2012 fincom session 3

TRANSCRIPT

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 1/36

Reporting and financialcommunication - 3Skema - MSc Finance - 2012

p ! r convaincre vos pa " enair e message d’entreprise

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 2/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Agenda

Main targets, expectations and impact

1. Main targets and expectations

2. Periodical communication : case study

3. Impact of analysts forecasts

2

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 3/36

Main targets

and expectations

3

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 4/36

The public involved and its expectation

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

4

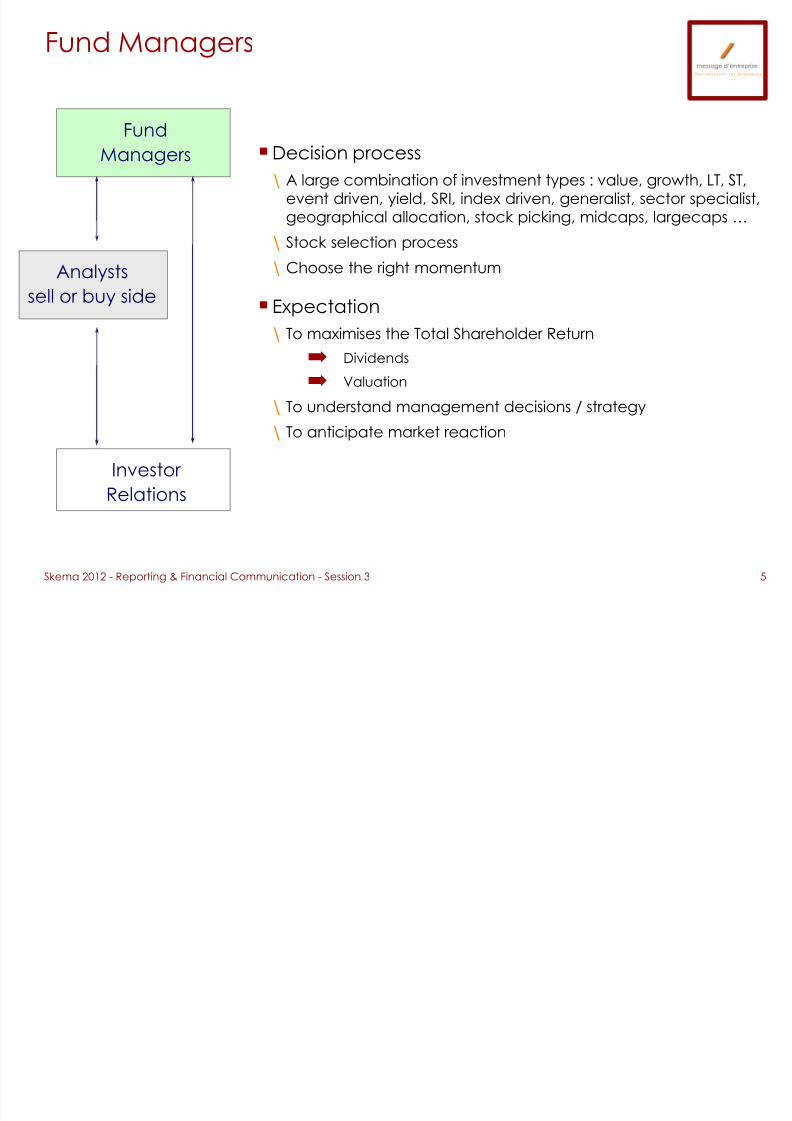

Funds Managers

Will take the final decision

Financial analysts « buy & sell side »

Recommendation to Fund managers

Individual shareholders / Employees shareholders

Banks

Rating agencies : credit, SRI

Press agency, journalists

Important source and relay of news

Internet sites : chat and forum

To have an eye on them : « watch for the rumour »

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 5/36

Decision process

\ A large combination of investment types : value, growth, LT, ST,event driven, yield, SRI, index driven, generalist, sector specialist,geographical allocation, stock picking, midcaps, largecaps …

\ Stock selection process

\ Choose the right momentum

Expectation

\ To maximises the Total Shareholder Return

➡ Dividends

➡ Valuation

\ To understand management decisions / strategy\ To anticipate market reaction

Fund Managers

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

5

Investor

Relations

Analystssell or buy side

FundManagers

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 6/36

An unavoidable market !

\ AUM US$170 billion in 1994

\ vs US$ 1,900 billion in 2010

Investment types

\ long/short equity, global macro, eventdriven, merger arbitrage …

\ Short selling process

Issuer interests

\ Different type of questions :more « direct to the point »

\ Could be more aggressive, dynamicdiscussion

\ To adapt the message in line with theinvestment type

\ To reduce the volatility on the stock

\ To limit the number of rumors

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

6

Focus : Hedge Funds

Hedge Fund Assets Under Management ($ billions)Source: HFR Industry Reports © HFR, Inc., Fourth Quarter 2010,

www.hedgefundresearch.com

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 7/36

ID

\ Market: ~ US$ 3,800 billion1 AUM in 2009

\ Highly concentrated :Top 10 have a 80% AUM market share

\ 75% are from Asia or Middle East

\ Directly or indirectly supervised by their respective government

\ Implemented to improve the return of StateReserves

Investment case

\ Bonds : 30%

\ Shares of listed stocks : 50/60%\ Others : 10/20%

Issuer interests

\ LT investment

\ An indicator for potential value

\ Passive shareholder / usually : no take over bidprocess

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

7

1 Source : FMI, OECD, FED / 2 source : Les Echos, Thomson One Banker, Fund

GIC - Singapore

Norwegian

Abu Dhabi

Samegeographical area

80%

50%

23%

Large cap.

55%

90%

80%

Focus : Sovereign Funds

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 8/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

8

Focus : SRI

ID\ European Market: ~ € 3,000 billion AUM in

2010vs € 1,033 billion in 2005

\ Active funds management

\ Mutual funds management

\ Management of employees profit sharingplan

Investment case

\ Exclusion strategy / social, environment or corporate governance theme

\ Rating agencies (Vigeo, Innovest, Eiris,

SIRI, trucost,…)

\ SRI index : FTS4good, DJSSI, Aspi, Ethibel,….

Issuer interests\ Specialised funds

\ LT investment

\ Brand name recognition

\ A different process : to fill in annualquestionnaires or dedicated presentation

0

1 500

3 000

4 500

6 000

2002 (EU 8) 2005 (EU 9) 2007 (EU 13) 2009 (EU 14)

Growth of SRI European Markets 2001-2009

B i l l i o n €

Source: Eurosif

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 9/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Fund managers: main concerns

Level of visibility / Level of risk

Market liquidity and market cap.

Volatility of share price

Understanding the business model\ How the company generates profit and cash

\ Which factors can impact the business model

Cash flow generation

\ Future cash flows condition the valuation

Management

Growth potential of the share price:is worth selling/ buying

9

‣ Strategic

‣ Personal

‣ Highly professional

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 10/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

10

Individual Shareholders

FINANCIAL

MARKET

Investor

Relations

Individual Shareholders

Highly segmented and heterogenous target

\ A dedicated team

\ Difficulties to identify shareholders

\ An expensive communication plan

A low impact and share price valuation

\ High stickiness

\ Employees profit sharing plan

Issuer interest

\ LT investors

\ Needed to reach a quorum at the AGM\ Management friendly in case of a take over bid

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 11/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Individual Shareholders: main concerns

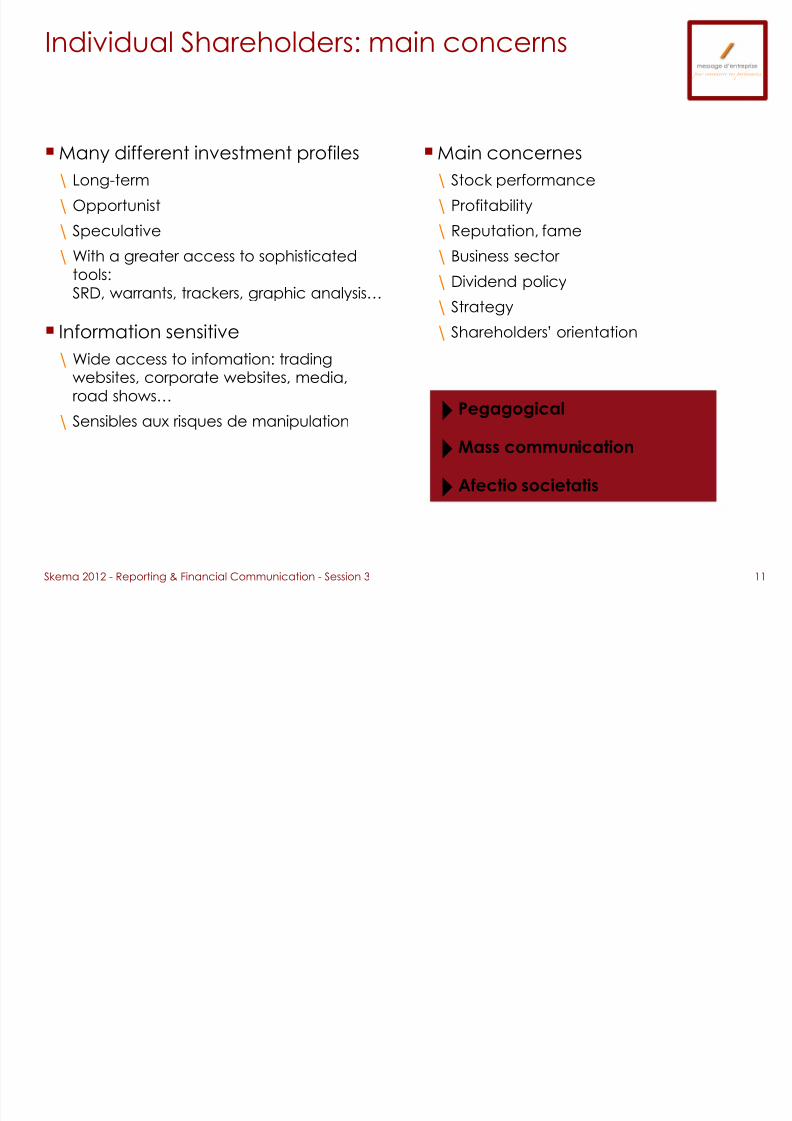

Many different investment profiles

\ Long-term

\ Opportunist

\ Speculative

\ With a greater access to sophisticated

tools:SRD, warrants, trackers, graphic analysis…

Information sensitive

\ Wide access to infomation: tradingwebsites, corporate websites, media,road shows…

\ Sensibles aux risques de manipulation

Main concernes

\ Stock performance

\ Profitability

\ Reputation, fame

\ Business sector

\ Dividend policy

\ Strategy

\ Shareholders’ orientation

11

‣ Pegagogical

‣Mass communication

‣Afectio societatis

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 12/36

Low awareness of financial anmarket mecanisms

\ Need for a simple and dedicatedcommunication

\ In messages and in communication tools

\ Jointly managed by CFO and HR\ Specific regulation framework

\ Relationship with Work council

\ Corporate investment plan regulation

\ High risks of information disclosure /conflict of interest

Main concerns

\ Strategy and forecast for the group andfor its subsidiaries

\ Dividend policy vs Social and wagespolicy

\ Tax and legal papers

\ Employees representativity

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Employee Shareholders: main concerns

12

‣ Pedagogy

‣ Specific tools: intranet, internal

letters, face-to-facecommunication…

‣ High probability of internal tensions

‣ Strong incentive for motivation andperformance

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 13/36

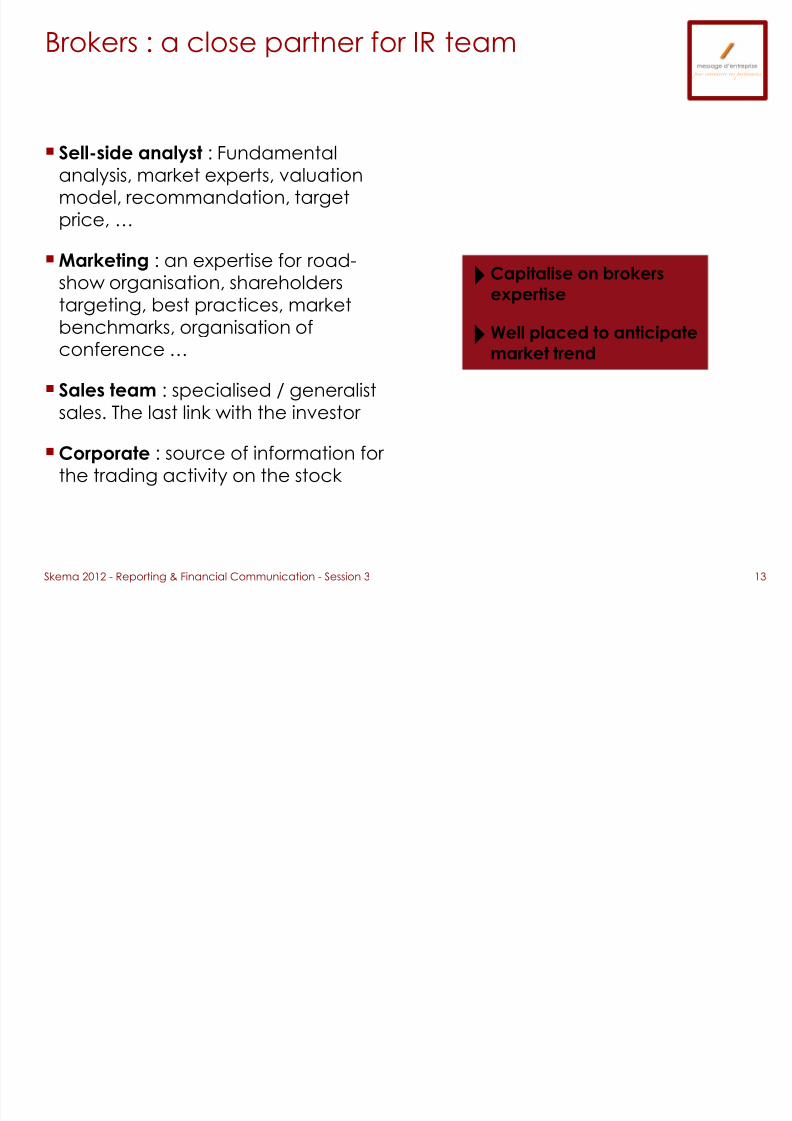

Sell-side analyst : Fundamentalanalysis, market experts, valuationmodel, recommandation, targetprice, …

Marketing : an expertise for road-

show organisation, shareholderstargeting, best practices, marketbenchmarks, organisation ofconference …

Sales team : specialised / generalist

sales. The last link with the investor

Corporate : source of information for the trading activity on the stock

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

13

Brokers : a close partner for IR team

‣Capitalise on brokersexpertise

‣Well placed to anticipatemarket trend

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 14/36

A powerfull guy/girl

\ 1st contact between the issuer and the broker firm

\ 1st source of information for investors

\ Direct impact on the stock price (recommandation /target price)

Market & sector expert

\ An in depth knowledge of the issuer and its competitivemarket

\ Information on investors needs / will

\ A more and more regulated and complex market

Highly concerned by his/her own credibilitytoward investors

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

14

Investor

Relations

FINANCIAL

MARKET

Sell-side

analysts

Brokers : Sell-side analyst

‣ To establish a win/winrelationship with the issuer

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 15/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Financial analysts: main concerns

Analysts missions

\ Analyser companies, sector, competitiveenvironment, prospects and results

\ Establish financial forecasts

\ Determine a fair value and compare itwith the actual stock price

\ Give an investment recommendation:strong buy, hold, sell…

\ Support marketing and dissemination ofthe analysis

\ Follow the company and the valuation

Main concerns

\ Sales and margin breakdown

\ Deep understanding of every accountingissue

\ Underlying hypothesis fof companyforecasts

\ Risks of failure

15

‣ Technical and detailed

‣ Personalised

‣Ongoing and proactive

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 16/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

16

Financial communication on debt

Why ?

\ To set up a fair and good relationship withbanks

\ To have access to a lower cost of debt

\ An interest for LT investors : liquidity risk ?Dividend level ?

\ To integrate a LT view in the valuation of thestock

\ HF needs : debt / equity arbitrage

Communication on :

\ Covenants

\ Liquidity : debt structure and amortizingprofile

\ Diversified financial sources (bond issue,bilateral credit line, …)

\ variable or fixe rate : sensibility to rateevolution / hedging

\ ratios (gearing, Net Debt/EBITDA, …)

Increasing interest from the marketin the context of limited access tocorporate funding

\ Rating agencies : S&P / Moodys / Fitch

\ The rating has a direct impact on thespread or cost of debt

‣ In the midst of a financial crisis :one motto : to be transparent

‣ Build a debt story along-side

the equity story

‣Deliver the same information tosell-side and credit analysts,equity or debt investors, creditrating agencies, banks

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 17/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Journalists : main concerns

Always in a rush and not alwaysexpert

\ Low financial background

\ Increased pressure due to media crisisand cost cutting among news companies

High impact, high risk

\ Journalists are totally free

\ They can make big misunderstanding or misleading resume

\ They can write even when you do notwant to talk to them

\ They prefer “late trains”

Main concerns

\ Competitive position

\ Strategic vision of top management,interview

\ Products and clients

\ Innovation\ Prospects

17

‣ Proximity

‣Ongoing and pedagogical

‣ Proactive and positive

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 18/36Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Other audiences

Employees, management, recruiting

\ Employee shareholders, stock options...

\ Corporate Brand image

Business, industrial and financialpartners

\ Customers, providers, sub-contractants,real estate owners…

\ Banks, credit insurance , leasingcompanies...

Competitors and competitiveauthorities

\ Publicly traded or not

\ Listing creates a distortion of thecompetitive environment

Civil society

\ Administrations, NGO’s,

\ Trade unions, lobbies

\ Consumers associations...

18

‣Anticipative

‣Specific

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 19/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

19

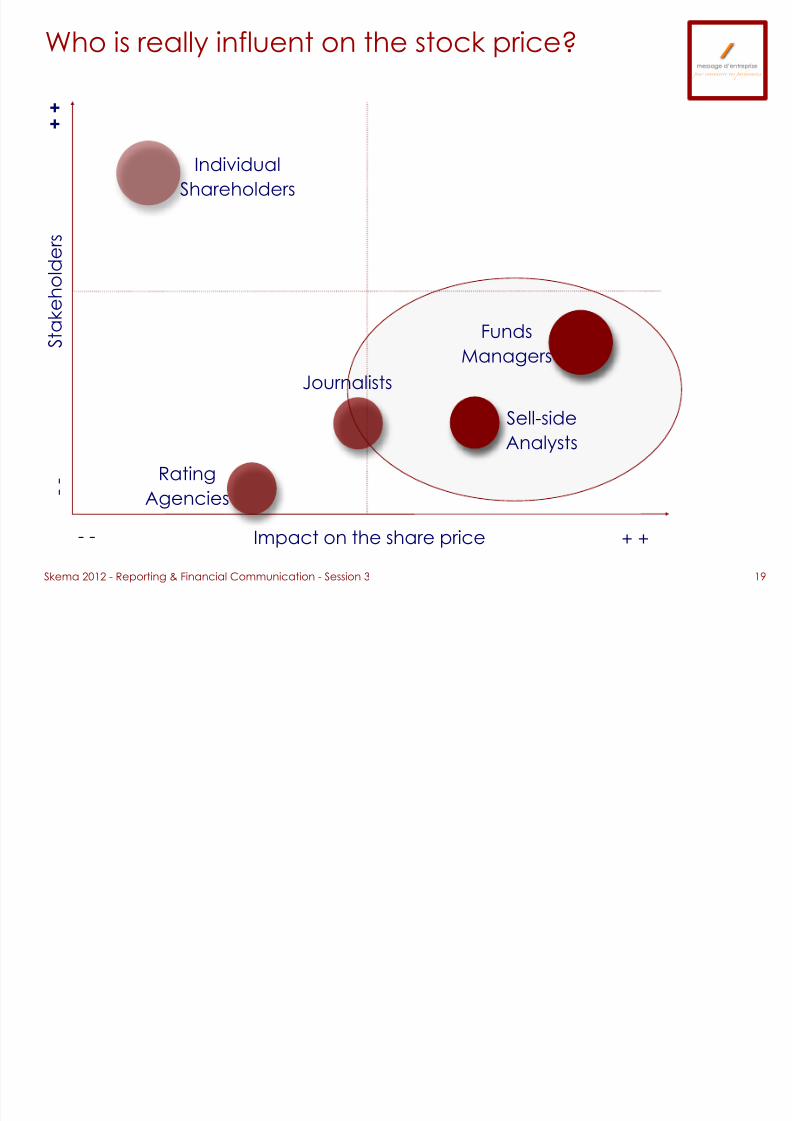

Sell-sideAnalysts

Funds

Managers

Individual

Shareholders

S t a k e h o

l d e r s

Impact on the share price- -

- -

+ +

+ +

Journalists

Rating

Agencies

Who is really influent on the stock price?

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 20/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

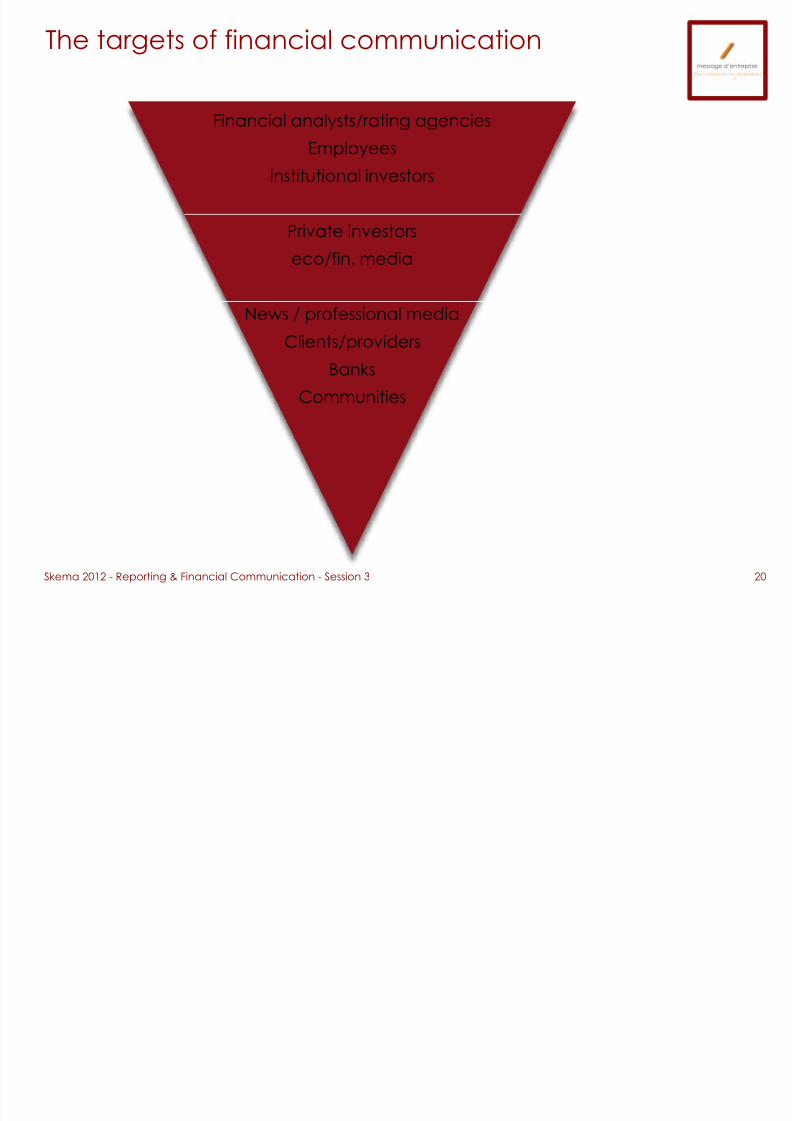

The targets of financial communication

20

Financial analysts/rating agencies

Employees

Institutional investors

Private investors

eco/fin. media

News / professional media

Clients/providers

Banks

Communities

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 21/36

Periodical communication :

case study

21

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 22/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Regulatory disclosure of financial results

22

Issuers shall inform the market on a regular basis, about:

\ corporate performance

\ changes in operational environment since the previous release

\ short and medium-term outlook

And shall guarantee fair access to information for every audience\shareholders or not

\professional or retail

\ local or international

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 23/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Information is used by market players with thepurpose of :

23

Adjust and update valuation models in accordance with actual corporateachievements and prospects

Assess what are the potential risks of the company not reaching targetedforecasts

Calculate the corporate / share fair value

Compare this value with the current share price

Make investment decisions:

\ purchase / sell, at which price ?

\ choose between the company stock and other comparable assets or other asset class

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 24/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Provisional FY financial results

Provisional annual results as approved by the Supervisory Board

\ Profitability: Group P&L

\ Financial soudness : Balance sheet and cashflow statements

\ Details : Group complete financial reporting

\ Outlooks and forecasts / guidance

Disclosure process

\ Press release: immediate and simultaneous dissemination

\ Analysts’ meeting: detailed presentation used as a key source for analysts’recommendationsPress conference: detailed presentation in order to get press coverage

\ Meetings with institutional investors:direct contacts to address every concerns and questions

24

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 25/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

FY financial results approved by the AGM

Financial results become definitive once approved by the Annual GeneralMeeting of shareholders

\ Approval of financial statements

\ Approval to the management team

\ Approval of dividend distribution policy

Disclosure process

\ Annual Financial report : legal request

\ Annual report : communication to general public, brand image

\ Reference Document : not legally requested, but eases the procedures for AMf certificationin the case of a market operation

\ Annual General Shareholders’ meeting

25

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 26/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

HY Group financial results

Interim results equivalent to the FY release

\ Same level of detail on financial statements as provided for FY consolidation

\ Except from Allocation of result (only once a year)

\ Outlook: generally an update on annual guidance and outlook previously released

Disclosure process

\ Equivalent to FY result process

\ With a lower “symbolic impact”

26

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 27/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Quarterly releases

Legal requirement: Quarterly disclosure on Turnover

\ As required by Transparency Directive:

detailed information per business segment

information on elements affecting business activity

\ Press release: immediate and simultaneous disclosure

\ Analysts conference call:allows to concentrate and share the answers on all questions at the same time

No requirement about full financial results

Although some companies do so

\ More complete image

\ Increased short-term prospective

\ Is correlated with best practises among the sector and the competitors

27

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 28/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Organisation and internal agenda

28

Example of a disclosure schedule in he case of a company releasing interiminformation

J-60 à J-5(1st July / 22nd August)

Consolidation processAudit of financial statements

Consolitation team + CFO + CEOExternal auditorsAudit committee

J-8 à J-4(18 / 22 August)

Analysis of financial performanceConception of messages

Communication materials design

Training with management, Q&A sessions

IR teamConsolitation team + CFO + CEO

External auditors

J-1(Monday, 25 August)

9h-12h : Board meeting16h00 : information to Work Council

18h00 : press release disclosure

CEO + CFO + BoardmembersExternal auditors

IR Team, HR

J

(Monday, 26 August)

08h30 : press conference11h00 : analysts meeting

13h00 : investors’ lunch15h-18h : RV One2One meetings with investors /

journalists

CEO + CFOIR Team

Communication team, PR, agencyBroker, analyst

J +1 to J + 17(Friday 12 Sept.)

Road show program,organised with the broker Follow-up of press clipping

Follow-up of analysts’ publications

CEO + CFOIR Team

Communication team, PR, agencyBroker, analyst

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 29/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

In theory, the market integrates any new information and re-assess hecompany / asset valuation (market efficiency)

\ Analysts update their forecasts and release new recommendations

\ Journalists put the information into perspective

\ Investors re-evaluate their investment position

In reality, sometimes, information may not have the expected impact

\ Confusing message, lacks of visibility

\ Lack of credibility of the issuer

\ Issuer’s newsflow is out of phase with the general or sectorial market environment

\ Information is hidden into a dense general newsflow

29

What is the impact

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 30/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Case study

Zodiac presentation FY 2010/2011

ID Midcap Research note about Zodiac disclosure

30

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 31/36

Impact of analysts forecasts

31

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 32/36

Analysts ratios and financial focus

\ Turnover breakdown by segment

\ EBIT / EBITDA

\ Net profit : reported / restated

\ EPS / PER

\ Others : Capex, change in workingcapital needs , FCF, net debt ...

Sector specificities

\ Programming costs : for a TV channel

\ Order book for constructing, aerospace,capital intensive companies

\ Number of active subs /ARPU / SAC /Churn for telecom or pay TV operators

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

32

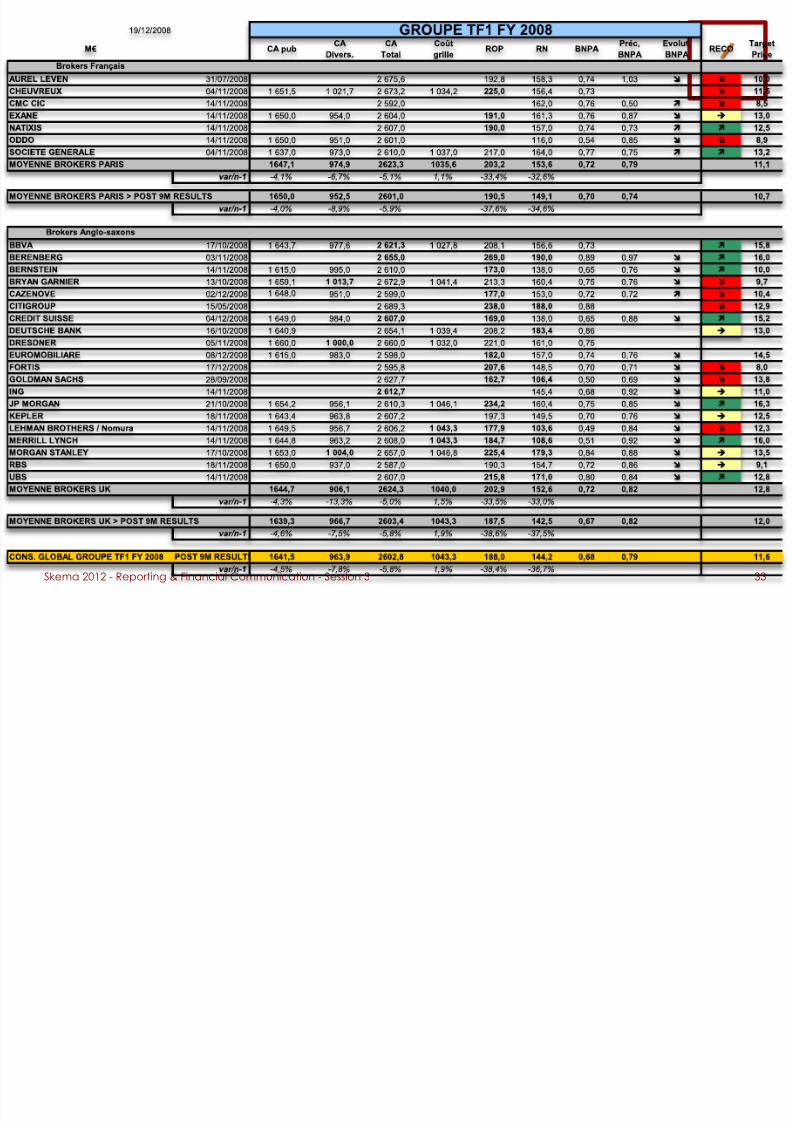

Consensus

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 33/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

33

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 34/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

Sell-side analysts and their impact on markets

Analysts are seen as financial experts and some of them are very popular among the media

Sell-side analysts and their impact on markets have been widely studied byacademics

Their impact on markets and prices\ Schipper, 1991: as information producers, thir main activity consists in analysing and selecting

companies and recommending their customers to sell/buy those companies

\ Womack, 1996: Analysts’ publications generate increases in transactions volume, namelywhen they change their recommendations

\ Easley, O’Hara, Paperman, 1998: analysts also have a positive effect on market liquidity as

they attract unsophisticated investors\ Brennan et Subrahmanyam, 1995: analysts’ publications tend to decrease asymmetry of

information for every market agents, even if these are not direct clients

\ Irvine, 2004 ; Jackson, 2005: thus, they allow the brokerage companies employing them toincrease their sales and profit

\ Brennan et Subrahmanyam, 1995: the consequence for investors clients is to reducetransaction costs related with the adverse selection dlemma

34

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 35/36

Skema 2012 - Reporting & Financial Communication - Session 3

p ! r convaincre vos pa " enair e

What is the real efficiency of analysts ?

Analysts are supposed to be able to predict the future value of assets

In reality, their recommendations impact on the very price of the asset

\ Womack (1996): a change in recommendation generates a change in asset price and thischange is persisting over the time

1 month for an upgrade

6 months for a downgrade

\ Stickel (1995): the impact on market is correlated with the reputation of the analyst and hisbrokerage company

And their forecasts are generally too optimistic

\ Francis et Philbrick (1993): analysts’ forecasts on Profit per Share are systematically optimistic

\ Rajan et Servaes (1997): in the case of an IPO, analysts’ forecast on growth prospects aresystematically optimistic

\ Easterwood et Nutt (1999): analysts under-react to bad news and over-react to good news

\ Trueman (1994): analysts tend to herding behaviours and their forecasts are systematicallyinfluenced by the sum of previous available forecasts

\ Womack (1996): analysts are reticent about downgrading companies they follow and adopt

a SELL recommendation35

8/3/2019 2012 FinCom Session 3

http://slidepdf.com/reader/full/2012-fincom-session-3 36/36

p ! r convaincre vos pa " enair e

Are the analysts irrational and inefficient ?

Some bias have been identified

\ Selection bias: as analysts are paid to make recommendations that generate increasedvolume transactions, they have an interest in following high potential stocks ie where theyare optimistic

\ Lim (2001): being optimistic is a way for analysts to have a better access to information fromcompany’s management

\ Michaely et Womack (1999): analysts are influenced by the necessity of corporate bankingto provide optimistic forecasts in the case of market operations (IPO…)

Companies may sometimes adapt their strategy in order to follow/ outperformanalysts recommendations

Financial analysts are quite not neutral in market efficiency and therelationship between companies and analysts is key