4. bpp 604 business law edited 112 slides my april 18 2015

TRANSCRIPT

04/18/2023 ExcelBright Training Consultants SB

1

BPP 604BUSINESS LAW

KSKV

BPP 604BUSINESS LAW

KSKV

Bahagian Pendidikan Teknik Dan Vokasional (BPTV) KPM

04/18/2023 ExcelBright Training Consultants SB

2

Learning Outcomes

1.Describe precisely the concept of law in Malaysia with regards to its definition and classification.

2.Explain clearly the application of law regarding contract and sale of goods

3.Identify accurately the principles of consumer protection such as hire-purchase and direct sales

At the END of the COURSE, students should be able to:

04/18/2023 ExcelBright Training Consultants SB

3

Suggested Modified Learning Outcomes

At the end of the COURSE, students should be able to

• Understand and apply the laws and regulations related to enforcement agencies

04/18/2023 ExcelBright Training Consultants SB

4

INTRODUCTION TO THE CONCEPT OF LAW IN MALAYSIA

04/18/2023 5

Undang-Undang Malaysia

• PERKESO9 [SOCSO]– http://www.perkeso.gov.my/my/

• KWSP– http://

www.kwsp.gov.my/portal/ms/web/kwsp/home

• Mahkamah Buruh– Wrongful Dismissal

ExcelBright Training Consultants SB

04/18/2023 6

Undang-Undang Malaysia

ExcelBright Training Consultants SB

CONTOH PROSES UTAMA (JABATAN BURUH1.Penerimaan Aduan Buruh2.Penyiasatan Aduan- Aduan Buruh3.Kes Buruh4.Mahkamah Buruh5.Penghantaran Saman6.Maklumbalas Pelanggan7.Kempen Kesedaran

04/18/2023 7

Undang-undang Malaysia

• SSM• LHDN• Kastam• PBT [Pihak Berkuasa Tempatan]• PSMB [HRDF]

ExcelBright Training Consultants SB

04/18/2023 ExcelBright Training Consultants SB

8

PENDAFTARAN MAJIKAN & PEKERJA

– Majikan dan pekerja hendaklah didaftarkan dengan PERKESO dalam tempoh tidak lewat daripada 30 hari dari tarikh seseorang pekerja diambil bekerja.

– Simpan lengkap rekod pekerja 7 tahun

– Seseorang yang diambil bekerja oleh sesuatu majikan di bawah kontrak perkhidmatan atau perantisan merupakan seorang pekerja seperti mana takrifan di bawah Akta. Perlindungan PERKESO hanyalah untuk pekerja warganegara Malaysia dan Pemastautin Tetap sahaja. Semua pekerja yang layak perlu didaftar dan dicarumkan dengan PERKESO tanpa mengira status perkhidmatannya sama ada sementara, sambilan, percubaan, kontrak atau telah disahkan dalam jawatan.

04/18/2023 ExcelBright Training Consultants SB

9

PENDAFTARAN MAJIKAN & PEKERJA

Pekerja yang layak diliputi di bawah AKSP 1969 adalah seperti berikut:• Bergaji RM3,000 atau kurang sebulan.

– Pekerja yang menerima gaji bulanan RM3,000 atau kurang, adalah wajib mendaftar dan mencarum.

• Prinsip ‘sekali layak-terus layak’.– Bagi pekerja yang telah mencarum dan kini bergaji melebihi

rm3,000 adalah wajib untuk terus mencarum selaras dengan prinsip ‘sekali layak terus layak’. Sekali pekerja berkenaan itu layak di bawah akta, beliau terus layak mencarum tanpa mengira jumlah gaji bulanannya selepas itu.

• Bergaji lebih daripada RM3,000 sebulan dan notis pemilihan– Pekerja yang menerima gaji melebihi RM3,000.00 sebulan dan

tidak layak di bawah AKSP 1969 / belum pernah mencarum, boleh memilih untuk mencarum dengan PERKESO melalui notis pemilihan.

04/18/2023 10

PENDAFTARAN MAJIKAN & PEKERJA

Pekerja yang tidak layak diliputi di bawah akta :• Bergaji melebihi RM3,000.00 & tidak pernah diliputi di bawah AKSP

1969• Suami atau isteri bagi majikan utama atau majikan langsung.• Sesiapa yang pekerjaannya berjenis sambilan dan yang diambil

bekerja bukan bagi maksud perusahaan majikannya.• Seseorang pekhidmat rumah tangga, iaitu seseorang yang diambil

bekerja semata-mata dalam kerja atau berkenaan dengan kerja bagi sesebuah rumah kediaman sendirian dan bukan kerja bagi apa-apa perdagangan, perniagaan atau profesyen yang dijalankan oleh majikan dalam rumah kediaman. Contoh; tukang masak, pekebun, jaga atau pemandu apa-apa kenderaan berlesen untuk kegunaan sendirian.

• Seseorang tributer, iaitu seseorang yang dibenarkan memperoleh apa-apa jenis galian atau hasil daripada atau atas tanah seseorang lain dan yang sebagai balasan bagi kebenaran itu, memberikan sebahagian galian atau hasil yang diperoleh itu kepada orang lain itu atau membayar kepadanya nilai bahagian itu.ExcelBright Training

Consultants SB

04/18/2023 ExcelBright Training Consultants SB

11

PENDAFTARAN MAJIKAN & PEKERJA

Pekerja yang tidak layak diliputi di bawah akta :• Pasukan bersenjata Malaysia• Pegawai polis• Seseorang yang ditahan dalam penjara, sekolah Henry

Gurney, sekolah yang diluluskan, tempat tahanan, hospital mental atau petempatan kusta.

• Setakat yang peruntukan akta ini berkaitan dengan pencen ilat :– (a) seseorang pekerja yang telah mencapai umur 60 tahun

dan yang berkenaan dengannya tiada caruman telah kena dibayar sebelum dia mencapai umur 55 tahun; atau

– (b) seseorang pekerja yang telah mencapai umur 60 tahun; atau

– (c) seseorang ilat diperakui yang menerima pencen ilat.

04/18/2023 12

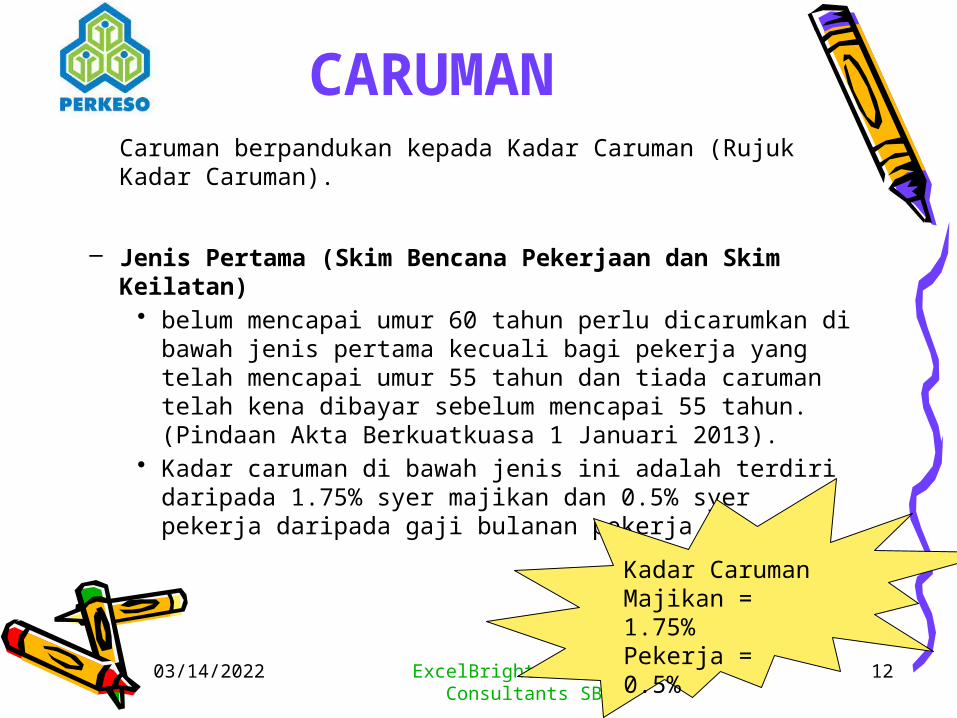

CARUMANCaruman berpandukan kepada Kadar Caruman (Rujuk Kadar Caruman).

– Jenis Pertama (Skim Bencana Pekerjaan dan Skim Keilatan)

• belum mencapai umur 60 tahun perlu dicarumkan di bawah jenis pertama kecuali bagi pekerja yang telah mencapai umur 55 tahun dan tiada caruman telah kena dibayar sebelum mencapai 55 tahun. (Pindaan Akta Berkuatkuasa 1 Januari 2013).

• Kadar caruman di bawah jenis ini adalah terdiri daripada 1.75% syer majikan dan 0.5% syer pekerja daripada gaji bulanan pekerja

ExcelBright Training Consultants SB

Kadar CarumanMajikan = 1.75%Pekerja = 0.5%

04/18/2023 13

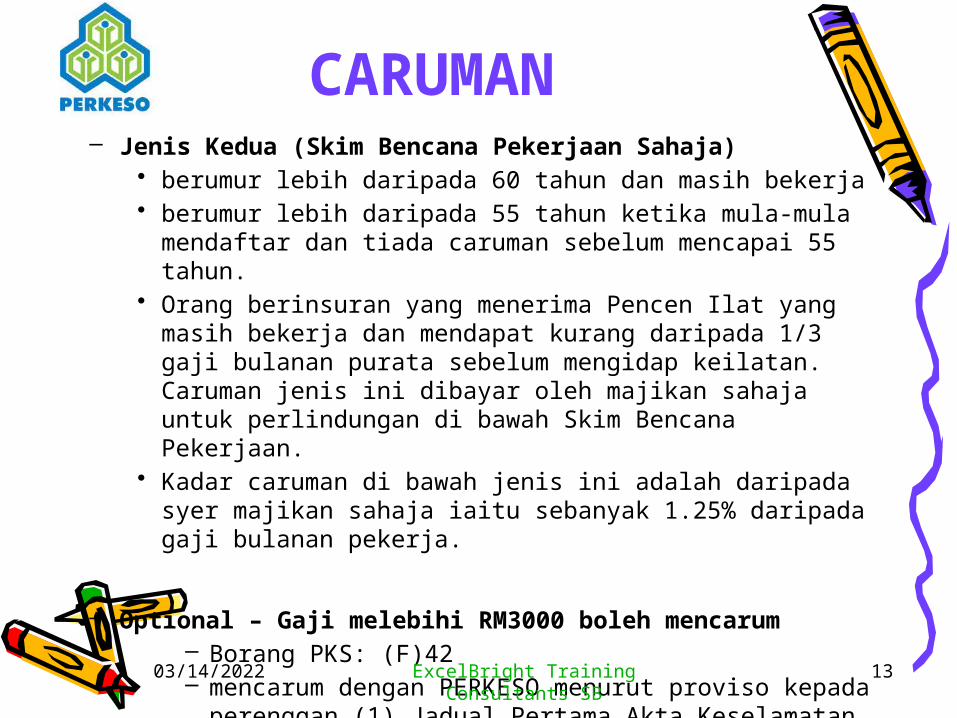

CARUMAN– Jenis Kedua (Skim Bencana Pekerjaan Sahaja)

• berumur lebih daripada 60 tahun dan masih bekerja• berumur lebih daripada 55 tahun ketika mula-mula

mendaftar dan tiada caruman sebelum mencapai 55 tahun.• Orang berinsuran yang menerima Pencen Ilat yang masih

bekerja dan mendapat kurang daripada 1/3 gaji bulanan purata sebelum mengidap keilatan. Caruman jenis ini dibayar oleh majikan sahaja untuk perlindungan di bawah Skim Bencana Pekerjaan.

• Kadar caruman di bawah jenis ini adalah daripada syer majikan sahaja iaitu sebanyak 1.25% daripada gaji bulanan pekerja.

– Optional – Gaji melebihi RM3000 boleh mencarum– Borang PKS: (F)42 – mencarum dengan PERKESO menurut proviso kepada

perenggan (1) Jadual Pertama Akta Keselamatan Sosial Pekerja 1969. ExcelBright Training

Consultants SB

04/18/2023 ExcelBright Training Consultants SB

14

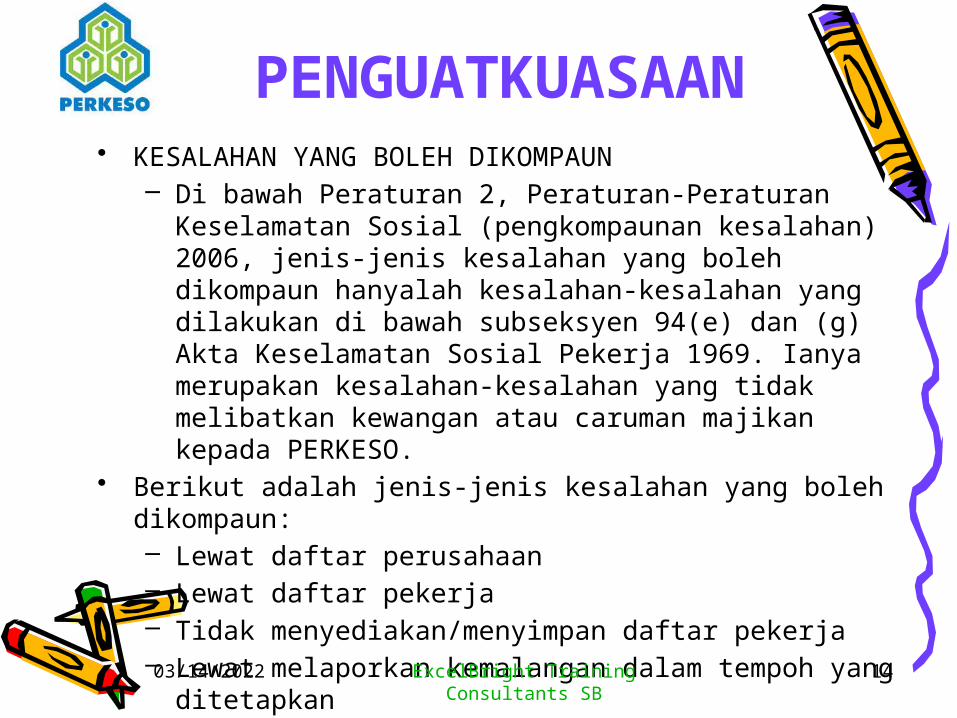

PENGUATKUASAAN• KESALAHAN YANG BOLEH DIKOMPAUN

– Di bawah Peraturan 2, Peraturan-Peraturan Keselamatan Sosial (pengkompaunan kesalahan) 2006, jenis-jenis kesalahan yang boleh dikompaun hanyalah kesalahan-kesalahan yang dilakukan di bawah subseksyen 94(e) dan (g) Akta Keselamatan Sosial Pekerja 1969. Ianya merupakan kesalahan-kesalahan yang tidak melibatkan kewangan atau caruman majikan kepada PERKESO.

• Berikut adalah jenis-jenis kesalahan yang boleh dikompaun:– Lewat daftar perusahaan– Lewat daftar pekerja– Tidak menyediakan/menyimpan daftar pekerja– Lewat melaporkan kemalangan dalam tempoh yang

ditetapkan– Tidak menyediakan jadual pembayaran caruman

04/18/2023 ExcelBright Training Consultants SB

15

PENGUATKUASAAN• Amaun kompaun yang boleh dikenakan hendaklah

tidak melebihi lima puluh peratus (50%) daripada amaun denda maksimum bagi kesalahan itu. Jumlah maksimum kompaun yang boleh dikenakan ialah RM 5,000 atau apa-apa amaun yang ditetapkan oleh Pertubuhan

• Pihak PERKESO akan datang ke premis untuk membuat AUDIT

04/18/2023 16

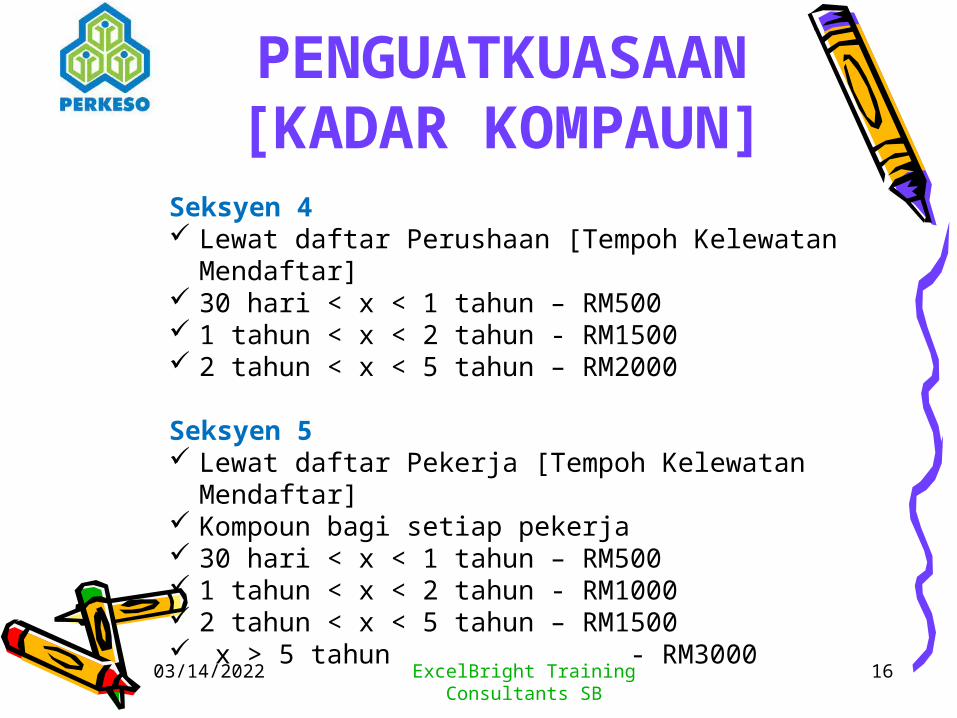

PENGUATKUASAAN [KADAR KOMPAUN]

ExcelBright Training Consultants SB

Seksyen 4 Lewat daftar Perushaan [Tempoh Kelewatan

Mendaftar] 30 hari < x < 1 tahun – RM500 1 tahun < x < 2 tahun - RM1500 2 tahun < x < 5 tahun – RM2000

Seksyen 5 Lewat daftar Pekerja [Tempoh Kelewatan

Mendaftar] Kompoun bagi setiap pekerja 30 hari < x < 1 tahun – RM500 1 tahun < x < 2 tahun - RM1000 2 tahun < x < 5 tahun – RM1500 x > 5 tahun - RM3000

04/18/2023 17

PENGUATKUASAAN [KADAR KOMPAUN]

ExcelBright Training Consultants SB

Peraturan 34(1) & (2)

Gagal Menyediakan / Menyimpan Daftar Pekerja dalam tempoh 7 tahun pada masa di AUDIT - RM300

Bila di AUDIT sekali lagi atas kesalahan sama - RM600

04/18/2023 18

PENGUATKUASAAN [KADAR KOMPAUN]

ExcelBright Training Consultants SB

Peraturan 44A

Gagal Menyediakan Jadual Caruman

Kes Kematian

2 bulan < x < 1 tahun - RM1000 x > 1 tahun - RM1500

Kecederaan kemalangan semasa perjalanan

3 bulan < x < 1 tahun - RM1000 x > 1 tahun - RM1500

04/18/2023 19

PENGUATKUASAAN [KADAR KOMPAUN]

ExcelBright Training Consultants SB

Peraturan 77A

Gagal Menyediakan / Menyimpan Daftar Pekerja dalam tempoh 7 tahun pada masa di AUDIT - RM300

Bila di AUDIT sekali lagi atas kesalahan sama - RM600

04/18/2023 20

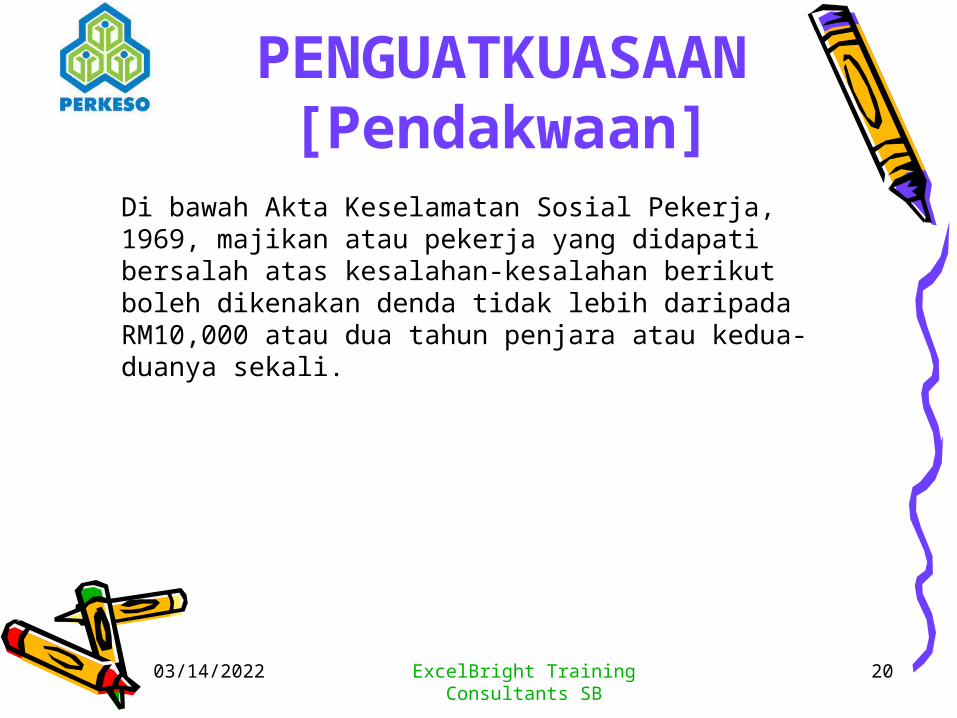

PENGUATKUASAAN [Pendakwaan]

ExcelBright Training Consultants SB

Di bawah Akta Keselamatan Sosial Pekerja, 1969, majikan atau pekerja yang didapati bersalah atas kesalahan-kesalahan berikut boleh dikenakan denda tidak lebih daripada RM10,000 atau dua tahun penjara atau kedua-duanya sekali.

04/18/2023 21

PENGUATKUASAAN [Pendakwaan]

ExcelBright Training Consultants SB

Jenis-Jenis Kesalahan Yang Boleh DidakwaBil Peruntukan Perundangan Jenis Kesalahan

1. Seksyen 4 Gagal atau lewat mendaftar perusahaan

2. Seksyen 5 dan Peraturan 12(1) Gagal atau lewat mendaftar pekerja yang layak

3. Seksyen 6(1)&(8) dan Peraturan 32 Gagal atau lewat membayar caruman

4. Seksyen 14(A)&Peraturan 33 Gagal membayar Faedah Caruman Lewat Bayar

5. Peraturan 71(1)&(2) Majikan gagal atau lewat lapor kemalangan

6. Seksyen 93(A)Memberi, membuat atau mengemukakan dokumen atau maklumat palsu

7. Seksyen 110(1) Gagal mematuhi saman jabatan

04/18/2023 ExcelBright Training Consultants SB

22

FAQ - PERKESO• 1) S : SIAPAKAH YANG DIKATEGORIKAN SEBAGAI

PEKERJA DI BAWAH AKTA KESELAMATAN SOSIAL PEKERJA 1969?

• J : Pekerja yang dimaksudkan adalah seorang yang diambil bekerja dengan bergaji di bawah satu kontrak perkhidmatan atau kontrak perantisan dengan seorang majikan, sama ada kontrak itu nyata atau disifatkan ada atau dengan lisan atau dengan bertulis, dalam atau berhubung dengan kerja sesuatu perusahaan yang diliputi di bawah Akta.

04/18/2023 ExcelBright Training Consultants SB

23

FAQ - PERKESO• 2) S : ADAKAH PEKERJA SEMENTARA/PEKERJA TIDAK

TETAP WAJIB DILINDUNGI OLEH PERKESO?• J : Pekerja sementara atau tidak tetap adalah wajib

didaftarkan dengan PERKESO.

• 3) S : PERLUKAH MAJIKAN MEMAKLUMKAN KEPADA PERKESO BAGI PEKERJA YANG BERHENTI?

• J : Majikan perlu mengisi tarikh pekerja berhenti di dalam borang 8A dan membuat tanda X di ruang-ruang Borang 8A.

04/18/2023 ExcelBright Training Consultants SB

24

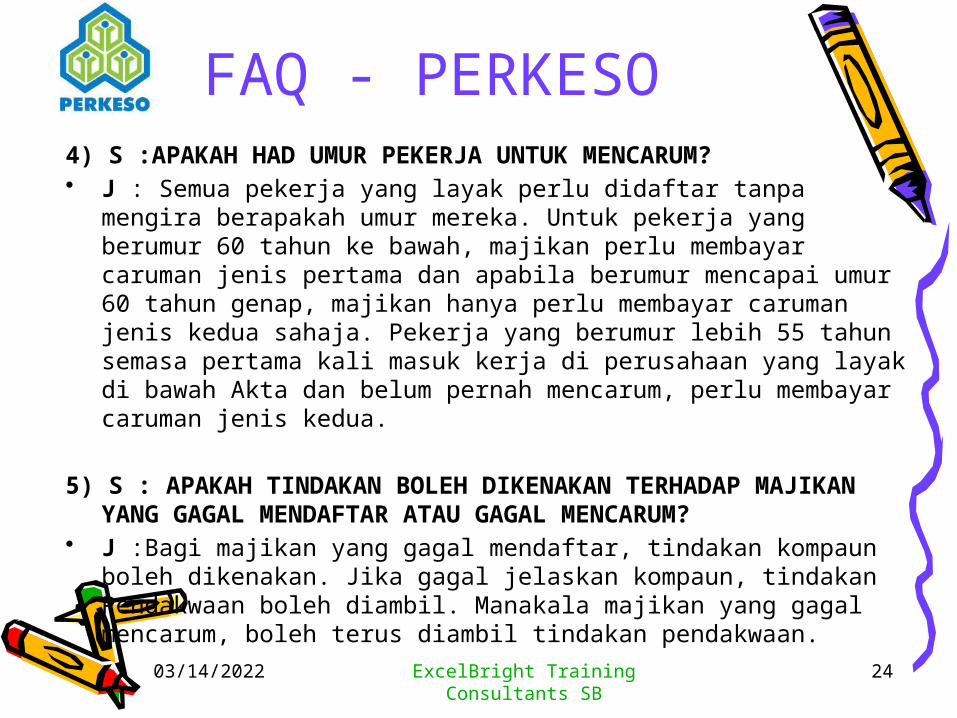

FAQ - PERKESO4) S :APAKAH HAD UMUR PEKERJA UNTUK MENCARUM?• J : Semua pekerja yang layak perlu didaftar tanpa mengira

berapakah umur mereka. Untuk pekerja yang berumur 60 tahun ke bawah, majikan perlu membayar caruman jenis pertama dan apabila berumur mencapai umur 60 tahun genap, majikan hanya perlu membayar caruman jenis kedua sahaja. Pekerja yang berumur lebih 55 tahun semasa pertama kali masuk kerja di perusahaan yang layak di bawah Akta dan belum pernah mencarum, perlu membayar caruman jenis kedua.

5) S : APAKAH TINDAKAN BOLEH DIKENAKAN TERHADAP MAJIKAN YANG GAGAL MENDAFTAR ATAU GAGAL MENCARUM?

• J :Bagi majikan yang gagal mendaftar, tindakan kompaun boleh dikenakan. Jika gagal jelaskan kompaun, tindakan Pendakwaan boleh diambil. Manakala majikan yang gagal mencarum, boleh terus diambil tindakan pendakwaan.

04/18/2023 ExcelBright Training Consultants SB

25

FAQ - PERKESO6) S : BAGAIMANAKAH MENENTUKAN KADAR CARUMAN?• J : Kadar caruman pekerja adalah berdasarkan kepada gaji

pekerja iaitu termasuk upah, kerja lebih masa, komisen dan caj perkhidmatan, bayaran cuti tahun, sakit, bersalin, rehat, kelepasan am, elaun insentif, sara hidup dan sebagainya. Semua pembayaran sama ada mengikut jam, harian, mingguan, bulanan, hasil kerja adalah dianggap gaji. Kadar caruman bulanan bagi syer majikan dan syer pekerja adalah seperti ditunjukkan pada Jadual Caruman berdasarkan 34 kategori gaji.

7) S : DI MANAKAH PEMBAYARAN CARUMAN BOLEH DILAKUKAN?

• J : Bayaran caruman boleh dilakukan di bank-bank yang telah dilantik seperti Maybank, CIMB, Public Bank, RHB, Pejabat-pejabat Pos (bagi Sabah & Sarawak) dan bank-bank yang dikhaskan bagi kawasan tertentu.

04/18/2023 ExcelBright Training Consultants SB

26

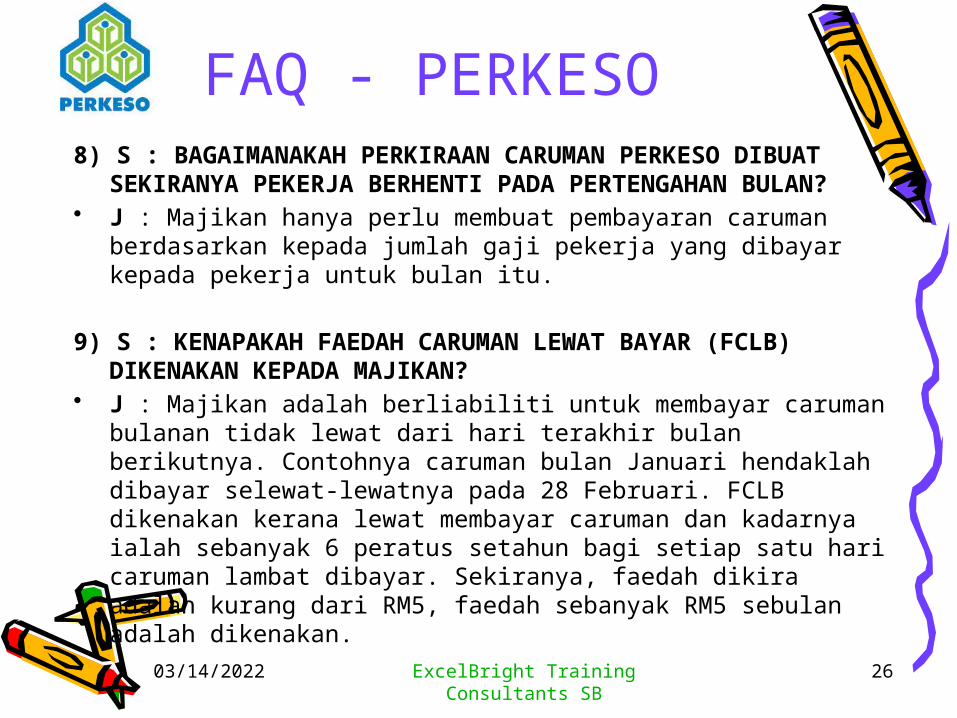

FAQ - PERKESO8) S : BAGAIMANAKAH PERKIRAAN CARUMAN PERKESO

DIBUAT SEKIRANYA PEKERJA BERHENTI PADA PERTENGAHAN BULAN?

• J : Majikan hanya perlu membuat pembayaran caruman berdasarkan kepada jumlah gaji pekerja yang dibayar kepada pekerja untuk bulan itu.

9) S : KENAPAKAH FAEDAH CARUMAN LEWAT BAYAR (FCLB) DIKENAKAN KEPADA MAJIKAN?

• J : Majikan adalah berliabiliti untuk membayar caruman bulanan tidak lewat dari hari terakhir bulan berikutnya. Contohnya caruman bulan Januari hendaklah dibayar selewat-lewatnya pada 28 Februari. FCLB dikenakan kerana lewat membayar caruman dan kadarnya ialah sebanyak 6 peratus setahun bagi setiap satu hari caruman lambat dibayar. Sekiranya, faedah dikira adalah kurang dari RM5, faedah sebanyak RM5 sebulan adalah dikenakan.

04/18/2023 ExcelBright Training Consultants SB

27

FAQ - PERKESO10) S : BAGAIMANAKAH CARA UNTUK MEMBAYAR FCLB?• J : FCLB boleh dibayar di Bank RHB dan Public Bank sahaja

dengan mengemukakan notis surat FCLB kepada bank untuk dicop tarikh terima dan nyatakan nombor akaun PERKESO untuk pembayaran. Majikan tidak perlu mengisi slip bank. Pembayaran cek bagi setiap satu bulan FCLB hendaklah diasingkan. Bayaran juga boleh dibuat dimana-mana Pejabat PERKESO.

04/18/2023 ExcelBright Training Consultants SB

28

FAQ - PERKESO

11) S : BAGAIMANAKAH MELAPORKAN KEMALANGAN DAN DOKUMEN-DOKUMEN YANG DIPERLUKAN UNTUK MEMBUAT TUNTUTAN?

• J : Majikan hendaklah melaporkan kepada PERKESO dengan mengisi Laporan Kemalangan (Borang 21) dan kemukakan bersama Borang Tuntutan (Borang 10), kad perakam waktu atau rekod kedatangan, sijil cuti sakit dan salinan kad pengenalan kepada Pejabat PERKESO berkenaan untuk kemalangan semasa di tempat kerja. Jikalau kemalangan berlaku semasa ke tempat kerja atau balik kerja, perlu disertakan laporan polis dan peta lakar yang menunjukkan arah perjalanan yang dilalui pekerja semasa kemalangan.

04/18/2023 29

FAQ - PERKESO12) S : ADAKAH PERKESO TANGGUNG KOS RAWATAN

PERUBATAN? DI MANAKAH BOLEH PEROLEHI RAWATAN?

• J : Seseorang pekerja yang ditimpa kemalangan berkaitan pekerjaan, perjalanan atau menghidap penyakit khidmat layak menerima rawatan perubatan percuma di klinik panel PERKESO atau klinik/hospital kerajaan.

13) S : DALAM KEADAAN MANAKAH ELAUN LAYANAN SENTIASA DIBAYAR?

• J : Kadar elaun ialah 40% daripada kadar faedah hilang upaya langsung yang kekal tertakluk kepada bayaran maksimum sebanyak RM500 sebulan (Berkuatkuasa mulai Januari 2013, kadar elaun tersebut telah ditetapkan sebanyak RM500 sebulan). Bayaran dibuat terus kepada penerima faedah.

ExcelBright Training Consultants SB

04/18/2023 ExcelBright Training Consultants SB

30

Isu Pentadbiran

• OPTION PENGAMBILAN PEKERJA:– Lantihan industri– Sambilan– Kontrak– Tetap

• RISIKO KEPADA SYARIKAT:– Saman/tuntutan oleh pekerja– Case Study: Premier Ayer Sdn Bhd - Kontraktor

NRW untuk SYABAS.

04/18/2023 ExcelBright Training Consultants SB

31

KWSP• KWSP merupakan sebuah institusi keselamatan sosial

yang ditubuhkan di bawah Undang-Undang Malaysia, Akta Kumpulan Wang Simpanan Pekerja 1991 (Akta 452) yang menyediakan faedah persaraan kepada ahlinya melalui pengurusan simpanan mereka secara cekap dan boleh dipercayai.

• KWSP juga menyediakan sistem yang efisien dan mudah bagi memastikan para majikan memenuhi tanggungjawab undang-undang serta kewajipan moral mereka untuk mencarum kepada KWSP bagi pihak pekerja mereka.

http://www.kwsp.gov.my/portal/ms/web/kwsp/home

04/18/2023 ExcelBright Training Consultants SB

32

KWSPMajikan• Majikan adalah orang yang dengannya seseorang pekerja

telah membuat kontrak perkhidmatan atau perantisan.• Majikan termasuklah:• Pengurus, ejen atau orang yang bertanggungjawab bagi

pembayaran gaji atau upah kepada seseorang 'pekerja';• Mana-mana kumpulan orang sama ada atau tidak berkanun

atau diperbadankan;• Mana-mana Kerajaan, jabatan Kerajaan, badan-badan

berkanun, pihak-pihak berkuasa tempatan atau badan-badan lain yang dinyatakan di dalam Jadual Kedua, Akta KWSP 1991.

Pekerja• Pekerja adalah orang yang diambil bekerja oleh majikan di

bawah suatu kontrak perkhidmatan atau perantisan. Kontrak perkhidmatan atau perantisan itu boleh dalam secara bertulis atau secara lisan, nyata atau tersirat.http://www.kwsp.gov.my/portal/ms/web/kwsp/home

04/18/2023 ExcelBright Training Consultants SB

33

KWSP

Tanggungjawab Majikan

UpahSemua saraan dalam bentuk wang yang kena dibayar kepada pekerja di bawah kontrak perkhidmatan atau perantisan sama ada ia dipersetujui untuk dibayar secara bulanan, mingguan, harian atau selainnya.

04/18/2023 ExcelBright Training Consultants SB

34

KWSPTanggungjawab MajikanAntara bayaran yang dikenakan caruman KWSP: Gaji Bayaran bagi cuti rehat tahunan dan cuti sakit yang tidak

digunakan Bonus Elaun Komisen Insentif Tunggakan upah Upah bagi cuti bersalin Upah bagi cuti belajar Upah bagi cuti separuh gaji Bayaran-bayaran lain di bawah kontrak perkhidmatan atau

sebaliknya

04/18/2023 ExcelBright Training Consultants SB

35

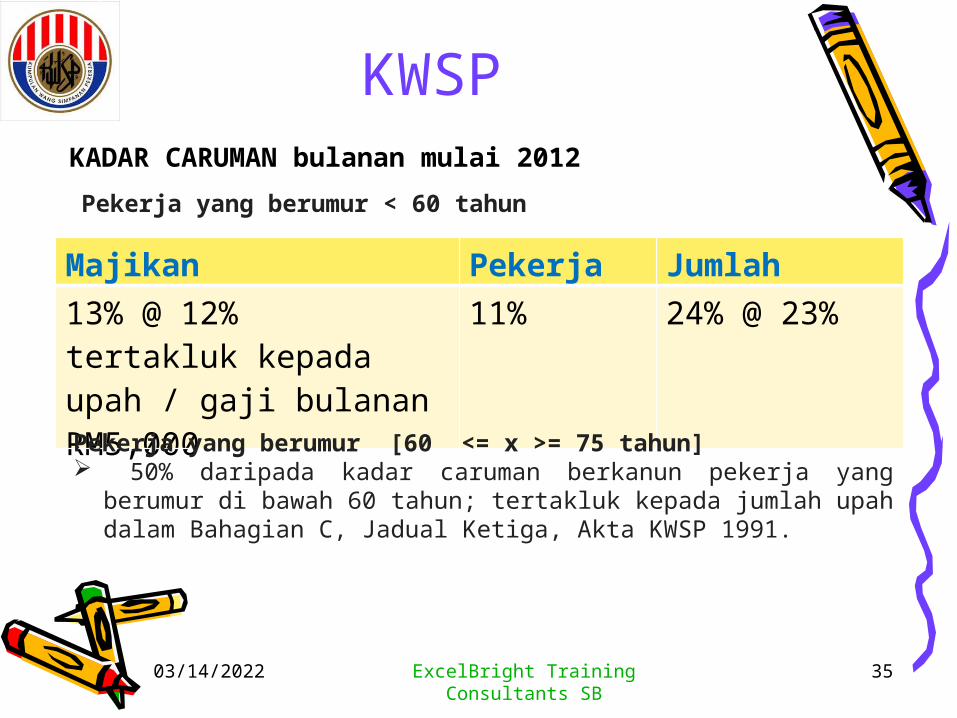

KWSPKADAR CARUMAN bulanan mulai 2012

Majikan Pekerja Jumlah

13% @ 12%tertakluk kepada upah / gaji bulanan RM5,000

11% 24% @ 23%

Pekerja yang berumur < 60 tahun

Pekerja yang berumur [60 <= x >= 75 tahun] 50% daripada kadar caruman berkanun pekerja yang berumur di

bawah 60 tahun; tertakluk kepada jumlah upah dalam Bahagian C, Jadual Ketiga, Akta KWSP 1991.

04/18/2023 ExcelBright Training Consultants SB

36

KWSP

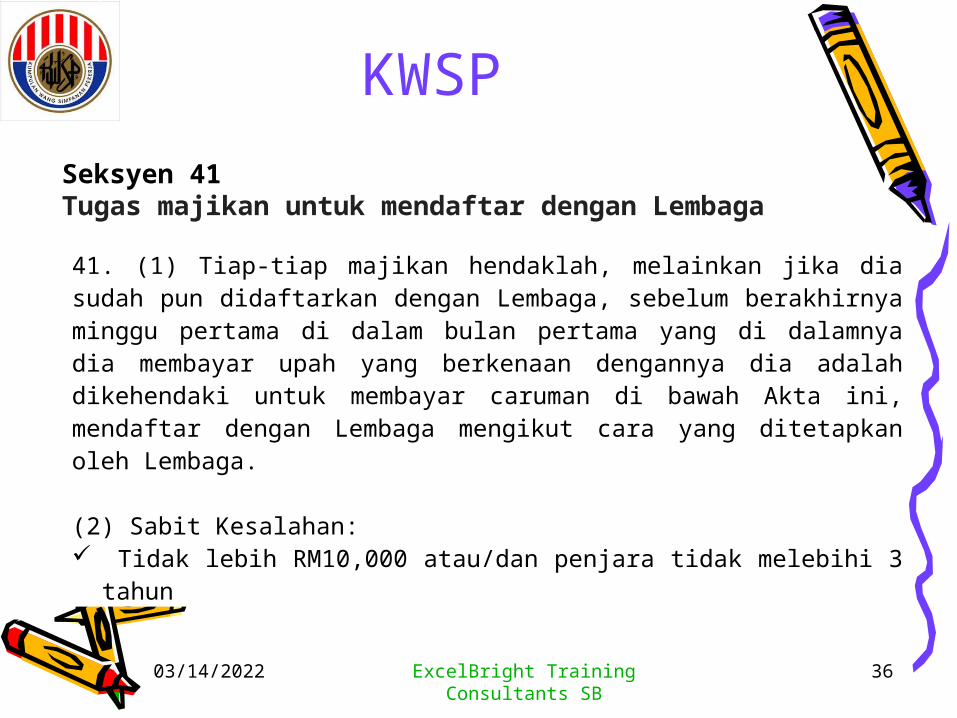

41. (1) Tiap-tiap majikan hendaklah, melainkan jika dia sudah pun didaftarkan dengan Lembaga, sebelum berakhirnya minggu pertama di dalam bulan pertama yang di dalamnya dia membayar upah yang berkenaan dengannya dia adalah dikehendaki untuk membayar caruman di bawah Akta ini, mendaftar dengan Lembaga mengikut cara yang ditetapkan oleh Lembaga.

(2) Sabit Kesalahan: Tidak lebih RM10,000 atau/dan penjara tidak melebihi 3 tahun

Seksyen 41Tugas majikan untuk mendaftar dengan Lembaga

04/18/2023 ExcelBright Training Consultants SB

37

KWSPSeksyen 42Tugas majikan untuk menyediakan dan memberikan penyata upah

Simpan Dokumen 6 tahun

04/18/2023 ExcelBright Training Consultants SB

38

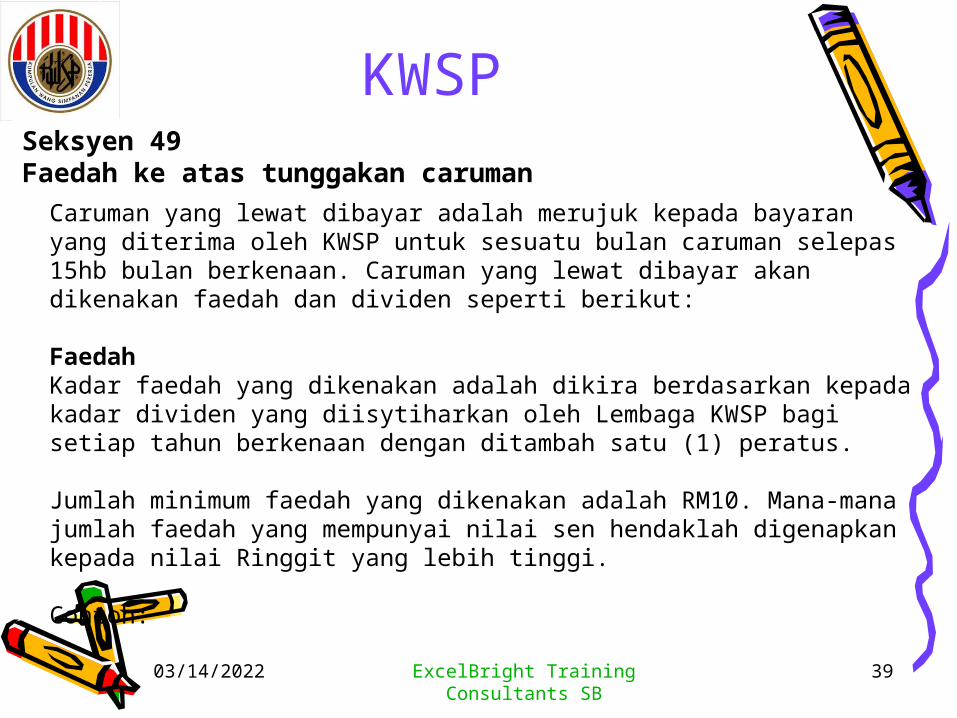

KWSPSeksyen 49Faedah ke atas tunggakan caruman

49. (1) Jika amaun caruman bulanan atau sebahagian daripada mana-mana caruman bulanan yang seseorang majikan adalah bertanggungan untuk membayar di bawah seksyen 45 tidak dibayar dalam apa-apa tempoh sebagaimana yang ditetapkan oleh Menteri, majikan itu hendaklah bertanggungan, sebagai tambahan kepada dividen yang hendaklah dibayar di bawah subseksyen 45(3), untuk membayar faedah yang hendaklah dikreditkan kepada Kumpulan Wang ke atas amaun itu pada apa-apa kadar dan mengikut apa-apa cara dan pengiraan yang ditentukan oleh Lembaga.

04/18/2023 ExcelBright Training Consultants SB

39

KWSPSeksyen 49Faedah ke atas tunggakan caruman

Caruman yang lewat dibayar adalah merujuk kepada bayaran yang diterima oleh KWSP untuk sesuatu bulan caruman selepas 15hb bulan berkenaan. Caruman yang lewat dibayar akan dikenakan faedah dan dividen seperti berikut:

FaedahKadar faedah yang dikenakan adalah dikira berdasarkan kepada kadar dividen yang diisytiharkan oleh Lembaga KWSP bagi setiap tahun berkenaan dengan ditambah satu (1) peratus.

Jumlah minimum faedah yang dikenakan adalah RM10. Mana-mana jumlah faedah yang mempunyai nilai sen hendaklah digenapkan kepada nilai Ringgit yang lebih tinggi.

Contoh:

04/18/2023 ExcelBright Training Consultants SB

40

KWSPSeksyen 49Faedah ke atas tunggakan caruman

Contoh:Faedah yang dikenakan ialah RM13.21 dan ianya hendaklah digenapkan kepada RM14 (Ringgit yang lebih tinggi).

Dividen

Kadar dividen yang dikenakan adalah dikira berdasarkan kepada kadar dividen yang diisytiharkan oleh Lembaga KWSP bagi setiap tahun berkenaan.Caruman yang dianggap lewat dibayar adalah termasuk:Caruman tertunggak;Caruman terkurang bayar

04/18/2023 ExcelBright Training Consultants SB

41

KWSPSeksyen 43Kadar caruman

Akta KWSP 1991 mewajibkan majikan membayar caruman bulanan sebelum atau pada 15hb. setiap bulan.Denda antara RM1000 hingga RM8000 bagi kesalahan di bawah seksyen 43(2) Akta KWSP 1991.

04/18/2023 ExcelBright Training Consultants SB

42

KWSPSeksyen 60Penalti am

60. Mana-mana orang yang melanggar mana-mana peruntukan Akta ini atau mana-mana peraturan atau kaedah yang dibuat di bawahnya adalah melakukan suatu kesalahan dan jika tiada penalti khas diperuntukkan dengan nyata dalam Akta ini atau peraturan-peraturan atau kaedah-kaedah yang dibuat di bawahnya itu,

Sabit Kesalahan = dipenjarakan selama suatu tempoh yang tidak melebihi 6 bulan atau didenda tidak melebihi RM2000 atau kedua-duanya.

04/18/2023 ExcelBright Training Consultants SB

43

KWSPSeksyen 49Faedah ke atas tunggakan caruman

Sekiranya caruman bulanan atau sebahagian dari caruman bulanan yang wajib dibayar oleh majikan tidak dijelaskan dalam tempoh yang ditetapkan, majikan akan dikenakan faedah penalti atas jumlah tersebut.

Menurut Seksyen 8(3), Akta KWSP 1951, yang berkuatkuasa mulai Januari 1987, majikan juga dikehendaki membayar dividen yang terakru di bawah seksyen 12(2) Akta KWSP 1951, ke atas caruman tersebut.

Faedah penalti dan dividen akibat dari pembayaran caruman yang lewat boleh dianggap sebagai kecuaian kawalan wang kerajaan dan pegawai yang cuai tersebut boleh diambil tindakan surcaj atau tindakan tatatertib,

04/18/2023 ExcelBright Training Consultants SB

44

KWSPSeksyen 49Faedah ke atas tunggakan caruman

Lazimnya, pihak mahkamah akan memberi majikan peluang untuk membayar secara ansuran sebanyak enam kali untuk menjelaskan tunggakan caruman. Dalam tempoh tersebut, pihak KWSP akan memantau majikan terbabit bagi memastikan tunggakan tersebut dibayar sepenuhnya dan dikreditkan ke akaun ahli.

04/18/2023 ExcelBright Training Consultants SB

45

KWSPKWSP SAMAN PERWAJA STEEL GAGAL BAYAR CARUMAN PEKERJA

http://pkrl.blogspot.com/2014/09/kwsp-saman-perwaja-steel-gagal-bayar.html

Perwaja Holdings dalam kenyataan kepada Bursa Malaysia berkata, KWSP telah menamakan Perwaja Steel dan sembilan pengarahnya sebagai defendan dalam samantersebut.

Dalam tuntutan itu, KWSP menuntut sejumlah RM4.6 juta daripada Perwaja Steel bagi tunggakan caruman pekerja manakala dividen dan faedah tunggakan yang terakru ke atas jumlah tunggakan akan dinilai oleh mahkamah daripada tarikh mula tunggakan sehingga penyelesaian, dan semua kos perundangan yang relavan terkandung dalam saman.

Perwaja Steel diberi 14 hari untuk memberi maklum balas.

04/18/2023 ExcelBright Training Consultants SB

46

LHDN

• Cukai Perniagaan– Syarikat - Fail C,– Soleproprietorship OG– Partnership - P– Trust, Artist, Hindu Joint Family [TFJ]

Tanggungjawab Syarikat

04/18/2023 ExcelBright Training Consultants SB

47

LHDN

• Hantar Borang E• Mendaftar Pekerja Baru, Berhenti• PCB [Potongan Cukai Berjadual] -

mandatory• Mengeluarkan Borang EA/EC

Tanggungjawab Majikan

04/18/2023 ExcelBright Training Consultants SB

48

LHDN

• Skim Ansuran CP204• Syarikat, perkongsian liabiliti terhad, badan amanah dan

koperasi yang belum memulakan operasi tidak perlu mengemukakan Borang CP204

• Bagi syarikat yang telah sedia beroperasi, anggaran cukai hendaklah dibayar secara ansuran yang sama banyak mulai bulan ke 2 tempoh asas bagi sesuatu tahun taksiran.

Tanggungjawab Syarikat

04/18/2023 ExcelBright Training Consultants SB

49

LHDN

• Denda Di Bawah Skim Ansuran• Denda dalam bentuk kenaikan cukai akan dikenakan jika:• Syarikat yang gagal membuat bayaran ansuran bulanan

sepenuhnya dalam tempoh ditetapkan, bayaran ansuran bulanan yang tidak dijelaskan akan dinaikkan sebanyak 10% tanpa sebarang notis diperlukan dari LHDNM.

• Jika perbezaan di antara cukai sebenar dan anggaran cukai dipinda anggaran asal cukai (jika tiada anggaran cukai dipinda dikemukakan) melebihi 30% dari cukai kena dibayar, cukai akan dinaikkan sebanyak 10% ke atas perbezaan melebihi 30% tanpa sebarang notis tambahan. Formula pengenaan denda ialah:

• Formula pengiraan amaun cukai yang dinaikkan seperti berikut;• Kenaikan cukai = [ (AT-ET) - (30%xAT) ] x 10%

Di mana: AT: Cukai sebenar yang kena dibayarET: Anggaran cukai dipinda atau anggaran cukai asal (jika tiada anggaran cukai dipinda dikemukakan).

Tanggungjawab Syarikat

04/18/2023 ExcelBright Training Consultants SB

50

LHDN

• Penalti Lewat Bayaran Baki Cukai• Jika baki cukai tidak dibayar pada tarikh ditetapkan,

penalti sebanyak 10% akan dikenakan. Jika amaun cukai dan penalti masih tidak dibayar selepas 60 hari dari tarikh ditetapkan, penalti tambahan sebanyak 5% akan dikenakan ke atas baki cukai dan penalti yang tidak dibayar.

• Rayuan Ke Atas Penalti• Rayuan secara bertulis dalam tempoh 30 hari dari tarikh

Notis Taksiran dikeluarkan perlu dikemukakan kepada Cawangan berkenaan (Unit Pungutan), jika syarikat tidak bersetuju terhadap penalti lewat bayar yang dikenakan.

• Syarikat perlu menjelaskan tanggungan cukai walaupun rayuan dibuat.

Tanggungjawab Syarikat

04/18/2023 ExcelBright Training Consultants SB

51

Kastam Pematuhan GST

• Goods and Services Tax [GST] • Berkuatkuasa 1 April 2015• Pendaftaran:

– Turnover > RM500,000 -> Mandatory– Turnover =< Rm500,000 -> Voluntary– Bulanan, 3 bulan, 6 bulan

http://gst.customs.gov.my/ms/Pages/default.aspx

04/18/2023 ExcelBright Training Consultants SB

52

Kastam Pematuhan GST

• Pengiraan Cukai Input dan Cukai Output• Mematuhi Borang GST04 • Pembayaran Cukai• Kesediaan:

– Sistem Perakaunan / PoS dengan pematuhan GST

– Staf yang siap sedia untuk pematuhan• Penalti yang berat terhadap 7 jenis kesalahan

04/18/2023 ExcelBright Training Consultants SB

53

Jabatan Tenaga Kerja, MOHR

&Mahkamah Buruh

04/18/2023 ExcelBright Training Consultants SB

54

Majikan Gagal Membayar Gaji

SELESAIKAN MASALAH PEMBAYARAN GAJI MELALUI JABATAN TENAGA KERJA• Masalah pembayaran gaji secara berjadual sering kali berlaku

terutamanya dalam sektor swasta dan permasalahan ini sering kali berlaku di mana-mana negeri termasuk negeri Kelantan.

• mengfailkan aduan kepada Jabatan Tenaga Kerja (JTK) yang berhampiran berkaitan tuntutan gaji yang tidak dibayar oleh majikan. Antara dokumen yang diperlukan adalah salinan kad pengenalan dan slip gaji terakhir yang ada (atau bawa semua sekali slip gaji). Anda kemudian perlu mengisi borang selengkapnya termasuk melengkapkan maklumat majikan seperti nama organisasi, alamat, no. telefon, no. faks, dan sebagainya. Slip gaji terakhir diperlukan untuk membolehkan JKT membuat anggaran bayaran gaji tertunggak yang perlu dilunaskan oleh majikan.

04/18/2023 ExcelBright Training Consultants SB

55

Majikan Gagal Membayar Gaji

MAHKAMAH BURUH• Mahkamah Buruh merupakan satu sistem quasi-judicial sebagai

alternatif kepada tuntutan sivil. Objektif Mahkamah Buruh adalah untuk menyediakan sistem pengadilan perburuhan yang adil, mudah, cepat dan murah bagi menyelesaikan tuntutan pekerja mengenai gaji dan lain-lain faedah kewangan yang layak dituntut terhadap mereka. Bersesuaian dengan rasional penubuhan sebagai mekanisme pengadilan membantu kebajikan pekerja. Mahkamah Buruh mempunyai ciri-ciri istimewa seperti berikut :

• membicarakan semua tuntutan pekerja tanpa sebarang had dari segi jumlah wang yang hendak dituntut.

• mengamalkan prosiding yang mudah dan tidak formal tetapi bertepatan dengan prinsip-prinsip keadilan yang diikuti oleh Mahkamah-Mahkamah Sivil. Amalan membicarakan kes buruh menurut prinsip-prinsip keadilan peraturan-peraturan Mahkamah Sivil telah diiktirafkan melalui keputusan-keputusan yang dibuat oleh Mahkamah Tinggi.

04/18/2023 ExcelBright Training Consultants SB

56

SSM

Acts & Regulations• Companies Commission of Malaysia (Amendment) Act 2015 gaz

etted on 5 January 2015 (to be read together with the Companies Commission of Malaysia Act 2001)

• Companies Commission of Malaysia Act 2001 (Act 614)• Companies Act 1965 (Act 125) (to be read together with the

Federal Government Gazette - Companies (Amendment of Schedule) Order 2013 dated 26 March 2013)

• Registration of Businesses Act 1956 (Act 197)• Trust Companies Act 1949 (Act 100)• Kootu Funds (Prohibition) Act 1971 (Act 28)• Act A1299 COMPANIES (AMENDMENT) ACT 2007• Limited Liability Partnerships Act 2012

04/18/2023 ExcelBright Training Consultants SB

57

SSM

Regulations• Companies Regulations 1966; • Registration of Businesses Rules 1957• Limited Liability Partnership Regulations 2012

04/18/2023 ExcelBright Training Consultants SB

58

SSM

Compliance Issues• Appointment of Company Secretary• Audited Report – annual submission• Penalties Loading

04/18/2023 ExcelBright Training Consultants SB

59

HRDFHuman Resources Development Levy• The Human Resources Development Levy is the mandatory

levy payment imposed by the Government on specified groups of employers for the purpose of employee training and skills upgrading.

• Under the law, certain categories of employers are liable to pay a Human Resource Development levy for each working employee at the rate of 1.0% of the monthly wages of the employee.

• However, the Minister of Human Resources may, from time to time, by order published in the Gazette, reduce or increase the rate of the levy specified.

• The minister is also empowered to exempt fully or partially any of the employers from the payment of this levy.

1% @ monthly wages of employee

04/18/2023 ExcelBright Training Consultants SB

60

HRDFCategories of Employers Covered Under the PSMB Act, 2001• Employers with 50 Malaysian employees and above in

the manufacturing sector (w.e.f. 1 January 1993)• Employers with 10 to 49 Malaysian employees and a

paid-up capital of RM2.5 million and above in the manufacturing sector (w.e.f. 1 January 1995)

04/18/2023 ExcelBright Training Consultants SB

61

HRDFCategories of Employers Covered Under the PSMB Act, 2001• Employers with 10 Malaysian employees and above in 21

selected industries in the services sector, among others; hotel industry, tour operating business (in-bound tour only), shipping, air transport, telecommunication, computer services, advertising, postal & courier services and freight forwarding (w.e.f. 1 January 1995); private higher education, training and the energy sector (w.e.f. 17 February 2000); and direct selling, port services, engineering support and maintenance services, research and development, warehousing services, security services, private hospital services and hypermarkets, supermarkets and departmental stores - (w.e.f. 1 January 2005). For hypermarkets, supermarkets and departmental stores, only employers with 50 Malaysian employees and above are required to register. Commercial land transport and railway transport services industry with 10 employees and above (w.e.f. 1 December 2007)

04/18/2023 ExcelBright Training Consultants SB

62

HRDFCategories of Employers Covered Under the PSMB Act, 2001• Employers in the manufacturing sector with 10 to 49

Malaysian employees and a paid-up capital of less than RM2.5 million are given the option to register with PSMB (w.e.f. 2 August 1996).

• Employer with 50 Malaysian employees and above in the mining and quarrying sector (w.e.f 1 June 2014)

• Employers with 10 to 49 Malaysian employees and a paid-up capital of RM2.5 million and above in the mining and quarrying sector (w.e.f 1 June 2014)

04/18/2023 ExcelBright Training Consultants SB

63

HRDFCategories of Employers Covered Under the PSMB Act, 2001• Employers with 10 Malaysian employees and above in 17

selected industries in the services sector, namely, gas, steam and air-conditioning supply, water treatment and supply, sewerage, waste management and material recovery services; production of motion picture, video and television programme, sound recording and music publishing, information service activities, tourism enterprise, building and landscape services, event management services, early childhood education, health support services, franchise, sale and repair of motor vehicles, private broadcasting services, driving school and veterinary services (w.e.f 1 June 2014)

04/18/2023 ExcelBright Training Consultants SB

64

HRDFCategories of Employers Covered Under the PSMB Act, 2001• Employer with 30 Malaysian employees and above in food

and beverage services (w.e.f. 1 June 2014)• Employers in the mining and quarrying sector with 10 to 49

Malaysian employees and a paid-up capital of less than RM2.5 million are given the option to register with PSMB (w.e.f. 1 June 2014).

04/18/2023 ExcelBright Training Consultants SB

65

HRDFCategories of Employers Covered Under the PSMB Act, 2001• Under Regulation 4(1) of the Pembangunan Sumber Manusia

Berhad (Registration of Employers and Payment of Levy) Regulations 2001, employers have 30 days to register with PSMB from the date they are liable. Employers falling in any of the categories elaborated are still liable to register with PSMB under the Pembangunan Sumber Manusia Berhad Act, 2001. Those who have yet to register are advised to do so, failing which legal actions shall be taken against them.

04/18/2023 ExcelBright Training Consultants SB

66

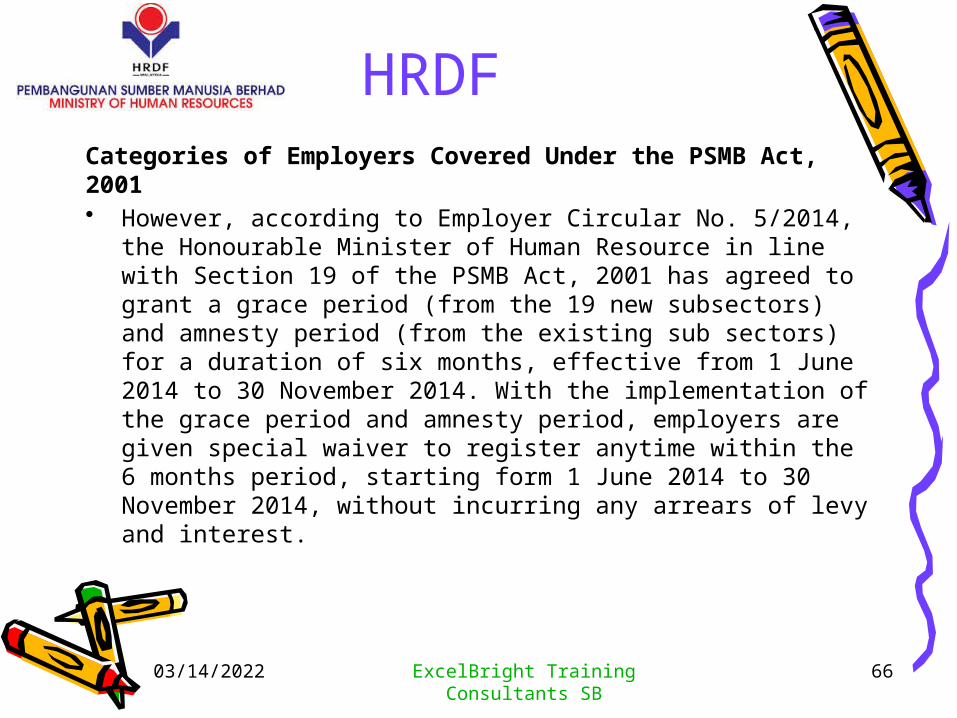

HRDFCategories of Employers Covered Under the PSMB Act, 2001• However, according to Employer Circular No. 5/2014, the

Honourable Minister of Human Resource in line with Section 19 of the PSMB Act, 2001 has agreed to grant a grace period (from the 19 new subsectors) and amnesty period (from the existing sub sectors) for a duration of six months, effective from 1 June 2014 to 30 November 2014. With the implementation of the grace period and amnesty period, employers are given special waiver to register anytime within the 6 months period, starting form 1 June 2014 to 30 November 2014, without incurring any arrears of levy and interest.

04/18/2023 ExcelBright Training Consultants SB

67

HRDFEligibility For Training Grant• Employers registered and/or incorporated in Malaysia who

have registered with PSMB and pay the HRD levy immediately upon registration are eligible to apply for training grants (financial assistance) to defray all or a major portion of the "allowable costs" of training their employees. Training must be in the area of direct benefit to their business operations. Financial assistance is, therefore, not given to individuals who enrol and finance their own training programmes, whether partially or fully, and subsequently requested for reimbursement from their employers. Neither is financial assistance given to employers who bear the cost of training after the successful completion of training by their employees.

04/18/2023 ExcelBright Training Consultants SB

68

HRDF

To facilitate employers to send their employees for training, PSMB has introduced various training schemes as follows:• SBL Scheme• SBL-Khas Scheme• Annual Training Plan Scheme• Juruplan Scheme• SME Training Needs Analysis Consultancy Scheme• Joint Training Scheme• Apprenticeship Scheme• SME Training Partners (SMETAP) Scheme• Computer-Based Training Scheme

Training Schemes under PSMB

04/18/2023 ExcelBright Training Consultants SB

69

HRDF

To facilitate employers to send their employees for training, PSMB has introduced various training schemes as follows:• Information Technology and Computer-Aided Training Scheme• Purchase of Training Equipment and Setting Up of Training

Room Scheme• English Language Programmes for Workers under the HRDF• Industrial Training Scheme• SME On-The-Job Training Scheme• Recognition Prior Learning Scheme (RPL)• Future Workers Training Scheme

Training Schemes under PSMB

04/18/2023 ExcelBright Training Consultants SB

70

HRDF

PART VI - OFFENCES AND PENALTIES• Section 40. Incorrect declaration, failure to furnish return, etc.• Section 41. Penalty for attempting to obtain or obtaining

money or benefit by false or misleading• statement or document• Section 42. Repayment• Section 43. General penalty• Section 44. Offences by body corporate or other bodies• Section 45. Joint and several liability of directors, etc.• Section 46. Institution of prosecution• Section 47. Order to register or pay levy

Pembangunan Sumber Manusia Berhad Act, 2001 (PSMB Act, 2001)

04/18/2023 71

Law of Malaysia• The law of Malaysia is mainly based on the

common law legal system. This was a direct result of the colonisation ofMalaya, Sarawak, and North Borneo by Britain between the early 19th century to 1960s. The supreme law of the land—the Constitution of Malaysia—sets out the legal framework and rights of Malaysian citizens.

• Federal laws enacted by the Parliament of Malaysia apply throughout the country. There are also state laws enacted by the State Legislative Assemblies which applies in the particular state. The constitution of Malaysia also provides for a unique dual justice system—the secular laws (criminal and civil) and sharia laws.

ExcelBright Training Consultants SB

04/18/2023 ExcelBright Training Consultants SB

72

Origin of Law of Malaysia

• The law relating to contracts in India is contained in Indian Contract Act, 1872. The Act was passed by British India and is based on the principles of English Common Law.

• Income Tax Ordinance -> Income Tax Act 1957• Originated from UK -> India -> Hong Kong ->

Singapore -> Strait Settlements -> Federated Malay States.

04/18/2023 ExcelBright Training Consultants SB

73

LAW OF CONTRACTLAW OF CONTRACT

04/18/2023 ExcelBright Training Consultants SB

74

What is the Law of Contract 1950?

• The Contracts Act of 1950 is an act that involves contracts made between individuals and also the basic fundamentals of how a contract works or functions, and what actions can be taken if someone against the act and how the other people in contract can claim for damages or sue the people for damages done.

Read more at Law Teacher: http://www.lawteacher.net/free-law-essays/contract-law/case-study-of-the-contracts-act-1950-contract-law-essay.php#ixzz3XYCgYhu7

04/18/2023 ExcelBright Training Consultants SB

75

What is a contract?• A contract is a legally binding or valid agreement between

two parties. The law will consider a contract to be valid if the agreement contains all of the following elements:

• offer and acceptance;• an intention between the parties to create binding relations;• consideration to be paid for the promise made;• legal capacity of the parties to act;• genuine consent of the parties; and• legality of the agreement.• An agreement that lacks one or more of the elements listed

above is not a valid contract.

04/18/2023 ExcelBright Training Consultants SB

76

Must contracts be in writing?

• Not all contracts need to be in writing. Contracts that are required by law to be in writing include contracts to buy and sell land or to buy a motor car and door-to-door sales contracts. However, it is always useful to have the terms agreed between the parties written down and attached to or kept with any other relevant papers; for example, copies of quotations, brochures, pamphlets, etc. that were supplied at the time the contract was entered into. Receipts for money paid should always be kept. If a dispute arises, these documents will assist in resolving differences between the parties.

• A written contract can be drawn up by listing all the terms agreed between the parties and getting each of the parties to sign and date the document at the end.

04/18/2023 ExcelBright Training Consultants SB

77

Common contracts in business

• Asset:– Office – rent [Rental Agreement]/ purchase [S&P]– Equipment [purchase outright / lease]– Vehicle – outright purchase / Hire Purchase]

• Utilities – TNB, Syabas, Telekom• Contract with:

– Supplier– Creditor / Debtor– Customer / Client– Business associates

04/18/2023 ExcelBright Training Consultants SB

78

Common non-written contracts in business

• Based on– TRUST– COMPETENCY

Boleh Kautin, Kau Tau Boss

04/18/2023 ExcelBright Training Consultants SB

79

SALES OF GOODS

04/18/2023 ExcelBright Training Consultants SB

80

MPH Bookstore RM 9.00

04/18/2023 ExcelBright Training Consultants SB

81

Sale of Good Act 1957 [SOGA]

• The Sale of Good Act 1957 (SOGA herein forth) was enacted in 1957 and the statue was applicable to sale of goods in peninsular Malaysia (East Malaysia), excluding the states of Penang and Malacca.

• The Act was later revised in 1990 and it includes both states1. The states of Sabah and Sarawak (West Malaysia) are not governed by this act instead they are governed by section 5(2) of the Civil Law Act of 1956, which provides, among others, that the law to be administered in England in the like case at the correspondent period.

04/18/2023 ExcelBright Training Consultants SB

82

Sale of Good Act 1957 [SOGA]

• The English statue applied is the Sale of Goods Act 1979, which is a revision of the Sales of Goods Act 1893.As a result Sabah and Sarawak are bound by statute to continue to apply principles of English law relating to the sale of goods.

• The contrast between the laws West and East Malaysia has the potential to raise unwarranted legal problems, even though English statue is the principle source of law for both parts of Malaysia (Pheng, 1997; Beatrix and Wu, 1991).

04/18/2023 ExcelBright Training Consultants SB

83

Sale of Good Act 1957 [SOGA]

The Act contains definitions or interpretations which clarify what the wording used in it refers to and the context. Below are some of the definitions of key terms in the SOGA.• Buyer -a person who buys or agrees to buy goods.• Seller -a person who sells or agrees to sell goods.• Goods -means every kind of movable property other than

actionable claims and money; and includes stock and shares, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale.

04/18/2023 84

Sale of Good Act 1957 [SOGA]

The Act contains definitions or interpretations which clarify what the wording used in it refers to and the context. Below are some of the definitions of key terms in the SOGA.• specific goods - means goods identified and agreed upon at

the time a contract of sale is made; and any expression used but not defined in this Act which is defined in the Contracts Act 1950 [Act 136], shall have the meaning assigned to it in that Act.

• Future goods - means goods to be manufacture or produced or acquired by the seller after the making of the contract of sale.

ExcelBright Training Consultants SB

04/18/2023 85

Sale of Good Act 1957 [SOGA]

• When enacted it was applicable in Federal Territory, Johore, Kedah, Kelantan, Negeri Sembilan, Pahang, Perak, Perlis, Selangor and Terengganu —23 April 1957. The statutory was later extended to Malacca and Penang—23 February 1990.

• Price - means the money consideration for a sale of goods.• Document of title to goods - includes a bill of lading, dock

warrant, warehouse keeper’s certificate, wharfinger’s certificate, railway receipt, warrant or order for delivery of goods and any other document used in the ordinary course of business as proof of the possession or control of goods, or authorizing or purporting to authorize, either by endorsement or by delivery, the possessor of the document to transfer or receive goods thereby represented.

• Nemo dat quod non habet - no one gives what he does not own.

ExcelBright Training Consultants SB

04/18/2023 ExcelBright Training Consultants SB

86

SOGABenefits To Concerned Parties• SOGA aims to protect concerned parties in the

transaction and the eventual transfer of ownership of a good from a seller to a buyer.

Implied Terms Of The Sale Of Goods Act, 1957• The statutory of implied terms main function is to

protect the rights to every buyer or consumer. These statutory implied terms are in Section 14- 17 of the Sales of Goods Act, 1957 and are the implied terms in every contract of sale of goods.

04/18/2023 ExcelBright Training Consultants SB

87

Case Study• I fought the store at TESCO UK and the law won• After 18 months, Peter Ward's TV broke down and Tesco

refused to repair it. But, as Miles Brignall reports, EU rules give you two-year replacement rights, not one

• The couple have since been given a replacement set worth £280

04/18/2023 ExcelBright Training Consultants SB

88

Case study

• Tesco Malaysia return policy = within 7 days with original box and receipt. The 7 days is not written in “Tesco’s Terms and Conditions”

http://www.tesco.com.my/eshop/html/Terms-and-Conditions.aspx

04/18/2023 ExcelBright Training Consultants SB

89

Case studyQ: I do not wish to fly after purchasing a flight or if I could not show up for flight, what can I refund?• Once your booking is confirmed, it cannot be cancelled and

the payment you made is not refundable.• However, you can get a refund on airport taxes.• The airport tax refund may only be made after the date of

Departure. If you would like to request a refund on Airport Taxes fill in this form by clicking this link.

http://www.airasia.com/ask/template.do?id=443

04/18/2023 ExcelBright Training Consultants SB

90

Case study – Personal Experience

• Early morning return flight from Bali to Yogyakarta was rescheduled to evening flight. 9 hours spent at the airport. NOT being compensated.

• Flight to London was cancelled without replacement. Hotel bookings in London forfeited.

04/18/2023 ExcelBright Training Consultants SB

91

Case Study: Malaysia• Goods sold not returnable

– Underware

• Hygiene Resons?

04/18/2023 ExcelBright Training Consultants SB

92

Case Study: SOGORETRUN POLICY:• All purchases may qualify for a return or exchange

within fourteen 14-day from the date of receiving the item(s). Customers may exchange an item for a different colour or size, and of equal value only.

The item(s) must be in resale-able condition with original packaging. For refund processing an invoice need to be attached upon return.

https://www.klsogo.com.my/index.php?mod=product_return&function=product_return

04/18/2023 ExcelBright Training Consultants SB

93

PRINCIPLES OF CONSUMER POTECTION

04/18/2023 ExcelBright Training Consultants SB

94

MPH Bookstore RM 22.50

04/18/2023 ExcelBright Training Consultants SB

95

Malaysia’s Consumer Protection Act 1999

Statistics show that perhaps you are not being old, you are just being right. ...Malaysia's National Consumers Complaints Centre (NCCC) has made a statement ...E-Aduan - National Consumer ... - Guide to Complaint - Info Pengguna - Pajak Gadai•The Consumer Protection Actwww.consumer.org.my/index.../rights/254-the-consumer-protection-act

The Malaysia's Consumer Protection Act 1999 (CPA) is an act which came into ... As a consumer, you have the right to all the products and services of daily ...

04/18/2023 ExcelBright Training Consultants SB

96

The Malaysia's Consumer Protection Act 1999 (CPA)

• CPA is an act which came into effect 1st October 1999. It is a piece of legislation enacted with the main objective to provide greater protection for consumers

• The provisions of this act cover areas not covered by other existing laws. This act provides simple, inexpensive redressal to the consumer's grievances and relief of a specific nature.

• Under this act, an aggrieved consumer may refer any dispute or claim of less then RM10,000 to the established Consumer Redressal Tribunal.

04/18/2023 ExcelBright Training Consultants SB

97

What are your rights as a consumer?

• your rights granted cannot be taken away from you notwithstanding conditions in any agreement that you have signed.

• As a consumer, you have the right to all the products and services of daily basic needs including food, clothing, health, education and house.

• You are also protected from products, services and manufacturing processes that may expose your health and life to danger

• To make the right choice, you have the right to obtain accurate and precise facts about the product and service that you want to consume

04/18/2023 ExcelBright Training Consultants SB

98

What are your rights as a consumer?

• Nobody can force you to buy a product or service. You have the freedom in buying or assuring that the product or service you need is obtained through the right channels, based on the right price.

• You have the right to claim for damages from unfair practices from the supplier or manufacturer

04/18/2023 ExcelBright Training Consultants SB

99

Case Study: Impact of GST on Consumer?

• To discuss with participantsLecturer in GST case releasedA lecturer was arrested over the restaurant’s alleged failure to display the GST registration number in its receipts.This is an offence under Section 33 (2) (b) of the Goods and Services Tax Act for issuing a tax invoice which does not contain the prescribed particulars.Offenders can be fined up to RM30,000 or face a maximum two years’ jail or both under Section 96 of the Act, Abd Hadi told reporters.He confirmed that the restaurant had a valid registration with the department with regard to the GST.

04/18/2023 ExcelBright Training Consultants SB

100

Hire-Purchase Act 1967

WHAT IS HIRE PURCHASE?

It is a system of buying things on credit whereby the seller of the goods is regarded as the dealer, the purchaser is regarded as the hirer and the finance company is the owner.The ownership of the goods bought on hire purchase does not pass to the hirer at the time of the hire purchase agreement or upon delivery of the goods. The ownership of the goods remains in the owner until the hirer has fully paid the price agreed upon in the hire purchase agreement.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

101

Hire-Purchase Act 1967

WHAT GOODS CAN I BUY ON HIRE PURCHASE?

You can buy all consumer goods on hire purchase as well as motor vehicles such as invalid carriages, motorcycles, motor cars including taxi cabs and hire cabs, good vehicles where the maximum permissible laden weight does not exceed 2540 kilograms, and also buses including stage buses.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

102

Hire-Purchase Act 1967

WHAT DOCUMENTS MUST I SIGN WHEN I BUY THINGS ON HIRE PURCHASE?

All the parties must sign a hire purchase agreement and the agreement, among other things, must specify the date when the hiring commences, the number of instalments, the amount of each instalment, the time for the payment of each instalment, the description of the goods and where the goods are kept. Note that the agreement must be in writing. An oral agreement is not a valid hire purchase agreement.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

103

Hire-Purchase Act 1967

DO I NEED A GUARANTOR?

The owner may require you to furnish information on or more guarantors to guarantee the performance of your obligation under the hire purchase agreement.

HOW MUCH IS THE INTEREST PAYABLE?

The interest, often referred to as 'Terms Charges', shall not exceed 10% per annum.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

104

Hire-Purchase Act 1967

HOW MUCH DEPOSIT SHOULD I PAY WHEN I BUY GOODS ON HIRE PURCHASE?

The deposit should not be less than 10% of the cash price of the goods bought. This means that the parties can agree to a deposit of more than 10% and the deposit may be paid in cash or in goods, or partly in cash and partly in goods.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

105

Hire-Purchase Act 1967

HOW MUCH DEPOSIT SHOULD I PAY WHEN I BUY GOODS ON HIRE PURCHASE?

The deposit should not be less than 10% of the cash price of the goods bought. This means that the parties can agree to a deposit of more than 10% and the deposit may be paid in cash or in goods, or partly in cash and partly in goods.

WHAT WILL HAPPEN IF I DEFAULT IN MY PAYMENTS?

The owner have the right to take possession of the goods if there have been two successive defaults of payments or a default of the last payment. Then the owner must serve on the hirer a notice in writing intending to re-possess the goods after a period of not less than 21 days after the service of the notice of intention to re-possess. Thus it is essential that you are prompt in your instalment payments.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

106

Hire-Purchase Act 1967

WHAT PROCEDURES MUST THE OWNER FOLLOW WHEN HE COMES TO REPOSSES THE GOODS?

If the owner comes personally to repossess the goods then he must produce his identity card and provide the hirer with the name and address of the company to which he belongs. If the owner sends his servant agent or employee then the person concerned must produce and show his identity card and his authority card. The authority card must bear the photograph of the servant agent or employee, his name and address, the name and address of the owner, the nature of appointment of the servant agent or employee and the signature of the owner.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

107

Hire-Purchase Act 1967

WHAT WILL HAPPEN IF THE GOODS ARE REPOSSESSED?

When the owner re-possesses the goods he must ,within 21 days serve on you and the guarantor(s), if any, a notice in writing informing you that if within 21 days after service of the notice, you pay the owner the amount due or remedy any breach and pay the reasonable costs incurred, the owner shall forthwith return the goods. If you do not make any attempt to recover the goods, within the time provided for, from the owner after the goods have been re-possessed, the owner will sell the goods usually by public auction or by tender. If the amount recovered form such sale by the owner is less than the amount due to the owner, then the owner shall sue you and the guarantor for the deficit sum.

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

108

Hire-Purchase Act 1967

WHAT WILL HAPPEN IF THE GOODS ARE REPOSSESSED?

When the owner re-possesses the goods he must ,within 21 days serve on you and the guarantor(s), if any, a notice in writing informing you that if within 21 days after service of the notice, you pay the owner the amount due or remedy any breach and pay the reasonable costs incurred, the owner shall forthwith return the goods. If you do not make any attempt to recover the goods, within the time provided for, from the owner after the goods have been re-possessed, the owner will sell the goods usually by public auction or by tender. If the amount recovered form such sale by the owner is less than the amount due to the owner, then the owner shall sue you and the guarantor for the deficit sum.

Repossession of motor vehicles are generally carried out by repossessors who are registered members of the Association of Hire Purchase Companies Malaysia (AHPCM)

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

109

Hire-Purchase Act 1967

CAN I COMPLETE PAYMENT OF THE INSTALMENTS EARLIER THAN THE DATE AGREED UPON?

The hirer can complete the hire purchase agreement earlier than the date originally agreed upon by paying the balance due at any time during the existence of the agreement or where the owner has repossessed the goods the hirer can complete the agreement by paying the owner within 21 days, the net balance due as well as reasonable costs incurred by the owner for storage, repair and maintenance of the goods repossessed

Hire Purchase of Goods

04/18/2023 ExcelBright Training Consultants SB

110

Hire-Purchase Act 1967

– bank (EON) charged RM500 for repossession

– Islamic HP - http://www.bnm.gov.my/index.php?ch=174&pg=469&ac=389

– Normally, bank will not repossess on default payments if total payment is more than 80%. Letter of Demand will be issued and followed by numerous telephone calls / messages

04/18/2023 ExcelBright Training Consultants SB

111

Business Options• Purchase outright?• Hire purchase?• Tax Deductions:

– As operating expenditure – in arriving at adjusted income

– As capital expenditure – capital allowance mechanism