2016.05 - apresentação institucional ingri.gerdau.com/enu/6989/2016.05 - apresentao institucional...

TRANSCRIPT

Investor Presentation

Heavy plate rolling mill starts operating in July at the Ouro Branco mill (MG)

Outlook

Gerdau Highlights

Agenda

2

Economic outlook

3

Sources: IMF and Focus

GDP Growth 2014 2015f 2016f

World 3.4% 3.1% 3.2%

US 2.4% 2.4% 2.4%

Brazil 0.1% -3.8% -3.8%

China 7.3% 6.9% 6.5%

Global steel demand is expected to decrease in 2016

4

Source: World Steel Association

Region / Country (in mmt and %)

2015 2016f 15/14 16/15

World 1,500 1,488 -3.0% -0.8%

European Union 153 155 2.8% 1.4%

NAFTA 135 139 -8.4% 3.2%

Central & South America 45 43 -7.3% -6.0%

Brazil 21 19 -16.7% -8.8%

Asia and Oceania 985 969 -3.3% -1.7%

China 672 645 -5.4% -4.0%

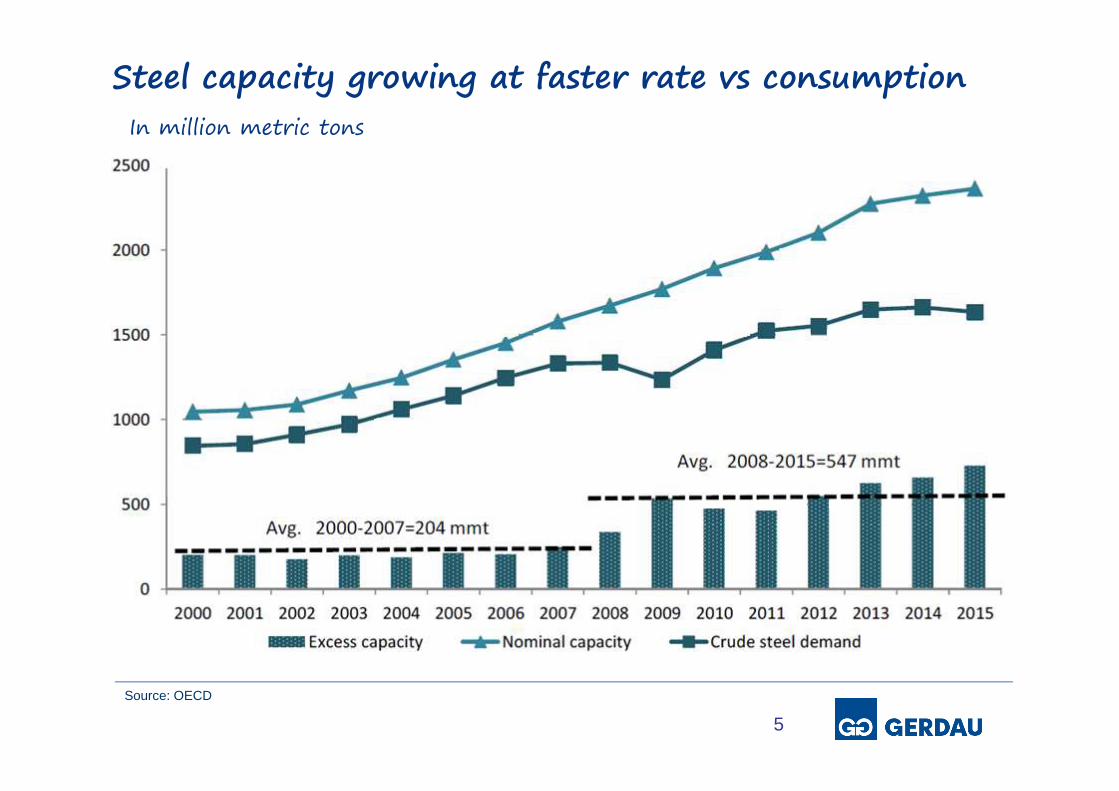

Steel capacity growing at faster rate vs consumption

5

Source: OECD

In million metric tons

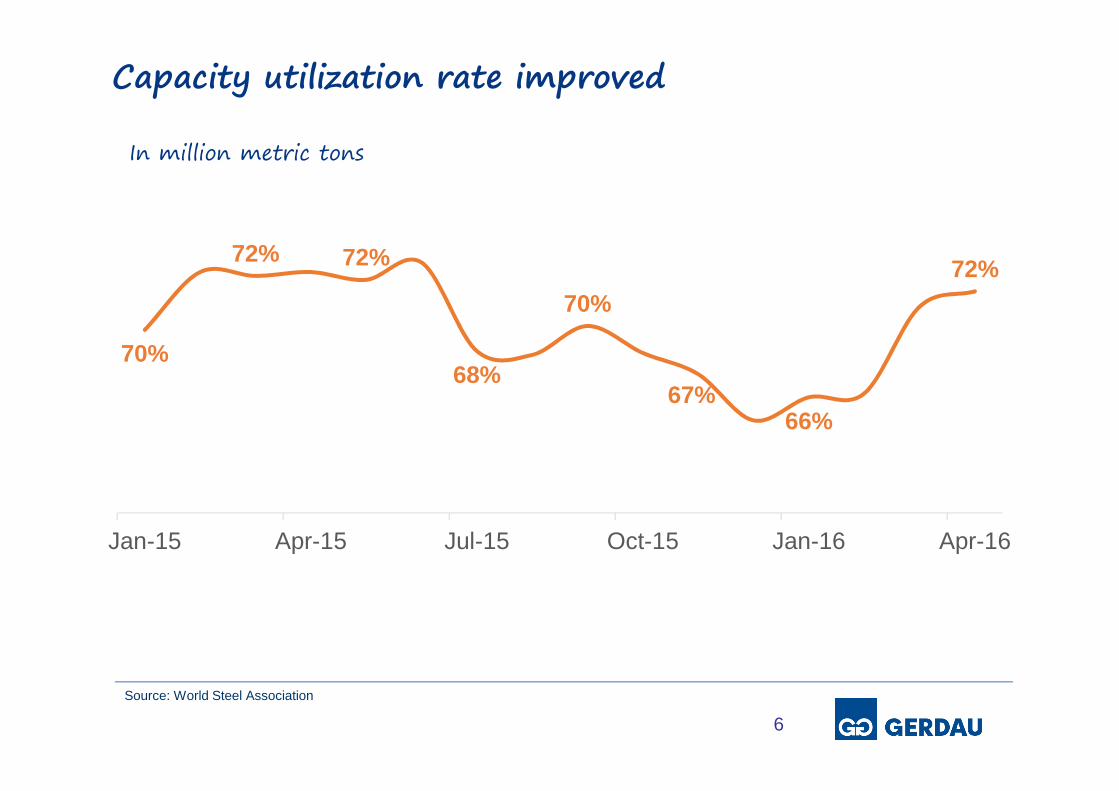

Capacity utilization rate improved

6

Source: World Steel Association

In million metric tons

70%

72% 72%

68%

70%

67%66%

72%

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16

Chinese steel exports are affecting steel industry

7

In million metric tons

Source: World Steel Association

*annualized from 1Q16

62

93

112 111

2013 2014 2015 2016 pace*

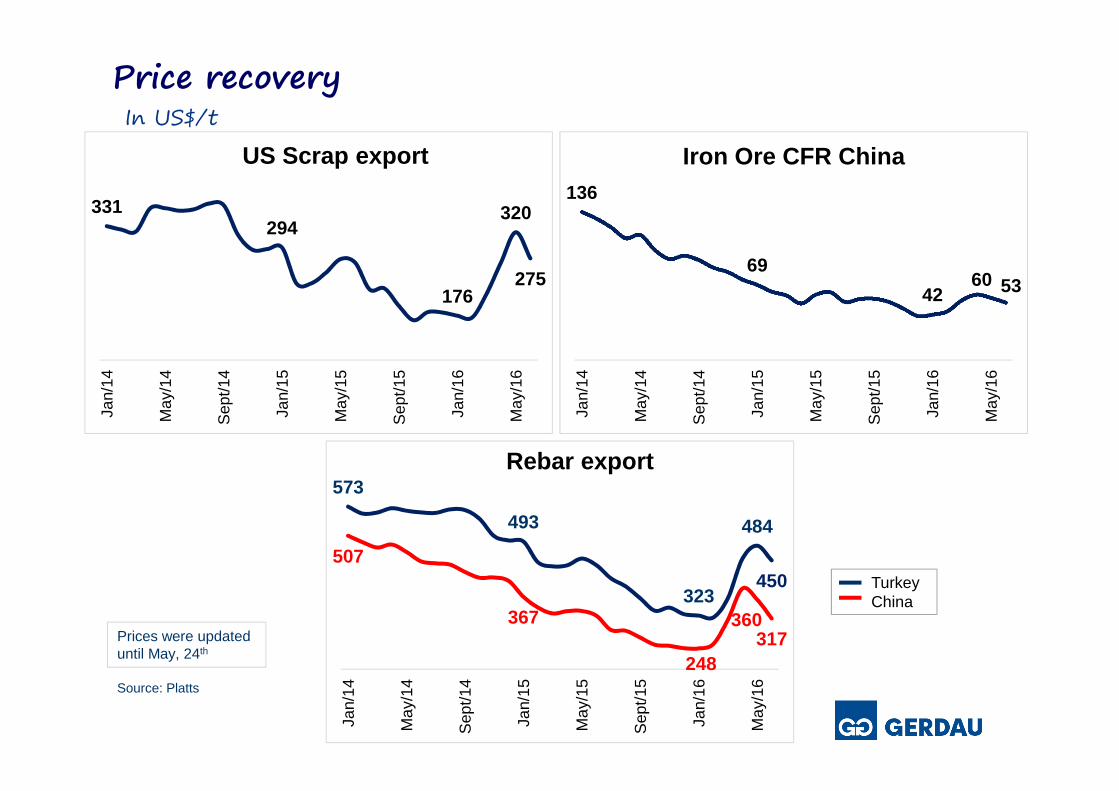

Price recovery

8

In US$/t

TurkeyChina

Source: Platts

Prices were updated until May, 24th

331294

176

320

275

Jan/

14

May

/14

Sep

t/14

Jan/

15

May

/15

Sep

t/15

Jan/

16

May

/16

US Scrap export

507

367

248

360317

573

493

323

484

450

Jan/

14

May

/14

Sep

t/14

Jan/

15

May

/15

Sep

t/15

Jan/

16

May

/16

Rebar export

136

69

4260 53

Jan/

14

May

/14

Sep

t/14

Jan/

15

May

/15

Sep

t/15

Jan/

16

May

/16

Iron Ore CFR China

Outlook

Gerdau Highlights

Agenda

9

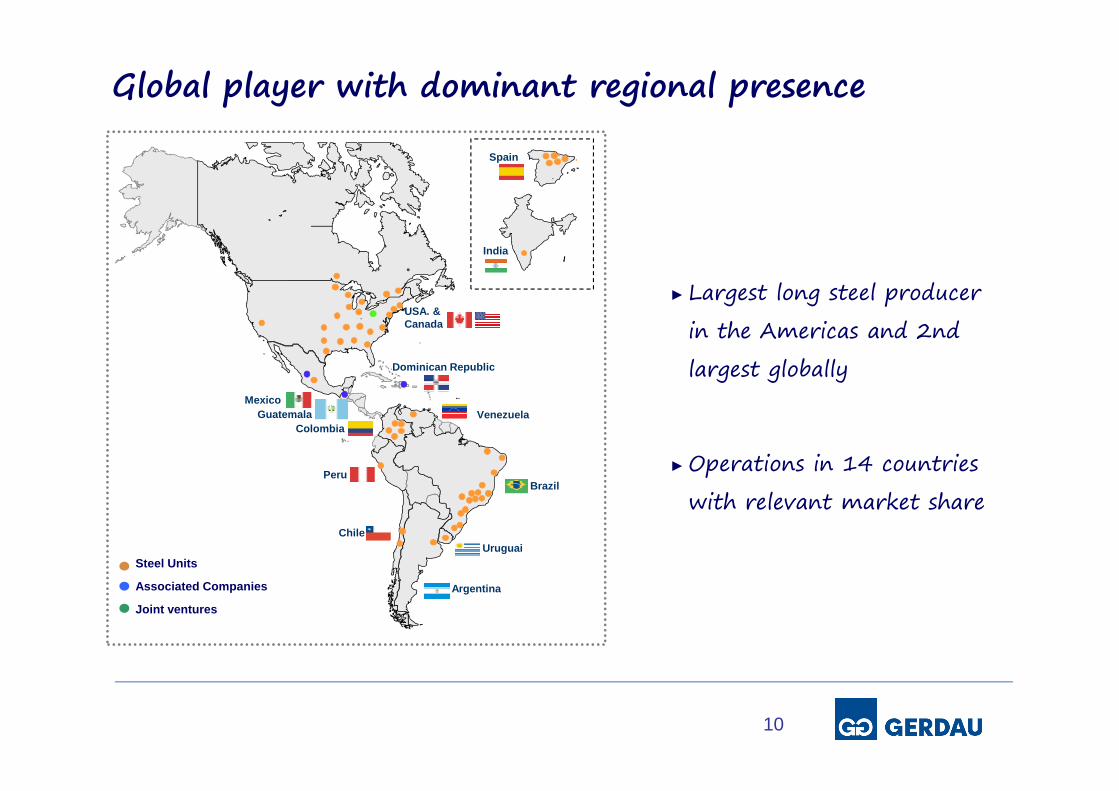

Global player with dominant regional presence

10

Steel Units

Associated Companies

Joint ventures

USA. & Canada

Mexico

Colombia

Peru

ChileUruguai

Argentina

Brazil

Dominican Republic

Venezuela

India

Spain

Guatemala

► Largest long steel producer

in the Americas and 2nd

largest globally

►Operations in 14 countries

with relevant market share

►Relevant level of direct

purchase and captive

scrap (50%)

►6.3 billion tons of iron

ore resources

– Self-sufficiency at

Ouro Branco mill

►Coke unit and coking

coal mines in Colombia

►Partial level of energy

self generation

Upstream

Vertically integrated operations

► Low cost structure

►Mini-mills and

integrated mills key to

low cost strategy

► Latest generation

technology

Steel

►Reinforcing steel

fabrication facilities (Fab

Shops)

►Drawn products

►Multi-product

distribution network

► Tailor-made added-

value approach (~40%

of sales to civil

construction)

Downstream

11

Brazil North America Special Steel

Ready-to-use products

► Housing

► Infrastructure

► Industrial and commercial buildings

► Agriculture

► Exports

► Infrastructure

► Non-residential

► Industrial

► Automotive

► Shipbuilding

► Energy

Billets, blooms& slabs

Merchant bars Rebars

Fabricated steel

Heavystructural shapes Wire-rod

Wires

NailsSBQ

South America

► Housing

► Infrastructure

► Industrial and commercial buildings

Broad product portfolio and geographic diversification

HRC Iron Ore

12

Wire

28% of Net Sales

31% of EBITDA

40% of Net Sales

38% of EBITDA

12% of Net Sales

14% of EBITDA

20% of Net Sales

17% of EBITDA

*Net sales and EBITDA in the last 12 months

Focus in adding value to our products

13

Technical Assistance Agreement

For the production of high-quality steel plates to be supplied to the Americas and to the World

• Technical support to optimize Gerdau’s Plate Mill learning curve• High level supervision and training for our Steelmaking and Plate Mill

teams• Short cut to high-tech steel plates (includes development of new products

with JFE’s know-how, e.g. API X80 grade steel plates)

Main Benefits for

Gerdau

To support our State-of-the-Art Plate Mill facility at Ouro Branco Works (Brazil)

Capacity 1.1 mt/yearStart-up: July 2016

Digital Mill Araçariguama (SP)

Plate milEarlier entrance: July

Gerdau among the best companies in Brazil in

leadership development!

Strategic RoadmapNew partnerships in wind power market

18 ideas implemented for 2 challenges addressed:

Processes simplification and Working capital reduction

The Gerdau we are creating

Transforming Gerdau to achieve our goals and share our success:

check out these great examples!

Gerdau Lean Delivery Systems in Special Steel

in North AmericaQuicker deliveries with optimized

logistic costs.

IT as a collaborative partner in North America BDTablets in the scrap yard, GoPro cameras for maintenance production, iPhone thermography capability

Gerdau Agile DayThink big. Start small.Deliver results in a valuable and simple way.

Gerdau is 4th - World-Class Steelmaker Ranking

7.97.6

7.57.3

7.37.2

7.17.1

7.17.0

7.07.0

7.07.0

6.96.96.9

6.96.9

6.96.86.86.8

6.7

POSCONucor

Nippon SumitomoGerdau

SeverstalJSW Steel

NLMKJFE

HyundaiErdemir

CSNSDI

SAILVoestalpine

Tata SteelHadded

JindalArcelorMittalChina Steel

EvrazBaosteelFinarvedi

MMKTernium

23 factors analyzed, including:

• Profitability

• Value-added product mix

• Cost-cutting efforts

• Pricing power in home market

• Threat from nearby competitors

• Size

• Downstream business

• M&A, alliances and JV’s

• …

15

Source: World Steel Dynamics

Financial highlights

16

G&A expenses declined 10% in 1Q16 compared to 1Q15

Unit 1Q16 1Q15 ∆% 4Q15 ∆%

Shipments '000 ton 3,851 4,143 -7.0% 3,887 -0.9%

Net Sales R$ million 10,085 10,447 -3.5% 10,449 -3.5%

Cost of Goods Sold R$ million (9,272) (9,335) -0.7% (9,662) -4.0%

SG&A R$ million (644) (660) -2.4% (655) -1.7%

EBITDA R$ million 930 1,106 -15.9% 911 2.1%

EBITDA Margin % 9.2% 10.6% 8.7%

Net Income R$ million 14 267 -94.8% (41)*

Free Cash Flow R$ million 11 (502) 1,225 -99.1%

* In the 4Q15, the net income was adjusted by extraordinary events

EBITDA and EBITDA margin per BD

17

Geographic diversification reduces volatility

EBITDA (R$ million) EBITDA Margin (%) Participation of adjusted EBITDA per BD

30.9%

Brazil BD

521

186 248

15.7%

6.9%9.2%

1Q15 4Q15 1Q16

38.4%

NorthAmerica BD

254396 355

6.6%9.2% 8.3%

1Q15 4Q15 1Q16

13.7%

SouthAmerica BD

127206 183

9.6%13.9% 14.8%

1Q15 4Q15 1Q16

17.0%

Special Steel BD

260151 174

11.6%

6.9% 8.0%

1Q15 4Q15 1Q16

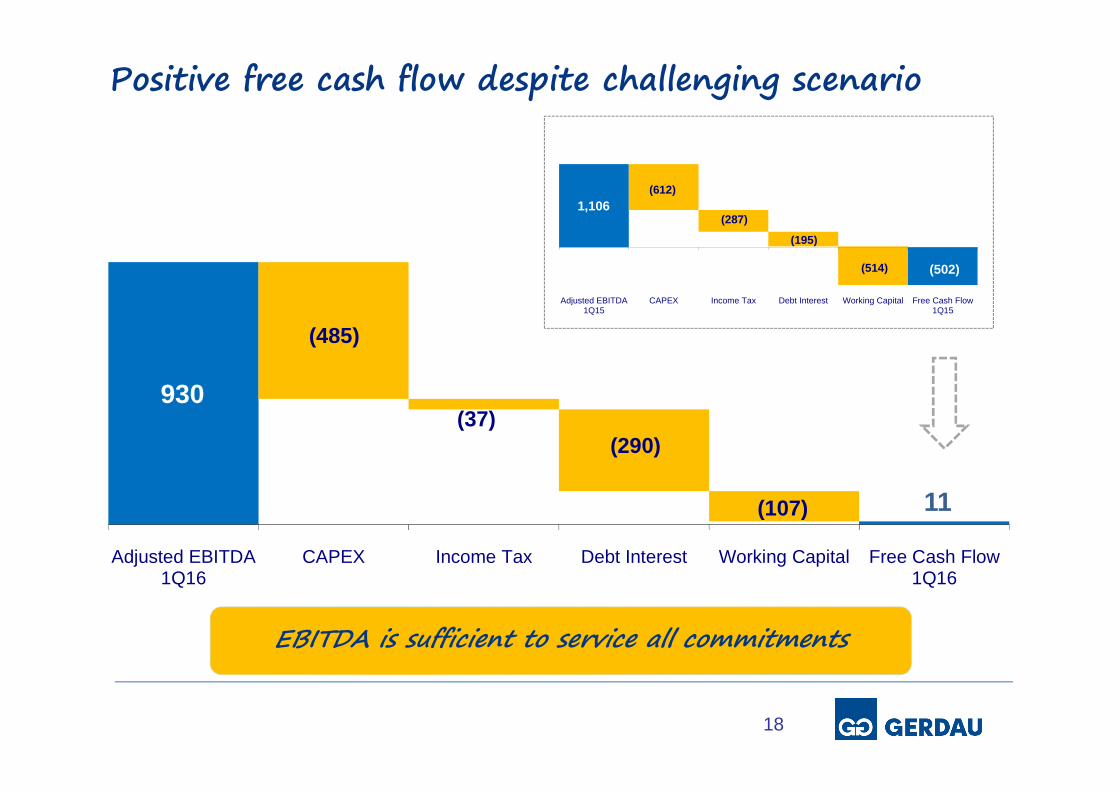

Positive free cash flow despite challenging scenario

EBITDA is sufficient to service all commitments

18

930

11

(37)(290)

(107)

Adjusted EBITDA1Q16

CAPEX Income Tax Debt Interest Working Capital Free Cash Flow1Q16

(485)

1,106

(502)

(287)

(195)

(514)

Adjusted EBITDA1Q15

CAPEX Income Tax Debt Interest Working Capital Free Cash Flow1Q15

(612)

35% CAPEX reduction in 2016

Main projects

� Construction of heavy plate rolling mill at Ouro Branco Unit in Brazil

� Construction of new melt shop in Argentina

3.1

2.6

2.3 2.3

1.5

2012 2013 2014 2015 2016 (F)

CAPEX Disbursements (R$ billion)

-35%

19

1Q16:

R$ 485

million

Indebtedness under control

20

EBITDA in the last 12 months

Average Debt Term: 6.3 years

R$ billion

Debt & Leverage Ratio

Average Debt Cost: 7.1%

Gross debt declined by R$ 2.8 billion; R$ 1.9 billion due to FX effect and R$ 0.9 billion to amortizations

4.0

1.2 0.9

3.5

4.1

0.2

2.3

3.2

1.8

2017 2018 2019 2020 2021 2022 2023 2024 2025andafter

R$ billion

Long-Term Debt Amortization Schedule

21

Closing Remarks� Strong presence in North America and management efforts in all operations

supported a 21% decrease in working capital in 1Q16 compared to 1Q15,

resulting in positive free cash flow.

� Improvement in consolidated EBITDA compared to 4Q15.

� Compared to 1Q15, EBITDA grew in both North America BD (+40%) and

South America BD (+44%).

� Gerdau's 1Q16 performance does not indicate the full year period trend.

� Recovery in international commodity prices.

� Focus on generating free cash flow and reducing financial leverage in 2016:

� Costs and SG&A reduction;

� CAPEX restriction (-35% in comparison with 2015).

22

Closing Remarks

� Gerdau continues to undergo a transformation process: creating

more value and strengthening the competitiveness of its operations.

� Long-term initiatives:

� Streamlining operations and internal structures;

� Modernizing the corporate culture; and

� Reassessing the potential profitability.

This presentation may contain forward-looking statements. These forward-looking

statements rely upon estimates, information or methods that may be incorrect or

inaccurate and may not actually occur. These estimates are also subject to risks,

uncertainties and assumptions, including, among others: general economic, political

and commercial conditions in Brazil and in the markets where we operate and existing

and future government regulations. Potential investors are hereby informed that these

estimates do not constitute a guarantee of future performance as they involve risks and

uncertainties. The Company does not undertake, and specifically denies, any obligation

to update any estimate, which only speak as of the date they are made.

Statement

23