26th pic - presentation (jason sadler - cigna) v7 final · apps development of megacities rising...

TRANSCRIPT

Agenda

• The Global Environment and Key Emerging Trends

• Understanding Tomorrow’s Customer Needs

• Implications for Future Strategy

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Providing for the Senior Segment

Rebalance of wealth(West to East)

Digital age

Emerging middle class

Mobile: Smartphones & Apps

Development of Megacities

Rising healthcare cost

Self-tracking medical devices

Increasing chronic

diseases in Emerging Markets

Global Mobility-Jobs, Universities, Nationalities

Economy Health

Social Technology

Global Macro Trends Driving Transformation

3

Total Healthcare costs in Asia-Pacific are projected to increase to USD2.7 trillion by 2020

Note: Markets included are Australia, China, Hong Kong, India, Indonesia, Japan, South Korea, MalaysiaPhilippines, Singapore, Taiwan, Thailand and Vietnam

Source: The World Health Organization Annual World Health Statistics Reports, Part 7 “Health Expenditure”; the United Nations; national statistics and Swiss Re projections

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 4

0

0.5

1

1.5

2

2.5

3

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

USD trillion 2011 – 2020 average growth: 8.2% p.a.

Based on projections of economic growth, medical inflation and population growth.

Population Growth

Increased burden of chronic diseases

Unhealthy lifestyles

Increased life expectancy/ageing population

New high cost treatments

Continued prevalence of endemic diseases

“The rise of chronic non-communicable diseases presents an enormous challenge…For some countries, it is no exaggeration to describe the situation as an impending disaster; a disaster for health, for society, and most of all for national economies.”

WHO Director-General Dr. Margaret Chan, 2011

THE PREVALENCE OF CHRONIC DISEASES IS INCREASING…

…PUTTING STRAIN ON THE ENTIRE HEALTHCARE SYSTEM

Source: CDC; US Census, 2010; AHA; NCI

PATIENTS

5

Prevalence of Chronic Diseases

6Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Under 20% age 55+ in 2012 Over 20% age 55+ in 2012

12% 13% 14% 14% 15%

20% 20%23% 24% 25% 26%

28% 29%

38%

18%22% 22% 22%

24%

31%33%

40%38%

32%30%

45%

34%

47%

India Mexico Indonesia Turkey Brazil Thailand China Korea Taiwan NewZealand

US Hong Kong UK Japan

Population Age 55+2012 2018 2030

Source: UN World Population

0

1

2

3

4

5World's total fertility ratemillion

Providing for the Senior Segment

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Providing for the Senior Segment

Rebalance of wealth(West to East)

Digital age

Emerging middle class

Mobile: Smartphones & Apps

Development of Megacities

Rising healthcare cost

Self-tracking medical devices

Increasing chronic

diseases in Emerging Markets

Global Mobility-Jobs, Universities, Nationalities

Economy Health

Social Technology

Global Macro Trends Driving Transformation

7

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 8

Going ViralPhiladelphia Orchestra in Beijing

June 2013

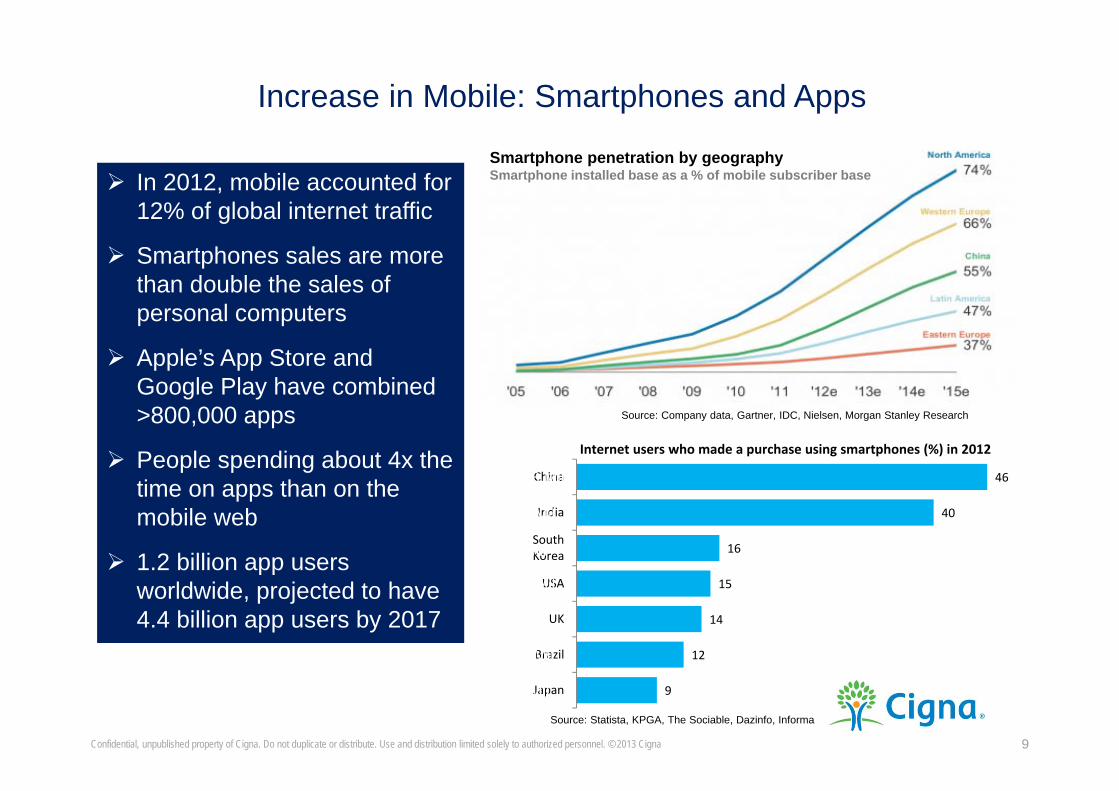

9

12

14

15

16

40

46

Japan

Brazil

UK

USA

SouthKorea

India

China

Internet users who made a purchase using smartphones (%) in 2012

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Source: Company data, Gartner, IDC, Nielsen, Morgan Stanley Research

9

Source: Statista, KPGA, The Sociable, Dazinfo, Informa

In 2012, mobile accounted for 12% of global internet traffic

Smartphones sales are more than double the sales of personal computers

Apple’s App Store and Google Play have combined >800,000 apps

People spending about 4x the time on apps than on the mobile web

1.2 billion app users worldwide, projected to have 4.4 billion app users by 2017

Smartphone penetration by geographySmartphone installed base as a % of mobile subscriber base

248 Mil

49 Mil

7 Mil

37 Mil

10 Mil

9 Mil

6 Mil

Increase in Mobile: Smartphones and Apps

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 10

Digital Age: Think Connected

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 11

Digital Age: Think Social

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 12

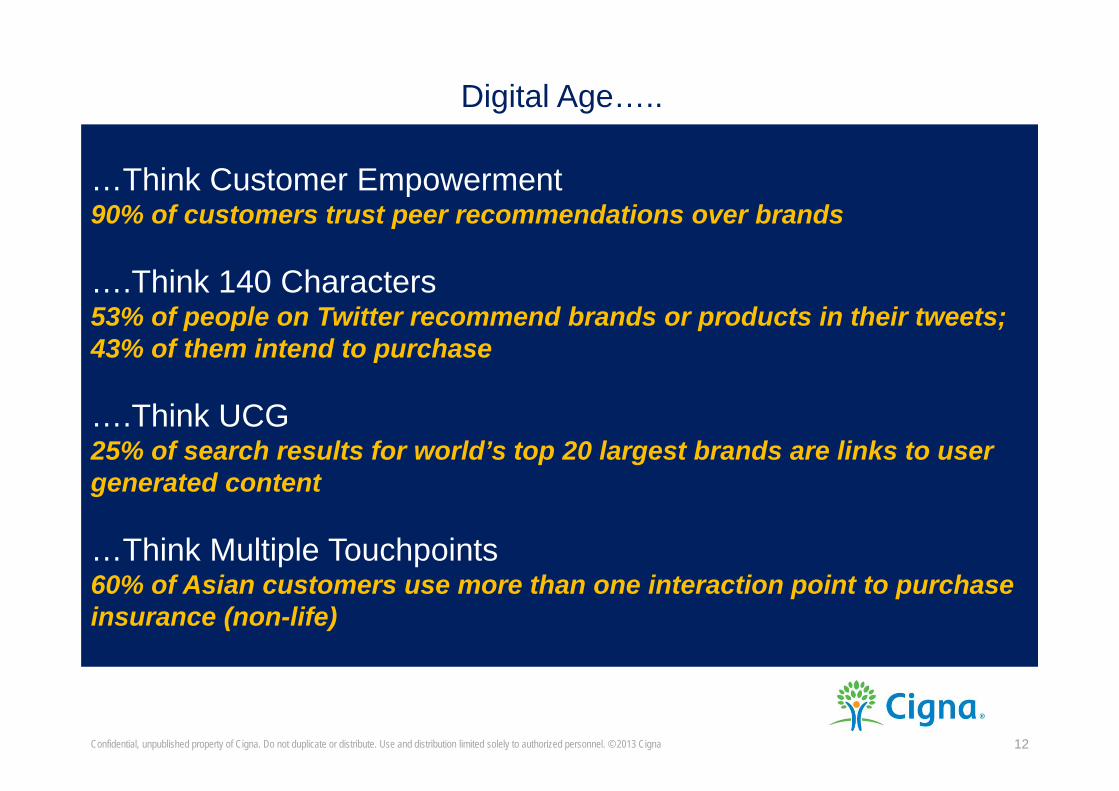

…Think Customer Empowerment90% of customers trust peer recommendations over brands

….Think 140 Characters53% of people on Twitter recommend brands or products in their tweets; 43% of them intend to purchase

….Think UCG25% of search results for world’s top 20 largest brands are links to user generated content

…Think Multiple Touchpoints60% of Asian customers use more than one interaction point to purchase insurance (non-life)

Digital Age…..

COPYRIGHT © 2013. ALL RIGHTS PROTECTED AND RESERVED.

Welcome to the Age of Transparency

Graph Search by Facebook…

…and independent social filtering aggregators, too

83% of consumers trust the recommendations of their friends

>50% trust online recommendations from complete strangers

Just 14% of consumers trust advertising

The Future of Customer Reviews

You trust your friends, and probably the friends of your friends…

So what are the opinions of people you know? Or that they know?

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 13

14COPYRIGHT © 2013. ALL RIGHTS PROTECTED AND RESERVED.

In 2010 the average shopper consulted five sourcesBut by 2011 they consulted ten!

In 2010 just 19% of shoppers checked social sourcesBut by 2011 37% did!

“ZMOT – Zero Moment of Truth”

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 14

Heightened Customer Demands

Perceivedquality

Perceivedprice

“Value”

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 15

Perceived value Perceived price

Continuous Cycle to Increase Customer Value

design

test

learn

smart innovation

Perceivedquality

Perceivedprice

“Value”

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 16

17

Business Action

Measurable Results

Insights

Supporting Data / AnalysisQualitative or quantitative pieces of

information that produce a core understanding, ideally from multiple sources

Defined business problem with measurable results

Business Objective

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Insights That Matter

Service ExperienceCare DeliverySolutionsReach

Insights that Matter Across the Value Chain

18

Unlocking and acting on insights allows us to help elevate the customer experience.

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

19Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Insight: Having an MRI is scary.

Observation: Fear

Challenge: Clear images, productivity

Opportunity: Clear MRIs, calm patients,better experiences

INSIGHTS and ACTIONS ABOUT CHILDREN AND MRI TESTS

20Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Solution #1

Make the Connection

21Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

22Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Solution #2Develop a Kitten Scanner

RESULTSHappier patients, happier parents, happier technicians.

One-and-done results improved dramatically.

23Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 24

Challenges for Our Industry

• Adding value while balancing rising costs• Availability and transparency of information• Dynamic pricing/new ways of payment (mobile)• Digital as foundation of business strategy • Self tracking medical devices – raising awareness and healthier living• Need for collaboration / partnerships across industries• Providing for the senior segment• Deeper understanding of customer needs

Confidential, unpublished property of Cigna. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2013 Cigna 25

Conclusions/Key Take Aways

• Macro trends will continue to drive strategic growth in businesses

• What does it mean to be a global business? The way we distribute, innovate, and interact with our customers are radically changing.

• Customers’ desire for value continue to evolve as they become more informed, more sophisticated in their purchasing behavior

• Deep customer insights allow us to develop relevant solutions –ensuring we deliver true value across all touchpoints

• Our industry faces various challenges but through innovation and collaborative partnerships, we can meet Tomorrow’s Customer Needs

Thank you