2015 state of the insurance industry

TRANSCRIPT

© 2015 Agency Revolution, All Rights Reserved

State of the Industry 2015

Mending The Broken Promise: How to close the breach, regain the trust and recover the heart of the insurance customer

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

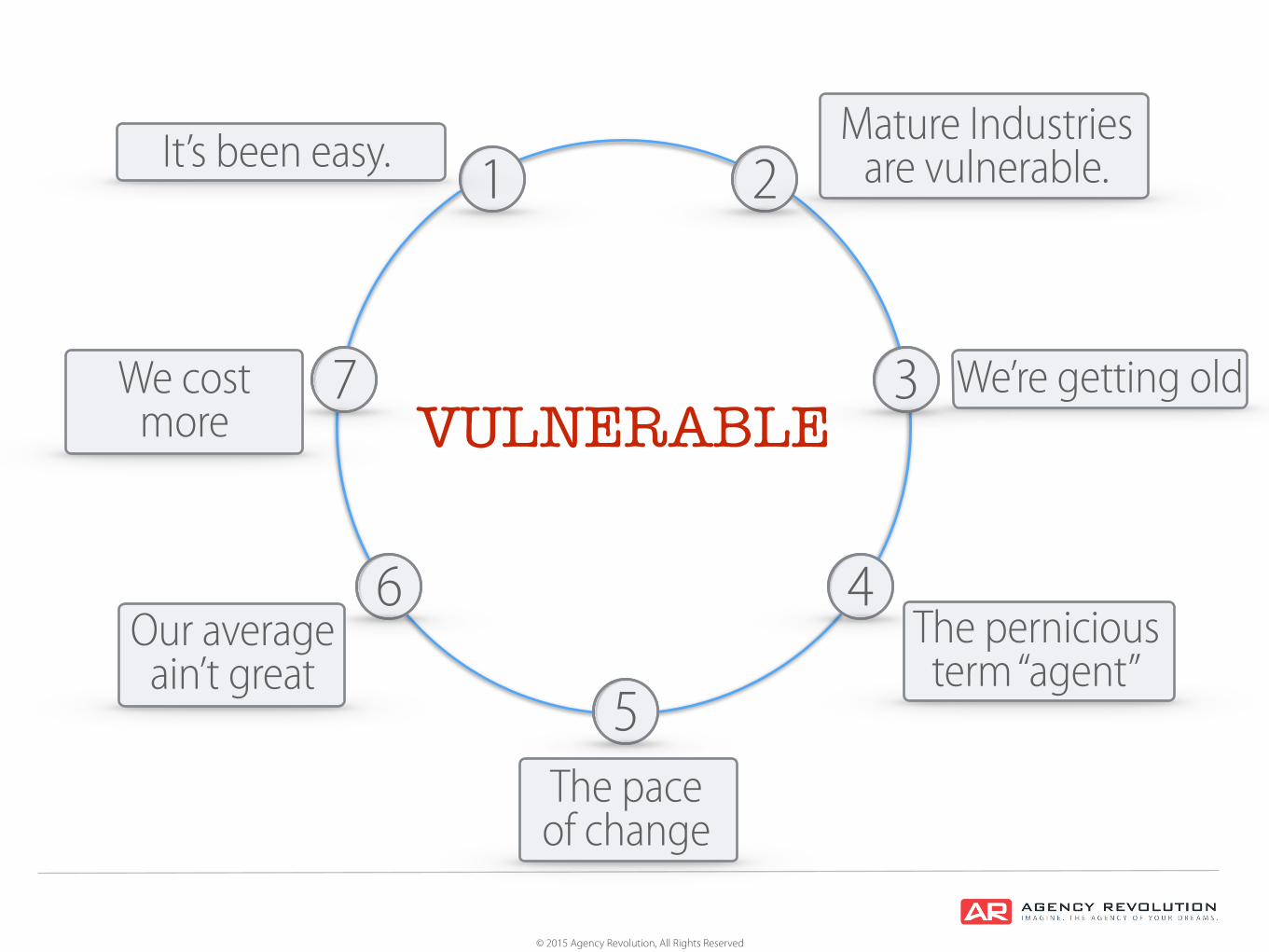

7 points of vulnerability.

Proof: Empirical evidence.‣Changes in consumer behavior.‣Changes in carrier behavior.‣Changes in the nature of risk.

5 point action plan.‣ For retail agents and the industry that

serves them.

© 2015 Agency Revolution, All Rights Reserved

“This is a relationship business.”

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

BROKEN PROMISE

© 2015 Agency Revolution, All Rights Reserved

VULNERABLE7

1 2

3

4

5

6

© 2015 Agency Revolution, All Rights Reserved

It’s been easy.

Points of vulnerability.

1

© 2015 Agency Revolution, All Rights Reserved

Growth of the US economy

It’s been easy.1

© 2015 Agency Revolution, All Rights Reserved

Growth of the US economy

It’s been easy.1

© 2015 Agency Revolution, All Rights Reserved

Marketing meant.

It’s been easy.1

© 2015 Agency Revolution, All Rights Reserved

VULNERABLE

What got you here, won’t get you there.

It’s been easy.1

© 2015 Agency Revolution, All Rights Reserved

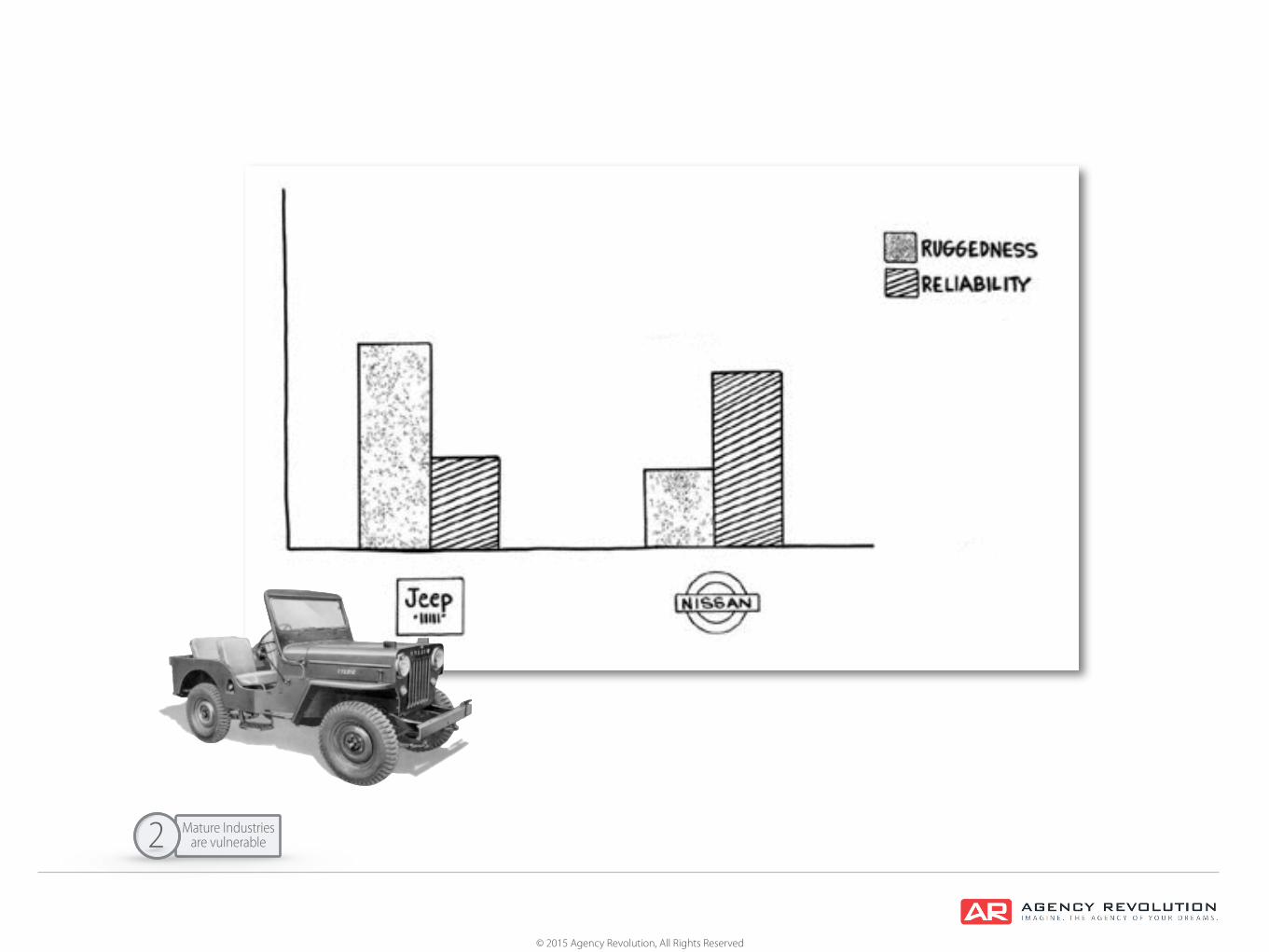

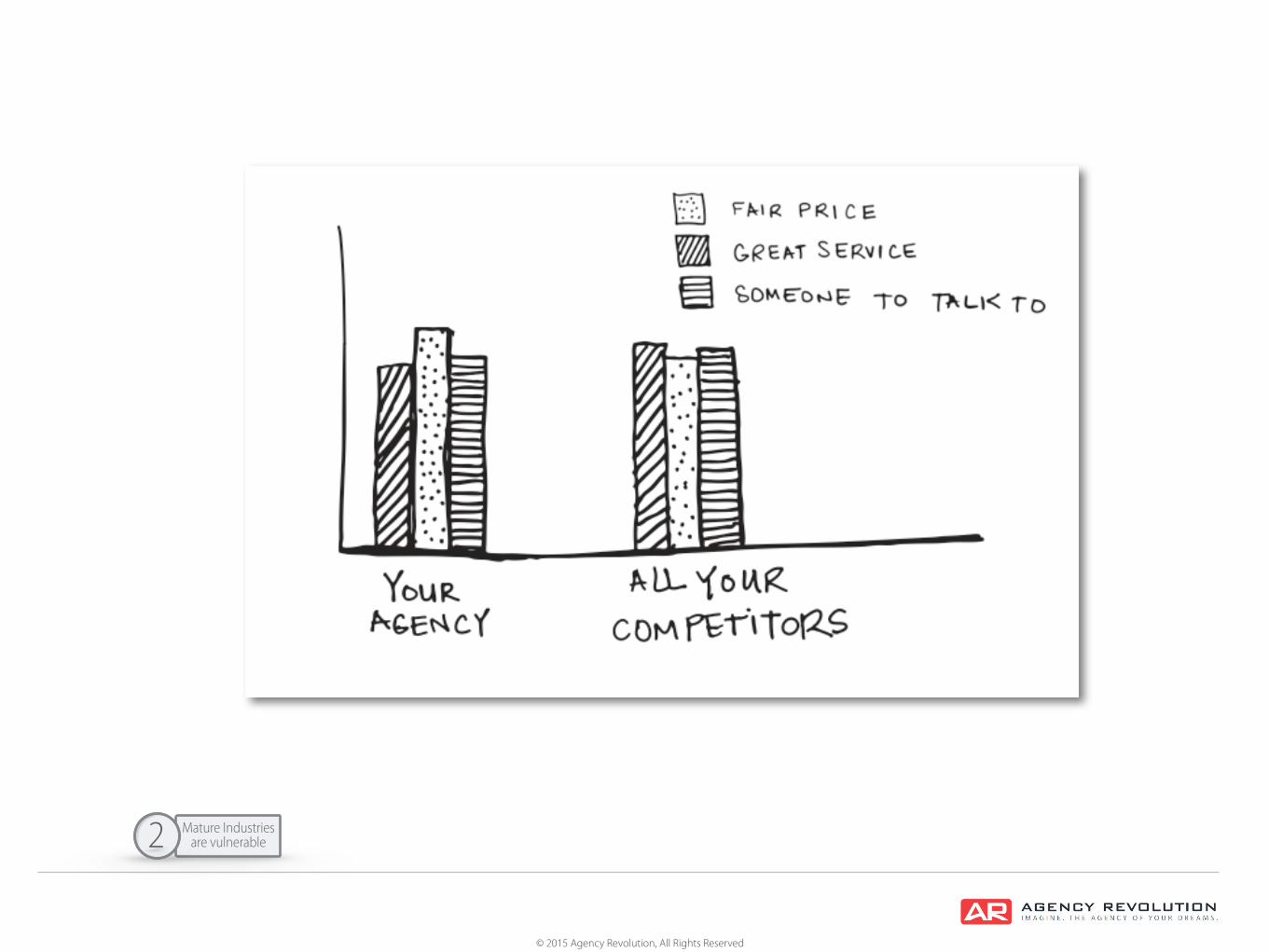

Mature Industries are vulnerable.

Points of vulnerability.

2

© 2015 Agency Revolution, All Rights Reserved

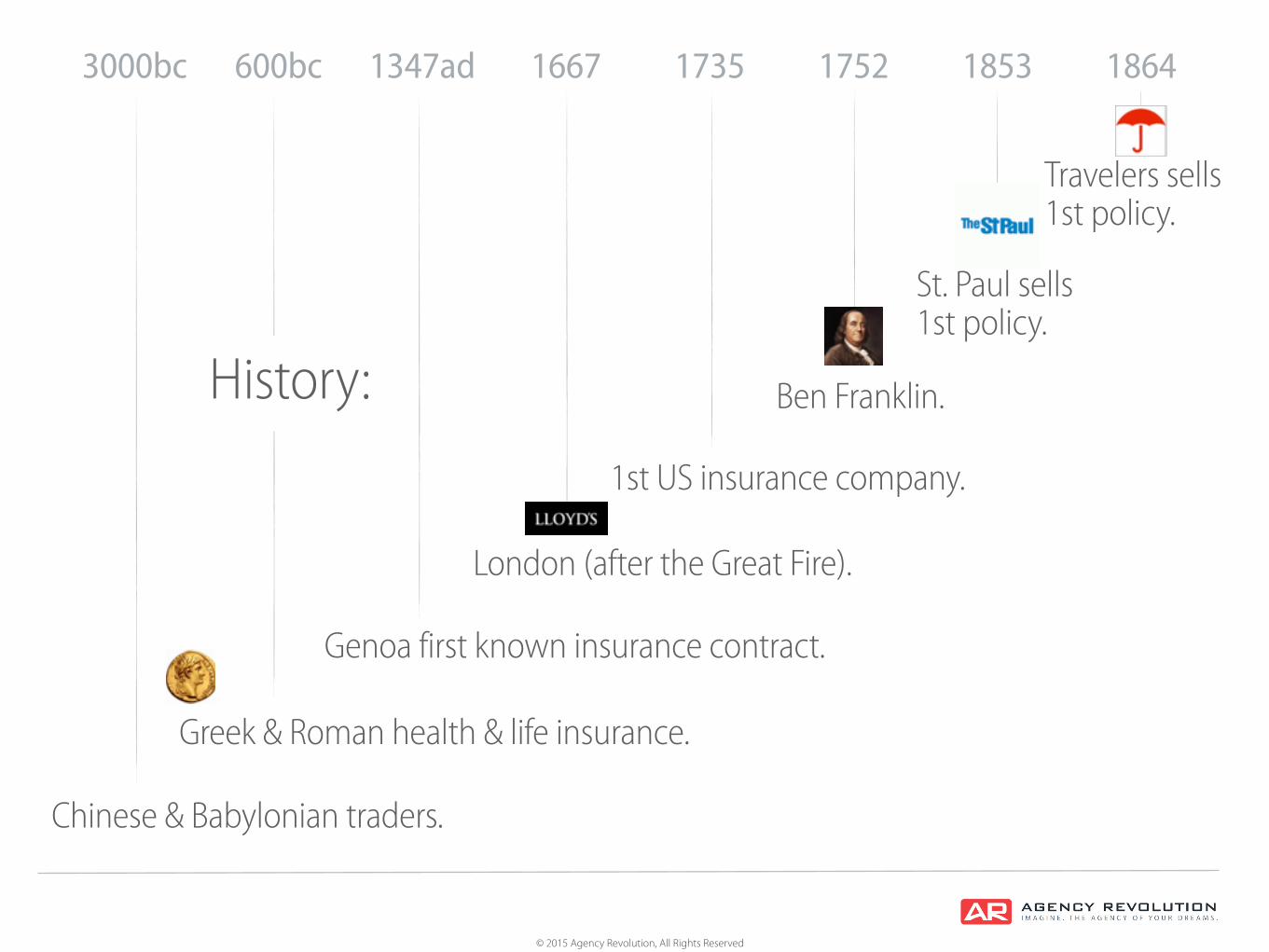

Chinese & Babylonian traders.

3000bc

Greek & Roman health & life insurance.

600bc

Genoa first known insurance contract.

1347ad

London (after the Great Fire).

1667

1st US insurance company.

1735

Ben Franklin.

1752

St. Paul sells1st policy.

1853 1864

History:

Travelers sells1st policy.

© 2015 Agency Revolution, All Rights Reserved

The habits, processes and bureaucratic interests resist CHANGE.

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Not because the industry isn't good.

Mature Industries are vulnerable2

Carrier

Agent

Consumer

© 2015 Agency Revolution, All Rights Reserved

Disruption generally happens when the industry is at its highest PEAK of Excellence.

Mature Industries are vulnerable2

VULNERABLE

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

ç

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Smaller, more nimble entities, oftenoutsiders, disrupt. ‣ Usually with technology.

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Blacksmith, Henry Ford

Mature Industries are vulnerable2

© 2015 Agency Revolution, All Rights Reserved

Kodak

Mature Industries are vulnerable2

“...it was film-less photography, so management’s reaction was, ‘that’s cute - but don’t tell anyone about it.’ ” Steve Sasson,1975

© 2015 Agency Revolution, All Rights Reserved

Netflix

Mature Industries are vulnerable2

“Neither RedBox nor Netflix are even on the radar screen in terms of competition...”

Blockbuster CEO Jim Keyes: 2008

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

A NEW INDUSTRY GROUPRUN UNDER THE GUIDANCE OF

THE ASSOCIATION OF OPTOMETRISTS (AOP)HAS BEEN CREATED TO ADDRESS PRACTICE DECLINE

© 2015 Agency Revolution, All Rights Reserved

Warby Parker ‣ Founder Neil Blumenthal’s 1st rule of success

“Cut Out the Middle Men.”

Mature Industries are vulnerable2

Started 2010Sold 500,000 pairs of glasses by 2013.

© 2015 Agency Revolution, All Rights Reserved

Travel agencies

Number of traditional travel agencies.

Source: Phocuswright; Airline reporting corp. (ARC); ASTA.org

1995

47,000

2011

14,000

2000

38,800

© 2015 Agency Revolution, All Rights Reserved

Mature Industries are vulnerable2

80,000 agencies. 1980 40,000 agencies.

2015

© 2015 Agency Revolution, All Rights Reserved

Points of vulnerability.

We're getting old.3

© 2015 Agency Revolution, All Rights Reserved

Average age of agency principal: 59.

We are getting old3

© 2015 Agency Revolution, All Rights Reserved

25% will be gone by 2018

We are getting old3 McKinsey & Co

2015 2018

© 2015 Agency Revolution, All Rights Reserved

‣ Number of employees 55 and older in P&C is 30% higher than any other industry.

‣ Carriers will have to replace 400,000employees by 2020.

‣ 72% of principals with over 20% ownershipis over 60.

We are getting old3Accenture, AM Best, IIABA

© 2015 Agency Revolution, All Rights Reserved

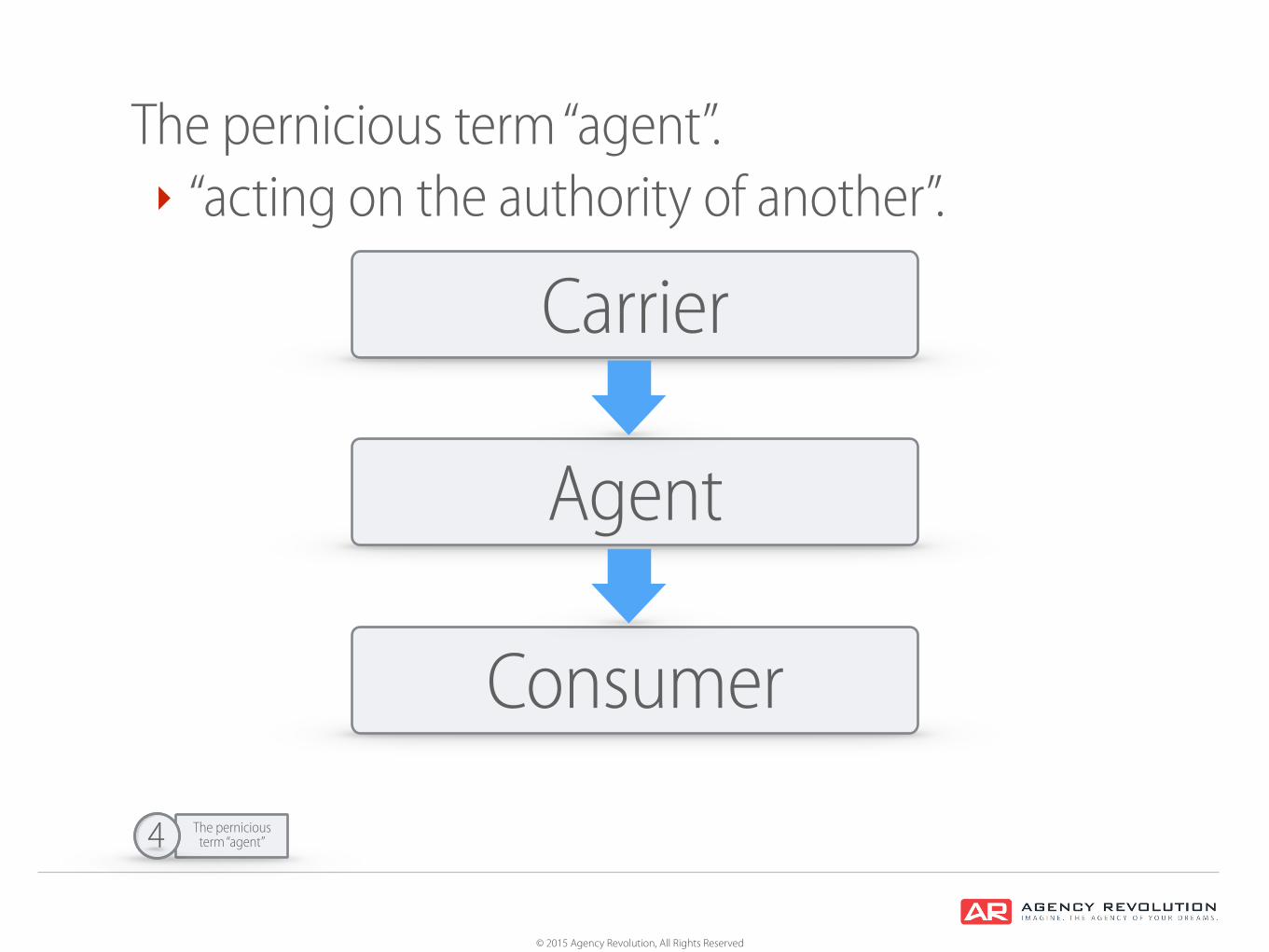

The pernicious term “agent".

Points of vulnerability.

4

© 2015 Agency Revolution, All Rights Reserved

The pernicious term “agent”. ‣ “acting on the authority of another”.

The pernicious term “agent”4

Carrier

Agent

Consumer

© 2015 Agency Revolution, All Rights Reserved

The paceof change.

Points of vulnerability.

5

© 2015 Agency Revolution, All Rights Reserved

The pace of change. "Worried the world is changing faster

than my agency.”

The paceof change5

4%

96%

© 2015 Agency Revolution, All Rights Reserved

“If the rate of change on the outside exceeds the rate of change on the inside, the end is near.”

Jack Welch

Chairman and CEO, General Electric,1981- 2001

The paceof change5

© 2015 Agency Revolution, All Rights Reserved

OUR AVERAGE AIN'T THAT GREAT

Points of vulnerability.

6

© 2015 Agency Revolution, All Rights Reserved

And “on average” thats how themarketplace judges us.

Average ain’t that great6

© 2015 Agency Revolution, All Rights Reserved

This is a built in systemic weakness.

The “independence” of 40,000 delivery entities inherently lacks business discipline.

Average ain’t that great6

© 2015 Agency Revolution, All Rights Reserved

Cannot enforce: ‣ Best Practices. ‣ Brand discipline.

Average ain’t that great6

© 2015 Agency Revolution, All Rights Reserved

Compare to: ‣ 17,000 Starbucks cafes ‣ 63,000 Nordstrom employees ‣ 437 Apple Stores

Statista 2015Average ain’t that

great6

© 2015 Agency Revolution, All Rights Reserved

Timken Professor of Business Administration, Harvard Business School

Cynthia A. Montgomery

“Does your company matter? That’s the most important question every business leader must answer.”

Average ain’t that great6

© 2015 Agency Revolution, All Rights Reserved

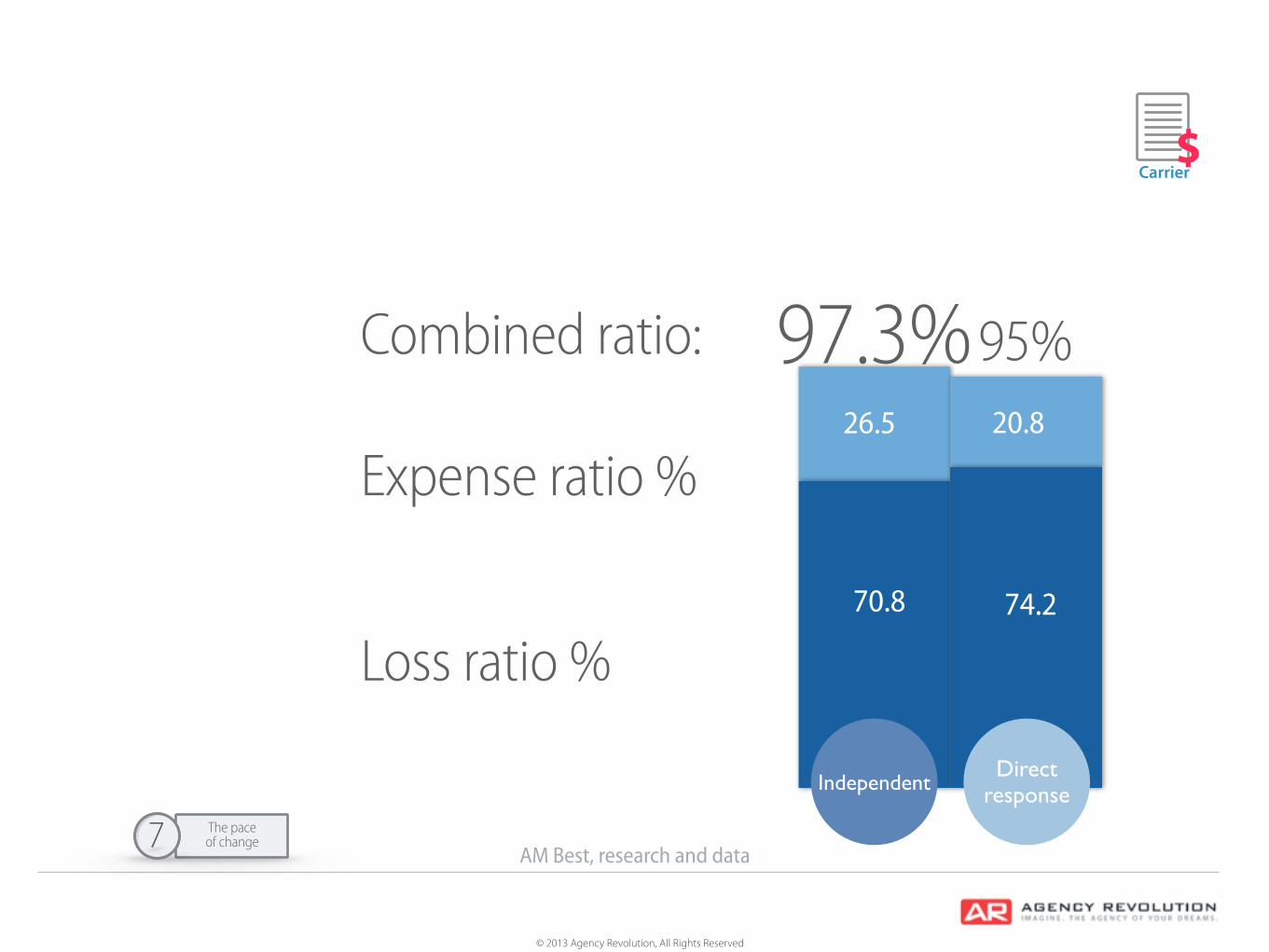

We cost more.

Points of vulnerability.

7

© 2013 Agency Revolution, All Rights Reserved

AM Best, research and data

70.8 74.2

Loss ratio %

Expense ratio %

97.3%95%Combined ratio:

Carrier$

IndependentDirect

response

26.5 20.8

The paceof change7

© 2015 Agency Revolution, All Rights Reserved

VULNERABLE7

1 2

3

4

5

6

It’s been easy. Mature Industries are vulnerable.

We’re getting oldWe cost more

Our averageain’t great

The perniciousterm “agent”

The paceof change

© 2015 Agency Revolution, All Rights Reserved

Prove It. ‣ What Consumers are saying and doing.

© 2015 Agency Revolution, All Rights Reserved

13%6%

10%

71%

Online800 NumberYellow PagesNot Sure

71% use the internet to research insurance. 54% have received a quote online.

© 2015 Agency Revolution, All Rights Reserved

New auto insurance placed by local broker:

2003 2008

80%

68%

Changes in Consumer Behavior.

© 2015 Agency Revolution, All Rights Reserved

New auto insurance placed by local broker:

2003 2008 2010

80%

63%

68%

Changes in Consumer Behavior.

© 2015 Agency Revolution, All Rights Reserved

How did you originally purchase your current auto insurance Policy?

Local Broker51%75%

Online26%

7%

Less than 1 year5+ years

© 2015 Agency Revolution, All Rights Reserved

Now it's #4. 24%

14%

2007 2012

In 2007, the service experience delivered by local brokers was the #1 driver of insurance customers’ overall satisfaction.

© 2015 Agency Revolution, All Rights Reserved

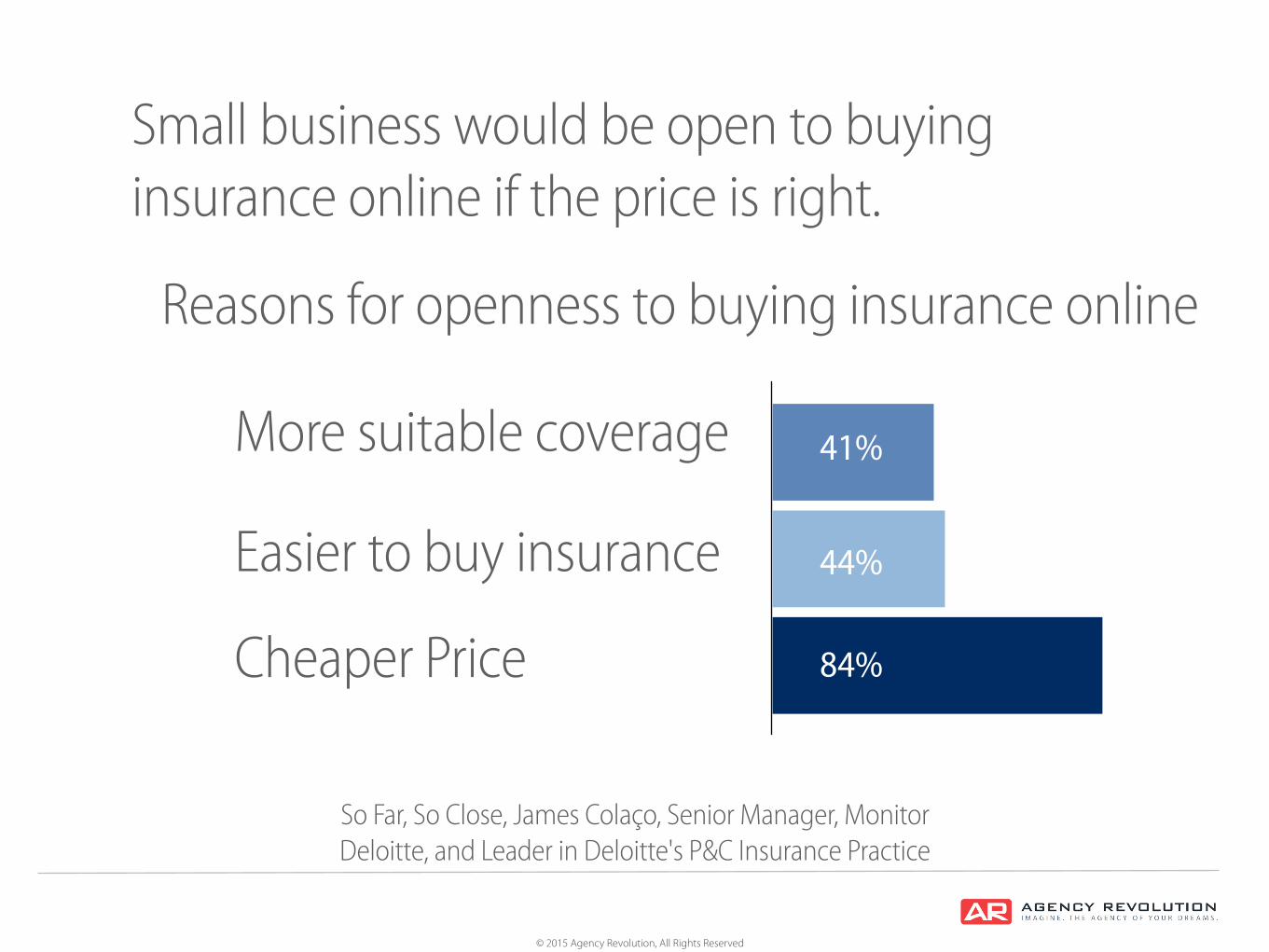

Small business would be open to buying insurance online if the price is right.

So Far, So Close, James Colaço, Senior Manager, Monitor Deloitte, and Leader in Deloitte's P&C Insurance Practice

84%

Cheaper Price

Easier to buy insurance

More suitable coverage

44%

41%

Reasons for openness to buying insurance online

84%

© 2015 Agency Revolution, All Rights Reserved

Prove It. ‣ What Carriers are doing.

© 2015 Agency Revolution, All Rights Reserved

2002 2011

1.7

5.9

Marketing spend for P&C carriers $ billions.

347% increase.

© 2015 Agency Revolution, All Rights Reserved

Marketing spend 2011:Millions of advertising dollars spent.

Farmers 718

State Farm 813Geico 1,000

Progressive 536

Allstate 745

Liberty Mutual

American FamilyTravelers

Nationwide

AIG

332

167166

277

12592USAA

$1 BILLION

© 2015 Agency Revolution, All Rights Reserved

Government Employee Insurance Company, “GEICO”

201220092008 2010 2011

$11 billion

$6

$3.5 billion

$7

$9

© 2015 Agency Revolution, All Rights Reserved

Progressive: Average growth 17% per year.

201220091996 2010 2011

$16 billion

$3.4 billion

© 2015 Agency Revolution, All Rights Reserved

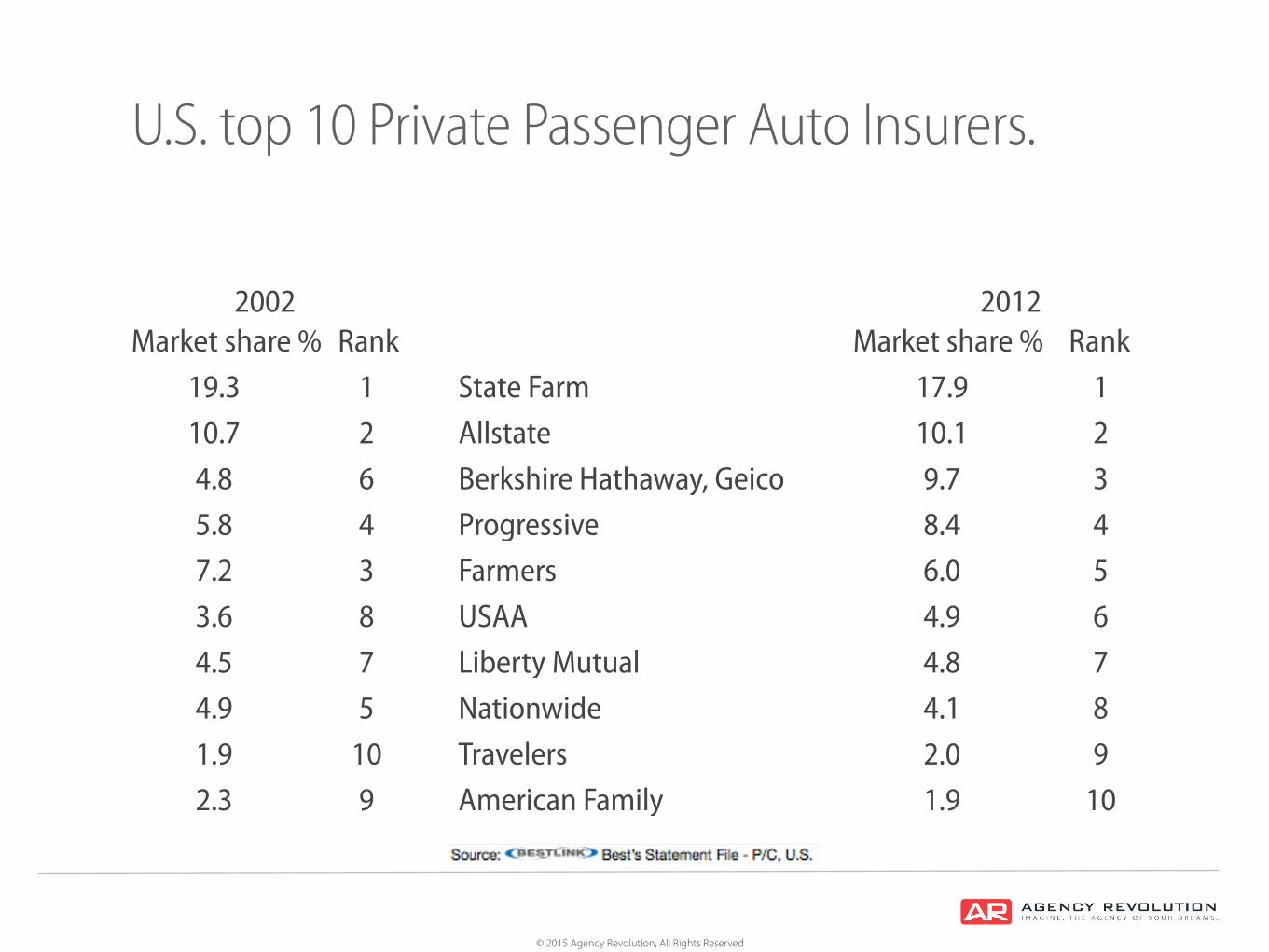

U.S. top 10 Private Passenger Auto Insurers.

State Farm1 117.919.3

Farmers3 56.07.2Progressive4 48.45.8

Allstate2 210.110.7

Market share %Market share % Rank Rank2002 2012

© 2015 Agency Revolution, All Rights Reserved

U.S. top 10 Private Passenger Auto Insurers.

State Farm1 117.919.3

Farmers3 56.07.2Progressive4 48.45.8

American FamilyTravelersNationwideLiberty MutualUSAA

Berkshire Hathaway, Geico

910578

6

109876

3

1.92.04.14.84.9

9.7

2.31.94.94.53.6

4.8Allstate2 210.110.7

Market share %Market share % Rank Rank2002 2012

© 2015 Agency Revolution, All Rights Reserved

U.S. top 10 Private Passenger Auto Insurers.

State Farm1 117.919.3

Farmers3 56.07.2Progressive4 48.45.8

American FamilyTravelersNationwideLiberty MutualUSAA

Berkshire Hathaway, Geico

910578

6

109876

3

1.92.04.14.84.9

9.7

2.31.94.94.53.6

4.8Allstate2 210.110.7

Market share %Market share % Rank Rank2002 2012

© 2015 Agency Revolution, All Rights Reserved

Available Now At The GEICO Store

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

Rise in direct response premium by channel.

AM Best, IIABA Market Share Report

© 2015 Agency Revolution, All Rights Reserved

Rise in direct response premium by channel.

AM Best, IIABA Market Share Report

48 46 44

32 31 29

2003 2007 2011

Personal auto

Independent broker

Captive agent

8077

73

© 2015 Agency Revolution, All Rights Reserved

Rise in direct response premium by channel.

AM Best, IIABA Market Share Report

20 23 27

48 46 44

32 31 29

2003 2007 2011

Personal auto

Independent broker

Captive agent

Direct

© 2015 Agency Revolution, All Rights Reserved

Rise in direct response premium by channel.

AM Best, IIABA Market Share Report

39 38 38

57 57 56

4 5 6

77 81 77

23 19 2320 23 27

48 46 44

32 31 29

2003 2007 2011 2003 2007 2011 2003 2007 2011

Personal auto Homeowners Small commercial

Independent broker

Captive agent

Direct

© 2015 Agency Revolution, All Rights Reserved

Prove It. ‣ Further threats.

© 2015 Agency Revolution, All Rights Reserved

Further Threats. (from technology) "Could the broad

adoption of currently available technologies result in a radical reduction in the auto insurance business?"

A Scenario: The End of Auto

Insurance. What Happens When

There Are (Almost)No Accidents.

© 2015 Agency Revolution, All Rights Reserved

Further Threats.The End of Auto Insurance.

Timings for the adoption of key technologies.

© 2015 Agency Revolution, All Rights Reserved

Further Threats.The End of Auto Insurance.

Mandatory

Preferred

Voluntary

Available

2012 2023-20272018-20222013-2017

Timings for the adoption of key technologies.

© 2015 Agency Revolution, All Rights Reserved

Further Threats.The End of Auto Insurance.

Mandatory

Preferred

Voluntary

Available

2012

Telematics

Automated Enforcement

2023-20272018-2022Automated

Enforcement

2013-2017

Telematics

Automated Enforcement

Timings for the adoption of key technologies.

© 2015 Agency Revolution, All Rights Reserved

Further Threats.The End of Auto Insurance.

Mandatory

Preferred

Voluntary

Available

2012

Telematics

Automated Enforcement

Collision Avoidance

2023-2027

Robot Cars

2018-2022Automated

Enforcement

Collision Avoidance

Robot Cars

2013-2017

Telematics

Automated Enforcement

Collision Avoidance

Robot Cars

Timings for the adoption of key technologies.

© 2015 Agency Revolution, All Rights Reserved

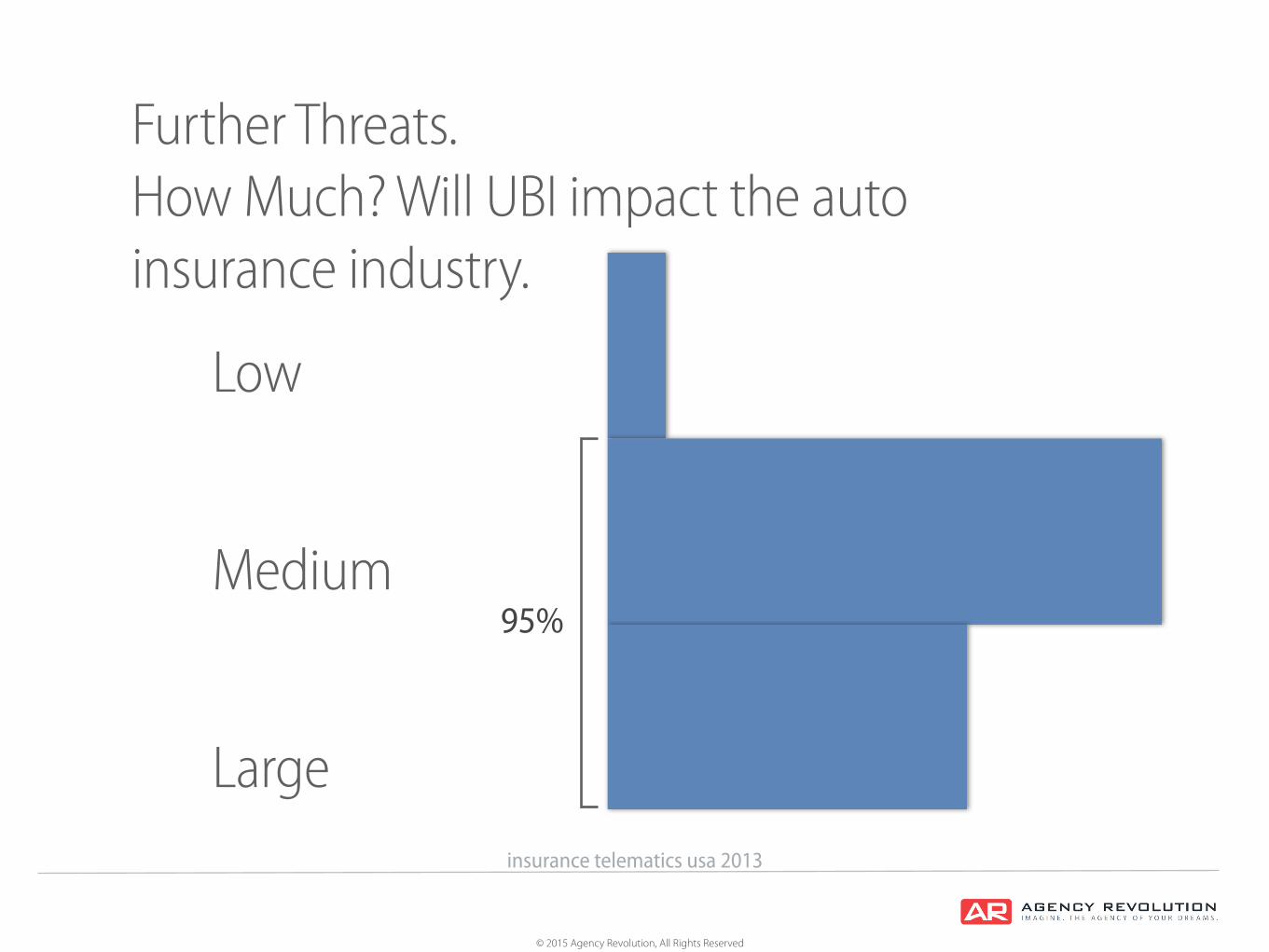

Further Threats.How Much? Will UBI impact the autoinsurance industry.

Low

Medium

Largeinsurance telematics usa 2013

95%

© 2015 Agency Revolution, All Rights Reserved

3 Predictions.

1 2 3

© 2015 Agency Revolution, All Rights Reserved

Fewer, bigger agencies.

Predictions

1

© 2015 Agency Revolution, All Rights Reserved

1

““There are 40,000 agencies in the U.S., and you could absolutely imagine them shrinking by a quarter…”

Ellen Carney

© 2015 Agency Revolution, All Rights Reserved

Top 10 P&C agencies: $3.186 billion in P&C revenue, 2011. 2013: $2.862 billion

1Insurance Journal, Top 100 Agencies Special Report

Revenue2.7 B

3.186 B

2.862 B

2011 2013

© 2015 Agency Revolution, All Rights Reserved

1

Fewer. Bigger.

Source: Phocuswright; Airline reporting corp. (ARC); ASTA.org

© 2015 Agency Revolution, All Rights Reserved

1

Fewer. Bigger.

Number of traditional travel agencies.

Air sales per location $ million.

1995

1.6

2011

5.8

2000

2.2

Source: Phocuswright; Airline reporting corp. (ARC); ASTA.org

47,000

1995

38,800

2000

14,000

2011

© 2015 Agency Revolution, All Rights Reserved

1

“Driven by performance pressures but lacking strategic vision, company after company has had no better idea than to buy up its rivals. The competitors left standing are often those that outlasted others, not companies withreal advantage.

Michael Porter

© 2015 Agency Revolution, All Rights Reserved

Continued market share erosion in P/L, Small C/L.

Predictions

2

© 2015 Agency Revolution, All Rights Reserved

Predictions

Continued vulnerability to disruption from outsiders,

smaller players or aggressive innovators willing and able

to leverage technology.

3

© 2015 Agency Revolution, All Rights Reserved

1

“Other things being equal, the larger army has the advantage whereas the winning business tends to be the one whose offerings are most preferred by customers, its size being more the consequence than the cause of its success.”

Richard Rumelt,

© 2015 Agency Revolution, All Rights Reserved

5 Point action plan for success.

1

2

34

5

© 2015 Agency Revolution, All Rights Reserved

5 Point action plan for success.

1 2 3 4 5

© 2015 Agency Revolution, All Rights Reserved

The solution:

1

“Because the purpose of business is to create a customer, the business enterprise has two and only two basic functions: marketing and innovation”.marketinginnovation

Peter Drucker

1

© 2015 Agency Revolution, All Rights Reserved

The solution:

1

marketing and innovation produce results; all the restare costs."

marketinginnovation

Peter Drucker

1

© 2015 Agency Revolution, All Rights Reserved

5 Point action plan for success. ‣ Master Marketing. ‣ Be the “Relationship Business” you always

claimed to be.

1

© 2015 Agency Revolution, All Rights Reserved

1

“The most advanced form of marketing is that which creates Meaningful Relationships”.

Michael Jans President /CEO Agency Revolution

5 Point action planfor success.

© 2015 Agency Revolution, All Rights Reserved

www.agencyrevolution.com/analyzer/

www.TheGrowthAnalyzer.com

1

© 2015 Agency Revolution, All Rights Reserved

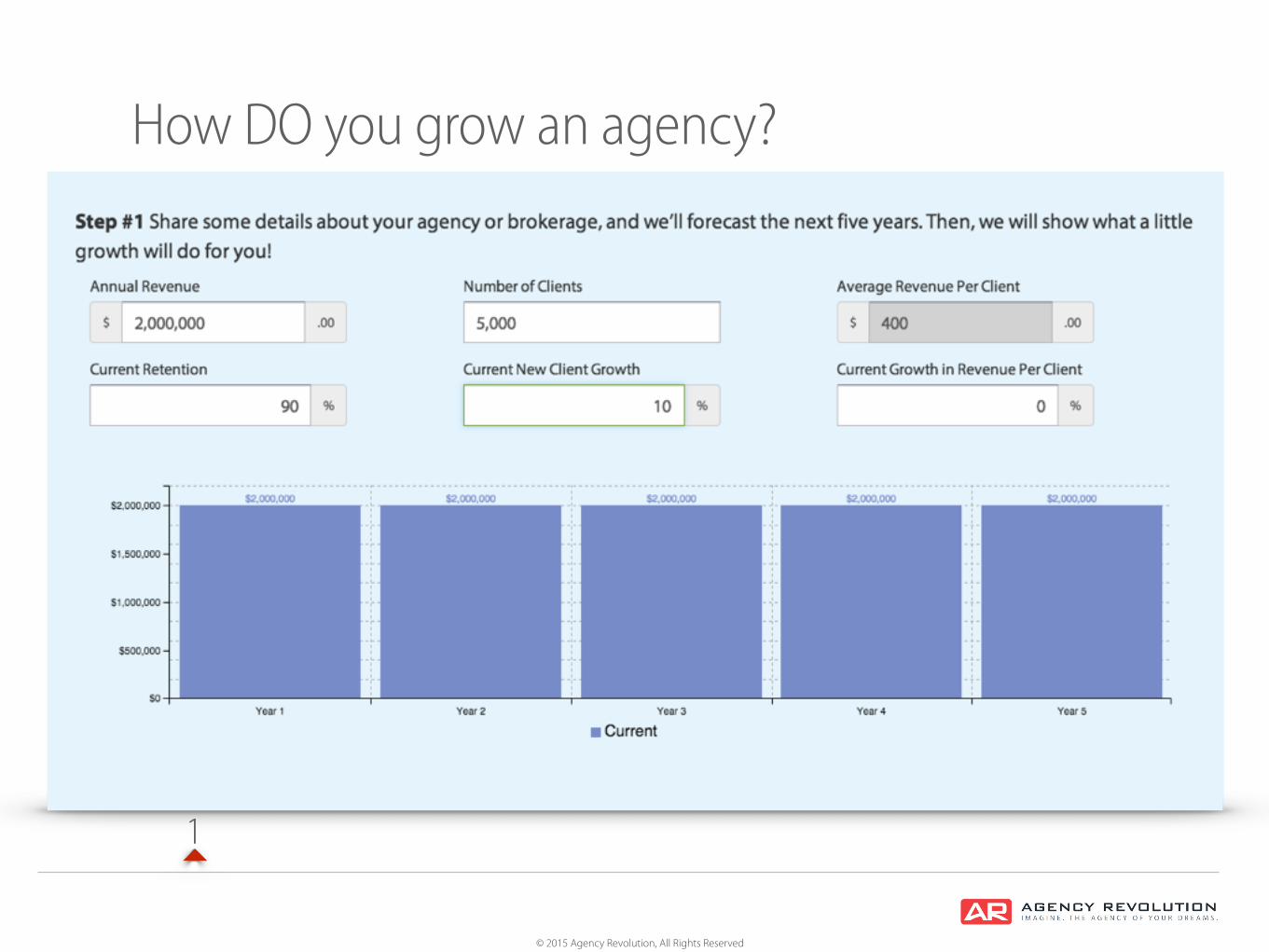

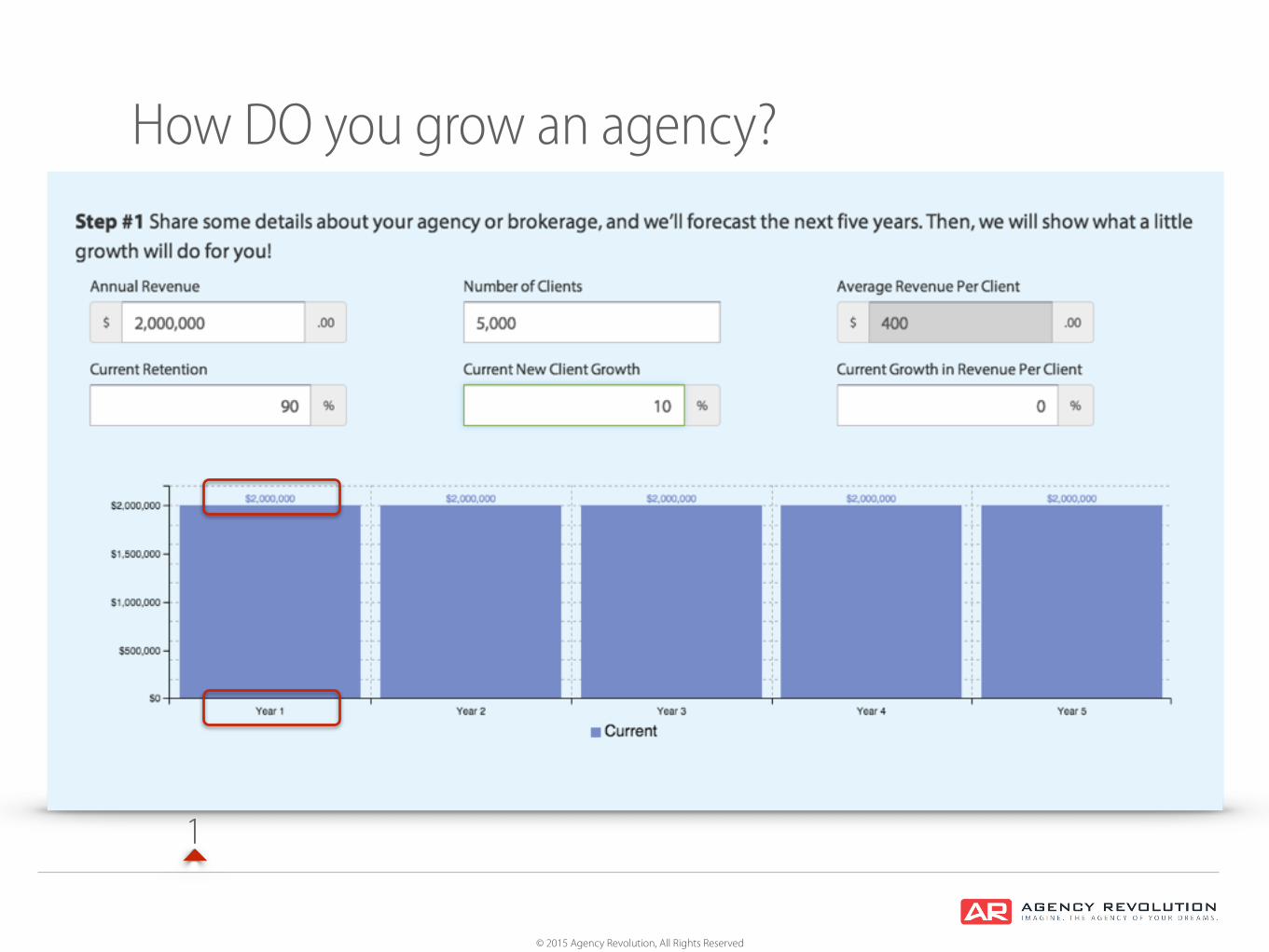

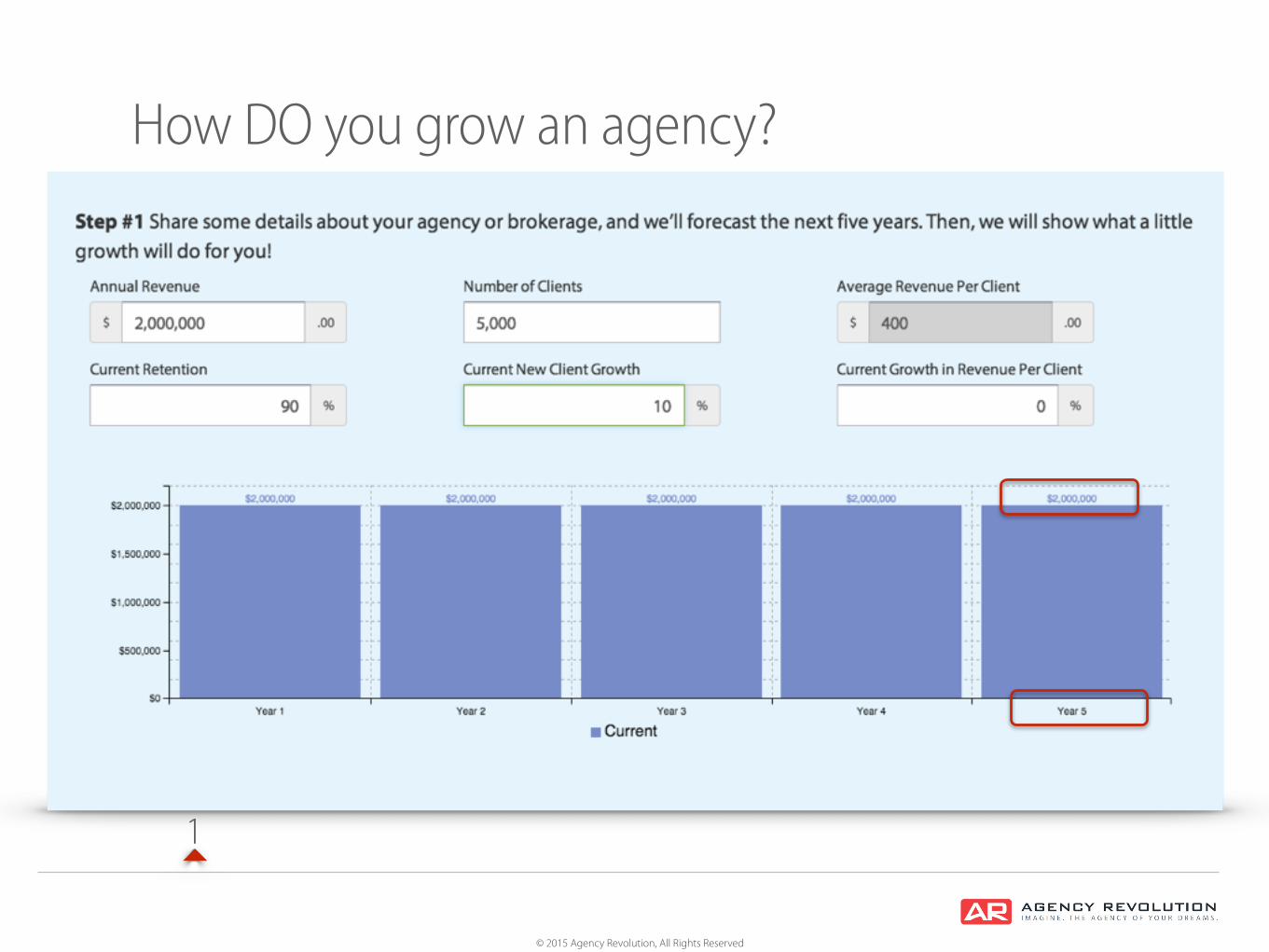

How DO you grow an agency?

1

© 2015 Agency Revolution, All Rights Reserved

How DO you grow an agency?

1

© 2015 Agency Revolution, All Rights Reserved

How DO you grow an agency?

1

© 2015 Agency Revolution, All Rights Reserved

How DO you grow an agency?

1

© 2015 Agency Revolution, All Rights Reserved

How DO you grow an agency?

1

© 2015 Agency Revolution, All Rights Reserved

How DO you grow an agency?

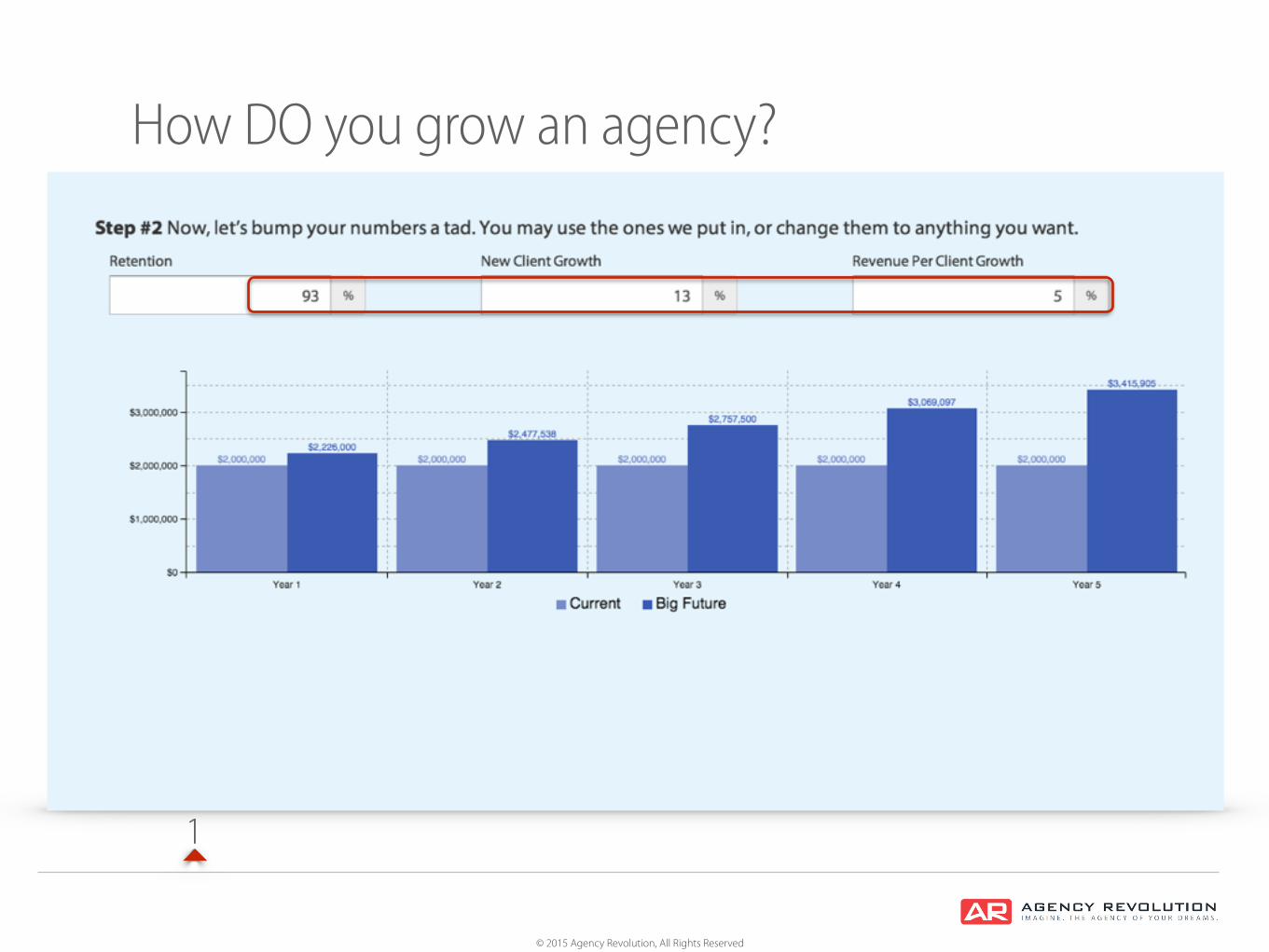

$2,226,000

1

© 2015 Agency Revolution, All Rights Reserved

How DO you grow an agency?

$2,226,000$3,415,905

1

© 2015 Agency Revolution, All Rights Reserved

How DO you grow an agency?

1

© 2015 Agency Revolution, All Rights Reserved

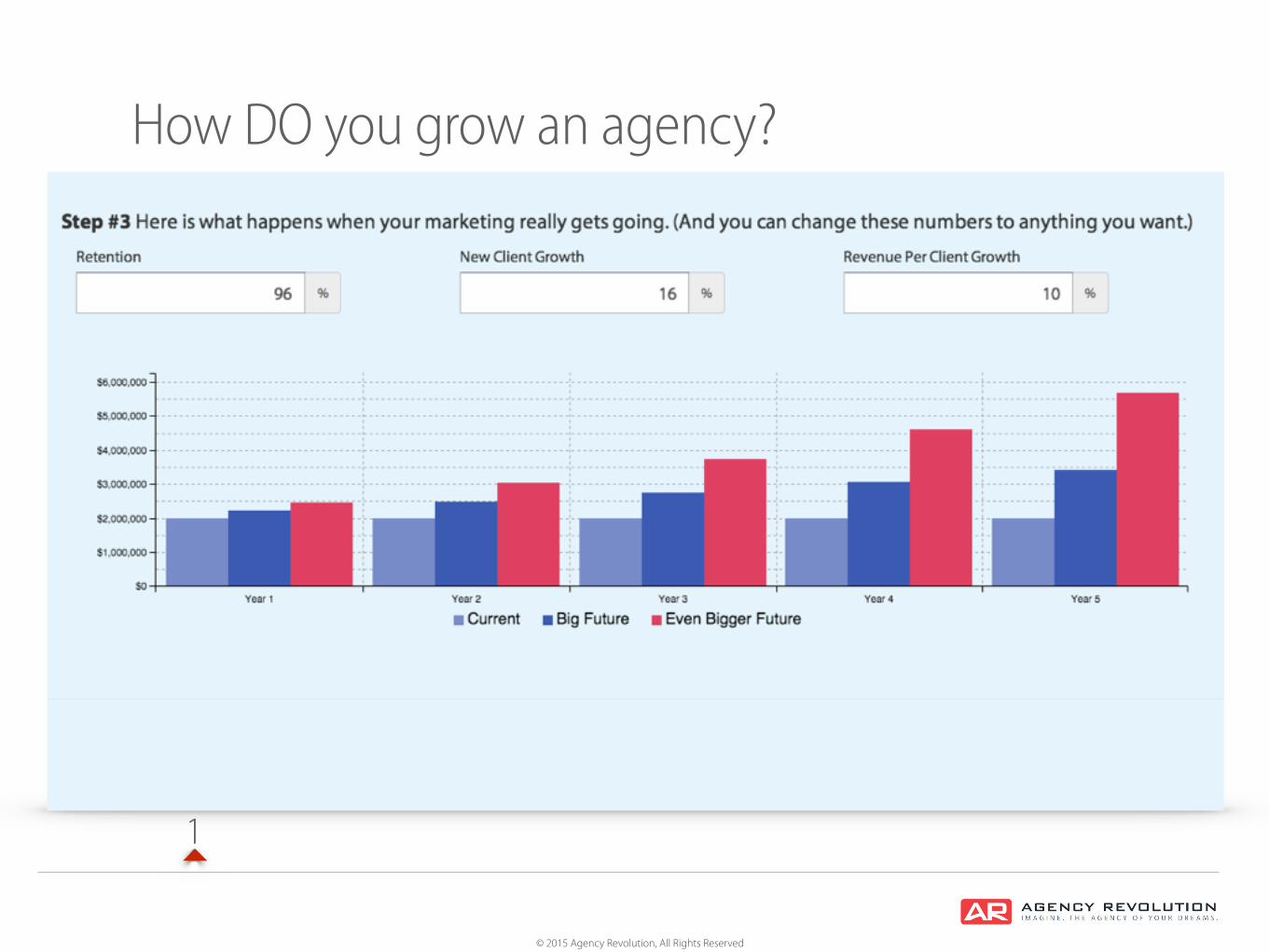

How DO you grow an agency?

$5,676,538

1

© 2015 Agency Revolution, All Rights Reserved

1

+DelightAt Every Stage in the Process

Attract Convert Optimize Retain

The ACOR+ Marketing Model

Prospects Buyers Clients PromotersLeads

C O RA

© 2015 Agency Revolution, All Rights Reserved

‣ Master Marketing & Get Bigger.

1

© 2015 Agency Revolution, All Rights Reserved

2

5 Point action plan for success. ‣ Master Innovation. ‣ Don’t Give Into The Commoditization Trap. ‣ (and don’t wait for carriers to fix that for you.)

© 2015 Agency Revolution, All Rights Reserved

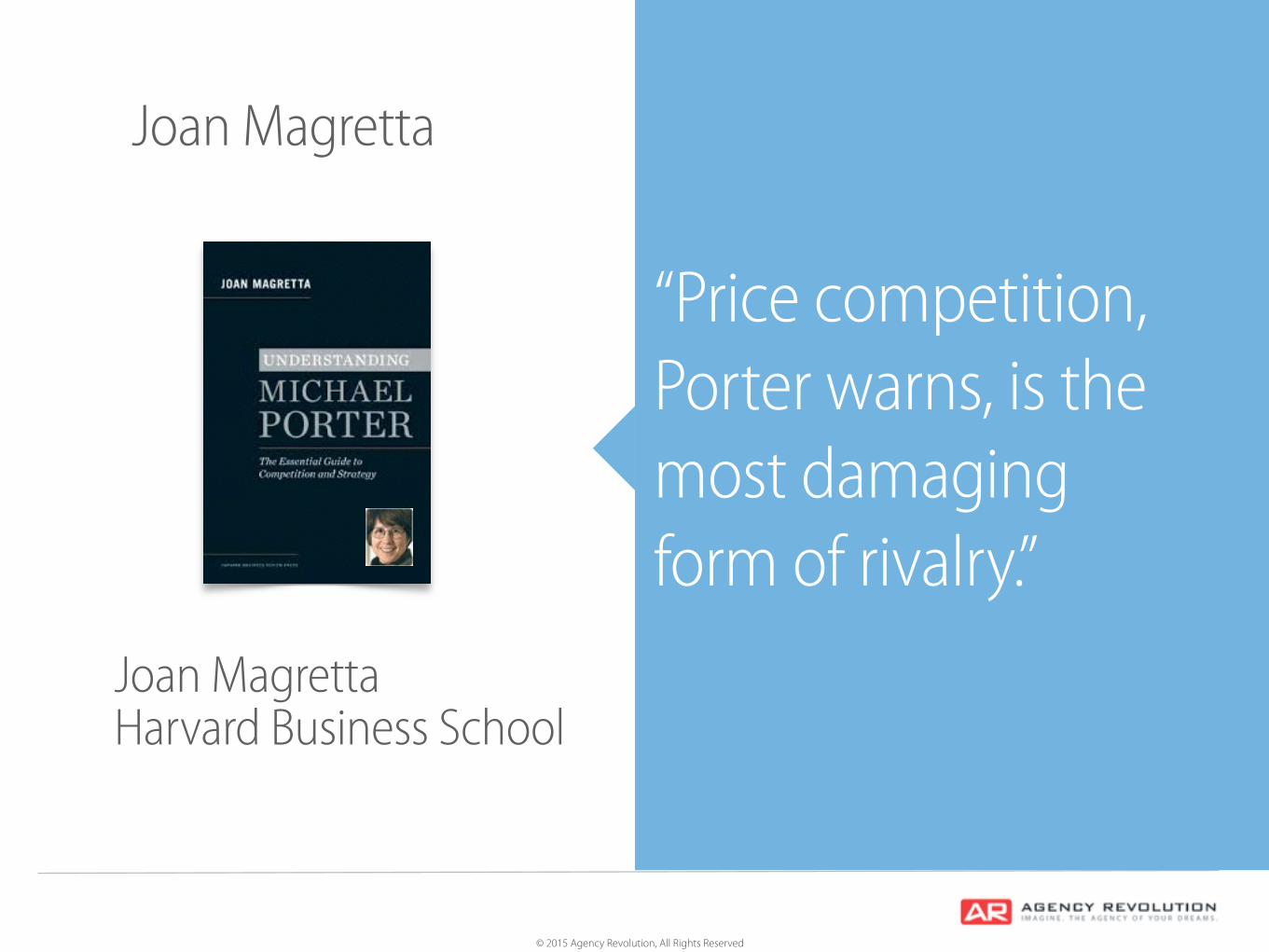

“Price competition, Porter warns, is the most damaging form of rivalry.”

Joan Magretta

Joan MagrettaHarvard Business School

© 2015 Agency Revolution, All Rights Reserved

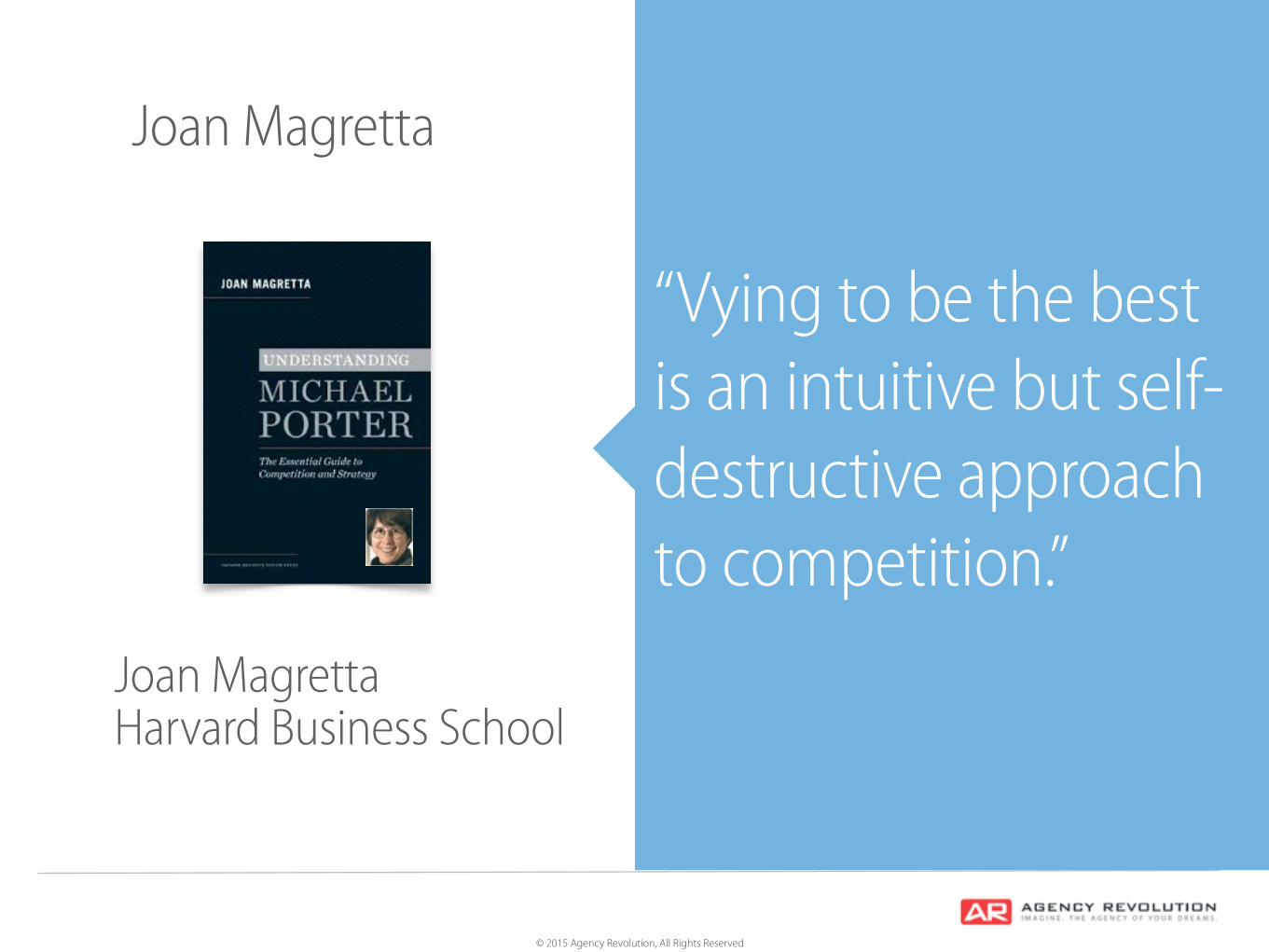

Joan Magretta

“Vying to be the best is an intuitive but self-destructive approach to competition.”

Joan MagrettaHarvard Business School

© 2015 Agency Revolution, All Rights Reserved

Joan Magretta

“Competing to be the best feeds on imitation. Competing to be unique thrives on innovation.”

Joan MagrettaHarvard Business School

© 2015 Agency Revolution, All Rights Reserved

2

Innovation demands: ‣ Stop selling on price. ‣ Beware ‘Best Practices’. ‣ Be unique.

© 2015 Agency Revolution, All Rights Reserved

second sub

Body 2

$65 billion...and growing

© 2015 Agency Revolution, All Rights Reserved

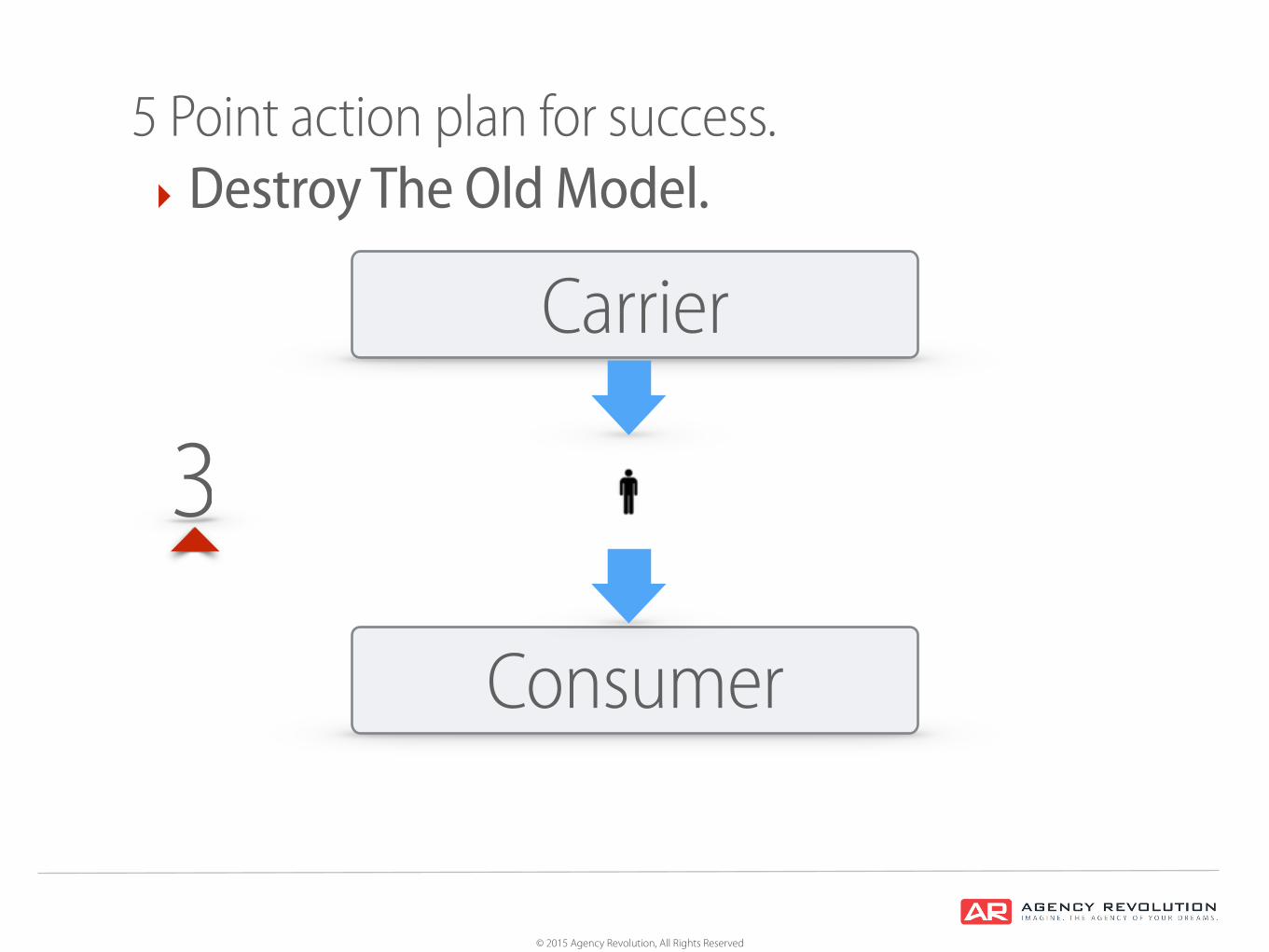

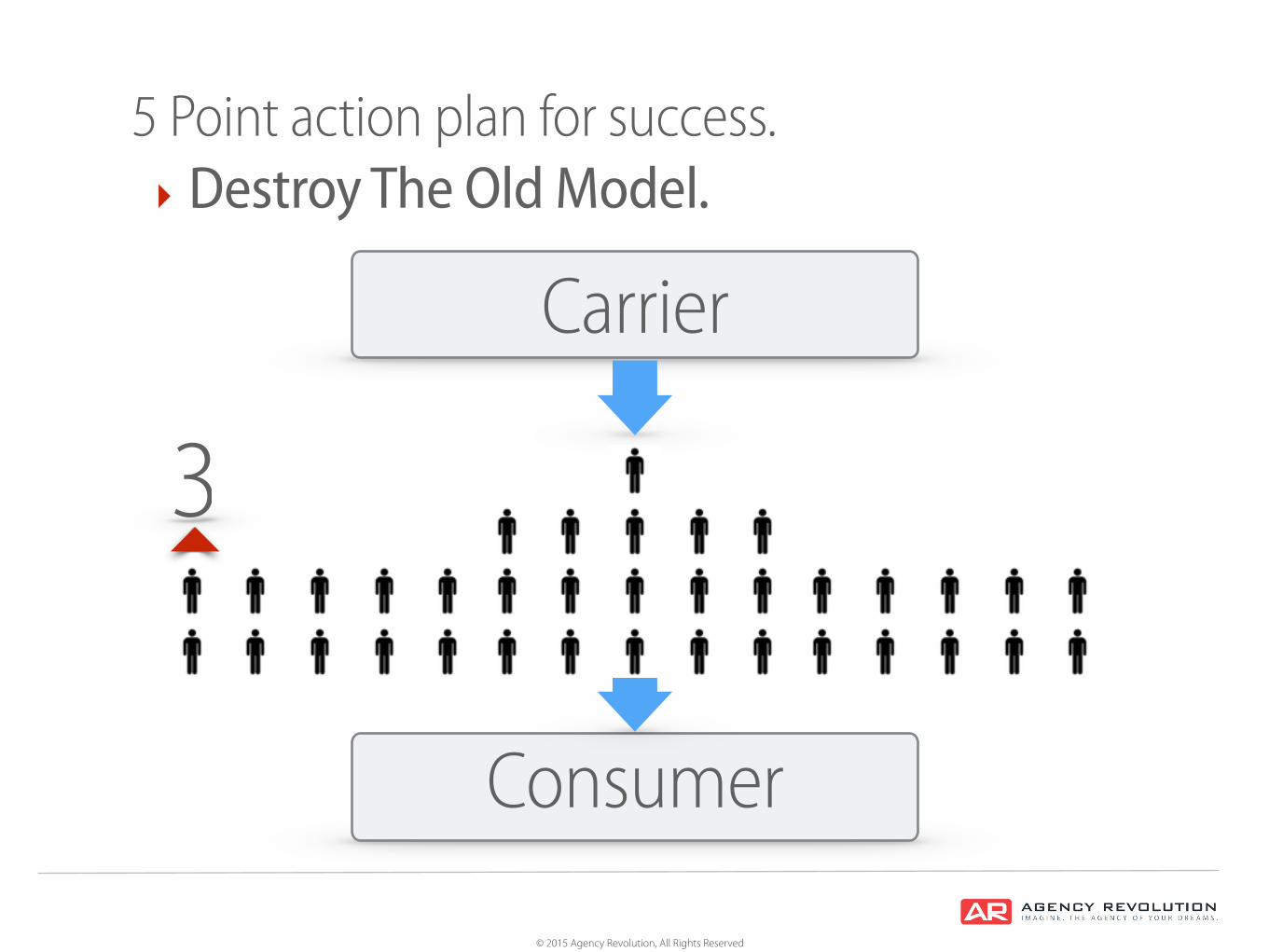

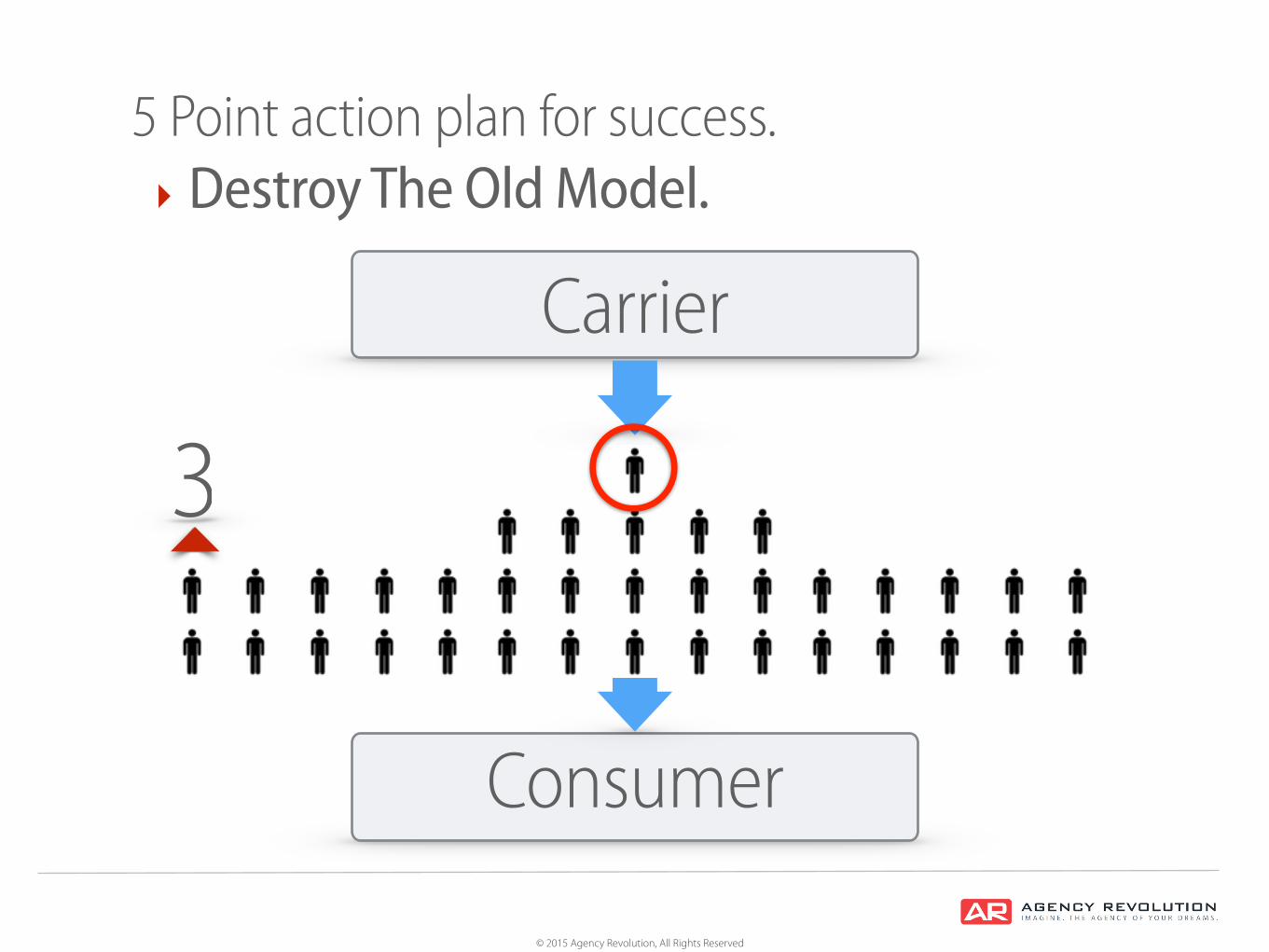

3

5 Point action plan for success. ‣ Destroy The Old Model.

Carrier

Consumer

© 2015 Agency Revolution, All Rights Reserved

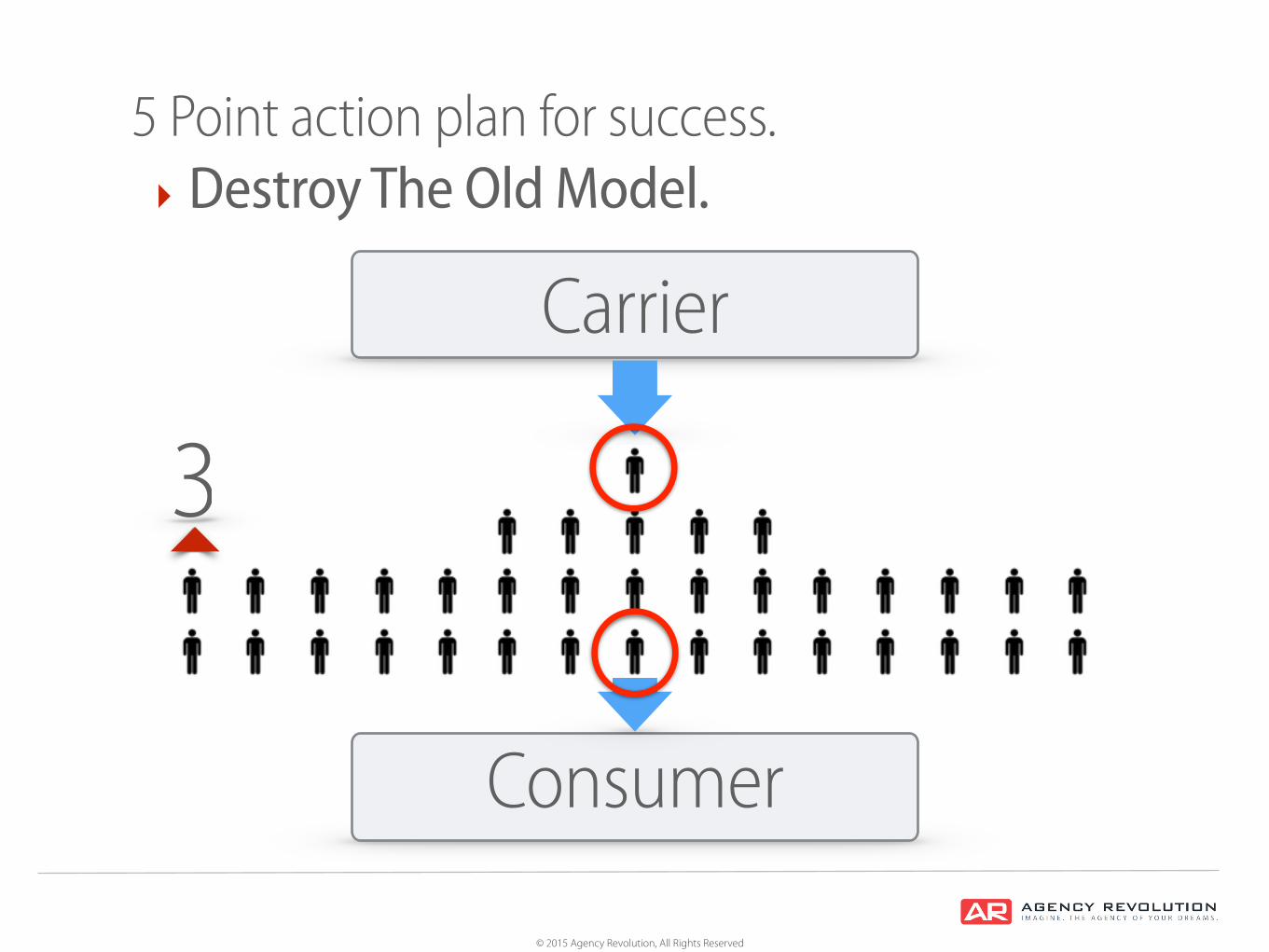

3

5 Point action plan for success. ‣ Destroy The Old Model.

Carrier

Consumer

© 2015 Agency Revolution, All Rights Reserved

3

5 Point action plan for success. ‣ Destroy The Old Model.

Carrier

Consumer

© 2015 Agency Revolution, All Rights Reserved

3

5 Point action plan for success. ‣ Destroy The Old Model.

Carrier

Consumer

© 2015 Agency Revolution, All Rights Reserved

3

5 Point action plan for success. ‣ Destroy The Old Model.

© 2015 Agency Revolution, All Rights Reserved

3Carrier

Agency

Consumer

5 Point action plan for success. ‣ Destroy The Old Model.

© 2015 Agency Revolution, All Rights Reserved

3CarrierAgency

Consumer

5 Point action plan for success. ‣ Destroy The Old Model.

© 2015 Agency Revolution, All Rights Reserved

4

5 Point action plan for success. ‣ Launch A New Academy of

Insurance Leadership.

© 2015 Agency Revolution, All Rights Reserved

4

5 Point action plan for success. ‣ For insura-preneurs. ‣ That teaches non-insurance business leadership. ‣ With fully credentialed certification.

© 2015 Agency Revolution, All Rights Reserved

4

5 Point action plan for success. ‣ Curriculum. ‣ Marketing ‣ Innovation ‣ Leadership ‣ Strategy ‣ Thought leadership ‣ Customer experience design

© 2015 Agency Revolution, All Rights Reserved

5

5 Point action plan for success. ‣ Urgent: Leverage Modern Technology. ‣ Modern Technology Attracts Younger Workers. ‣ Because it's what consumers want us to do

© 2013 Agency Revolution, All Rights Reserved

What Makes Consumers Happy? Channel usage, agent serviced customers.

© 2013 Agency Revolution, All Rights Reserved

What Makes Consumers Happy? Channel usage, agent serviced customers.

Ove

rall

satis

fact

ion

inde

x.

Agent + emerging

852

822

Boomer

Gen Y

774

743No interaction

797

822

Agent only

830

814

Agent + traditional

810

795

Non-agent only

© 2015 Agency Revolution, All Rights Reserved

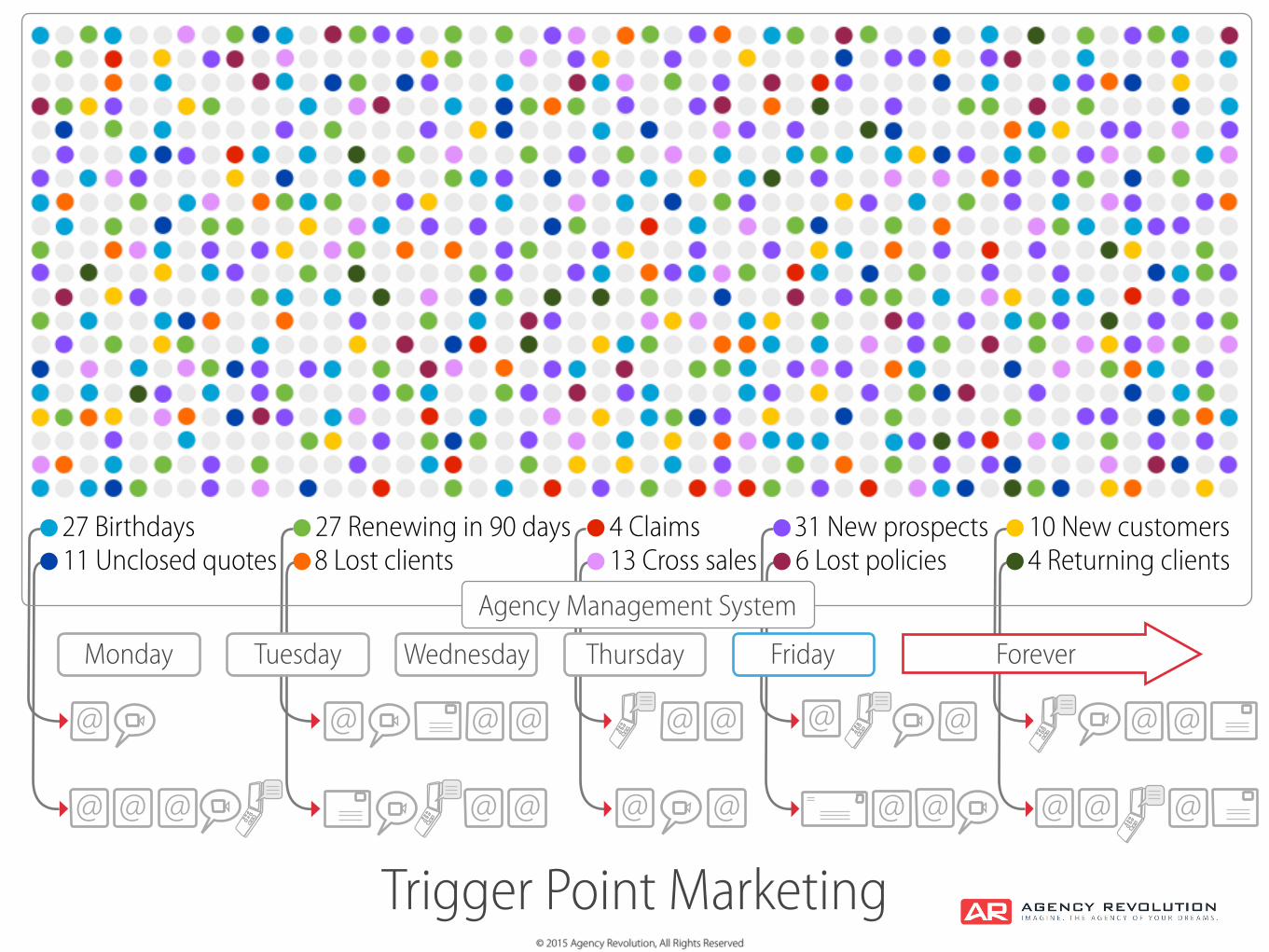

4 Claims27 Birthdays 27 Renewing in 90 days 31 New prospects 10 New customers

Monday

4 Returning clients8 Lost clients 13 Cross sales 6 Lost policies

Trigger Point Marketing

11 Unclosed quotes

© 2015 Agency Revolution, All Rights Reserved

Agency Management System

© 2015 Agency Revolution, All Rights Reserved

4 Claims27 Birthdays 27 Renewing in 90 days 31 New prospects 10 New customers

@

@ @

@ @ @ @@ @ @

@ @ @ @ @ @ @

@ @

@ @@

Monday

4 Returning clients8 Lost clients 13 Cross sales 6 Lost policies

Trigger Point Marketing

11 Unclosed quotes

Tuesday Wednesday Thursday Friday Forever

© 2015 Agency Revolution, All Rights Reserved

Agency Management System

© 2015 Agency Revolution, All Rights Reserved

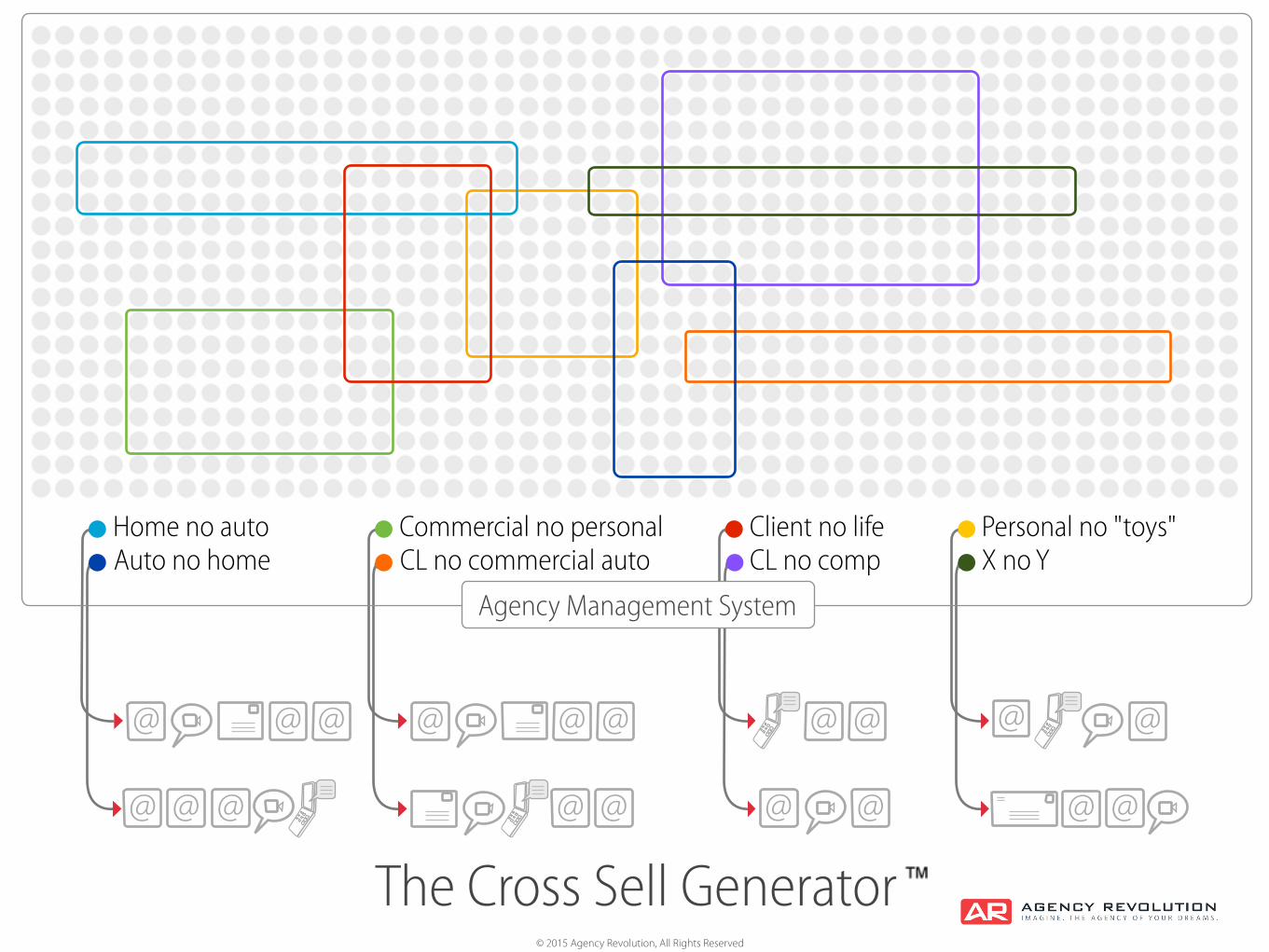

The Cross Sell Generator

Agency Management System

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

@ @

@ @ @ @@ @ @

@ @ @ @@ @@

The Cross Sell Generator

Client no lifeX no Y

Home no auto Commercial no personalCL no comp

Personal no "toys"CL no commercial autoAuto no home

@ @ @

Agency Management System

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved

"If all we’re doing is defending the status quo, the game is over"

© 2015 Agency Revolution, All Rights Reserved

© 2015 Agency Revolution, All Rights Reserved