2015 price control review for adwec pc5a first...

TRANSCRIPT

2015 Price Control Review for ADWEC

PC5A First Consultation Paper

28 January 2015 EC/E02/100

Document Approved by Recipients of controlled copies

EC/E02/100 SSQ ADWEC, ADWEA, Bureau Library

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 1 of 40

2015 Price Control Review for ADWEC

PC5A First Consultation Paper

EC/E02/100

28 January 2015

Foreword

1. This document marks the start of the periodic review by the Bureau of the price controls that apply to the Abu Dhabi Water and Electricity Company (ADWEC), the single-buyer in the water and electricity sector in the Emirate of Abu Dhabi.

2. The existing framework of price controls for ADWEC (to be called the "fourth price controls for ADWEC" or "PC4A") was set to apply for at least 5 years from 2010 to 2014 and was structured to apply for a longer period if necessary. Originally, it was envisaged that the framework will be reviewed and revised, if necessary, in 2014 for 2015 onwards. However, such a review could not occur in 2014. ADWEC has now committed to actively support the price control review in 2015.

3. This first consultation paper sets out the high-level issues which need to be considered in setting the new or fifth price controls for ADWEC (PC5A) for 2016 onwards, These issues relate to:

(a) the potential extension of the existing framework for another year or two;

(b) the introduction of supply businesses (to sell electricity to transmission system connected customers in the Emirate of Abu Dhabi), as new licensed activities with their own separate price controls;

(c) the potential extension of the price control framework to cover the unlicensed activities to sell electricity and water to entities outside the Emirate of Abu Dhabi;

(d) Emiratisation and capacity building for new or enhanced activities such as capacity procurement, nuclear and supply businesses;

(e) the scope, structure and duration of new price controls; and

(f) the streamlining and strengthening of the performance and output incentives.

4. We plan to publish draft and final proposals for ADWEC's new price controls in May and October 2015, respectively.

5. Written responses to the issues raised in this paper should be sent by 26 March 2015 to:

Aftab Raza Head of Network Price Controls Regulation and Supervision Bureau PO Box 32800, Abu Dhabi Fax: 02-6424217 Email: [email protected]

6. The Bureau proposes to make responses to the consultation exercise publicly available.

ED AL N Director Genera actor Gee \pc,

4 Suoers\5

2015 Price Control Review for ADWEC — PC5A First Consultation Paper

Author AR/KM/SI/NB

Document EC/E02/100

Version Issue 1

Page 2 of 40

Publication date 28 January 2015

Approved by SSQ

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 3 of 40

Executive Summary

Introduction

1. This document sets out a range of high-level issues that should be considered indeveloping the new PC5A price controls for ADWEC for 2016 onwards.

Issues for consultation

Form of controls (Section 2)

2. We have identified the following issues on the scope, form, structure and duration of newprice controls for ADWEC. Many of these issues have been recently discussed withADWEC, who have expressed their support.

(a) The existing framework of price controls, originally intended to apply up to 2014, can continue indefinitely. Given the timing of this price control review, we believe that the existing price controls should apply up to 2015 and the new price controls (to be agreed by the end of 2015) should apply for 2016 onwards. It is not ideal to apply price controls retrospectively from 1 January 2015 unless we have strong reasons.

(b) We seek views on what should be the priority areas of focus at this price control review. These priority areas may include:

(i) capability building for ADWEC’s new or enhanced responsibilities such as nuclear energy, supply business, economic despatch and capacity procurement;

(ii) Emiratisation;

(iii) introduction of new supply businesses and associated price controls;

(iv) extension of price controls to cover ADWEC’s unlicensed activities outside the Emirate of Abu Dhabi (particularly Northern Emirates); and

(v) strengthening and streamlining of incentives.

(c) Some of the issues may require more time than available within the timetable for this price control review. We may therefore design the new price controls to provide some flexibility to continue working with ADWEC on a pre-defined areas and modify the relevant components of the price controls to incorporate the outcome of such work.

(d) Our current thinking is to retain the present features of price controls for ADWEC:

(i) CPI-X form of price controls which focuses on its procurement costs;

(ii) the flexible regulatory framework which allows annual adjustments for cost deviations to cater for uncertainties that ADWEC may face, for example, in terms of its obligations or requirements;

(iii) the pass-through arrangements for PWPA and fuel costs;

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 4 of 40

(iv) the pass-through of Bureau’s project-specific licence fee via derogation; and

(v) the Q term in the Maximum Allowed Revenue (MAR) formula which provides incentives for important obligations and performance indicators.

(e) Should the scope of price controls be extended to cover the following three items or consider other alternatives to deal with them:

(i) liquidated damages received from IWPPs (to allow them to be shared with the customers);

(ii) Unlicensed Activities (to allow ADWEC a management fee in the form of additional procurement cost allowances within the procurement price controls); and/or

(iii) new water and electricity supply businesses if introduced as Licensed Activities (via new separate price controls for supply businesses)?

(f) How ADWEC should be incentivised to perform its obligations in relation to capacity planning and fuel supplies as efficiently as possible? Further, assuming the role of capacity procurement via IWPPs is transferred from ADWEA to ADWEC, how ADWEC should be incentivised to perform its obligations in relation to the capacity procurement as efficiently as possible?

(g) Should the allowed procurement costs be adjusted each year to allow additional costs from Emiratisation and training requirements for the UAE National staff?

(h) Whether the new price controls should apply for 4 years from 2016 to 2019?

Price control calculations (Section 3)

3. Our current thinking for the price control calculations is to employ the same approach as used at the last price control review. This would mean calculating the allowed procurement cost for electricity and water for the first year of the control period (ie, 2016). The base level of costs could be based on the latest actual audited costs (ie, 2014) and a profit margin of 0.023% on the forecast BST turnover.

Incentives and outputs (Section 4)

4. We seek views on our suggestions for the following changes to the performance incentive scheme:

(a) Discontinue the concept of category B incentives;

(b) Introduce flexible arrangements for incorporating new incentives during the control period;

(c) Retain the existing incentives for SBAs, PCRs and AIS with the current target dates but with a single, symmetric incentive covering the merged submission of SBAs and PCRs;

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 5 of 40

(d) Adjust the bonus or penalty for SBAs/PCRs and AIS submissions pro-rata to the proportion of the Technical Assessor (TA) recommendations completed to formalise the existing practice;

(e) Retain the existing incentives for peak demand forecast accuracy with (i) potential extension to cover annual quantity forecast accuracy and longer term peak demand forecast accuracy and (ii) potential arrangements to exclude, subject to TA verification, the factors outside ADWEC’s control that affect the forecasting accuracy;

(f) Introduce new incentives for performance obligations on Seven Year Planning Statement (7YS) and Bulk Supply Tariff (BST), separating them from annual cost deviation and adjustment mechanism;

(g) Consider a new incentive for key indicator arising from our ongoing discussion with TRANSCO on the economic despatch and Unit Commitment (UC) model;

(h) Introduce incentives for ADWEC to undertake supply businesses for transmission connected customers using the size and growth of businesses as the measures;

(i) Introduce incentives for ADWEC’s initiatives to reduce fuel costs via modifications or enhancements to production plant or fuel supply arrangements subject to independent verification of the benefits;

(j) Consider introducing a new incentive for improved fuel planning and procurement;

(k) Consider a new incentive for ADWEC to develop compliance reporting and improved contract management in relation to the IWPPs; and

(l) Apply different financial caps for different incentives based on their importance and costs while keeping in view the overall financial impact on ADWEC.

5. Some of the above changes to incentive scheme have recently been discussed or agreed with ADWEC. These include items 4(b), 4(c), 4(e), 4 (h) and 4(i) above. Further, items from 4(a) through 4(d) are in line with the arrangements put in place for the sector network companies for their PC5 price controls

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 6 of 40

Glossary

7YS Seven-Year Planning Statement

AED UAE Dirham

AADC Al Ain Distribution Company

ADDC Abu Dhabi Distribution Company

ADWEA Abu Dhabi Water and Electricity Authority

ADWEC Abu Dhabi Water and Electricity Company

AIS Annual Information Submission

BST Bulk Supply Tariff

CPI Consumer Price Index

GWh Giga Watt-hour

KPI Key Performance Indicator

MAR Maximum Allowed Revenue

MIG Million Imperial Gallons

MIGD Million Imperial Gallons per Day

MW Mega-Watt

PC1 First Price Control covering the period 1999-2002

PC2 Second Price Control covering the period 2003-2005

PC3 Third Price Control covering the period 2006-2009

PC4A Fourth Price Control covering the period 2010-2014 or 2015

PC5A Fifth Price Control covering the period 2015 or 2016 onwards

PCR Price Control Return

PIS Performance Incentive Scheme

PWPA Power and Water Purchase Agreement

RAG Regulatory Accounting Guideline

RIG Regulatory Instruction and Guidance

SBA Separate Business Account

TA Technical Assessor

TIG Thousand Imperial Gallon

TUoS Transmission Use of System

TRANSCO Abu Dhabi Transmission and Despatch Company

UC Unit Commitment

WACC Weighted Average Cost of Capital

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 7 of 40

Contents

1. Introduction .................................................................................... 8

2015 price control review ........................................................................... 8

The role and duties of the regulator ........................................................... 9

ADWEC’s existing separate businesses .................................................... 9

ADWEC’s potential new supply businesses ............................................ 11

ADWEC’s current price controls .............................................................. 13

ADWEC’s financial performance .............................................................. 15

ADWEC’s incentive and output performance .......................................... 20

Timetable for this review .......................................................................... 21

Structure of this document ....................................................................... 22

2. Form of price controls .................................................................. 23

Introduction .............................................................................................. 23

Objectives and priorities of this review .................................................... 23

Approach to economic regulation ............................................................ 26

Scope and separation of controls ............................................................ 27

Cost pass-through arrangements ............................................................ 29

Structure of controls ................................................................................. 30

Annual adjustment mechanism ................................................................ 31

Duration of controls .................................................................................. 33

3. Price control calculations ............................................................. 34

Introduction .............................................................................................. 34

Approach to calculation ............................................................................ 34

4. Incentives and outputs ................................................................. 36

Introduction .............................................................................................. 36

Approach and arrangements for incentives ............................................. 36

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 8 of 40

1. Introduction

2015 price control review

1.1 The water and electricity sector in the Emirate of Abu Dhabi has a single-buyer structure, whereas the single buyer (ADWEC) performs the following transactions:

(a) ADWEC purchases water and electricity from a number of generation and desalination companies, both inside and outside the Emirate of Abu Dhabi, under the terms of long-term Power and Water Purchase Agreements (PWPAs). It also procures natural gas for the production companies.

(b) As part of its “Licensed Activities”, it sells water and electricity to the two distribution companies in the Emirate of Abu Dhabi (AADC and ADDC) at Bulk Supply Tariffs (BSTs).

(c) It also undertakes “Unlicensed Activities” which involve selling water and electricity to certain utilities outside the Emirate of Abu Dhabi.

1.2 Like other monopoly companies in the sector (AADC, ADDC, ADSSC, RASCO and TRANSCO), the Licensed Activities of ADWEC have been subject to the CPI-X price controls set by the Bureau as follows:

(a) the first price controls (PC1) set in 1999 ran for four years (1999-2002);

(b) the second price controls (PC2) applied for three years (2003-2005);

(c) the third price controls (PC3) were set in 2005 for four years (2006-2009); and

(d) the current fourth price controls (PC4A) were intended to apply for five years (2010-2014) but were structured to continue to apply for a longer period.

1.3 This document marks the commencement of our review of the price controls for ADWEC for 2016 onwards. While setting the existing framework of price controls in 2010, we stated that this would be reviewed and revised, if necessary, in 2014 for 2015 onwards. It is therefore possible that at the end of this review, the existing price controls may be retained with or without any change.

1.4 The price control review could not be initiated in 2014 as per the Bureau’s letter of 28 November 2013, which set out the proposed timetable for price control review in 2014. However, ADWEC has now committed via its letter dated 3 November 2014 to actively support the price control review in 2015.

1.5 The price control review provides an opportunity to assess the company’s performance against the price controls and the efficiency and performance targets, and the key challenges and issues that the company or the sector may face in future.

1.6 Section 1 summarises ADWEC’s performance against the previous price controls and performance incentives as well as its overall financial performance.

1.7 We published our final proposals on 6 November 2013 regarding the PC5 price controls for the four network companies (AADC, ADDC, ADSSC and TRANSCO). In this

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 9 of 40

document, we have referred to this document and earlier consultation papers on PC5. These documents are available on our website (www.rsb.gov.ae).

The role and duties of the regulator

1.8 Law No (2) of 1998 established the Bureau as the regulatory body for the water and electricity sector in the Emirate of Abu Dhabi and defined its duties, functions and powers. Law No (17) of 2005 extended these powers to include the sewerage services sector. Any entity wishing to undertake any of the defined regulated activities in the Emirate requires a licence from the Bureau and it is through licence conditions that the Bureau is able to regulate sector companies. In doing so, we must have regard to our statutory duties and functions, which are summarised below:

(a) The primary duty of the Bureau (Article 53 of Law No (2) of 1998) is "to ensure, so far as it is practicable for it to do so, the continued availability of potable water for human consumption and electricity for use in hospitals and centres for the disabled, aged and sick". The Bureau has a number of general duties (Article 54 of Law No (2) of 1998), the most relevant of which in relation to the price control review is to "protect the interest of consumers ………as to the terms and conditions and price of supply (whether consumers are domestic, commercial or industrial)".

(b) The Bureau also has a number of general functions (Article 55 of Law No (2) of 1998), including "the regulation of prices charged to consumers ………and the methods by which they are charged."

(c) In carrying out its functions under the Law, the Bureau is under an obligation (Article 96 of Law No (2) of 1998) to act consistently, to minimise the regulatory burden on licensees, to take account of the financial position of licensees, and to give reasons for its decisions.

1.9 Accountability is reinforced by the fact that the Bureau's decisions on licence modifications (including those that will be made at the end of this review relating to the price control conditions) can be challenged by licensees through an arbitration process.

ADWEC’s existing separate businesses

1.10 As shown in Figure 1.1 below, ADWEC’s licence presently defines two separate businesses as the Licensed Activities, namely:

(a) electricity procurement business; and

(b) water procurement business;

1.11 Each of the these two businesses is subject to separate price controls set by the Bureau and involves mainly the following activities:

(a) purchase of water or electricity from production plant;

(b) purchase of fuel for delivery to the production plant; and

(c) sale of water or electricity to the distribution companies.

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 10 of 40

1.12 In addition, ADWEC supplies water and electricity to utilities in other Emirates in the UAE and trade electricity with the GCC countries. These are Unlicensed Activities requiring the Bureau’s prior consent (as per ADWEC’s licence). The Unlicensed Activities are not subject to any price controls by the Bureau and are financially ring-fenced to avoid any cross subsidy from Licensed Activities. This is also illustrated in Figure 1.1 below.

Figure 1.1: ADWEC’s existing Licensed and Unlicensed Activities

1.13 The financial ring-fencing between Licensed and Unlicensed Activities is achieved mainly through application of prescribed cost allocation methodologies and separate treatment of revenues and profits.

1.14 At present, ADWEC produces two types of audited statements each year separately for water and electricity. These statements are:

(a) audited Separate Business Accounts (SBAs), which allocate costs and incomes between water and electricity businesses for the Licensed and Unlicensed Activities, according to the Bureau’s guidelines; and

(b) audited Price Control Returns (PCRs), which show compliance of the Licensed Activities with the price controls.

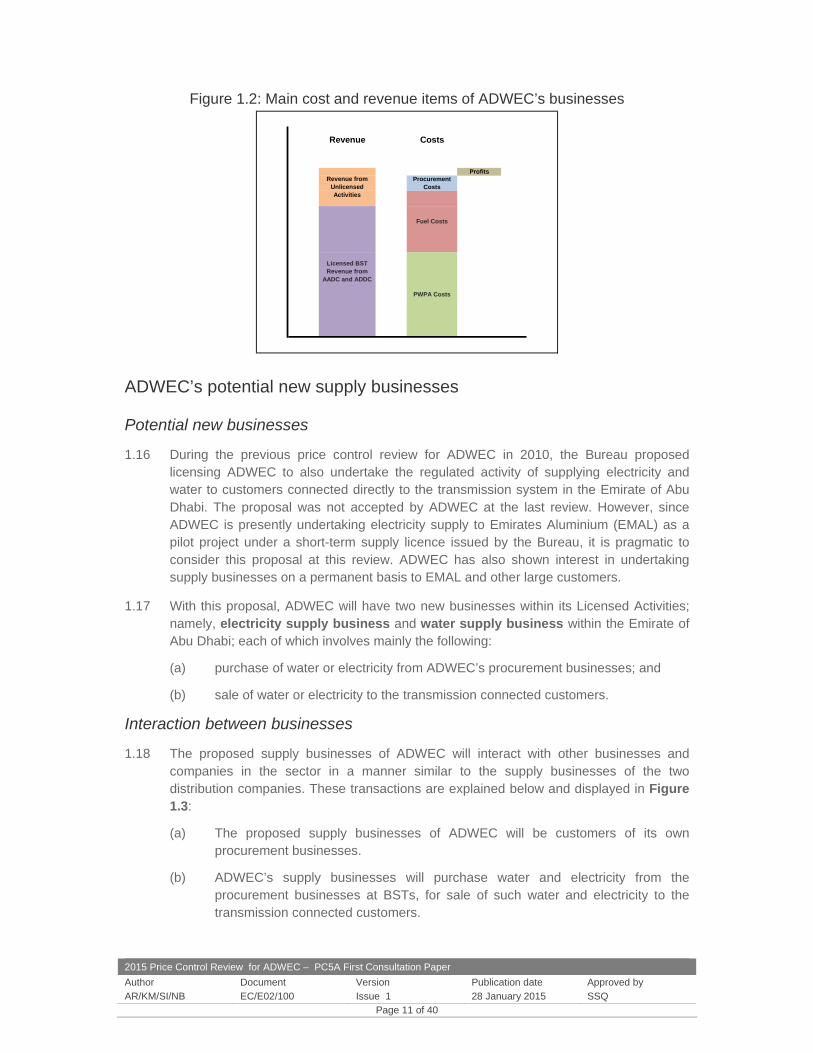

1.15 The above arrangements ensure transparency and ring-fencing of costs and subsidy within the businesses. Figure 1.2 below summarises the main revenue and cost items of ADWEC’s businesses:

Production costs (PWPA + Fuel)

AADC

ADDC Water Procurement

Business

Unlicensed Water Supply

Business

Customers outside Emirate

of Abu Dhabi

Customers outside Emirate

of Abu Dhabi

Electricity Procurement

Business

Unlicensed Electricity

Supply Business

Licensed Activities Unlicensed Activities

Subject to Price Controls Subject to Consent

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 11 of 40

Figure 1.2: Main cost and revenue items of ADWEC’s businesses

ADWEC’s potential new supply businesses

Potential new businesses

1.16 During the previous price control review for ADWEC in 2010, the Bureau proposed licensing ADWEC to also undertake the regulated activity of supplying electricity and water to customers connected directly to the transmission system in the Emirate of Abu Dhabi. The proposal was not accepted by ADWEC at the last review. However, since ADWEC is presently undertaking electricity supply to Emirates Aluminium (EMAL) as a pilot project under a short-term supply licence issued by the Bureau, it is pragmatic to consider this proposal at this review. ADWEC has also shown interest in undertaking supply businesses on a permanent basis to EMAL and other large customers.

1.17 With this proposal, ADWEC will have two new businesses within its Licensed Activities; namely, electricity supply business and water supply business within the Emirate of Abu Dhabi; each of which involves mainly the following:

(a) purchase of water or electricity from ADWEC’s procurement businesses; and

(b) sale of water or electricity to the transmission connected customers.

Interaction between businesses

1.18 The proposed supply businesses of ADWEC will interact with other businesses and companies in the sector in a manner similar to the supply businesses of the two distribution companies. These transactions are explained below and displayed in Figure 1.3:

(a) The proposed supply businesses of ADWEC will be customers of its own procurement businesses.

(b) ADWEC’s supply businesses will purchase water and electricity from the procurement businesses at BSTs, for sale of such water and electricity to the transmission connected customers.

Revenue Costs

Profits

Licensed BST Revenue from

AADC and ADDC

Revenue from Unlicensed Activities

Procurement Costs

Fuel Costs

PWPA Costs

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 12 of 40

(c) These supply businesses will pay Transmission Use of System (TUoS) charges to TRANSCO for using the transmission system for water and electricity supplies to the transmission connected customers.

(d) ADWEC’s supply businesses will receive tariff income from the transmission connected customers.

(e) In addition, ADWEC’s supply businesses may also receive subsidy from the government in respect of those transmission connected customers who are subject to the subsidised tariffs.

(f) However, we envisage that most of transmission connected customers would be supplied at cost-reflective tariffs and would not require subsidy from the Government.

Figure 1.3: Transactions between existing and new businesses

Accounting arrangements

1.19 The proposed new supply businesses for ADWEC would require SBAs and PCRs separately for electricity supply business and water supply business, in addition to present arrangements for the two procurement businesses. This is necessary to ensure transparency and ring-fencing of costs and subsidy within the businesses. Figure 1.4 summarises the main revenue and cost items of these businesses.

1.20 For the short-term supply licence which is being issued to ADWEC in relation to EMAL pilot project, we have proposed simpler, pragmatic arrangements in terms of accounting and commercial treatment. Given that ADWEC undertakes this activity on no loss, no profit basis (ie, with all costs and incomes on a pass-through basis), we have not set separate price controls nor have asked for full, separate SBAs and PCRs for this activity. However, to ensure full transparency and effective regulation, we have asked ADWEC to record and show all costs and incomes relating to this activity as separate line items on the existing SBAs and PCRs for the procurement businesses.

TUoS Charge Subsidy

Water or Electricity

BST

Water or Electricity Water or Electricity BST Tariff

GovernmentTRANSCO

ADWEC Procurement

Business

ADWEC Supply Business

AADC / ADDCTransmission

Connected Customers

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 13 of 40

Figure 1.4: Main cost and revenue items of ADWEC’s licensed businesses

ADWEC’s current price controls

1.21 The current price controls are in the form of revenue caps, which define Maximum Allowed Revenue (MAR) for ADWEC’s Licensed Activities, for each year of the price control duration as follows:

MAR = PWPA costs + Fuel costs + A + Q – K

where:

(a) PWPA and fuel costs are the costs which are pass-through on an actual basis subject to ADWEC’s economic purchasing obligation.

(b) ‘A’ is the price-controlled procurement cost or the notified value in UAE Dirhams, which allows ADWEC to recover its staff and other operating costs relating to the Licensed Activities. The notified value ‘A’ is set by the Bureau for the first year of the control period and is subsequently adjusted each year according to the mechanism described below.

(c) ‘Q’ is the revenue adjustment for performance during a year under the Performance Incentive Scheme (PIS), discussed in Section 4 of this paper.

(d) ‘K’ is the correction factor adjusting any over or under-recovery of revenue in the preceding year.

1.22 There have been separate price controls for the water and electricity businesses for ADWEC’s Licensed Activities.

1.23 At the last price control review, we established a detailed framework to determine the price-controlled procurement cost for each year of the PC4A period once the notified value ‘A’ was set by the Bureau for the first year of the control period. This framework (illustrated in Figure 1.5) requires the value of A for any year t to be calculated as follows:

Procurement Business Supply Business

Revenue Costs

Profits

Revenue Costs

Profits

Admin Costs

Admin Costs

TUoS Charge Payment to TRANSCO

Subsidy

PWPA Costs

Fuel Costs

BST Payment to Procurement

Business

Tariff Income

BST Revenue from ADDC

BST Revenue from AADC

BST Revenue from Supply

Business

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 14 of 40

A t = A t-1 (1 + CPIt) (1 + Dt) (1 + S1t) (1 + S2t)

1.24 This involves four automatic adjustments each year:

(a) Annual adjustment for UAE CPI inflation: The price-controlled procurement cost is adjusted each year using a formula for (i) the UAE Consumer Price Index (CPI) inflation for the previous year less (ii) an ‘X’ factor (which has been zero to date) set by the Bureau.

(b) Annual adjustment for cost deviations (D): The price-controlled procurement costs applicable for each year is adjusted as follows:

(i) 1% upward or downward adjustment for each 1% increase or decrease in the actual audited procurement costs in the preceding year in comparison to the allowed procurement costs for that preceding year, for cost increases / decreases of up to 10%; and

(ii) for further cost increase or decrease beyond 10%, adjustment by 0.5% upward or downward in the allowed procurement costs for a year for each 1% further increase or decrease in the preceding year, without any cap.

(c) Annual adjustments for performance of two important obligations (S1 and S2): If the draft Seven Year Planning Statement (7YS) or draft BST is not submitted to the Bureau’s satisfaction by 31 May or 30 November, respectively, the price-controlled procurement cost for each of ADWEC’s water and electricity businesses for the following year is adjusted downward by 1% for each month of delay up to a maximum of 5% adjustment in each case.

Figure 1.5: Annual adjustments to ADWEC’s price-controlled procurement costs

1.25 In addition, the framework allows the pass-through of costs (using a licence derogation) of any additional workload requested or approved by the Bureau, to the extent such costs are not covered by the price control mechanism described above.

1.26 The following table summarises the allowed procurement costs or the notified values in the price controls for the recent years:

Adjustment for BST and 7YS

Performance in Year " t-1 "

(S t )

Possible Adjustment via derogation for

additional workload

Final Notified Value for Year

" t " (A t )

Notified Value for Year " t-1 "

(A t-1 )

CPI-X Indexation for

Year " t-1 "

Adjustment for Cost Deviation

in Year " t-1 " (D

t )

Notified Value for Year " t "

(B t )

- Full pass-through of first 10% deviation- Pass-through of half of deviation beyond 10%

Penalty up to 5% of Notified Value for year "t" in each case

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 15 of 40

Table 1.1: Notified values ‘A’ for ADWEC’s procurement businesses to date PC3 PC4A

AED million, nominal prices 2006 2007 2008 2009 2010 2011 2012 2013

Electricity procurement cost

Base cost 11.80 11.80 12.90 14.33 21.01 21.01 21.80 44.41

Adjustment for CPI n/a 9.29% 11.13% 12.25% n/a 0.88% 0.88% 0.66%

Adjustment for cost deviation n/a n/a n/a n/a n/a 3.74% 113% -20.8%

Adjustment for BST performance n/a n/a n/a n/a n/a - - -1%

Adjustment for 7YS performance n/a n/a n/a n/a n/a - -5% -

Electricity - total 11.80 12.90 14.33 16.09 21.01 21.80 44.41 36.9

Water procurement cost

Base cost 7.56 7.56 8.26 9.18 22.30 22.30 23.49 52.29

Adjustment for CPI n/a 9.29% 11.13% 12.25% n/a 0.88% 0.88% 0.66%

Adjustment for cost deviation n/a n/a n/a n/a n/a 5.35% 132% -24.1%

Adjustment for BST performance n/a n/a n/a n/a n/a - - -1%

Adjustment for 7YS performance n/a n/a n/a n/a n/a - -5% -

Water - total 7.56 8.26 9.18 10.31 22.30 23.49 52.29 41.6

Total procurement costs 19.36 21.16 23.51 26.40 43.31 45.29 96.68 78.5

Source: ADWEC’s audited PCRs

1.27 ADWEC’s current price controls also includes an incentive scheme (discussed in Section 4) whereby the MAR can be adjusted upward or downward by the Q term for financial bonus or penalty for ADWEC’s performance against the following four key indicators:

(a) timeliness of submission of audited SBAs;

(b) timeliness of submission of audited PCRs;

(c) timeliness of Annual Information Submission (AIS); and

(d) accuracy of peak demand forecast.

ADWEC’s financial performance

1.28 In contrast to the network companies, ADWEC has a small capital base. However, it manages a number of long-term PWPAs with production plant both inside and outside the Emirate of Abu Dhabi. ADWEC handles an annual turnover of about AED 11.2 billion (in 2013) for its Licensed Activities, which is about 57% of the total turnover of the sector (about AED 19.5 billion in 2013). Further, ADWEC deals with the trading of electricity and water with other Emirates and the GCC countries, with a turnover of about AED 3.9 billion in 2013. At the end of 2013, ADWEC had a total asset base of around AED 7.6 billion.

1.29 Given ADWEC’s unique financial position, any regulatory framework considered for ADWEC should pay attention to these distinct features. Therefore, it is useful to assess the trends and composition of ADWEC’s costs, revenues and profits over the recent years. The following paragraphs discuss these trends in nominal prices over the PC3 period (2006-2010) and PC4A period to date (2010-2013).

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 16 of 40

Cost profile

1.30 As shown in Figures 1.6 and 1.7 below, ADWEC’s costs are dominated by PWPA and fuel costs. For both Licensed and Unlicensed Activities, the total costs increased from about AED 7.1 billion in 2006 to AED 13.4 billion in 2013, at an average rate of 10% per annum.

Figure 1.6: ADWEC’s cost profile – breakdown by business

Figure 1.7: ADWEC’s cost profile – breakdown by cost items

Revenue profile

1.31 ADWEC’s revenue from the Licensed Activities significantly exceeds the revenue from the Unlicensed Activities (see Figure 1.8). The revenue from Licensed Activities increased from about AED 6.5 billion to AED 11.2 billion over 2006-2013 (at an average rate of 8% per annum). In contrast, revenue from Unlicensed Activities increased from AED 0.8 billion to AED 3.9 billion over this period.

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000Licensed

Unlicen

sed

Licensed

Unlicen

sed

Licensed

Unlicen

sed

Licensed

Unlicen

sed

Licensed

Unlicen

sed

Licensed

Unlicen

sed

Licensed

Unlicen

sed

Licensed

Unlicen

sed

2006 2007 2008 2009 2010 2011 2012 2013

Costs

(AED

million, nominal prices)

Water

Electricity

‐

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

2006 2007 2008 2009 2010 2011 2012 2013

Costs

(AED

million, nominal prices)

PWPA

Fuel

Procurement

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 17 of 40

Figure 1.8: ADWEC’s revenue profile

Actual procurement cost profile

1.32 ADWEC’s actual procurement cost for the Licensed Activities increased from AED 15 million to AED 53.8 million over 2006-2013 i.e., an increase of about 20% per annum:

Figure 1.9: ADWEC’s actual licensed procurement costs profile

1.33 With the exception of 2011, administrative and other expenses accounted for the majority (about 55%) of ADWEC’s actual procurement cost, with the remaining accounted for by the staff costs. Depreciation on ADWEC’s own fixed assets accounted for a very small proportion. Electricity and water businesses contributed equally to these procurement costs.

1.34 In 2011, ADWEC incurred significant amounts of financial lease and related deprecation due to the accounting treatment of payments for a fuel supplier’s pipeline. We understand that these financial lease charges were reversed in the 2012. The above chart shows these effects in terms of very large depreciation in 2011 and usual, small depreciation in 2012 and 2013. For price control purposes, such financial lease and deprecation were

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Licensed

Unlicensed

Licensed

Unlicensed

Licensed

Unlicensed

Licensed

Unlicensed

Licensed

Unlicensed

Licensed

Unlicensed

Licensed

Unlicensed

Licensed

Unlicensed

2006 2007 2008 2009 2010 2011 2012 2013

Reven

ue

(AED

million, nominal prices)

Water

Electricity

‐

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

2006 2007 2008 2009 2010 2011 2012 2013

Costs

(AED

million, nominal prices)

Admin and otherexpenses

Depreciation

Staff costs

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 18 of 40

not intended to be treated as part of ADWEC’s own procurement costs. Instead, they could have been treated as part of the fuel costs in the MAR formulae. Going forward, we would like to ensure that this does not raise any issue.

Performance against price controls

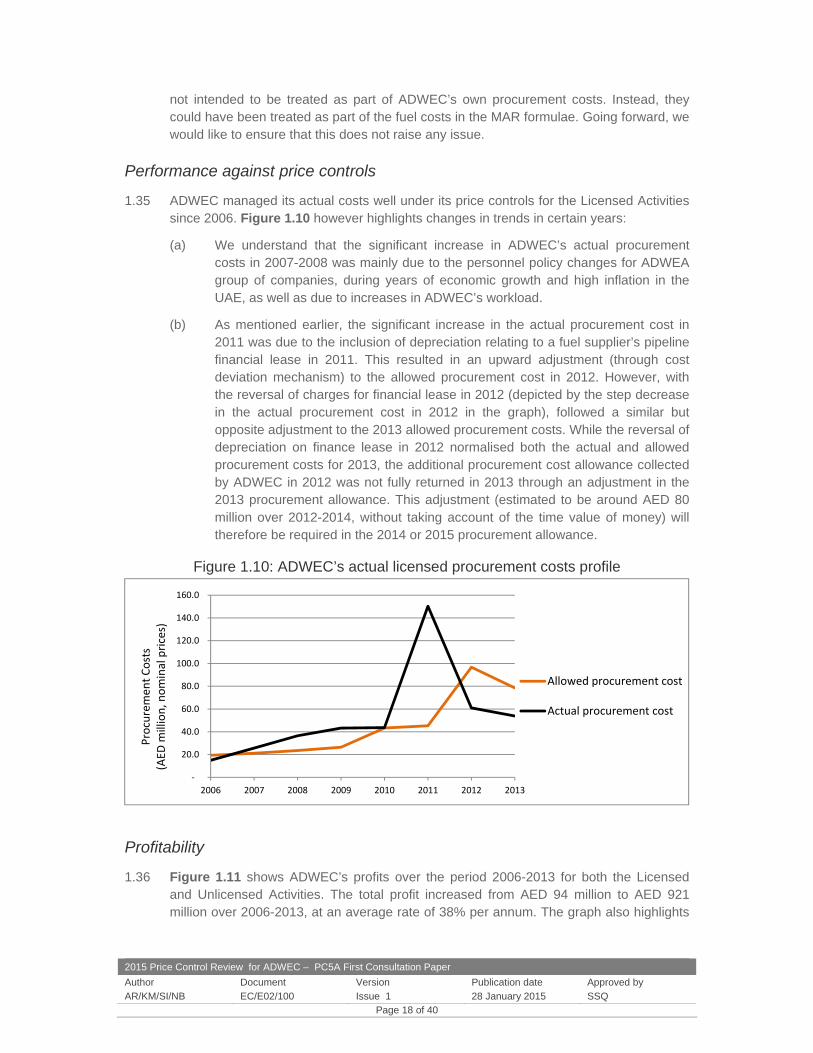

1.35 ADWEC managed its actual costs well under its price controls for the Licensed Activities since 2006. Figure 1.10 however highlights changes in trends in certain years:

(a) We understand that the significant increase in ADWEC’s actual procurement costs in 2007-2008 was mainly due to the personnel policy changes for ADWEA group of companies, during years of economic growth and high inflation in the UAE, as well as due to increases in ADWEC’s workload.

(b) As mentioned earlier, the significant increase in the actual procurement cost in 2011 was due to the inclusion of depreciation relating to a fuel supplier’s pipeline financial lease in 2011. This resulted in an upward adjustment (through cost deviation mechanism) to the allowed procurement cost in 2012. However, with the reversal of charges for financial lease in 2012 (depicted by the step decrease in the actual procurement cost in 2012 in the graph), followed a similar but opposite adjustment to the 2013 allowed procurement costs. While the reversal of depreciation on finance lease in 2012 normalised both the actual and allowed procurement costs for 2013, the additional procurement cost allowance collected by ADWEC in 2012 was not fully returned in 2013 through an adjustment in the 2013 procurement allowance. This adjustment (estimated to be around AED 80 million over 2012-2014, without taking account of the time value of money) will therefore be required in the 2014 or 2015 procurement allowance.

Figure 1.10: ADWEC’s actual licensed procurement costs profile

Profitability

1.36 Figure 1.11 shows ADWEC’s profits over the period 2006-2013 for both the Licensed and Unlicensed Activities. The total profit increased from AED 94 million to AED 921 million over 2006-2013, at an average rate of 38% per annum. The graph also highlights

‐

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2006 2007 2008 2009 2010 2011 2012 2013

Procurement Costs

(AED

million, nominal prices)

Allowed procurement cost

Actual procurement cost

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 19 of 40

the dominance of profits by the Unlicensed Activities. (Note that large profits of Unlicensed Activities are due to the methodology employed for cost allocation between Licensed and Unlicensed Activities using the average production cost.)

Figure 1.11: ADWEC’s actual profitability (as reported)

1.37 While the price controls envisage only a nominal profit element in the procurement cost, the annual profit from the Licensed Activities during 2006-2013 was significant – varying between AED -132 million and AED 446 million per annum as shown in Figure 1.11.

1.38 We understand that these variations in ADWEC’s profits for the Licensed Activities were caused mainly by the receipt of liquidated damages from production companies, the accounting treatment of payments for a fuel supplier’s pipeline and their subsequent reversals and correction factors (representing the difference between entitled revenue and revenue recovered during a year). Figure 1.12 below shows ADWEC’s adjusted profits after excluding these effects.

Figure 1.12: ADWEC’s actual profitability (adjusted for one-off items)

‐200.0

‐

200.0

400.0

600.0

800.0

1,000.0

1,200.0

2006 2007 2008 2009 2010 2011 2012 2013

Profits

(AED

million, nominal prices)

Unlicensed

Licensed

‐200

‐

200

400

600

800

1,000

2006 2007 2008 2009 2010 2011 2012 2013

Profits

(AED

million, nominal prices)

Unlicensed

Licensed

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 20 of 40

Capacity and demand trends

1.39 ADWEC’s financial performance presented above should be seen in the context of increasing trends of electricity and water demands. The four charts in Figure 1.13 summarise the demand trends for both Licensed and Unlicensed Activities since 2006:

(a) electricity and water peak demands increased at average rates of 13% and 6% a year to reach 10,105 MW and 794 MIGD by 2013; and

(b) the quantities of electricity and water units supplied increased at average growth rates of 11% and 5% a year to reach 57,451 GWh and 254,797 MIG by 2013.

1.40 The increasing demands have been met by increasing production capacities. Electricity generation capacity has increased from 8,312 MW in 2006 to 13,899 MW in 2013 at an average annual growth rate of 7.6% per annum and water production capacity has increased from 668 MIGD to 916 MIGD over the same period at an annual rate of 4.6% per annum.

Figure 1.13: Actual electricity and water demand profiles

ADWEC’s incentive and output performance

1.41 For 2011 onwards, the price controls gave strong incentives for ADWEC to submit draft 7YS and BST in a timely manner (through a penalty of up to 5% of the allowed procurement cost in each case). ADWEC was able to make timely submissions in 2011 and 2012 and avoided such negative adjustments. The only exceptions were a 5% penalty in 2012 for a lack of submission of draft 7YS to our satisfaction and a 1% penalty in 2013 for late submission of draft BST to our satisfaction (see in Table 1.1 above).

1.42 Figure 1.14 below summarises the financial bonuses and penalties that ADWEC received through the Q terms in its MAR formulas. These reflect its performance on each of the four PIS category A indicators for electricity and water businesses. With some

‐

2,000

4,000

6,000

8,000

10,000

12,000

2006 2007 2008 2009 2010 2011 2012 2013

MW

Electricity peak demand

Unlicensed

Licensed

‐

10,000

20,000

30,000

40,000

50,000

60,000

70,000

20062007200820092010201120122013

GWH

Electricity units supplied

Unlicensed

Licensed

‐

100

200

300

400

500

600

700

800

900

2006 2007 2008 2009 2010 2011 2012 2013

MIGD

Water peak demand

Unlicensed

Licensed

‐

50,000

100,000

150,000

200,000

250,000

300,000

2006 2007 2008 2009 2010 2011 2012 2013

MIG

Water units supplied

Unlicensed

Licensed

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 21 of 40

exceptions (particularly for peak demand forecasting accuracy), ADWEC performed well on these incentives as indicated by positive values in the chart.

Figure 1.14: ADWEC’s performance on PIS category A indicators

Timetable for this review

1.43 Following a meeting held with ADWEC in October 2014, ADWEC via its letter dated 3 November 2014 committed to actively and constructively engage in the price control review in 2015. ADWEC also highlighted its proposal to undertake a full review of its roles and organisational structure in 2015 in parallel with the price control review and to provide important inputs into the Bureau’s price control proposals. Our letter to ADWEC on 17 November 2014 welcomed ADWEC’s engagement and set out the timetable for setting the new price controls for ADWEC. A further meeting was held on 16 December 2014 with ADWEC to discuss the priority issues for consideration during the price control review. These issues are discussed in the relevant sections of this document.

1.44 Table 1.2 below sets out the timetable for this price control review for ADWEC in line with our letter dated 17 November to ADWEC. The timetable envisages publication of three consultation papers/proposals by the Bureau during 2014. This timetable allows two months for ADWEC to respond to each of our consultation or proposal papers:

Table 1.2: Timetable for 2014 Price Controls Review Approximate time Task

28 January 2015 Bureau publishes this First Consultation Paper

26 March 2015 ADWEC to respond to First Consultation Paper

May 2015 Bureau to publish Draft Proposals

July 2015 ADWEC to respond to Draft Proposals

October 2015 Bureau to publish Final Proposals and proposed draft licence modification

November 2015 ADWEC to respond to Final Proposals and proposed draft licence medication

1 January 2016 Licence modification with new price controls to take effect

‐0.6

‐0.4

‐0.2

‐

0.2

0.4

0.6

0.8

1.0

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

Electricity

Water

2006 2007 2008 2009 2010 2011 2012 2013

Perform

ance Incentive

(AED

million, nominal prices)

Demand forecastingincentive

AIS incentive

PCR incentive

SBAs incentive

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 22 of 40

Structure of this document

1.45 The remainder of this document is structured as follows:

(a) Section 2 discusses the fundamental issues relating to the form of the new controls, including the structure, scope and duration of controls, the potential introduction of new supply businesses for ADWEC, and the potential extension of the existing price controls.

(b) Section 3 describes our approach to price control calculations and raises the relevant issues for consultation.

(c) Section 4 sets out our current thinking on the streamlining and strengthening of the output and performance incentives for ADWEC.

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 23 of 40

2. Form of price controls

Introduction

2.1 In this section, we discuss the key challenges and priorities for this price control review. We then discuss the fundamental aspects of the new controls, such as the form, duration, and scope of the controls. The discussion reflects our desire:

(a) to support capacity building within ADWEC;

(b) to retain the positive and pragmatic features of the existing price control framework;

(c) to appropriately change or strengthen other aspects of the framework; and

(d) to streamline the performance and output incentives.

Objectives and priorities of this review

Considerations

2.2 A separate price control review for ADWEC provides opportunities for deliberations and consultation on the issues specific to ADWEC. It also covers important issues which have wider implications. It may be appropriate that the focus of this price control should be to address the following key challenges and priorities:

Organisational capabilities

2.3 Building organisational capabilities should be one of the initial steps towards meeting new challenges and enhanced responsibility in a number of areas that ADWEC intends to take over. As discussed below, these include nuclear energy, supply business, economic despatch and capacity procurement via IWPPs. In its letter dated 30 October 2014, ADWEC outlined its initiative and approach to ‘redefining’ their overall role within the sector and its approach to development of new such roles, responsibilities and resources. We are supportive of this work and believe that regulatory arrangements should provide the licensee an adequate level of funding to finance its activities, build capabilities and, if possible, eliminate any undue risks to the sector.

Nuclear

2.4 The commissioning of the nuclear power project in the Emirate of Abu Dhabi scheduled for 2017 onwards presents significant technical and commercial implications for the sector. ADWEC being the singe-buyer in the sector and off-taker under the relevant power purchase agreement (PPA) has a critical role in the development and management of this project. The most significant responsibility relates to the appointment and management of an independent charge rate auditor (CRA), under the nuclear PPA to ensure economical and cost-efficient procurement of electricity.

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 24 of 40

Emiratisation

2.5 Given that the Emiratisation is a key government policy, ADWEC’s approach and plan for Emiratisation could be an important consideration in developing the price controls. For instance, the PC5 final proposals for the network companies incorporate specific allowances for additional staff costs of the UAE National employees as compared to the expat employees. We look forward to receiving ADWEC’s proposed plan for Emiratisation.

Supply businesses

2.6 Law No (9) of 2009 which amended Law No (2) of 1998 expressly allows the Bureau to license entities to engage in multiple regulated activities. At the last price control review, we therefore proposed licensing ADWEC to undertake the regulated activity of supplying electricity and water to customers connected directly to the transmission system in the Emirate of Abu Dhabi. We accordingly proposed price controls for the two new supply businesses. Our final proposals of 10 June 2010 explained in detail how the relevant transactions and accounting and price control arrangements would work for these and other businesses. However, this proposal could not materialise at the last review. As discussed in Section 1 of this paper, It is now more eminent and pragmatic to consider the proposal again at this review, given that:

(a) there are a number of large customers of unique load profiles;

(b) there are now volume-based transmission use of system (TUoS) charges in place to facilitate adoption of more streamlined and cost-reflective customer tariffs;

(c) ADWEC is presently undertaking electricity supply to Emirates Aluminium (EMAL) as a pilot project under a short-term supply licence being issued by the Bureau; and

(d) ADWEC has shown interest at the meeting on 16 December 2014 in undertaking supply businesses on a permanent basis to large customers.

Incentives

2.7 Another objective of the price control review could be to simplify and streamline the incentives provided by the price controls to improve effectiveness and efficiency. This work can build on the incentives contained in the present price controls, as follows:

(a) Present price controls provide incentives for the timely provision of information such as SBAs, PCRs and AIS (through the Q term of the MAR formula) and capacity planning statement and BST (via annual adjustment to allowed procurement costs). The rationale behind these incentives is that access to timely and high quality information and forecasts is important to facilitate effective regulation of the sector. Further, robust capacity planning statement is critical to ensure long-term availability and security of supply of both water and electricity. These incentives can be streamlined and made more effective, if provided in the same manner.

(b) The current incentives for annual peak demand forecasting errors can be extended to cover forecasts of annual quantities of water and electricity and

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 25 of 40

longer term peak demand forecasts. At the meeting on 16 December 2014, ADWEC suggested that the incentives for demand forecasting accuracy should take account of the factors that are outside its control.

(c) At the 16 December meeting, ADWEC suggested developing new incentives to encourage ADWEC to undertake supply business and take initiatives to reduce fuel costs.

(d) A consultant appointed by the Bureau has assessed the economic despatch activities of TRANSCO and has identified the need for an improvement in various scheduling and despatch processes and tools including the unit commitment (UC) model used by both TRANSCO and ADWEC. Any such improvement can be facilitated by developing new incentives for TRANSCO as well as ADWEC.

Flexible regulatory arrangements

2.8 Some of the above issues may require more time than available in the timetable discussed in Section 1 for this price control review. We may therefore find the schedule for this review challenging to address all the issues in a robust manner, during the review. In such a case, we may design the new price controls to provide some flexibility to continue working with ADWEC on a pre-defined areas and modify the relevant components of the price controls to incorporate the outcome of such work. However, to ensure sanctity and efficiency of the price controls, any such flexibility need to be agreed during this review to allow objective, time-bound and automatic adjustment as much as possible.

Issues for consultation

2.9 We seek views on what should be the priority areas of focus at this price control review. These priority areas may include:

(a) capability building for ADWEC’s new or enhanced responsibilities such as nuclear energy, supply business, economic despatch and capacity procurement;

(b) Emiratisation;

(c) introduction of new supply businesses and associated price controls;

(d) extension of price controls to cover ADWEC’s unlicensed activities outside the Emirate of Abu Dhabi (particularly Northern Emirates); and

(e) strengthening and streamlining of incentives.

2.10 Some of the issues may require more time than available in the timetable for this price control review. We may therefore design the new price controls to provide some flexibility to continue working with ADWEC on pre-defined areas and modify the relevant components of the price controls to incorporate the outcome of such work.

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 26 of 40

Approach to economic regulation

Bureau’s current approach

2.11 Since 1999, the monopoly companies in the sector including ADWEC have been subject to CPI-X regulation. This means that their allowed revenues are constrained to change each year by a measure of price inflation (represented by the UAE CPI) less a factor X. The factor X is set to reflect a number of considerations particularly the profiling of the future revenue. In the case of ADWEC, the CPI-X regulation has applied to its procurement costs only, with PWPA and fuel costs allowed a pass-through treatment on an actual basis, subject to economic purchasing obligations.

Considerations

2.12 To ensure consistency in the regulatory framework established for the sector, we believe that all the monopoly companies should remain subject to CPI-X type of regulation. We consider that the efficiency incentives inherent in this approach are consistent with our statutory duty towards an efficient and economic sector.

2.13 However, the form of present controls for ADWEC has been set to be more cost-reflective than CPI-X regulation. This has been done to address the uncertainties specific to ADWEC’s business because ADWEC’s procurement business is different from the other monopoly companies in the sector. ADWEC does not have the financial capability to manage uncertainties and risks, such as those arising from:

(a) a smaller capital base, compared to large cash flows ADWEC handles;

(b) potential contractual issues relating to ‘change in law’ and liquidated damages payable by or to the production companies;

(c) responsibility for forecasting, planning and procurement of production capacities having significant impact on the rest of the sector;

(d) major changes in workload and staff requirements from time to time relative to the size of its business; and

(e) trading with other Emirates or countries.

2.14 The last price control review concluded that it was appropriate for ADWEC to have a more flexible regulatory arrangement, whereby the allowed procurement costs could be adjusted each year if the circumstances required. Accordingly, while the main structure of the MAR formula for ADWEC was unchanged from previous price controls, the notified value “A” for the price-controlled procurement was allowed to adjust each year to reflect ADWEC’s performance or requirements (rather than CPI adjustment only). The related structure and adjustments are described in Section 1 of this paper.

Issues for consultation

2.15 In view of the above, the Bureau’s current thinking is to retain:

(a) the present CPI-X form of price controls for ADWEC focusing on its procurement costs; and

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 27 of 40

(b) the flexible regulatory framework allowing annual adjustments to cater for uncertainties that ADWEC may face, for example, in terms of its obligations or requirements.

Scope and separation of controls

Current arrangements

2.16 The scope of present price controls covers only the Licensed Activities of ADWEC. Further, there are separate price controls for licensed electricity and water procurement businesses.

2.17 The Unlicensed Activities involving sale of water and electricity to other Emirates and GCC countries are not subject to the price controls.

Considerations

2.18 There are three potential changes that can be considered in relation to the scope of ADWEC’s price controls:

(a) treatment of liquidated damages under PWPAs;

(b) treatment of profits from Unlicensed Activities; and

(c) introduction of new supply businesses.

Treatment of liquidated damages under PWPAs

2.19 Currently, the liquidated damages received by ADWEC from IWPPs are outside the scope of price controls (through the licence definition of PWPA costs for the MAR formulas) and are allowed to be retained by ADWEC. This has resulted in significant profits for ADWEC in certain years and has incentivised ADWEC to pursue efficiently the PWPA compliance or the receipt of liquidated damages from IWPPs.

2.20 We note that this income is from the Licensed Activities and any risks of non-performance by IWPPs giving rise to such liquidated damages are ultimately borne by the sector. Therefore, it can be argued that all or some part of it should be shared in full or part with ADWEC’s customers and ultimately with the final customers or government to reduce customer tariffs or subsidy.

Treatment of profits from Unlicensed Activities

2.21 As ADWEC has a very large turnover but low capital base, it has relied on implicit or explicit guarantees from its parent organisation (ADWEA) to mitigate any risk exposure. Were ADWEC a standalone company, it would require considerable capital base to withstand such risks.

2.22 Allowing ADWEC to retain the profit (as retained earnings on its balance sheet) from its activities has been the main means of building its capital base. In particular, ADWEC’s profit from the Unlicensed Activities has increased significantly in recent years. This is because, on average, the tariff charged for these activities was higher than the average

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 28 of 40

production costs of electricity and water in the sector. While the Bureau currently does not regulate the tariffs for these activities in the same manner as the BST for the Licensed Activities, the Bureau requires these tariffs to be cost-reflective and not to receive any cross-subsidy from the Licensed Activities. This is achieved through the Bureau’s consents under ADWEC’s licence for the Unlicensed Activities and the Bureau’s guidelines for cost allocation for the purpose of SBAs. ADWEC’s retained earnings (due principally to accumulated profits from Unlicensed Activities) were around AED 4.1 billion at the end of 2013.

2.23 Profits from the Unlicensed Activities are possible only because ADWEC undertakes the Licensed Activities. At the last price control review for PC4A, we initially proposed that once ADWEC is adequately capitalised (with AED 2 billion in the retained earnings), ADWEC can retain 10% of future profits up to a maximum of AED 100 million per annum, and the remaining profits should be passed on to the customers in terms of lower BST. However, the PC4A final proposals adopted a regulatory policy that ADWEC should retain only the first AED 100 million of such profits each year to build its capital base and then pass the remaining profits to the BST customers.

2.24 While we can assess the implementation of this regulatory policy to date and the need for any revision of this policy, the current amount of retained earnings (AED 4.1 billion as of the end of 2013) in our view indicates sufficient capital base for ADWEC. More importantly, our recent discussions with ADWEC have concluded that:

(a) ADWEC would apply BST charges to the Unlicensed Activities for a pre-defined quantity of exports to the Northern Emirates and higher charges for additional exports.

(b) The resulting additional revenue from the Unlicensed Activities over and above the BST charges would be passed on to the customers of the Licensed Activities in full by accounting for all revenue from the Unlicensed Activities, along with the Licensed Activities, towards the recovery of Maximum Allowed Revenue (MAR).

2.25 To achieve this, the scope of price controls should be extended to cover both Licensed and Unlicensed Activities (with the separation between water and electricity retained) so that the total revenue from both sets of activities will be capped by the MAR formulas. This will eliminate excessive profits from the Unlicensed Activities, by reducing the BST revenue to be collected from the Licensed Activities.

2.26 Further, the present methods for presentation and allocation of incomes and costs in the SBAs and PCRs of ADWEC will continue to ensure separation and transparency of the financial implications of the Licensed and Unlicensed Activities. This arrangement would also align with the price controls for TRANSCO which covers similar licensed and unlicensed activities.

Introduction of new supply businesses

2.27 Finally, the scope of price controls could be extended to cover the new supply businesses if ADWEC is authorised to undertake them as the Licensed Activities. Our PC4A final proposals explained in detail the consequent changes to the price controls. In essence, two new separate price controls can be developed to apply to water and electricity supply businesses to ensure transparency and ring-fencing of income, costs

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 29 of 40

and subsidy of these businesses. For each supply control, the MAR formula can comprise of the BST and TUoS costs as pass-through items (similar to PWPA and fuel costs under MAR formulas for procurement businesses) and ADWEC’s own supply business costs subject to CPI-X indexation and other annual adjustments (see paragraph 2.38 below).

Issues for consultation

2.28 Should the scope of price controls be extended to cover the following three items or consider other alternatives to deal with them:

(a) liquidated damages received from IWPPs (to allow them to be shared with the customers);

(b) Unlicensed Activities (to allow ADWEC a management fee in the form of additional procurement cost allowances within the procurement price controls); and/or

(c) new water and electricity supply businesses if introduced as Licensed Activities (via new separate price controls for supply businesses)?

Cost pass-through arrangements

Current arrangements

2.29 To date, the PWPA and fuel costs paid by ADWEC to the production companies for purchase of water and electricity capacity and output have been allowed a pass-through treatment under the MAR formulas, based on actual costs and subject to satisfying the economic purchasing obligations under Law No (2) of 1998 and ADWEC’s licence.

Considerations

2.30 PWPA and fuel costs paid to external parties account for almost all the costs incurred by ADWEC. By contrast, its internal costs are small and comprise mainly staff costs and administrative expenses (termed as procurement costs). Further, PWPA and fuel costs amount to more than half of the sector turnover. To ensure economic purchasing of water and electricity by ADWEC, we rely on the competitive tendering undertaken to award IWPP contracts, based on the lowest levelised unit costs of electricity and water over the PWPA term.

2.31 In the case of renewable energy projects developed to date in the Emirate of Abu Dhabi, electricity prices have not been determined directly from such a competitive tendering. For such cases, we determine a reasonable price based on the assessment of tendering, cost estimates and benchmarking. For all future RE projects, we believe that an IPP/IWPP-style tendering approach used in the sector should be adopted to achieve the lowest levelised cost of electricity encompassing all costs in a single tendering.

2.32 Given ADWEC’s small capital base, incentivising efficient procurement and use of production capacity and fuel is challenging in regulating ADWEC, without risking its financial position. Further, the PWPA prices in Abu Dhabi are also considered to be

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 30 of 40

reasonable. However, it would be sensible to incentivise ADWEC to prepare timely and robust capacity planning statements and fuel requirement forecasts and to take the initiative for arranging long-term fuel supplies at reasonable prices and with reasonable security.

2.33 At a meeting on 16 December 2014, ADWEC highlighted its recent efforts to reduce the fuel costs by enhancement to a production plant, changes to the swap arrangements between its gas suppliers and renting of a fuel pipeline (originally dedicated to ADWEC only) for other users. ADWEC suggested that it should be rewarded for such initiatives in order to continue its efforts that benefit the sector. Section 4 discusses this matter, as well as better fuel planning and procurement and improved contract management and compliance reporting of production plant, and makes suggestion on how to incentivise such endeavours.

Issues for consultation

2.34 Our current thinking is to retain the existing pass-through arrangements for PWPA and fuel costs. However, we seek views on how best to incentivise ADWEC to perform its obligations in relation to capacity planning and fuel supplies.

Structure of controls

Current structure

2.35 Section 1 describes the structure of the current price controls in the form of annual MAR for ADWEC’s Licensed Activities as follows:

MAR = PWPA costs + Fuel costs + Procurement cost allowance + Incentives – Correction factor

2.36 Currently, there are separate price controls for the water and electricity businesses of ADWEC’s Licensed Activities.

Considerations

2.37 The discussions in this section suggest that the existing structure of price controls or MAR formula for the procurement businesses should be retained in its general form, with the following elements, given their desirable features and their consistency over time:

(a) Current MAR formula structure;

(b) Current pass-through treatment of PWPA and fuel costs;

(c) Current separation of controls between water and electricity businesses;

(d) Current scope of controls, that covers only the Licensed Activities – pending consultation on the potential changes discussed earlier to cover liquidated damages received from production companies and Unlicensed Activities;

(e) Current scope of price-controlled procurement costs to cover staff costs, depreciation, administrative expenses, and a nominal profit element and current automatic annual CPI-X indexation of such costs; and

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 31 of 40

(f) Incentives through the Q term, with necessary changes discussed below and in Section 3.

2.38 If it is agreed that ADWEC should undertake supply businesses as new Licensed Activities, then we would need to develop two new separate price controls to apply for water and electricity supply businesses as discussed in paragraph 2.27 above. In this regard, we propose that the price controls for ADWEC’s supply businesses should also be in the form of revenue caps, defining Maximum Allowed Revenue (MAR) for each year of the price control duration as follows:

MARS = BST costs + TUoS costs + Supply cost allowance + Incentives – Correction factor

Issues for consultation

2.39 Our current thinking is to retain the existing structure of price controls or MAR formula for the procurement businesses in its general form and adopt similar structure and MAR formula for the new supply businesses. However, some changes could be considered to the scope of controls for the procurement businesses (as discussed earlier) and to the annual adjustments to the notified values “A” (as discussed later in this section and Section 4).

Annual adjustment mechanism

Current adjustments

2.40 Section 1 describes the current framework for determining the price-controlled procurement cost for each year of the PC4A period, once the notified value ‘A’ was set by the Bureau for the first year of the control period. This framework requires the value of A for any year t to be calculated as follows:

A t = A t-1 (1 + CPIt) (1 + Dt) (1 + S1t) (1 + S2t)

2.41 This involves:

(a) annual adjustment for standard CPI-X indexation;

(b) annual adjustment for actual cost deviation (D), allowing actual procurement cost deviation in full in the preceding year upto +/-10% and half of such deviation beyond +/-10%; and

(c) an annual downward adjustment (through S1 and S2 factors) for ADWEC’s failure to submit the final draft 7YS or BST by 31 May or 30 November, respectively, by 1% for each month of delay in such submission up to a maximum of 5% adjustment in each case.

Considerations

2.42 The annual adjustment for cost deviation provides flexibility to address risks and uncertainties (including increase in staff costs and allowances) for ADWEC, as well as gives the incentives to reduce costs. It will be useful to assess the performance of this adjustment mechanism. So far, a high-level analysis in Section 1 suggests it has helped

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 32 of 40

ADWEC manage its costs within the price control allowance. Therefore, our current thinking is to retain this adjustment for the new price controls.

2.43 Further, it will be sensible to consider adjustments to costs during the control period for any additional costs arising from a work required or approved by the Bureau. This could be used to allow pass-through treatment of the Bureau’s project-specific licence fee as well as additional costs arising from Emiratisation (to the extent the total number of staff does not increase, except otherwise allowed).

2.44 Consistent with our PC5 final proposals for the network companies, we could incorporate a provisional allowance for Emiratisation at this review based on a reasonable assumption about future Emiratisation rate and an additional unit staff cost for the UAE National as compared to an expat employee. The allowance can cover additional training requirements for the UAE National staff. This provisional allowance can then adjust each year for the actual Emiratisation rate achieved in the year and actual training requirements. It is however possible that the adjustments to provisional allowances may be captured automatically by the existing adjustment mechanism for cost deviation and may not be required separately.

2.45 With regard to the adjustments for performance obligations on 7YS and BST, these reflect the fact that the costs of meeting these important obligations in a timely manner are already financed in the allowed procurement costs. It seems reasonable that a failure to perform them should take away some of the allowed funds. However, we are not convinced that this mechanism has worked satisfactorily. Perhaps, a more step-by-step detailed requirement for each obligation should be set out upfront with appropriate incentive provided for each step. Further, the present adjustment appears to be penalty-only and could be replaced by a more symmetric incentive, that involves both bonus and penalty to encourage the desired behaviour. Overall, we believe that these refinements will be better achieved by incentivising these obligations through the Q term, in line with other incentives for ADWEC. This should simplify the determination of price-controlled procurement costs and operation of price controls for ADWEC. It should also streamline all the incentives in the Q term and provide consistency across the regulation of different companies in the sector.

Issues for consultation

2.46 Our current thinking is to retain the annual adjustments to price-controlled procurement costs for cost deviations.

2.47 It is for consideration whether the procurement costs should be adjusted each year to allow pass-through of:

(a) the Bureau’s project-specific licence fee;

(b) the additional costs arising from new tasks or obligation approved by the Bureau; and

(c) the additional costs arising from change in actual Emiratisation rate or actual training course requirements for the UAE National staff compared to assumptions used in setting the initial notified values of “A” to the extent not already covered by the existing annual adjustment mechanism for cost deviations.

2015 Price Control Review for ADWEC – PC5A First Consultation Paper

Author Document Version Publication date Approved by

AR/KM/SI/NB EC/E02/100 Issue 1 28 January 2015 SSQ Page 33 of 40