2015 - sharedata

TRANSCRIPT

2015AUDITED RESULTS

Brait SE (Registered in Malta as a European Company)(Registration No. SE1)Share code: BAT ISIN: LU0011857645Share code: BATPISIN: MT0000680208(“Brait”, the “Company” or “Group”)

FOR THE YEAR ENDED31 MARCH 2015

Audited results for the year ended 31 March 2015

DisclaimerThis booklet may contain certain forward-looking statements with respect to the financial condition and results of operations of the Group, which by their nature, involve risk and uncertainty as they relate to events and depend on circumstances that may occur in the future.

Item Page reference

Section 1: Brait results presentation FYE 31 March 2015 3• Agenda 4• Highlights FYE 31 March 2015 5• BraitNAVanalysis As at 31 March 2015 8• Brait’sauditedresults FYE 31 March 2015 13• Pepkor Investment returns 17• Premier Results: 9 months ended 31 March 2015 18• Brait’snewacquisitions: – VirginActive Introductory presentation 36 – NewLook Introductory presentation 55 – Attractions to Brait 78• IcelandFoods Results: FYE 31 March 2015 79• Conclusion 113

Section 2: Appendices 114• Braitoverview 115• Summarisedfinancialinformation: – Premier 120 – Iceland Foods 123 – Other investments 127

Section 3: Brait audited results announcement FYE 31 March 2015 134

4 Audited results for the year ended 31 March 2015

Results presentation FYE 31 March 2015

4

Agenda

Welcome

Brait Audited results: FYE 31 March 2015

Pepkor Investment returns

Premier Results: 9 months ended 31 March 2015

Virgin Active Introductory presentation

New Look Introductory presentation

Iceland Foods Results: FYE 31 March 2015

Conclusion

5 Audited results for the year ended 31 March 2015

Highlights FYE 31 March 2015

5

NAV per share

R77.12

Increase on FY2014’s R31.95 NAV per share • 141.4%

Uplift primarily due to the realisation of Pepkor • 7.0x cost multiple• 69.5% IRR

3 year CAGR (benchmark of 15%)• 55.3% on reported NAV per share• 55.8% including bonus shares issued / cash dividend paid

Dividends

Proposed ordinary share bonus issue (with cash dividend alternative) • 77.12 cents per share (141.4% increase on FY2014)

Preference share dividend declared (for the six months ended 31 March 2015) • 479.68 cents per share (R95.9m in total)

Investment portfolio flows

Pepkor realised on 30 March 2015• R30.010bn total consideration received:

− R15.086bn cash− R14.924bn value for 200m Steinhoff shares (1)

Rest of portfolio • R746m received • R841m invested

(1) Valued at the 30 March 2015 closing Steinhoff share price of R74.62

6 Audited results for the year ended 31 March 2015

Highlights FYE 31 March 2015

6

Virgin Active

• Brait announced on 16 April 2015 the acquisition of a c.80% interest in Virgin Active, a leading international health club operator, for c.£682m (1)

• Brait will partner alongside an experienced management team, the founder and the Virgin Group

New Look

• Brait announced on 15 May 2015 the acquisition of a c.90% interest in New Look, a leading fast fashion multichannel retailer operating in the value segment, for c.£780m (expected completion date of 25 June 2015)

• Brait will partner alongside an experienced management team and the founder

• New Look raised £1.2 billion in Bonds (12 June 2015) • Proceeds raised will refinance existing debt resulting in average cost (pre-FX hedging) reducing from 9.42% to 6.25%

Brait’s inclusionin indices

• MSCI Emerging Markets Index on 28 August 2014

• FTSE / JSE Africa Series Top 40 Index on 22 June 2015

(1) Virgin Active acquisition remains subject to approval by the South African and Namibian competition authorities

7 Audited results for the year ended 31 March 2015

Highlights FYE 31 March 2015

7

Performance against targets

Performance metric Position at 31 March 2015

1 NAV CAGR > 15% per year over any 3 year period a • 55.3% CAGR since 31 March 2012 ‒ 55.8% CAGR including bonus shares issued / dividends paid

2 Dividend: 1% - 2.5% of closing NAV ‒ (bonus shares or cash election) a • FY15: 1% of R77.12 NAV proposed (141% up on FY14)

‒ FY14: 1% of R31.95 (92% of shareholders elected bonus shares)

3 Operating costs: < 0.85% of Brait AUM a• 0.44% of Brait AUM (1)

• 0.27% net after fee income (1)

4 Minimal cash drag: < 25% of NAV X• 34.7% of NAV (33.0% of total assets)

‒ Ratio distorted by Pepkor cash consideration received 30 March 2015 ‒ Normalises post Virgin Active and New Look acquisitions

5 Primarily unlisted investments X• Target remains a primarily unlisted investment portfolio

‒ Steinhoff shareholding received as consideration for the Pepkor realisation‒ Brait will seek opportunities to reduce holding in an orderly manner

6 Demonstrate cash flow within underlying investments a • Strong EBITDA cash flow conversion across portfolio

(1) AUM represents the aggregate of the Group’s total assets and Brait IV invested capital under management. Percentages quoted based on closing FY15 AUM. Using average AUM as the reference basis, operating costs are 0.60% and net after fee income 0.36%

8 Audited results for the year ended 31 March 2015

Brait NAV Analysis

8(1) Restated as a result of adoption of IFRS 10 Consolidated Financial Statements. No impact on reported NAV per share; reclassifications not material

Restated (1)

AuditedRestated (1)

Audited Audited

Amounts in R'm 31 March 2013 31 March 2014 31 March 2015

Investments 13,151 87% 17,229 93% 27,144 66%Pepkor 9,278 61% 11,145 60% - -Steinhoff - - - - 15,206 37%Premier 1,463 10% 3,053 17% 8,241 20%Iceland Foods 1,449 10% 1,513 8% 1,259 3%Other investments 961 6% 1,518 8% 2,438 6%

Loan receivable 1,399 9% 523 3% 574 1%Cash and equivalents 493 3% 320 2% 13,689 33%Property and equipment 10 - 8 - - -Accounts receivable 88 1% 342 2% 12 -

Total assets 15,141 100% 18,422 100% 41,419 100%

Borrowings (141) (164) -Accounts payable and other liabilities (73) (47) (86)

Total liabilities (214) (211) (86)

Preference share equity (1,469) (1,964) (1,964)

NAV: ordinary shareholders 13,458 16,247 39,369

Number of issued ordinary shares ('m) excluding treasury 505.2 508.5 510.5

NAV per share R26.64 R31.95 R77.12

9 Audited results for the year ended 31 March 2015

Brait NAV Analysis

9

Rolling CAGR: reported NAV

Commencing 1 April 2011, Brait’s performance benchmark for NAV growth is to exceed 15% CAGR over any three year period

1-Apr-11 FY 2012 FY 2013 FY 2014 FY 2015

Reported NAV per ordinary share R16.50 R20.59 R26.64 R31.95 R77.12

Rolling 3-year CAGR (1) - 24.8% 27.1% 24.6% 55.3%

Adjustment: ordinary share dividend (2) - - R0.2059 R0.4723 R0.7918

• 1% of March 2012 NAV of R20.59 - - R0.2059 R0.2059 R0.2059

• 1% of March 2013 NAV of R26.64 - - - R0.2664 R0.2664

• 1% of March 2014 NAV of R31.95 - - - - R0.3195

Adjusted NAV per ordinary share R16.50 R20.59 R26.85 R32.42 R77.91

Rolling 3-year CAGR (including dividends) (1) - 24.8% 27.6% 25.2% 55.8%

(1) Period for which quoted CAGR calculated 1-Apr-11 to 31-Mar-12 1-Apr-11 to 31-Mar-13 1-Apr-11 to 31-Mar-14 1-Apr-12 to 31-Mar-15

(2) Percentage of ordinary shareholders that elected the receipt of bonus shares for respective year’s dividend Not applicable 85% 91% 92%

Note: The four year CAGR (1-Apr-11 to 31-Mar-15) for Reported NAV per share is 47.0%; including dividends is 47.4%

10 Audited results for the year ended 31 March 2015

Brait NAV analysis

10

Reported assets and % weighting

(1) Reported NAV per share(2) The Other investments category in the above chart includes accounts receivable

50%57%

61%60%

37%

11%10%

10%

17%

20%

8%

10%

8%

3%

14%

9%

7%

10%

6%

12%

12%

9%

3%

1%

13%

4%

3%

2%

33%

R9,789R11,794

R15,141

R18,422

R41,419

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Rights-offer Mar-12 Mar-13 Mar-14 Mar-15

R'm

Pepkor Steinhoff Premier Iceland Foods Other investments Loan receivable Cash and equivalents(2)

(1) R16.50 R20.59 R26.64 R31.95 R77.12(1) (1) (1) (1)

11 Audited results for the year ended 31 March 2015

Brait NAV analysis

11

Pro forma assets and % weighting

Pro forma assumptions applied

AuditedMar-15

R’m

Pro forma adjustments

R’m

Pro forma carrying

valueR’m

% of Total

Assets

Steinhoff 15,206 (15,206) 1 - -

Premier 8,241 - 8,241 20%

Virgin Active - 12,549 2 12,549 30%

New Look - 14,352 3 14,352 35%

Iceland Foods 1,259 - 1,259 3%

Other investments 2,450 - 2,450 6%

Loan receivable 574 - 574 1%

Cash 13,689 (11,695) 4 1,994 5%

Total assets 41,419 - 41,419 100%

Notes:

1 On the basis that Steinhoff is not a long term holding for Brait, pro forma assumption is to reflect this holding as realised

2 Pro forma carrying value for Virgin Active based on estimated cost of £682m (16-Apr-2015 announcement) translated using assumed £/R exchange rate of R18.40

3 Pro forma carrying value for New Look based on estimated cost of £780m (15-May-2015 announcement) translated using assumed £/R exchange rate of R18.40

4 Pro forma decrease in carrying value for cash is based on assumption of maintaining Total Assets at the 31-Mar-2015 reported total R41,419m for comparability

37%

20%

20%

3%

3%

6%

6%

1%

1%

33%

5%

30%

35%

R41,419 R41,419

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Audited Mar-15 Pro forma

Steinhoff Premier Iceland FoodsOther Investments Loan receivable Cash and equivalentsVirgin Active New Look

R’m

12 Audited results for the year ended 31 March 2015

Brait NAV analysis

12

EV/EBITDA multiples to 31 March 2015

Peer group for Premier

Tiger Brands

Pioneer Foods

Peer group for Iceland Foods

Tesco

Sainsbury

WM Morrison

Booker

Poundland (included from Jun-14)

Legend Brait valuation multiple discount

Brait valuation multiple Premier Iceland Foods

Trailing 3 year peer average multiple - 21%

Peer average multiple at reporting date 16% 30%

6.5 x 6.5 x 6.5 x 7.5 x12.3 x9.5 x 10.3 x 11.0 x 11.5 x

12.3 x10.9 x12.8 x 12.4 x

13.4 x 14.6 x

3.0 x

6.0 x

9.0 x

12.0 x

15.0 x

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15

MultiplePremier

6.5 x 6.5 x 6.5 x 6.5 x 7.5 x8.4 x 8.8 x 9.1 x 9.2 x 9.5 x

9.8 x10.5 x 10.6 x

9.3 x10.7 x

3.0 x

6.0 x

9.0 x

12.0 x

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15

Multiple Iceland Foods

13 Audited results for the year ended 31 March 2015

Brait’s audited results: FYE 31 March 2015

13

Summarised statement of comprehensive incomeRestated

March 2015 March 2014

R’m R’m

Investment gains (1) 22,979 2,683Interest 261 225Dividend income 147 83Fees 80 93Foreign exchange gains 123 48

Income 23,590 3,132

Operating expenses (201) (143)

Profit from operations 23,389 2,989

Finance costs and taxation (55) (44)

Profit for the year 23,334 2,945

Translation adjustments (1) 9 16

Comprehensive income for the year 23,343 2,961

(1) The March-14 reported values have been restated as a result of the adoption of IFRS 10: Consolidated Financial Statements. The primary effect of the restatement is to reclassify the Translation Adjustment on the GBP investment in Iceland Foods to Investment Gains. This results in a corresponding restatement to Profit for the year, with no impact to the reported Comprehensive Income for the year

14 Audited results for the year ended 31 March 2015

Brait’s audited results: FYE 31 March 2015

Operating expenses to AUM: Performance metric <0.85%

14

March 2015 March 2014

R’m R’m

Total assets 41,419 18,423

Brait IV invested capital under management 3,867 3,471

Total closing AUM 45,286 21,894

Operating costs 201 144

Fee income (80) (72)

Operating costs after fee income 121 72

Ratios based on closing AUM:

- Operating costs to AUM 0.44% 0.66%

- Operating costs after fee income to AUM 0.27% 0.33%

Note: Using average AUM as the reference basis, FY2015 operating costs are 0.60% and net after fee income 0.36%

15 Audited results for the year ended 31 March 2015

Brait’s audited results: FYE 31 March 2015

15

Investment proceeds 14,671Pepkor realisation: Cash proceeds received 15,086

Less: settlement of SPV gearing (1,161)Portfolio inflows 746

Share of Pepkor’s June 2014 dividend received (1) 228Premier 424

Repayment of short term loan receivable 330Interest received 94

Other investments 94Realisation proceeds 64Fees received 30

Other fees received 54Interest received - bank 19Operating expenses paid (214)Interest and taxation paid (56)Operating cash flow (excluding purchase of investments) 14,474Purchase of investments (841)

Premier (shareholder loan funding for acquisitions and exercise of put and call options) (596)Southern View Finance (“SVF” capital raise by way of specific share issue during November 2014) (234)Other investments (11)

Net cash flow from operating activities 13,633Net repayment of long term borrowings (164)Net purchase of treasury shares (22)Ordinary dividend paid (cash election) (14)Preference dividend paid (185)

Net increase in cash and cash equivalents 13,248

(1) Dividend income in the statement of comprehensive income reflects the R147m relating to Brait’s direct shareholding in Pepkor. Brait’s indirect share of R81m was received by way of capital distribution from the Pepkor SPV and is thus recognised under investment gains

Summarised cash flows (R’m)

16 Audited results for the year ended 31 March 2015

Brait’s audited results: FYE 31 March 2015

16

(1) RestatedMarch

2015R’m

March 2014R’m

Net increase / (decrease) in cash and cash equivalents 13,248 (219)Effects of exchange rate changes on cash and cash equivalents 121 46Cash and cash equivalents at beginning of year 320 493

Cash and cash equivalents at end of year 13,689 320

Comprising:

ZAR cash 3,034 161USD cash 178 159GBP cash (2) 10,477 -

Cash and cash equivalents 13,689 320

Available from undrawn gearing facilities (3) 16,500 2,311

Total cash and available facilities 30,189 2,631

(1) Comparatives restated as a result of adoption of IFRS 10. The effect is to reclassify cash held by subsidiaries designated as ‘Investment Entities at fair value through profit and loss’ to the investments line of the statement of financial position

(2) GBP cash holding at 31 March 2015 is placed with five banks, each having an investment grade credit rating

(3) Gearing facilities increased post year-end to facilitate the funding of New Look and Virgin Active acquisitions

Analysis of cash position

17 Audited results for the year ended 31 March 2015

Steinhoff offer25-Nov-2014

Per the 25 November 2015 detailed terms announcement, Steinhoff International Holdings (“Steinhoff”) offered a total consideration of R26.4 billion for Brait’s effective 37.06% interest in Pepkor, to be settled through a combination of:

• Cash amount of R15 billion • 200 million Steinhoff ordinary shares issued at a price of R57 per share (such price guaranteed by Steinhoff for 12 months to 30 March 2016)

Shareholder vote

The ordinary resolutions necessary to authorise the transaction were passed by a 99.8% majority of Brait’s shareholders present and voting at the Extraordinary General Meeting held on 27 January 2015

Effective date30-Mar-2015

All conditions precedent to the disposal of Brait’s effective 37.06% interest in Pepkor to Steinhoff were fulfilled by 30 March 2015Brait received a total consideration from Steinhoff of R30.010 billion, comprising:• Cash of R15.086 billion (which included a purchase price escalation calculated from 1 March 2015)• Value of R14.924 billion for the 200 million Steinhoff ordinary shares received (closing Steinhoff share price on 30 March 2015 was R74.62)

Pepkor

17

Investment returns

Implied metrics Based on Steinhoff offer price R’m

Based on total consideration receivedR’m

Consideration to Brait 26,400 30,010

Brait’s effective interest in Pepkor 37.06% 37.06%

Implied Equity Value for Pepkor 71,242 80,985

Pepkor net debt (1) 2,140 2,140

Implied Enterprise Value for Pepkor 73,382 83,125

Pepkor EBITDA (1) 3,994 3,994

Implied EV/EBITDA multiple (2) 18.4x 20.8x

Implied PE multiple (3) 37.4x 42.5x

(1) Per Pepkor audited Jun-14 financial statements(2) Calculated as Implied Enterprise Value for Pepkor; divided by Pepkor’s FY14 EBITDA from Continuing Operations of R3.994 billion(3) Calculated as Implied Equity Value for Pepkor; divided by Pepkor’s FY14 Net Profit from Continuing Operations of R1.906 billion

19 Audited results for the year ended 31 March 2015

Premier

19

Business overview

• A leading staple foods producer with the strategic intent to be a FMCG manufacturer offering branded and

private label FMCG solutions

• Strong heritage brands dating back to 1852

− Snowflake (wheat flour), Iwisa No 1 (maize meal), Blue Ribbon (bread)

− Lil-lets (feminine hygiene), Manhattan and Super C (sugar confectionery)

• Operates through a wide footprint

− 15 bakeries, 8 wheat mills, 4 maize mills, a sugar confectionery plant, a feminine hygiene manufacturing plant, a

biscuit plant, a pasta plant and an animal feeds plant

− 29 distribution depots in South Africa, Swaziland, Lesotho and Mozambique, with a Lil-lets sales office in the UK

• On a large scale

− Sells c.550 million loaves of bread and 1 million tons of maize and wheat per year

− Makes over 45,000 deliveries daily with a fleet of c.930 bakery trucks and

− Employs 8,650 people

• Serves all channels to the market with significant exposure to the informal market which accounts for 70% of

bread sales volumes

20 Audited results for the year ended 31 March 2015

Premier

20

Regional footprint

29 Distribution Depots in SA, Swaziland, Lesotho & Mozambique

8 Wheat Mills in SA, Swaziland & Mozambique

15 Bakeries in SA & Swaziland1 Biscuit Plant in Mozambique

4 Maize Mills in SA, Swaziland & Mozambique1 Pasta Mill in Mozambique

1 Sugar Confectionery Plant in SA

1 Home & Personal Care manufacturing plant (1)

(1) Lil-lets has offices in both SA and Birmingham, UK

1 Animal Feed Plant in Mozambique

21 Audited results for the year ended 31 March 2015

Premier

21

(R’m)(1) YTD FY15 Growth

(1) YTD FY14

FY2014 Commentary

Net revenue 6,720 31% 5,141 7,750• Revenue growth of 31%; LFL growth of 21% (excluding acquisitions)• Volumes increase on prior period: 27% for bread (9% LFL (excluding Star Bakeries));

4% for maize; 3% for wheat; 39% for sugar confectionery; 12% for Lil-lets

EBITDA (2)

% Margin6149.1% 70% 362

7.0%5737.4%

• EBITDA margin expansion continues due to:‒ repositioning bread quality and brand has enabled Premier to lift prices‒ focus on manufacturing and distribution efficiency‒ introduction of higher margin FMCG products

• Reinvested profits in brands and people to build business: ‒ marketing expenditure up 67% on the prior period‒ in-sourcing labour at all sites

EBIT (2)

% Margin4196.2% 51% 277

5.4%4385.7%

(1) Results for 9 months YTD FY15 exclude CIM (acquired in March 2015); 9 months YTD FY14 exclude Lil-lets and Star Bakeries (2) Before non-recurring costs (YTD FY15: R7m; YTD FY14: R13m; FY14: R53m)

YTD 9 months ended 31 March 2015

(R’m) YTD FY15 Growth YTD

FY14FY

2014 Commentary

Cash from operations% EBITDA

33555% 33% 251

69%52491%

• Rising commodity prices in YTD FY15 led to a higher working capital absorption of R241m (YTD FY14: R148m)

Capex (425) 51% (281) (408)

• Focus continues on funding capex programme from operational cash flows• c.60% is expansionary capex. Major projects invested in during YTD FY15 include:

‒ a new bakery line in Durban (commissioned in Nov-14); ‒ a new bakery line in Cape Town (commissioned in Feb 15); and ‒ work on a new wheat mill in Durban (to be commissioned in H1 of FY16)

• Significant investment into vehicle fleet to improve efficiencies

Operating cash flow post capex% EBITDA

(90)(15%)

(200%) (30)(8%)

11620%

• Function of above

22 Audited results for the year ended 31 March 2015

Premier

22

Trading performance since implementation of five year strategic plan

4,896

5,731

6,272

7,750

8,531

222

289

422

573

775

4.5%

5.0%

6.7%

7.4%

4%

5%

6%

7%

8%

9%

10%

4,000

5,000

6,000

7,000

8,000

9,000

2011 2012 2013 2014 2015 LTM

Rm

Revenue(LHS) EBITDA(LHS) EBITDA margin(RHS)

9.1%

For the three years to 30 June 2014, Premier has:• Grown revenue by 58% at a CAGR of 17%

• Grown EBITDA by 158% at a CAGR of 37%

• Expanded its EBITDA margin from 4.5% in FY11 to 7.4% in FY14

• Tracking 9.1% based on the Last Twelve Months (LTM) to March 2015

This strong trading performance is attributable to the 3 pillars of Premier’s growth strategy:• Optimising milling and baking operations by investing in people, brands and assets

• Converting from a staple foods producer to an FMCG branded business

• Geographic expansion

23 Audited results for the year ended 31 March 2015

Premier

23

Acquisitions to date (1)

Company Date acquired Business description

1. Acquired assets of SwazilandUnited Bakeries andMister Bread in Swaziland

Feb 2012 Acquired a controlling stake in in the two leading bakeries in Swaziland and created Premier Swazi Bakeries. Bought out minorities during March 2015

2. Manhattan and Super C May 2013 Entry into sugar confectionery sub-categories of gums & jellies, marshmallows and compressed tablets

3. Star Bakeries Nov 2013Bakeries in Eastern Cape giving Premier a national SA bread footprint; ‘Mister Bread’ and ‘Star’ brands

4. Lil-lets Nov 2013 Leading brand in feminine hygiene with operations in the UK and SA

5. Ngwane Mills April 2014Largest wheat and maize miller in Swaziland to complement Premier Swazi Bakeries’ operations

6. Mister Bread Milling March 2015An Eastern Cape flour mill currently supplying c.50% of the Eastern Cape bakeries’ flour requirements

7. La Femme March 2015Durban based business manufacturing tampons for Lil-lets SA. Provides entry into in-sourcing all tampon production in SA and the UK

8. Companhia Industrial daMatola S.A. (CIM) March 2015

Acquired a controlling stake in the leading food producer in Mozambique with a diversified product range; maize, wheat, pasta, biscuit and animal feeds

(1) Premier has invested R2.2bn to date in these acquisitions at an average EV / EBITDA multiple of 7x

24 Audited results for the year ended 31 March 2015

Flagship national brands

Other national brands

Regional brands

Premier

24

South African milling and baking brands

25 Audited results for the year ended 31 March 2015

Acquired maize and

wheat milling operations in

Swaziland

New TV and social media

campaign launched for Blue

Ribbon

Commissioned 3rd

bakery line at Durban bakery (R120m project which increasedcapacity by 50%)

All mills and 3 of Premier’s

bakeries obtain

FSSC 2200 accreditation (a first in SA)

Premier commences

refinance and restructure of bakery fleet;in-sources

milling distribution

Premier

25

Pillar 1 – Optimising milling and baking operations by investing in people, brands and assetsFocus has been on:

‒ Changing bread positioning (packaging, range, recipe) from a “price fighter” brand to a strong “challenger” brand

‒ Developing people to build a winning team and bolster the company leadership

‒ Upgrading assets to use latest technology to have “best of breed” equipment in bakeries

Acquired twobakeries in

Swaziland and formed Premier Swazi Bakeries

Recruited new

executive to head

bakeries

Re-launched “Blue Ribbon”

brand and added a range of “value add”

loaves

July2011

Feb2012

Nov2012

Sept2013

Nov 2013

Dec2013

April2014

Aug2014

Aug2014

Nov2014

Feb2015

Feb2015

Mar2015

Acquired Star Bakeries in the Eastern

Cape

Launched new recipe

and pan-size for Blue

Ribbon and BB bread

Commissioned 3rd

line at Cape Town bakery

(R250m project which increased capacity by 36%)

Acquired Mr Bread Milling, a wheat mill in

the Eastern Cape

Re-launched “Iwisa” maize

brand

26 Audited results for the year ended 31 March 2015

Premier

26

Pillar 1 – Optimising milling and baking operations by investing in people, brands and assetsCategory Premier brand Trading update: 9 months ended 31 March 2015

Bread

• Blue Ribbon

• BB Bread

• Star Bread

• Mister Bread

• SUB Bread

• Bread sales volumes up 27%; 9% LFL (excluding Star Bakeries which was acquired in November 2013)

• Despite aggressive competition in the formal channel, Premier has retained its formal market share to March 2015 and

grown LFL informal sales volumes by 11%

• Improved depth of distribution in retail channel (e.g. strike rate for Spar increased from c.50% to c.70%)

• Grew volumes in KZN by 16% despite a fire in the Durban bakery in February 2015 which has been mitigated by the

acquisition of an independent bakery in Durban (Masterbake)

Maize

• Iwisa

• Invicta

• Nyala

• Super Sun

• Maize sales volumes up 4% (including Ngwane Mills acquisition in April 2014)

• Maize value market share in the formal sector in line with the prior year

• Improved margin management by linking selling prices to commodity prices

Wheat• Snowflake

• Blue Ribbon

• Wheat sales volumes up 3% (including Ngwane Mills acquisition in April 2014)

• Consumer flour sales only account for 33% of Premier’s total flour sales. Focus on margin management means that

Snowflake trades at a significant value / volume premium

• Snowflake won 2015 Product of the Year Innovation Awards for its Corn flour and Treats range

• Continued range extension in baking category (e.g. cake mixes, baking powder, corn flour) has reinforced Snowflake’s

leading position in the category

27 Audited results for the year ended 31 March 2015

Premier

27

Pillar 1 – InnovationsRe-launched Iwisa maize brand (Jul-11) Re-launched Blue Ribbon bread and added a range of “value-add” loaves (Sep-13)

New TV and social media campaign launched for Blue Ribbon (Feb-15)Re-launch of BB bread in Kwa Zulu Natal (Nov 2014)

28 Audited results for the year ended 31 March 2015

Acquired the assets and

operations of La Femme from Libstar Operations (Pty) Ltd, a

tampon manufacturer that supplies

Lil-lets SA tampons

Premier

28

Pillar 2 – Conversion from a staple food producer to an FMCG branded businessFocus has been on:

‒ Establishing a new business unit to house the non-staple foods FMCG products

‒ Acquiring businesses operating in other FMCG categories

‒ Organic expansion through innovation

Acquired Lil-lets, a feminine

hygiene business in the UK and SA

Recruited new

executive to head

Groceries

July2011

April 2013

May 2013

Nov2013

Nov 2013

Aug2014

Sept 2014

Mar2015

Mar2015

Acquired sugar

confectionery operations and brands (Manhattan, Super C and Romantics)

Re-launched Super C and extended the

range

Launched new

“Bubbles” range under Manhattan

Extended Snowflake

by launching dessert

range and baking aids

Launched Lil-lets

Feminine Hygiene Solutions

range

29 Audited results for the year ended 31 March 2015

Premier

29

Pillar 2 – Conversion from a staple food producer to an FMCG branded businessCategory Premier brand Trading update: 9 months ended 31 March 2015

Sugar

confectionery

• Manhattan

• Super C

• Grown volumes (39%) and market share by filling sales gaps in formal and informal sectors

• Focus on innovation:

− Sales from innovation (products launched in last 12 months) accounted for 22% of March 2015 sales

− New Manhattan Bubbles range has led to 2% market share gain in the formal sector

• Since acquisition in May 2013, market share has doubled to c.9%

Home &

Personal Care

(“HPC”)

• Lil-lets

• Dove (1)

• Vulco (2)

• South Africa:

− Stable market share (c.24% of formal Femcare sales by value)

− Won SA 2015 Product of the Year awards for sanitary pad range and feminine hygiene wipes

• United Kingdom:

− While the overall tampon market declined 5.5%, Lil-lets UK tampon sales down 0.7%

− Focus on Lil-lets’ teen range to recruit new customers in the UK

− Started selling products through distributors into China and the Middle East

(1) Licenced from Unilever Plc for cotton wool products in South Africa(2) Vulco is the No. 1 household glove brand in SA

30 Audited results for the year ended 31 March 2015

Premier

30

Pillar 2 – Innovations

Launched Lil-lets Feminine Hygiene Solutions range (Sept-14)

Launch of new Bubbles range under Manhattan (Aug-14)

Re-launched Super C and extended the range (Mar-15)

Extended Snowflake by launching dessert range and baking aids (Nov-13)

31 Audited results for the year ended 31 March 2015

Premier

31

Focus has been on:

‒ Expansion by acquisitions:

• Premier acquired two bakeries in Swaziland in February 2012 to create Premier Swazi

Bakeries and then integrated these with a milling operation (acquired in April 2014) to

form the leading milling and baking business in that country

• In March 2015, acquired controlling interest in CIM, the leading food manufacturer in

Mozambique

‒ Driving export sales of products from SA into other African countries:

• Export sales (1) YTD FY15 are R73.8m (135% up on prior period)

‒ In the current year Lil-lets (UK) has started selling products through distributors into China and

the Middle East

Pillar 3 – Geographic expansion

(1) Comprise direct export sales, sales through agents and sales to SA retailers for sale outside SA

32 Audited results for the year ended 31 March 2015

Premier

32

Pillar 3 – Geographic expansion

Acquired 68% of the shares in issue in CIM during March 2015

• CIM is a leading food manufacturer in Mozambique in operation since the mid-1940’s

• Revenue of R1.2bn and EBITDA of R115m

• Diversified product range of maize, wheat, pasta, biscuits and animal feed products

• Brands include:

‒ Maize: the leading maize brand in Mozambique “Top Score”, as well as “Celeste” and

“Matabicho”

‒ Wheat: “Florbela” cake flour and “Favorita” bread flour sold mainly to bakeries

‒ Biscuits: CIM is the market leading biscuit brand

‒ Pasta: The number 2 pasta brand “Polana”

• Facilities in Matola near Maputo comprise a wheat and maize mill, as well as a biscuit, pasta

and animal feeds plant

• Operates 5 depots across Mozambique

• Employs c.650 people

• Potential for synergies with Premier on procurement and CIM to benefit from Premier’s

milling technical assistance

• New sales and marketing plan to accelerate growth of brands in the country

• In the process of acquiring the balance of CIM’s shares in issue

Maputo City

Beira

Tete

Quelimane

Nampula

Chimoio

33 Audited results for the year ended 31 March 2015

Premier

33

Outlook

Milling and baking:

• Comfortable with steps taken to secure maize supply given outlook of rising

commodity prices and risk of maize shortages in 2015/16

• Commission new Durban wheat mill in November 2015

• Restore the Durban bakery damaged by the fire and continue with the bakery

upgrade programme

• Blue Ribbon bread is well positioned in terms of quality and brand to compete in the

market on a national basis

FMCG:

• Stretch existing brands by launching new products in related categories

• Acquisitions made to date have been integrated into Premier and the focus on

achieving the targeted investment returns and maximising synergies and revenue

opportunities

• Evaluating FMCG acquisition opportunities

Geographic expansion:

• At an advanced stage of negotiating an acquisition in East Africa

34 Audited results for the year ended 31 March 2015

Premier

34

Brait’s audited valuation31-Mar-15 31-Mar-14

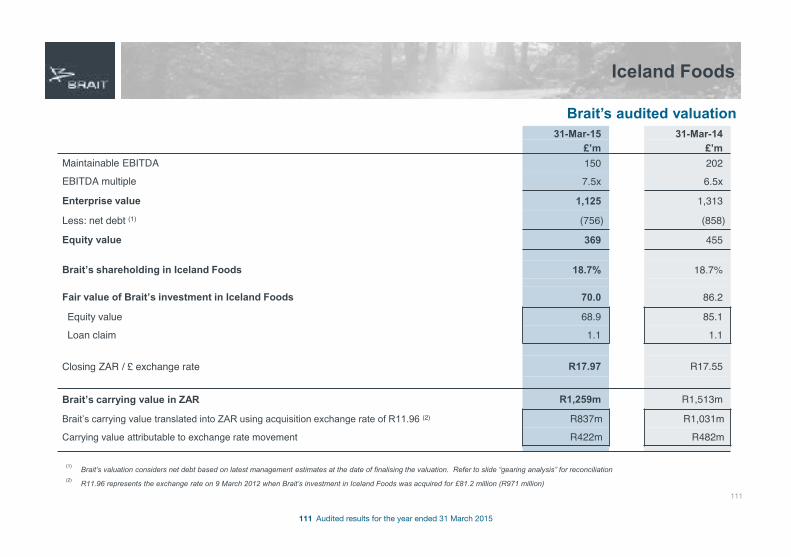

R'm R'mMaintainable EBITDA 829 497

EBITDA multiple (1) 12.3 x 6.5 x

Enterprise value 10,197 3,227

Less: net debt considered in valuation (3,187) (1,226)

Net debt (including shareholder loans) (3,738) (2,793)Adjustment for acquisitions and capex (2) 551 1,567

Equity value 7,010 2,001

Brait’s shareholding in Premier (3) 86.5% 84.6%

Fair value of Brait’s investment in Premier 8,241 3,053Equity value 6,061 1,692Shareholder loans (4) 1,989 1,334Financial derivative asset (5) 191 27

Notes(1) FY15 valuation multiple used of 12.3x represents the peer trailing three year average EV/EBITDA multiple. This 12.3x multiple is at a 16% discount to the 31 March 2015 peer average EV/EBITDA

multiple of 14.6x(2) Adjustment is made to normalise net debt for the cost of those acquisitions and capex that are not yet generating EBITDA. For the current year, this comprises (i) capex on the new Cape Town bakery

line (commissioned in February 2015); (ii) capex spend to date on the new wheat mill in Durban (to be commissioned in H1 FY16) and (iii) the cost of acquiring CIM in March 2015. The March 2014 adjustment was to recognise the November 2013 acquisitions of Lil-lets and Star Bakeries at their cost; as well as capex spend to date on the Cape Town bakery line

(3) Increase in Brait’s shareholding due to the exercise of options under agreements with former Premier shareholders(4) Increase in shareholder loans to fund the March 2015 acquisitions of La Femme, Mister Bread Milling and CIM. Note that Premier serviced R94m interest on Brait’s shareholder loans during FY15

(Premier has repaid Brait a total of R166m interest since July 2012) (5) Fair value of remaining options held with former Premier shareholders. Exercise of the remaining options over the next 2 years enables Brait to increase its shareholding to c.90%

35 Audited results for the year ended 31 March 2015

Premier

35

Attractions to Brait

Cash flow generative • Strong cash flow characteristics due to nature of the product basket that is focused on cash sales into the informal market

Market leader • Market leading staple food brands• Includes some of the oldest brands in the country

Clear strategy• Optimising core operations by investing in people, brands and assets• Investing in a number of internal projects with attractive returns• Target acquisitions in a wide range of adjacent and FMCG categories

• Distribution platform – opportunity for other product sets• Sizeable footprint and reach – not easy to build / replicate• Operating leverage – ability to expand margins and improve production efficiencies

Well positioned

• Well exposed to cash consumer in higher growth LSM 1 – 6 categories• CIM acquisition enhances exposure to neighbouring countries Cash consumer

Demonstrated throughAttractions

Management team • Deep bench with significant industry experience across all categories

Alignment • Shareholders are Brait and management • Management increased their stake in Premier in October 2014, acquiring a further c.3.5% shareholding

38 Audited results for the year ended 31 March 2015

Virgin Active

38

The world’s leading international health club operator

Overview

An outstanding business across South Africa and market-leading positions in Europe

Platform for further growth, particularly in Africa and Asia

Over 1.3m adult members worldwide

£639m revenue in 2014

267 clubs in nine countries across four continents

Exclusive rights to use the Virgin Active brand globally for 30 years

7

146

114 43%55%

2%

Geographic mix(1)

Asia Pacific <1%Clubs Members Revenue

Southern Africa Europe Asia Pacific

267 1.3m £639m

Notes 1. As of 31 December 2014

28%

69%

4%

39 Audited results for the year ended 31 March 2015

Virgin Active

39

Geographic diversity of operations and earnings

Current locations

Southern Africa

No. Clubs(1) 114

No. Adult Members(1) 722k

VA Market Position (SA)(4) No. 1

2014 Revenue(3) £176m

UK

No. Clubs(1) 101

No. Adult Members(1) 380k

VA Market Position(2) No. 1

2014 Revenue(3) £324m

Continental Europe(5)

No. Clubs(1) 45

No. Adult Members(1) 183k

VA Market Position No.1 in Italy

2014 Revenue(3) £114m

Asia Pacific

No. Clubs(1) 7

No. Adult Members(1) 25k

2014 Revenue(3) £25m

Notes:1. As at 31 December 2014; 2. Based on UK revenues, source: IHRSA; 3. Audited financial results; 4. Based on revenues of private health clubs; 5. Continental Europe presence includes Italy, Spain and Portugal

40 Audited results for the year ended 31 March 2015

Bernado De VicenteIberia

Virgin Active

40

Highly experienced management team

Mark BurrowsGroup

Chief Financial Officer

Ross Faragher-ThomasAfrica

Paul WoolfGroup

Chief Executive Officer

Matthew BucknallGroup

President & Founder

Matthew MerrickUK

Luca ValottaItaly

41 Audited results for the year ended 31 March 2015

Why the Virgin Brand People Brand

Brand Pioneer Opportunity Brand

Virgin Active

The VA story

41

42 Audited results for the year ended 31 March 2015

Virgin Active

42

Key investment highlights

A proven model that is repeatable, flexible and resilient3

4 An outstanding business in South Africa

Targeted exposure to positive macro health & wellness trends

1

2

Aspirational global consumer brand

A market-leading premium focused operator in Europe5

Multiple channels of growth, including an exciting growth platform in Asia Pacific6

Experienced management team 8

Excellent financial track record, strong returns and cash flow, and earnings visibility7

43 Audited results for the year ended 31 March 2015

Virgin Active

43

Targeted exposure to positive macro and health & wellness trends

6.87.7

9.3

1990 2000 20121,179

1,881

3,478

1990 2000 2012

3

10

1

14

72

69

27

3

2319

6

13

Africa Americas S.E. Asia Europe East. Med. West.Pacific

Global

1980 2008

Rise in life expectancyLife expectancy at birth globally(1)

4859

64 6973 76

1950-1955 1970-1975 1990-1995 2010-2015 2030-2035 2050-2055

13%25%

~3x increase

Growing healthcare costs OECD average US $ per capita spend(5)

Notes:1. United Nations 2010 2. Data shows age-standardised prevalence and obesity is defined as BMI>30kg.m2; 3. Approximated numbers based on World Health Organisation (2012); 4. International Diabetes Federation 2013; 5. OECD 2014 health statistics; 6. The Global Burden of Disease Update Geneva, WHO

Governments under increasing pressureOECD countries average healthcare cost % of GDP(5)

Increase in diabetes prevalenceNumber of people affected by diabetes (m)(4)

37 24 20 3556

72

138

50 39 4268 69

123

202

N America& Carrib.

S&CAmerica

Africa MENA Europe SE Asia W Pacific

2013 2035

c. 17%

c. 19%

c. 24%

2008 2015 2030

Cardiovascular Diseases

Projected mortality trend of cardiovascular diseasesDeaths by cause (%)(6)

Growing prevalence of obesityAdults aged 20+ by region (%)(2,3)

44 Audited results for the year ended 31 March 2015

Virgin Active

44

A proven model that is repeatable, flexible and resilient

Market selection criteria

Large and growing middle class

Strong or growing fitness culture

Opportunity to become leading scale premium focused operator in market

Site selection criteria

Strong member demand

• Detailed demographic analysis focusing on population density and socioeconomic factors such as incomes and family orientation

• Clearly identified catchments based on market relevant drive times in suburban locations and walk times in CBD locations

Strategic networks

• Focus on complementary networks in major cities

• Reciprocal rights highly valued by members

• Strong work and home club combinations

• Ability to offer a range of facilities and price points

Financial feasibility

• Affordable property deal• Attractive yield / rent relationship• Large formats can trade on volumes and

/ or price• Ability to leverage economies of scale in

major cities

Convenience, access & exposure

• Convenience and exposure critical to attract and retain members

• Sufficient secure car parking essential in suburban locations

• Enabling infrastructure such as arterial roads and transport hubs

Development pipeline available for expansion

Favourable competitive dynamics

Goal is to reach scale quickly in each market as scale provides a fantastic

consumer proposition and key defensive qualities

45 Audited results for the year ended 31 March 2015

841 967

1,113 1,284

1,412 1,599

1,811 2,107

2,436

2,783

3,125

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Virgin Active

45

An outstanding business in South Africa

Partnerships with wellness incentive schemes

Subsidised VA membership key customer acquisition tool

Gym subsidy drives both acquisitionand retention

Higher profits: maintains healthy lives

Benefits to Virgin Active Benefits to providers

A successful relationship with Discovery since 2001

Bias to higher LSMs

Schemes attract and retain stickier members with subsidies

Schemes market on VA’s behalf

Schemes incentivise regular usage

Estimated market share by revenue(3,4,5)

60%15%

5%

7%

13%

Revenue (1)Highlights

Notes:1. Revenue on a Current Club Portfolio basis; 2. FY2012- FY2014 average; 3. Market defined as commercial indoor gym market; 4. Leading international consultancy; 5. Virgin Active has 114 (or 24%) of a total of 482 comparable clubs in South Africa –leading international consultancy

Strong and sustained leadership position: 4x larger than nearest competitor

Unique national network of 114 well-invested, high-quality clubs

Market segmentation through use of flexible club formats

Best in class brand awareness and member loyalty(4)

Strong member base profile with 83% of our members being LSM 9-10 resulting in low credit risk and supporting resilience through the economic cycle

Substantial new club roll-out potential of 8-10 clubs p.a. in the medium term

Excellent financial profile with strong growth, margins and operating cash conversion (c.85%)(2)

Small chains

Independents

ZARMM

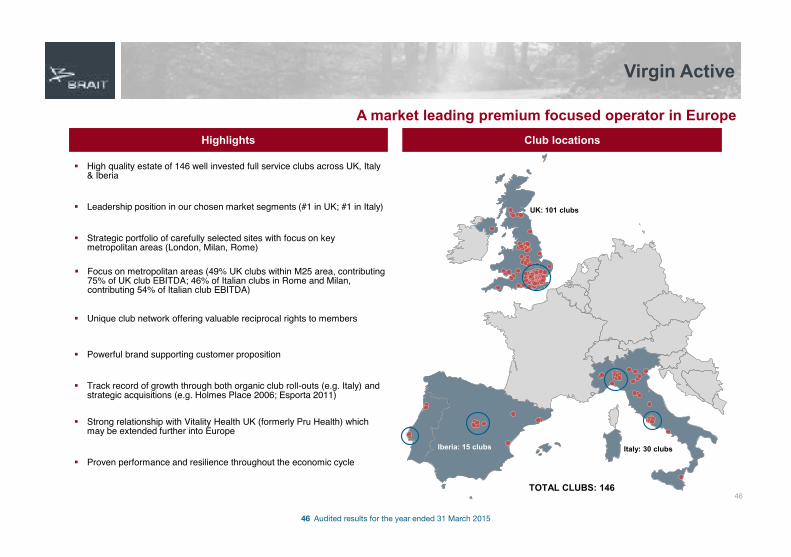

46 Audited results for the year ended 31 March 2015

Virgin Active

46

A market leading premium focused operator in EuropeClub locations Highlights

Leadership position in our chosen market segments (#1 in UK; #1 in Italy)

Strategic portfolio of carefully selected sites with focus on key metropolitan areas (London, Milan, Rome)

High quality estate of 146 well invested full service clubs across UK, Italy & Iberia

Unique club network offering valuable reciprocal rights to members

Powerful brand supporting customer proposition

Focus on metropolitan areas (49% UK clubs within M25 area, contributing 75% of UK club EBITDA; 46% of Italian clubs in Rome and Milan, contributing 54% of Italian club EBITDA)

Track record of growth through both organic club roll-outs (e.g. Italy) and strategic acquisitions (e.g. Holmes Place 2006; Esporta 2011)

Proven performance and resilience throughout the economic cycle

Strong relationship with Vitality Health UK (formerly Pru Health) which may be extended further into Europe

TOTAL CLUBS: 146

UK: 101 clubs

Iberia: 15 clubs Italy: 30 clubs

47 Audited results for the year ended 31 March 2015

Virgin Active

Multiple channels of growth

Manage to revenue

Manage price and volume to maximise revenue, rather than either measure in isolation

High capacity large club format facilitates a flexible approach which few competitors can match

Continual focus on retention initiatives

CPI + LFL revenue growth

1

Our growth & value creation drivers

Secondary revenue

Better monetise member base by driving secondary revenue

Market-by-market assessment of opportunities

Technology used to engage members within and outside of clubs

Secondary streams assist member retention (e.g. PT, swim)

Increase contribution from

secondary revenue each year

2

Existing estate Expansion

Margin enhancement

Leverage existing cost base in clubs and central support structures

New clubs layered into existing central cost base

Shared best practice across the business

Purchasing efficiencies from scale

50-100bps improvement in

Underlying EBITDA margin each year

3Premiumise the estate

and manage the portfolio

Disciplined ongoing capital expenditure to maintain quality estate

Strategic investment in refurbishments to premiumise clubs and differentiate from competitors where demographics are supportive

Select portfolio management of underperforming clubs

UK premiumisation programme peaking

in 2014/15

4

New club roll-out pipeline

Clear roll-out pipeline confirmed in South Africa & wider Africa

Selective pipeline in leading European cities

Roll-out pipeline established in Asia Pacific

Global brand rights to support further growth into new territories

Grow estate by 13-15 clubs p.a. over the medium term

5

Strategic & tactical M&A

Strategic & tactical M&A building on successful track record

Disciplined approach based on ability to improve operating performance through implementation of the proven Virgin Active model

Opportunity for further consolidation in existing markets

Key global targets under continual

review

6

47

48 Audited results for the year ended 31 March 2015

6 57

7

221

2

13

8

11

14-1612-14

0

5

10

15

20

25

2012A 2013A 2014A 2015P 2016PSouth Africa Europe Asia Pacific Pipeline

Virgin Active

A strong roll out pipeline including an exciting growth platform in Asia PacificGroup roll out strategy

An attractive market - Growing health and fitness demand, attractive demographics and highly attractive club profitability dynamics

where we are ideally positioned to succeed - Brand aspiration supportive of premium yields and strong margins and strong developer relationships established with high affinity to the brand

has been successfully established - Five clubs in Australia and successfully launched into both Singapore and Thailand

is poised to capitalise on recent investment - Significant start-up costs on new clubs in 2014, Underlying EBITDA expected to be broadly breakeven in 2015, significant embedded EBITDA from recently opened clubs

and has significant growth potential- Opportunity to leverage brand to expand across broader Asia Pacific, expected roll-out of 4-6 clubs over the next 2 years

Disciplined and return focused roll-out

# clubs

Asia Pacific highlights

Rigorous approach to market and site selection

Seek to become leading scale premium focused operator in any market

Continue successful track record of new club roll-outs:

- >10 new clubs opened on average per annum 2012-14

- Attractive ROCE profiles across geographies – historical club openings have achieved an average 3yr ROCE of >40%(2)

- South Africa: leverage market position to seize on market opportunities across multiple segments and extend to other African countries (e.g. Namibia, Kenya, Botswana)

- Europe: focus on prime metropolitan locations in key cities

- Asia Pacific: build network in Thailand, Singapore and Australia and explore opportunities to launch in other Asian markets (e.g. Manila, Jakarta, Beijing, Shanghai)

Focused property team with unique execution capabilities

- Development team comprises of three former territory MD’s, including group founder

- Excellent track record of meeting projected member targets for each new club

Future rollout plans broadly in line with historical trajectory, plus new RED format

Notes:1. Pipeline defined as sites for which a lease or Letter of Intent has been signed or the site is under advanced discussion; 2. Includes 2 clubs under construction

(1)

48

49 Audited results for the year ended 31 March 2015

2030

38

6574 81 83

9199

111124

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Virgin Active

Excellent track record of long term growth

Underlying EBITDA

Clubs

96 115

164 169 180 189 194235 248 256 267

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Members

506625

832 873 881 921 9781,160

1,242 1,298 1,321

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

000s(1)

£m(1)

Units(1)

Constant FX

Revenue

£m(1)

Constant FX

Notes:1. Clubs and members as at 31 December and 2011-2014 on a Current Club Portfolio basis, FY2012 – FY2014 revenues on a Current Club Portfolio basis, translated at 2014 average actual FX rates (£1: ZAR 17.8; £1: €1.2; £1: A$1.8; £1: S$2.1; £: THB B53.5)

88 123

186

302 328 352 381 466

586 616 639

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

49

51 Audited results for the year ended 31 March 2015

Virgin Active

Virgin Active has highly attractive financial characteristics

Strong cash generation

Majority of member fees received in advance via direct debit

Operating Cash conversion of c.70%(2)

Strong cash generation supports investment into attractive growth opportunities

5

High visibility:

− ~75% of annual revenues generated by opening membership base

Attrition rates – stable for the last decade

Earnings visibility – subscription-based model3

Notes:1. Year 3 EBITDA ROCE, 2. Average FY2012-2014; 3. CAGR for 2004-2014 Underlying EBITDA translated at 2014 average actual FX rates; 4. Defined as projected incremental EBITDA at maturity of clubs that, at the end of the relevant period, had been open for less than three full years plus premiumisation returns

Significant embedded EBITDA(4) from:

− New club maturity ramp up

− Premiumisation programme

Embedded EBITDA as at 31 Dec 2014 of £23m, which supports attractive near term growth

- Provides visibility on future growth

Earnings visibility – embedded EBITDA4

Manage to revenue

Secondary revenue

Margin enhancement

Premiumise the estate and manage the portfolio

New club roll-out pipeline

Strategic & tactical M&A

Long-term track record of strong growth (20% CAGR)(3)

Excellent future prospects via six growth drivers:

1

2

3

5

4

6

High growth1

Track record of performance through the economic cycle:

− Revenue and Underlying EBITDA growth in every one of the past ten years

Earnings spread across multiple geographies

Resilient performance ¤cy diversification2

3 year club ROCE of ~40% for new club openings across the Group

Higher returns in South Africa (over 100%)(1)

Attractive new club returns 6

51

52 Audited results for the year ended 31 March 2015

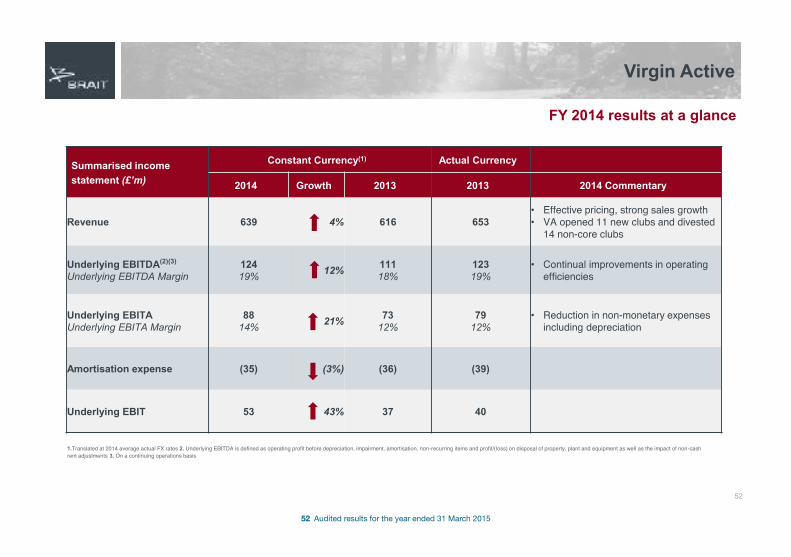

Virgin Active

FY 2014 results at a glance

Summarised income statement (£’m)

Constant Currency(1) Actual Currency

2014 Growth 2013 2013 2014 Commentary

Revenue 639 4% 616 653• Effective pricing, strong sales growth• VA opened 11 new clubs and divested

14 non-core clubs

Underlying EBITDA(2)(3)

Underlying EBITDA Margin12419% 12% 111

18%12319%

• Continual improvements in operatingefficiencies

Underlying EBITAUnderlying EBITA Margin

8814% 21% 73

12%79

12%• Reduction in non-monetary expenses

including depreciation

Amortisation expense (35) (3%) (36) (39)

Underlying EBIT 53 43% 37 40

1.Translated at 2014 average actual FX rates 2. Underlying EBITDA is defined as operating profit before depreciation, impairment, amortisation, non-recurring items and profit/(loss) on disposal of property, plant and equipment as well as the impact of non-cash rent adjustments 3. On a continuing operations basis

52

53 Audited results for the year ended 31 March 2015

Virgin Active

Strong cash flow conversion

Strong cash flow generation reflects good EBITDA growth profile and disciplined capital expenditure

schedule

Maintenance capex relates to all capital expenditure

other than new clubs and premiumisation programme

2012-14 operating cash conversion(8) of c.70%

Cash generation supports self-funded growth

opportunities in new attractive regions

Premiumisation programme expected to peak in 2014 and 2015

Commentary Cash Flow

Notes:1. Group level Operating Cash flow conversion excluding new club capex and Premiumisation capex; 2. Translated at 2014 average actual FX rates; 3. Working capital excludes non-recurring cost cash flows; 4. Working capital adjusted to reflect full licence fee payment within each year (2012 and 2013 incremental licence fee was paid in 2014); 5. Fixed asset disposal proceeds excluded from capex cash flow; 6. Maintenance capex includes head office and IT capex 7. Non-recurring IT and rebranding capex; 8. Defined as (Operating cashflow / Underlying EBITDA (Actual FX)); Based on actual exchange rates; 9. Primarily relates to accrued license fee charges being expensed through the P&L with one-off payment in 2014; 10. On a continuing operations basis

Unlevered cash flow (£m) 2012 2013 2014

Underlying EBITDA(2,10) 99 111 124

Forex adjustment to actual exchange rates 22 12 -

Underlying EBITDA (Actual FX)(10) 122 123 124

Working capital movement(3,4) and discontinued operations (3) (2) (3)

Underlying cash flow from operations 119 121 121

Maintenance and head office capex(5,6) (33) (38) (31)

Operating cashflow(1) 86 83 90

Operating cash conversion(8) 70% 67% 73%

Investments - new clubs, acquisitions and premiumisation (29) (30) (46)

Non-recurring capex(7) (17) - (5)

Exceptional, one off items and proceeds on disposal of assets(4,9) 6 6 (13)

Free cash flow before financing, interest and tax 46 59 26

53

54 Audited results for the year ended 31 March 2015

Virgin Active

54

Update: Q1 FY 2015

Operations

2 new clubs opened in APAC

Completion of the premiumisation of 12 further clubs in the UK

A further 8 non-core clubs divested in the UK

Successful launch of a new UK membership system

New website and app launch soon

Financial

Total revenue up 2%

EBITDA up 16%

56 Audited results for the year ended 31 March 2015

New Look

Consistent delivery of proven strategy

Proven fashion brand with a differentiated product offer

Disciplined financial model and strong track record

Focused international growth

Clear momentum with multiple growth drivers

56

57 Audited results for the year ended 31 March 2015

Managing Director UK & ROIDanny Barrasso

Chief Executive OfficerAnders Kristiansen

New Look CEO since January 2013

Former Vice CEO of Bestseller China, President of Staples China

Previously held senior positions at Lyreco, Herlitz and GBC Corp

Chief Financial OfficerMike Iddon

New Look CFO since September 2014

Former roles at Tesco of Group Planning, Treasury and Tax Director and UK Finance Director

Previously held senior positions at Kingfisher Plc and Whitbread Plc

Chief Creative OfficerRoger Wightman

New Look since February 1990

Previously Group Buying Director for Womenswear and Brands

New Look

Executive Directors

57

New Look since August 2012

Previously at Hilton and Thomas Cook

58 Audited results for the year ended 31 March 2015

New Look

New Look at a glance

Founded in 1969

The UK’s largest total womenswear retailer for under 35’s²

No. 2 for womenswear in the UK² (6.0%)

569 UK stores

Fast growing multichannel operations

Targeted approach to International

Note: All financials to March year end, excluding Mim and on a 52 week basis except for FY13 on a 53 week basisAdjusted EBITDA is a non-IFRS measure, calculated as underlying operating profit before depreciation of tangible fixed assets and amortisation of intangible assets. Adjusted EBITDA margin is Adjusted EBITDA as a percentage of revenue. Adjusted EBITDA and Adjusted EBITDA related measures are not a measurement of performance or liquidity under IFRS or US GAAP and should not be considered by investors in isolation or as a substitute for measures of profit, or as an indicator of the Group’s operating performance or cash flows from operating activities as determined in accordance with IFRS or US GAAP¹ Sales are based on Gross Transactional Value excluding adjustment for concession income on a net basis for statutory reporting purposes² Kantar Worldpanel, 52 weeks ending 15 March 2015; by value³ Kantar Worldpanel, 52 weeks ending 15 March 2015

FY15 Revenue£1,415m

FY15 Adjusted EBITDA£212m

FY12-15 Revenue CAGR3.2%

FY12-15 Adjusted EBITDA CAGR

13.8%

no. of stores as at FY15809

unique UKcustomers in FY15³

13.6m

of UK women shopat New Look³

42%

UK 73%

E-commerce14%

International13%

Sales¹ (FY15) Product mix (FY15)

key 3rd Party E-commerce(“3PE”) partners

11

Fast-fashion74%

Wardrobe essentials

14%

High-fashion12%

58

59 Audited results for the year ended 31 March 2015

• Refresh of brand and customer engagement

• Greater control of margin, inventory and costs

• Refurbishment of store portfolio driving 5.3% gross profit uplift¹

• c.300 stores completed to date

• International strategy focused on 4 priority markets

• China roll-out underway

• Mim disposed in 2014

• Strong multichannel and 3rd party E-commerce expansion

Source: Company information¹ vs. unconverted stores to end FY15, measurable refurbishments only (290 stores)

New Look

Strong momentum underpinned by consistent execution

59

61 Audited results for the year ended 31 March 2015

6.8 10.0 12.6 16.1

24.825.3

28.635.131.6

35.341.2

51.2

2004 2009 2014 2019F

Rest ofMarket

ValueMarket

UK clothing market 1

Value share of UK clothing 1

New Look UK womenswear share 3

No. 2 in UK womenswear 2

11.2

6.0 5.5 5.3 5.13.8

2.5 2.5 2.3 2.3

Mar

ks &

Spen

cer

New

Look

Next

Prim

ark

Debe

nham

s

Geo

rge

Tesc

o

Tops

hop

Mat

alan

Rive

r Isl

and

Valu

e %

Sha

re

1 © 2014 Verdict, reproduced with permission; 2 Kantar Worldpanel (by value) 52 weeks ended March 2015; 3 Kantar Worldpanel; 4 © 2014 Verdict Clothing & Footwear Quarterly Forecasts, reproduced with permission; 5 Company information FY15; 6 Includes girlswear, boyswear and infantswear

Total market size £41.2bn 4

Accessories7%

Childrenswear 6

12%

Menswear 25%

Womenswear 56%

By value (£bn)

21.5%

2004

30.6%

2014

3.2%

FY04

5.8%

FY14

New Look product sales mix 5

New Look

Longstanding and leading position in the value fashion sector

61

Womenswear61%

Footwear16%

Accessories10%

Teenswear6%

Menswear3%

Other4%

* Total market

*

62 Audited results for the year ended 31 March 2015

Source: Company information; Verdict¹ TNS UK Brand Tracker, 9 months to March Note: Mean Net Promoter Score is the average rating that people give when asked how likely they are to recommend the brand to a friend. The score is out of 10 at an individual level and this is then expressed as a %

Brand Awareness¹

91%Prompted awareness

NPS – Recommendation¹

77%Our customers continue to respond positively

and consistently to the brand with strong advocacy levels

MID MARKET BRANDSTraditional UK brands. Higher price, lower fashion content

HIGH FASHIONFashion driven brand. High price points, high fashion

content

VALUE ORIENTED MASS MARKETSupermarkets and value focused

retailers. Low price points low fashion content

VALUE FASHIONCombination of value and fashion content

New Look

Our distinctive brand positioning

62

Low Price

High Price

Trad

ition

al

Hig

h-Fa

shio

n

VeryTopshop

River Island

H&M

Primark

ASOS

boohoo

Debenhams NextM&S

Dorothy Perkins

Asda (George)

PeacocksMatalan

Zara

Online pure-play

63 Audited results for the year ended 31 March 2015

Our price positioning STRATEGY

Inclusive customer profile

1 Source: Kantar Worldpanel, 52 weeks ending March 2015

Price architecture to offer true choice

From EARLY TEENS TO OVER

45’s, with an average customer

age of 33 YEARS

13.6m¹ unique UK CUSTOMERS

in FY15

42%¹ OF UK WOMEN shop at New Look

and we had over 506m VISITS to our

stores and websites

New Look

Fast fashion at value price points maximising our customer appeal

63

HIGH-FASHION

80% cheaper than high-fashion brands; e.g.

MID MARKET BRANDS

40% cheaper than mid market brands; e.g.

FAST-FASHION

Prices to match our competitors;e.g.

MASSMARKET

Wider range of fast-fashion products than value-led mass market brands; e.g.

64 Audited results for the year ended 31 March 2015

New Look

Our extensive fashion media coverage

We’re an award winning fashion retailer

Fabulous High Street AwardsFabulous for footwear

Lorraine High Street Awards Best Shoes

Cosmopolitan #fashfestAwards Best hot for heels

World Retail Awards 2014 Best store design

White City, >1,200 sq m

Topshop 1New Look 2M&S 3River Island 4ASOS 5Zara 6H&M 7Next 8Primark 9Dorothy Perkins 10

245kFollowers on Twitter1

300kWeibo fans1

538kFollowers on Instagram1

3.0mFans on Facebook1

1 End of March 20152 vs. key competitors3 Source: MyMarketMonitor, March 2015 Share of shout based on PR value (£)

£78m PR value in UK and ROI in FY15 3

£15m PR value in China in FY15 3

Our social media mission is to be the “Friendliest Fashion Brand”

We’re a social brand with engaged fans and followers

64

We’re number 2 in the UK for PR value 2

65 Audited results for the year ended 31 March 2015

• 244 suppliers from 778 factories in 29 countries

• Strong relationships based on 40+ years experience

• Our flexible supply chain means we can book orders later and therefore make less investments in stock

• Markdown and discount minimised to maximise margin

New look’s tactical approach to successful trends: Kimono

Initial quantity delivered in February had strong reaction. Buy increased by 60k units in March

Trading and trends indicate bestseller. Total buy increased by nearly 700k units from April to June

We generated £9.7 million of kimono sales in the 13 week period ended June 28, 2014Kimonos

identified as a key trend for spring/summer in January. 40k units sold across January and February 2014

From design to shop floor in 13 weeks... for certain products it’s just 2 weeks

• Directly operated, highly automated distribution centre in Stoke-on-Trent

• c.£100m investment; upgrade programme complete

• 75,000 sq m (0.8m sq ft) with a capacity of c.180m units p.a.

• 3.1 deliveries per UK store per week

• We currently achieve a 98% delivery accuracy

• Outsourced distribution hubs in Singapore and Shanghai serve our markets in Asia

Fast Fashion 74%

High Fashion12%

Wardrobe Essentials

14%

Product intake mix

Source: Company information

New Look

Flexible fast fashion supply chain

65

66 Audited results for the year ended 31 March 2015

• 569 stores, 98% profitable

• 371,000 sq m (4.0m sq ft) footprint

• Successful across a range of locations: shopping centres, prime high street and local markets

• Flexible with average remaining lease length less than 5 years

Store numbers ¹

Well established store presence in the UK

United Kingdom 569Asia China 19Europe France 28

Germany 23²Poland 13Republic of Ireland 29Netherlands and Belgium 23²

Total Owned 704

Franchise 105

Total Owned and Franchise 809

A growing global footprint

Continued investment in refreshing our owned stores

Growth is focused on 4 markets

• China

• Poland

• France

• Germany

New Look

Proven multichannel platform: integrated store base

¹ As at FY15² Includes concessions 66

67 Audited results for the year ended 31 March 2015

New Look

Proven multichannel platform: E-commerce

Fully integrated with store base• Multichannel spend continues to rise• Drives ATV and customer spend• Click & Collect and Returns both proven processes across the estate

E-commerce• Average of 4.5m visits a week2

• 3rd most visited website³ with a share of 4.3% by visits³• In house pick & pack and DC• France and Germany local language websites

M-commerce• Now accounting for c.45% of online visits• Core future focus, especially via apps

New Look own website sales¹ (£m)

c.26% of E-commerce orders

E-commerce M-commerce Click & Collect Order In Store28% use Click & Collect 9% of E-commerceProven ATG/Oracle platform

62.7

89.8

127.8

166.7

FY12 FY13 FY14 FY15

Source: Company informationNote: All financials to March year end1 Sales based on Gross Transactional Value excluding adjustment for concession income on a net basis for statutory reporting purposes; 2 Company information; 3 Experian, March 2015, Hitwise category “Shopping and Classifieds-Apparel and Accessories” 67

68 Audited results for the year ended 31 March 2015

Launched in 2013 with select partners

• 11 supply partnerships

Attractive financial model

• Profitable wholesale commercial arrangements

• Low capital employed

• Minimal stock risk

International reach

• Over 240 countries served

• Strong menswear participation (c.16%)0.0

1.6

22.0

34.0

FY12 FY13 FY14 FY15

3rd party E-commerce sales 1 (£m)

Source: Company informationNote: All financials to March year end1 Sales based on Gross Transactional Value excluding adjustment for concession income on a net basis for statutory reporting purposes

(Europe)

New Look

Proven multichannel platform: 3rd party E-commerce

68

69 Audited results for the year ended 31 March 2015

KPI commentary Key financials ¹

• Robust sales growth with UK business driving LFL sales growth and improving market share3

• Expanding gross margins driven by full price sales and focused promotions

• Productivity improvements and tight management of the cost base supporting adjusted EBITDA margin growth

• Strong cash generative business model

• Disciplined capital investment throughout the period

Source: Company information* Restated to reflect the divestment of Mim in FY15 1 All financials on a 52 week basis except for 2013 on a 53 week basis2 FCF defined as cash flow from continuing operating activities (pre tax) less net investing activities; FCF conversion defined as FCF/adjusted EBITDA3 Womenswear (Kantar Worldpanel (by value) 52 weeks to end March 2015)

March YE (£m) 2012* 2013* 2014* 2015 CAGR 2012-2015

Revenue 1,286 1,330 1,368 1,415 3.2%

% growth (0.5)% 3.4% 2.9% 3.4%

UK LFL sales growth (5.7)% (0.5)% 3.0% 5.0%

Gross profit 652 700 722 746 4.6%

% margin 50.7% 52.6% 52.8% 52.7%

Adjusted EBITDA 144 184 204 212 13.8%

% margin 11.2% 13.8% 14.9% 15.0%

Underlying operating profit 75 118 141 153 26.8%

% margin 5.8% 8.9% 10.3% 10.8%

Free Cash Flow (FCF) 2 80 99 145 147 22.5%

% conversion 2 55.6% 53.8% 71.1% 69.3%

Total capex 47 60 49 60 8.5%

% revenue 3.7% 4.5% 3.6% 4.2%

New Look

A track record of growth

69

70 Audited results for the year ended 31 March 2015

New Look

Focused strategy for growth

Product Development

International ExpansionBrand

E-commerce Menswear

Our strategy is based

upon 5 key pillars

70

71 Audited results for the year ended 31 March 2015

New Look

Brand

Consistent global brand identity now established across:

Stores

E-commerce

Product

Concept store refurbishment programme being rolled-out

Dual-gender approach to be created to develop Menswear identity

CRM strategy to drive long term loyalty and leverage profit

71

72 Audited results for the year ended 31 March 2015

8 1983

157278

312 342

6,340

2012 2014 2010 2006 2007 2006Excl.Zara

2005(Re-

launch)

1996 19 stores trading at end March 2015

A range of Tier 1, 2 & 3 cities and malls

Aggregate positive store contribution

Experienced local management team based in Shanghai

Rapid development of local skills and supply chain

Tmall E-commerce presence

New Look

International expansion

Significant growth opportunityChina

Launch

Source: Retailer websites

72

73 Audited results for the year ended 31 March 2015

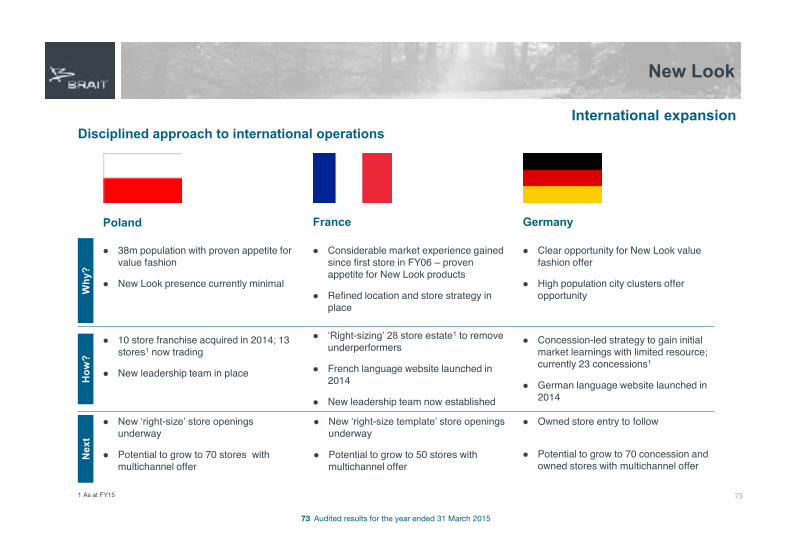

Disciplined approach to international operations

Poland Germany

38m population with proven appetite for value fashion

New Look presence currently minimal

Clear opportunity for New Look value fashion offer

High population city clusters offer opportunity

10 store franchise acquired in 2014; 13 stores1 now trading

New leadership team in place

New ‘right-size’ store openings underway

Potential to grow to 70 stores with multichannel offer

France

Considerable market experience gained since first store in FY06 – proven appetite for New Look products

Refined location and store strategy in place

‘Right-sizing’ 28 store estate1 to remove underperformers

French language website launched in 2014

New leadership team now established

New ‘right-size template’ store openings underway

Potential to grow to 50 stores with multichannel offer

Concession-led strategy to gain initial market learnings with limited resource; currently 23 concessions1

German language website launched in 2014

Owned store entry to follow

Potential to grow to 70 concession and owned stores with multichannel offer

New Look

International expansion

Why

?H

ow?

Nex

t

1 As at FY15 73

74 Audited results for the year ended 31 March 2015

Multichannel customers are our best customers

3x more spend than in-store only 1

1 in 10 store visits is a result of a visit to the website 2

1 in 5 Click and Collect customers make an additional purchase when collecting 2

Local language websites rolling out internationally

France and Germany already live

97%77%3%

23%

FY12 FY15

Desktop sales Mobile / Tablet sales

Online sales (£m)

£62.7m

£166.7m

New Look

E-commerce

Already shipping to over 240 countries globally

New Look brand embodies British fashion to global consumers

Lifts brand awareness ahead of potential market entry

Resource light, low capital intensity

Looking to seal further wholesale partnerships

New opportunities are currently being explored in Europe, Africa, South & North America and Asia

We already have 11 partnerships with selected 3rd party e-tailers

Multichannel 3rd party E-commerce

Multichannel makes our product available any way our customers want to shop

1 Kantar Worldpanel data, 52 weeks ending March 20152 Company information

74

75 Audited results for the year ended 31 March 2015

Consistent delivery across ranges building on our track record and brand signature

“Selling a look” concept to drive incremental profit

Broader range construction to offer maximum choice

Drive sales and margins1 Kantar Worldpanel, 52 weeks to March 20152 Verdict, 2015

New categories and improved range construction

UK market grew by 26.3%1 YOY; our share is currently only 0.5%1

Launched in August 2014 with 10 store trial

Rolled out to 150 UK stores in January 2015

Trialling in international markets

Activewear case study Cosmetics and fragrance case studyUK market forecast to grow by 24% in the 5 years to 2019 2

Launched in October 2014 across 200 stores

Now rolled out across UK and Europe

Fragrance now in 520+ stores

Cosmetics now in 450+ stores

Further potential expansion into body care and bath products

New Look

Product development

75

76 Audited results for the year ended 31 March 2015

New Look

Menswear

Menswear accounts for 25% of UK clothing market worth c.£10bn by value1

Refurbished stores have doubled the mix in menswear

16% of stock sold to our largest 3rd party partner is Menswear

Strengthened management team and approach:

Dual gender homepage launched in 2014

New men’s shop-in-shop trial in March 2015

Menswear brand awareness campaign planned from Summer 2015

New Menswear Director joining from H&M in Summer 2015

Driving menswear mix from 3%

16%menswear mix

to ASOS

761 Verdict, 2015

77 Audited results for the year ended 31 March 2015

New Look

New look is well positioned for future growth

Increasingly global dual gender fashion brand

Flexible fast fashion operating model

Differentiated multichannel capabilities

In the fastest growing market segment

Disciplined financial model and strong track record

Focused international growth

Clear momentum with multiple growth drivers

77

78 Audited results for the year ended 31 March 2015

Brait’s attraction to new acquisitions

78

Attractions Demonstrated through

Alignment • Brait is the controlling shareholder alongside management, the founder and Virgin Group

• Brait is the controlling shareholder alongside management and the founder

Management • Experienced, aligned and proven team • Experienced, aligned and proven team

Market leader

• Outstanding business in South Africa• No. 1 in UK and Italy

• Strong brand awareness in particular amongst women in the UK• No. 2 UK overall womenswear; No. 1 UK under-35 womenswear

Clear strategy