2.2 islamic finance segments - assaif islamic fin… · 2.2 islamic finance segments 2.2.1 islamic...

TRANSCRIPT

15GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

2.2 Islamic Finance Segments

2.2.1 Islamic Banking

• The Islamic banking sector worldwide has grown at a strong rate of 15.0%-20.0% annually over the past decade, from approximately USD150.0 billion in the mid-1990s to an estimated USD1.1 trillion in 2011. Based on a compound annual growth rate (CAGR) of 21.1% between 2007 and 2011, the Islamic banking assets are expected to grow to USD1.3 trillion in 2012, accounting for more than 80.0% of global Islamic fi nance assets market share.

• The Islamic banking industry is not only confi ned to Muslim-majority countries in the GCC and South East Asia regions, but also into new territories within Central Asia and Europe, many of which are currently in the midst of implementing appropriate regulatory and legal reforms that would facilitate the provision of Islamic fi nancial products. At the end-2011, there are 363 full-fl edged Islamic fi nancial institutions and a further 108 conventional fi nancial institutions operating an Islamic window.

• Although the Islamic banking industry currently constitutes only 1.6% of the total assets of the top 50 largest banks in the world (totalling USD66.2 trillion at the end-2011), it remains one of the fastest growing segments in the global fi nancial services sector. The Islamic banking industry is expected to witness further developments in the future, particularly in terms of the development of new products and services as well as the opening up of new markets or jurisdictions, in light of the industry’s resilience during the global fi nancial crisis.

• The growth of Islamic banking has had many positive spillover effects to the real economy. Given that the industry is tied to fi nancing real assets through the buying and selling of goods ensures that funds are intermediated towards and utilised for real economic activities. This asset-based feature of Islamic banking also ensures that speculative lending is restricted and the fi nancial sector remains in balance with economic growth.

• The rapid growth of Islamic banking across the globe gives weight to the commercial viability of the industry in providing business returns as well as positively impacting its stakeholders. The viability of Islamic fi nance has been derived from its ability to meet the changing demands of the economy and from its cost competitiveness. Its development has also been supported by a well-developed legal, regulatory and supervisory framework that has been important in ensuring its soundness and stability. The industry’s growth has also created avenues for specialised employment in Islamic banking practices which in turn has helped to enhance employment within the various jurisdictions.

• The development of the Islamic banking system over the years is a response to both demand for faith-based fi nance and to address economic needs. The Islamic faith calls for the

Global Islamic Banking Assets Growth Trends

0

1,000

2,000

3,000

4,000

5,000

6,000

2007

2008

2009

2010

2011

2012

f

2013

f

2014

f

2015

f

2016

f

2017

f

2018

f

2019

f

2020

f

US

D b

illion

2007-2011 CAGR =

21.1%

Source: Regulatory authorities, Bloomberg, Zawya and Comporate Communications, Central Banks, Individuals institutions, The Banker, KFHR

Share of Global Islamic Banking Asset in 2011

Iran39.7%

Saudi Arabia13.7% Malaysia

9.8%

UAE9.1%

Kuwait9.0%

Qatar4.1%

Turkey2.7%

Bahrain2.3%

Indonesia1.5%

Egypt 1.3%

Sudan1.1%

Others5.6%

Source: Central Banks, Individuals institutions, The Banker

avoidance of any transaction based on interest or riba while the economic side provides an avenue to promote investment and productive activities, taking a role in the distribution of income and adding stability to the economy.

• Islamic banks have been capitalising on a demand-driven niche market growing at a fast pace. However, with a larger number of existing Islamic banks and growing interest from conventional institutions tapping into the emerging market, the industry is becoming highly competitive. Conventional fi nancial institutions are now realising the value of Islamic fi nancing techniques and starting to incorporate them either in their lending practices or via separate Islamic windows operations, which has further stimulated the spread of Islamic banking.

16 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

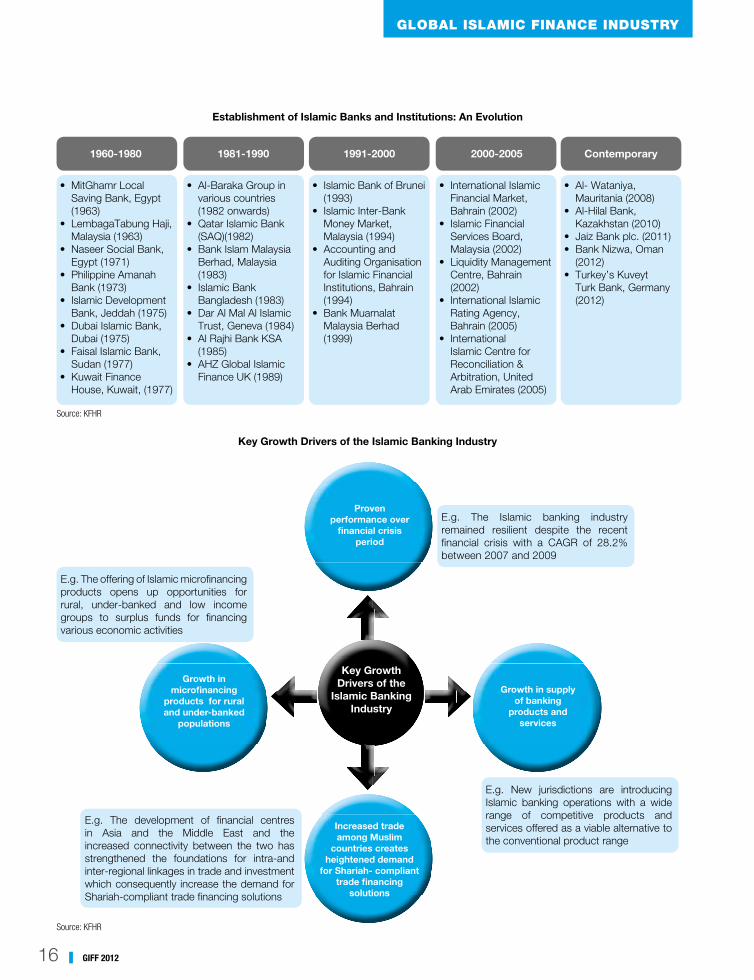

E.g. The offering of Islamic microfi nancing products opens up opportunities for rural, under-banked and low income groups to surplus funds for fi nancing various economic activities

E.g. The Islamic banking industry remained resilient despite the recent fi nancial crisis with a CAGR of 28.2% between 2007 and 2009

E.g. New jurisdictions are introducing Islamic banking operations with a wide range of competitive products and services offered as a viable alternative to the conventional product range

E.g. The development of fi nancial centres in Asia and the Middle East and the increased connectivity between the two has strengthened the foundations for intra-and inter-regional linkages in trade and investment which consequently increase the demand for Shariah-compliant trade fi nancing solutions

Key Growth Drivers of the

Islamic Banking Industry

Growth in microfi nancing

products for rural and under-banked

populations

Growth in supply of banking

products and services

Increased trade among Muslim

countries creates heightened demand

for Shariah- compliant trade fi nancing

solutions

Proven performance over

fi nancial crisis period

Establishment of Islamic Banks and Institutions: An Evolution

Key Growth Drivers of the Islamic Banking Industry

1960-1980 1981-1990 1991-2000 2000-2005 Contemporary

• MitGhamr Local Saving Bank, Egypt (1963)

• LembagaTabung Haji, Malaysia (1963)

• Naseer Social Bank, Egypt (1971)

• Philippine Amanah Bank (1973)

• Islamic Development Bank, Jeddah (1975)

• Dubai Islamic Bank, Dubai (1975)

• Faisal Islamic Bank, Sudan (1977)

• Kuwait Finance House, Kuwait, (1977)

• Al-Baraka Group in various countries (1982 onwards)

• Qatar Islamic Bank (SAQ)(1982)

• Bank Islam Malaysia Berhad, Malaysia (1983)

• Islamic Bank Bangladesh (1983)

• Dar Al Mal Al Islamic Trust, Geneva (1984)

• Al Rajhi Bank KSA (1985)

• AHZ Global Islamic Finance UK (1989)

• Islamic Bank of Brunei (1993)

• Islamic Inter-Bank Money Market, Malaysia (1994)

• Accounting and Auditing Organisation for Islamic Financial Institutions, Bahrain (1994)

• Bank Muamalat Malaysia Berhad (1999)

• International Islamic Financial Market, Bahrain (2002)

• Islamic Financial Services Board, Malaysia (2002)

• Liquidity Management Centre, Bahrain (2002)

• International Islamic Rating Agency, Bahrain (2005)

• International Islamic Centre for Reconciliation & Arbitration, United Arab Emirates (2005)

• Al- Wataniya, Mauritania (2008)

• Al-Hilal Bank, Kazakhstan (2010)

• Jaiz Bank plc. (2011)• Bank Nizwa, Oman

(2012)• Turkey’s Kuveyt

Turk Bank, Germany (2012)

Source: KFHR

Source: KFHR

17GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Performance of Islamic Banking

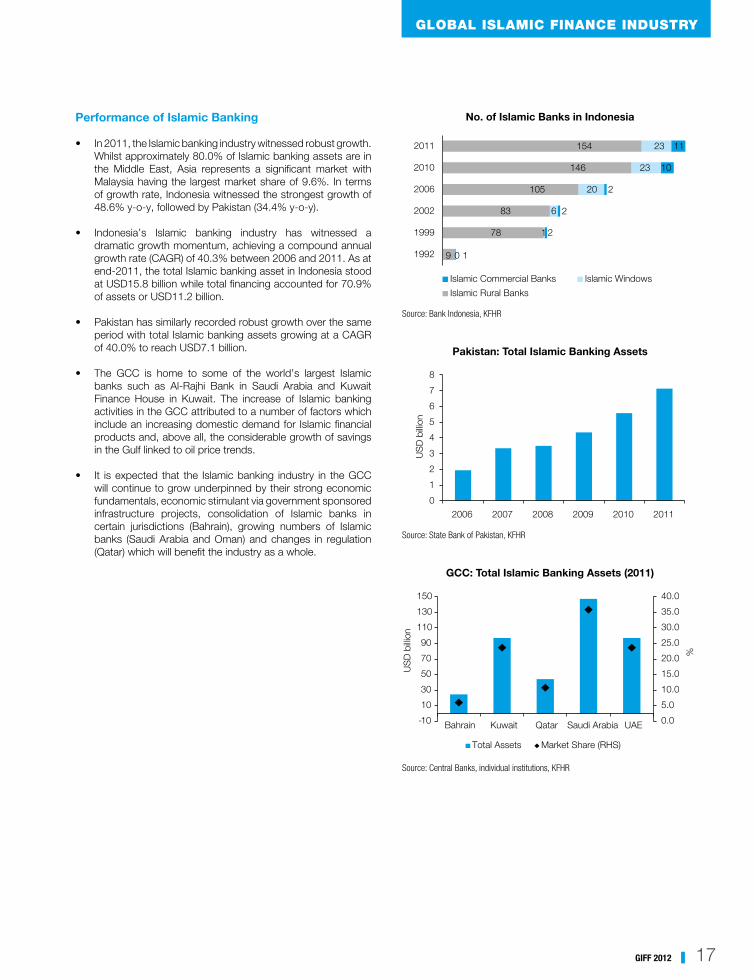

• In 2011, the Islamic banking industry witnessed robust growth. Whilst approximately 80.0% of Islamic banking assets are in the Middle East, Asia represents a signifi cant market with Malaysia having the largest market share of 9.6%. In terms of growth rate, Indonesia witnessed the strongest growth of 48.6% y-o-y, followed by Pakistan (34.4% y-o-y).

• Indonesia’s Islamic banking industry has witnessed a dramatic growth momentum, achieving a compound annual growth rate (CAGR) of 40.3% between 2006 and 2011. As at end-2011, the total Islamic banking asset in Indonesia stood at USD15.8 billion while total fi nancing accounted for 70.9% of assets or USD11.2 billion.

• Pakistan has similarly recorded robust growth over the same period with total Islamic banking assets growing at a CAGR of 40.0% to reach USD7.1 billion.

• The GCC is home to some of the world’s largest Islamic banks such as Al-Rajhi Bank in Saudi Arabia and Kuwait Finance House in Kuwait. The increase of Islamic banking activities in the GCC attributed to a number of factors which include an increasing domestic demand for Islamic fi nancial products and, above all, the considerable growth of savings in the Gulf linked to oil price trends.

• It is expected that the Islamic banking industry in the GCC will continue to grow underpinned by their strong economic fundamentals, economic stimulant via government sponsored infrastructure projects, consolidation of Islamic banks in certain jurisdictions (Bahrain), growing numbers of Islamic banks (Saudi Arabia and Oman) and changes in regulation (Qatar) which will benefi t the industry as a whole.

No. of Islamic Banks in Indonesia

1

2

2

2

10

11

0

1

6

20

23

23

9

78

83

105

146

154

1992

1999

2002

2006

2010

2011

Islamic Commercial Banks Islamic Windows

Islamic Rural Banks

Source: Bank Indonesia, KFHR

Pakistan: Total Islamic Banking Assets

0

1

2

3

4

5

6

7

8

2006 2007 2008 2009 2010 2011

US

D b

illion

Source: State Bank of Pakistan, KFHR

GCC: Total Islamic Banking Assets (2011)

%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-10

10

30

50

70

90

110

130

150

Bahrain Kuwait Qatar Saudi Arabia UAE

US

D b

illion

Total Assets Market Share (RHS)

Source: Central Banks, individual institutions, KFHR

18 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

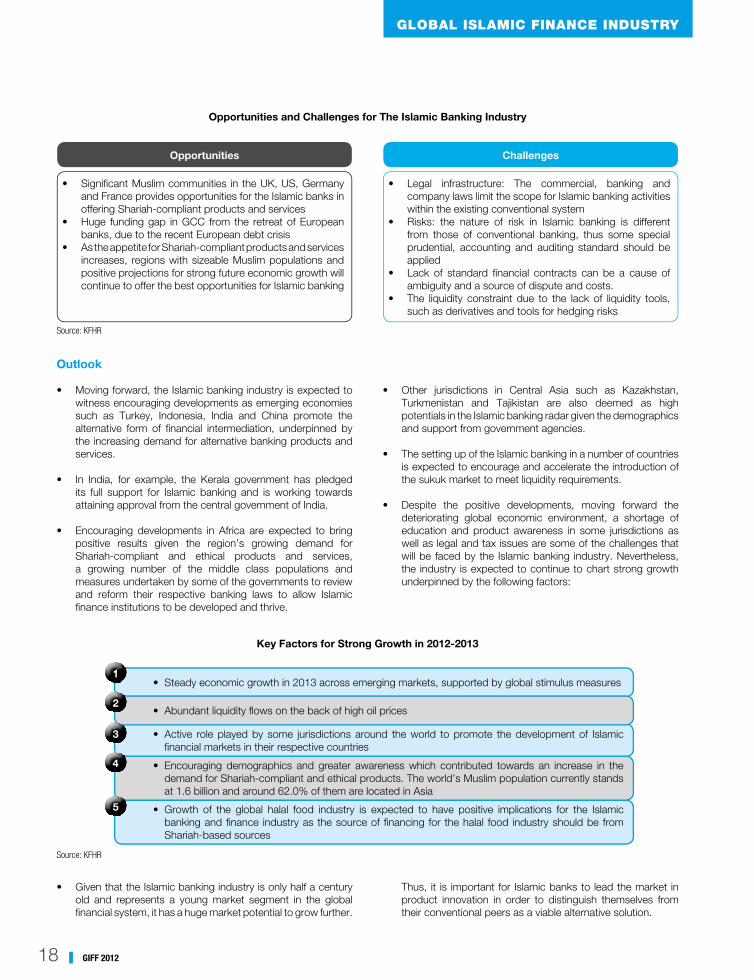

Key Factors for Strong Growth in 2012-2013

• Steady economic growth in 2013 across emerging markets, supported by global stimulus measures

• Active role played by some jurisdictions around the world to promote the development of Islamic fi nancial markets in their respective countries

• Growth of the global halal food industry is expected to have positive implications for the Islamic banking and fi nance industry as the source of fi nancing for the halal food industry should be from Shariah-based sources

• Abundant liquidity fl ows on the back of high oil prices

• Encouraging demographics and greater awareness which contributed towards an increase in the demand for Shariah-compliant and ethical products. The world’s Muslim population currently stands at 1.6 billion and around 62.0% of them are located in Asia

1

2

3

4

5

Source: KFHR

• Given that the Islamic banking industry is only half a century old and represents a young market segment in the global fi nancial system, it has a huge market potential to grow further.

Thus, it is important for Islamic banks to lead the market in product innovation in order to distinguish themselves from their conventional peers as a viable alternative solution.

Opportunities and Challenges for The Islamic Banking Industry

Opportunities Challenges

• Signifi cant Muslim communities in the UK, US, Germany and France provides opportunities for the Islamic banks in offering Shariah-compliant products and services

• Huge funding gap in GCC from the retreat of European banks, due to the recent European debt crisis

• As the appetite for Shariah-compliant products and services increases, regions with sizeable Muslim populations and positive projections for strong future economic growth will continue to offer the best opportunities for Islamic banking

• Legal infrastructure: The commercial, banking and company laws limit the scope for Islamic banking activities within the existing conventional system

• Risks: the nature of risk in Islamic banking is different from those of conventional banking, thus some special prudential, accounting and auditing standard should be applied

• Lack of standard fi nancial contracts can be a cause of ambiguity and a source of dispute and costs.

• The liquidity constraint due to the lack of liquidity tools, such as derivatives and tools for hedging risks

Source: KFHR

Outlook

• Moving forward, the Islamic banking industry is expected to witness encouraging developments as emerging economies such as Turkey, Indonesia, India and China promote the alternative form of fi nancial intermediation, underpinned by the increasing demand for alternative banking products and services.

• In India, for example, the Kerala government has pledged its full support for Islamic banking and is working towards attaining approval from the central government of India.

• Encouraging developments in Africa are expected to bring positive results given the region’s growing demand for Shariah-compliant and ethical products and services, a growing number of the middle class populations and measures undertaken by some of the governments to review and reform their respective banking laws to allow Islamic fi nance institutions to be developed and thrive.

• Other jurisdictions in Central Asia such as Kazakhstan, Turkmenistan and Tajikistan are also deemed as high potentials in the Islamic banking radar given the demographics and support from government agencies.

• The setting up of the Islamic banking in a number of countries is expected to encourage and accelerate the introduction of the sukuk market to meet liquidity requirements.

• Despite the positive developments, moving forward the deteriorating global economic environment, a shortage of education and product awareness in some jurisdictions as well as legal and tax issues are some of the challenges that will be faced by the Islamic banking industry. Nevertheless, the industry is expected to continue to chart strong growth underpinned by the following factors:

19GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

2.2.2 Sukuk

Overview

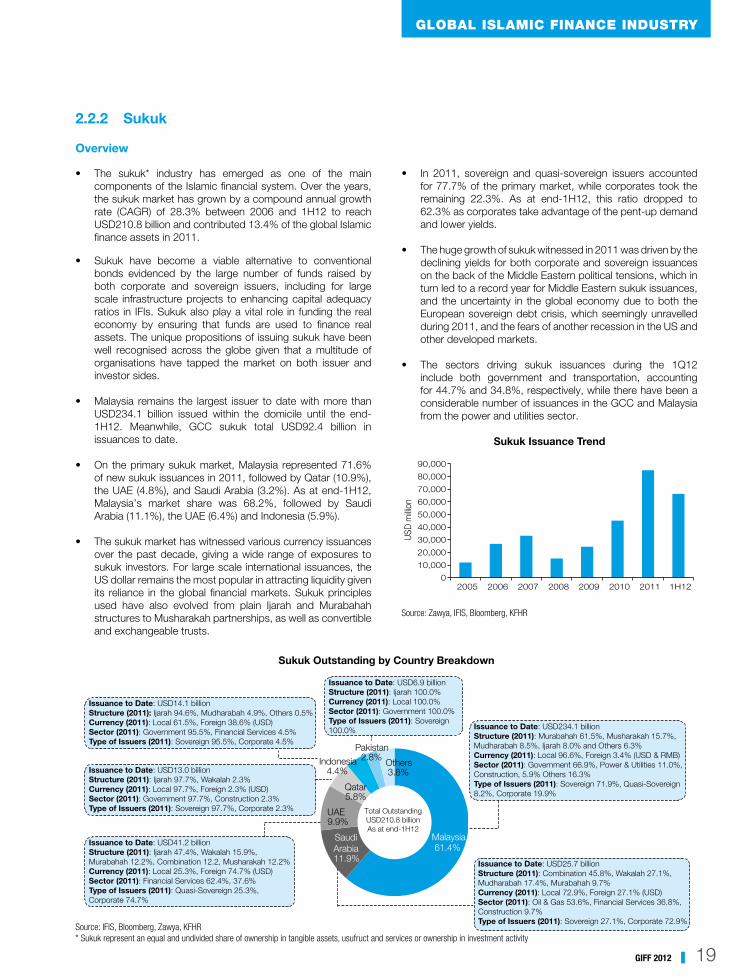

• The sukuk* industry has emerged as one of the main components of the Islamic fi nancial system. Over the years, the sukuk market has grown by a compound annual growth rate (CAGR) of 28.3% between 2006 and 1H12 to reach USD210.8 billion and contributed 13.4% of the global Islamic fi nance assets in 2011.

• Sukuk have become a viable alternative to conventional bonds evidenced by the large number of funds raised by both corporate and sovereign issuers, including for large scale infrastructure projects to enhancing capital adequacy ratios in IFIs. Sukuk also play a vital role in funding the real economy by ensuring that funds are used to fi nance real assets. The unique propositions of issuing sukuk have been well recognised across the globe given that a multitude of organisations have tapped the market on both issuer and investor sides.

• Malaysia remains the largest issuer to date with more than USD234.1 billion issued within the domicile until the end-1H12. Meanwhile, GCC sukuk total USD92.4 billion in issuances to date.

• On the primary sukuk market, Malaysia represented 71.6% of new sukuk issuances in 2011, followed by Qatar (10.9%), the UAE (4.8%), and Saudi Arabia (3.2%). As at end-1H12, Malaysia’s market share was 68.2%, followed by Saudi Arabia (11.1%), the UAE (6.4%) and Indonesia (5.9%).

• The sukuk market has witnessed various currency issuances over the past decade, giving a wide range of exposures to sukuk investors. For large scale international issuances, the US dollar remains the most popular in attracting liquidity given its reliance in the global fi nancial markets. Sukuk principles used have also evolved from plain Ijarah and Murabahah structures to Musharakah partnerships, as well as convertible and exchangeable trusts.

• In 2011, sovereign and quasi-sovereign issuers accounted for 77.7% of the primary market, while corporates took the remaining 22.3%. As at end-1H12, this ratio dropped to 62.3% as corporates take advantage of the pent-up demand and lower yields.

• The huge growth of sukuk witnessed in 2011 was driven by the declining yields for both corporate and sovereign issuances on the back of the Middle Eastern political tensions, which in turn led to a record year for Middle Eastern sukuk issuances, and the uncertainty in the global economy due to both the European sovereign debt crisis, which seemingly unravelled during 2011, and the fears of another recession in the US and other developed markets.

• The sectors driving sukuk issuances during the 1Q12 include both government and transportation, accounting for 44.7% and 34.8%, respectively, while there have been a considerable number of issuances in the GCC and Malaysia from the power and utilities sector.

Sukuk Issuance Trend

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2005 2006 2007 2008 2009 2010 2011 1H12

USD

milli

on

Source: Zawya, IFIS, Bloomberg, KFHR

Sukuk Outstanding by Country Breakdown

Source: IFIS, Bloomberg, Zawya, KFHR* Sukuk represent an equal and undivided share of ownership in tangible assets, usufruct and services or ownership in investment activity

Total OutstandingUSD210.8 billionAs at end-1H12

Malaysia61.4%

SaudiArabia11.9%

UAE9.9%

Qatar5.8%

Indonesia4.4%

Pakistan2.8%

Others3.8%

Issuance to Date: USD14.1 billionStructure (2011): Ijarah 94.6%, Mudharabah 4.9%, Others 0.5%Currency (2011): Local 61.5%, Foreign 38.6% (USD)Sector (2011): Government 95.5%, Financial Services 4.5%Type of Issuers (2011): Sovereign 95.5%, Corporate 4.5%

Issuance to Date: USD234.1 billionStructure (2011): Murabahah 61.5%, Musharakah 15.7%, Mudharabah 8.5%, Ijarah 8.0% and Others 6.3%Currency (2011): Local 96.6%, Foreign 3.4% (USD & RMB)Sector (2011): Government 66.9%, Power & Utilities 11.0%, Construction, 5.9% Others 16.3%Type of Issuers (2011): Sovereign 71.9%, Quasi-Sovereign 8.2%, Corporate 19.9%

Issuance to Date: USD25.7 billionStructure (2011): Combination 45.8%, Wakalah 27.1%, Mudharabah 17.4%, Murabahah 9.7%Currency (2011): Local 72.9%, Foreign 27.1% (USD)Sector (2011): Oil & Gas 53.6%, Financial Services 36.8%, Construction 9.7%Type of Issuers (2011): Sovereign 27.1%, Corporate 72.9%

Issuance to Date: USD6.9 billionStructure (2011): Ijarah 100.0%Currency (2011): Local 100.0%Sector (2011): Government 100.0%Type of Issuers (2011): Sovereign 100.0%

Issuance to Date: USD13.0 billionStructure (2011): Ijarah 97.7%, Wakalah 2.3%Currency (2011): Local 97.7%, Foreign 2.3% (USD)Sector (2011): Government 97.7%, Construction 2.3%Type of Issuers (2011): Sovereign 97.7%, Corporate 2.3%

Issuance to Date: USD41.2 billionStructure (2011): Ijarah 47.4%, Wakalah 15.9%, Murabahah 12.2%, Combination 12.2, Musharakah 12.2%Currency (2011): Local 25.3%, Foreign 74.7% (USD)Sector (2011): Financial Services 62.4%, 37.6%Type of Issuers (2011): Quasi-Sovereign 25.3%, Corporate 74.7%

20 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

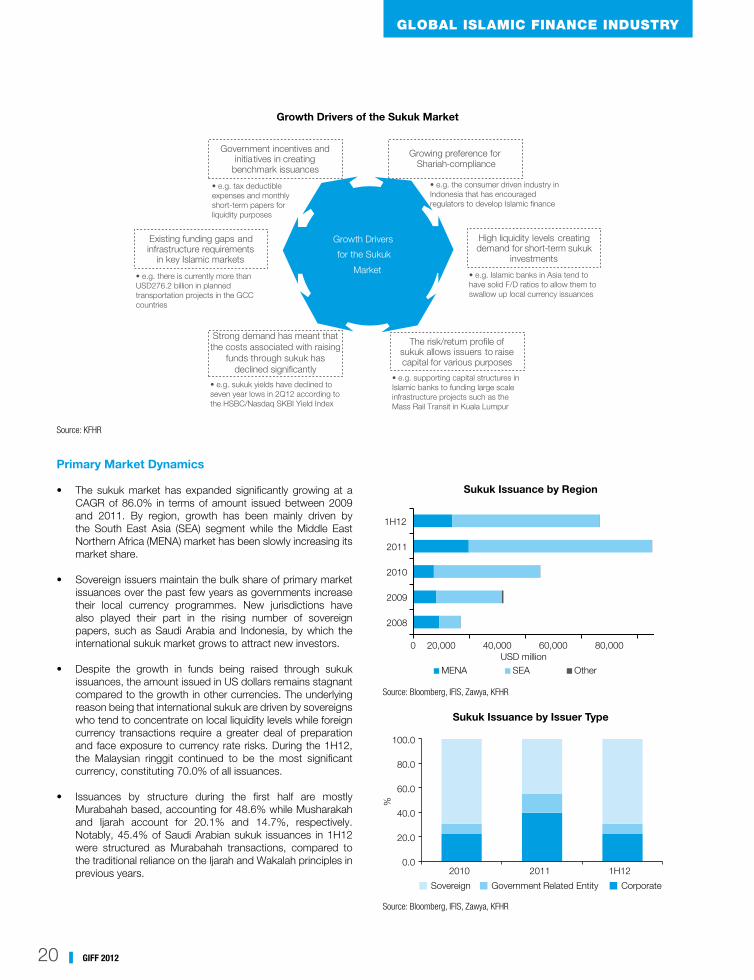

Growth Drivers of the Sukuk Market

Growing preference for Shariah-compliance

Growth Drivers

for the Sukuk

Market

Existing funding gaps and infrastructure requirements

in key Islamic markets

The risk/return profile of sukuk allows issuers to raise capital for various purposes

High liquidity levels creating demand for short-term sukuk

investments

Government incentives and initiatives in creating

benchmark issuances

• e.g. tax deductible expenses and monthly short-term papers for liquidity purposes

• e.g. the consumer driven industry in Indonesia that has encouraged regulators to develop Islamic finance

• e.g. Islamic banks in Asia tend to have solid F/D ratios to allow them to swallow up local currency issuances

• e.g. supporting capital structures in Islamic banks to funding large scale infrastructure projects such as the Mass Rail Transit in Kuala Lumpur

• e.g. sukuk yields have declined to seven year lows in 2Q12 according to the HSBC/Nasdaq SKBI Yield Index

• e.g. there is currently more than USD276.2 billion in planned transportation projects in the GCC countries

Strong demand has meant that the costs associated with raising

funds through sukuk has declined significantly

Source: KFHR

Primary Market Dynamics

• The sukuk market has expanded signifi cantly growing at a CAGR of 86.0% in terms of amount issued between 2009 and 2011. By region, growth has been mainly driven by the South East Asia (SEA) segment while the Middle East Northern Africa (MENA) market has been slowly increasing its market share.

• Sovereign issuers maintain the bulk share of primary market issuances over the past few years as governments increase their local currency programmes. New jurisdictions have also played their part in the rising number of sovereign papers, such as Saudi Arabia and Indonesia, by which the international sukuk market grows to attract new investors.

• Despite the growth in funds being raised through sukuk issuances, the amount issued in US dollars remains stagnant compared to the growth in other currencies. The underlying reason being that international sukuk are driven by sovereigns who tend to concentrate on local liquidity levels while foreign currency transactions require a greater deal of preparation and face exposure to currency rate risks. During the 1H12, the Malaysian ringgit continued to be the most signifi cant currency, constituting 70.0% of all issuances.

• Issuances by structure during the fi rst half are mostly Murabahah based, accounting for 48.6% while Musharakah and Ijarah account for 20.1% and 14.7%, respectively. Notably, 45.4% of Saudi Arabian sukuk issuances in 1H12 were structured as Murabahah transactions, compared to the traditional reliance on the Ijarah and Wakalah principles in previous years.

Sukuk Issuance by Region

0 20,000 40,000 60,000 80,000

2008

2009

2010

2011

1H12

USD millionMENA SEA Other

Source: Bloomberg, IFIS, Zawya, KFHR

Sukuk Issuance by Issuer Type

0.0

20.0

40.0

60.0

80.0

100.0

2010 2011 1H12

Sovereign Government Related Entity Corporate

%

Source: Bloomberg, IFIS, Zawya, KFHR

21GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Sukuk Issuance by Currency

0

10

20

30

40

50

60

70

80

90

2005 2006 2007 2008 2009 2010 2011 1H12

US

D b

illion

Other MYR USD

Source: Bloomberg, IFIS, Zawya, KFHR

Sukuk Issuance by Structure (2011-1H12)

Wakalah6.4%

Bai' Inah0.4%

Ijarah11.5%

Mudharabah4.3%

Murabahah54.8%

Salam0.4%

Musharakah18.0%

Combination1.1%

BBA3.1%

Source: Bloomberg, IFIS, Zawya, KFHR

• During the 1H12 there have been a number of notable sukuk. Amongst them are the fi rst sovereign issuance from Saudi Arabia by the General Authority of Civil Aviation (GACA), and the largest single issuance to-date by PLUS Berhad, a Malaysian highway toll operator.

Notable Sukuk Issuance

Issuer Structure Country CurrencyIssue Date

Issue Size (USD million)

Tenor (Years)

Sector

Abu Dhabi National Energy Company

Murabahah Malaysia MYR Mar-12 215.1 10 Power & Utilities

Emirates Islamic Bank Wakalah UAE USD Jan-12 500.0 5 Financial Services

General Authority of Civil Aviation

Murabahah Saudi Arabia SAR Jan-12 4,000.0 10 Transport

First Gulf Bank Wakalah UAE USD Jan-12 500.0 5 Financial Services

Majid Al Futtaim Wakalah UAE USD Feb-12 400.0 5 Real Estate

PLUS Berhad Musharakah Malaysia MYR Jan-12 9,728.1 5-27 Transport

Saudi Electric Ijarah Saudi Arabia USD Mar-12 500.0 5 Power & Utilities

Saudi British Bank Combination Saudi Arabia SAR Mar-12 400.0 5 Financial Services

Tamweel Wakalah UAE USD Jan-12 300.0 5 Financial Services

Khazanah Nasional Musharakah Malaysia USD Mar-12 357.8 7 Financial Services

Source: Bloomberg, IFIS, Zawya, KFHR

Secondary Market Dynamics

• Global outstanding sukuk reached USD210.8 billion as at end-1H12, up 18.3% from the USD178.2 billion at end-2011. The total amount outstanding has continuously advanced, even during the fi nancial crisis, and in recent years growth has accelerated due to the infl ux of new issuers and the growing amounts issued by sovereigns and central banks. Between 2006 and 2011, the secondary market has grown at a CAGR of 28.1%.

• The two main factors driving growth in the secondary market are:

o The rapid growth in new issuances which gives an immediate impact to outstanding fi gures

o The trend towards more short-term maturities means growth has accelerated over recent years

• Sukuk yields dropped by 81 basis points in 2011 to 3.991%, according to the HSBC/Nasdaq SKBI Yield Index. The Middle East uprisings and the amplifi cation of the European debt crisis sent investors rushing for the safety of fi xed income instruments which in turn pushed up sukuk prices. Despite these turbulent times, sukuk turned out to be a viable investment with demand for high quality Shariah-compliant papers remaining strong.

22 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

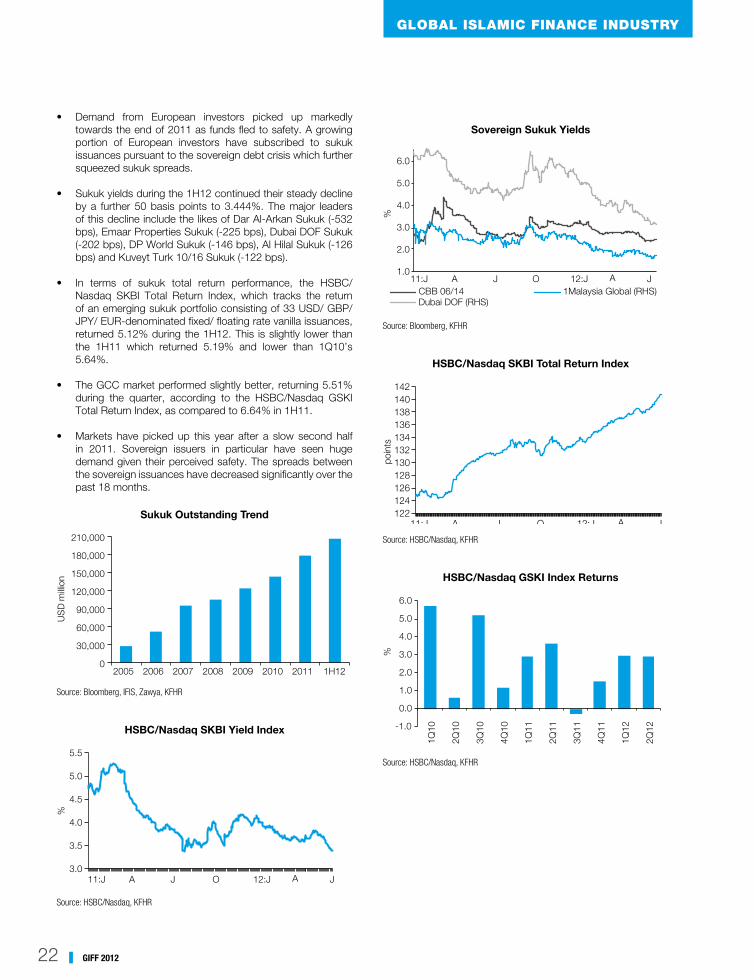

• Demand from European investors picked up markedly towards the end of 2011 as funds fl ed to safety. A growing portion of European investors have subscribed to sukuk issuances pursuant to the sovereign debt crisis which further squeezed sukuk spreads.

• Sukuk yields during the 1H12 continued their steady decline by a further 50 basis points to 3.444%. The major leaders of this decline include the likes of Dar Al-Arkan Sukuk (-532 bps), Emaar Properties Sukuk (-225 bps), Dubai DOF Sukuk (-202 bps), DP World Sukuk (-146 bps), Al Hilal Sukuk (-126 bps) and Kuveyt Turk 10/16 Sukuk (-122 bps).

• In terms of sukuk total return performance, the HSBC/Nasdaq SKBI Total Return Index, which tracks the return of an emerging sukuk portfolio consisting of 33 USD/ GBP/ JPY/ EUR-denominated fi xed/ fl oating rate vanilla issuances, returned 5.12% during the 1H12. This is slightly lower than the 1H11 which returned 5.19% and lower than 1Q10’s 5.64%.

• The GCC market performed slightly better, returning 5.51% during the quarter, according to the HSBC/Nasdaq GSKI Total Return Index, as compared to 6.64% in 1H11.

• Markets have picked up this year after a slow second half in 2011. Sovereign issuers in particular have seen huge demand given their perceived safety. The spreads between the sovereign issuances have decreased signifi cantly over the past 18 months.

Sukuk Outstanding Trend

0

30,000

60,000

90,000

120,000

150,000

180,000

210,000

2005 2006 2007 2008 2009 2010 2011 1H12

US

D m

illion

Source: Bloomberg, IFIS, Zawya, KFHR

HSBC/Nasdaq SKBI Yield Index

11:J A AJ JO 12:J3.0

3.5

4.0

4.5

5.0

5.5

%

Source: HSBC/Nasdaq, KFHR

Sovereign Sukuk Yields

11:J A AJ JO 12:J1.0

2.0

3.0

4.0

5.0

6.0

%

CBB 06/14 1Malaysia Global (RHS)Dubai DOF (RHS)

Source: Bloomberg, KFHR

HSBC/Nasdaq SKBI Total Return Index

11:J A AJ JO 12:J122124126128130132134136138140142

poin

ts

Source: HSBC/Nasdaq, KFHR

HSBC/Nasdaq GSKI Index Returns

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

%

Source: HSBC/Nasdaq, KFHR

23GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Outlook

• Having already grown by 40.1% y-o-y at the end-1H12, the sukuk market looks set to have another bright year ahead. The main drivers of growth continue to stem from the sovereign and quasi-sovereign issuers who constitute 77.7% of the primary market. The sukuk pipeline holds a number of potential sovereign issuances from the likes of Indonesia, Malaysia, South Africa, Mauritania, Pakistan, Sudan, the UAE, Nigeria and Turkey.

• In the scenario that the sovereign debt crisis in Europe hampers growth in the global economy, many different supply lines will be affected across sectors and asset classes, thereby possibly impacting corporates wishing to issue sukuk, as was the case in 2008 and 2009.

• In the event that the current situation is prolonged, sukuk yields currently indicate that it may well become cheaper for corporates to take the sukuk route and tap the liquid Islamic markets moving forward.

• The implementation of the Basel III requirements signals the strong probability that Islamic fi nancial institutions will be tapping the sukuk market over the coming years as they improve capital structures. Similarly the demand for highly rated papers will intensify as banks and other institutions beef up portfolios.

• Meanwhile the corporate sukuk issuers came out in force in 1H12 on the back of lower funding costs and signifi cant investor appetite. This trend looks set to continue as long as the market remains favourable over the coming months. Being part of the larger fi nancial system, the troubles in the conventional bond markets, especially in Europe, pose both a threat and an opportunity to the global sukuk market.

• Other factors supporting a 25.0%-30.0% growth forecast for this year include the following:

o The cumulative infrastructure projects and funding needs in both the GCC and Asian regions are expected to support the sukuk market in 2012. Infrastructure spending has been one of the key drivers or economic growth in the GCC over the past decade. In spite of some refocusing during the global economic crisis, the project pipeline is showing no signs of slowing down

o New IFIs as well as other types of issuers are expected to tap the sukuk market

o Increasing demand and popularity for Shariah-compliant products and structures post global fi nancial crisis will form a strong demand base for sukuk moving forward

o Initiatives taken by various jurisdictions in developing legislative and regulatory frameworks, as part of efforts to attract foreign investments, would allow these new players to explore the sukuk industry for the fi rst time

24 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

2.2.3 Islamic Funds

• The Islamic fund industry has developed rapidly over the last decade to become one of the key components of the Islamic fi nance industry. The fundamental principles of the Shariah have provided the basis for the creation of a new breed of investment vehicles designed for Shariah-compliant capital growth and wealth appreciation. Given the growing demand for Islamic investments amongst discerning customers, the range of Islamic funds has multiplied in terms of investing in different asset classes and has diversifi ed in terms of tailoring to the requirements of various investor types and categories.

• As the Islamic fi nance industry gains momentum across the globe and awareness of Shariah-compliant solutions amongst various population increases, Islamic funds have become increasingly retail driven. Furthermore the rising wealth in Muslim nations, especially in the emerging economies and oil-rich countries, has helped drive investible assets to new heights. As sovereigns embark on introducing Islamic fi nance in their respective jurisdictions, many have realised the need to create strategies for managing sovereign wealth in a Shariah-compliant way. This has led to further demand for Islamic investment solutions.

• Despite the global economic struggles and the sovereign debt crisis in Europe, Islamic funds have managed to grow their assets on the back of descent market performance, as well as experiencing a number of new funds raised. With the global equity indices underperforming, investors continue to search for alternative asset classes. In particular, commodity funds have been an attractive safe haven for a wide range of investors during the turbulent times.

• Islamic fund managers have been able to tap this demand for unconventional investments by marketing Islamic funds as viable alternative products. Islamic funds have consequently diversifi ed portfolios to invest in a range of asset classes from commodities such as palm oil and precious metals to green technology for energy production. This has been able to translate into attracting subscriptions from sophisticated investors from almost all regions.

Growth Drivers of Islamic Funds

Diverse product range

Increasing awareness

Strong demand for Shariah-

compliant products

Rising global wealth

Growing range of

investible asset

classes

Source: KFHR

25GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

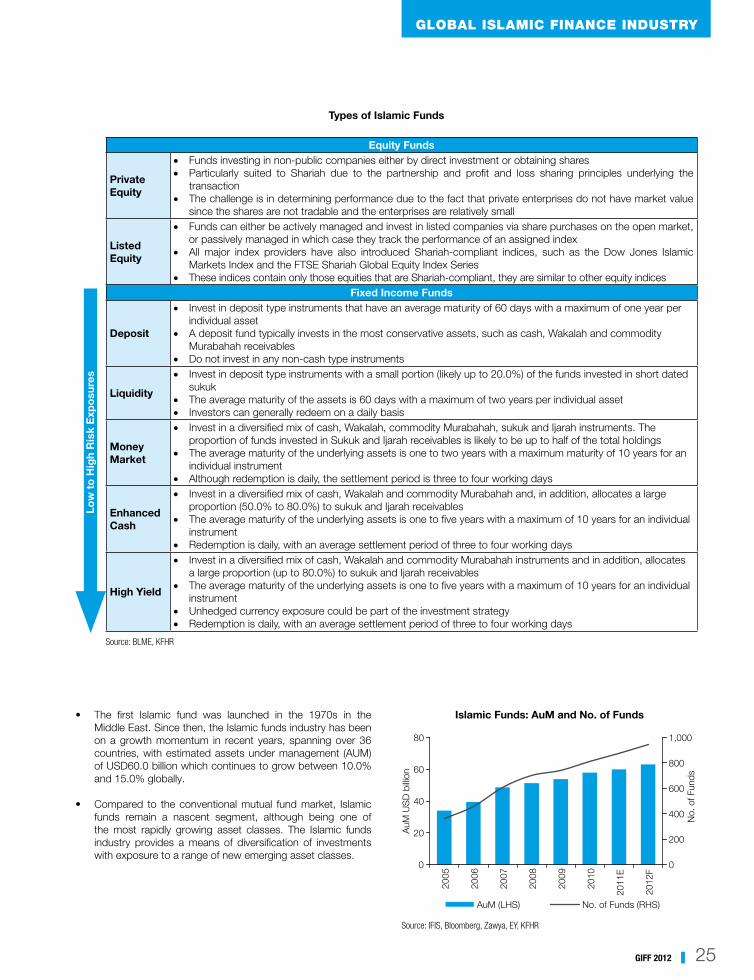

• The fi rst Islamic fund was launched in the 1970s in the Middle East. Since then, the Islamic funds industry has been on a growth momentum in recent years, spanning over 36 countries, with estimated assets under management (AUM) of USD60.0 billion which continues to grow between 10.0% and 15.0% globally.

• Compared to the conventional mutual fund market, Islamic funds remain a nascent segment, although being one of the most rapidly growing asset classes. The Islamic funds industry provides a means of diversifi cation of investments with exposure to a range of new emerging asset classes.

Islamic Funds: AuM and No. of Funds

0

200

400

600

800

1,000

0

20

40

60

80

2005

2006

2007

2008

2009

2010

2011

E

2012

F

No.

of F

unds

AuM

US

D b

illion

AuM (LHS) No. of Funds (RHS)

Source: IFIS, Bloomberg, Zawya, EY, KFHR

Low

to

Hig

h R

isk

Exp

osu

res

Types of Islamic Funds

Equity Funds

Private Equity

• Funds investing in non-public companies either by direct investment or obtaining shares• Particularly suited to Shariah due to the partnership and profi t and loss sharing principles underlying the

transaction• The challenge is in determining performance due to the fact that private enterprises do not have market value

since the shares are not tradable and the enterprises are relatively small

Listed Equity

• Funds can either be actively managed and invest in listed companies via share purchases on the open market, or passively managed in which case they track the performance of an assigned index

• All major index providers have also introduced Shariah-compliant indices, such as the Dow Jones Islamic Markets Index and the FTSE Shariah Global Equity Index Series

• These indices contain only those equities that are Shariah-compliant, they are similar to other equity indicesFixed Income Funds

Deposit

• Invest in deposit type instruments that have an average maturity of 60 days with a maximum of one year per individual asset

• A deposit fund typically invests in the most conservative assets, such as cash, Wakalah and commodity Murabahah receivables

• Do not invest in any non-cash type instruments

Liquidity

• Invest in deposit type instruments with a small portion (likely up to 20.0%) of the funds invested in short dated sukuk

• The average maturity of the assets is 60 days with a maximum of two years per individual asset• Investors can generally redeem on a daily basis

Money Market

• Invest in a diversifi ed mix of cash, Wakalah, commodity Murabahah, sukuk and Ijarah instruments. The proportion of funds invested in Sukuk and Ijarah receivables is likely to be up to half of the total holdings

• The average maturity of the underlying assets is one to two years with a maximum maturity of 10 years for an individual instrument

• Although redemption is daily, the settlement period is three to four working days

Enhanced Cash

• Invest in a diversifi ed mix of cash, Wakalah and commodity Murabahah and, in addition, allocates a large proportion (50.0% to 80.0%) to sukuk and Ijarah receivables

• The average maturity of the underlying assets is one to fi ve years with a maximum of 10 years for an individual instrument

• Redemption is daily, with an average settlement period of three to four working days

High Yield

• Invest in a diversifi ed mix of cash, Wakalah and commodity Murabahah instruments and in addition, allocates a large proportion (up to 80.0%) to sukuk and Ijarah receivables

• The average maturity of the underlying assets is one to fi ve years with a maximum of 10 years for an individual instrument

• Unhedged currency exposure could be part of the investment strategy• Redemption is daily, with an average settlement period of three to four working days

Source: BLME, KFHR

26 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Specifi c Requirements of Islamic Funds

Shariah-compliant Investment

Shariah Audit

Appointment of a Shariah Board

Asset Owners

• For Shariah funds, screening is necessary to ensure compliance with the Shariah framework

• Preliminary screening will eliminate companies performing Shariah non-compliant activities and industries

• Second level of screening will be based on the companies’ fi nancials where companies with fi nancial ratios exceeding the acceptable levels will be removed

• Shariah audit must be conducted regularly to ensure that the fund is constantly compliant with Shariah principles

• Shariah audit is usually conducted by the Shariah board/committee, or any other external party with strong Shariah knowledge

• According to the Accounting and Auditing Organisation for Islamic Financial Institutions’ (AAOIFI) standards, it is necessary for Shariah-compliant funds to appoint at least three Shariah scholars to make up the respective Shariah board

• The responsibility of the scholars is to issue verdicts related to the permissibility of the funds investment structures

• The custodian of the assets must also adhere to Shariah principles

Source: KFHR

Dynamics

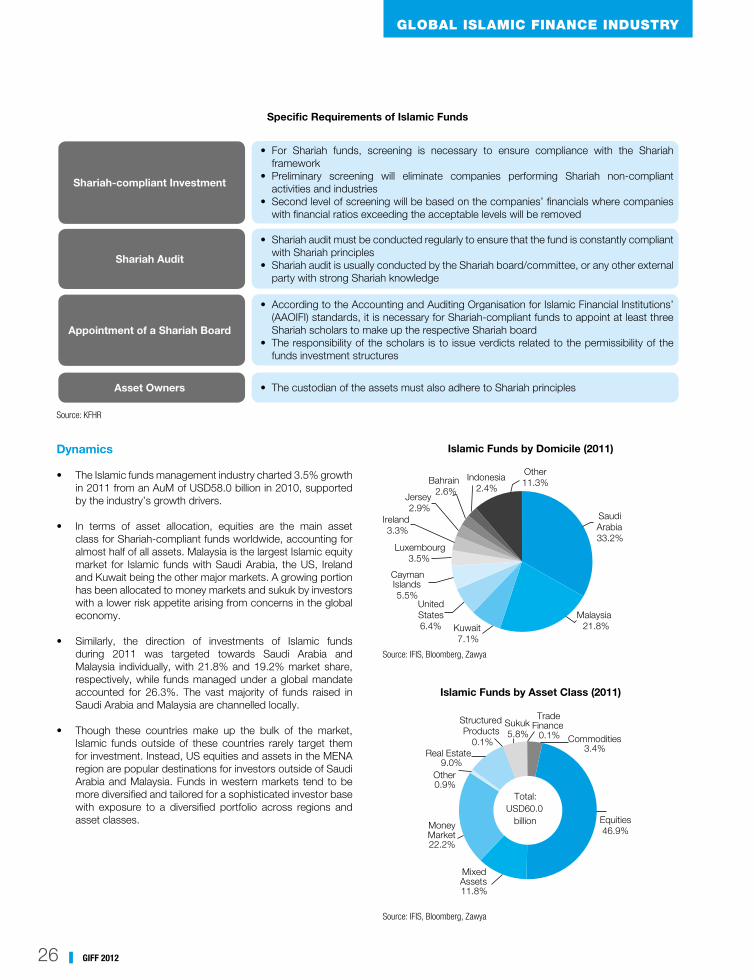

• The Islamic funds management industry charted 3.5% growth in 2011 from an AuM of USD58.0 billion in 2010, supported by the industry’s growth drivers.

• In terms of asset allocation, equities are the main asset class for Shariah-compliant funds worldwide, accounting for almost half of all assets. Malaysia is the largest Islamic equity market for Islamic funds with Saudi Arabia, the US, Ireland and Kuwait being the other major markets. A growing portion has been allocated to money markets and sukuk by investors with a lower risk appetite arising from concerns in the global economy.

• Similarly, the direction of investments of Islamic funds during 2011 was targeted towards Saudi Arabia and Malaysia individually, with 21.8% and 19.2% market share, respectively, while funds managed under a global mandate accounted for 26.3%. The vast majority of funds raised in Saudi Arabia and Malaysia are channelled locally.

• Though these countries make up the bulk of the market, Islamic funds outside of these countries rarely target them for investment. Instead, US equities and assets in the MENA region are popular destinations for investors outside of Saudi Arabia and Malaysia. Funds in western markets tend to be more diversifi ed and tailored for a sophisticated investor base with exposure to a diversifi ed portfolio across regions and asset classes.

Islamic Funds by Domicile (2011)

Saudi Arabia33.2%

Malaysia21.8%Kuwait

7.1%

United States6.4%

Cayman Islands5.5%

Luxembourg3.5%

Ireland3.3%

Jersey2.9%

Bahrain2.6%

Indonesia2.4%

Other11.3%

Source: IFIS, Bloomberg, Zawya

Islamic Funds by Asset Class (2011)

Commodities3.4%

Equities46.9%

Mixed Assets11.8%

Money Market22.2%

Other0.9%

Real Estate9.0%

Structured Products

0.1%

Sukuk5.8%

Trade Finance

0.1%

Total: USD60.0

billion

Source: IFIS, Bloomberg, Zawya

27GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

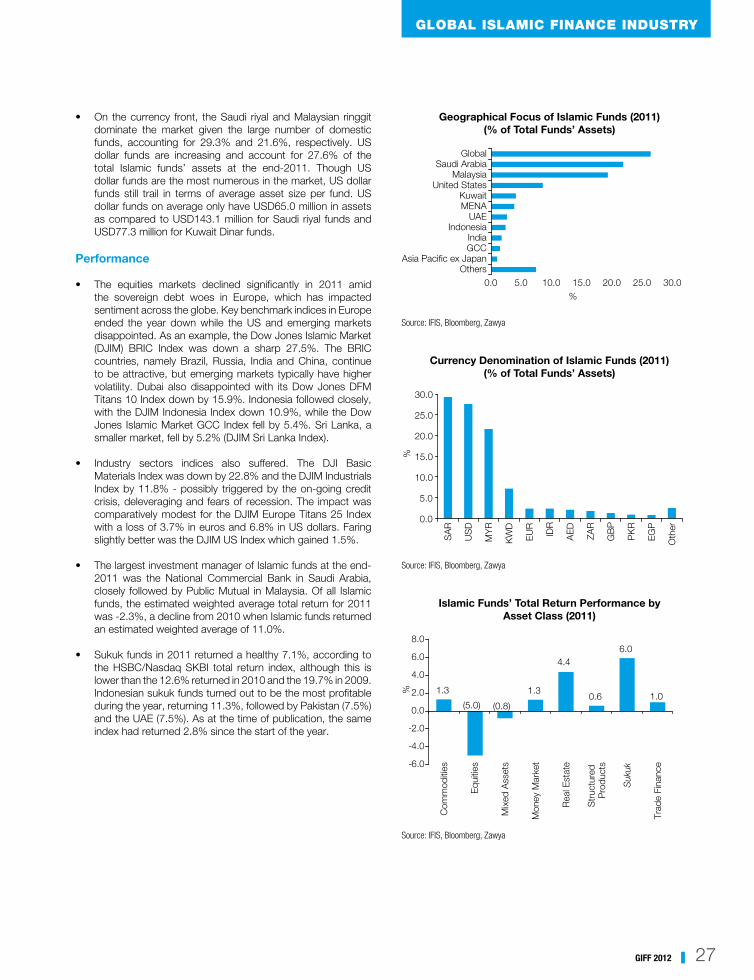

• On the currency front, the Saudi riyal and Malaysian ringgit dominate the market given the large number of domestic funds, accounting for 29.3% and 21.6%, respectively. US dollar funds are increasing and account for 27.6% of the total Islamic funds’ assets at the end-2011. Though US dollar funds are the most numerous in the market, US dollar funds still trail in terms of average asset size per fund. US dollar funds on average only have USD65.0 million in assets as compared to USD143.1 million for Saudi riyal funds and USD77.3 million for Kuwait Dinar funds.

Performance

• The equities markets declined signifi cantly in 2011 amid the sovereign debt woes in Europe, which has impacted sentiment across the globe. Key benchmark indices in Europe ended the year down while the US and emerging markets disappointed. As an example, the Dow Jones Islamic Market (DJIM) BRIC Index was down a sharp 27.5%. The BRIC countries, namely Brazil, Russia, India and China, continue to be attractive, but emerging markets typically have higher volatility. Dubai also disappointed with its Dow Jones DFM Titans 10 Index down by 15.9%. Indonesia followed closely, with the DJIM Indonesia Index down 10.9%, while the Dow Jones Islamic Market GCC Index fell by 5.4%. Sri Lanka, a smaller market, fell by 5.2% (DJIM Sri Lanka Index).

• Industry sectors indices also suffered. The DJI Basic Materials Index was down by 22.8% and the DJIM Industrials Index by 11.8% - possibly triggered by the on-going credit crisis, deleveraging and fears of recession. The impact was comparatively modest for the DJIM Europe Titans 25 Index with a loss of 3.7% in euros and 6.8% in US dollars. Faring slightly better was the DJIM US Index which gained 1.5%.

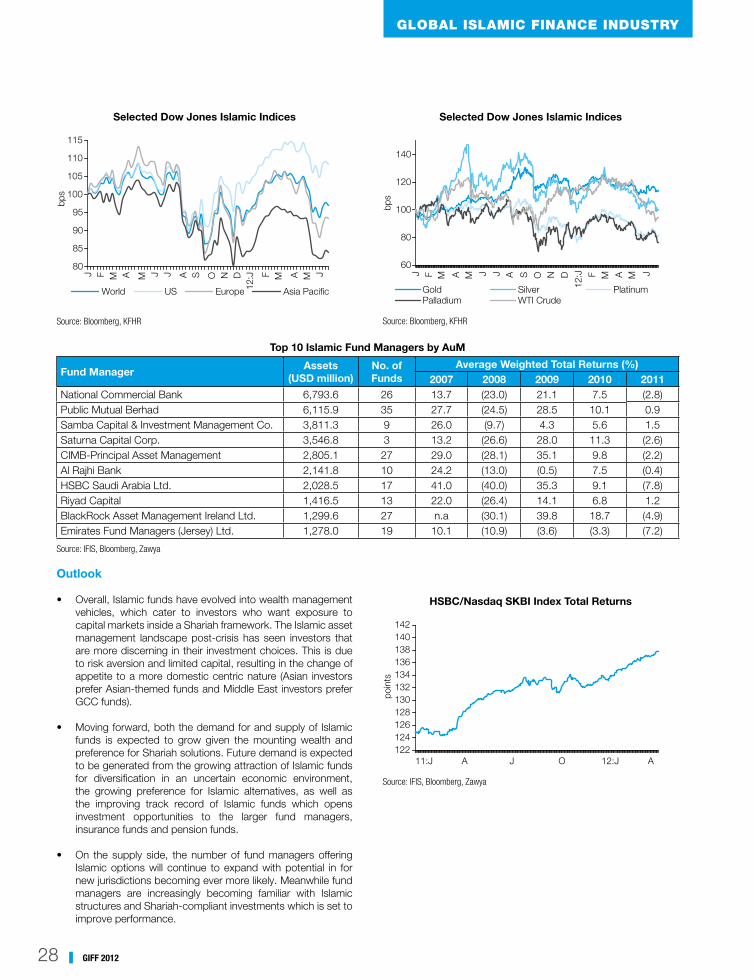

• The largest investment manager of Islamic funds at the end-2011 was the National Commercial Bank in Saudi Arabia, closely followed by Public Mutual in Malaysia. Of all Islamic funds, the estimated weighted average total return for 2011 was -2.3%, a decline from 2010 when Islamic funds returned an estimated weighted average of 11.0%.

• Sukuk funds in 2011 returned a healthy 7.1%, according to the HSBC/Nasdaq SKBI total return index, although this is lower than the 12.6% returned in 2010 and the 19.7% in 2009. Indonesian sukuk funds turned out to be the most profi table during the year, returning 11.3%, followed by Pakistan (7.5%) and the UAE (7.5%). As at the time of publication, the same index had returned 2.8% since the start of the year.

Geographical Focus of Islamic Funds (2011)(% of Total Funds’ Assets)

GlobalSaudi Arabia

MalaysiaUnited States

KuwaitMENA

UAEIndonesia

IndiaGCC

Asia Pacific ex JapanOthers

0.0 5.0 10.0 15.0 20.0 25.0 30.0%

Source: IFIS, Bloomberg, Zawya

Currency Denomination of Islamic Funds (2011)(% of Total Funds’ Assets)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

SA

R

US

D

MY

R

KW

D

EU

R

IDR

AE

D

ZAR

GB

P

PK

R

EG

P

Oth

er

%

Source: IFIS, Bloomberg, Zawya

Islamic Funds’ Total Return Performance by Asset Class (2011)

1.3

(5.0) (0.8)

1.3

4.4

0.6

6.0

1.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Com

mod

ities

Equ

ities

Mix

ed A

sset

s

Mon

ey M

arke

t

Rea

l Est

ate

Str

uctu

red

Pro

duct

s

Suk

uk

Trad

e Fi

nanc

e

%

Source: IFIS, Bloomberg, Zawya

28 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Selected Dow Jones Islamic Indices

80

85

90

95

100

105

110

115

J F M A M J J A S O N D12

:J F M A M J

bps

World US Europe Asia Pacific

Source: Bloomberg, KFHR

Selected Dow Jones Islamic Indices

60

80

100

120

140

J F M A M J J A S O N D

12:J F M A M J

bps

Gold Silver PlatinumPalladium WTI Crude

Source: Bloomberg, KFHR

Top 10 Islamic Fund Managers by AuM

Fund ManagerAssets

(USD million)No. of Funds

Average Weighted Total Returns (%)2007 2008 2009 2010 2011

National Commercial Bank 6,793.6 26 13.7 (23.0) 21.1 7.5 (2.8)Public Mutual Berhad 6,115.9 35 27.7 (24.5) 28.5 10.1 0.9Samba Capital & Investment Management Co. 3,811.3 9 26.0 (9.7) 4.3 5.6 1.5Saturna Capital Corp. 3,546.8 3 13.2 (26.6) 28.0 11.3 (2.6)CIMB-Principal Asset Management 2,805.1 27 29.0 (28.1) 35.1 9.8 (2.2)Al Rajhi Bank 2,141.8 10 24.2 (13.0) (0.5) 7.5 (0.4)HSBC Saudi Arabia Ltd. 2,028.5 17 41.0 (40.0) 35.3 9.1 (7.8)Riyad Capital 1,416.5 13 22.0 (26.4) 14.1 6.8 1.2BlackRock Asset Management Ireland Ltd. 1,299.6 27 n.a (30.1) 39.8 18.7 (4.9)Emirates Fund Managers (Jersey) Ltd. 1,278.0 19 10.1 (10.9) (3.6) (3.3) (7.2)

Source: IFIS, Bloomberg, Zawya

Outlook

• Overall, Islamic funds have evolved into wealth management vehicles, which cater to investors who want exposure to capital markets inside a Shariah framework. The Islamic asset management landscape post-crisis has seen investors that are more discerning in their investment choices. This is due to risk aversion and limited capital, resulting in the change of appetite to a more domestic centric nature (Asian investors prefer Asian-themed funds and Middle East investors prefer GCC funds).

• Moving forward, both the demand for and supply of Islamic funds is expected to grow given the mounting wealth and preference for Shariah solutions. Future demand is expected to be generated from the growing attraction of Islamic funds for diversifi cation in an uncertain economic environment, the growing preference for Islamic alternatives, as well as the improving track record of Islamic funds which opens investment opportunities to the larger fund managers, insurance funds and pension funds.

• On the supply side, the number of fund managers offering Islamic options will continue to expand with potential in for new jurisdictions becoming ever more likely. Meanwhile fund managers are increasingly becoming familiar with Islamic structures and Shariah-compliant investments which is set to improve performance.

HSBC/Nasdaq SKBI Index Total Returns

11:J A 12:J AJ O122124126128130132134136138140142

poin

ts

Source: IFIS, Bloomberg, Zawya

29GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

HNWI Distribution by Region

3.1 2.6 3 3.1 3.2

3.3 2.7 3.1 3.4 3.4

2.8 2.4 3 3.3 3.4

0.4 0.4 0.5 0.5 0.50.4 0.4 0.4 0.4 0.50.1 0.1 0.1 0.1 0.1

0.0

20.0

40.0

60.0

80.0

100.0

2007 2008 2009 2010 2011

%

Africa Middle East Latin AmericaAsia-Pacific North America Europe

Source: IFIS, Bloomberg, Zawya

Personal Income in the Muslim World: GDP per Capita (PPP) (USD)

0 50,000 100,000 150,000 200,000

JordanEgypt

AlgeriaTunisia

IranTurkey

MalaysiaSaudi Arabia

OmanBahrainKuwait

UAEBruneiQatar

USD

Source: IFIS, Bloomberg, Zawya

30 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Factors Supporting Takaful Growth

There are a number of drivers behind this growth but one that is becoming increasingly important is regulatory support through appropriate amendments in legislature to provide a level playing fi eld with conventional insurance companies. Other factors fuelling the growth of takaful worldwide are:

• Growing demand for Shariah-compliant products. Demand rather than supply is driving the development of takaful products and services. Increasingly, existing Islamic banking customers are looking for an ever-broader range of Islamic fi nancial instruments. Study by Standard and Poor’s, in the GCC and parts of Asia, where Islamic fi nance has been far more entrenched, it is estimated that 20.0% of banking customers spontaneously choose an Islamic fi nancial product over a conventional one with a similar risk-return profi le.

• Abundant liquidity. The growth of the global takaful industry is expected to be closely related to the increasing liquidity of oil-producing nations. Sustained high oil prices over the years contributed to the growing class of affl uent individuals. This has encouraged this new class to give more thought to other aspects like savings, investment and protection in the form of takaful which conforms to the belief of Muslims.

• Increasing levels of foreign direct investment. Increasing levels of foreign direct investment, particularly in the infrastructure and real estate sectors in the GCC region, are expected to contribute to higher premiums/contributions written in those countries. Nevertheless, the takaful industry will really take off when governments use takaful to cover their major developments and infrastructure projects. Currently the takaful industry is dominated by retail sales to individuals but it will have to become a product for corporates to really gain scale.

2.2.4 Takaful

Introduction & Overview

Takaful or Islamic insurance is based on the principle of cooperation (ta’awun) and donation (tabarru’) whereby the risk associated with it is shared among a group of people voluntarily. It helps to reduce the fi nancial burden of the individual by transferring it to the group and helps foster a spirit of cooperation/mutual help among the group members. Unlike conventional insurance, the relationship between the takaful company and the participants (policyholders) is independent i.e. funds are distinguished between that owned by the takaful company, which only acts as the manager of participants’ funds, and the policyholders’ funds, which are used to indemnify policyholders. Through this business model, most takaful companies benefi t from either management fees, return on investments or a mixture of both.

Presently, the takaful markets are highly concentrated across the Muslim countries like Malaysia and the GCC. However, the industry’s continued growth trend as well as its resilience during the global fi nancial crisis have driven the rise of takaful companies in non-Muslim majority countries, particularly in Africa and Europe.

The modern Islamic insurance practice as witnessed today was fi rst seen when the Islamic Insurance Companies Ltd was established in Sudan in the year 1979. Based on latest available statistics, the number of Islamic insurance companies or takaful companies (TCs) has grown from 113 TCs in 2008 to 195 TCs in year 2010. Today, takaful products are available in more than 30 countries with the number expected to grow further in the near future.

Number of Takaful Companies in 2010

GCC, 77

Far East, 40

Africa, 32

Middle East (Non Arab), 18

East Indian Sub-

Continent, 12

Levant, 9 Others, 7

Total: 195 operators

Source: World Islamic Insurance Directory 2012

31GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Key Success Factors for Takaful Companies

Source: KFHR

Shariah compliance

Pricing

Dis

tribu

tion

chan

nel

Innovative

products

Rob

ust

regu

lato

ry

fram

ewor

k

Custom

er

service

Treat Shariah compliance as an end-to-end process

Improvise on thedistribution channel

Provide quality customer services

Providing clear operating environment & confi dence to market

participants

Develop need-basedand innovative takaful

products

Competitive product pricing

Resiliency of takaful

companies

• Growth of retakaful capacity. International re-insurers namely Swiss Re, Hannover Re, Tokio Marine and Converium have entered the retakaful business in several jurisdictions like Malaysia, Bahrain and the Dubai International Financial Centre. At the moment there are around 30 retakaful companies in jurisdiction such as Bahamas, Bahrain, Egypt, Indonesia, Iran, Kuwait, Malaysia, Qatar, Saudi Arabia, Sudan, Tunisia and the UAE.

• Growth of high quality sukuk papers for takaful companies to invest in. The growth of the global sukuk market is expected to become a key supporting factor for the strong growth of takaful and retakaful industries. Sukuk are increasingly becoming an important investment avenue for the takaful industry. Issuance of longer-tenured sukuk will match the investment and risk management needs of the takaful industry which usually has large long-term liabilities.

• Increased awareness amongst consumers. Today, Muslims customers are more aware of the alternative product to conventional insurance. This can be attributed to the

increase in the number of Islamic fi nance courses around the globe and effort by the market players particularly the regulators in promoting Islamic fi nance.

• A more effi cient distribution channel of takaful products. The strategic cooperation between takaful companies and other fi nancial institutions such as the banks has helped to spread takaful products at a faster rate. The bancatakaful products helps the takaful companies to leverage the customer base of other fi nancial institution thus increases the takaful penetration rate.

• Growth in other fi nancing products such as housing fi nancing which leads to increase in housing takaful. There is likely to be a domino effect when other Islamic fi nancial products are being introduced. For example, the introduction of Islamic mortgage facility would eventually require the support of Shariah-compliant insurance (takaful) product. Similar impact is expected to occur for other Islamic fi nancial products e.g. Shariah-compliant auto-fi nancing.

32 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Performance of the Takaful Industry

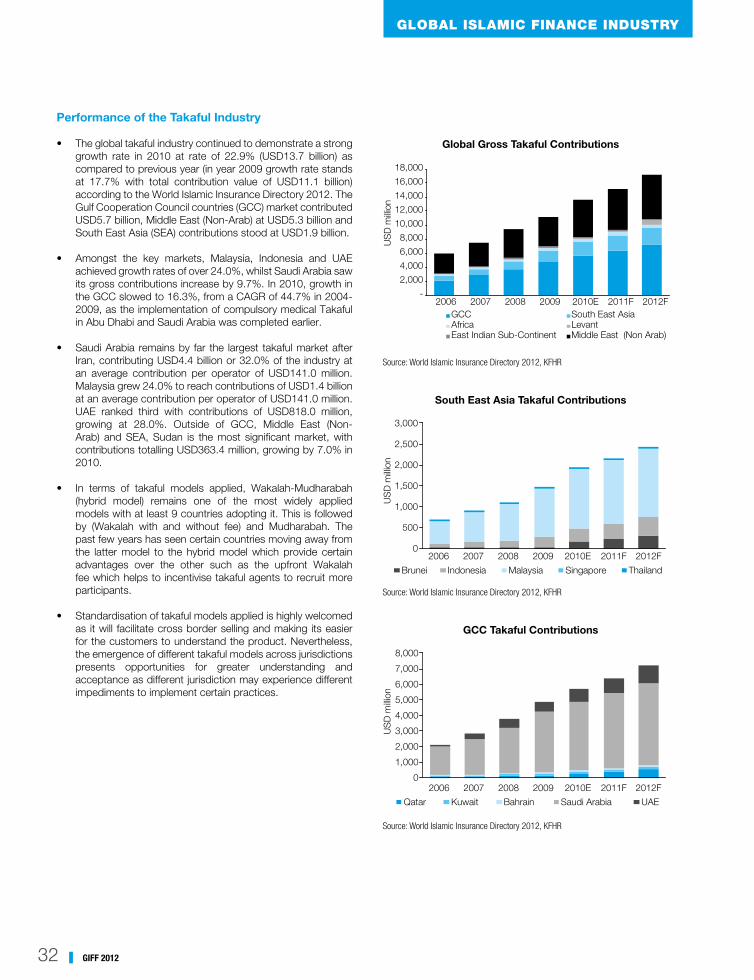

• The global takaful industry continued to demonstrate a strong growth rate in 2010 at rate of 22.9% (USD13.7 billion) as compared to previous year (in year 2009 growth rate stands at 17.7% with total contribution value of USD11.1 billion) according to the World Islamic Insurance Directory 2012. The Gulf Cooperation Council countries (GCC) market contributed USD5.7 billion, Middle East (Non-Arab) at USD5.3 billion and South East Asia (SEA) contributions stood at USD1.9 billion.

• Amongst the key markets, Malaysia, Indonesia and UAE achieved growth rates of over 24.0%, whilst Saudi Arabia saw its gross contributions increase by 9.7%. In 2010, growth in the GCC slowed to 16.3%, from a CAGR of 44.7% in 2004-2009, as the implementation of compulsory medical Takaful in Abu Dhabi and Saudi Arabia was completed earlier.

• Saudi Arabia remains by far the largest takaful market after Iran, contributing USD4.4 billion or 32.0% of the industry at an average contribution per operator of USD141.0 million. Malaysia grew 24.0% to reach contributions of USD1.4 billion at an average contribution per operator of USD141.0 million. UAE ranked third with contributions of USD818.0 million, growing at 28.0%. Outside of GCC, Middle East (Non-Arab) and SEA, Sudan is the most signifi cant market, with contributions totalling USD363.4 million, growing by 7.0% in 2010.

• In terms of takaful models applied, Wakalah-Mudharabah (hybrid model) remains one of the most widely applied models with at least 9 countries adopting it. This is followed by (Wakalah with and without fee) and Mudharabah. The past few years has seen certain countries moving away from the latter model to the hybrid model which provide certain advantages over the other such as the upfront Wakalah fee which helps to incentivise takaful agents to recruit more participants.

• Standardisation of takaful models applied is highly welcomed as it will facilitate cross border selling and making its easier for the customers to understand the product. Nevertheless, the emergence of different takaful models across jurisdictions presents opportunities for greater understanding and acceptance as different jurisdiction may experience different impediments to implement certain practices.

Global Gross Takaful Contributions

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2006 2007 2008 2009 2010E 2011F 2012F

US

D m

illion

GCC South East AsiaAfrica LevantEast Indian Sub-Continent Middle East (Non Arab)

Source: World Islamic Insurance Directory 2012, KFHR

South East Asia Takaful Contributions

0

500

1,000

1,500

2,000

2,500

3,000

2006 2007 2008 2009 2010E 2011F 2012F

US

D m

illion

Brunei Indonesia Malaysia Singapore Thailand

Source: World Islamic Insurance Directory 2012, KFHR

GCC Takaful Contributions

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006 2007 2008 2009 2010E 2011F 2012F

US

D m

illion

Qatar Kuwait Bahrain Saudi Arabia UAE

Source: World Islamic Insurance Directory 2012, KFHR

33GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Takaful Business Models Practiced by Various Countries

Country

Model

Mudharabah^

Wakalah (with or without incentive fee)^^

Wakalah - Mudharabah(Hybrid)^^^

Wakalah with Waqf

Others

Bahrain • • Bangladesh • Brunei • Egypt • Luxembourg • Malaysia • • • • Pakistan • • Qatar • Saudi Arabia* • • •Singapore • South Africa & other African countries • • Sri Lanka • UAE • • United Kingdom •

Source: Milliman, takaful companies, KFHRNote: ^ There has been a gradual move away from this model to a hybrid model especially in Malaysia but legacy business remains on this model^^ Primarily used for protection products such as term takaful^^^ Primarily used for saving products such as investment-linked* Uses the cooperative model

Global Takaful Gross Contribution Income by Class 2010E

SouthEast Asia

TotalEast IndianSub-continent

0.010.020.030.040.050.060.070.080.090.0

100.0

Iran GCC &Levant

%

Family & Medical Marine & Aviation Property & Accident Motor

Source: World Islamic Insurance Directory 2012, KFHR

Takaful/Insurance Companies Comparative Indices

2008 2009 2010 2011 2012-20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

%

TKFL Index MSCI World InsuranceBloomberg European 500 Insurance

Source: Bloomberg, KFHR

34 GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

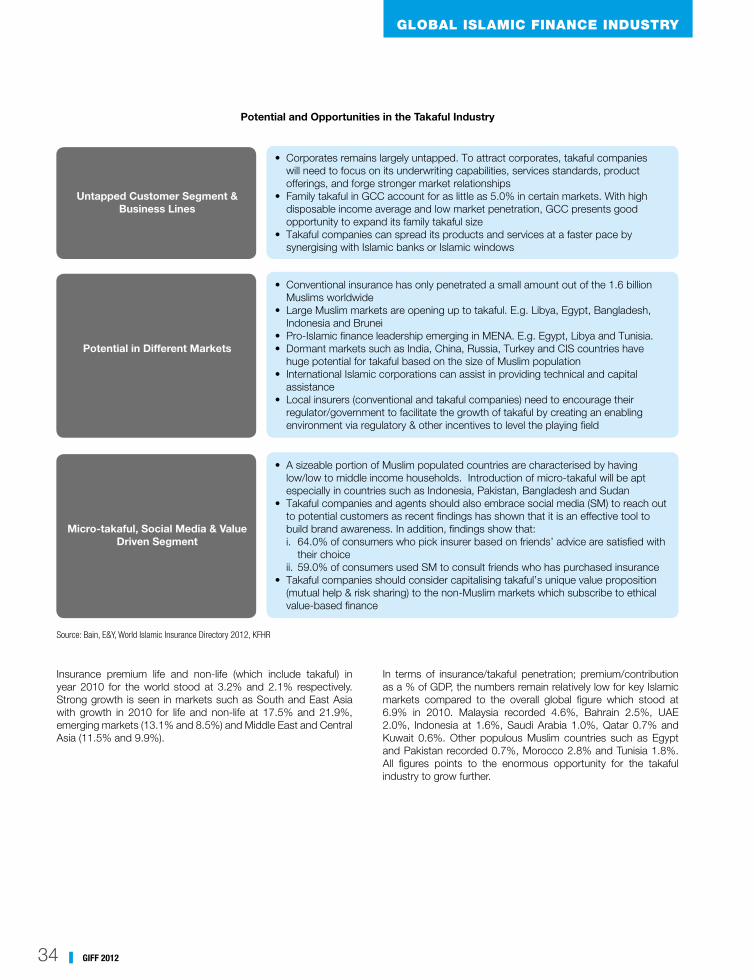

Potential and Opportunities in the Takaful Industry

Untapped Customer Segment & Business Lines

Potential in Different Markets

Micro-takaful, Social Media & Value Driven Segment

• Corporates remains largely untapped. To attract corporates, takaful companies will need to focus on its underwriting capabilities, services standards, product offerings, and forge stronger market relationships

• Family takaful in GCC account for as little as 5.0% in certain markets. With high disposable income average and low market penetration, GCC presents good opportunity to expand its family takaful size

• Takaful companies can spread its products and services at a faster pace by synergising with Islamic banks or Islamic windows

• Conventional insurance has only penetrated a small amount out of the 1.6 billion Muslims worldwide

• Large Muslim markets are opening up to takaful. E.g. Libya, Egypt, Bangladesh, Indonesia and Brunei

• Pro-Islamic fi nance leadership emerging in MENA. E.g. Egypt, Libya and Tunisia.• Dormant markets such as India, China, Russia, Turkey and CIS countries have

huge potential for takaful based on the size of Muslim population• International Islamic corporations can assist in providing technical and capital

assistance• Local insurers (conventional and takaful companies) need to encourage their

regulator/government to facilitate the growth of takaful by creating an enabling environment via regulatory & other incentives to level the playing fi eld

• A sizeable portion of Muslim populated countries are characterised by having low/low to middle income households. Introduction of micro-takaful will be apt especially in countries such as Indonesia, Pakistan, Bangladesh and Sudan

• Takaful companies and agents should also embrace social media (SM) to reach out to potential customers as recent fi ndings has shown that it is an effective tool to build brand awareness. In addition, fi ndings show that:i. 64.0% of consumers who pick insurer based on friends’ advice are satisfi ed with

their choiceii. 59.0% of consumers used SM to consult friends who has purchased insurance

• Takaful companies should consider capitalising takaful’s unique value proposition (mutual help & risk sharing) to the non-Muslim markets which subscribe to ethical value-based fi nance

Source: Bain, E&Y, World Islamic Insurance Directory 2012, KFHR

Insurance premium life and non-life (which include takaful) in year 2010 for the world stood at 3.2% and 2.1% respectively. Strong growth is seen in markets such as South and East Asia with growth in 2010 for life and non-life at 17.5% and 21.9%, emerging markets (13.1% and 8.5%) and Middle East and Central Asia (11.5% and 9.9%).

In terms of insurance/takaful penetration; premium/contribution as a % of GDP, the numbers remain relatively low for key Islamic markets compared to the overall global fi gure which stood at 6.9% in 2010. Malaysia recorded 4.6%, Bahrain 2.5%, UAE 2.0%, Indonesia at 1.6%, Saudi Arabia 1.0%, Qatar 0.7% and Kuwait 0.6%. Other populous Muslim countries such as Egypt and Pakistan recorded 0.7%, Morocco 2.8% and Tunisia 1.8%. All fi gures points to the enormous opportunity for the takaful industry to grow further.

35GIFF 2012

GLOBAL ISLAMIC FINANCE INDUSTRY

Outlook

The takaful industry is facing strategic challenges as the market establishes itself. Signifi cant investments are required to establish the Shariah board, develop technical expertise on Shariah compliance, train staff, create brand awareness among customers, as well as implementing the appropriate technology. To ensure the success and sustainability of the takaful and

retakaful industry, the companies will need to work with their respective national regulator to address impediments facing the industry. Despite all the challenges, takaful is a viable alternative to conventional insurance and is expected record gross takaful contribution of USD17.2 billion by end of 2012.

Issues and Challenges in the Takaful Industry

Source: E&Y, KFHR

Human Resource

Scarcity of Data

Distribution

Leakage to Reinsurance

Financial CrisisLack of Global Standards

Applicability of IFRS 4

Standardisation - Models and Practices

Governance - Policyholders’ interest

• Shortage of qualifi ed takaful professionals may stunt the growth of the industry

• The talent issue has been partly addressed with the increase in the number of institutions offering Islamic fi nance related courses

• The industry lacks statistical data claims experiences in many jurisdiction

• Data availability can help the industry players to formulate relevant policies and innovate products that fi ts the industry

• Presently, takaful companies rely a lot on their agency sales force to distribute their products

• Other means such as the bancatakaful, “Islamic window” or “takaful window” and various social media tools can be utilised to gain more customer

• Leakage to conventional reinsurance companies is impeding the growth of retakaful industry

• Regulators and Shariah advisors should play more proactive roles to encourage takaful companies to ced its underwriting risks to retakaful companies instead

• The on-going fi nancial crisis might result in slower growth in takaful contribution

• Worsening claims scenario as a result of fi nancial turmoil and economic downturn would also affect retakaful players

• Retakaful companies have to be extra cautious and prudent in its underwriting process and takaful players is expected to focus on personal lines which they can weather during crisis

• A uniformed regulations that work across the globe will facilitate effi cient transactions

• This will be useful for global marketing initiatives and cross border activity especially in non-traditional market like US and Europe

• Concerns over applicability of IFRS framework on takaful companies

• The list of issues include how to tackle the policyholders’ fund, whether or not to apply IFRS 4 on the company as a whole, how to treat fi nancial instruments, how to treat Al-Qard Al-Hasan, and etc.

• Modifi cation required if IFRS were to be applied

• Standardisation is required for global acceptability, growth and stability

• Having a standardised model recognised by all jurisdiction will make it easy for cross border selling of takaful products and services, making it easier for customer to understand the products and services and making it easy for takaful companies to export its business to new jurisdictions

• At the moment, the different models is a major barrier for cross-border operation and M&A activities, thus limiting scale of the takaful industry

• Good governance mechanism needs to be in place as takaful company has additional fi duciary responsibilities due to the unique relationship between takaful company and the participants

• Governance standards issued by AAOIFI and IFSB as well as nationally endorsed codes of conduct and ethics can provide guidance

Solvency - Treatment of Funds

• IFSB solvency standard and almost all regulatory regimes require the company as a whole to be solvent. This is on the ground that through a mandatory or constructive obligation of payments of Al-Qard Al-Hasan, Takaful Companies (TCs) eventually become subject to a similar risk level, as of a conventional insurance company

• IFSB standard further requires that TCs need to endeavour to ensure that the policyholders’ funds also become solvent at their own. A balance between the two is probably amongst the most important regulatory challenges that regulators are facing

• It is also important to note that Shariah scholars throughout the world are discouraging the increasing use of Al-Qard Al-Hasan and hence the need for self-solvent funds is increasing

• Presently there remains policyholders’ funds in some jurisdictions that cannot be considered to be solvent by themselves

Shariah Compliance

• It has been bearing on customers’ confi dence and buy in to the industry

• There is a need to ensure an end-to-end Shariah compliance

• Presently three approaches being used to ensure Shariah compliance:o Shariah board at national levelo Market forceso Shariah committee at the takaful

company level