3q21 earnings release - ri.taesa.com.br

TRANSCRIPT

3Q21 Earnings ReleaseNovember 11, 2021

The individual and consolidated financial statements were prepared in accordance with accounting practices adopted in Brazil, comprising the Brazilian Corporation Law, Statements, Guidance and Interpretations issued by Accounting Pronouncement Committee (“CPC”) and thestandards of the Brazilian Securities Exchange Commission (CVM), combined with specific legislation issued by Electricity Regulatory Agency -ANEEL. ANEEL, as a regulatory agency, has the power to regulate concessions. Results will be presented in both formats, IFRS format and the regulatory format to allow comparison with other years. Note that Regulatory results will not be audited. Taesa's dividend declaration is performed based on the reviewed IFRS results.

Statements in this document related to business perspectives, projections on operating and financial income, and those related to Taesa’sgrowth perspective are merely projections and, as such, are based solely on Executive Board’s expectations about business future. Theseexpectations depend substantially on changes in market conditions, on Brazilian economy performance, and on industry and internationalmarket performance; therefore, subject to unannounced changes.

EBITDA is net income before taxes, net financial expenses, and depreciation, amortization and income expenses. EBITDA is not recognized byaccounting practices adopted in Brazil or in IFRS, does not represent cash flow for presented periods, and should not be considered asalternative net income. Presented EBITDA is used by Taesa to measure its own performance. Taesa understands that some financial investorsand analysts use EBITDA as an operating performance index.

“Net Debt” is not recognized by accounting practices adopted in Brazil nor by IFRS and does not represent cash flow for presented periods.Presented Net Debt is used by Taesa to measure its own performance. Taesa understands that some investors and financial analysts use NetDebt as an indication of its financial performance.

Presented managerial results are the sum of Taesa consolidated income with equity in its partially-owned subsidiaries and associatedcompanies. The purpose of this information is to permit better understanding of Taesa business.

Disclaimer

2

Sustainability Agenda - EnvironmentFight against climate change: actions under way

3

• Scope 1: Direct emissions from sources that

belong to or are controlled by the organization.

• Scope 2: Emissions resulting from the

generation of electricity that is lost during

transmission.

3.0%

4,499

54.7%

15.5%

Owned fleet

Vegetation removal

26.8%

Scope 1

Isulating gas

Others

Green House Gases Inventory

Taesa 2020

Mitigation Actions

(Scope 1)

Review of operational processes and procedures seeking

better eco-efficiency

Efficiency in the maintenance of assets containing SF6

insulating gases

Review of cleaning and maintenance procedures for line

easements

Prioritize biofuel consumption

Upgrading to a hybrid electric vehicle fleet

Educational socio-

environmental campaigns

Prevention and reduction

against wildfires

Additional Initiatves

Reforestation

Plant nurseries and seedling

distribution

(in tCO2e)

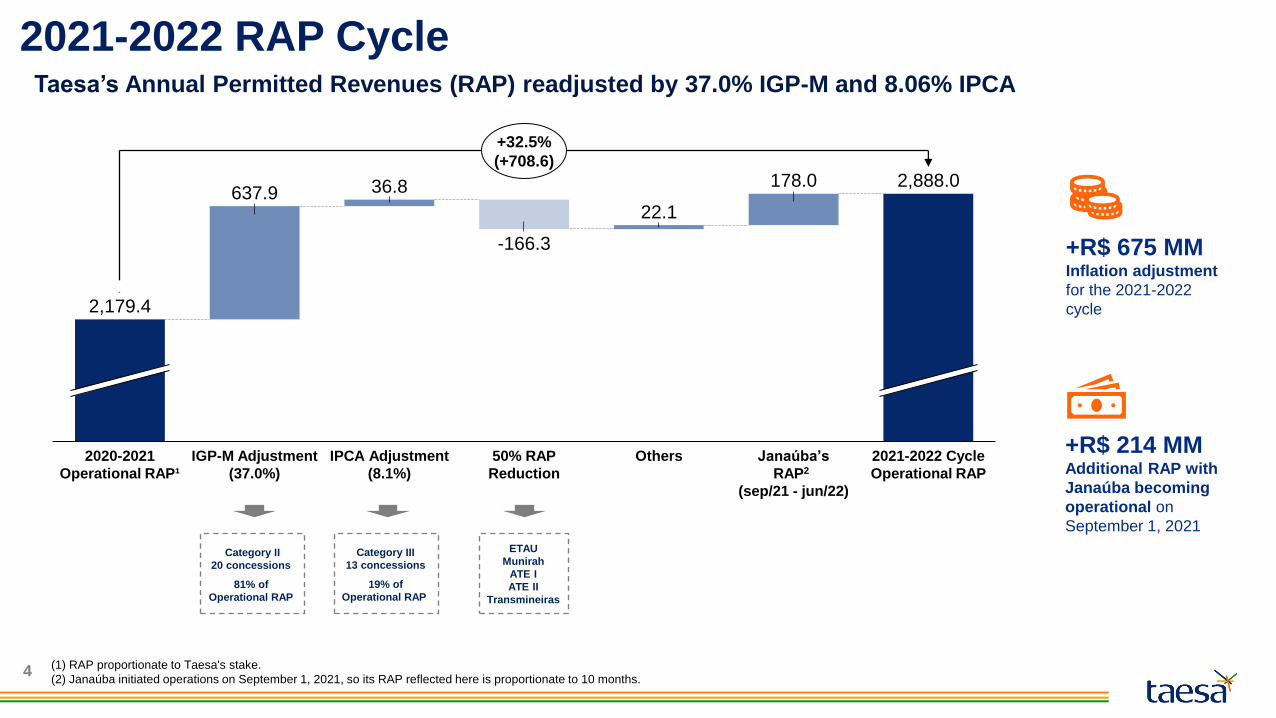

2021-2022 RAP Cycle

4

-166.3

2020-2021

Operational RAP¹

IGP-M Adjustment

(37.0%)

637.92,888.0

Janaúba’s

RAP2

(sep/21 - jun/22)

Others

178.0

50% RAP

Reduction

2,179.4

IPCA Adjustment

(8.1%)

36.8

22.1

2021-2022 Cycle

Operational RAP

+32.5%

(+708.6)

Taesa’s Annual Permitted Revenues (RAP) readjusted by 37.0% IGP-M and 8.06% IPCA

Category II

20 concessions

81% of

Operational RAP

+R$ 675 MMInflation adjustment

for the 2021-2022

cycle

Category III

13 concessions

19% of

Operational RAP

ETAU

Munirah

ATE I

ATE II

Transmineiras

+R$ 214 MMAdditional RAP with

Janaúba becoming

operational on

September 1, 2021

(1) RAP proportionate to Taesa's stake.

(2) Janaúba initiated operations on September 1, 2021, so its RAP reflected here is proportionate to 10 months.

5

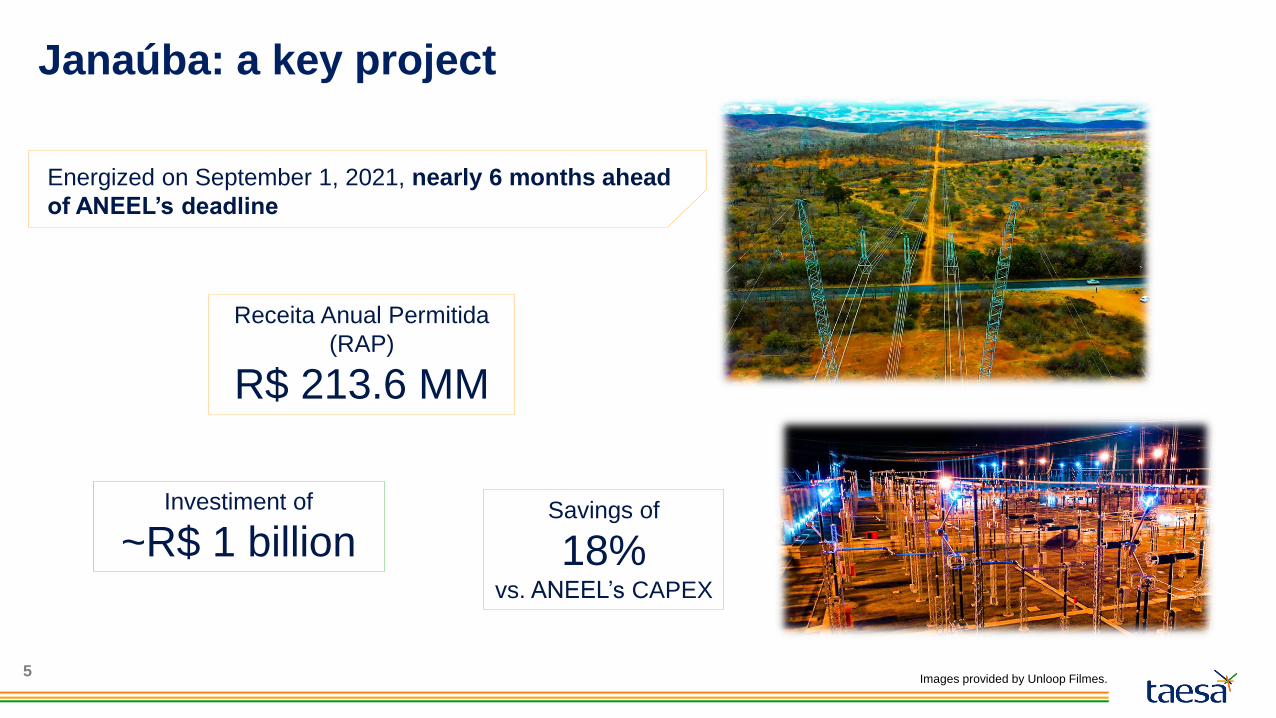

Janaúba: a key project

Energized on September 1, 2021, nearly 6 months ahead

of ANEEL’s deadline

Receita Anual Permitida

(RAP)

R$ 213.6 MM

Savings of

18%vs. ANEEL’s CAPEX

Investiment of

~R$ 1 billion

Images provided by Unloop Filmes.

6

26crossings

3substations

Employing

881people per

monthUtilizing

12k tons of structure

More than

12.5ktons of power cables

Janaúba: a key project

Images given by Unloop Filmes.

7Images shared by Renata Hossell Schiffer.

Integration of the power transmission systems

between the states of Bahia and Minas Gerais

Capacity

1,600 MW To service more than

5 million people

Outflow from renewable energy plants in the Northeast

to the Southeast and Central-West regions

Janaúba: a key project

8

RAP/CAPEX*: 87.4 / 341

ANEEL construction deadline: Feb 22

End of concession: Feb 47

SUDENE benefit

50% Taesa

%

208 km

50% Taesa

RAP/CAPEX*: 130,4 / 510

SUDENE benefit

%

338 km

ESTE RAP/CAPEX*: 123.6 / 486

ANEEL construction deadline: Feb 22

End of concession: Feb 4749.98% Taesa

%

236 km

SUDENE benefit

100 100 100 94

Land Licenses Funding Physical

100 100 100 93

FundingLicensesLand Physical

Paraguaçu

Aimorés

Investments(in R$ mm)

2014 2015 2016

3

2017 202020192018

5 22109

209

718

1,535

Ivaí

50% Taesa

RAP/CAPEX*: 323.7 / 1.937

ANEEL construction deadline: Aug 22

End of concession: Aug 47

%

600 km(CD)

98 100 100 89

PhysicalLand Licenses Funding

Sant’Ana RAP/CAPEX*: 67.1 / 610

ANEEL construction deadline: Mar 23100% Taesa

%

End of concession: Mar 49

591 km

99 100 10076

Land Licenses Funding Physical

9M219M20

1,109

819

-26.1%

R$ 3.4 billionTotal investments by

TAESA in theses projects

(2014 to 2021)

RAP/CAPEX*: 130.4 / 510

End of concession: Feb 47

338 km

99 100 100 91

Land FundingLicenses Physical

ANEEL construction deadline: Feb 22

* R$ million (2021-2022 RAP cycle / ANEEL CAPEX)** Funding does not consider the fundraising of Taesa’s partners in each project

Projects under Construction

Status of Projects

Regulatory Results

3Q20 3T21

383.3497.5

+29.8%

Net Revenues(in R$ mm – Taesa consolidated)

82.9% 84.6%

EBITDA margin

EBITDA(in R$ mm – Taesa consolidated)

3Q20 3Q21

421.0317.6

+32.6%

Net Income(in R$ mm – Taesa consolidated)

3Q20

192.1

3Q21

165.5

+16.0%

9

Operating Performance(in %)

Availability Rate

9M219M20

1,141.81,286.3

+12.6%

947.11,068.8

9M20 9M21

+12.8%

83.1%82.9%

258.4

9M20

Δ Financial Result

(net of IR*)

411.8

9M21

562.4

-26.8%99.97

9M219M20

99.92

-0.05pp

* IR estimated with an effective rate of 15%.

IFRS Net Income

10

(in R$ mm)

• Monetary restatement revenues and equity method negatively impacted by lower IGP-M index between the compared

periods (2.05% accumulated in 3Q21 versus 6.67% in 3Q20).

• Operation and Maintenance Revenue (O&M) readjusted by the same indexes from 2021-2022 RAP Cycle (37.04%

IGP-M and 8.06% IPCA).

• Growth of implementation margin and of remuneration of the contractual asset due to higher-than-expected inflation

in the quarter, which expanded the balance of these contracts' assets.

• Reduction of the operational costs due to lower investments in projects under construction.

• Growth of Net Financial Expenses (Financial Result) due to the growth of IPCA and CDI and to the reduction of

average cash balance.

(1) The Company performed the adjustments and reclassifications of its balance sheets as of September 30, 2020, in order to present such amounts for comparative purposes with the interim information as of September 30, 2021, due to the impact of OFFICIAL-NOTICE/CVM/SNC/SEP/nº 04/2020 referring to CPC 47.

54.6

3Q20 Net

Income1

Δ Net

Revenues

1.7

Δ OpEx

81.6

Δ Equity

Method

111.1

Δ Net Financial

Results

19.3

Others 3Q21 Net

Income

657.4

536.9

-18.3%

(-120.5)

1,790.6

9M219M201

1,512.8

+18.4%

Financial Results

3Q20

1,915

3Q21

1,937

4,797

23 14

4,937

6,735 6,888

IPCACDI Others

Financial Expenses(in R$ mm)

Financial Revenues(in R$ mm)

Average cash

balance(in R$ mm)

Average debt

balance(in R$ mm)

3Q20 3Q21

10.78.7

-18.6%

(-2.0)

838

1,600

3Q20 3Q21

Profitability(% of CDI)

3Q20 3Q21

-130.0

-239.0

+83.9%

(-109.1)

3Q20 3Q21

-119.3

-230.4

+93.1%

(-111.1)

Financial Results(in R$ mm)

Indexes(%)

100.9 100.4

3Q20 3Q21

1.21

3Q20

0.50

3Q21

1,243,02

3Q20 3Q21

1) Reduction in the average cash

balance impacted the financial

revenues by R$ 2.0mm.

2) Rising macroeconomic

indexes (IPCA and CDI) influenced

the growth of financial expenses by

R$ 109.1mm.

11

0.501.21

CDI(average - %)

(avg.)(avg.)

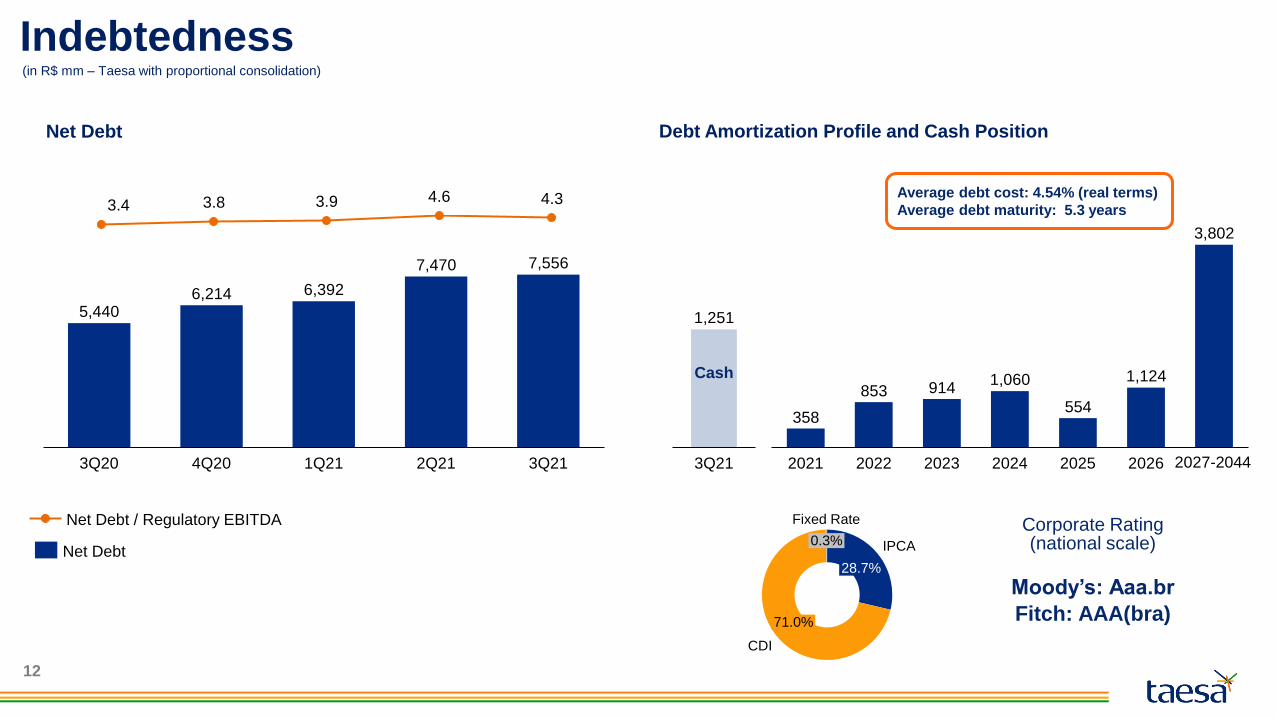

3.83.4 4.33.9 4.6

Indebtedness

12

6,214

3Q20 4Q20 3Q211Q21 2Q21

5,440

6,392

7,470 7,556

Net Debt / Regulatory EBITDA

Net Debt

358

853 914

554

2021 2023 20262022 2024

1,060

2025

1,124

3,802

1,251

3Q21

Cash

Average debt cost: 4.54% (real terms)

Average debt maturity: 5.3 years

Net Debt Debt Amortization Profile and Cash Position

2027-2044

Fixed Rate

28.7%

IPCA

CDI

71.0%

0.3%Corporate Rating(national scale)

Moody’s: Aaa.br

Fitch: AAA(bra)

(in R$ mm – Taesa with proportional consolidation)

SEE YOU THERE!

Scan below to

register now:

SUSTAINABILITY, DIVERSITY AND STRATEGY. BUILD TODAY FOR A BETTER TOMORROW.

VIRTUAL EVENT

DECEMBER 3rd

8:00-10:30 AM (EDT)

10 AM-12:30 PM (BRT)