns

Striving Urban Melting Pot

Striving Suburban Mix

Striving Small City Living

Affluent Suburbs

Affluent Minipolitan Sprawl

Affluent Country Living

Cosmopolitan Urban Mix

Cosmopolitan Suburbs

Midscale Suburban Mix

Post College Degree

Spectra LifeStyle

Urban High Society

Suburban Aristocrats

Prosperous Suburbs

Elite Country Manors

Variables and Measures

Demographic Variables

Education of Head of Household

Not a High School Graduate

High School Graduate

Some College

College Graduate

7 | P a g e

The average consumers of Doritos are Hispanic with 3 or more people in the household,

reaching a HHI of $50,000 - $74,000. Age of head of household are ages 35 – 44 with children

aged from 6 – 17. The occupation this consumer has are crafts and precision and transportation

and moving materials. This person is also married with kids and owns 3 or more vehicles. The

education this consumer has accomplished is a high school diploma or no high school education

at all. This consumer also lives in North West Central America.

A clear indication of households with 5 or more people reaches an index of 206. Most

consumers in the house hold are children from ages 12 – 17 at 193 index, 93% over the average.

Total

Consumption Index

22% 206

33% 193

14% 180

36% 179

38% 178

23% 162

17% 161

29% 155

4% 155

18% 154

Age 35 - 44

Male Head Only with Children

Precision Production, Craft & Repair Occupations

Demographic Skews5+ Person Households

Oldest Child 12 - 17

Presence of Both Children Under 6 and 6 - 17

Presence of Only Children 6 - 17

Married Families with Children

4 Person Households

Oldest Child 6 - 11

Number of Persons-Total Consumption Index

0

50

100

150

200

250

1 Person 2 Persons 3 Persons 4 Persons 5+ Persons

8 | P a g e

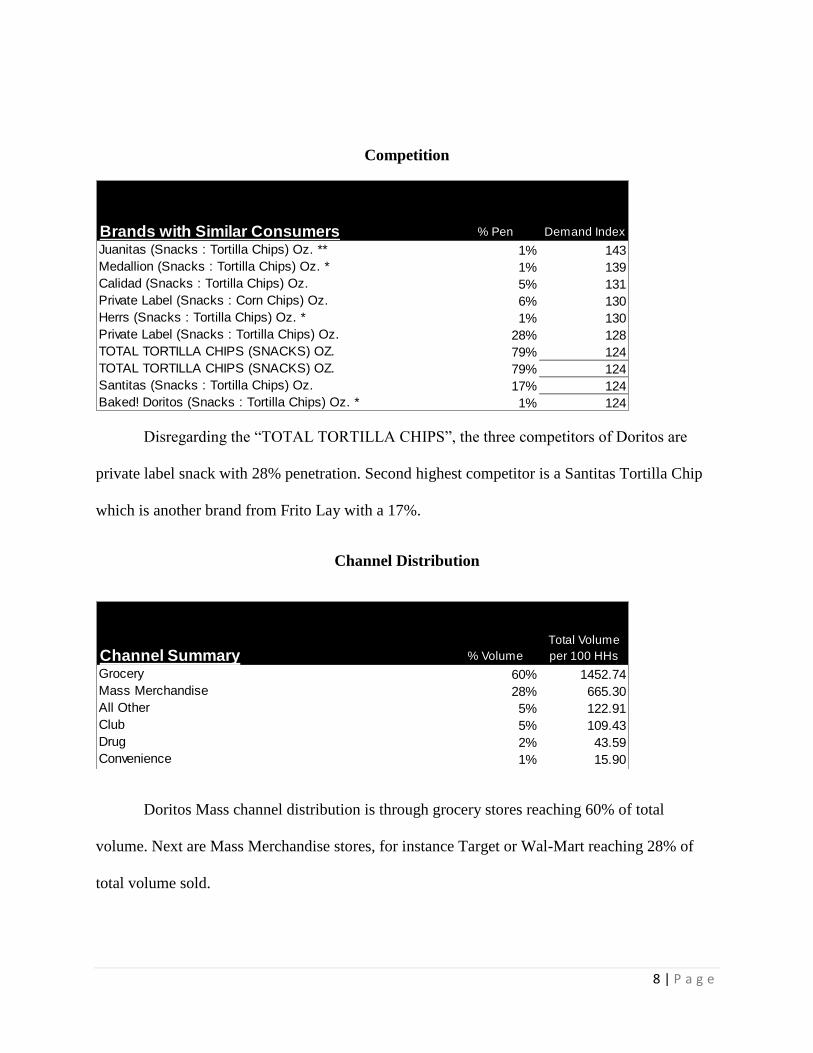

Competition

Disregarding the “TOTAL TORTILLA CHIPS”, the three competitors of Doritos are

private label snack with 28% penetration. Second highest competitor is a Santitas Tortilla Chip

which is another brand from Frito Lay with a 17%.

Channel Distribution

Doritos Mass channel distribution is through grocery stores reaching 60% of total

volume. Next are Mass Merchandise stores, for instance Target or Wal-Mart reaching 28% of

total volume sold.

% Pen Demand Index

1% 143

1% 139

5% 131

6% 130

1% 130

28% 128

79% 124

79% 124

17% 124

1% 124

Private Label (Snacks : Tortilla Chips) Oz.

TOTAL TORTILLA CHIPS (SNACKS) OZ.

TOTAL TORTILLA CHIPS (SNACKS) OZ.

Santitas (Snacks : Tortilla Chips) Oz.

Baked! Doritos (Snacks : Tortilla Chips) Oz. *

Brands with Similar ConsumersJuanitas (Snacks : Tortilla Chips) Oz. **

Medallion (Snacks : Tortilla Chips) Oz. *

Calidad (Snacks : Tortilla Chips) Oz.

Private Label (Snacks : Corn Chips) Oz.

Herrs (Snacks : Tortilla Chips) Oz. *

% Volume

Total Volume

per 100 HHs

60% 1452.74

28% 665.30

5% 122.91

5% 109.43

2% 43.59

1% 15.90Convenience

Channel SummaryGrocery

Mass Merchandise

All Other

Club

Drug

9 | P a g e

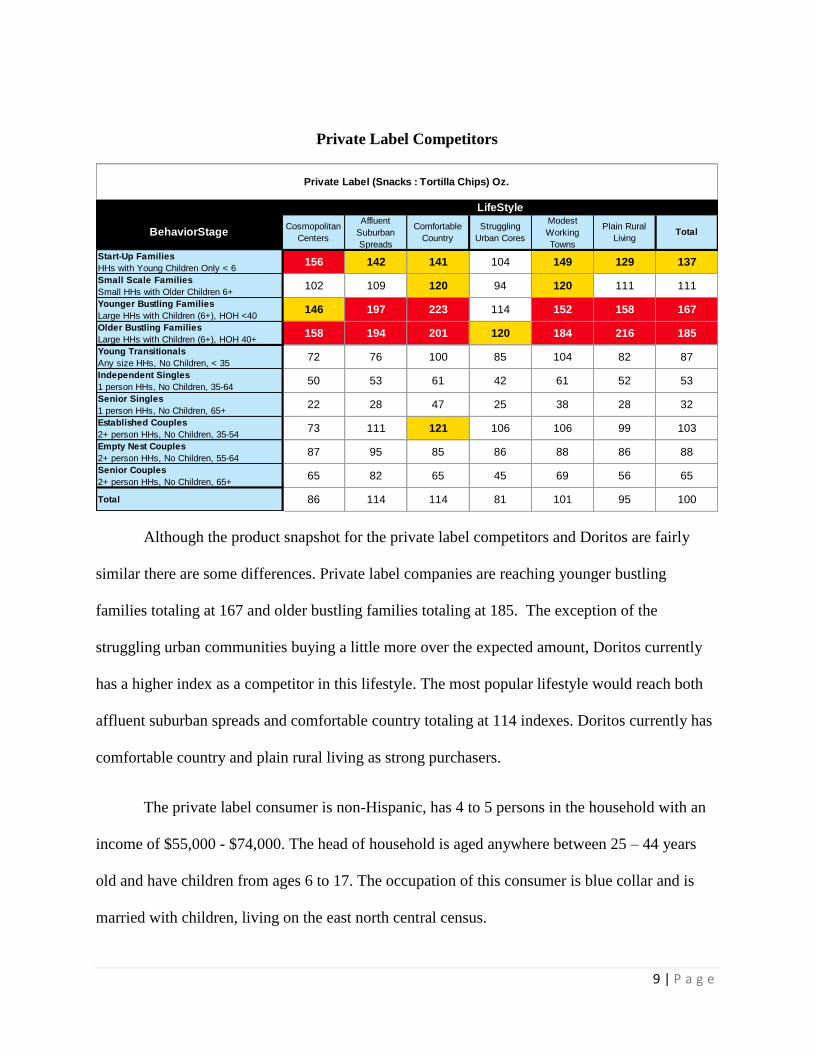

Private Label Competitors

Although the product snapshot for the private label competitors and Doritos are fairly

similar there are some differences. Private label companies are reaching younger bustling

families totaling at 167 and older bustling families totaling at 185. The exception of the

struggling urban communities buying a little more over the expected amount, Doritos currently

has a higher index as a competitor in this lifestyle. The most popular lifestyle would reach both

affluent suburban spreads and comfortable country totaling at 114 indexes. Doritos currently has

comfortable country and plain rural living as strong purchasers.

The private label consumer is non-Hispanic, has 4 to 5 persons in the household with an

income of $55,000 - $74,000. The head of household is aged anywhere between 25 – 44 years

old and have children from ages 6 to 17. The occupation of this consumer is blue collar and is

married with children, living on the east north central census.

Affluent

Suburban

Spreads

Cosmopolitan

Centers

Young Transitionals

Any size HHs, No Children, < 35

Older Bustling Families

Large HHs with Children (6+), HOH 40+

Younger Bustling Families

Large HHs with Children (6+), HOH <40

Small Scale Families

Small HHs with Older Children 6+

Start-Up Families

HHs with Young Children Only < 6

TotalPlain Rural

Living

Modest

Working

Towns

Struggling

Urban Cores

Comfortable

Country

Total

Senior Couples

2+ person HHs, No Children, 65+

Empty Nest Couples

2+ person HHs, No Children, 55-64

Established Couples

2+ person HHs, No Children, 35-54

Senior Singles

1 person HHs, No Children, 65+

Independent Singles

1 person HHs, No Children, 35-64

103

88

65

10086 114 114 81 101 95

111

167

185

87

53

32

65 82 65 45 69 56

87 95 85 86 88 86

73 111 121 106 106 99

22 28 47 25 38 28

50 53 61 42 61 52

72 76 100 85 104 82

158 194 201 120 184 216

146 197 223 114 152 158

102 109 120 94 120 111

Private Label (Snacks : Tortilla Chips) Oz.

LifeStyle

BehaviorStage

156 142 141 104 149 129 137

10 | P a g e

Santitas Competitor

Viewing Santitas as a big tortilla chip competitor differentiates from Doritos slightly.

Reaching younger bustling families at 150 index and older bustling families at 157 indexes,

Doritos still takes the lead reaching an average 200 index between the two behavior stages.

Santitas popular lifestyles are comfortable country at 124 and plain rural living at 121 indexes,

taking the lead from Doritos in these 2 categories.

The average consumers for Santitas are mainly Hispanic with 5 or more people in the

household, gaining an income of $50,000 - $74,999. The age of the head of household is 35 – 54

with children primarily 6 – 17 but younger as well. The consumer has a high school education

and their occupation is farming, fishing and forestry. This person is married and lives primarily

in mountain or west south central census.

Affluent

Suburban

Spreads

Cosmopolitan

Centers

Young Transitionals

Any size HHs, No Children, < 35

Older Bustling Families

Large HHs with Children (6+), HOH 40+

Younger Bustling Families

Large HHs with Children (6+), HOH <40

Small Scale Families

Small HHs with Older Children 6+

Start-Up Families

HHs with Young Children Only < 6

TotalPlain Rural

Living

Modest

Working

Towns

Struggling

Urban Cores

Comfortable

Country

Total

Senior Couples

2+ person HHs, No Children, 65+

Empty Nest Couples

2+ person HHs, No Children, 55-64

Established Couples

2+ person HHs, No Children, 35-54

Senior Singles

1 person HHs, No Children, 65+

Independent Singles

1 person HHs, No Children, 35-64

120

106

69

10081 86 124 78 95 121

121

150

157

76

68

33

44 47 78 68 82 79

81 77 134 90 112 123

101 105 145 91 113 145

27 32 39 20 31 40

48 58 87 82 62 75

64 86 117 61 60 98

96 126 194 107 167 232

198 135 156 82 155 177

160 97 131 93 113 135

LifeStyle

BehaviorStage

81 75 151 96 124 175 119

11 | P a g e

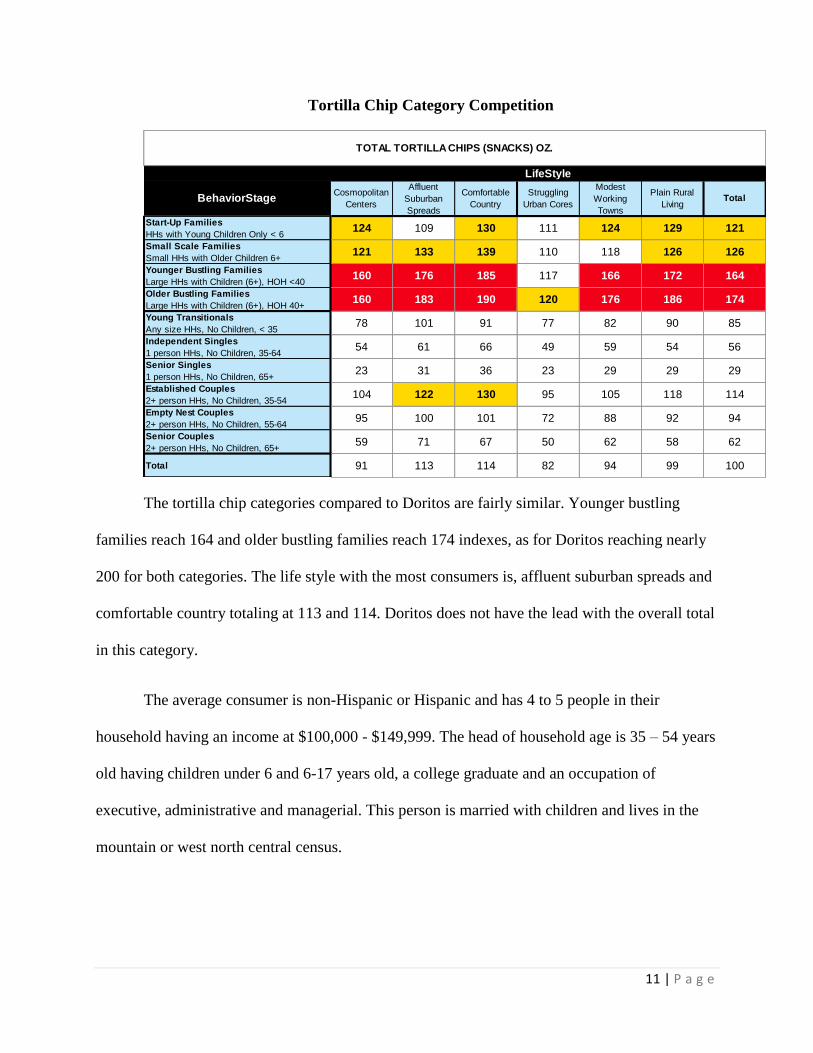

Tortilla Chip Category Competition

The tortilla chip categories compared to Doritos are fairly similar. Younger bustling

families reach 164 and older bustling families reach 174 indexes, as for Doritos reaching nearly

200 for both categories. The life style with the most consumers is, affluent suburban spreads and

comfortable country totaling at 113 and 114. Doritos does not have the lead with the overall total

in this category.

The average consumer is non-Hispanic or Hispanic and has 4 to 5 people in their

household having an income at $100,000 - $149,999. The head of household age is 35 – 54 years

old having children under 6 and 6-17 years old, a college graduate and an occupation of

executive, administrative and managerial. This person is married with children and lives in the

mountain or west north central census.

Affluent

Suburban

Spreads

Cosmopolitan

Centers

Young Transitionals

Any size HHs, No Children, < 35

Older Bustling Families

Large HHs with Children (6+), HOH 40+

Younger Bustling Families

Large HHs with Children (6+), HOH <40

Small Scale Families

Small HHs with Older Children 6+

Start-Up Families

HHs with Young Children Only < 6

TotalPlain Rural

Living

Modest

Working

Towns

Struggling

Urban Cores

Comfortable

Country

Total

Senior Couples

2+ person HHs, No Children, 65+

Empty Nest Couples

2+ person HHs, No Children, 55-64

Established Couples

2+ person HHs, No Children, 35-54

Senior Singles

1 person HHs, No Children, 65+

Independent Singles

1 person HHs, No Children, 35-64

114

94

62

10091 113 114 82 94 99

126

164

174

85

56

29

59 71 67 50 62 58

95 100 101 72 88 92

104 122 130 95 105 118

23 31 36 23 29 29

54 61 66 49 59 54

78 101 91 77 82 90

160 183 190 120 176 186

160 176 185 117 166 172

121 133 139 110 118 126

TOTAL TORTILLA CHIPS (SNACKS) OZ.

LifeStyle

BehaviorStage

124 109 130 111 124 129 121

12 | P a g e

SWOT Analysis

Strengths

Does well in engagement marketing by redirecting their website directly to Facebook.

Dominated the tortilla chip world with the number one flavor.

Strong, bold and entertaining television and print ads.

Fights for differentiation on advertising and high market share.

Loyal consumers.

Shaped partnerships.

Delivered solid operating and financial performance and generated significant operating

cash flow.

Highly diversified brand by having 102 flavors since 1964.

Weaknesses

Insufficient health benefits

Image damage due to recall of other PepsiCo products.

Overdependence on US markets.

Opportunities

Expand brand with mergers and acquisitions for strong presence all over the world.

Invest in R&D to expand offerings of more nutritional health conscience lifestyles.

Threats

Increase of a health conscious economy.

Intense competition of big competitors.

Smaller company’s becoming furious competitor which makes competition harsh.

13 | P a g e

Marketing Objectives

Gain 10% market share of healthy customers in 18 months.

Grow international sales by 15%.

International media awareness and coverage.

Key Strategies

Looking further in to Research and Design will help identify and build new offerings into

more nutritional health conscience life styles.

Partnerships with healthier brands (Sun Chips, Kashi) to help leverage a healthier image.

Expand brand with current partners and mergers (Mountain Dew, Microsoft Xbox, EA

Sports, NFL) for a stronger worldwide presence.

Create more partnership relations with overseas companies to leverage global market.

Doritos is a top sponsor of the NFL, therefore becoming a top sponsor for the biggest

international sport FIFA/MLS, will have the same increasing impact as the U.S. has.

Price promotions – holiday promotions.

By adding to the strength of Frito lays current portfolio, we believe that we can

deliver quicker financial returns to investors over the long-term. Creating deeper

expansion of Doritos into other countries and a more “better for you, good for you

product,” The growth will translate over to high single digit earnings per share,

increasing margins and increasing returns on capital.

14 | P a g e

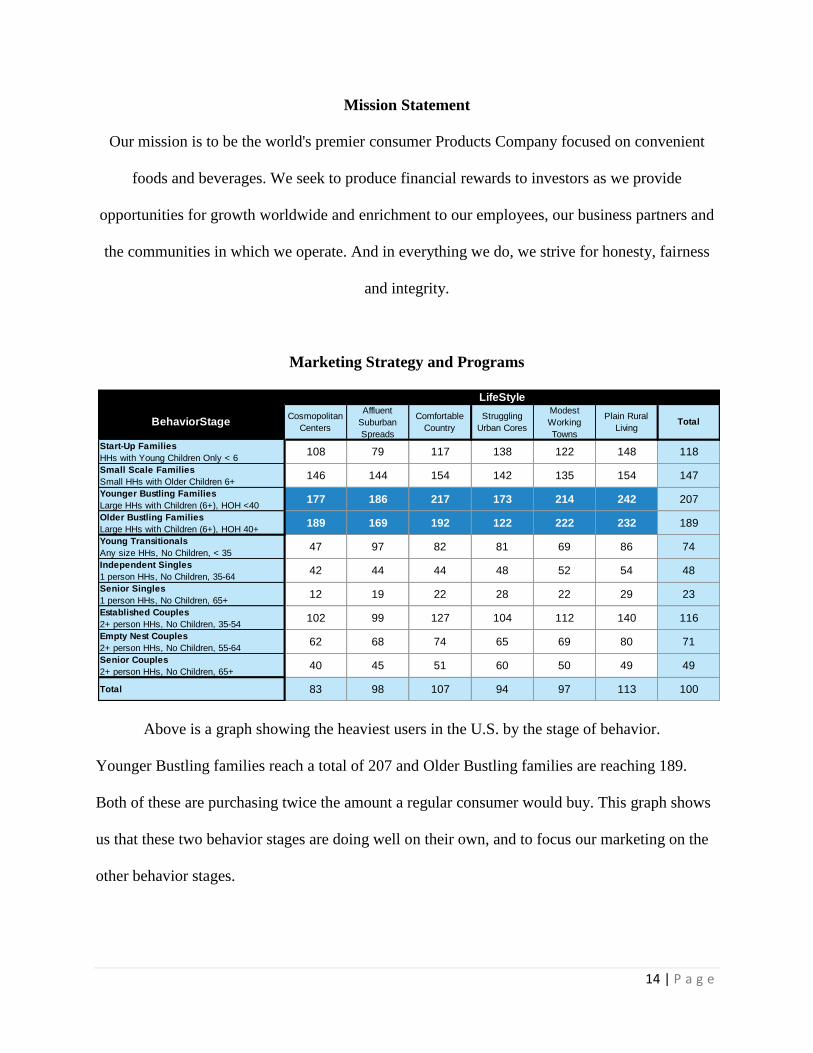

Mission Statement

Our mission is to be the world's premier consumer Products Company focused on convenient

foods and beverages. We seek to produce financial rewards to investors as we provide

opportunities for growth worldwide and enrichment to our employees, our business partners and

the communities in which we operate. And in everything we do, we strive for honesty, fairness

and integrity.

Marketing Strategy and Programs

Above is a graph showing the heaviest users in the U.S. by the stage of behavior.

Younger Bustling families reach a total of 207 and Older Bustling families are reaching 189.

Both of these are purchasing twice the amount a regular consumer would buy. This graph shows

us that these two behavior stages are doing well on their own, and to focus our marketing on the

other behavior stages.

214 242

189 169 192 122 222 232

Affluent

Suburban

Spreads

Cosmopolitan

Centers

177 186 217 173

Young Transitionals

Any size HHs, No Children, < 35

Older Bustling Families

Large HHs with Children (6+), HOH 40+

Younger Bustling Families

Large HHs with Children (6+), HOH <40

Small Scale Families

Small HHs with Older Children 6+

Start-Up Families

HHs with Young Children Only < 6

TotalPlain Rural

Living

Modest

Working

Towns

Struggling

Urban Cores

Comfortable

Country

Total

Senior Couples

2+ person HHs, No Children, 65+

Empty Nest Couples

2+ person HHs, No Children, 55-64

Established Couples

2+ person HHs, No Children, 35-54

Senior Singles

1 person HHs, No Children, 65+

Independent Singles

1 person HHs, No Children, 35-64

116

71

49

10083 98 107 94 97 113

147

207

189

74

48

23

40 45 51 60 50 49

62 68 74 65 69 80

102 99 127 104 112 140

12 19 22 28 22 29

42 44 44 48 52 54

47 97 82 81 69 86

146 144 154 142 135 154

LifeStyle

BehaviorStage

108 79 117 138 122 148 118

15 | P a g e

The graph above is showing Small Scale Families reach 147 index and Established

Couples reach 116. I chose these to behavioral stages because they are the middle ranged average

buyers, buying around one and a half times the average buyer. These are 2 groups we could

focus on to have them purchase twice the amount they do now. That would put them in the heavy

user category.

135 154

102 99 127 104 112 140

Affluent

Suburban

Spreads

Cosmopolitan

Centers

146 144 154 142

Young Transitionals

Any size HHs, No Children, < 35

Older Bustling Families

Large HHs with Children (6+), HOH 40+

Younger Bustling Families

Large HHs with Children (6+), HOH <40

Small Scale Families

Small HHs with Older Children 6+

Start-Up Families

HHs with Young Children Only < 6

TotalPlain Rural

Living

Modest

Working

Towns

Struggling

Urban Cores

Comfortable

Country

Total

Senior Couples

2+ person HHs, No Children, 65+

Empty Nest Couples

2+ person HHs, No Children, 55-64

Established Couples

2+ person HHs, No Children, 35-54

Senior Singles

1 person HHs, No Children, 65+

Independent Singles

1 person HHs, No Children, 35-64

116

71

49

10083 98 107 94 97 113

147

207

189

74

48

23

40 45 51 60 50 49

62 68 74 65 69 80

12 19 22 28 22 29

42 44 44 48 52 54

47 97 82 81 69 86

189 169 192 122 222 232

177 186 217 173 214 242

LifeStyle

BehaviorStage

108 79 117 138 122 148 118

29

140

80

49

148

154

242

232

86

54

Young Transitionals

Any size HHs, No Children, < 35

Older Bustling Families

Large HHs with Children (6+), HOH 40+

Younger Bustling Families

Large HHs with Children (6+), HOH <40

Small Scale Families

Small HHs with Older Children 6+

Start-Up Families

HHs with Young Children Only < 6

TotalPlain Rural

Living

Modest

Working

Towns

Struggling

Urban Cores

Comfortable

Country

Total

Senior Couples

2+ person HHs, No Children, 65+

Empty Nest Couples

2+ person HHs, No Children, 55-64

Established Couples

2+ person HHs, No Children, 35-54

Senior Singles

1 person HHs, No Children, 65+

Independent Singles

1 person HHs, No Children, 35-64

83 98 107 94 97 113

48

23

116

71

49

100

40 45 51 60 50

118

147

207

189

74

102 99 127 104 112

62 68 74 65 69

42 44 44 48 52

12 19 22 28 22

189 169 192 122 222

47 97 82 81 69

146 144 154 142 135

177 186 217 173 214

LifeStyle

BehaviorStage

108 79 117 138 122

Affluent

Suburban

Spreads

Cosmopolitan

Centers

16 | P a g e

In this graph above I wanted to show the highest outreach specifically in lifestyles of the

consumer. I pulled Plain Rural Living as the highest users reaching 113 indexes, a little over the

average user. Looking at the life styles in certain locations would also help build market share.

Also, looking at the total number of life style, it’s possible that we can penetrate Comfortable

Country, Affluent suburban spreads, and modest working towns.

Kashi Overview

The Graph above is Kashi products and is a target market for the Doritos new angle on a

healthier tortilla chip. The majority of Kashi’s “healthy consumers” are in suburban affluent

spreads. This consumer is white with a yearly income of $100,000 +. They’re aged between 25 –

34, have graduated college, and have children under the age of 6 with 1-2 people living in the

house hold.

Cosmopolitan

Centers

Affluent

Suburban

Spreads

Comfortable

Country

Struggling Urban

Cores

Modest Working

Towns

Plain Rural

LivingTotal

Start-Up Families - HHs with Young Children Only < 6 97 282 127 78 31 120 129

Small Scale Families - Small HHs with Older Children 6+ 107 178 63 48 37 69 84

Younger Bustling Families - Large HHs with Children (6+), HOH <40 133 135 225 74 49 110 120

Older Bustling Families - Large HHs with Children (6+), HOH 40+ 182 295 128 33 66 53 145

Young Transitionals - Any size HHs, No Children, < 35 96 168 91 45 107 48 89

Independent Singles - 1 person HHs, No Children, 35-64 126 195 45 22 32 34 70

Senior Singles - 1 person HHs, No Children, 65+ 16 106 22 19 33 9 30

Established Couples - 2+ person HHs, No Children, 35-54 198 290 127 48 78 43 133

Empty Nest Couples - 2+ person HHs, No Children, 55-64 170 168 109 104 88 46 112

Senior Couples - 2+ person HHs, No Children, 65+ 160 180 58 135 60 34 93

Total 130 211 98 55 58 53 100

BehaviorStage

17 | P a g e

The heaviest use for Doritos in the U.S. is the west south central region with 116 as target

index. The highest percentage is the Pacific region and the West South Central reaching 21%

penetration. Since this is the most popular geographical target, few are right behind it. The

Pacific and south Atlantic geographic locations have potential for increasing their target index.

Future goals are to increase south Atlantic, Pacific and East north central target % HHs by 5

percent. This decision should also increase target penetration %.

The average consumers of Doritos are mostly located in the East South Central reaching

241 index, 2 and a half times what an average person would by. This location also has a 50%

Doritos heavy user consumption

Total % HHs Target % HHsTarget %

PenTarget Index Target HHs

South Atlantic 20.02% 18.59% 16.88% 93 3,949,014

Pacific 14.84% 16.38% 20.07% 110 3,480,738

East North Central 15.39% 14.98% 17.70% 97 3,183,060

West South Central 11.40% 13.20% 21.06% 116 2,805,679

Middle Atlantic 13.21% 12.12% 16.69% 92 2,575,662

Mountain 7.04% 7.50% 19.37% 107 1,592,738

West North Central 6.96% 6.86% 17.93% 99 1,458,306

East South Central 6.31% 6.10% 17.60% 97 1,296,866

New England 4.84% 4.26% 15.99% 88 905,314

Total 100.00% 100.00% 18.18% 100 21,247,377

Geography

Name

Doritos average user consumption (country)

Total % HHs Target % HHsTarget %

PenTarget Index Target HHs

East South Central 6.31% 15.19% 50.08% 241 3,690,987

West North Central 6.96% 9.70% 28.99% 139 2,357,551

West South Central 11.40% 15.76% 28.74% 138 3,828,882

South Atlantic 20.02% 24.69% 25.63% 123 5,998,075

East North Central 15.39% 13.48% 18.22% 88 3,276,127

Mountain 7.04% 6.14% 18.14% 87 1,491,615

Middle Atlantic 13.21% 7.08% 11.14% 54 1,719,887

New England 4.84% 2.28% 9.81% 47 555,188

Pacific 14.84% 5.68% 7.96% 38 1,379,435

Total 100.00% 100.00% 20.79% 100 24,297,748

Geography

Name

18 | P a g e

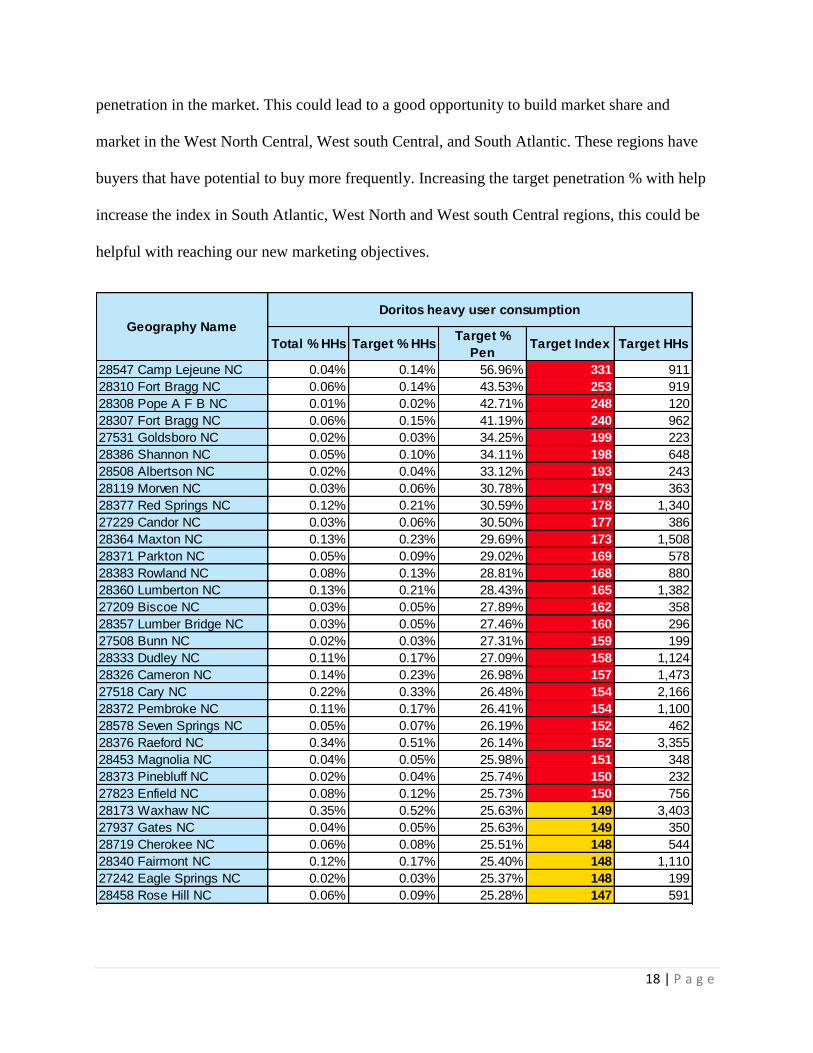

penetration in the market. This could lead to a good opportunity to build market share and

market in the West North Central, West south Central, and South Atlantic. These regions have

buyers that have potential to buy more frequently. Increasing the target penetration % with help

increase the index in South Atlantic, West North and West south Central regions, this could be

helpful with reaching our new marketing objectives.

Doritos heavy user consumption

Total % HHs Target % HHsTarget %

PenTarget Index Target HHs

28547 Camp Lejeune NC 0.04% 0.14% 56.96% 331 911

28310 Fort Bragg NC 0.06% 0.14% 43.53% 253 919

28308 Pope A F B NC 0.01% 0.02% 42.71% 248 120

28307 Fort Bragg NC 0.06% 0.15% 41.19% 240 962

27531 Goldsboro NC 0.02% 0.03% 34.25% 199 223

28386 Shannon NC 0.05% 0.10% 34.11% 198 648

28508 Albertson NC 0.02% 0.04% 33.12% 193 243

28119 Morven NC 0.03% 0.06% 30.78% 179 363

28377 Red Springs NC 0.12% 0.21% 30.59% 178 1,340

27229 Candor NC 0.03% 0.06% 30.50% 177 386

28364 Maxton NC 0.13% 0.23% 29.69% 173 1,508

28371 Parkton NC 0.05% 0.09% 29.02% 169 578

28383 Rowland NC 0.08% 0.13% 28.81% 168 880

28360 Lumberton NC 0.13% 0.21% 28.43% 165 1,382

27209 Biscoe NC 0.03% 0.05% 27.89% 162 358

28357 Lumber Bridge NC 0.03% 0.05% 27.46% 160 296

27508 Bunn NC 0.02% 0.03% 27.31% 159 199

28333 Dudley NC 0.11% 0.17% 27.09% 158 1,124

28326 Cameron NC 0.14% 0.23% 26.98% 157 1,473

27518 Cary NC 0.22% 0.33% 26.48% 154 2,166

28372 Pembroke NC 0.11% 0.17% 26.41% 154 1,100

28578 Seven Springs NC 0.05% 0.07% 26.19% 152 462

28376 Raeford NC 0.34% 0.51% 26.14% 152 3,355

28453 Magnolia NC 0.04% 0.05% 25.98% 151 348

28373 Pinebluff NC 0.02% 0.04% 25.74% 150 232

27823 Enfield NC 0.08% 0.12% 25.73% 150 756

28173 Waxhaw NC 0.35% 0.52% 25.63% 149 3,403

27937 Gates NC 0.04% 0.05% 25.63% 149 350

28719 Cherokee NC 0.06% 0.08% 25.51% 148 544

28340 Fairmont NC 0.12% 0.17% 25.40% 148 1,110

27242 Eagle Springs NC 0.02% 0.03% 25.37% 148 199

28458 Rose Hill NC 0.06% 0.09% 25.28% 147 591

Geography Name

19 | P a g e

Doritos heavy user consumption

Total % HHs Target % HHsTarget %

PenTarget Index Target HHs

60165 Stone Park IL 0.02% 0.06% 44.30% 239 525

62225 Scott Air Force Base IL 0.03% 0.07% 37.71% 203 588

60958 Pembroke Township IL 0.02% 0.03% 33.05% 178 270

60501 Summit Argo IL 0.07% 0.13% 32.96% 178 1,121

60585 Plainfield IL 0.11% 0.20% 32.86% 177 1,786

60426 Harvey IL 0.20% 0.35% 32.79% 177 3,115

62424 Dieterich IL 0.01% 0.02% 32.74% 177 220

60428 Markham IL 0.08% 0.13% 32.64% 176 1,184

60564 Naperville IL 0.25% 0.43% 31.83% 172 3,798

60827 Riverdale IL 0.20% 0.34% 31.60% 170 3,037

60472 Robbins IL 0.04% 0.06% 31.46% 170 524

60072 Ringwood IL 0.01% 0.01% 31.32% 169 86

60153 Maywood IL 0.14% 0.24% 31.04% 167 2,134

60037 Fort Sheridan IL 0.00% 0.00% 30.98% 167 27

60110 Carpentersville IL 0.24% 0.41% 30.92% 167 3,592

60804 Cicero IL 0.45% 0.74% 30.76% 166 6,529

60565 Naperville IL 0.30% 0.49% 30.52% 165 4,338

60490 Bolingbrook IL 0.12% 0.20% 30.47% 164 1,731

62467 Teutopolis IL 0.02% 0.04% 30.32% 164 347

61065 Poplar Grove IL 0.07% 0.12% 30.08% 162 1,040

60410 Channahon IL 0.09% 0.15% 30.04% 162 1,301

60432 Joliet IL 0.15% 0.25% 29.82% 161 2,159

62445 Montrose IL 0.01% 0.01% 29.76% 161 116

60505 Aurora IL 0.39% 0.63% 29.72% 160 5,572

61769 Saunemin IL 0.00% 0.01% 29.68% 160 67

60487 Tinley Park IL 0.18% 0.28% 29.55% 159 2,483

60623 Chicago IL 0.53% 0.85% 29.53% 159 7,472

62030 Fidelity IL 0.00% 0.00% 29.47% 159 13

60104 Bellwood IL 0.13% 0.20% 29.46% 159 1,765

60491 Homer Glen IL 0.15% 0.25% 29.42% 159 2,165

60442 Manhattan IL 0.07% 0.12% 29.41% 159 1,039

60639 Chicago IL 0.50% 0.79% 29.21% 158 6,992

60043 Kenilworth IL 0.02% 0.03% 29.05% 157 223

62365 Plainville IL 0.01% 0.01% 28.99% 156 70

60133 Hanover Park IL 0.23% 0.36% 28.96% 156 3,149

60423 Frankfort IL 0.20% 0.31% 28.88% 156 2,714

62462 Sigel IL 0.01% 0.01% 28.79% 155 115

60088 Great Lakes IL 0.03% 0.05% 28.79% 155 434

62063 Medora IL 0.01% 0.01% 28.59% 154 131

60175 Saint Charles IL 0.15% 0.23% 28.57% 154 2,026

60652 Chicago IL 0.25% 0.39% 28.39% 153 3,399

62218 Bartelso IL 0.01% 0.02% 28.29% 153 150

62206 East Saint Louis IL 0.12% 0.18% 28.26% 152 1,600

60145 Kingston IL 0.02% 0.03% 28.22% 152 256

60484 University Park IL 0.05% 0.08% 28.21% 152 692

60073 Round Lake IL 0.36% 0.55% 28.18% 152 4,828

60545 Plano IL 0.10% 0.16% 28.07% 151 1,384

60440 Bolingbrook IL 0.37% 0.56% 28.06% 151 4,890

60919 Cabery IL 0.00% 0.01% 28.06% 151 54

61011 Caledonia IL 0.02% 0.04% 28.05% 151 330

60632 Chicago IL 0.49% 0.74% 27.89% 150 6,524

60629 Chicago IL 0.63% 0.94% 27.85% 150 8,301

60448 Mokena IL 0.17% 0.26% 27.80% 150 2,309

62357 New Salem IL 0.00% 0.00% 27.79% 150 29

61010 Byron IL 0.06% 0.09% 27.72% 150 788

61020 Davis Junction IL 0.02% 0.03% 27.67% 149 286

61470 Prairie City IL 0.00% 0.01% 27.57% 149 49

60451 New Lenox IL 0.23% 0.33% 27.51% 148 2,943

61052 Monroe Center IL 0.01% 0.01% 27.49% 148 127

60164 Melrose Park IL 0.13% 0.20% 27.45% 148 1,755

60447 Minooka IL 0.09% 0.14% 27.44% 148 1,201

Geography Name

20 | P a g e

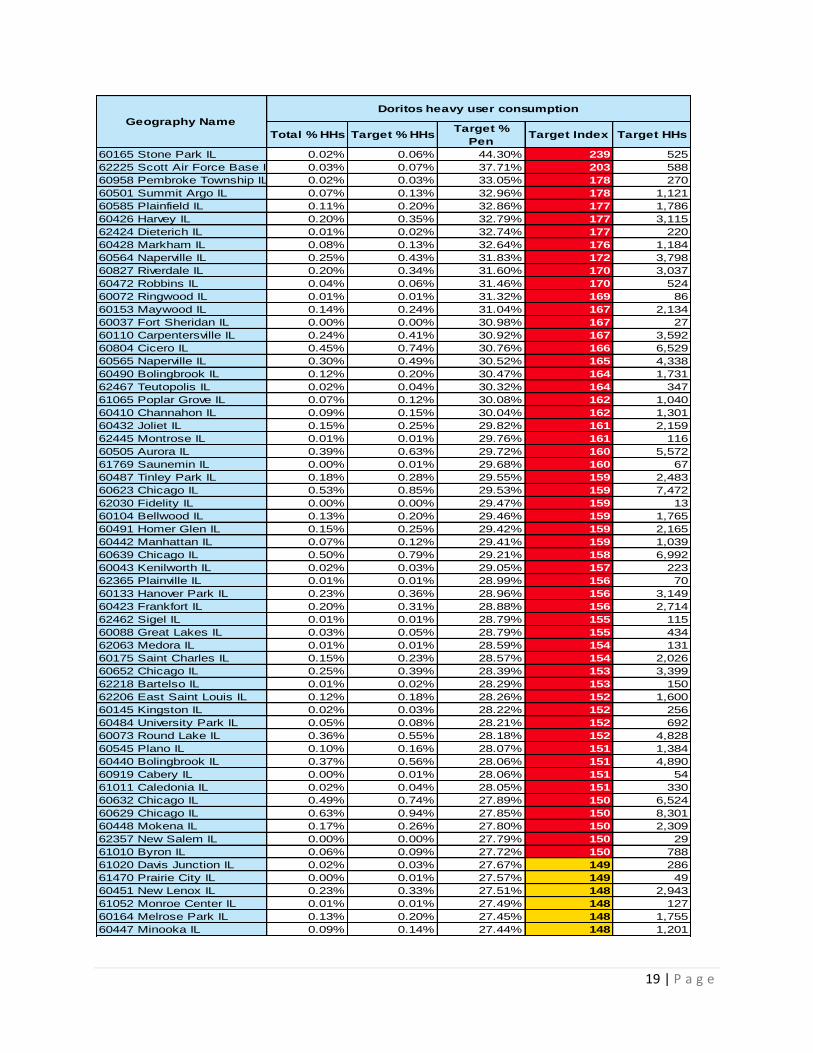

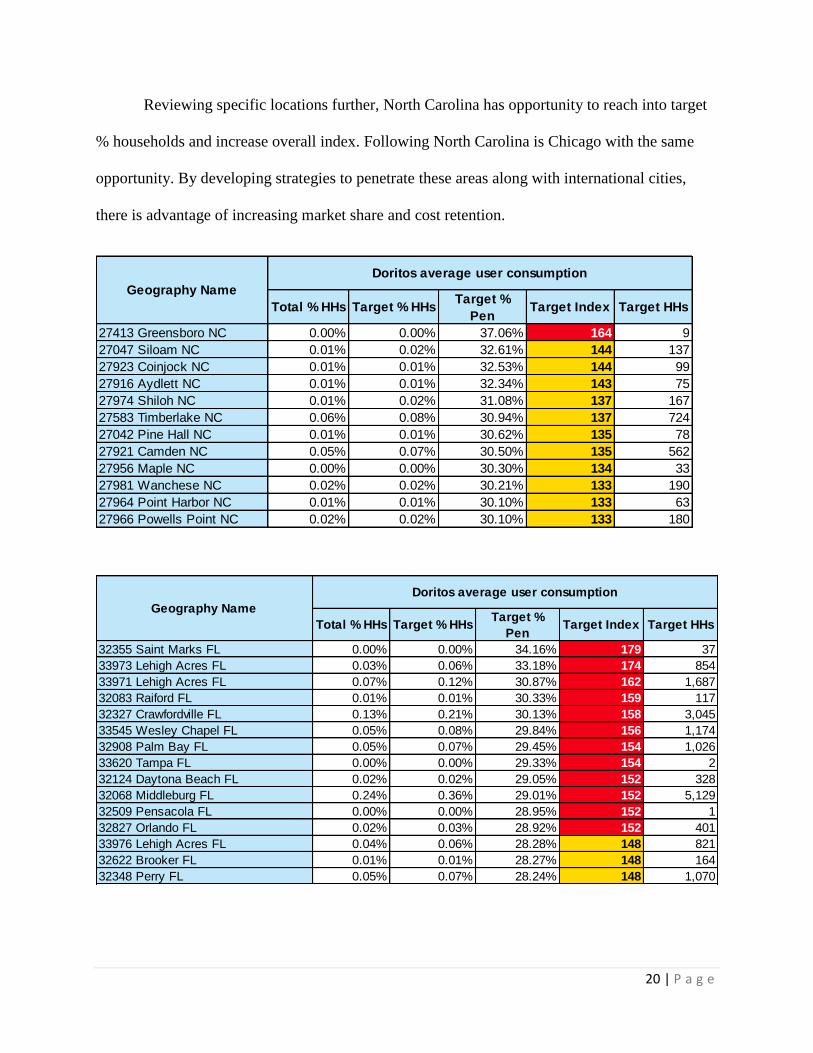

Reviewing specific locations further, North Carolina has opportunity to reach into target

% households and increase overall index. Following North Carolina is Chicago with the same

opportunity. By developing strategies to penetrate these areas along with international cities,

there is advantage of increasing market share and cost retention.

Doritos average user consumption

Total % HHs Target % HHsTarget %

PenTarget Index Target HHs

27413 Greensboro NC 0.00% 0.00% 37.06% 164 9

27047 Siloam NC 0.01% 0.02% 32.61% 144 137

27923 Coinjock NC 0.01% 0.01% 32.53% 144 99

27916 Aydlett NC 0.01% 0.01% 32.34% 143 75

27974 Shiloh NC 0.01% 0.02% 31.08% 137 167

27583 Timberlake NC 0.06% 0.08% 30.94% 137 724

27042 Pine Hall NC 0.01% 0.01% 30.62% 135 78

27921 Camden NC 0.05% 0.07% 30.50% 135 562

27956 Maple NC 0.00% 0.00% 30.30% 134 33

27981 Wanchese NC 0.02% 0.02% 30.21% 133 190

27964 Point Harbor NC 0.01% 0.01% 30.10% 133 63

27966 Powells Point NC 0.02% 0.02% 30.10% 133 180

Geography Name

Doritos average user consumption

Total % HHs Target % HHsTarget %

PenTarget Index Target HHs

32355 Saint Marks FL 0.00% 0.00% 34.16% 179 37

33973 Lehigh Acres FL 0.03% 0.06% 33.18% 174 854

33971 Lehigh Acres FL 0.07% 0.12% 30.87% 162 1,687

32083 Raiford FL 0.01% 0.01% 30.33% 159 117

32327 Crawfordville FL 0.13% 0.21% 30.13% 158 3,045

33545 Wesley Chapel FL 0.05% 0.08% 29.84% 156 1,174

32908 Palm Bay FL 0.05% 0.07% 29.45% 154 1,026

33620 Tampa FL 0.00% 0.00% 29.33% 154 2

32124 Daytona Beach FL 0.02% 0.02% 29.05% 152 328

32068 Middleburg FL 0.24% 0.36% 29.01% 152 5,129

32509 Pensacola FL 0.00% 0.00% 28.95% 152 1

32827 Orlando FL 0.02% 0.03% 28.92% 152 401

33976 Lehigh Acres FL 0.04% 0.06% 28.28% 148 821

32622 Brooker FL 0.01% 0.01% 28.27% 148 164

32348 Perry FL 0.05% 0.07% 28.24% 148 1,070

Geography Name

21 | P a g e

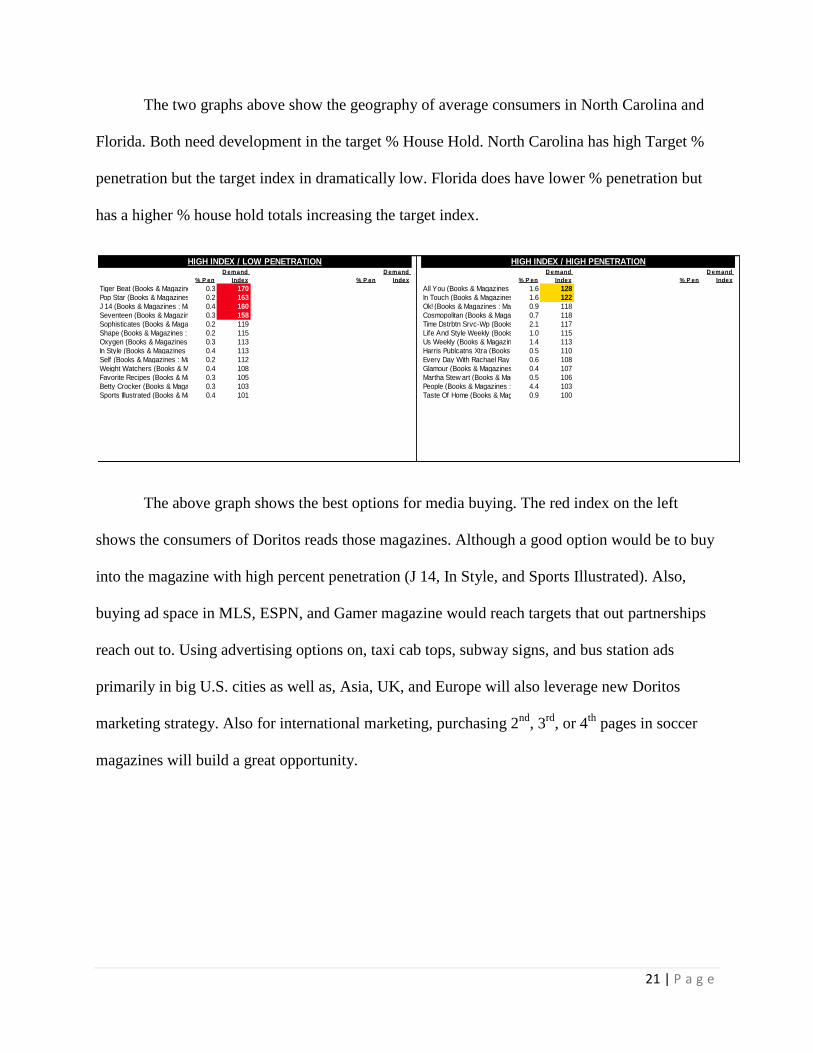

The two graphs above show the geography of average consumers in North Carolina and

Florida. Both need development in the target % House Hold. North Carolina has high Target %

penetration but the target index in dramatically low. Florida does have lower % penetration but

has a higher % house hold totals increasing the target index.

The above graph shows the best options for media buying. The red index on the left

shows the consumers of Doritos reads those magazines. Although a good option would be to buy

into the magazine with high percent penetration (J 14, In Style, and Sports Illustrated). Also,

buying ad space in MLS, ESPN, and Gamer magazine would reach targets that out partnerships

reach out to. Using advertising options on, taxi cab tops, subway signs, and bus station ads

primarily in big U.S. cities as well as, Asia, UK, and Europe will also leverage new Doritos

marketing strategy. Also for international marketing, purchasing 2nd

, 3rd

, or 4th

pages in soccer

magazines will build a great opportunity.

% P en

D emand

Index % P en

D emand

Index % P en

D emand

Index % P en

D emand

Index

Tiger Beat (Books & Magazines : Magzn Select Titles) Ct. ***0.3 170 All You (Books & Magazines : Magzn Select Titles) Ct. 1.6 128

Pop Star (Books & Magazines : Magzn Select Titles) Ct. ***0.2 163 In Touch (Books & Magazines : Magzn Select Titles) Ct. 1.6 122

J 14 (Books & Magazines : Magzn Select Titles) Ct. ***0.4 160 Ok! (Books & Magazines : Magzn Select Titles) Ct. *0.9 118

Seventeen (Books & Magazines : Magzn Select Titles) Ct. ***0.3 158 Cosmopolitan (Books & Magazines : Magzn Select Titles) Ct. **0.7 118

Sophisticates (Books & Magazines : Magzn Select Titles) Ct. ***0.2 119 Time Dstrbtn Srvc-Wp (Books & Magazines : Magzn Select Titles) Ct. 2.1 117

Shape (Books & Magazines : Magzn Select Titles) Ct. ***0.2 115 Life And Style Weekly (Books & Magazines : Magzn Select Titles) Ct. *1.0 115

Oxygen (Books & Magazines : Magzn Select Titles) Ct. ***0.3 113 Us Weekly (Books & Magazines : Magzn Select Titles) Ct. 1.4 113

In Style (Books & Magazines : Magzn Select Titles) Ct. **0.4 113 Harris Publcatns Xtra (Books & Magazines : Magzn Select Titles) Ct. **0.5 110

Self (Books & Magazines : Magzn Select Titles) Ct. ***0.2 112 Every Day With Rachael Ray (Books & Magazines : Magzn Select Titles) Ct. **0.6 108

Weight Watchers (Books & Magazines : Magzn Select Titles) Ct. **0.4 108 Glamour (Books & Magazines : Magzn Select Titles) Ct. **0.4 107

Favorite Recipes (Books & Magazines : Magzn Select Titles) Ct. **0.3 105 Martha Stew art (Books & Magazines : Magzn Select Titles) Ct. **0.5 106

Betty Crocker (Books & Magazines : Magzn Select Titles) Ct. **0.3 103 People (Books & Magazines : Magzn Select Titles) Ct. 4.4 103

Sports Illustrated (Books & Magazines : Magzn Select Titles) Ct. **0.4 101 Taste Of Home (Books & Magazines : Magzn Select Titles) Ct. *0.9 100

HIGH INDEX / LOW PENETRATION HIGH INDEX / HIGH PENETRATION

22 | P a g e

Budget

Calendar

Objectives Strategies Programs Tactics $1. • Gain 10% market share of healthy A. Market Positioning 1. Launch a healthier product 1. R&D 100,000

customers in 18 months. 2. Promotions 2. Engagement marketing 5,000

3. Holiday promotions 50,000

B. Follow healthier brands footsteps 1. Partnerships with healthier brands (Sun Chips, Kashi) 1. Integrated brand awareness

2. Partner with healthy activities 2. Sponsor Marathons 80,000

3. Sponsor high school athletics 50,000

Subtotal: $285,000

2. • Grow international sales by 15%. A. Expand with current partners 1. Sponsoring sports 1. In-game promotions 80,000

2. Sponsoring video games 2. Host Xbox competitions 100,000

3

B. Create more partnerships overseas 1. Tour De France 1. In game promotions 50,000

2. World Cup 2. On screen promotions 80,000

3. Give aways 20,000

Subtotal: $150,000

3.• International media awareness and coverage. A. Advertising 1. Print 1. Taxi tops (Chi, LA, NY,Miami,San Diego) 70,000

2. Other 2. Subway signs 50,000

3. Bus station ads 50,000

4. 2nd, 3rd, 4th page ads 100,000

B. Media coverage 1. International Magazines 1. MLS magazine 80,000

2. Commercials 2. EuroSport TV - ESPN Euro 100,000

3. ESPN Magazine 80,000

Subtotal: $710,000 4.ESPN TV 100,000

5. Gamer Magazine 80,000

ADDS TO STAFF 2 Events managers' 70,000

TOTAL: 1,395,000

jan feb march april may june july august sept oct nov dec

Considerations 1st Xbox Comp New Product Launch 31st MLS Season Starts 1st MLS ends

Social Media

FB 15th launch 25th kick off 1st xbox

Twitter 15th launch 25th kick off 1st xbox

Email 15th launch 20st kick off 20th xbox

website 15th launch 20th kick off 5th xbox

Target Ads

Taxi/Bus/subway Ads 20th launch 30th aug MLS kick off

MLS magazine 1st aug MLS kick off ad 20th xbox

Gamer magazine 20th xbox

Commercials 15th launch

23 | P a g e

Bibliography

http://www.warc.com/Content/ContentViewer.aspx?MasterContentRef=bb6918bd-a6aa-480b-

8246-5c5bb14383a8&q=doritos

http://www.warc.com/PDFFilesTmp/f6a05142-7a6c-498f-815b-71cb05ae4aaf.PDF

www.pepsico.com/company/our-mission-and-vision.html

http://ehis.ebscohost.com/ehost/detail?sid=3228ddd-1ffe-4c16-95 .html

http://finance.yahoo.com/q/ks?s=PEP

http;//bi.galegroup.com/global/company/40783