2020 msrs pre-retirement seminar

TRANSCRIPT

2020 MSRS Pre-Retirement Seminar

State Employee Pension Plans

Health Care Savings Plan

(HCSP)

Deferred Compensation Plan

(MNDCP)

Minnesota State Retirement System

Who we are

Seminar topics

Readiness

Pension

Social Security

Income Gap

MNDCP

HCSP

YOURRETIREMENT

Click to edit Master title style What do you imagine

for your retirement?

•Travel

•Hobbies

•Enjoying time with friends & family

•Volunteering

•Starting your own business

Sky’s the limit

Stages of RetirementEach stage has its own characteristics and costs

EARLY YEARS MIDDLE YEARS LATER YEARS

Click to edit Master title style Consider the realitiesBe Prepared

•High cost of health care

High cost of health care

For a 50% chance of covering

For a 90% chance of covering

$79,000 $144,000

$104,000 $163,000

$183,000 $301,000

Amount needed to cover health care costs in retirement

Source: Employee Benefit Research Institute Issue Brief, May 16, 2019 Excludes long-term care*For a couple with median prescription drug expenses

FOR ILLUSTRATIVE PURPOSES ONLY

65-year-old couple*

65-year-old woman

65-year-old man

Click to edit Master title style Consider the realitiesBe Prepared

•High cost of health care

•We’re living longer

Life expectancy – we’re living longer

Source: Society of Actuaries RP-2014 Mortality Table projected with Mortality Improvement Scale MP-2014 as of 2015*At least one surviving individual.

FOR ILLUSTRATIVE PURPOSES ONLY

50% Chance Age 87 Age 90 Age 94

25% Chance Age 93 Age 96 Age 98

65-year-old couple*65-year-old woman65-year-old man

Click to edit Master title style Consider the realities

•High cost of health care

•We’re living longer

•Inflation

Be Prepared

Inflation – what money will buy

$2.53

$3.21

$1.84

$3.80

$0.09

$0.14

27%increase

106%increase55%

increase

The effect of inflation over 20 years

Source: U.S. Bureau of Labor Statistics, Consumer Price Index, Average Price Data (9/1997 – 9/2017)

1997 2017

Milk(per gallon)

1997 2017

Electricity(per KWH)

1997 2017

Lean ground beef(per lb)

FOR ILLUSTRATIVE PURPOSES ONLY

Click to edit Master title style Consider the realities

•High cost of health care

•We’re living longer

• Inflation

•Market volatility

Be Prepared

600.00

900.00

1200.00

1500.00

1800.00

2100.00

2400.00

2700.00

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Expect stock market volatility

FOR ILLUSTRATIVE PURPOSES ONLY Past performance is not a guarantee or prediction of future results. You cannot invest directly in a benchmark index. The S&P 500 ® Index measures the performance of the domestic large-cap equity market and is used as a proxy of the stock market in general. The S&P 500 ® is a registered trademark of Standard & Poor’s Financial Services LLC.Source: CBOE ®, Chicago Board Options Exchange ® Data from 1/1/1998 – 1/1/2018 www.cboe.com/products/stock-index-options-spx-rut-msci-ftse/s-p-500-index-options/s-p-500-index/spx-historical-data

Market volatility over the past 20 yearsS&P 500® Index –monthly returns

Mortgage meltdownDot-com

bubble collapse

Keep perspectiveIt has paid to stay invested in U.S. stocks during troubled times

May 1932 July 1982 March 2009Great Severe Mortgage

Depression recession meltdown

Subsequent 5-year return

FOR ILLUSTRATIVE PURPOSES ONLY Past performance is not a guarantee or prediction of future results. You cannot invest directly in a benchmark index. U.S. stock market returns represented by total return of S&P 500®, which is an index used as a proxy for the stock market in general.Source: Fidelity Investments. https://institutional.fidelity.com/app/item/RD_13569_23965.html With data provided by Ibbotson, Factset, FMR Co., Fidelity Asset Allocation Research Team (AART) as of 3/31/2015.

Prepare your retirement budget

Review your financial situation to determine:

• all your sources of retirement income

• how your expenses will differ in retirement

How much will you need to maintain your standard of living?

Be Prepared

Take into account all of your assets, including:

• Projected Social Security benefit

• Projected Pension benefit

• Money saved in retirement plan accounts MNDCP 457(b) plan, 403(b) plan, 401(k) plan, IRAs

• Money saved in Health Savings Plans HCSP, HRA, HSA, VEBA

• Spouse’s retirement plan accounts

At Different

Ages

Consider your income

Consider your expenses

Retirement expenses may decrease• Housing • Payroll taxes (e.g., FICA)• Transportation• Retirement plan contributions

Retirement expenses may increase

• Health Care

• Travel

1 Includes cash contributions, alcohol, tobacco, personal care products and services, reading, education, life and personal insurance, and miscellaneous expensesSource: U.S. Bureau of Labor Statistics, Consumer Expenditures in 2015 Report 1066, April 2017

Median consumer expenses

Housing33.3%

Food12.6%

Health Care11.6%

Clothing2.7%

Ages 65-74

Other1

10.9%

Transportation16.2%

•Higher health care costs

•Increasing life expectancies

•Inflation

•Stock market volatility

Take action

Prepare a retirement budget

Consider how the following factors could affect your retirement savings

Service Credit

Benefit Multiplier

High-5Salary

Possible Reduction

Pension benefit factors

• Every month that deductions from pay are taken

Part-time (<50%) is pro-rated

• Workers’ Compensation leave of absence

• Leaves of absence, if purchased

• Repaid refunds

Service Credit

• Vesting requirements3 years of total service –hired < 7-1-20105 years of total service –hired > 7-1-2010

What do you receive credit for?

Service with another MN public plan (e.g., TRA or PERA)

Requirements:

• Minimum six months with each plan

• Must terminate from all plans

• Must collect from all plans within one year

Service Credit

Combined service credit(CSA)

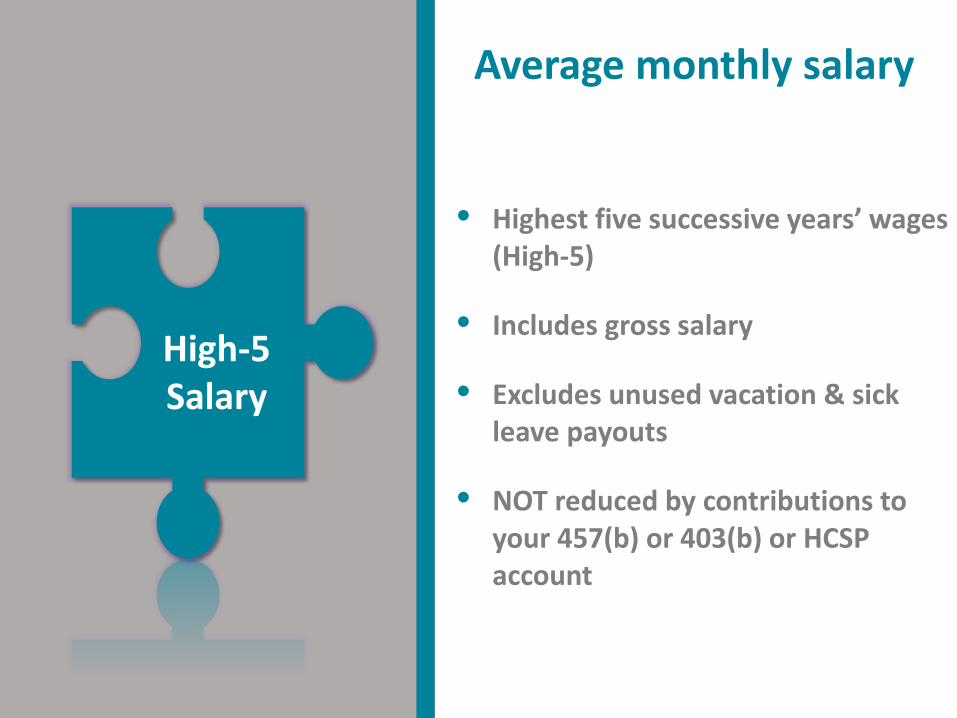

High-5 Salary

Average monthly salary

• Highest five successive years’ wages(High-5)

• Includes gross salary

• Excludes unused vacation & sick leave payouts

• NOT reduced by contributions to your 457(b) or 403(b) or HCSP account

The formula dictated by Minnesota law used to calculate your benefit

1.7%

Benefit Multiplier

A set multiplier

PossibleReduction

Depends on age

Full Retirement Ageif hired prior to 7-1-1989

• Age 65, or• Rule of 90

Full Retirement Ageif hired after 7-1-1989

• Age 66

Apply reduction if you collect pension benefit before your FULL

RETIREMENT AGE

Meet Anita & Sarah

Anita Plans to retire at age 66 With 30 years at DNR

Sarah Plans to retire at age 62 With 26 years at DOT

Each began employment at the same timeEach earn the same salary

MONTHLY BENEFIT

Anita retires age 66

Sarah retires age 62

Benefit example

x x

x x x

=

=

x

FOR ILLUSTRATIVE PURPOSES ONLY Your actual results will vary based on your retirement date.

SERVICE CREDIT

BENEFIT MULTIPLIER

HIGH-5SALARY

POSSIBLE REDUCTION

=

30 years $5,000 1.7% N/A $2,550

26 years $4,619 1.7% 0.7445 $1,520

MONTHLY BENEFIT

Sarah retires age 62 BUT DEFERS TO AGE 66

Benefit example

x x

x x x

=

=

x

SERVICE CREDIT

BENEFIT MULTIPLIER

HIGH-5SALARY

POSSIBLE REDUCTION

=

26 years $4,619 1.7% N/A $2,042

Sarah retires age 62

26 years $4,619 1.7% 0.7445 $1,520

FOR ILLUSTRATIVE PURPOSES ONLY Your actual results will vary based on your retirement date.

Benefit Type Your Benefit

Survivor Benefit

Bounce Back

Single Life $2,550 N/A N/A

Joint & Survivor (retiree & survivor are age 66)

100% Option $2,238 $2,238 $2,55075% Option $2,308 $1,731 $2,55050% Option $2,384 $1,192 $2,550

Life Income 15-Year Certain

$2,385 $2,385 N/A

Joint & Survivor benefit options

• Irrevocable election

FOR ILLUSTRATIVE PURPOSES ONLY Your actual results will vary.

• Survivor(s) doesn’t have to be a spouse

• Younger age survivor(s) = smaller benefit

• Non-spouse survivor(s) more than 19 years younger may only select 50% option

• Non-spouse survivor(s) between 10 and 19 years younger may select 75% or 50% option

Retirement age 62 66

Contributions to MSRS (6% of salary) $65,927 $80,471

Monthly benefit $1,520 $2,550

Total benefit paid in retirement (live to age 90) $628,942 $876,186

NET GAIN $563,015 $795,715

Value of pension benefit

Example

Sarah Anita

Your pension benefit is taxable

• Withhold federal & state tax (for MN only)

• Adjust tax withholding at any time

• Receive tax form 1099-R each January

Remember to plan for taxes

Post retirement benefit increase

Retirees receive an annual pension benefit increase each January

• First increase pro-rated

If you return to MSRS eligible position ONLY:

• Notify MSRS of re-employment

• 30 day break in service is required

• No retirement deductions taken

• When under Social Security’s full-retirement age, pension benefit suspends at earnings limit ($18,240 - 2020)

• Restarts at end of employment or January 1st of next year

• May affect eligibility to access your MNDCP & HCSP assets

Working after retirement

Death prior to retirement

Surviving Spouse Benefit

• 100% Joint & Survivor lifetime monthly benefit, or

• Monthly payment for 10, 15 or 20 years, or

• Lump-sum payment of employee contributions only plus 3% interest

Non Spouse Benefit

• Lump-sum payment of employee contributions only plus 3% interest

• If no surviving spouse, minor child benefit

1. Application for Retirement Benefit

2. Direct Deposit form

3. Birth records

4. Copy of Marriage Certificate(if applicable)

5. Certified copy of Divorce Decree orDomestic Relations Order (if applicable)

Forms neededPension benefitApplication process

Contact your pension plan provider when applying for

your pension benefit

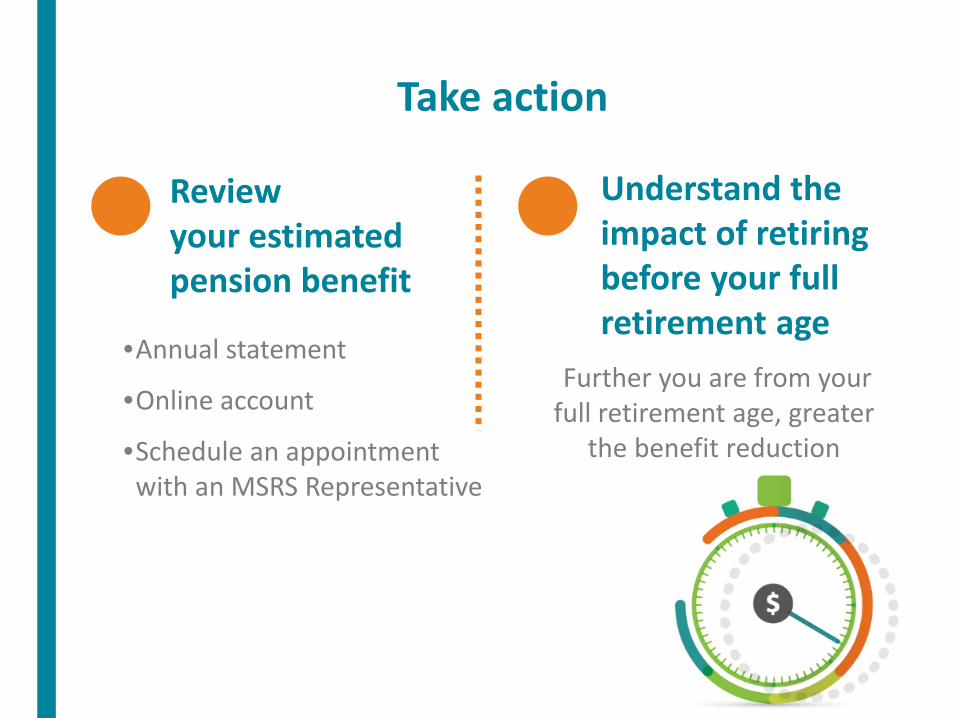

•Annual statement

•Online account

•Schedule an appointment with an MSRS Representative

Further you are from your full retirement age, greater

the benefit reduction

Take action

Understand the impact of retiring before your full retirement age

Review your estimated pension benefit

IncomeGAP

What is an income gap?

You might have an income gap if:

your savings does not meet your retirement income needs

you retire early and need more retirement savings

or you fear you will outlive your savings

100%80%

You may need

of your current income to maintain your lifestyle in

retirement

How much income will it take?

$48,000

$60,000 annual salary

FOR ILLUSTRATIVE PURPOSES ONLY Figure represents 80% of $60,000 salary

Bridge any income gaps

SocialSecurity

403(b)

457(b)

IRA

Pension

RETIREMENTINCOME

SAVINGS

Income your MN public pension replaces:1

• 10 years service = 17%

• 20 years service = 34%

• 30 years service = 51%

Income your Social Security replaces:2

• Average MN public employee recipient = 31%

Pension & Social Security may not be enough

1 Based on the years of service of MSRS pension recipients. Assumes full retirement age of 66. A TRA recipient replacement percentage would be higher.

2 Based on the collecting an unreduced social security benefit at age 66 and a final average salary of 2016 retirees from MSRS, PERA, TRA public pension plans. Does not assume future earnings. Salary Source: MSRS, PERA and TRA 2016 Comprehensive Annual Financial Report. Social Security Source: SSA Benefit Calculator.

Retirement Age 62 66

High-5 monthly salary $4,619 $5,000

Pension replacement 33% 51%

Social Security replacement 24% 30%

TOTAL INCOME REPLACEMENT 57% 81%

Case study income replacement

FOR ILLUSTRATIVE PURPOSES ONLY Your actual results will vary.

Sarah Anita

Retirement Age 62 66

TOTAL INCOME REPLACEMENT 57% 81%

Savings needed to replace 80% $240,300* $0

Savings needed to replace 100% $453,500* $198,500*

Case study savings needed

FOR ILLUSTRATIVE PURPOSES ONLY Your actual results will vary.Based on a 5% annual rate of return (not guaranteed) and 2% inflation. Assuming annual withdrawals to reach stated income replacement lasting until age 90.

Sarah Anita

Calculate how much retirement income you will need

www.msrs.state.mn.us/toolbox#mndcpDo your own calculation

Take action Ways to bridge the income gap

MNDCP 457(b) & 403(b) account assetsIncrease your annual contribution if possible

HCSP account assetsLearn how to use your HCSP account assets

Pension & Social SecurityDefer, if possible, the date of your retirement

Available to all MN public employees

A voluntary savings plan to supplement

your pension & Social Security income

State sponsored 457(b) Plan

What is the MNDCP?

Minimize stock market volatility

Save more each paycheck

Maximize your contributions1

2

3

Take advantage of lower fees4

Make the most of the MNDCP

Bridge the income gap

Age 50 & over

$26,000 Within 3 years of

normal retirement age

Maximize your contribution

Ramping up contributions by $200/paycheck can add up

$17,075

10 years $71,186

5 years

3 years

$30,291

What you contribute What you may earn

FOR ILLUSTRATIVE PURPOSES ONLY Figures represent the growth of bi-weekly contributions at 6% rate of return (not guaranteed) compounded monthly, reinvestment of earnings with no withdrawals. The tax-deferred amounts shown do not reflect any charges, expenses or fees.

The impact of saving more

Multiple

More Diverse

One

Less Diverse

Investment diversification: Spreading your investments over multiple asset classes

FOR ILLUSTRATIVE PURPOSES ONLY Diversification does not ensure a profit or protect against loss in declining markets.

Minimize market fluctuation impactBridge the income gap

How diversification works

Sample asset allocation of an investment portfolio

Diversification within the stock allocation

FOR ILLUSTRATIVE PURPOSES ONLY Diversification does not ensure a profit or protect against loss in declining markets.

BONDS

CMDTY

CASH

STOCKS

U.S. Large-cap

U.S. Mid-cap

U.S. Small-cap

Inter-national

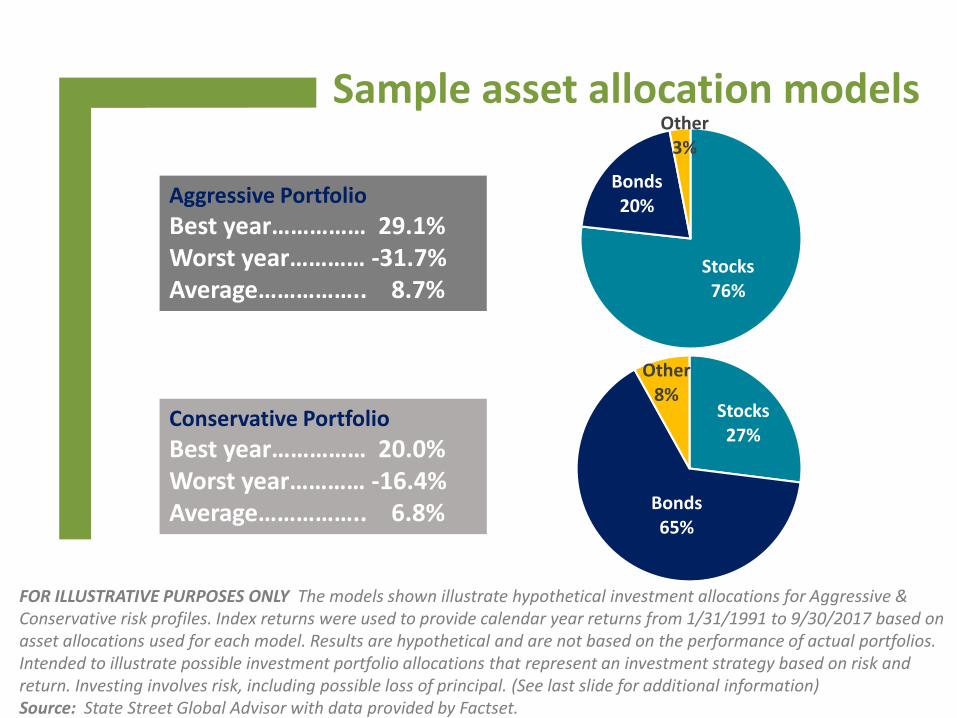

Aggressive PortfolioBest year…………… 29.1%Worst year………… -31.7%Average…………….. 8.7%

Conservative PortfolioBest year…………… 20.0%Worst year………… -16.4%Average…………….. 6.8%

Sample asset allocation models

FOR ILLUSTRATIVE PURPOSES ONLY The models shown illustrate hypothetical investment allocations for Aggressive & Conservative risk profiles. Index returns were used to provide calendar year returns from 1/31/1991 to 9/30/2017 based on asset allocations used for each model. Results are hypothetical and are not based on the performance of actual portfolios. Intended to illustrate possible investment portfolio allocations that represent an investment strategy based on risk and return. Investing involves risk, including possible loss of principal. (See last slide for additional information)Source: State Street Global Advisor with data provided by Factset.

Stocks 76%

Bonds 20%

Other 3%

Stocks27%

Bonds 65%

Other8%

Please consider the investment objectives, fees and expenses carefully before investing. The prospectus and/or disclosure documents contain this and other important information about the investments offered through your plan. To obtain a prospectus or disclosure document, or to learn more about the investment options, visit www.msrs.state.mn.us or call 800-657-5757. Read such materials carefully before investing.

Investment Disclosure

Avoid rollover regret

Upon separation of employment:

• You are not required to close or rollout your 457(b) or 403(b) account to an IRA

• Consider consolidating your retirement plan accounts

• Discuss rolling money from one account to another with your financial advisor/planner and consider any potential fees and/or limitations of available investment options

Rollover remorse

One final point!

Once all assets are out of the plan, you may not rejoin

Click to edit Master title style Fees can erode your gains

1 Source: 2017 Advisory HQ study; Average Financial Advisor Fees based on assets under management for a $100,000 account

2 MNDCP administrative fee as of 1/1/2020 capped at $125/year

For illustrative purposes only This hypothetical illustration is not intended as a projection of future investment results, nor is it intended as financial planning or investment advice. Rates of any return may vary. The illustration does not reflect other associated charges, expenses of fees. The tax-deferred accumulation shown would be reduced if these fees had been deducted.

Assumptions

• Starting balance: $65,000

• No contributions

• 5% annual rate of return• Annual 4% withdrawal

of account balance

• After 25 years

$77,460$79,330

$60,670

Account balance with a 1.12% Advisor fee1

MNDCP account with a 0.10% Administrative fee2

No Account Fee

Withdrawal considerations Goals

• Number of years savings should last• Leave savings to heirs• Philanthropic wishes

Realities

• Meet fixed expenses• Allow for discretionary expenses• Cover emergency expenses

Other

• Coordinate withdrawals with the use of other assets

• Tax efficient withdrawals

How to generate income from your retirement plan

Lump-sum withdrawal

Automatic/periodic withdrawal schedule

Partial withdrawals

when needed

Flexible Withdrawal Options

Savings Balance$50,000 $100,000 $150,000

11 yrs 4 mos

4 yrs 9 mos

3 yrs

> 50 yrs

11 yrs 4 mos

6 yrs 8 mos

> 50 yrs

22 yrs 3 mos

11 yrs 4 mos

Gross Withdrawal

$500/month

$1,000/month

$1,500/month

FOR ILLUSTRATIVE PURPOSES ONLY Your actual results will vary. This hypothetical example assumes a 6% annual rate of return. Rate of return not guaranteed.

How long will your savings last?

Calculate how long your savings will last

Do your own calculation www.msrs.state.mn.us/toolbox#mndcp

Withdrawals are taxable

20% mandatory federal withholding, except• Withdrawal schedules lasting 10 or more years • RMD payments

Withdrawals are tax-free if:• Withdrawal made after age 59 ½

(death or disability)AND

• Roth account established at least five tax years

Pre-tax savings

Roth after-tax savings

Understand the tax landscape

Withdrawals made prior to age 59 ½ that are attributable to rollovers from another type of plan may incur a 10% early withdrawal IRS penalty

Click to edit Master title style Fulfill your RMD

RMDs are mandated by the IRS once you reach age 72 or retire, whichever is later

Required MinimumDistributions

(RMDs)

Click to edit Master title style

1. MNDCP account balance as of previous December 31 $______

2. Life expectancy factor (see table) The age you will turn this year _______

3. RMD Amount (line 1 ÷ line 2) $______

Uniform Lifetime Table III

For use by: • Unmarried owner

• Married owner whose spouse is not more than 10 years younger

• Married owner whose spouse is not the sole beneficiary

Calculation

AgeLife

Expectancy Factor

72 25.6

73 24.7

74 23.8

75 22.9

Excess accumulation penalty• 50% of amount not

distributed as required

RMD rules to remember

Required Minimum Distribution• Age 72• Every year thereafter• Not required if employed

Factors change in 2020

Keep beneficiarydesignations up to date

A beneficiary will inherit

your money

What happens if something happens to

you?

Plan aheadAVOID

PROBATE

Take action

Maximizeyour contributions

Keep in mindyou are not required to roll out or close your 457(b) or 403(b) retirement accountMinimize

account fluctuations with a diversified investment strategy

Considera withdrawal plan that is right for you

Sample health care costs

Retiree only Retiree & Spouse

$144,000 $288,000

$175,236 $374,196

Amount needed to cover retiree health insurance1 to age 90

SOURCE: MSRS 20201Based on SEGIP health insurance cost of $701/month retiree; $2.061 retiree & spouse from age 62 to age 65 and$355 SEGIP supplemental insurance and $145 Medicare Part B / month for retiree & spouse from age 65 to age 90

FOR ILLUSTRATIVE PURPOSES ONLY

Anita retires age 66

Sarah retires age 62

A tax-free savings account

Tax-free contributions Tax-free potential growth Tax-free reimbursements No Social Security, Medicare or income taxes

Reimburse post-employment health care expenses for employee, spouse, legal tax dependents, and children up to 26th birthday.

NOTE: Your Social Security benefit may be slightly reduced because no FICA tax is collected on contributions

What is the HCSP?

Severance payment $10,000Federal Income Tax 2,200 State Income Tax 680 FICA Tax 765

Net cash payment $6,355

This hypothetical example assumes a 22% federal withholding rate + 6.80% state withholding rate + 7.65% FICA (Social Security and Medicare) tax rate. Individual tax rates will vary based on total taxable income and filing status for the year.

Tax-Free HCSP Payout

Tax-free matters

FOR ILLUSTRATIVE PURPOSES ONLY

Taxable Cash Payout

Severance payment $10,000Federal Income Tax 0 State Income Tax 0 FICA Tax 0

Net cash payment $10,000

Eligibility for participation

Participation CANNOT be…

individual choice—group participation must be specified in union contract or personnel policy

Participation MUST be…

negotiated in union contract

or

included in personnel policy for non-union employees

Investment Default Money Market Fund

You could lose money by investing in a money market fund. Although the fund seeks to preserve the value of your investment at $1 per share, it cannot guarantee it will do so. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The fund’s sponsor has no legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financial support to the fund at any time.

Seeks to maintain the value of a participant's original investment

Seeks to earn interest that is competitive with short-term interest rates

Plan expenses may exceed earned interest

Click to edit Master title style

T. Rowe Price Small Cap Stock Fund

Vanguard Total International Stock Index Fund

Vanguard Mid Cap Index Fund

Vanguard Total Stock Market Index FundVanguard Dividend Growth Fund

Vanguard Balanced Index Fund

Dodge & Cox Income FundVanguard Total Bond Market Index Fund

Stable Value Fund

Higher Risk Potential Reward

Lower RiskPotential Reward

Investment options

FOR ILLUSTRATIVE PURPOSES ONLY The chart reflects the expected relative risk/return potential over the long-term. Past

performance is not a guarantee of future results.

Investment DisclosurePlease consider the investment objectives, fees and expenses carefully before investing. The prospectus and/or disclosure documents contain this and other important information about the investments offered through your plan. To obtain a prospectus or disclosure document, or to learn more about the investment options, visit www.msrs.state.mn.usor call 800-657-5757. Read such materials carefully before investing.

No investment is 100% risk free. You can incur loss of principal by investing. There is no assurance that investing will ensure a profit or protect against loss.

Foreign investments involve special risks, including currency fluctuation, taxation differences and political developments. Equity securities of small and mid-sized companies may be more volatile than securities of larger, more established companies. Asset allocation and balanced investment options and models are subject to the risks of the underlying funds, which can be a mix of stocks/stock funds and bond/bond funds. A bond fund’s yield, share price and total return change daily and are based on changes in interest rates, market conditions, economic and political news, and the quality and maturity of its investments. In general, bond prices fall when interest rates rise and vice versa.

• Upon termination of employment… at any age

• Once retired

• If collecting a disability benefit from a MN public pension plan

Returning to work?You may have limited or no access

When can yourequest reimbursements?

Eligible medical/dental expenses, including:

Insurance Premiums• Health, Medicare, Dental, Long-Term Care

Dental costs

Eye-care costs

Co-payments & prescription drugs

Over-the-counter drugs with prescription

What is reimbursable

For other eligible expenses, see IRS Publication 502

Life insurance premiums

Teeth bleaching

Cosmetic surgery

Finance charges on bills

Fees for health club membership

Funeral expenses

Vitamins

What cannot be reimbursed

Reimbursement requests

Paid directly to participant, not to insurer or provider

Out-of-pocket expenses• Minimum payout $75

• Maximum limit: $35,000 in 2020

Monthly insurance premiums• Medical, dental, long-term care,

Medicare

• Set up direct deposit to bank account

REIMBURSED

Patient Billed

Pay Bill

Request Reimbursement

from HCSP

EligibilityVerification

If a contribution is made to an HSA on your behalf in same year you are eligible to access your HCSP:

Your HCSP account becomes “limited-use”

May request reimbursements for dental & vision expenses only during the year.

HCSP/HSA compatibility

Complete a Reimbursement Suspension Electionform each calendar year that you or your employer contribute to an HSA

Account balance transfers to HCSP account for spouse

OR, if no spouse

Account balance transfers to HCSP account for dependent(s)Spouse or legal dependent reimbursements remain tax-free

What happens if you die?

1Legal dependent is someone you can claim on your federal tax return.

Spouse or legal dependents1

Account balance transfers to HCSP account for your designated beneficiaries

Reimbursements taxed as ordinary income (MSRS will issue IRS Form 1099-MISC)

What happens if you die?

If NO spouse or legal dependents1

1Legal dependent is someone you can claim on your federal tax return.

Receive an HCSP Welcome Packet

after your first contribution is received

after your termination date is entered or your employer remits severance payment

in approximately 4 weeks:

Review your investments

The Money Market Fund is the investment default

Rememberpost-employment account for health expenses only

Do not reportreimbursements fromyour account on your federal/state tax return since the HCSP is a tax-free plan

Take Action

Time Table

PRIOR TO RETIREMENT ACTION

5 years

• Maximize contributions to your 457(b) and/or 403(b) account in your final working years

• Calculate your retirement budget• Adjust your 457(b) and/or 403(b) & HCSP

investment allocation as appropriate

1 year• Explore your retirement income & expenses• Prepare your retirement budget

6 - 12 months Contact your pension plan provider to request an audited pension estimate

3 months Contact Social Security, if retiring at age 62+

1 - 2 months

• Complete pension application File with pension plan

• Contact H.R. Office about insurance & HCSP eligibility

Pre-retirement timetable

AFTER RETIREMENT ACTION

Immediately Enjoy Enjoy Enjoy Enjoy Enjoy

Up to 6 weeks Receive pension authorization letter & first payment

30 days after receipt of pension authorization letter

Your joint & survivor benefit option becomes irrevocable

1st week of the next month Receive monthly pension payment

December Receive notification of post-retirement increase

January Receive tax Form 1099-R for pension & MNDCP payments

Post-retirement timetable

Get more information

NOTE: These Web sites are for general education & information only and are provided as a benefit to the users of the site.

Pension PlanMSRSTRAPERA

www.msrs.state.mn.us www.minnesotatra.org www.mnpera.org

1-800-657-57571-800-657-36691-800-652-9026

Retiree insurance(health, dental, life) Contact your designated retiree insurance dept, or:

State employees 651-355-0100University of MN employees 612-624-8647Met Council employees 651-602-1601

Social Security www.ssa.gov 1-800-772-1213

Medicare www.medicare.gov

Administration for Community Living

www.acl.gov

www.msrs.state.mn.us

1.800.657.5757 or 651.296.2761

Contact Us!

Receive more details about the information you just saworMake an appointment to speak to one of our retirement counselors

St. Paul - 60 Empire Drive · Suite 300

St. Cloud - 4150 Second Street S · Suite 330

Mankato - 11 Civic Center Plaza · Suite 150

Detroit Lakes - 714 Lake Ave · Suite 102

Duluth - 625 East Central Entrance

Locations:

Important Notes

Core securities, when offered, are offered through GWFS Equities Inc. and/or other broker dealers.

GWFS Equities Inc., Member FINRA/SIPC, is a wholly owned subsidiary of Great-West Life & Annuity Insurance Company.

GWL&A and/or its subsidiaries are not responsible for, have not reviewed and do not endorse the content contained on msrs.state.mn.us.

Today’s workshop was designed to: Provide you with fundamental information

on your MSRS retirement plans Objectively highlight your

investment options Outline other sources of information

for your decisions

Please read all investment-related information prior to investing

This presentation is for general education purposes only and does not, nor is intended to constitute legal, tax, investment or financial advice of any kind.

• Please consult your own advisors for such advice

AM553491-07.18

The hypothetical illustrations are for informational and educational purposes only. They are not intended to be a recommendation of a specific investment or investment strategy. In applying a particular asset allocation model to your individual situation, you should consider other assets, income, and investments in addition to the account you are considering for investment, to the extent the model does not consider these additional assets.

Index returns shown are not those of an actual fund or portfolio, and are used to provide calendar year returns back to 1995 based on hypothetical asset allocations used for a Conservative and Aggressive model, respectively. They are not backtested returns and do not reflect the changes to glide paths over time. A benchmark index is not actively managed, does not have a defined investment objective, and does not incur fees or expenses. You cannot invest directly in a benchmark index.

For calendar year return calculations, the following index data from 9/30/2017 to 1/31/1991 was used, reflective of the underlying indices used for the asset allocations. US Large Cap Equities: S&P 500 Index; Global REIT: FTSE EPRA/NAREIT Developed Index; Commodities: Bloomberg Roll Select Commodity Index; US Core Bonds: Bloomberg Barclays US Aggregate; and International Equity: MSCI ACWI ex USA IMI Index.

For returns back to 1991 for indices with insufficient track records, used current indices for existing track records and replaced with equivalent indices with longer track records for the periods prior to index inception. Small/Mid Cap US Equities: Russell Small Cap Completeness Index from 4/1/1999-9/30/2017 and the MSCI Small/Mid Cap Index from 3/31/1999 to 1/31/1991; US Intermediate TIPS: Bloomberg Barclays US Treasury Inflation Protected Notes (1-10 Y) from 7/1/2001-9/30/2017 and the Bloomberg Barclays US Aggregate Index from 6/30/2001 to 1/31/1991 (TIPS returns were not available prior to 2001); US Short Term Government/Credit: Bloomberg Barclays Capital 1-3 Yr Government Credit Index from 5/1/2004-9/30/2017 and the Bloomberg Barclays US Aggregate Government & Credit (1-3 Y) from 4/30/2004 to 1/31/1991; US High Yield Bonds: Bloomberg Barclays High Yield Very Liquid from 2/1/1994-9/30/2017 and the Bloomberg Barclays US Corporate High Yield Index from 1/31/1994 to 1/31/1991; and Long Government Bonds: Bloomberg Barclays Long Government Bond Index from 1/1/1997-9/30/2017 and the Bloomberg Barclays Long Treasury Index from 12/31/1996 to 1/31/1991.

Asset Allocation Model Disclosurefrom slide 50