4 cpas are held to the highest ethical standands cpas are held to the highest ethical standands

Post on 21-Dec-2015

219 views

TRANSCRIPT

4444CPAs ARE HELD TO THECPAs ARE HELD TO THE

HIGHEST ETHICAL HIGHEST ETHICAL STANDANDSSTANDANDS

CPAs ARE HELD TO THECPAs ARE HELD TO THEHIGHEST ETHICAL HIGHEST ETHICAL

STANDANDSSTANDANDS

Chapter 4 Issues:Chapter 4 Issues:

Distinguish ethical from unethical behavior in personaland professional contexts. Why is this difficult

without agreed-upon fundamentals/ “moral absolutes?”

Distinguish ethical from unethical behavior in personaland professional contexts. Why is this difficult

without agreed-upon fundamentals/ “moral absolutes?”

Resolve ethical dilemmas using an ethical framework - maybe? Perhaps a reward/penalty

system?

Resolve ethical dilemmas using an ethical framework - maybe? Perhaps a reward/penalty

system?

Describe the purpose and content of the AICPAAICPA Codeof Professional Conduct.

Describe the purpose and content of the AICPAAICPA Codeof Professional Conduct.

WHAT ARE ETHICSWHAT ARE ETHICS??????????????

Ethics can be defined broadly asEthics can be defined broadly asa set of moral principles or values.a set of moral principles or values.

Each of us has such a set of values

We many or may not have considered them explicitly

Ethical behavior is necessary forEthical behavior is necessary fora society to function in an orderly mannera society to function in an orderly manner..

The need for ethics in society issufficiently important that many

commonly held ethical valuesare incorporated into laws.

The need for ethics in society issufficiently important that many

commonly held ethical valuesare incorporated into laws.

When a Person’s Moral StandardsDiffer from YoursWhen a Person’s Moral StandardsDiffer from Yours

Extreme examples of people whose behaviorExtreme examples of people whose behaviorviolates a wide array of moral standardsviolates a wide array of moral standardsare drug dealers, bank robbers, and sex offendersare drug dealers, bank robbers, and sex offenders.

Common American Moral Standards?Is fundamentalism good or bad?

Common American Moral Standards?Is fundamentalism good or bad?

Resolving EthicalDilemmasResolving EthicalDilemmas

Formal framework has beenFormal framework has beendeveloped to help people resolvedeveloped to help people resolveethical dilemmas.ethical dilemmas.

The six-step approachwas intended to be asimple approach to

resolving ethical dilemmas.

1. Obtain the relevant facts.

2. Identify the ethical issues from the

facts.

3. Determine who is affected.

4. Identify the alternatives available to

the person who must resolve

the dilemma.

5. Identify the likely consequences of

each alternative.

6. Decide the appropriate action.

(“APPROPRIATE ACTION?”)

1. Obtain the relevant facts.

2. Identify the ethical issues from the

facts.

3. Determine who is affected.

4. Identify the alternatives available to

the person who must resolve

the dilemma.

5. Identify the likely consequences of

each alternative.

6. Decide the appropriate action.

(“APPROPRIATE ACTION?”)

Special Need for Ethical Special Need for Ethical Conduct In ProfessionsConduct In Professions

Our society has attached a specialOur society has attached a specialmeaning to the term professional.meaning to the term professional.

A professional is expected to conductA professional is expected to conducthimself orhimself or herself at aherself at a higher level thanhigher level thanmost other members of society.most other members of society.

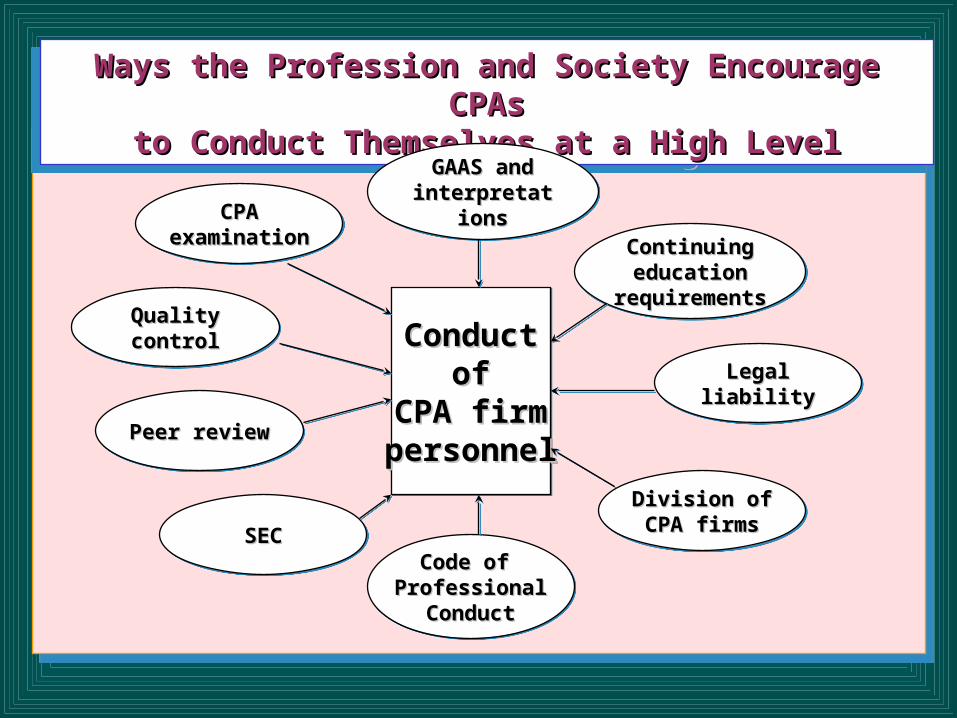

Ways the Profession and Society Encourage CPAsWays the Profession and Society Encourage CPAsto Conduct Themselves at a High Levelto Conduct Themselves at a High Level

Ways the Profession and Society Encourage CPAsWays the Profession and Society Encourage CPAsto Conduct Themselves at a High Levelto Conduct Themselves at a High Level

GAAS andGAAS andinterpretationsinterpretations

GAAS andGAAS andinterpretationsinterpretationsCPACPA

examinationexaminationCPACPA

examinationexamination

QualityQualitycontrolcontrolQualityQualitycontrolcontrol

Peer reviewPeer reviewPeer reviewPeer review

ContinuingContinuingeducationeducation

requirementsrequirements

ContinuingContinuingeducationeducation

requirementsrequirements

LegalLegalliabilityliabilityLegalLegal

liabilityliability

Division ofDivision ofCPA firmsCPA firmsDivision ofDivision ofCPA firmsCPA firms

Code of Code of ProfessionalProfessional

ConductConduct

Code of Code of ProfessionalProfessional

ConductConduct

SECSECSECSEC

ConductConductofof

CPA firmCPA firmpersonnelpersonnel

ConductConductofof

CPA firmCPA firmpersonnelpersonnel

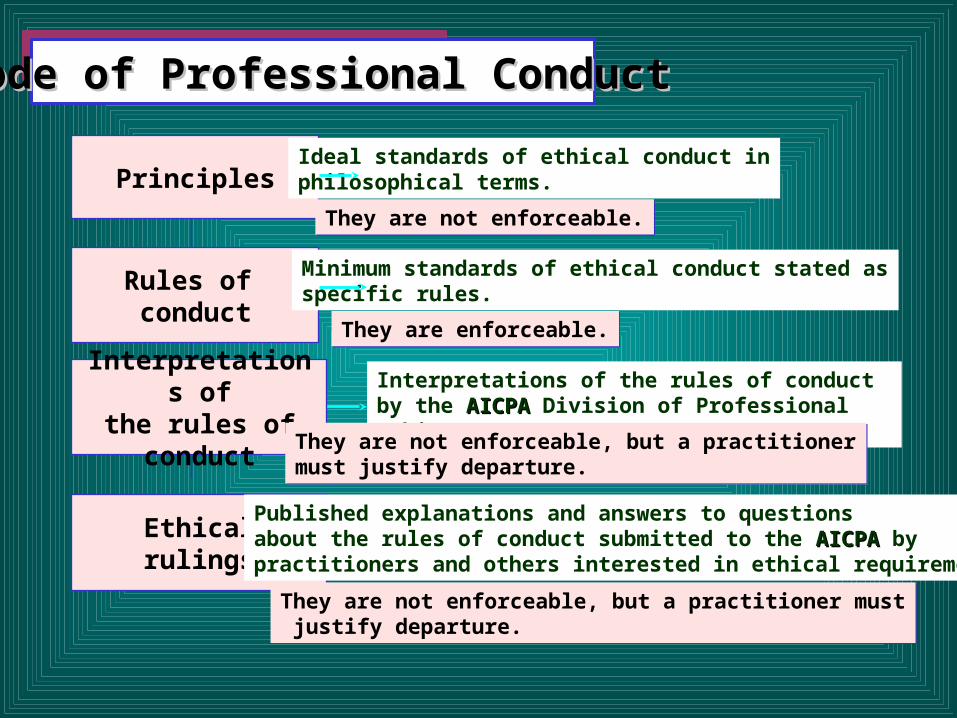

Code of Professional ConductCode of Professional Conduct

Principles

Rules of conduct

Interpretations ofthe rules of conduct

Ethicalrulings

Ideal standards of ethical conduct inphilosophical terms.

They are not enforceable.They are not enforceable.

Minimum standards of ethical conduct stated asspecific rules.

They are enforceable.They are enforceable.

Interpretations of the rules of conduct by the AICPAAICPA Division of Professional Ethics.

They are not enforceable, but a practitionermust justify departure.They are not enforceable, but a practitionermust justify departure.

Published explanations and answers to questionsabout the rules of conduct submitted to the AICPAAICPA bypractitioners and others interested in ethical requirements.

They are not enforceable, but a practitioner must justify departure.They are not enforceable, but a practitioner must justify departure.

FIGURE 4-4 Standards of ConductFIGURE 4-4 Standards of Conduct

Principles

Rules ofconduct

Substandardconduct

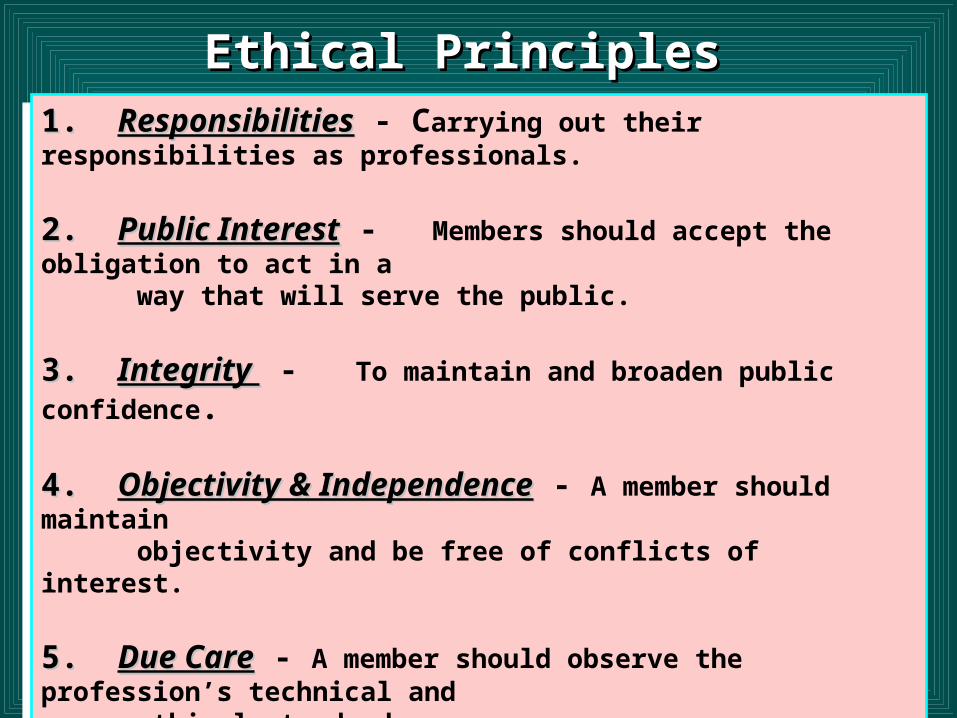

Ethical PrinciplesEthical Principles

1.1. ResponsibilitiesResponsibilities - Carrying out their responsibilities as professionals.

2. 2. Public InterestPublic Interest - Members should accept the obligation to act in away that will serve the public.

3. 3. Integrity Integrity - To maintain and broaden public confidence.

4. 4. Objectivity & IndependenceObjectivity & Independence - A member should maintainobjectivity and be free of conflicts of interest.

5. 5. Due CareDue Care - A member should observe the profession’s technical andethical standards.

6. 6. Scope & Nature of ServicesScope & Nature of Services - A member in public practice shouldobserve the principles of the Code of Professional Conduct.Code of Professional Conduct.

1.1. ResponsibilitiesResponsibilities - Carrying out their responsibilities as professionals.

2. 2. Public InterestPublic Interest - Members should accept the obligation to act in away that will serve the public.

3. 3. Integrity Integrity - To maintain and broaden public confidence.

4. 4. Objectivity & IndependenceObjectivity & Independence - A member should maintainobjectivity and be free of conflicts of interest.

5. 5. Due CareDue Care - A member should observe the profession’s technical andethical standards.

6. 6. Scope & Nature of ServicesScope & Nature of Services - A member in public practice shouldobserve the principles of the Code of Professional Conduct.Code of Professional Conduct.

Partners or ShareholdersPartners or Shareholdersversusversus

Nonpartners or Nonshareholders Nonpartners or Nonshareholders

Rule 101 applies to partners and shareholdersfor all clients of a CPA firm.

Rule 101 applies to partners and shareholdersfor all clients of a CPA firm.

Rule 101Rule 101 - Independence: - Independence: A member in public practice shall be A member in public practice shall be independent in the performance of professional services as required byindependent in the performance of professional services as required bystandards promulgated by bodies designated by Council.standards promulgated by bodies designated by Council.

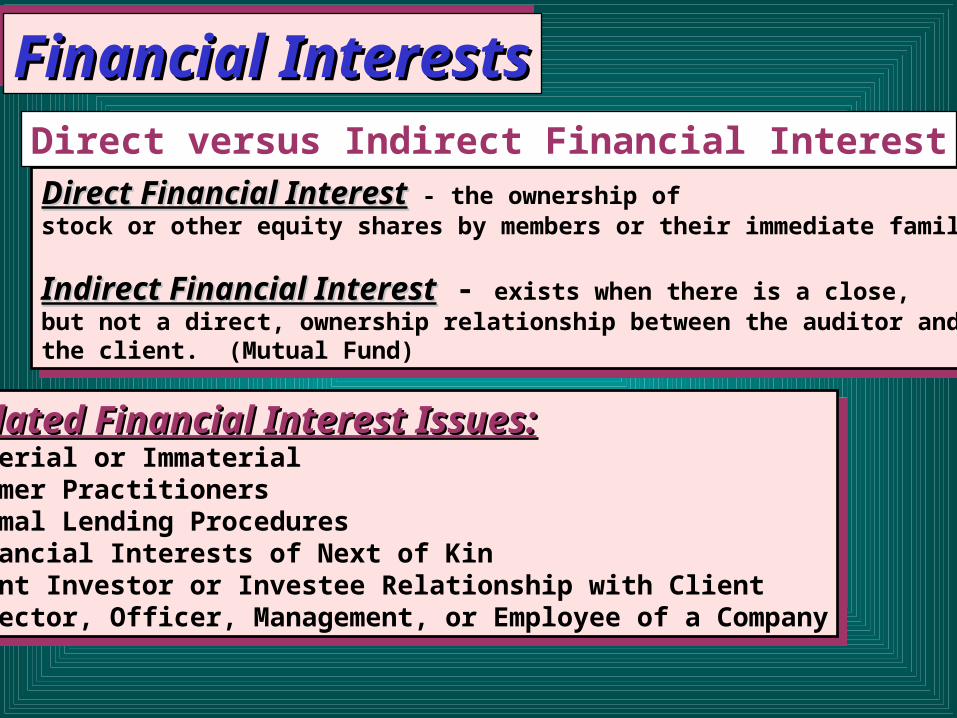

Financial InterestsFinancial InterestsFinancial InterestsFinancial InterestsDirect versus Indirect Financial Interest

Direct Financial InterestDirect Financial Interest - the ownership ofstock or other equity shares by members or their immediate family.

Indirect Financial InterestIndirect Financial Interest - exists when there is a close,but not a direct, ownership relationship between the auditor andthe client. (Mutual Fund)

Direct Financial InterestDirect Financial Interest - the ownership ofstock or other equity shares by members or their immediate family.

Indirect Financial InterestIndirect Financial Interest - exists when there is a close,but not a direct, ownership relationship between the auditor andthe client. (Mutual Fund)

Related Financial Interest Issues:Related Financial Interest Issues:Material or ImmaterialFormer PractitionersNormal Lending ProceduresFinancial Interests of Next of KinJoint Investor or Investee Relationship with ClientDirector, Officer, Management, or Employee of a Company

Related Financial Interest Issues:Related Financial Interest Issues:Material or ImmaterialFormer PractitionersNormal Lending ProceduresFinancial Interests of Next of KinJoint Investor or Investee Relationship with ClientDirector, Officer, Management, or Employee of a Company

Litigation between CPA Firm and ClientLitigation between CPA Firm and Client

A lawsuit or intent to start a lawsuit between aA lawsuit or intent to start a lawsuit between aCPA firm and its client is a violation of Rule 101CPA firm and its client is a violation of Rule 101for the current audit.for the current audit.

Bookkeeping & Other ServicesBookkeeping & Other Services

The interpretations do not allow a CPA firm to do bothThe interpretations do not allow a CPA firm to do bothbookkeeping and auditing for public clients.bookkeeping and auditing for public clients.

Conflicts Arising from Employment Relationships

The SEC has added a one year “cooling off ”period before a member of the auditengagement team can work for theclient in certain key management positions.

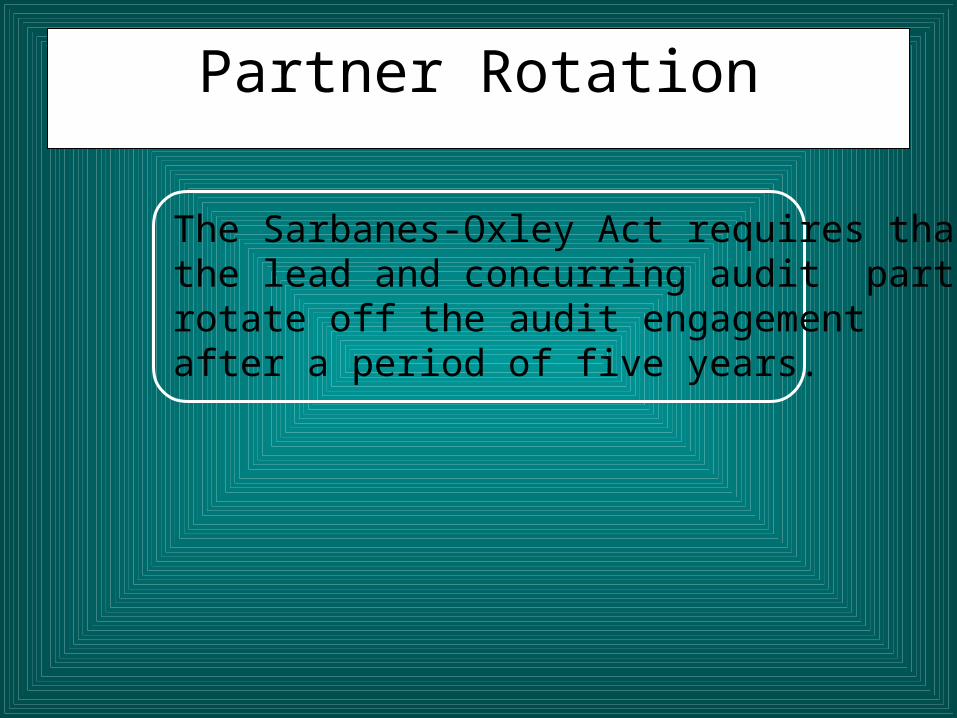

Partner Rotation

The Sarbanes-Oxley Act requires thatthe lead and concurring audit partnerrotate off the audit engagementafter a period of five years.

Other Rules of ConductOther Rules of ConductOther Rules of ConductOther Rules of ConductRule 102 - Integrity and ObjectivityRule 102 - Integrity and ObjectivityRule 102 - Integrity and ObjectivityRule 102 - Integrity and Objectivity

Rule 201 - General StandardsRule 201 - General StandardsRule 201 - General StandardsRule 201 - General Standards

Rule 202 - Compliance with StandardsRule 202 - Compliance with Standards

Rule 203 - Accounting PrinciplesRule 203 - Accounting PrinciplesRule 203 - Accounting PrinciplesRule 203 - Accounting Principles

Rule 301 - Confidential Client InformationRule 301 - Confidential Client InformationRule 301 - Confidential Client InformationRule 301 - Confidential Client Information

Rule 302 - Contingent FeesRule 302 - Contingent FeesRule 302 - Contingent FeesRule 302 - Contingent Fees

Rule 501 - Acts DiscreditableRule 501 - Acts DiscreditableRule 501 - Acts DiscreditableRule 501 - Acts Discreditable

Rule 502 - Advertising and Other Forms of SolicitationRule 502 - Advertising and Other Forms of SolicitationRule 502 - Advertising and Other Forms of SolicitationRule 502 - Advertising and Other Forms of Solicitation

Rule 503 - Commissions and Referral FeesRule 503 - Commissions and Referral FeesRule 503 - Commissions and Referral FeesRule 503 - Commissions and Referral Fees

Rule 505 - Form of Organization and NameRule 505 - Form of Organization and NameRule 505 - Form of Organization and NameRule 505 - Form of Organization and Name

ENFORCEMENTENFORCEMENT

Action by AICPAAction by AICPAProfessional Ethics Professional Ethics

DivisionDivision

Action by a State BoardAction by a State Boardof Accountancyof Accountancy

It’s All a Matter of Trust It’s All a Matter of Trust AND REPUTATION!AND REPUTATION!