2012 results - laird plc · 2012 results 1 march 2013 1 . agenda 1. introduction and results...

TRANSCRIPT

2012 Results 1 March 2013

1

Agenda

1. Introduction and Results overview – David Lockwood

2. Financial performance - Jonathan Silver

3. Operational performance – David Lockwood

2

Our differentiation

3

Customer Mindshare

Innovation Reliable Fulfilment

Speed

2012 highlights: delivering growth

• Revenue up 6% on 2011

• Flat organic growth (in USD) with sequential improvements throughout 2012

• Underlying profit before tax up 17%

• Strong profit improvement from operational efficiencies and management of a

beneficial product mix

• Full year underlying earnings per share of 19.1 pence, up 18%

• Final dividend per share declared of 6.6 pence, total 2012 dividend of 10.0

pence, in-line with recommendations

4

5

Financial Performance

Jonathan Silver

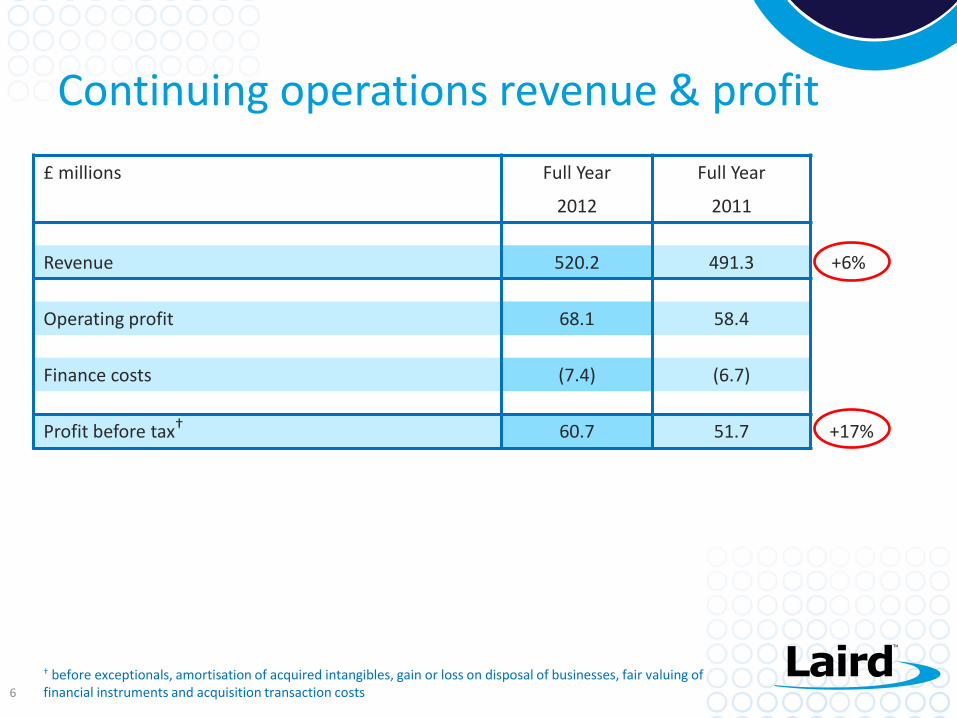

Continuing operations revenue & profit

6

£ millions Full Year Full Year

2012 2011

Revenue 520.2 491.3 +6%

Operating profit 68.1 58.4

Finance costs (7.4) (6.7)

Profit before tax† 60.7 51.7 +17%

† before exceptionals, amortisation of acquired intangibles, gain or loss on disposal of businesses, fair valuing of financial instruments and acquisition transaction costs

Segmental analysis in £ and US$

7

Actual 2012 £m

Actual 2011 £m

%

Δ Actual 2012 $m

Actual 2011 $m

%

Δ

Performance Materials (PM)

Revenue 324.7 305.0 +6% 514.4 489.5 +5%

Operating profit† 48.9 43.0 +14% 77.5 69.0 +12%

Wireless Systems (WS)

Revenue 195.5 186.3 +5% 309.7 299.1 +4%

Operating profit† 25.8 22.7 +14% 40.9 36.4 +12%

Unallocated costs (6.6) (7.3) (10.5) (11.7)

Total

Revenue 520.2 491.3 +6% 824.1 788.6 +5%

Operating profit† 68.1 58.4 +17% 107.9 93.7 +15%

† before exceptionals, amortisation of acquired intangibles, gain or loss on disposal of businesses and acquisition transaction costs

Margin performance

8

Actual 2012

Actual 2011

US$m US$m

Revenue 824.1 788.6

Cost of sales (494.1) (491.1)

Gross margin 330.0 40.0% 297.5 37.7%

SG&A (169.2) (160.4)

Gross R&D (58.0) 7.0% (49.7) 6.3%

Net capitalised development 5.1 6.3

Operating profit† 107.9 13.1% 93.7 11.9%

† before exceptionals, amortisation of acquired intangibles, gain or loss on disposal of businesses and acquisition transaction costs

• Stepping up R&D spend in 2012/2013

Performance Materials – revenue bridge

9

$21m

EMI

$15m Thermal

$489m

$514m

+6%*

-12%*

$14m

EMI acq

$1m

SIP

2%*

0

10

20

30

40

50

2009 2010 2011 2012

0

20

40

60

80

100

120

140

2009 2010 2011 2012

0

100

200

300

400

2009 2010 2011 2012

EMI

Thermal

Signal Integrity Products

* year on year organic growth in US$ † refers to Klüver acquisition made in 2011

• Performance Materials organic revenue growth was 1%

• Smartphones and tablet shielding principal driver of EMI growth

• Thermal revenues impacted by subdued Telecoms market

$4m

Thermal acq†

Year ended 31 December 2012 2011

($ millions) Year Year

Revenue 514.4 489.5 +5%

Operating profit† 77.5 69.0 +12%

Return on sales 15.1% 14.1%

Performance Materials Division

10

• $3m profit contribution from acquisitions

† before exceptionals, amortisation of acquired intangibles and acquisition transaction costs

$(2)m TELE/M2M

$299m

$310m

-1%*

-6%*

$m

WACS

$13m

M2M acq

Wireless Systems – revenue bridge

11 * year on year organic growth in US$

• Revenue on an organic basis 1% lower

• Good demand from the automotive and wireless infrastructure markets

• Weaker industrial and European market demand

0

40

80

120

160

200

2009 2010 2011 2012

0

20

40

60

80

2009 2010 2011 2012

Infrastructure Antennae

Telematics / M2M

0

20

40

60

80

2009 2010 2011 2012

Wireless Automation & Control Solutions

$13m

IAS

+25%*

$(4)m

WACS $(9)m TELE

Inventory transfer

Year ended 31 December 2012 2011

($ millions) Year Year

Revenue 309.7 299.1 +4%

Operating profit† 40.9 36.4 +12%

Return on sales 13.2% 12.2%

Wireless Systems Division

12

† before exceptionals, amortisation of acquired intangibles and acquisition transaction costs

• $2m profit contribution from acquisitions

• Margin improvement driven by vertical integration and product rationalisation

£ millions Discontinued Continuing Full Year

2012 2012 2011

Operating profit 1.5 68.1 59.4

Depreciation 13.5 17.0

Amortisation of capitalised development 5.3 6.4

Other and non-cash 1.8 1.3

1.5 88.7 84.1

Decrease / (increase) in working capital† 11.1 7.5 (0.3)

Capitalised development - (8.5) (9.1)

Capital expenditure (0.3) (13.3) (12.0)

Operating cash flow 12.3 74.4 62.7

Total 86.7

Strong cash conversion

13 † after adjusting for creditor decreases on exceptional items of £12.4m at 31 December 2012

• Cash conversion of 109 % (2011, 104%) from continuing operations

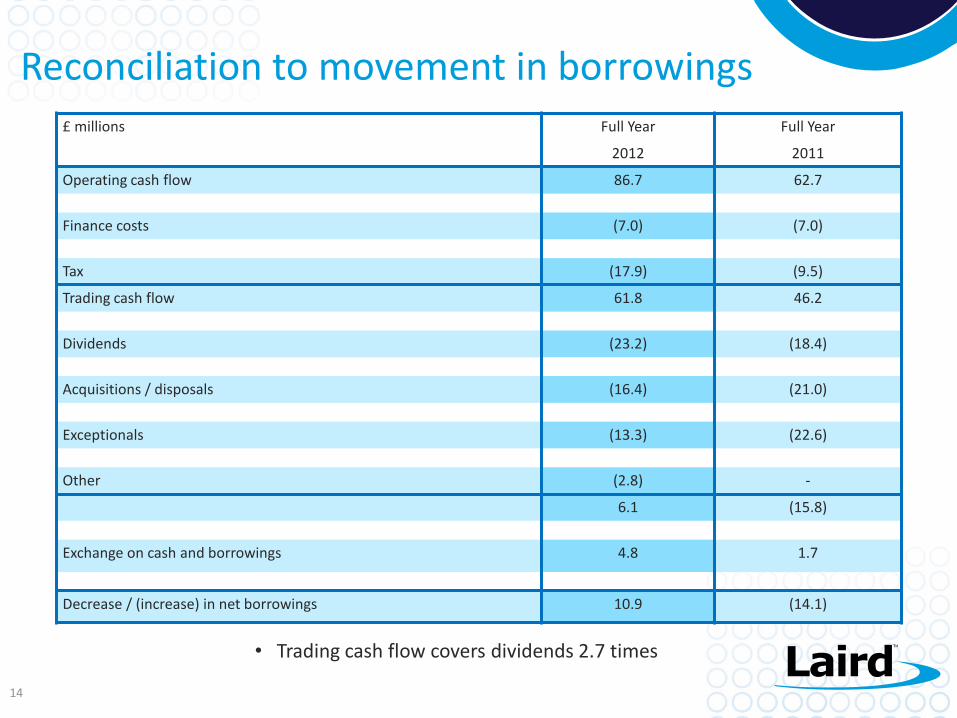

£ millions Full Year Full Year

2012 2011

Operating cash flow 86.7 62.7

Finance costs (7.0) (7.0)

Tax (17.9) (9.5)

Trading cash flow 61.8 46.2

Dividends (23.2) (18.4)

Acquisitions / disposals (16.4) (21.0)

Exceptionals (13.3) (22.6)

Other (2.8) -

6.1 (15.8)

Exchange on cash and borrowings 4.8 1.7

Decrease / (increase) in net borrowings 10.9 (14.1)

Reconciliation to movement in borrowings

14

• Trading cash flow covers dividends 2.7 times

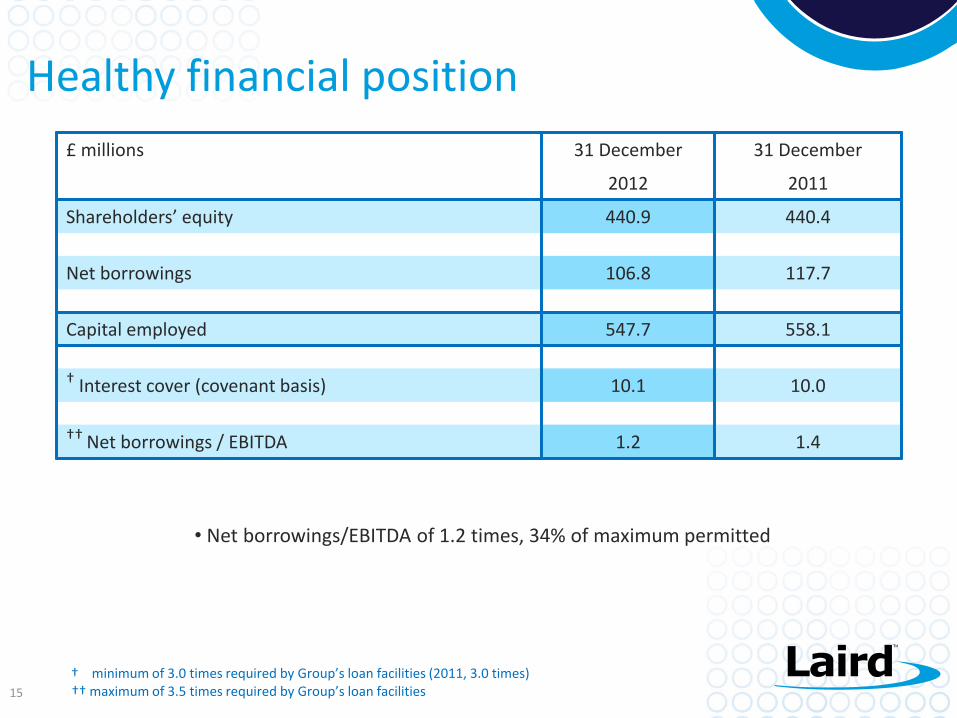

Healthy financial position

15

£ millions 31 December 31 December

2012 2011

Shareholders’ equity 440.9 440.4

Net borrowings 106.8 117.7

Capital employed 547.7 558.1

† Interest cover (covenant basis) 10.1 10.0

†† Net borrowings / EBITDA 1.2 1.4

† minimum of 3.0 times required by Group’s loan facilities (2011, 3.0 times) †† maximum of 3.5 times required by Group’s loan facilities

• Net borrowings/EBITDA of 1.2 times, 34% of maximum permitted

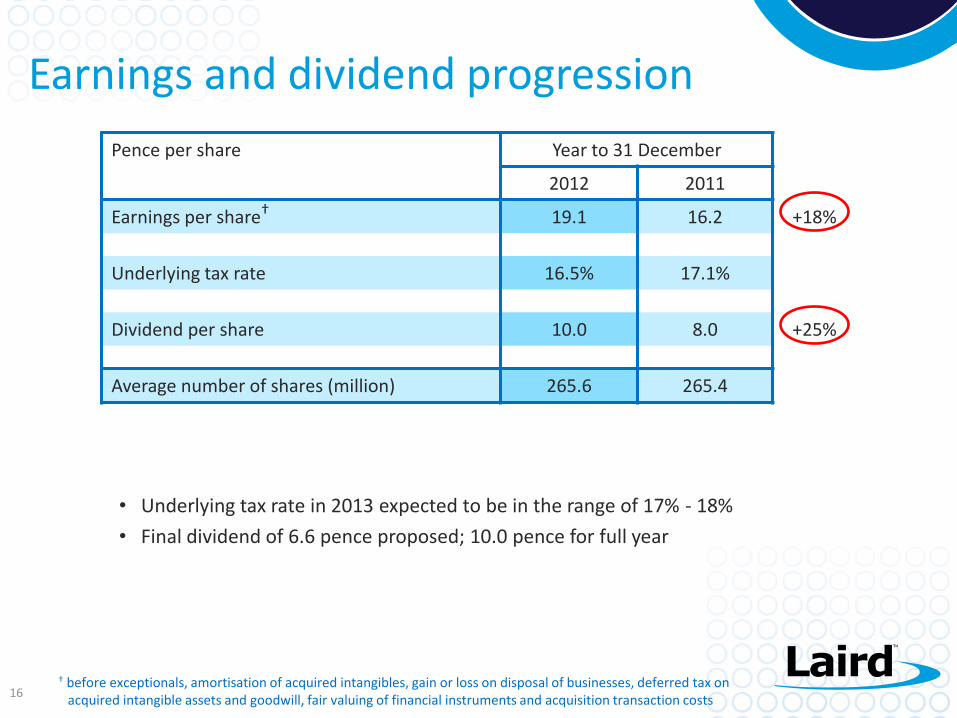

Earnings and dividend progression

16

Pence per share Year to 31 December

2012 2011

Earnings per share† 19.1 16.2 +18%

Underlying tax rate 16.5% 17.1%

Dividend per share 10.0 8.0 +25%

Average number of shares (million) 265.6 265.4

• Underlying tax rate in 2013 expected to be in the range of 17% - 18%

• Final dividend of 6.6 pence proposed; 10.0 pence for full year

† before exceptionals, amortisation of acquired intangibles, gain or loss on disposal of businesses, deferred tax on acquired intangible assets and goodwill, fair valuing of financial instruments and acquisition transaction costs

17

Operational Performance

David Lockwood

Laird’s differentiation

captured

Growth opportunities

identified

Operations aligned to refined Business Model

Growth Opportunities

• New segments in Industrial / Medical and Automotive

• Expansion in Automotive and Wireless Telecom

• Handset target one or two additional key OEMs

• Notebook strategic saturation and commoditization

Ind/Med/Mil Notebook Automotive -OEM

Handset Automotive -T1

Telecom -Wireless

Other IT Telecom -Wired

Tablet Consumer

Segment OEM Design Opportunity and Laird Penetration

Market Laird

USA RoEMEA Taiwan Germany Japan Korea China RoA RoAPAC Other

Regional OEM Design Opportunity and Laird PenetrationMarket Laird

* 'Other' represents broadly mixed geography

• Germany and Europe growth in new segments

• Expand current capabilities into China, Korea, and Japan through local OEM’s

A year of significant change

18

28%

11%

25%

3%

16%

11%

6%

IT / Telecom Industrial Transportation Medical

Handsets Other Consumer

Serving the right market segments

19

BY PRODUCT SEGMENT (%)

FY 2012 REVENUE £520.2m

BY MARKET SEGMENT (%)*

43%

14% 5%

22%

8%

8%

EMI Shielding

Thermal

Signal Integrity

Telematics / Wireless Modules

Infrastructure Antennae

Wireless Automation and Control

Performance Materials

Wireless systems

Performance Materials

Wireless systems

* % has been reclassified from Industrial to Transportation from H1 2012

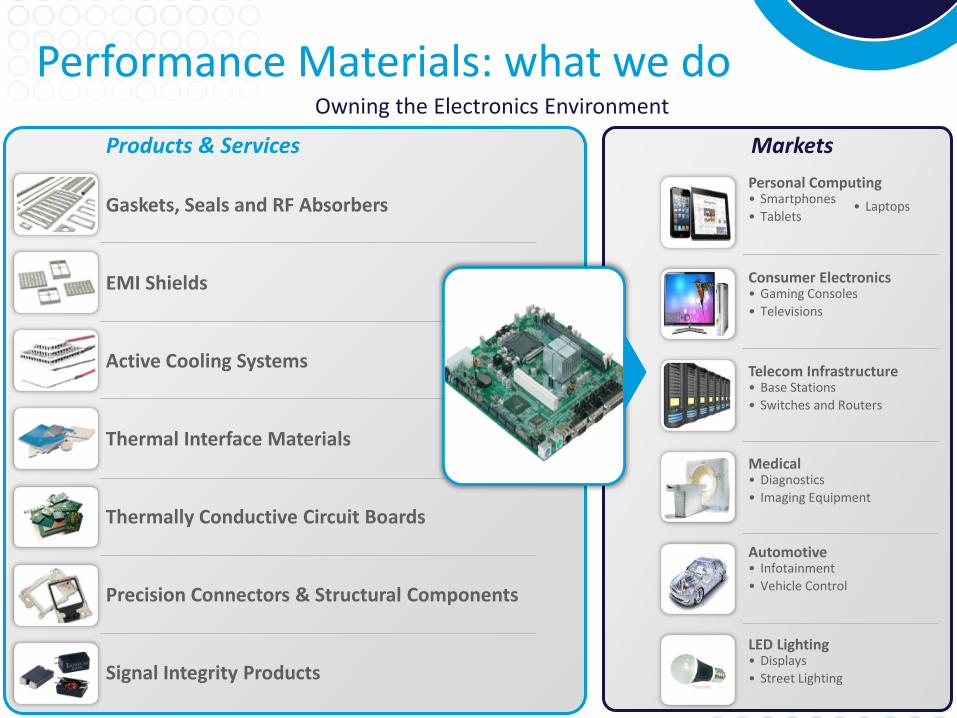

Performance Materials: what we do

20

Gaskets, Seals and RF Absorbers

EMI Shields

Active Cooling Systems

Thermal Interface Materials

Thermally Conductive Circuit Boards

Precision Connectors & Structural Components

Signal Integrity Products

Products & Services Markets

Personal Computing • Smartphones

• Tablets

Consumer Electronics • Gaming Consoles

• Televisions

Telecom Infrastructure • Base Stations

• Switches and Routers

Medical • Diagnostics

• Imaging Equipment

Automotive • Infotainment

• Vehicle Control

LED Lighting • Displays

• Street Lighting

• Laptops

Owning the Electronics Environment

Value ‘Sweet Spot’: Matching demand in Performance Materials

OEM Design

Contract Manufacture

Commodity • Available from many sources • Minimal differentiation • Minimal engineering required • Sales through distribution

System Core • Significant customer resource

to design and purchase • Large part of customer BOM • Specialised supply base • Typically capital intensive • Life-cycle driver

Custom Engineered • Capabilities enable design

freedom • Engineered customer cost saving • Low cost relative to core parts • Provide customer design resource • Short customer design time

DES

IGN

DES

IGN

DES

IGN

Component Supply

Well positioned to provide as devices become smaller, faster and higher powered

Client / Server applications

Antennas

Rechargeable Power

Embedded Radio Modules

Tracking Devices/Smart Antennas

Wireless Automation And Control

Products & Services

Transportation • Rail

• Automotive and commercial truck • Fleet management

Industrial • Heavy equipment and mining

• Material handling

• Energy and remote monitoring

Wireless infrastructure • WLAN

• Telecom (WWAN) • Public Safety

• Industrial and Commercial Wireless

Medical • Hospital equipment

• Home health care devices • Client Server application

Markets

Wireless Systems Enabling Wireless Communication

Turning data into insights and actions in real time – predictive and preventive thorough innovative Software solutions

Sensing, Connecting and collecting data to and from devices and systems of “all things” via embedded wireless and sensing technology

Improve wireless devices and system performance thorough antenna technology

Powering remote or handheld wireless communication devices

Enablement

Innovation in Wireless Systems

23

Smart 4G MIMO antenna for use in automotive global navigation and communication systems

Exi

stin

g

MA

RK

ET

Ne

w

Existing PRODUCT New

x

Bluetooth Low Energy (BLE) modules enable short range wireless connectivity for ultra-low power sensor applications. Launching in Q2 2013

Exi

stin

g

MA

RK

ET

Ne

w

Business Unit Roles

& Responsibility

Existing PRODUCT New

x

Business Unit Roles

& Responsibility

Innovation in Performance Materials

Thermal interface material used to cool microprocessors

Exi

stin

g

MA

RK

ET

Ne

w

Business Unit Roles

& Responsibility

Existing PRODUCT New

x

Robotic arm used in small part process assembly for smartphones and tablets

Exi

stin

g

MA

RK

ET

Ne

w

Business Unit Roles

& Responsibility

Existing PRODUCT New

x x

Acquisition of Nextreme

25

Thermal thin film energy harvesting

Exi

stin

g

MA

RK

ET

Ne

w

Business Unit Roles

& Responsibility

Existing PRODUCT New

x

• Year-long relationship with Nextreme

prior to acquisition

• Enabled us to test the market

• Deep understanding of the product

• De-risked the acquisition

• Innovative technology

• Enables us to move into complementary

new markets

Outlook

26

Innovation, reliable fulfilment and speed are key to delivering

future growth

Positioned in growth markets with

comprehensive product offering

Increasing investment on innovation through

disciplined R&D

Strategic direction for growth aligned to

selected markets, not OEMs

Confident in our ability to deliver on medium to long-term targets

Strong balance sheet 2013 revenue seasonally weighted to second half of the year

27

Q&A

28

Appendix

Business Model

29

Market Development

New segments to Laird

New geographies to Laird

Adjacent segments

Cross Business Unit

Mergers & Acquisitions

New Laird business

New geographic expansion

Business Unit strategic

Core Business

Customer and product focused growth

Technology Development

Organic business development

New Business Unit products

Division enables BU-Company and

Cross-BU interaction

E

xist

ing

MA

RK

ET

New

Existing PRODUCT New

Company Roles

& Responsibility

Business Unit Roles

& Responsibility

Margin trajectory model

30

PBIT 12

PBIT 20

IO 26

IO 31

Rev 100

Rev 133

ASSUMPTIONS

• No change in product mix

• 70% of costs variable, 30% fixed

• Variable moves with revenue, fixed with inflation

MODEL OUTPUT

• Profit drop through 25% on incremental revenue

• Revenue growth >30%; PBIT growth >60%

REV: Revenue IO: Indirect overheads PBIT: Profit before interest & tax

12.0% RoS 15.0%

Economies of scale from organic revenue growth

I N

D E

X

Performance Materials Division performance

31

• Revenue up 11% YoY • Strong demand for tablets & smartphones • Additional capacity expansion serving us well • Telecoms and IT markets remained subdued • Lower demand seen for some consumer electronics e.g. plasma display TVs

Supplying the Handset, IT,/datacom & automotive sectors

• Revenue down 8% YoY • Telecoms demand remained subdued • Some initial signs of demand improving

Supplying the IT/datacom, medical & consumer sectors

EMI Shielding

• Revenue up 2% YoY • IT & Printer sales remained weak • Maintained market position with the customers we serve [despite this]

Supplying the IT, consumer & automotive sectors

Thermal Solutions Signal Integrity

BY PRODUCT SEGMENT

69%

22%

9% EMI

Thermal

Signal Integrity

BY MARKET SEGMENT

• Revenue up 6% YoY • Organic revenue up 1% • Sequential growth in 2012 • Good margin improvements

2012 REVENUE £325m

35%

25%

23%

8% 5%

4% IT/Telecom

Handset

Other

Consumer

Medical

Transportation

• Revenue up 1% YoY • N.American auto market remained robust • M2M products rationalised to avoid more standardised areas • Vertical integration has helped improve margins

Supplying the transportation and industrial sectors

• Revenue down 6% YoY • Capital spend in rail markets has been deferred • Solid after-market revenues

Supplying the rail, industrial (transportation) and mining sectors

Telematics/M2M

• Revenue up 25% YoY • Strong demand from WLAN, RFID, cellular networks • Demand driven by increasing bandwidth requirements

Supplying the IT/datacom and industrial sectors

Wireless Automation & Control Solutions

Infrastructure Antennae

• Revenue up 5% YoY • Organic revenue 1% lower • Variable performance dependent on specific markets and geographies • Good margin improvements

2012 REVENUE £196m

57% 22%

21% Telematics & "M2M"

WACS

Infrastructure & otherantennae

BY PRODUCT SEGMENT

BY MARKET SEGMENT

Wireless Systems Division performance

32

58% 21%

17% 4%

Transportation

Industrial

IT/Telecom

Other

Measuring our strategic progress

33

Target: Medium to Long-term FY 2012 result

Organic revenue growth averaging 10% per annum

Flat/+1% in a low growth environment

Underlying return on sales margin of 15% 13.1% from operating efficiencies, product mix and vertical integration

Dividend per share of 10p for 2012 Total dividend of 10p declared