26th annual health sciences tax conference€¦ · examples are where careful plan document...

TRANSCRIPT

26th Annual Health Sciences Tax ConferenceUpdate on compensation and benefits for tax directors

December 7, 2016

Page 2 Update on compensation and benefits for tax directors

Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

► This presentation is © 2016 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Page 3 Update on compensation and benefits for tax directors

Presenters

► Catherine L. CreechErnst & Young LLPWashington, [email protected]+1 202 327 8047

► Rachael WalkerErnst & Young LLPNew York, New [email protected]+1 212 773 9180

Page 4 Update on compensation and benefits for tax directors

Compensation and benefits issues are not the main purview of the tax department ... until something goes wrong.

Page 5 Update on compensation and benefits for tax directors

Topics and agenda

► Technical updates► Deferred compensation and 409A► Income tax deduction limits► Taxation of equity awards► Fringe benefits

► Common errors and examination risks► Best role for the tax department

Page 6 Update on compensation and benefits for tax directors

Deferred compensation and 409A

Page 7 Update on compensation and benefits for tax directors

Section 409A — general rule refresh

► Section 409A regulates “nonqualified deferred compensation” (NQDC).

► NQDC: legally binding right to receive compensation that is payable more than 2½ months after the end of the taxable year in which a substantial risk of forfeiture lapses.

► There are numerous requirements on the time and form of payments and timing of deferral elections.

► If NQDC violates Section 409A, the NQDC is includible in income upon vesting (or if later upon the violation) and is subject to a 20% additional tax and a premium interest tax.

► Important exceptions are qualified plans, transfers of property, short-term deferrals, fair value options and stock appreciation rights.

Page 8 Update on compensation and benefits for tax directors

Section 409A — tax department role

► Typical NQDC includes supplemental pensions and savings plans, deferrals of annual bonuses and certain types of severance.

► Other arrangements that may require analysis are employment agreements, negotiated departures, payments to expatriates and directors’ plans.

► 409A typically does not present material income tax issues for the employer, but does affect reporting and withholding.

► Errors can create significant executive tax issues and liabilities.

Page 9 Update on compensation and benefits for tax directors

Section 409A — typical errors and corrections

► 409A errors generally can be categorized as “paying too early or too late.”► Deferral elections applied incorrectly► Failure to start payments on a separation from service or specified

date ► Failure to properly calculate supplemental annuity payments

► Corrections ► Not every unexpected event is a 409A error.► “Self-help” may be available through constructive receipt,

forfeiture, rescission or “windfalls.”► Notice 2008-113 provides limited correction programs that include

IRS reporting and, in some cases, limited application of the 20% addition to tax.

Page 10 Update on compensation and benefits for tax directors

Section 409A — how to manage the risks?

► Tax should not be the “last to know” when a 409A issue arises.

► Careful coordination with HR and payroll is needed.► Tax needs a role in managing outside vendors when issues arise.► Tax needs to be involved in any effort to “fix” a problem or any

internal review to find potential problems.

► Coordination with legal is necessary.► Examples are where careful plan document drafting and legal

analysis may be helpful to eliminate or favorably resolve “errors.”

► Tax needs to be involved in corrections and reporting.► Notice 2008-113 typically requires attachments to the corporate

return.

Page 11 Update on compensation and benefits for tax directors

Section 409A — new proposed regulations

► Issued in June of 2016► Not likely to be finalized before 2017► Generally make technical corrections and confirm prior

IRS interpretations► Generally do not “open up” new areas under 409A► May suggest more limited self-correction for unvested

amounts ► Accompanied by additional proposed regulations under

457(f) (applicable to tax-exempt organizations)

Page 12 Update on compensation and benefits for tax directors

Income tax deduction limits

Page 13 Update on compensation and benefits for tax directors

Section 162(m) general rule refresh

► Annual $1 million deduction limit applies to:► Compensation, other than “performance-based compensation” ► “Covered employees” of public companies, other than the CFO

► Performance-based compensation is:► Compensation paid solely upon attainment of one or more pre-

established, objective performance goals set up by a compensation committee of outside directors

► Shareholder disclosure and approval of the goal, and compensation committee certification that the goal is met, also required

Page 14 Update on compensation and benefits for tax directors

Section 162(m) common issues

► Although the deduction limit has been in place for over 20 years, errors are not uncommon.► Changes to performance standards ► Failure to document compensation committee determinations► Discretionary increases in compensation payable under the plan► Failure of compensation committee to act within the specified time

frames

► Interaction with 409A:► May delay a payment to the extent that payout at the time

specified would cause the payment to be nondeductible under 162(m)

► Note that post-separation-from-service payments are not subject to 162(m)

Page 15 Update on compensation and benefits for tax directors

Section 162(m) common issues

► Cannot guarantee bonuses on involuntary termination or retirement► Revenue Ruling 2008-13 — addresses bonuses potentially payable on

involuntary termination or retirement regardless of whether the performance goal is met.

► Issues on severance pay based on bonus targets.► Change in control trigger is not affected by the ruling.

► Questions arise on application of the rule to the CFO► Notice 2007-49 — coordinates 162(m) with changes in SEC disclosure

rules.► Covered employees now limited to the principal executive officer (PEO)

and the three highest paid officers other than the PEO or principal financial officer (PFO) — the PFO is never a covered employee.

► But note clarification on small registrants in CCA 201543003.

Page 16 Update on compensation and benefits for tax directors

Section 162(m)(6) general rule refresh

► Imposes a $500,000 limit on the federal income tax deduction for compensatory payments by a covered health insurance provider to all individual service providers (limited exceptions for some independent vendors)

► Applies to compensation attributable to a “disqualified taxable year” in 2010 or later, including post-employment payments

► See final regulations at § 1.162-31 ► Key concept: an annual $500,000 limit applies for each

individual who is providing services in a disqualified taxable year

Page 17 Update on compensation and benefits for tax directors

Covered health insurance provider and de minimis exception

► Covered health insurance provider definition applies on a controlled group basis

► Exception applies if annual premium revenue from minimum essential coverage is less than 2% of the controlled group’s gross revenue► Effectively excludes insurance companies with relatively small health

insurance businesses► Utilized by Medicare and Medicaid providers with little marketplace

coverage► Recent Chief Counsel Advice (CCA) confirms that Medicare and Medicaid

are not health insurance for this purpose► One-year grace period if fail to meet the de minimis in the subsequent

year

Page 18 Update on compensation and benefits for tax directors

Section 162(m)(6) corporate transactions and related rules

► If a covered health insurance provider acquires a non-covered entity:► Acquired entity becomes subject to the deduction limit► Regulations’ “transition rule” allows acquired entity to escape deduction

limit only for the taxable year ending with the acquisition (and prior years)► If covered health insurance provider departs from the controlled

group:► Remaining affiliates continue to be covered health insurance providers for

the taxable year even if the remaining entities are not covered health insurance providers tested alone.

► Potential exception if the de minimis rule can be met.► Departing entity’s premiums must be counted for period of the taxable

year that is in the affiliated group. ► No pro-rated $500,000 limit for short years

Page 19 Update on compensation and benefits for tax directors

Section 162(m)(6) noncovered entity acquires covered entity

► The acquired entity remains subject to the $500,000 limit for all prior disqualified taxable years.

► Will the acquisition of the covered entity cause the controlled group to be a covered health insurance provider or will the controlled group satisfy the 2% de minimisexception? ► If the de minimis exception will not be met by the controlled group

after the acquisition, there likely is a one-year transition rule available if the pre-acquisition controlled group met the de minimisexception.

► Thus, the year following the acquisition likely becomes the first disqualified taxable year for the affiliated group.

Page 20 Update on compensation and benefits for tax directors

Section 162(m)(6) covered entity acquires noncovered entity

► Is it beneficial to accelerate payments (to the extent permissible) to the target’s short year to avoid the $500,000 limit?

► Are there pre-2010 grants for the target that can be excluded from future application of the $500,000 limit?► For example, pre-2010 stock options

Page 21 Update on compensation and benefits for tax directors

Taxation of equity awards

Page 22 Update on compensation and benefits for tax directors

Taxation of equity awards

► Actual equity ► Restricted stock► Stock options► Partnership interests

► Phantom equity ► Restricted stock units (RSUs)/phantom stock► Stock appreciation rights (SARs)► Long-term incentive compensation (LTIP)

Page 23 Update on compensation and benefits for tax directors

Equity awards: key tax provisions

► Restricted stock — § 83► Income inclusion: on vesting, unless Section 83(b) election is made;

Section 409A does not apply► Deduction: “year within which” rule if not vested at transfer

► Nonqualified stock options — § 83► Income inclusion: at exercise; Section 409A does apply if FMV exercise

price and other requirements satisfied► Deduction: normal method of accounting if vested on exercise

► RSUs, SARs, LTIP — §§ 451, 409A, 461, 404► Income inclusion: when paid (§ 451), unless plan terms or operation fail

§ 409A payment timing requirements► Deduction if not deferred comp: when fixed, determinable (§ 461)► Deduction if deferred comp: “year within which” rule (§ 404(a)(5)), unless

delivered in vested stock

Page 24 Update on compensation and benefits for tax directors

Equity awards: other key tax provisions

► Section 3121(v)(2) ► Governs the time when “nonqualified deferred compensation”

(e.g., certain RSUs, SARs, LTIP) is treated as wages for FICA tax purposes. Nonqualified stock options — § 83

Page 25 Update on compensation and benefits for tax directors

Equity awards: common errors and potential audit issues

► Restricted stock and Section 83(b) elections ► Retirement vesting ► Section 162(m)► Transactions► Section 409A and transactions► FICA withholding and deposits

Page 26 Update on compensation and benefits for tax directors

Common errors and potential audit issues:Restricted stock and Section 83(b) elections

► Background: ► Section 83(b) election accelerates the time of income inclusion

(and employer’s tax deduction) from date of vesting to the date on which the property is transferred.► Federal income tax and FICA withholding are required.

► Amount of income is FMV as of the date of transfer.► There are no tax consequences at vesting.► If property is forfeited, employee does not get a loss for amount

included in income, but a deduction only for amount actually paid.► Election must be made within 30 days of transfer.

► The taxpayer is no longer required to attach election notice to tax return, but still must make initial election within 30 days.

Page 27 Update on compensation and benefits for tax directors

Common errors and potential audit issues:Restricted stock and Section 83(b) elections

► Issues:► Has there been a transfer of property?

► Restricted stock vs RSUs ► Redemption price — did transferee receive a beneficial ownership that

would be forfeited if the vesting condition is not satisfied (e.g., does transferee have a risk of loss)?

► Did employee make a proper Section 83(b) election?► Timely filed with proper IRS office within 30 days; no exception for

holidays► Failure to provide employer with a copy of the election; if not, employer

may be liable for failing to withhold federal income tax and FICA at vesting

► Failure to identify property correctly► Failure to include the correct FMV

Page 28 Update on compensation and benefits for tax directors

Common errors and potential audit issues:Retirement vesting

► Background:► Common retirement vesting provisions include age and service

requirements (e.g., age 55 and 10 years of service); attainment of a specified age (e.g., age 65).

► Issues:► Timing and amount of income inclusion — for restricted stock,

executive has income inclusion if retirement vesting provision applies regardless of actual retirement.

► Section 409A — for RSUs, the short-term deferral exception may no longer apply.

► FICA — for restricted stock, amount is taken into account when transferred and vested; for RSUs, when vested regardless of timing of transfer.

Page 29 Update on compensation and benefits for tax directors

Common errors and potential audit issues:Transactions

► Background:► Acquisitions, divestitures and spin-offs raise a number of equity-based

compensation issues. ► Issues:

► Which party receives the deduction: employer entitled to the deduction may be different from the party making the payment.

► In what period is deduction taken: depends if transfer or payment is deferred compensation subject to the § 404(a)(5) “year within which” rule, or is not deferred compensation and is deductible under the taxpayer’s method of accounting.► Generally, an amount is not deferred compensation if paid within 2½ months

after the year in which compensation first vests.► Tax-free transaction: exchange of shares is tax free.

► Vested for vested, nonvested for nonvested, vested for nonvested or nonvestedfor vested

Page 30 Update on compensation and benefits for tax directors

Common errors and potential audit issues:FICA withholding and deposits

► Background:► Employer must withhold FICA tax when nonqualified deferred

compensation becomes vested and when other equity or performance-based compensation is included in income; employers generally must deposit FICA on a monthly or semi-weekly basis; however, employers must deposit by the next business day if $100,000 or more of employment taxes has accumulated.

► Issues:► Timely FICA withholding: is the amount considered nonqualified deferred

compensation? ► Timely deposit of FICA withholding: IRS field service directive provides

that deposit is deemed timely if made within one day after stock option exercise settlement, provided settlement is within three days of the exercise; no accommodation for other compensation.

Page 31 Update on compensation and benefits for tax directors

Fringe benefits

Page 32 Update on compensation and benefits for tax directors

Overview of fringe benefits: issues to consider

► Taxation of employee: is benefit taxable to employee? (That is, must item be included in income?)

► Amount of taxation: how is amount of income inclusion determined?

► Timing of taxation: if there is income inclusion, when does it occur?► Deduction: may employer claim a deduction for providing benefit?► Timing of deduction: if there is a deduction available, when can it

be claimed?► Amount of deduction: how is amount of deduction determined? Is

there applicable disallowance?

Page 33 Update on compensation and benefits for tax directors

Overview of fringe benefits: general rule of inclusion

► Starting point: anything of value is income. ► Section 61: Gross income means all income from whatever source

derived, including compensation for services, fees, commissions, fringe benefits and similar items.

► A fringe benefit provided by employer to employee is presumed to be income to employee, unless it is specifically excluded from gross income by another section of the Internal Revenue Code (the Code).

► Various Code sections provide authority for excluding specific items from gross income or valuing item to limit inclusion.

► This presentation focuses on a few of the more common types of fringe benefits.

Page 34 Update on compensation and benefits for tax directors

Overview of fringe benefits: primary Code sections

► Section 61: General rule of inclusion in income ► Section 132: Statutory exclusions from income ► Section 274: Limits on employer’s deduction of costs

Page 35 Update on compensation and benefits for tax directors

Overview of fringe benefits: Section 132

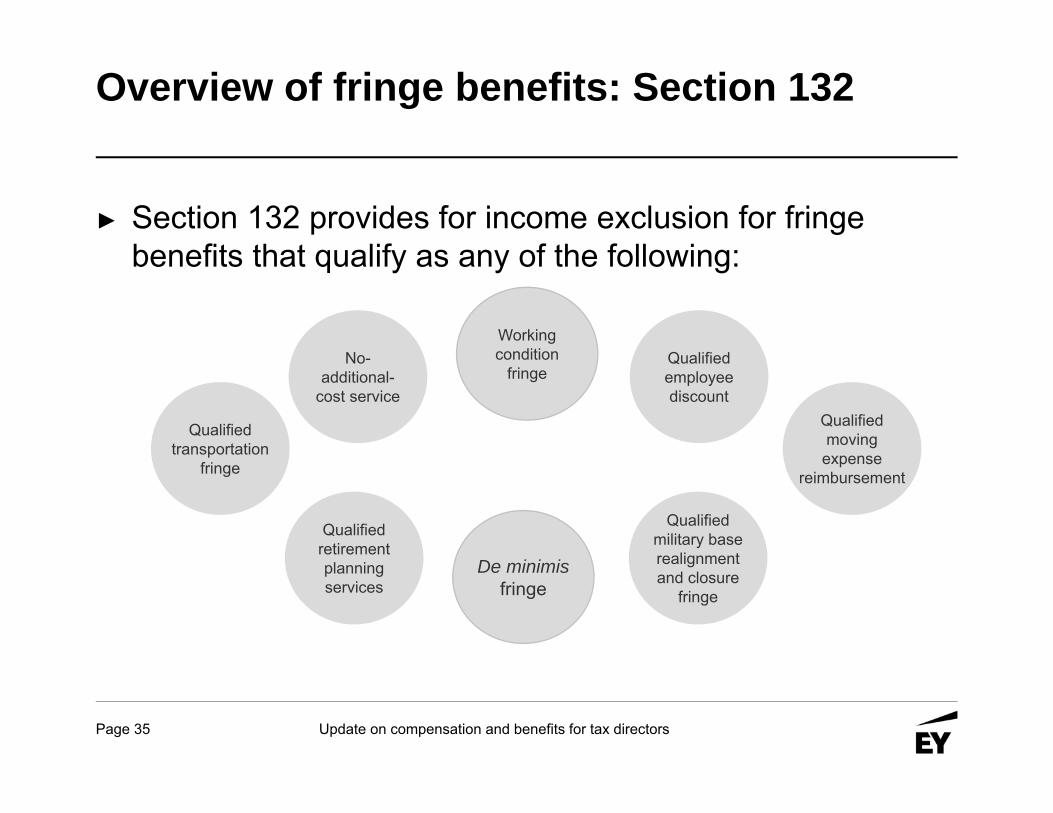

► Section 132 provides for income exclusion for fringe benefits that qualify as any of the following:

No-additional-

cost service

Working condition

fringe

De minimisfringe

Qualifiedtransportation

fringe

Qualified retirement planning services

Qualified employee discount

Qualifiedmovingexpense

reimbursement

Qualified military base realignment and closure

fringe

Page 36 Update on compensation and benefits for tax directors

Working condition fringe: Section 132(a)(3)

► Working condition fringe: Any property or services provided to employee to the extent that, if employee had paid for such property or services, such payment would be allowable as a deduction under § 162 or § 167.

► Thus, in order to qualify as a working condition fringe, it must have been able to have been claimed as a business deduction.► Ordinary and necessary business expense► Reasonable in amount► Actually incurred primarily for business

Page 37 Update on compensation and benefits for tax directors

Working condition fringe: deductible as business expense

► Must have been a deductible expense if claimed by employee on individual return

► Must relate to trade or business of employer providing benefit

► 2% of adjusted gross income (AGI) floor that would be applicable on individual return is ignored

► Exclusion limited to current employees, partners, directors or independent contractors

► No nondiscrimination rule

Page 38 Update on compensation and benefits for tax directors

Working condition fringe: common examples

► Employer reimbursement of business-related travel expenses► Airfare, lodging, ground transportation, etc.

► Employer-owned or leased vehicles► Personal use is includible in income► Various valuation methods apply to determine value of any

personal use of vehicle

► Employer reimbursements (discussed later)► Business usage of employer-owned or leased aircraft► Car services

► Personal use of car services is includible in income

Page 39 Update on compensation and benefits for tax directors

De minimis fringe: Section 132(a)(4)

► De minimis fringe benefits are excludible from recipient’s income

► De minimis fringe is a gift of service or property (other than cash), the value of which is, after taking into account frequency with which similar fringes are provided by employer to employees, so small that accounting for it is administratively impracticable.

Page 40 Update on compensation and benefits for tax directors

De minimis fringe: requirements

► Key characteristics of a de minimis fringe include:► Value (must be small in value)► Frequency (must occur infrequently and on a non-routine basis)► Administrative impracticability

► Frequency of service or property is a key element.► Generally, it may be discriminatory.► Burden is on the employer to establish that accounting for

the benefit would be administratively impracticable.

Page 41 Update on compensation and benefits for tax directors

De minimis fringe: common examples

► Qualifies as de minimis fringe:► Occasional personal use of company photocopying and fax

machines► Traditional gifts given upon completion of lengthy service for

employee (e.g., a gold watch at retirement)► Length of stay or safety awards of nominal value (e.g., award of a

pin)► De minimis personal use of a company-provided vehicle► De minimis reimbursement for meals (e.g., very occasional

overtime meals)► Occasional cocktail parties, group meals or picnics for employees► Coffee, donuts, etc., provided for employees

Page 42 Update on compensation and benefits for tax directors

De minimis fringe: benefits which are not de minimis

► Does not qualify as de minimis fringe:► Gift certificates (no matter what value)► Cash gift, awards or prizes (no matter what value) ► Holiday gifts provided monthly to employees ► Tickets to sporting or entertainment events that are given more

frequently than only occasionally, or value of which is not de minimis (e.g., season tickets)

Page 43 Update on compensation and benefits for tax directors

Qualified employee discount: Section 132(a)(2)

► Qualified employee discount excluded from employee’s income► Requirements:

► Only for goods or services of a type that employer offers for sale to customers in ordinary course of business

► Exclusion not permitted for goods or services sold primarily to employees► No special rights (e.g., special exchange, return or warranty rights)► Employee must work in line of business in which item or service is sold► Discount may not discriminate in favor of highly compensated employees► Discount exclusion is not available for employee purchases of real or

investment property

Page 44 Update on compensation and benefits for tax directors

Qualified employee discount: maximum excludible discount

► For services, maximum excludible discount is 20% of regular price.

► For goods, maximum excludible discount is gross profit margin.

► It is based on price at time of sale.

Page 45 Update on compensation and benefits for tax directors

Qualified employee discount: gross profit percentage

► Gross profit percentage is normally determined by aggregating all sales revenues and cost of goods sold in line of business for employer’s taxable year.

► Gross profit percentages may be computed for units smaller than lines of business.► Each line of business must be carved up reasonably.► May not discriminate in favor of highly compensated employees.

► Example: ► Sales revenue: $500,000► Cost: $250,000► Gross profit percentage: ($500k-$250k)/$500k = 50%► Maximum excludible discount for $50 widget: $25

Page 46 Update on compensation and benefits for tax directors

Qualified employee discount: treatment of excess discount

► If a discount exceeds maximum excludible discount, only excess must be treated as compensation.

Page 47 Update on compensation and benefits for tax directors

No-additional-cost services: Section 132(a)(1)

► Exclusion permitted for employee usage of excess unused capacity

► Examples:► Standby flights by airline employees► Telephone services for telephone employees

► Requirements:► Service must be one that employer offers for sale to customers in

ordinary course of its business► Employee must be employed in line of business in which service is

provided► Employer may not incur any substantial additional expense or

forgo any revenue in providing service

Page 48 Update on compensation and benefits for tax directors

No-additional-cost services: separate line of business limitation

► Employees may perform services for multiple lines of business.► Service for each line must be substantial.

► Factors for determining what is a line of business:► All affiliated entities are a single employer.► Employer is engaged in multiple lines of business if it sells

products or services in more than one industry group.► Regulations define line of business as any two-digit code

classification in Enterprise Standard Industrial Classification Manual (e.g., general retail merchandise stores; hotels and other lodging places; auto repair, services and garages; and food stores).

Page 49 Update on compensation and benefits for tax directors

No-additional-cost services: other characteristics

► Exclusion extends to services provided to:► Spouses► Dependent children► Retired employees► Surviving spouses► Partners

► No exclusion for highly compensated employees unless service is available on a nondiscriminatory basis► Full inclusion, not just excess discriminatory piece

► Reciprocal agreements between employers to provide services to other’s employees OK ► Agreement must be written. ► No substantial additional cost may be incurred.

Page 50 Update on compensation and benefits for tax directors

Cash reimbursements: overview

► If paid for by employee, expense must be properly substantiated in order for reimbursement by employer to qualify as working condition fringe.

► Accountable plan treatment:► Amounts paid under accountable plan are not deemed wages and

are not subject to payroll taxes.► Amounts not paid under accountable plan are includible in income

and are subject to payroll taxes.

Page 51 Update on compensation and benefits for tax directors

Accountable plans: basic requirements

► Three requirements for accountable plans:► Business connection► Adequate accounting ► Return of excess

Page 52 Update on compensation and benefits for tax directors

Accountable plans: business connection

► Business connection: expense must be a deductible business expense incurred in connection with services performed as employee for reimbursing employer.

► If expense were not reimbursed by employer, expense would qualify as a deductible expense by employee on employee’s 1040 income tax return.► Determined without regard to 2% floor for miscellaneous itemized

deductions or § 274 limitations

Page 53 Update on compensation and benefits for tax directors

Accountable plans: adequate accounting

► Employee must actually incur expense.

► Documentation must be provided timely (usually within 60 days of incurring expense).

► Employee must verify:► Date► Time ► Place► Amount► Business purpose

► Adequate documentation must be provided (receipts, cancelled checks, bills, etc.).

► Exceptions to documentation requirements:► Meal or lodging expenses

that are reimbursed on a per diem basis, at rate at or below allowable maximum, under accountable plan

► Expenditures for transportation expense for which receipt is not readily available

Page 54 Update on compensation and benefits for tax directors

Accountable plans: return of excess

► Employee is required to return excess reimbursements/payments to employer within a reasonable period of time.

► If employee is not required to return excess, the plan fails as an accountable plan and all amounts paid under the plan are taxable.

► If employee is required to return excess but fails to do so, excess that is not returned is taxable.

Page 55 Update on compensation and benefits for tax directors

Cash reimbursements: advances

► Travel advances paid under accountable plan are excludable from income.

► If employee does not substantiate expenses or return excess advances timely, advance is includible in wages and subject to income and employment taxes no later than the first payroll period following the end of a reasonable period of time.

Page 56 Update on compensation and benefits for tax directors

Cash reimbursements: settling up advances

► Safe harbors for reasonable period of time:► Fixed date method

► 30 days prior: advance may be made► 60 days after: expense must be substantiated► 120 days after: excess must be returned

► Periodic statement method► Substantiation and return of excess must be made within 120 days

after employer provides employee with a periodic statement (at least quarterly), stating that any excess amounts are required to be returned.

► If arrangement does not meet one of the safe-harbor methods, it may still be considered timely, if it is reasonably based on facts and circumstances.

Page 57 Update on compensation and benefits for tax directors

Cash reimbursements: per diem reimbursement

► Per diem is daily allowance to pay for lodging, meals and incidental expenses while traveling on business.

► An accountable plan may include per diem allowance component.► The amount of expenses reimbursed under per diem allowance is

deemed substantiated without receipts.► Time, place and business purpose must still be substantiated.► Per diem requirements:

► Must be for ordinary and necessary business expenses incurred by employee for business travel away from home

► Must be reasonably calculated not to exceed amount of expenses or anticipated expenses

► Must be at or below applicable federal per diem rate

Page 58 Update on compensation and benefits for tax directors

Listed property: deduction disallowance

► Accountable plan rules impose substantiation requirements as prerequisites to any income exclusion of a cash reimbursement to employee.

► Listed property rules impose substantiation prerequisites to employer’s deduction of certain costs.

► Section 274(d) disallows employer’s deduction related to listed property specified in § 280F(d)(4) unless substantiation rules are satisfied.

Page 59 Update on compensation and benefits for tax directors

Listed property: Section 280F

► Any property used as transportation► Airplanes► Passenger automobiles► Boats

► Any property used for entertainment, recreation or amusement

► Any computer or peripheral equipment► Cell phones (not anymore!)

Page 60 Update on compensation and benefits for tax directors

Listed property: Section 274(d) substantiation requirements

► Taxpayer must substantiate by adequate records or by sufficient evidence corroborating taxpayer’s own statement:► Amount of each separate expenditure with respect to listed

property (including costs of acquisition, capital improvements, lease payments, and maintenance and repairs)

► Amount of each individual use of property for business or income-producing purposes (by mileage for automobiles and other means of transportation) and total such use for taxable period

► Date of expenditure or use of property► Business purpose for expenditure or use of listed property

► No estimation is permitted.► No de minimis exception to substantiation.

Page 61 Update on compensation and benefits for tax directors

Meals: overview

► Absent applicable statutory exclusion, value of meals must be included in income.

► Certain meals may be excluded from income depending on circumstances.

► Relevant exclusions:► Section 119 (employer-provided cafeterias)► De minimis fringe meals► Working condition fringe meals

Page 62 Update on compensation and benefits for tax directors

Meals: employer cafeterias

► Furnishing of free meals to employees for employer’s convenience is excluded.

► It is difficult to meet § 119 requirements.► Meals must be provided:

► In-kind► On business premises► For substantial non-compensatory business reasons, such as:

► Need to be on call for emergencies during meals► Short meal period due to workload► Geographic isolation of workplace

► If more than 50% of employees meet § 119 requirements, value of meals may be excluded for all employees.

► If 50% or less of employees meet requirements, only those employees meeting requirements may exclude value of meals.

Page 63 Update on compensation and benefits for tax directors

Meals: employer-operated eating facilities as de minimis fringe

► Even if § 119 requirements are not met, the value of meals at an employer-operated eating facility may be excluded as a de minimis fringe if facility’s revenue normally equals or exceeds direct operating costs of the facility.

► Revenue direct operating costs.► Direct operating costs:

► Cost of food and beverages► Cost of on-site labor

► Costs and revenues for § 119 employees may be excluded from calculation. ► Additional requirements:

► Facility must be on or near premises► Facility must be owned (or leased) and operated (contracted operation OK) by

employer ► Meals may be served only during, or immediately before or after, workday► Nondiscrimination rule applies

Page 64 Update on compensation and benefits for tax directors

Meals: reimbursed meals

► Reimbursed meals may qualify for exclusion as a working condition fringe.

► Taxability depends on whether expense would be deductible as a business expense under § 162.

► Non-travel meals would have to be supported by a valid business purpose (e.g., client meeting).

► To be excludable, reimbursement must meet accountable plan rules.

► Travel and entertainment meals will be separately discussed.

Page 65 Update on compensation and benefits for tax directors

Meals: employer’s deduction

► Employer’s deduction for meals of employees is limited by § 274(n)(1) to 50% of costs.

► If meals are excludible as de minimis fringe benefits under § 132(e), expenses are excepted from 50% limitation.

► 50% cutback affects only employers that do not treat meals as compensation.

► Employee income exclusion is not affected.

Page 66 Update on compensation and benefits for tax directors

Travel: overview of business-related travel expenses

► Employer reimbursement of travel expenses incurred by employees or independent contractors while on a work assignment may qualify as a working condition fringe, provided certain conditions are met.

► Expense must be:► Business-related► Actually incurred ► Incurred while away from home► Reasonable and necessary in amount► Properly substantiated

► Examples of business-related travel expenses include:► Taxi fare► Airfare► Lodging► Meals

Page 67 Update on compensation and benefits for tax directors

Travel: substantiation requirements

► Employer’s deduction of travel expenses is subject to substantiation requirements of § 274(d).

► To claim a deduction, taxpayer must substantiate: ► Amount of each separate away-from-home traveling expenditure,

such as daily cost of transportation or lodging► Daily totals may be shown for taxpayer’s incidental expenditures if

separated into reasonable categories, such as meals, gas, taxi fares.► Date of departure and return for each trip away from home► Number of days away from home spent on business► Locality of travel► Business reason for trip

Page 68 Update on compensation and benefits for tax directors

Travel: mixed business and personal travel

► A trip must be categorized as primarily business or primarily personal.

► It depends on facts and circumstances.► The amount of time spent on employer’s business is a

significant factor.► Incidental business conducted during a primarily personal

trip (or incidental business benefit to employer) does not convert personal use (and taxable income which results) into a nontaxable business trip.

Page 69 Update on compensation and benefits for tax directors

Travel: primary purpose of trip

► Primary purpose of trip: facts and circumstances► Amount of time spent on personal activity compared to business activity► No bright-line test► Rev. Rul. 84-55: spending two hours per day on business not sufficient for primary

business purpose ► Other factors

► Business agenda► Location► Characterization of trip► Presence of spouse or guest

► Townsend Industries, Inc. v. U.S.: company meeting at fishing retreat in Canada with business discussions and no spouses was primarily business

► Danville Plywood Corporation v. U.S.: company Super Bowl trip for employees, customers and family members was not primarily business

Page 70 Update on compensation and benefits for tax directors

Travel: away from home

► Travel must be away from employee’s tax home.► Tax home is not employee’s residence.► Guidelines:

► Where employee spends majority of working time► Significance of work done at location► Amount of revenue earned at location► Common now for executives to have a residence that is not in

same location as tax home

Page 71 Update on compensation and benefits for tax directors

Travel: temporary vs permanent assignments

► Expenses incurred while employee/independent contractor is on a temporary assignment are generally excludable from income.

► Temporary assignments are assignments lasting one year or less in a general geographic location that is not the taxpayer’s home.

► Permanent assignments are assignments lasting longer (or intended to last longer) than one year.

► Once an employee is assigned to a geographic area for longer than one year, reimbursement of business-related travel expenses becomes taxable to employee/independent contractor.

► Key to determining whether the assignment is temporary is intent.► Documentation may act as evidence of intent, but it doesn’t trump

facts.

Page 72 Update on compensation and benefits for tax directors

Travel: breaks in assignment

► Breaks in assignment can restart the clock to avoid permanent assignment, but only if they are significant in duration.

► The IRS has provided only limited guidance: ► Three weeks is not significant ► Seven months is significant

► Insignificant breaks in assignment:► Assignments before and after period of break — including period

of break — are treated as one assignment.

► Significant breaks in assignment:► Assignments before and after period of break are treated as

separate assignments.

Page 73 Update on compensation and benefits for tax directors

Entertainment: overview

► Section 274 limits deductibility of expenses that are related to entertainment.

► Section 274 provides no deductions of its own but limits deductions provided by other sections.

► That is, ordinary and necessary business expense deductible under § 162 may be limited or disallowed by § 274.

Page 74 Update on compensation and benefits for tax directors

Entertainment: definition

► Objectively defined► Considers circumstances of taxpayer

► For example, going to the theater is entertainment to lawyers and accountants but may be business to a professional theater critic.

► Entertainment may include:► Entertaining at nightclubs, cocktail lounges, theaters, country

clubs, golf and athletic clubs, sporting events, and on hunting, fishing, vacation and similar trips

► Not everything that is personal is entertainment► For example, running errands, attending funerals and commuting

are personal but not entertainment.

Page 75 Update on compensation and benefits for tax directors

Entertainment: restrictions on deductibility

► To be deductible at all, activity must be directly related or associated with business.

► Directly related► For deduction of activity, it must be directly related to active

conduct of taxpayer’s trade or business. ► This usually refers to expenses incurred in context of active

business discussions or a clear business setting.

► Associated with► For deduction of activity that directly precedes or follows a

substantial bona fide business discussion, it must be associated with active conduct of a trade or business.

► This generally includes expenses incurred for purpose of building goodwill following or preceding business meetings or discussions.

Page 76 Update on compensation and benefits for tax directors

Entertainment: additional substantiation required

► To deduct entertainment expense, taxpayer must substantiate:► Amount of each separate entertainment expenditure; daily totals may

be shown for incidental items such as taxi fares and telephone calls► Date of entertainment► Name (if any), address or location of place of entertainment► Type of entertainment (e.g., dinner or theatre) if not apparent from

designation of place► Business purpose, such as business reason for, or business benefit

derived or expected from, entertainment► Nature of business discussion or activity► Name, title, occupation or other information concerning person

entertained sufficient to establish business relationship to taxpayer

Page 77 Update on compensation and benefits for tax directors

Entertainment: further limitations

► Lavish or extravagant expenses are not deductible.► Even if expenditure meets all other prerequisites for

deductibility under § 274, deduction is limited to 50% of expense.

Page 78 Update on compensation and benefits for tax directors

Reporting and withholding

► General rule: taxable fringe benefits are reported as wages on Form W-2 for the year in which the employee received the benefit.

► Amount reported should be fair market value of taxable benefit.

► A number of special valuation rules exist.

Page 79 Update on compensation and benefits for tax directors

Reporting and withholding: timing

► IRS Announcement 85-113 provides some flexibility for the employer to elect when to withhold.

► Employer may elect to treat taxable fringe benefits as paid in a pay period, quarterly, semiannual or annual basis, but no less frequently than annually.

► Employer may elect to add taxable fringe benefits to employee regular wages and withhold on total, or may withhold on benefit at supplemental wage rate.

► Special accounting rule: November and December benefits may be treated as paid in the following year.

Page 80 Update on compensation and benefits for tax directors

Questions?

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2016 Ernst & Young LLP.All Rights Reserved.

1608-2011220

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.