2015 shakopee communication letter

TRANSCRIPT

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 1/22

City of Shakopee

Communications Letter

December 31, 2015

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 2/22

City of Shakopee Table of Contents

Report on Matters Identified as a Result ofthe Audit of the Financial Statements 1

Significant Deficiency 3

Other Deficiencies 4

Required Communication 5

Financial Analysis 8

Emerging Issues 19

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 3/22

1

Report on Matters Identified as a Result of

the Audit of the Financial Statements

Honorable Mayor, Membersof the City Council and Management

City of ShakopeeShakopee, Minnesota

In planning and performing our audit of the financial statements of the City of Shakopee,Minnesota, as of and for the year ended December 31, 2015, in accordance with auditingstandards generally accepted in the United States of America, we considered the City’s

internal control over financial reporting (internal control) as a basis for designing auditing procedures that are appropriate in the circumstances for the purpose of expressing ouropinion on the financial statements, but not for the purpose of expressing an opinion on theeffectiveness of the City’s internal control. Accordingly, we do not express an opinion onthe effectiveness of the City’s internal control.

Our consideration of internal control was for the limited purpose described in the preceding paragraph and was not designed to identify all deficiencies in internal control that might bematerial weaknesses or significant deficiencies and, therefore, material weaknesses orsignificant deficiencies may exist that were not identified.

A deficiency in internal control exists when the design or operation of a control does notallow management or employees, in the normal course of performing their assignedfunctions, to prevent, or detect and correct, misstatements on a timely basis. A materialweakness is a deficiency, or a combination of deficiencies in internal control, such that thereis a reasonable possibility that a material misstatement of the City’s financial statements willnot be prevented, or detected and corrected on a timely basis. We did not identify anydeficiencies in internal control that we consider to be material weaknesses.

A significant deficiency is a deficiency, or a combination of deficiencies, in internal controlthat is less severe than a material weakness, yet important enough to merit attention by thosecharged with governance. The significant deficiency identified is stated within this letter.

During our audit, we also became aware of deficiencies in internal control other thansignificant deficiencies or material weaknesses, and other matters that are opportunities forstrengthening internal controls and operating efficiency. They are described in theaccompanying letter under Other Deficiencies.

The accompanying memorandum also includes financial analysis provided as a basis fordiscussion. The matters discussed herein were considered by us during our audit and they donot modify the opinion ex pressed in our Independent Auditor’s Report dated May 23, 2016,on such statements.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 4/22

2

This communication is intended solely for the information and use of management, the CityCouncil, others within the City and state oversight agencies and is not intended to be andshould not be used by anyone other than these specified parties.

St. Cloud, MinnesotaMay 23, 2016

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 5/22

3

City of Shakopee

Significant Deficiency

LACK OF SEGREGATION OF ACCOUNTING DUTIES

Adequate segregation of accounting duties is in place when the four areas of a transaction have beenseparated: authorization, custody, recording, and reconciliation. During 2015, the City did not havesufficient staff to segregate the duties listed above. The lack of adequate segregation of accountingduties could adversely affect the City’s ability to initiate, record, process, and report financial dataconsistent with the assertions of managements in the financial statements. Specific areas where there is alack of internal controls include (but is not all-inclusive):

PayrollThe Payroll Clerk processes payroll, posts payroll to the general ledger, issues direct deposits, prepares the payroll taxes, initiates transfers for payment of payroll, prepares all W-2s, andmaintains all data files as well as the payroll program.

Cash ReceiptsDeposits at City Hall – The front desk personnel receives money, codes the revenue, and prepares bank deposits. The Accounting Manager reconciles cash and posts all deposits into the generalledger.

Deposits at Recreation Center – One employee is able to receipt money and prepare the bankdeposit.

Cash Disbursements

The Accounting Clerk enters invoices, matches purchase orders to invoices, and prepares checks for payment. The Accounting Manager reconciles cash.

Management is aware of this condition and has taken certain steps to compensate for the lack ofsegregation but due to the number of staff needed to properly segregate all of the accounting duties, thecosts of obtaining desirable segregation of accounting duties often exceeds benefits which could bederived. However, management must remain aware of this situation and should continually monitor theaccounting system, including changes that occur.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 6/22

4

City of Shakopee

Other Deficiencies

IMPROVE ICE ARENA RECEIPTING INTERNAL CONTROL

During our audit, we analyzed the receipts collection process of the ice arena and found the process to be decentralized from the City’s regular receipting process. Currently, the City employs an Ice ArenaManager who collects and records funds and also maintains copies of signed ice rental contracts and alist of payers, creating a segregation of duties incompatibility.

Areas where controls could be implemented include:

Segregate duties so that employees are not able to receipt money, prepare reconciliations, and prepare the deposit

Have an employee independent of collecting the cash maintain and create the billing contracts toensure that all the contracts are being billed and the revenue is being deposited by the City

Check ice arena schedules to contracts to ensure that all ice time is being billed

To improve internal control over the ice arena receipting process and to prevent potential omissions anderrors, we recommend the City implement additional oversight procedures to ensure the accuracy andcompleteness of ice arena receipts.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 7/22

5

City of Shakopee

Required Communication

We have audited the basic financial statements of the City for the year ended December 31, 2015, andhave issued our report dated May 23, 2016. Professional standards require that we provide you with thefollowing information related to our audit.

OUR RESPONSIBILITY UNDER AUDITING STANDARDS GENERALLY ACCEPTED IN

THE UNITED STATES OF AMERICA AND GOVERNMENT AUDITING STANDARDS

As stated in our engagement letter, our responsibility, as described by professional standards, is toexpress an opinion about whether the financial statements prepared by management with your oversightare fairly presented, in all material respects, in conformity with accounting principles generally acceptedin the United States of America. Our audit of the financial statements does not relieve you ormanagement of your responsibilities.

As part of our audit, we considered the internal control of the City. Such considerations were solely for

the purpose of determining our audit procedures and not to provide any assurance concerning suchinternal control.

As part of obtaining reasonable assurance about whether the financial statements are free of materialmisstatement, we performed tests of the City's compliance with certain provisions of laws, regulations,contracts, and grants. However, the objective of our tests was not to provide an opinion on compliancewith such provisions.

Our responsibility for the supplementary information accompanying the financial statements, asdescribed by professional standards, is to evaluate the presentation of the supplementary information inrelation to the financial statements as a whole and to report on whether the supplementary information is

fairly stated, in all material respects, in relation to the financial statements as a whole.

PLANNED SCOPE AND TIMING OF THE AUDIT

An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in thefinancial statements; therefore, our audit involved judgment about the number of transactions to beexamined and the areas to be tested.

Our audit included obtaining an understanding of the City and its environment, including internalcontrol, sufficient to assess the risks of material misstatement of the financial statements and to designthe nature, timing, and extent of further audit procedures. Material misstatements may result from

(1) errors, (2) fraudulent financial reporting, (3) misappropriation of assets, or (4) violations of laws orgovernmental regulations that are attributable to the City, or to acts by management or employees actingon behalf of the City.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 8/22

6

City of Shakopee

Required Communication

QUALITATIVE ASPECTS OF ACCOUNTING PRACTICES

Management is responsible for the selection and use of appropriate accounting policies. The significantaccounting policies used by the City are described in Note 1 to the financial statements. No newaccounting policies were adopted and the application of existing policies was not changed during theyear ended December 31, 2015. We noted no transactions entered into by the City during the year forwhich there is a lack of authoritative guidance or consensus. All significant transactions have beenrecognized in the financial statements in the proper period.

Accounting estimates are an integral part of the financial statements prepared by management and are based on management’s knowledge and experience about past and current events and assumptions aboutfuture events. Certain accounting estimates are particularly sensitive because of their significance to thefinancial statements and because of the possibility that future events affecting them may differsignificantly from those expected. The most sensitive estimates affecting the financial statements were:

Depreciation – The City is currently depreciating its capital assets over their estimated useful lives,as determined by management, using the straight-line method.

Expense/Expenditure Allocation – The City is currently allocating certain costs among the programsand supporting services benefited. The costs are allocated based on management’s estimates.

Net Other Post Employment Benefits (OPEB) Obligation – This liability is based on an actuarialstudy using estimates of future obligations of the City for post-employment benefits.

Net Pension Liability, Deferred Outflows of Resources Relating to Pension Activity, and Deferred

Inflows of Resources relating to Pension Activity – These balances are based on an allocation by the pension plans using estimates based on contributions.

The financial statement disclosures are neutral, consistent, and clear.

DIFFICULTIES ENCOUNTERED IN PERFORMING THE AUDIT

We encountered no significant difficulties in dealing with management in performing and completingour audit.

CORRECTED AND UNCORRECTED MISSTATEMENTS

Professional standards require us to accumulate all misstatements identified during the audit, other thanthose that are clearly trivial, and communicate them to the appropriate level of management.Management did not identify and we did not notify them of any uncorrected financial statementmisstatements.

In addition, none of the misstatements detected as a result of audit procedures and corrected bymanagement were material, either individually or in the aggregate, to the financial statements taken as awhole.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 9/22

7

City of Shakopee

Required Communication

DISAGREEMENTS WITH MANAGEMENT

For purposes of this letter, a disagreement with management is a financial accounting, reporting, orauditing matter, whether or not resolved to our satisfaction that could be significant to the financialstatements or the auditor ’s report. We are pleased to report that no such disagreements arose during thecourse of our audit.

MANAGEMENT REPRESENTATIONS

We requested certain representations from management that are included in the managementrepresentation letter.

MANAGEMENT CONSULTATIONS WITH OTHER ACCOUNTANTS

In some cases, management may decide to consult with other accountants about auditing and accountingmatters, similar to obtaining a “second opinion” on certain situations. If a consultation involvesapplication of an accounting principle to the City’s financial statements or a determination of the type ofauditor’s opinion that may be expressed on those statements, our professional standards require theconsulting accountant to check with us to determine that the consultant has all the relevant facts. To ourknowledge, there were no such consultations with other accountants.

OTHER AUDIT FINDINGS OR ISSUES

We generally discuss a variety of matters, including the application of accounting principles andauditing standards, with management each year prior to retention as the City’s auditors. However, these

discussions occurred in the normal course of our professional relationship and our responses were not acondition to our retention.

OTHER MATTERS

With respect to the supplementary information accompanying the financial statements, we made certaininquiries of management and evaluated the form, content and methods of preparing the information todetermine that the information complies with accounting principles generally accepted in the UnitedStates of America, the method of preparing it has not changed from the prior period, and the informationis appropriate and complete in relation to our audit of the financial statements. We compared andreconciled the supplementary information to the underlying accounting records used to prepare the

financial statements or to the financial statements themselves.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 10/22

City of ShakopeeFinancial Analysis

8

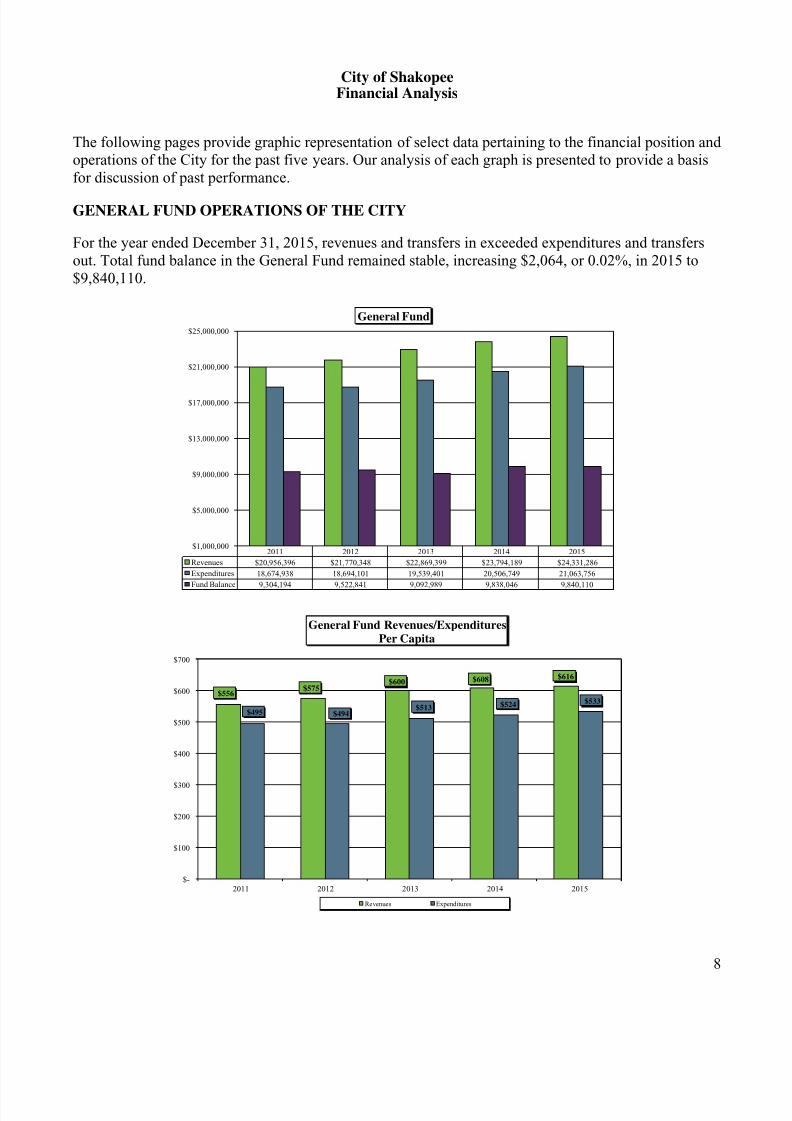

The following pages provide graphic representation of select data pertaining to the financial position andoperations of the City for the past five years. Our analysis of each graph is presented to provide a basisfor discussion of past performance.

GENERAL FUND OPERATIONS OF THE CITY

For the year ended December 31, 2015, revenues and transfers in exceeded expenditures and transfersout. Total fund balance in the General Fund remained stable, increasing $2,064, or 0.02%, in 2015 to$9,840,110.

2011 2012 2013 2014 2015

Revenues $20,956,396 $21,770,348 $22,869,399 $23,794,189 $24,331,286

Expenditures 18,674,938 18,694,101 19,539,401 20,506,749 21,063,756

Fund Balance 9,304,194 9,522,841 9,092,989 9,838,046 9,840,110

$1,000,000

$5,000,000

$9,000,000

$13,000,000

$17,000,000

$21,000,000

$25,000,000

General Fund

$556$575

$600 $608 $616

$495 $494$513 $524 $533

$-

$100

$200

$300

$400

$500

$600

$700

2011 2012 2013 2014 2015

General Fund Revenues/ExpendituresPer Capita

Revenues Expenditures

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 11/22

City of ShakopeeFinancial Analysis

9

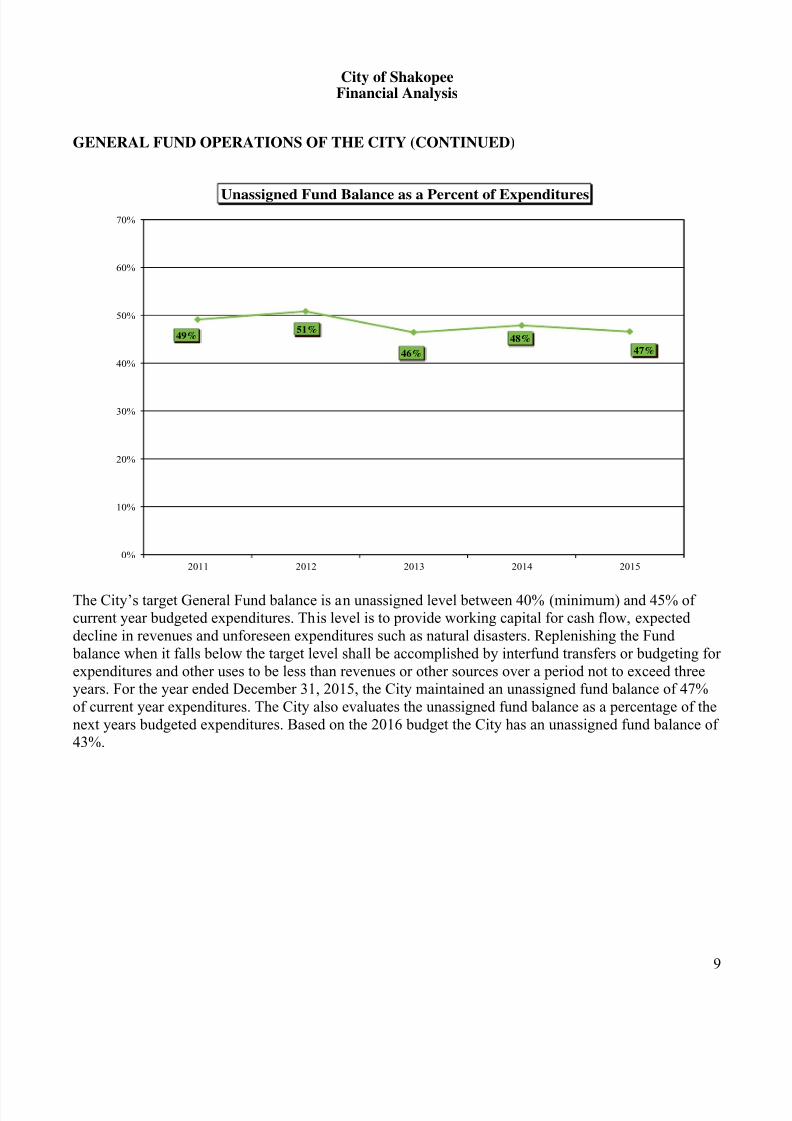

GENERAL FUND OPERATIONS OF THE CITY (CONTINUED)

49%51%

46%

48%

47%

0%

10%

20%

30%

40%

50%

60%

70%

2011 2012 2013 2014 2015

Unassigned Fund Balance as a Percent of Expenditures

The City’s target General Fund balance is an unassigned level between 40% (minimum) and 45% ofcurrent year budgeted expenditures. This level is to provide working capital for cash flow, expecteddecline in revenues and unforeseen expenditures such as natural disasters. Replenishing the Fund balance when it falls below the target level shall be accomplished by interfund transfers or budgeting forexpenditures and other uses to be less than revenues or other sources over a period not to exceed threeyears. For the year ended December 31, 2015, the City maintained an unassigned fund balance of 47%of current year expenditures. The City also evaluates the unassigned fund balance as a percentage of thenext years budgeted expenditures. Based on the 2016 budget the City has an unassigned fund balance of43%.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 12/22

City of ShakopeeFinancial Analysis

10

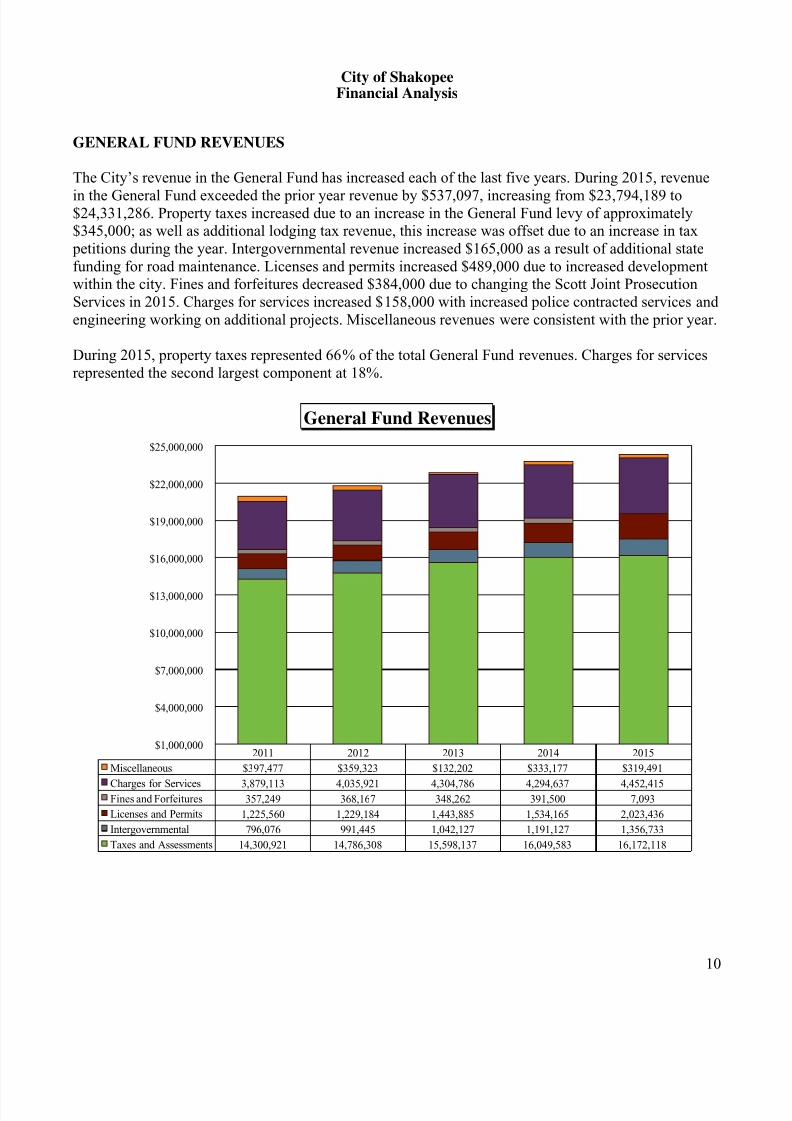

GENERAL FUND REVENUES

The City’s revenue in the General Fund has increased each of the last five years. During 2015, revenue

in the General Fund exceeded the prior year revenue by $537,097, increasing from $23,794,189 to$24,331,286. Property taxes increased due to an increase in the General Fund levy of approximately$345,000; as well as additional lodging tax revenue, this increase was offset due to an increase in tax petitions during the year. Intergovernmental revenue increased $165,000 as a result of additional statefunding for road maintenance. Licenses and permits increased $489,000 due to increased developmentwithin the city. Fines and forfeitures decreased $384,000 due to changing the Scott Joint ProsecutionServices in 2015. Charges for services increased $158,000 with increased police contracted services andengineering working on additional projects. Miscellaneous revenues were consistent with the prior year.

During 2015, property taxes represented 66% of the total General Fund revenues. Charges for servicesrepresented the second largest component at 18%.

2011 2012 2013 2014 2015

Miscellaneous $397,477 $359,323 $132,202 $333,177 $319,491

Charges for Services 3,879,113 4,035,921 4,304,786 4,294,637 4,452,415Fines and Forfeitures 357,249 368,167 348,262 391,500 7,093

Licenses and Permits 1,225,560 1,229,184 1,443,885 1,534,165 2,023,436

Intergovernmental 796,076 991,445 1,042,127 1,191,127 1,356,733

Taxes and Assessments 14,300,921 14,786,308 15,598,137 16,049,583 16,172,118

$1,000,000

$4,000,000

$7,000,000

$10,000,000

$13,000,000

$16,000,000

$19,000,000

$22,000,000

$25,000,000

General Fund Revenues

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 13/22

City of ShakopeeFinancial Analysis

11

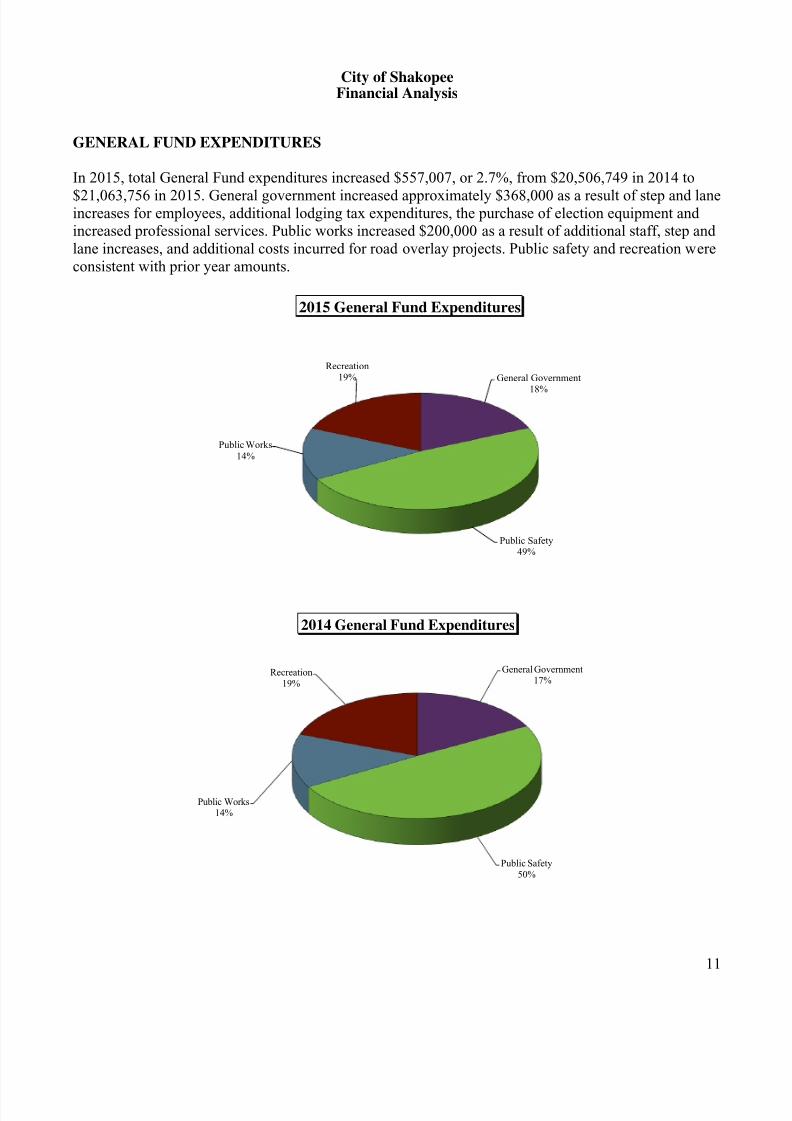

GENERAL FUND EXPENDITURES

In 2015, total General Fund expenditures increased $557,007, or 2.7%, from $20,506,749 in 2014 to

$21,063,756 in 2015. General government increased approximately $368,000 as a result of step and laneincreases for employees, additional lodging tax expenditures, the purchase of election equipment andincreased professional services. Public works increased $200,000 as a result of additional staff, step andlane increases, and additional costs incurred for road overlay projects. Public safety and recreation wereconsistent with prior year amounts.

General Government

18%

Public Safety49%

Public Works14%

Recreation19%

2015 General Fund Expenditures

General Government17%

Public Safety50%

Public Works14%

Recreation19%

2014 General Fund Expenditures

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 14/22

City of ShakopeeFinancial Analysis

12

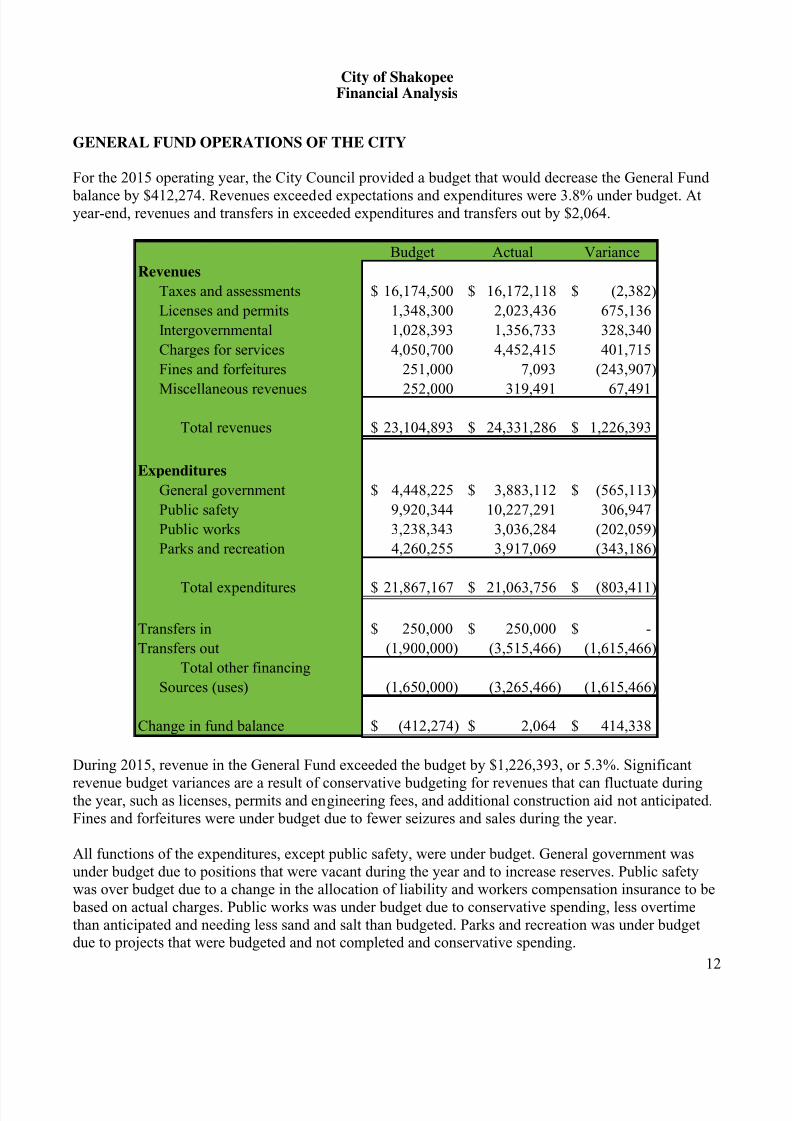

GENERAL FUND OPERATIONS OF THE CITY

For the 2015 operating year, the City Council provided a budget that would decrease the General Fund

balance by $412,274. Revenues exceeded expectations and expenditures were 3.8% under budget. Atyear-end, revenues and transfers in exceeded expenditures and transfers out by $2,064.

Budget Actual Variance

Revenues

Taxes and assessments 16,174,500$ 16,172,118$ (2,382)$

Licenses and permits 1,348,300 2,023,436 675,136

Intergovernmental 1,028,393 1,356,733 328,340

Charges for services 4,050,700 4,452,415 401,715

Fines and forfeitures 251,000 7,093 (243,907)

Miscellaneous revenues 252,000 319,491 67,491

Total revenues 23,104,893$ 24,331,286$ 1,226,393$

Expenditures

General government 4,448,225$ 3,883,112$ (565,113)$

Public safety 9,920,344 10,227,291 306,947

Public works 3,238,343 3,036,284 (202,059)

Parks and recreation 4,260,255 3,917,069 (343,186)

Total expenditures 21,867,167$ 21,063,756$ (803,411)$

Transfers in 250,000$ 250,000$ -$

Transfers out (1,900,000) (3,515,466) (1,615,466)

Total other financing

Sources (uses) (1,650,000) (3,265,466) (1,615,466)

Change in fund balance (412,274)$ 2,064$ 414,338$

During 2015, revenue in the General Fund exceeded the budget by $1,226,393, or 5.3%. Significant

revenue budget variances are a result of conservative budgeting for revenues that can fluctuate duringthe year, such as licenses, permits and engineering fees, and additional construction aid not anticipated.Fines and forfeitures were under budget due to fewer seizures and sales during the year.

All functions of the expenditures, except public safety, were under budget. General government wasunder budget due to positions that were vacant during the year and to increase reserves. Public safetywas over budget due to a change in the allocation of liability and workers compensation insurance to be based on actual charges. Public works was under budget due to conservative spending, less overtimethan anticipated and needing less sand and salt than budgeted. Parks and recreation was under budgetdue to projects that were budgeted and not completed and conservative spending.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 15/22

City of ShakopeeFinancial Analysis

13

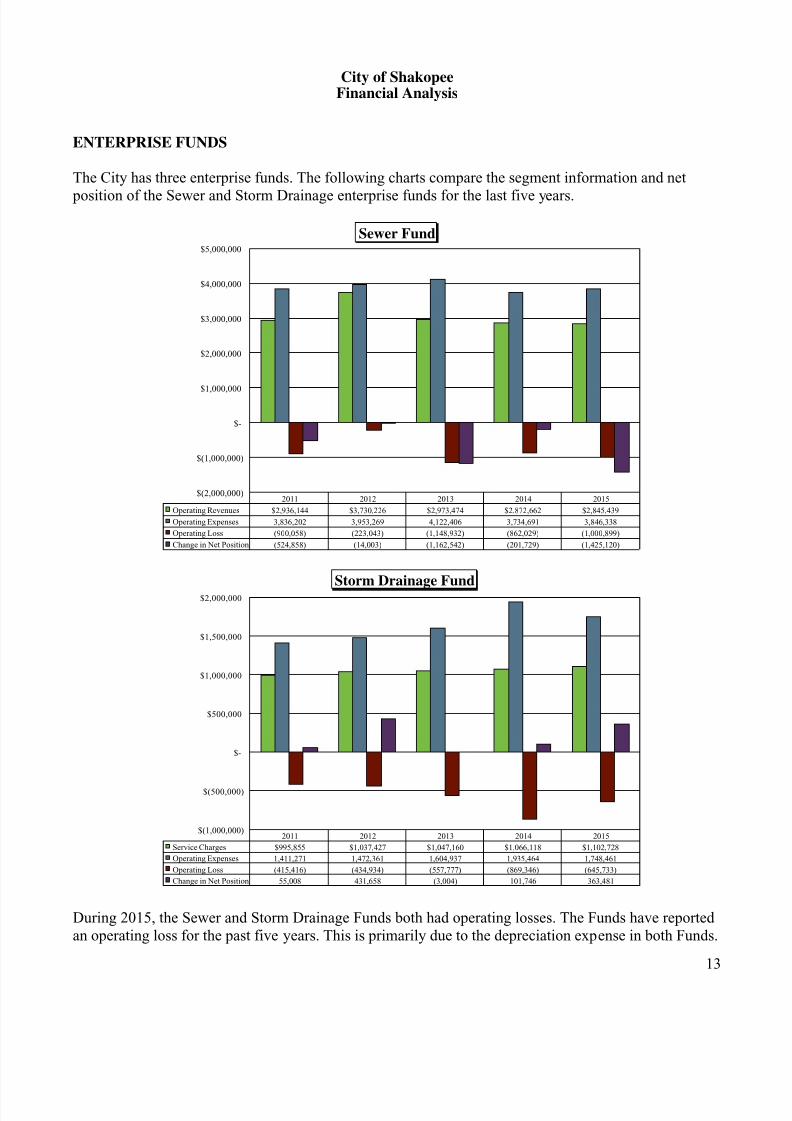

ENTERPRISE FUNDS

The City has three enterprise funds. The following charts compare the segment information and net

position of the Sewer and Storm Drainage enterprise funds for the last five years.

2011 2012 2013 2014 2015

Operating Revenues $2,936,144 $3,730,226 $2,973,474 $2,872,662 $2,845,439

Operating Expenses 3,836,202 3,953,269 4,122,406 3,734,691 3,846,338

Operating Loss (900,058) (223,043) (1,148,932) (862,029) (1,000,899)

Change in Net Position (524,858) (14,003) (1,162,542) (201,729) (1,425,120)

$(2,000,000)

$(1,000,000)

$-

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

Sewer Fund

2011 2012 2013 2014 2015

Service Charges $995,855 $1,037,427 $1,047,160 $1,066,118 $1,102,728

Operating Expenses 1,411,271 1,472,361 1,604,937 1,935,464 1,748,461

Operating Loss (415,416) (434,934) (557,777) (869,346) (645,733)

Change in Net Position 55,008 431,658 (3,004) 101,746 363,481

$(1,000,000)

$(500,000)

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

Storm Drainage Fund

During 2015, the Sewer and Storm Drainage Funds both had operating losses. The Funds have reportedan operating loss for the past five years. This is primarily due to the depreciation expense in both Funds.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 16/22

City of ShakopeeFinancial Analysis

14

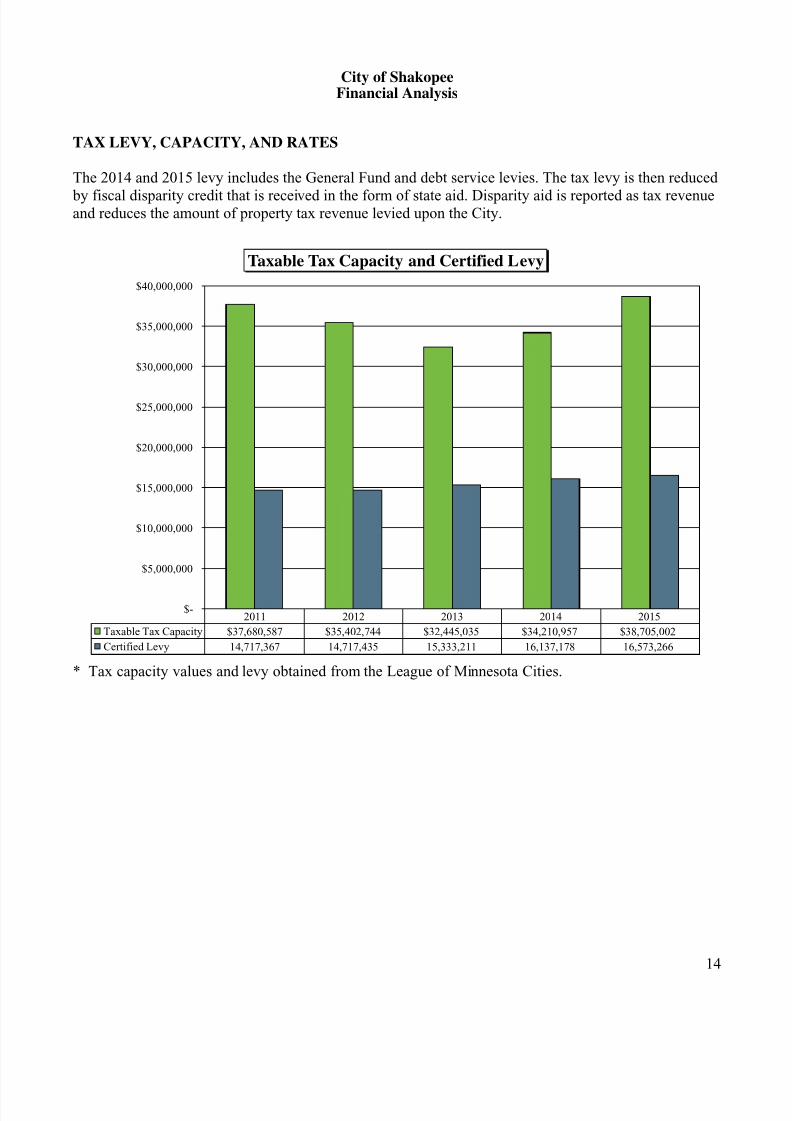

TAX LEVY, CAPACITY, AND RATES

The 2014 and 2015 levy includes the General Fund and debt service levies. The tax levy is then reduced

by fiscal disparity credit that is received in the form of state aid. Disparity aid is reported as tax revenueand reduces the amount of property tax revenue levied upon the City.

2011 2012 2013 2014 2015

Taxable Tax Capacity $37,680,587 $35,402,744 $32,445,035 $34,210,957 $38,705,002

Certified Levy 14,717,367 14,717,435 15,333,211 16,137,178 16,573,266

$-

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

$40,000,000

Taxable Tax Capacity and Certified Levy

* Tax capacity values and levy obtained from the League of Minnesota Cities.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 17/22

City of ShakopeeFinancial Analysis

15

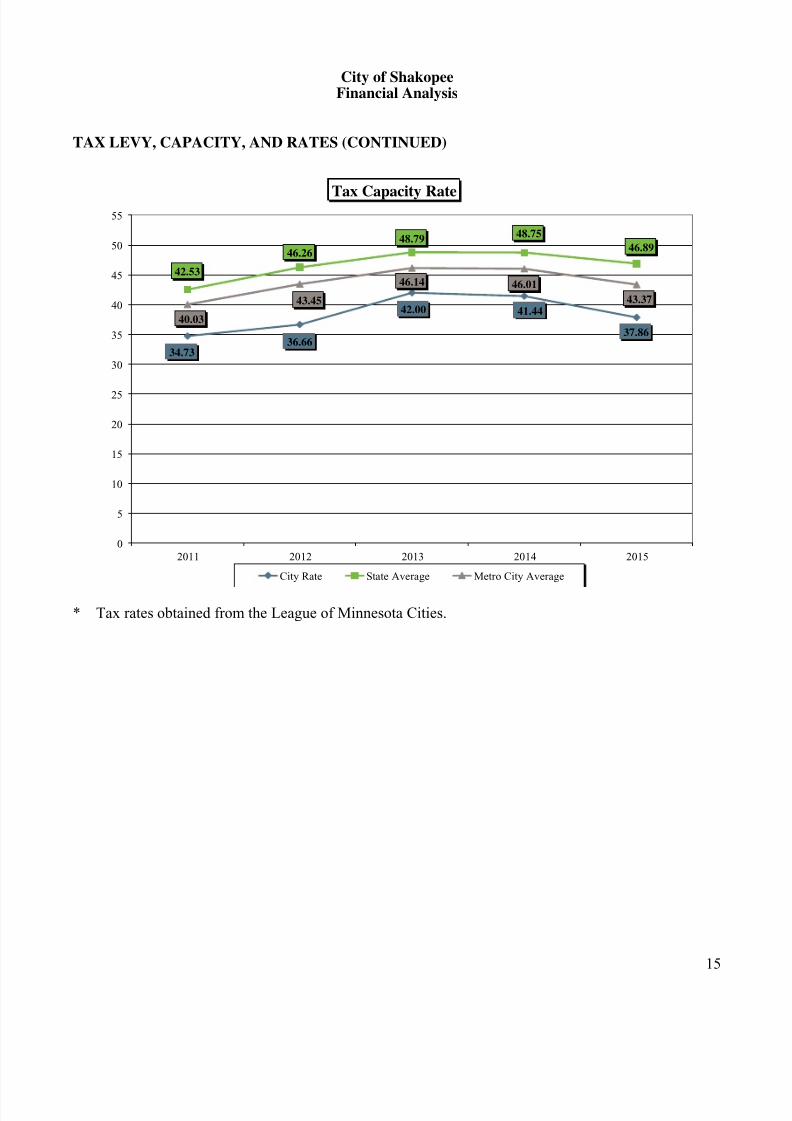

TAX LEVY, CAPACITY, AND RATES (CONTINUED)

34.7336.66

42.00 41.44

37.86

42.53

46.26

48.79 48.75

46.89

40.03

43.45

46.14 46.01

43.37

0

5

10

15

20

25

30

35

40

45

50

55

2011 2012 2013 2014 2015

Tax Capacity Rate

City Rate State Average Metro City Average

* Tax rates obtained from the League of Minnesota Cities.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 18/22

City of ShakopeeFinancial Analysis

16

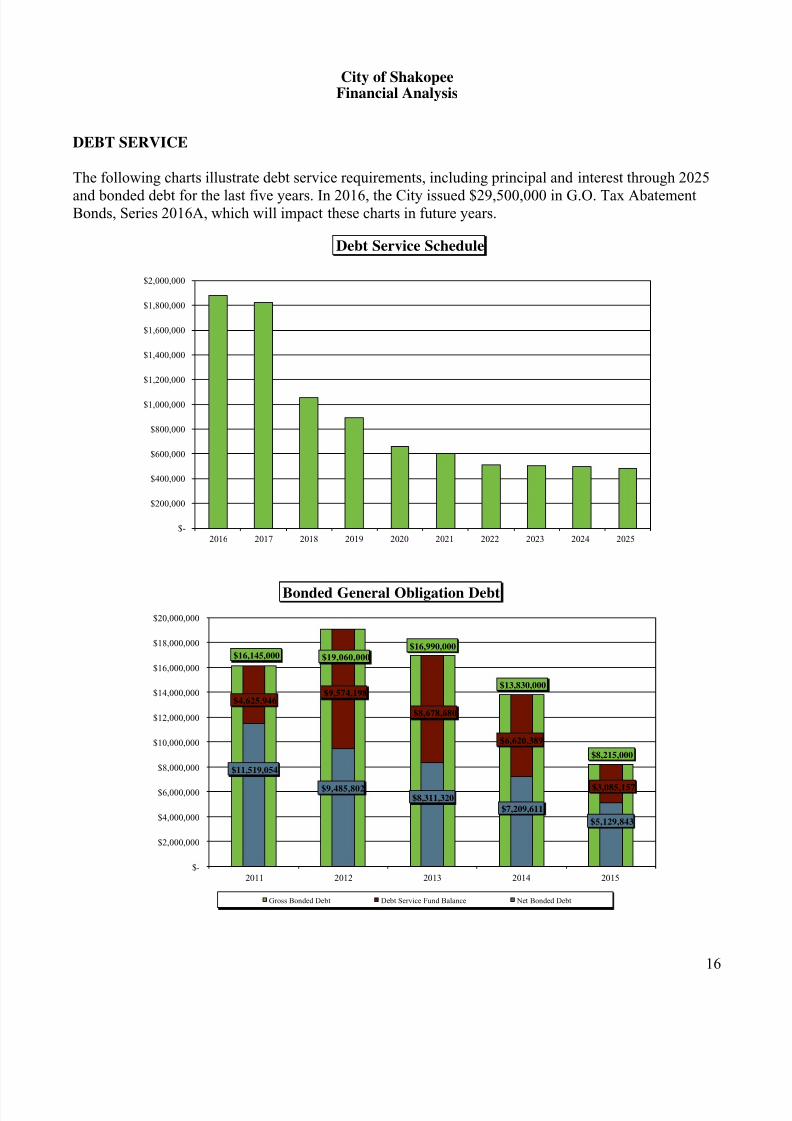

DEBT SERVICE

The following charts illustrate debt service requirements, including principal and interest through 2025

and bonded debt for the last five years. In 2016, the City issued $29,500,000 in G.O. Tax AbatementBonds, Series 2016A, which will impact these charts in future years.

$-

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Debt Service Schedule

$16,145,000 $19,060,000$16,990,000

$13,830,000

$8,215,000

$11,519,054

$9,485,802$8,311,320

$7,209,611

$5,129,843

$4,625,946$9,574,198

$8,678,680

$6,620,389

$3,085,157

$-

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

$18,000,000

$20,000,000

2011 2012 2013 2014 2015

Bonded General Obligation Debt

Gross Bonded Debt Debt Service Fund Balance Net Bonded Debt

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 19/22

City of ShakopeeFinancial Analysis

17

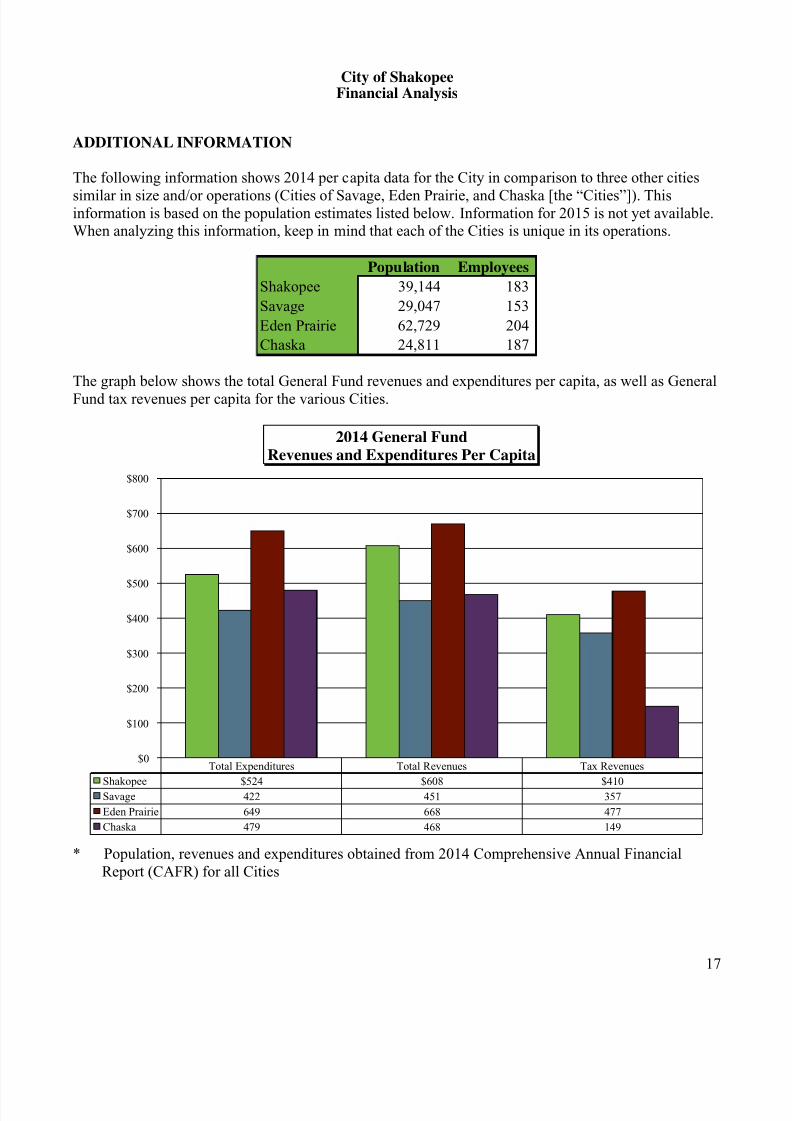

ADDITIONAL INFORMATION

The following information shows 2014 per capita data for the City in comparison to three other cities

similar in size and/or operations (Cities of Savage, Eden Prairie, and Chaska [the “Cities”]). Thisinformation is based on the population estimates listed below. Information for 2015 is not yet available.When analyzing this information, keep in mind that each of the Cities is unique in its operations.

Population Employees

Shakopee 39,144 183

Savage 29,047 153

Eden Prairie 62,729 204

Chaska 24,811 187

The graph below shows the total General Fund revenues and expenditures per capita, as well as GeneralFund tax revenues per capita for the various Cities.

Total Expenditures Total Revenues Tax Revenues

Shakopee $524 $608 $410Savage 422 451 357

Eden Prairie 649 668 477

Chaska 479 468 149

$0

$100

$200

$300

$400

$500

$600

$700

$800

2014 General FundRevenues and Expenditures Per Capita

* Population, revenues and expenditures obtained from 2014 Comprehensive Annual Financial

Report (CAFR) for all Cities

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 20/22

City of ShakopeeFinancial Analysis

18

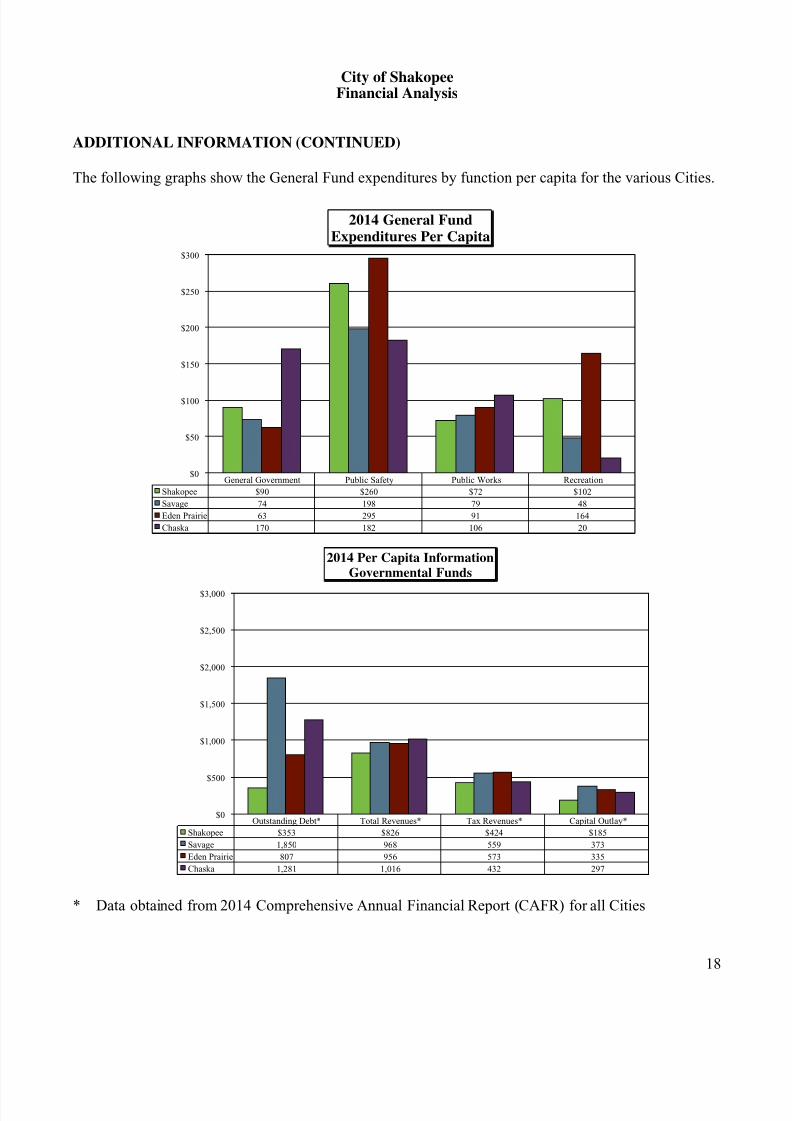

ADDITIONAL INFORMATION (CONTINUED)

The following graphs show the General Fund expenditures by function per capita for the various Cities.

General Government Public Safety Public Works Recreation

Shakopee $90 $260 $72 $102

Savage 74 198 79 48

Eden Prairie 63 295 91 164

Chaska 170 182 106 20

$0

$50

$100

$150

$200

$250

$300

2014 General FundExpenditures Per Capita

Outstanding Debt* Total Revenues* Tax Revenues* Capital Outlay*

Shakopee $353 $826 $424 $185

Savage 1,850 968 559 373

Eden Prairie 807 956 573 335

Chaska 1,281 1,016 432 297

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2014 Per Capita InformationGovernmental Funds

* Data obtained from 2014 Comprehensive Annual Financial Report (CAFR) for all Cities

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 21/22

19

City of Shakopee Emerging Issues

Executive Summary

The following is an executive summary of financial and business related updates to assist you in staying

current on emerging issues in accounting and finance. This summary will give you a preview of the newstandards that have been recently issued and what is on the horizon for the near future. The most recentand significant updates include:

Accounting Standard Update – Accounting and Financial Reporting for Postemployment

Benefits Other Than Pensions – Governmental Accounting Standards Board (GASB) has issuedGASB statement 75 relating to accounting and financial reporting for postemployment benefits otherthan pensions. The new statement requires governments in all types of OPEB plans to present moreextensive note disclosures and required supplementary information (RSI) about their OPEBliabilities.

The following are extensive summaries of each of the current updates. As your continued business partner, we are committed to keeping you informed of new and emerging issues. We are happy todiscuss these issues with you further and their applicability to your City.

ACCOUNTING STANDARD UPDATE – GASB STATEMENT NO. 75 - ACCOUNTING AND

FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS

The primary objective of this statement is to improve accounting and financial reporting by state andlocal governments for postemployment benefits other than pensions (other postemployment benefits orOPEB). It also improves information provided by state and local governmental employers aboutfinancial support for OPEB that is provided by other entities. This statement results from a

comprehensive review of the effectiveness of existing standards of accounting and financial reportingfor all postemployment benefits (pensions and OPEB) with regard to providing decision-usefulinformation, supporting assessments of accountability and interperiod equity, and creating additionaltransparency.

This statement replaces the requirements of Statements No. 45, Accounting and Financial Reporting by

Employers for Postemployment Benefits Other Than Pensions, as amended, and No. 57, OPEB

Measurements by Agent Employers and Agent Multiple-Employer Plans, for OPEB. Statement No.74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, establishes newaccounting and financial reporting requirements for OPEB plans.

GASB Statement 75 requires governments to report a liability on the face of the financial statements forthe OPEB that they provide:

Governments that are responsible only for OPEB liabilities related to their own employees andthat provide OPEB through a defined benefit OPEB plan administered through a trust that meetsspecified criteria will report a net OPEB liability — the difference between the total OPEBliability and assets accumulated in the trust and restricted to making benefit payments.

8/15/2019 2015 Shakopee Communication Letter

http://slidepdf.com/reader/full/2015-shakopee-communication-letter 22/22

City of Shakopee

Emerging Issues

ACCOUNTING STANDARD UPDATE – GASB STATEMENT NO. 75 - ACCOUNTING AND

FINANCIAL REPORTING FOR POSTEMPLOYMENT BENEFITS OTHER THAN PENSIONS

(CONTINUED)

Governments that participate in a cost-sharing OPEB plan that is administered through a trustthat meets the specified criteria will report a liability equal to their proportionate share of the

collective OPEB liability for all entities participating in the cost-sharing plan.

Governments that do not provide OPEB through a trust that meets specified criteria will reportthe total OPEB liability related to their employees.

GASB Statement 75 carries forward from Statement 45 the option to use a specified alternativemeasurement method in place of an actuarial valuation for purposes of determining the total OPEB

liability for benefits provided through OPEB plans in which there are fewer than 100 plan members(active and inactive). This option was retained in order to reduce costs for smaller governments.

GASB Statement 75 requires governments in all types of OPEB plans to present more extensive notedisclosures and required supplementary information (RSI) about their OPEB liabilities. Among the newnote disclosures is a description of the effect on the reported OPEB liability of using a discount rate anda healthcare cost trend rate that are one percentage point higher and one percentage point lower thanassumed by the government. The new RSI includes a schedule showing the causes of increases anddecreases in the OPEB liability and a schedule comparing a government's actual OPEB contributions toits contribution requirements.

Information provided above was obtained from www.gasb.org.