2012

TRANSCRIPT

To Our Business Partners

Each year we write this letter to you to discuss theresults of the past year and our plans and aspirations forthe future. We think of you as business partners whohave trusted us with your firm. Through this letter, we tryour best to tell you howwe think about your company,what happened over the course of the last year, andwhat you should expect of us in the year(s) to come.Wealso write this letter to our colleagues throughout Markelto provide a sense of perspective on how things havegone for the organization as a whole, and to provide asense of where we are going.

Well, partners, this has been one heck of a year. 2012was busy. More things went on this year than any inrecent memory. There is a long list of things weaccomplished. We’ve also got a full slate of ongoinggoals in place, and actions taken to build the future ofyour company.

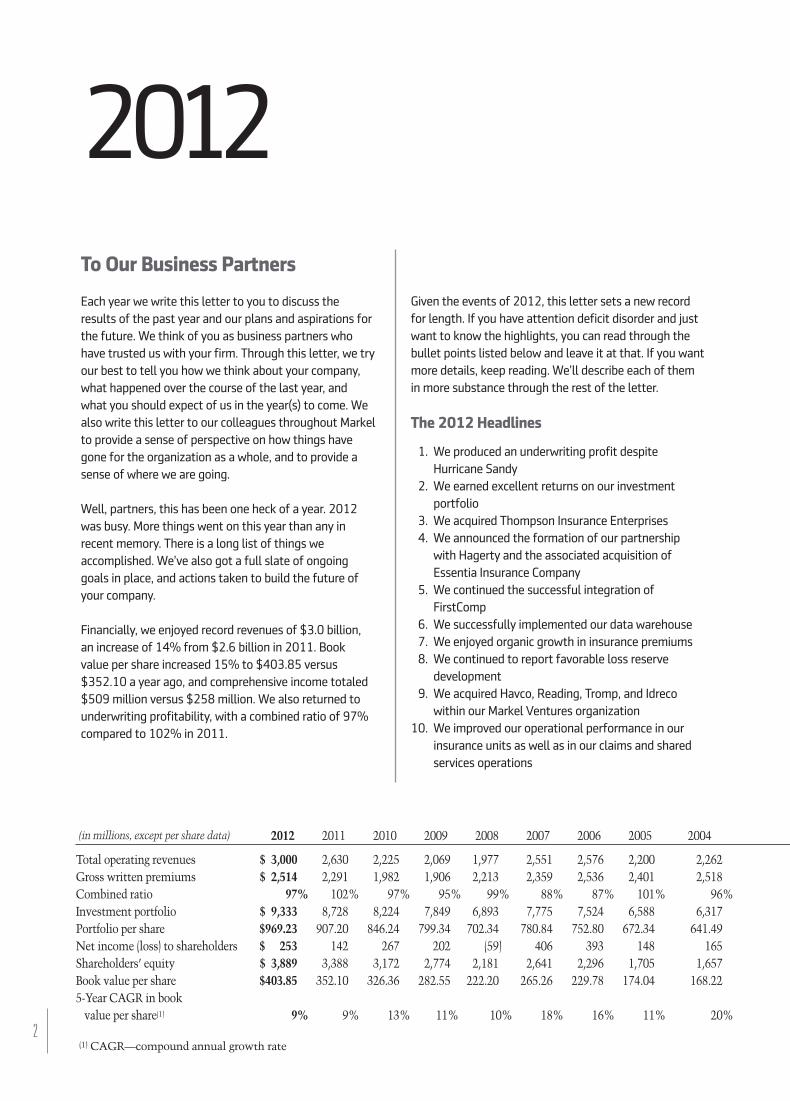

Financially, we enjoyed record revenues of $3.0 billion,an increase of 14% from $2.6 billion in 2011. Bookvalue per share increased 15% to $403.85 versus$352.10 a year ago, and comprehensive income totaled$509million versus $258million. We also returned tounderwriting profitability, with a combined ratio of 97%compared to 102% in 2011.

2

Given the events of 2012, this letter sets a new recordfor length. If you have attention deficit disorder and justwant to know the highlights, you can read through thebullet points listed below and leave it at that. If you wantmore details, keep reading. We’ll describe each of theminmore substance through the rest of the letter.

The 2012Headlines

01. We produced an underwriting profit despiteHurricane Sandy

02. We earned excellent returns on our investmentportfolio

03. We acquired Thompson Insurance Enterprises04. We announced the formation of our partnership

with Hagerty and the associated acquisition ofEssentia Insurance Company

05. We continued the successful integration ofFirstComp

06. We successfully implemented our data warehouse07. We enjoyed organic growth in insurance premiums08. We continued to report favorable loss reserve

development09. We acquired Havco, Reading, Tromp, and Idreco

within our Markel Ventures organization10. We improved our operational performance in our

insurance units as well as in our claims and sharedservices operations

2012

(1) CAGR—compound annual growth rate

Total operating revenuesGross written premiumsCombined ratioInvestment portfolioPortfolio per shareNet income (loss) to shareholdersShareholders’ equityBook value per share5-Year CAGR in bookvalue per share(1)

2012

$ 3,000%$ 2,514%

97%$ 9,333%$969.23%$ 253%$ 3,889%$403.85%

9%

2011

2,630%2,291%102%

8,728%907.20%

142%3,388%

352.10%

9%

2010

2,225%1,982%

97%8,224%

846.24%267%

3,172%326.36%

13%

2009

2,069%1,906%

95%7,849%

799.34%202%

2,774%282.55%

11%)

2008

1,977)%2,213)%

99%)6,893)%

702.34)%(59)%

2,181)%222.20)%

10%

2007

2,551%2,359%

88%7,775%

780.84%406%

2,641%265.26%

18%

2006

2,576%2,536%

87%7,524%

752.80%393%

2,296%229.78%

16%

2005

2,200%2,401%101%

6,588%672.34%

148%1,705%

174.04%

11%

2004

2,262%2,518%

96%6,317%

641.49%165%

1,657%168.22%

20%

(in millions, except per share data)

underwriting profits occurred duringmajor headlinecatastrophes such as theWorld Trade Center attack,Hurricane Katrina and sometimes, as anticipated, in thewake of major acquisitions which required changing theunderwriting culture at acquired firms.

The good news is that each of those events, whilepainful, taught us something, and we learned to bebetter at managing risks and running your company.Each of these “learnings” caused us to reexamine ourprocesses and assumptions and to improve them goingforward. Each challenge caused us as individuals, and asteams, to figure out how to improve and find newwaysto succeed.

The fact that we earned an underwriting profit this yeardespite Hurricane Sandy speaks to howwe’ve learnedand improved our underwriting process. The losses fromSandy were within our risk tolerances. We served ourpolicyholders by providing insurance coverage, and weearned a profit while doing so. That is a “win-win”situation for all involved.

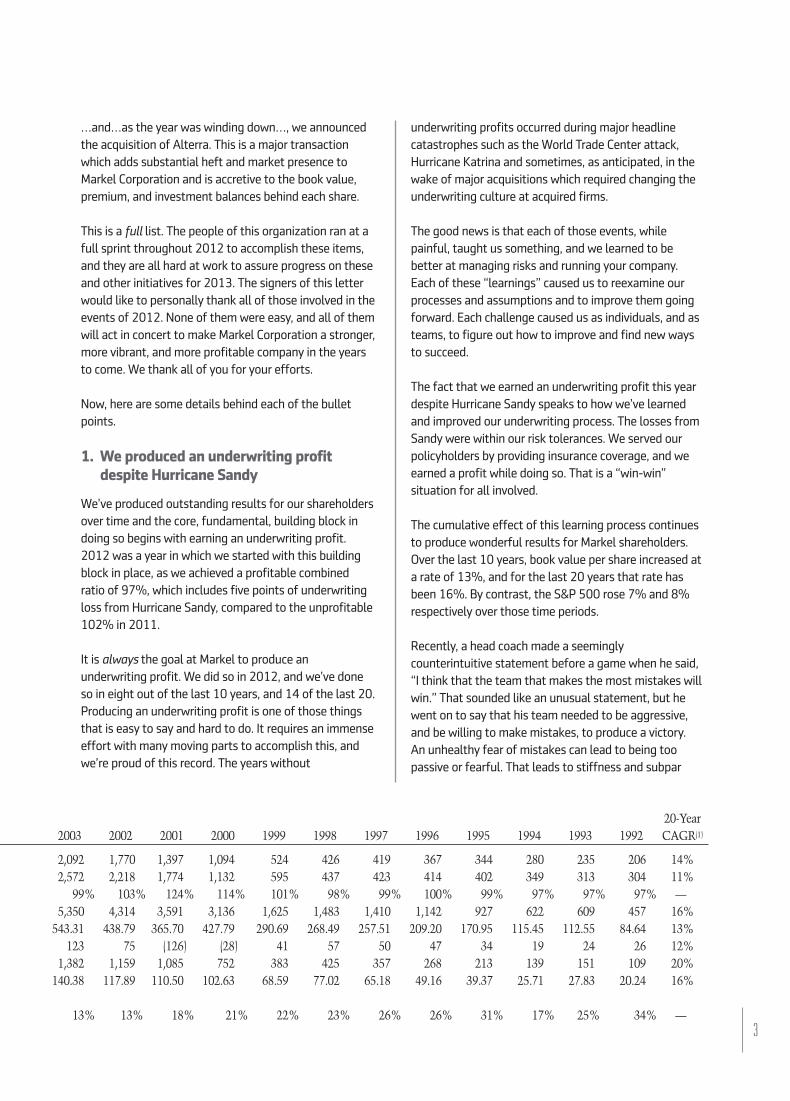

The cumulative effect of this learning process continuesto produce wonderful results for Markel shareholders.Over the last 10 years, book value per share increased ata rate of 13%, and for the last 20 years that rate hasbeen 16%. By contrast, the S&P 500 rose 7% and 8%respectively over those time periods.

Recently, a head coachmade a seeminglycounterintuitive statement before a gamewhen he said,“I think that the team that makes themost mistakes willwin.” That sounded like an unusual statement, but hewent on to say that his team needed to be aggressive,and be willing tomakemistakes, to produce a victory.An unhealthy fear of mistakes can lead to being toopassive or fearful. That leads to stiffness and subpar

…and…as the year was winding down…, we announcedthe acquisition of Alterra. This is a major transactionwhich adds substantial heft andmarket presence toMarkel Corporation and is accretive to the book value,premium, and investment balances behind each share.

This is a full list. The people of this organization ran at afull sprint throughout 2012 to accomplish these items,and they are all hard at work to assure progress on theseand other initiatives for 2013. The signers of this letterwould like to personally thank all of those involved in theevents of 2012. None of themwere easy, and all of themwill act in concert tomakeMarkel Corporation a stronger,more vibrant, andmore profitable company in the yearsto come.We thank all of you for your efforts.

Now, here are some details behind each of the bulletpoints.

1. We produced an underwriting profitdespite Hurricane Sandy

We’ve produced outstanding results for our shareholdersover time and the core, fundamental, building block indoing so begins with earning an underwriting profit.2012was a year in which we started with this buildingblock in place, as we achieved a profitable combinedratio of 97%, which includes five points of underwritingloss fromHurricane Sandy, compared to the unprofitable102% in 2011.

It is always the goal at Markel to produce anunderwriting profit. We did so in 2012, and we’ve doneso in eight out of the last 10 years, and 14 of the last 20.Producing an underwriting profit is one of those thingsthat is easy to say and hard to do. It requires an immenseeffort withmanymoving parts to accomplish this, andwe’re proud of this record. The years without

3

2003

2,092%2,572%

99%5,350%

543.31%123%

1,382%140.38%

13%

2002

1,770%2,218%103%

4,314%438.79%

75%1,159%

117.89%

13%)

2001

1,397)%1,774)%124%)

3,591)%365.70)%

(126)%1,085)%

110.50)%

18%)

2000

1,094)%1,132)%114%)

3,136)%427.79)%

(28)%752)%

102.63)%%

21%

1999

524%595%101%

1,625%290.69%

41%383%

68.59%

22%

1998

426%437%98%

1,483%268.49%

57%425%

77.02%

23%

1997

419%423%99%

1,410%257.51%

50%357%

65.18%

26%

1996

367%414%100%

1,142%209.20%

47%268%

49.16%

26%

1995

344%402%99%

927%170.95%

34%213%

39.37%

31%

1994

280%349%97%

622%115.45%

19%139%

25.71%

17%

1993

235%313%97%

609%112.55%

24%151%

27.83%

25%0

1992

206%304%97%

457%84.64%

26%109%

20.24%

34%

20-YearCAGR(1)

14%11%—%%16%13%12%20%16%

—%%

results. It is important to be willing to act positively, andaccept reasonablemistakes, so that the organization canlearn, and grow, and deal with a rapidly changing world.

We do that at Markel, and we think that this willingnessto take personal responsibility, admit errors, learn, andmove forward is a unique competitive advantage forthe company.

The first key to our consistency in earning underwritingprofits is our discipline and our unwavering commitmentto this standard.We are all long-term partners in Markel,and we don’t willingly accept any underwritingproposition which we think carries the likelihood of anunderwriting loss. While wemay not get this right all ofthe time, we start out with the advantage of a clearsense of purpose. No underwriter in Markel receivesincentive compensation unless his or her book ofbusiness produces an underwriting profit. Furthermore,that is not just a one year assessment, but amulti-yearview. Long-term risks require long-termmeasurement,and we reward our talented underwriters only when wehave reasonable certainty that their books of businessare indeed profitable over time. We are confident thatour new Alterra colleagues, as well as the existingMarkel underwriting team, will enjoy professional andpersonal achievement by being part of a long-termwinning organization. We find that the best underwriterswelcome and enjoy this approach since it yields the bestprofessional outcomes possible for them. Underwritersat Markel are not asked to subsidize weaker performers.A great underwriter will do better at Markel than at otherorganizations that do not have such a firm commitmentto underwriting profitability.

Wewelcome our new colleagues fromAlterra, and weare confident that they will find that the long-termfocus, and rational nature, of Markel will be the bestpossible environment for them to realize theirprofessional potential.

2. We earned excellent returns on ourinvestment portfolio

During 2012, we earned a total return of 9% on ourinvestment portfolio. Our equity returns were 20% andour fixed income returns were 5%.We are very happywith these results, and we hope that you are as well.

The 2012 equity returns of 20% added to a long stringof excellent results. Over the last 10 years, we’ve earneda total equity return of 9% versus the S&P 500 index4

returns of 7% and for the last 20 years we earned 10%versus the index return of 8%.

Over the years, we’ve never made decisions based onour forecasts of what was ahead for the economy,governmental policies, tax rates, currency values,interest rates, technological changes or other incrediblyimportant but fundamentally unknowable futuredevelopments.

Instead, we’ve simply looked at individual companies,one at a time, and asked ourselves a few questions.By considering four basic types of questions aboutindividual companies and securities we try to developenough confidence tomake a decision.

Our first question is, “Is this a profitable business withgood returns on capital without using toomuch debt?”Second, we ask ourselves, “Is themanagement teamequally and sufficiently talented and honest?” Third, weask, “What are the reinvestment dynamics of thebusiness and how do theymanage capital?” and finallywe ask, “What is the valuation and what do we have topay to acquire ownership in the business?”

While these are four simple questions, the process ofthinking deeply about them tends to produce robustresults over time as demonstrated by our long-termrecord. Those questions also tend to encompassconsideration of some of themacroeconomic factorsthat tend to cause somuch worry and anxiety for somany investors.

Consider the first question of profitability and returns oncapital. The best andmost durable businesses in theworld are ones that serve their customers well.Profitability is a marker that says a business is servingits customers with products that they need and wantand that they are efficient and skilled enough in doing sothat there is ameasure of profit left over after all is saidand done.

If a business is not making an appropriate profit it meansthat either they are doing something that the customersdon’t particularly care about, or that they are not goodenough at the task to accomplish it in a cost effectivemanner. Neither one of those outcomes is good. As such,just thinking about the long-term profitability and returnon capital record of a business gives us a wonderfulinsight into whether the company is indeed serving itscustomers in a fruitful way.

The best marker to describe a successful long-termcompany is a long-term record of profitability and goodreturns on capital, and that is the first thing we look forin seeking equity investments in either our public orprivate equity investments.

Second, we think about the talent and integrity of themanagers running the business. If a manager hasintegrity but is short of talent, that manager may be avery nice person and a pleasant friend or neighbor.However, in the context of business, they can’t get thejob done and that will not produce a good economicoutcome. Similarly, if someone is talented but has anintegrity problem, theymight do something profitable inthe short run but it will fall apart in the fullness of time.

We look for these same attributes in all of our colleaguesinside Markel, in themanagers of the companies in ourpublic security portfolios, and themanagers of thecompanies we’ve acquired in our Markel Venturesoperations.

Third, we think about the reinvestment dynamics of abusiness. A wonderful business can take the profits itearns and reinvest them at similar or better returns overtime and compound value. Organic growth companieslike this are rare and hard to find and none of them lastforever. In this world, perfection is not attainable, but wetry to snuggle up as close to it as we can whenever wecan find it.

The second best business in the world is one that makesvery good returns on capital but cannot fully reinvest theprofits at similar rates. Those businesses are fine as longas themanagement team accepts the reality andallocates capital to other uses. In our public equityholdings we own several fine businesses whichmeet thisdefinition and paymeaningful dividends, repurchaseshares, or make good acquisitions. Also, within ourMarkel Ventures operations, several of our companiesmatch this profile.

When we own a controlling interest in a company likethis we canmake the capital allocation decisions and doso in a very tax-efficient manner. While we pay full taxesat any entity when theymakemoney, we cansubsequently re-allocate the earnings from any area ofMarkel to any other, all around the world. By contrast,when we earn passive income through the receipt ofdividends on our public equity portfolio, the payingcompanies paid taxes on their earnings and we pay a taxon the dividends received. By building the controlled 5

interests of Markel Ventures operations, we are able toeliminate this tax drag and increase the value of Markelwith less friction than would otherwise be the case.

Fourth, we think about the valuation wemust pay to buya company with the three lovely attributes we describedearlier. We’ve learned over the years, as Charlie Mungerfrom Berkshire Hathaway noted, that, “it is better to paya fair price for a great business than a great price for afair business.” Great businesses compound their valueover time while fair businesses wallow inmediocrity. Aslong as we find great businesses at reasonable prices,we’ll allocate your capital to owning them to the fullestextent possible. When great businesses sell forirrationally high prices, and sometimes they do, we’llbuild cash, continue to look elsewhere, and continue oursearch for long-term compoundingmachines that areotherwise known as common stocks of great businesses.

Finally, we are pursuing unusual tactics in our investmentstrategy in the current environment. We believe thatinterest rates are fundamentally too low. We expect thatwill change within the next few years and wewant to beprepared for the time when it does.

As such, we are letting our fixed income holdingsmatureand come closer and closer to turning into cash and cashequivalents. The investment yield from this is literallyalmost nothing so it is painful to be building cash.However, the investment yield of investing longer-termin fixed income is not muchmore. Just as an insuranceunderwriter needs tomake a good risk/reward decisionabout whether to accept a risk or not, wemust do thesame thing in our investment decisions. We’ve concludedthat we are not being paid adequately to assume the riskof owning longer-term fixed income securities so we areletting our cash balances build up.

We look forward to deploying this cash into longer-termand higher yielding investments when the opportunitiesinevitably present themselves. Meanwhile, we will wait.

At the same time, we continue to own a portfolio ofequity interests, both passively through our public equityholdings and actively through our build out of theMarkelVentures operation. We believe that our companiesrepresented by these holdingsmeet the four questiontest we discussed earlier and will prove to be durable andprofitable businesses into the future. With the Alterraacquisition the size of our portfolio will increasedramatically. The addition of this portfolio and thegrowing cash balances create a “coiled spring” that we

Markel Corporation

are looking to deploy and uncoil when opportunitiespresent themselves.

The fantastic news is that the opportunity costs fromtaking this approach are as low right now as they haveever been given the low level of interest rates. As we seethe “whites of their eyes” in investmentmarkets we havemore ammo to expend than ever before. This is a toughconcept to quantify but it represents one of themostdramatic capital allocation and value opportunities thathas ever existed at Markel.

Over time, we’ve compiled a record that should give yousome confidence wewill act rationally and produce goodresults for you as shareholders. Stay tuned for furtherdevelopments…

3. We acquired Thompson InsuranceEnterprises

In January of 2012we completed the previouslyannounced acquisition of Thomco. Thomco administeredapproximately 20 insurance programs in fields such asmedical transportation, senior living, childcare, fitnessclubs, pest control, inflatable rentals, and other specialtyinsurance lines. We’re bouncing up and downwith joywith the progress and benefits from this acquisitionso far.

Greg Thompson and Bob Heaphey of Thomco havealready broadened their roles during 2012. Gregassumed the role of President of Markel Specialty, andBob became theManaging Executive of Thomco.

Thomco is a classic example of howwe’ve added value toMarkel shareholders over the years and createdwonderful opportunities for the Thomco associates inthe process. Thomco controlled approximately $170million in insurance premiums and collected commissionincome in return.

As part of Markel, we’ve begun to underwrite thisinsurance through various Markel insurance companyentities. Wewill benefit from Thomco’s intellectualcapital as we earn the associated underwriting profitsfrom the business. Wewill also build investment assetsfrom the associated insurance reserves.

Additionally, just as has been the case in our otheracquisitions, the people of Thomco now have apermanent homewith permanent capital to run their

6

business. They also now enjoy broader cross selling andcareer opportunities than before.

4. We announced the formation of ourpartnership with Hagerty and theassociated acquisition of EssentiaInsurance Company

Hagerty is the premier insurance agency serving theclassic collector car and boat market. Essentia InsuranceCompany underwrites insurance exclusively for theHagerty customer base. We finalized the terms of ourpartnership with Hagerty during 2012 and we closed onthe acquisition of Essentia in January 2013.We are nowaccepting the underwriting risks produced by theHagerty organization.

McKeel Hagerty leads the second generation of theHagerty firm. This partnership between Hagerty andMarkel is yet another example of the value of thelong-term nature of Markel and our well knownconsistent focus on building durable businesses thatproduce excellent results over long periods of time.

The Hagerty family choseMarkel after extensive duediligence on their part to assure themselves that wewould be quality partners in their business which theybuilt over decades. The cognoscenti of the collectingworld know and trust the Hagerty organization tomeettheir specialized needs in the world of collectible autosand boats. Hagerty believed that Markel would be thebest possible partner to help them ensure that heritagecontinues into the future.

We are excited about the formation of this partnershipand we look forward to reporting on its progress in theyears to come.

5. We continued the successful integrationof FirstComp

We acquired FirstComp in October of 2010. It is ouroperating unit which provides workers compensationinsurance with a focus on smaller businesses. From thebeginning, we were impressed with their customerservice orientation, risk selectionmethodology,marketing skills, and use of technology.

Our initial plan at FirstCompwas to provide their salesforce with access to other Markel products which theycould then sell through their extensive agency network.

Additionally, we hoped to benefit from theirtechnological sophistication and improve our speed andefficiency throughout the rest of Markel. We expected aninitial period of underwriting losses at FirstComp as westrengthened their reserves towards the levels wetraditionally prefer at Markel and as we bore theexpenses of integration.

We’re happy to report that process has gonewell.FirstComp is a key contributor to increased gross writtenpremiums in 2012 andwe believe that the businessbeing written today is being priced to ultimately earn anunderwriting profit. Themarketing and technologyexpertise embedded in that organization is nowworkingon behalf of the entire Markel organization andwe arejust beginning to leverage the cross sell potential of over14,000 retail producers among FirstComp, Thomco andMarkel.

6. We successfully implemented our datawarehouse

This is amajor development.

The combination of the pace of technological change,the complexity of our business, and our history ofacquisitions withmultiple legacy systemsmade the taskof building a data warehouse challenging and thisaccomplishmentmarks a significant success.

During the second quarter of 2012, we went ‘live’ withourWholesale data warehouse. This was theculmination of amulti-year effort to consolidate all ofourWholesale data into one reporting environment.

The warehouse has improved our ability to leverage ourdata in a number of ways. First, it has improved ourreserving and pricing analyses, allowing us tomorequickly assess the profitability of our books of business.It has also dramatically improved our reportingcapabilities, making it easier to provide decision-makerswith the information they need tomanage their business.The warehouse also provides a platform for improvedanalytics, allowing us to drill down into our data andmore easily determine the profit/loss drivers.

Finally, the warehouse provides a platform fromwhichwe can expand these capabilities into other areas of thebusiness.

7. We enjoyed organic growth ininsurance premiums

We enjoyed, and we domean enjoyed, growth ininsurance premiums in 2012. In 2012, gross writtenpremiums totaled $2.5 billion, up 10% from $2.3 billionin 2011. Excluding premiums attributable toacquisitions, gross written premiums increased 6% in2012.

We believe the growth in our premium volume largelystems from our efforts to improve our internaloperations and our ability to serve our clients moreefficiently. We’ve also enhanced and refreshed ourproducts to provide greater value to our customers.

We’ve substantially increased our marketing efforts toreflect the breadth and depth of what we can offer tothemarketplace and we’ve worked to increase theawareness of theMarkel brand worldwide.

Organic growth was also driven bymodest priceincreases during the year. While we still believe that thegeneral level of insurance prices should be higher giventhe low level of interest rates and recurring investmentincome, we are pleased to see prices moving up ratherthan down. The underwriters throughout Markel havedone a great job of exercising underwriting discipline andachieving pricing improvements.

8. We continued to report favorable lossreserve development

In 2012we reported favorable reserve development of$399million. In every report you’ll ever see fromMarkel,which dates from the initial public offering in 1986,you’ll see the statement that our policy is to establishinsurance reserves at a level which is “more likely to beredundant than deficient.” This is a key underlying valueof Markel which goesmuch deeper than just the surfacefact of positive reserve development.

The policy creates a virtuous cycle that is a relativelyunique and a significant advantage for Markel comparedto the insurance industry in general. First, it fosters aculture of conservatism and discipline whichacknowledges reality rather than denying it. When youaremaking decisions it is always helpful (but often notfun or pleasant) to be dealing with real facts, andaccurate data, as compared to what you wish things

7

Markel Corporation

see the table on page 108.While many of theMarkelVentures operations are cyclical and dependent on theoverall economy, we are optimistic that we will achieveadditional growth in bottom line profitability in 2013and beyond.

Also, just as is the case in our insurance and otherinvestment operations, we will be opportunistic inresponding to and walking away from extreme prices. Aswe enter 2013, we do not expect to add substantial newacquisitions at Markel Ventures. Transaction prices arenowmoving up rapidly, and wewill wait for betteropportunities to show up before committing your capital.

Fortunately, we were able to add several businesses atattractive prices during 2012.We added Havco in April2012, and they are off to a great start. Havco is theleading supplier of wood flooring for the trailer part of atractor trailer, and we are delighted with theircontribution toMarkel. At Ellicott Dredge we addedIdreco, a Dutch based dredgemanufacturer. At ParkLandVentures we increased the size of our footprint by over30%. At Diamond Healthcare we opened amajor newtreatment facility inWilliamsburg, Virginia, and atPartner MDwe opened new offices and increased thenumber of physicians practicing with us by over 40%.

We also added Reading and Tromp to our existing AMFBakery systems operation. These acquisitions continueAMF’s process of becoming the preferred supplier ofbakery equipment to food companies around the globe.AMFwas the first company acquired byMarkel Ventures,and we now begin our eighth year of operations together.

While baking is not a rapidly growing industry, in 2013,AMF should produce revenues and earnings that are upmore than four fold since we bought the company in2005.While this multiple expansion includesacquisitions, it also, andmore importantly, reflects theadvantages we offer to our Markel Venture companies.

Specifically, when we showed up at AMF, we empoweredmanagement to take a long-term view, and we reduceddebt levels from those previously employed. Our goalwas simple - we wantedmanagement to focus onsatisfying their customers with the best possibleequipment and service levels, and we didn’t want to haveartificial pressures of near-term debt repayments and anunhealthy focus on short-term results to get in the wayof this clear and simple goal.

were like. In insurance, setting loss reserves involvesmaking predictions about the uncertain future. We knowthat we will not be precisely right about the exact levelof reserves needed. In the face of that reality what we dois tomake every effort to err on the side of caution.

Second, conservative reserving practices help our frontline underwriters make good decisions when it comes toquoting and pricing current business opportunities.Conservative loss picks help prevent underwriters frommaking inadvertent mistakes and underpricing newbusiness.

Third, conservative reserving practices help our claimsprofessionals as they seek to fairly and quickly settlelosses when unfortunate events occur to ourpolicyholders. No one enjoys having a loss. In the eventof a loss, we want to assist our policyholders as quicklyand as fairly as possible. By having conservative lossreserves set aside and ready for losses, our claimsprofessionals know that they can do their job for ourpolicyholders to the best of their ability and that seniormanagers will not wince at the payment of appropriateclaims.

Our history indicates that we’ve accomplished the goal ofconsistent conservatism in the setting of loss reservesover the years, and 2012was yet another year of thispolicy in action.

We’ve designed our incentive systems and we’ve spentyears getting to know, and test, and trust, the seniorleaders of this organization tomake sure that yourcompany is in the hands of people with a long-termorientation. If you want to test our resolve and fidelity inkeeping this pledge to you, keep checking on our annualreserve development. It is a hallmark of a consistent,conservative, and prudently managed insuranceorganization.

9. We acquired Havco, Reading, Tromp andIdreco within ourMarkel Venturesorganization

2012was an exciting year in the ongoing growth anddevelopment of our Markel Ventures operations.

Total revenues for the group grew to $489million versus$318million in 2011 and EBITDA grew to $60millionversus $37million a year ago. For a reconciliation ofMarkel Ventures EBITDA to net income to shareholders,

8

Ken Newsome and his team respondedmagnificently tothis charge, and they’ve been gainingmarket share andbuilding the company ever since. We think we’re justgetting started there.

Throughout Markel Ventures, our management teamsare working to build the recurring revenue andprofitability of their firms and we are delighted with theiroverall progress.

We also want to express our thanks and our pleasurewith themanagers who joined us when they sold us theirbusinesses. We have had NO turnover among the seniorleaders who’ve joinedMarkel Ventures since inception in2005.We think this speaks volumes about the claritywith which we’ve communicated our long-term goals andexpectations for the businesses we bought, and for thedesire of thesemanagers to be able to build greatcompanies unfettered by artificial constraints.

In many cases, thesemanagers don’t “need to” work but“want to” work and they do so because they are excitedand dedicated to our values, and to themission ofbuilding one of the world’s great companies.

This is nothing different than what is true in ourinsurance operations, TheMarkel Style, and ourmulti-generational history of a focus on durablelong-term values, pervades the operations at MarkelVentures, and attracts leaders whowant to be part ofthis company to accomplish great things.

We are not for everyone. Being part of Markel requires acommitment to long-term values and a level ofteamwork that doesn’t suit some personalities. Thatsaid, if you want to be in an environment where you canexcel, and be recognized and rewarded for doing so,Markel offers a unique opportunity.

With the scale created by the Alterra acquisition, ourability to continue to build Markel Ventures increases.Wewill be able to pursue larger opportunities, and wewill be an attractive buyer to a wider set of potentialsellers.

If you, or anyone you know, owns a business where theanswers to our four investment questions would begood, and they want to be part of this organization,please give us a call. We are always looking for goodpartners.

9

10.We improvedour operational performancein our insurance units aswell as in ourclaims and shared services operations

Organic growth of 6% in 2012 gross written premiums isan encouraging sign that demonstrates the value of ouroperational andmarketing improvement efforts thathave been underway in recent years.

Markel International, under the leadership ofWilliamStovin and his team produced outstanding underwritingresults with a combined ratio of 89% and at the sametime increased gross written premiums from $825million in 2011 to $888million in 2012. A lowercombined ratio on greater volume is as good as it gets,and we thank and applaud theMarkel International teamfor their results in 2012.

OurWholesale unit, under the leadership of John Lathamand his team, produced a combined ratio for the yearof 94% compared to 86% in 2011with gross writtenpremiums of $956million versus $893million a yearago. This continues a long-term history of superbperformance.

Our Specialty operation, now under the leadership ofGreg Thompson and his team, produced a combined ratiofor the year of 108% versus 109% in 2011with grosswritten premiums of $670million versus $572million ayear ago.

In all of our operations, we’ve focused on becomingeasier to deal with. We’ve developed web basedapplications, broadened our product array, andproactively marketed our growing product breadth anddepth to the global insurancemarketplace.

Additionally, our increasingly effective analytical effortsare enabling us to refine our risk appetite on newbusiness opportunities. We’re increasingly able tounderstand where, and why, we should be raising pricesto accept risks, and we’re able to also better understandwhere, and why, we can lower prices, attract additionalbusiness, and still earn appropriate returns.

In general, industry prices remain too low and the returnson capital for the insurance industry aremediocre. We’reproud of the fact that we’ve been able to increase thebook value per share at good rates despite this headwindthrough continuing disciplined efforts in insurance, aswell as better than average returns from our investingactivities, and our growingMarkel Ventures group.

Markel Corporation

We fully expect to be able to continue to earn goodreturns on your capital from the comprehensive activitiesof Markel Corporation. Economic activity and demand isincreasing and industry capital is not growing at highrates. The lines of supply and demand are headingtowards one another in a way that suggests insurancepricingmay improve rather than decline.

We’ll manage our operations to earn appropriate returnseven if the industry doesn’t cooperate, but we’ll enjoy aseason of higher overall insurance prices should thatcome to pass.

Alterra

As we noted at the beginning of this report, 2012was asfull and busy a year as any that we can remember. Justbefore year end, we added to our 2013 and beyond“to do” list by announcing the acquisition of Alterra. Partof what we hope to do in this letter is to welcome thetalented professionals of Alterra to theMarkel family.We are excited about the newMarkel Corporation thatcomes about as a result of this transaction and we lookforward to building on our legacy of excellent financialperformance with our existing and new colleagues.

This is a major transaction in the history of Markel andwe’d like to discuss our reasons for engaging in thisacquisition.

To state something obvious but important, Alterra is aquality insurance operation with a demonstrated trackrecord of excellent underwriting performance.Underwriting profitability and reserve integrity arehallmarks of their organization as demonstrated by theiryears of consistent underwriting excellence.

Unlikemany other insurance entity deals that Markel didin the past, this is not a troubled company with problemsto be fixed and a new culture to be installed. Alterra hasalready demonstrated the ability to produce a consistentrecord of underwriting profits.

We believe that by joining forces, both the existingMarkel organization and that of Alterra will be able toimprove performance. We believe that we will both bebetter off as one company, as opposed to what eitherone of us could achieve as stand alone entities.

Among the reasons for our optimism about thelong-term future of the combined entity is the fact thatthe new entity is a larger andmore important firm in the

global insurance world. Immediately, this moves us upthe ladder in terms of opportunities that we will see towrite business. Agents and producers look for themostefficient way to find coverage for their clients. The sizeand breadth of the combined entity will make it easierandmore efficient for agents and allow us tomeetmoreof our potential clients’ needs. We’ll seemore business,and we’ll be able to write more of the business we see.

Further, we’ll have a larger balance sheet which will bemore attractive to buyers of reinsurance and large globalinsurance programs. The combined entity will enjoy ahigher profile and be amore attractive market for biglimit insurance needs. We also will be able to optimizethe returns that Markel shareholders should earn byoffering our reinsurance and large account underwritersa culture of long-term underwriting profitability. Thismeans that they will be able to write more businesswhenmarketplace conditions are favorable and just asimportantly, if not more so, reduce writings and walkaway from business when the rewards don’t justifytaking the risks.

Wewill be a large enough and diverse enough and, moreimportantly, mentally prepared to walk away frombusiness when it is the right thing to do. This is whatwe’ve always done at Markel and this transaction is aforcemultiplier for the underwriting team at Alterra toimprove upon their already solid results.

This mindset of focusing on the long-term discipline ofonly writing business that carries with it the expectationof an underwriting profit, as well as the reality of a largerandmore secure balance sheet, will create a new andexpanded set of opportunities for Alterra associates andMarkel as a whole. Our new format shouldmake themost of the circumstances.

While we are pleased with the early days of a trendtowards improving our expense ratio, this transactionshould increase the rate at which we enjoy increasedoperating efficiency. Wewill be writingmore businesswith our existing infrastructure, and this should serve tolower our expense ratio in the years to come.

The transaction is immediately accretive to importantmetrics at Markel such as premiums, investments, andbook value per share of Markel. Wewill recast the Alterrainvestment portfolio towards that of Markel’s historicalapproach to investments, with our focus on prudentallocations to equities, ownership of controlledbusinesses, and a hawk like focus on extremely lowinvestmentmanagement costs.

10

The newMarkel offers all of our associates from ourexisting operations, as well as those of Alterra, newopportunities and challenges. While this is difficult toquantify, it is a huge factor in the long-term success ofyour company. We’ve taken on challenges before andwe’ve stepped up to tackle bigger and biggeropportunities as time has gone by. In each of thesecircumstances a wonderful virtuous circle took hold.

Specifically, many of our associates rose tomeet newchallenges and gained skills and abilities that one cangain only by actually doing the work. Also, manyassociates from the acquired companies showed theirskills and abilities and rose to new and broader roleswithin Markel over time.

The effect of this process is that the talent level, andbench strength, and skills of the organization continue toimprove both from the development and growth ofexisting colleagues, and the addition of new talentedcolleagues. This statement applies to our seniorleadership team in the sameway as every associate ofthe company and vice versa.

This organic and eco-system like environment at Markelreflects a dynamic firm and not a stale or bureaucraticlike system. The world changes at an ever increasingpace and we’ve got an organization that is designed toadapt and change along the way.

This is a huge reason why we’ve been successful in thepast and will continue to adapt and grow in the future.Things don’t stay the same. Fortunately, we know that,and we’re willing to keep ourselves a bit agitated andnever complacent about recognizing the need forongoing change and growth.

Markel is an organization well suited for dynamic peoplewhowant to be challenged and grow.We are not a goodplace for people comfortable in a stable bureaucracy.

The Beginning

There is no sense of conclusion at Markel. We are at apoint of new and ongoing beginning. We understand thatthis letter is starting to feel like a book. However, 2012was a phenomenal year for your company and it takessome time and space to describe the reality of what isgoing on around here. Wewere hard at work during theentire year building, rebuilding, tearing down, andrebuilding again, the very foundations of your company.

11

Alan I. Kirshner, Chairman of the Board and Chief Executive Officer

Anthony F. Markel, Vice Chairman

Steven A. Markel, Vice Chairman

Richard R.Whitt, III, President and Co-Chief Operating Officer

Thomas S. Gayner, President and Chief Investment Officer

Markel Corporation

F.Michael Crowley, President and Co-Chief Operating Officer

We acquired a wonderful operation in the case ofThomco, we added organic growth through the internaldevelopment of new insurance products and increasedmarketing efforts. Wemade breakthroughs in our multi-year challenge of developing an appropriate informationtechnology environment tomanage and conduct ourbusiness, and we earned wonderful investment returns.We raised the average IQ of our team by increasing theIQ points of the existing players through new challenges,and adding new associates whowe hope are evensmarter andmore talented than we are.

Then after we did all these things, we announced theacquisition of Alterra, which will create a whole new levelof opportunity for Markel and its shareholders.

Markel is an exciting place to be and we are proud of ourlong-term record of creating great value for our partners.Our partners are our associates, almost all of whom areshareholders, as well as the external shareholders whoprovide us with the capital, and the trust, and the timehorizon, we need to continue our task of building one ofthe world’s great companies.

Thank you for your support and confidence. We lookforward tomeeting the challenges of 2013 and beyondand we look forward to reporting our progress to younext year.