50 tips for over 50's - ebook 2014

TRANSCRIPT

By David Reed

50 Tips for

Over 50’s

A word from the author

Society has long held the view that retirement can be a life of leisure with guaranteed relaxation and happiness the day after finishing paid work.

Our practical experience, combined with neuroscience and psychological research, proves that retirement can be a hazardous journey and presents more health, relationship, mental and financial issues than many people are aware.

We would like to briefly touch upon some of these issues as well as provide handy action tips to ensure that more people are aware of both the ‘pros’ and ‘cons’ when contemplating retirement.

The views expressed in this publication are solely those of the author; they are not reflective or indicative of Millennium3 Financial Services Pty Ltd (Millennium3) position, and are not to be attributed to Millennium3. They cannot be reproduced in any form without the express written consent of the author. This document has been prepared without taking account your objectives, financial situation and needs, and because of that, before acting on any information, you should consider the appropriateness of the information having regard to your objectives, financial situation and needs. The Retirement Advice Centre is a Corporate Authorised Representative of Millennium3 Financial Services Pty Ltd ABN 61 094 529 987 AFSL No. 244252

The Retirement Advice Centre

Australian Research has shown that pre-retirees have the following concerns when planning for retirement: Challenger (Dec, 2012)

1. Transitioning from working life to retirement

2. Maintaining pre-retirement lifestyle

3. Planning for a longer life expectancy

4. Protection of savings

5. Lack of control over their investments

6. Ensuring reliability in investment returns

In an easy-to-read format, we’ve touched upon each of these aspects based upon either academic evidence or practical experience from our retiree clients.

We trust you find our 50 Tips useful for your retirement planning journey!

“Our aim is to make retirement enjoyable

in planning, and comfortable in living.”

Retirement Adviser, David Reed

1Neuroscience has proven that your brain is a muscle. Just like any muscle, if it’s not active it can atrophy and wither.

Keep your brain active by doing stimulating activities.

It doesn’t necessarily mean ‘paid’ work, it can be a hobby, volunteering, new business venture or partnership.

Purpose and Meaning, ie. a reason to get out of bed in the morning, is crucially important.

The well known adage of ‘retiring today, dying tomorrow’ has an element of truth associated with this research.

Successful Retirees are those that focus upon retirement with Purpose and Meaning.2

Those who succeed in retirement are those who obviously know what they are retiring from, but more importantly know that what they are retiring to.

Have a clear picture of what retirement looks like for you, how you will engage your skills and resources and how you will stay challenged.

For many robust retirees, retirement is an artificial finish line that they will never cross.

Retirement is one of the top 10 most stressful life events.

(Holmes and Rahe)

3When you are contemplating retirement, it is recommended that you place a greater emphasis on ‘be-ing’.

Ask yourself the question – “If I had my time over at the start of my career and education, what would I do differently (or what would I continue to do)?”

Envision your transition into retirement less as the encore, but rather as the next phase of your lifetime journey.

Habits of thinking need not be forever.

One of the most significant findings in psychology in

the last twenty years is that individuals can choose the

way they think. - Martin Seligman

Retirement boosts your risk of depression by 40%.4

Understand that there are inherent risks in retirement, financially, emotionally and psychologically.

George Vaillant conducted years of research from the Grant Study that launched in 1939 to identify that in his work ‘Aging Well’, he wrote “…it is social aptitude, not intellectual brilliance or parental social class, that leads to successful aging.”

Additionally, mature coping styles, ie. “making lemonade out of lemons” is in social and psychological terms the most powerful predictor of successful ageing.

9 Recommendations by George Vaillant include:-

1. A good marriage before age 50

2. Ingenuity to cope with difficult situations

3. Altruistic behaviour

4. Stop smoking

5. Do not use alcohol to the point where your behaviour shames you or your family

6. Stay physically active. Walk, run, mow your own grass, play tennis or golf

7. Keep your weight down

8. Pursue education as far as your native intelligence permits

9. After retirement, stay creative, do new things, learn how to play again

Continued maturation no matter a person’s age can influence these results.

To prepare ourselves, Vaillant writes “We can start by admiring how other skilful people cope. Then ponder, when things go badly for us, how we might have used self-defeating mechanisms. Don’t try to think less of yourself, but try to think of yourself less.”

In the USA, rates for male suicide spike significantly after the age of 65 to almost triple the overall rate.

In Australia, the rate of suicide of those in retirement phase of life exceeds that of teenage males:

5 Have a purpose.

Many retirees are of the view that it’s best to ‘transition’ into retirement slowly, rather than an abrupt change in one day.

So rather than focus upon whether you have enough money to retire, spend time contemplating what a fulfilling lifestyle looks like in retirement.

Read books such as Authentic Happiness or website material of Martin Seligman.

His work over many decades has led to important findings around Purpose and Meaning as key features towards building a fulfilling life and robust attitude.

The average retiree spends 43.5 hours per week watching television.

(Age Wave, 2012)

6Identify your values in life and discuss with others how your vision of retirement should be. Pleasure is external (eg. TV), while Happiness is intrinsic (eg. fulfilling activities aligned with your Values).

Diarise your time with these Values including family time, friends, socialising, mini-break holidays, hobby or courses.

Retirement is much, much more than reaching a target of

accumulated cash.

The Paradox of Leisure -

A retirement that totally consists of leisure must be a good thing.

7Psychologist Barry La Valley highlights an important perspective on this myth:

“We like our holidays and weekends when we are working, therefore imagine if that were now your life.

Consider the paradox of leisure: we like leisure because it is a break from work.

If you had leisure seven days a week for thirty years, where is your break?”

Christmas time is an ideal period to reflect and plan for the future. 8Complete an ideal year (a suggested tip is to start with holidays first, then seasonal activities, etc).

Then complete your view of what an ideal week would be (tip – start with the weekends first).

Finally, complete what an ideal day would look like (tip – start with sleep and exercise as they are your most important factors).

It can help to schedule your day just like you would ‘going to work’ so as to get out of the house or undertake activities.

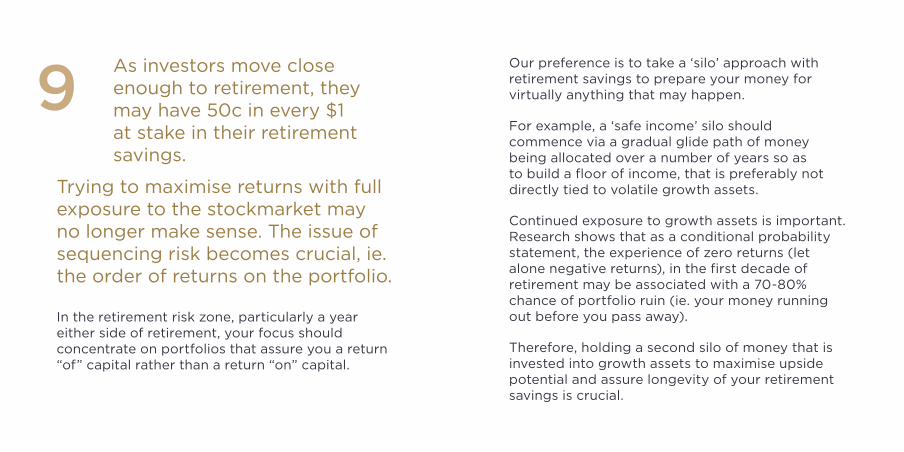

9As investors move close enough to retirement, they may have 50c in every $1 at stake in their retirement savings.

Trying to maximise returns with full exposure to the stockmarket may no longer make sense. The issue of sequencing risk becomes crucial, ie. the order of returns on the portfolio.

In the retirement risk zone, particularly a year either side of retirement, your focus should concentrate on portfolios that assure you a return “of” capital rather than a return “on” capital.

Our preference is to take a ‘silo’ approach with retirement savings to prepare your money for virtually anything that may happen.

For example, a ‘safe income’ silo should commence via a gradual glide path of money being allocated over a number of years so as to build a floor of income, that is preferably not directly tied to volatile growth assets.

Continued exposure to growth assets is important. Research shows that as a conditional probability statement, the experience of zero returns (let alone negative returns), in the first decade of retirement may be associated with a 70-80% chance of portfolio ruin (ie. your money running out before you pass away).

Therefore, holding a second silo of money that is invested into growth assets to maximise upside potential and assure longevity of your retirement savings is crucial.

Many people sell their family home when entering Aged Care facilities10

If you are part of the ‘sandwich generation’, ie. caring for your own kids and parents at the same time, then issues such as Aged Care Accommodation may be an issue that will arise in the future.

This is a specialist area where good advice can give you more options than just selling the family home, and may literally save you many thousands of dollars. Seek out a meeting with an Aged Care Advice specialist (and preferably before you attend the first meeting with the Accommodation provider).

As we age, our bones (a living tissue) change and results in loss of bone tissue. This weakens the bone and increases risk of breaks from bumps and falls.

11

Research shows that exercise can make bones stronger and help slow the rate of bone loss. Include activities such as walking, swimming and the gym visits into your weekly routine.

Recent studies show that less than 1 in 10 Australians over the age of 50 do enough exercise to improve or maintain cardiovascular fitness (Vic Govt, 2014). Grab a gym or walking partner to keep yourself disciplined, or hire a personal trainer to ensure that you make exercise a habit.

Retirement is a transition, not a destination. There are going to be phases during this transition.

12

Retirement is a multi-phase journey. But also remind yourself that time isn’t always your friend—getting older means doing as much as you can as quickly as you can (never put anything off!)

“Longevity is only a luxury if you can afford it”

For couples with a joint or shared credit card, it may be prudent to consider applying for a credit card for each of you prior to retirement.

13

If either spouse were to pass away, and the credit card was in their name, then the bank may cancel that card.

If there is little income, then it may be difficult for the surviving spouse to obtain a new credit card in their own name.

Emotions of Greed and Fear are likely to have more effect upon your retirement savings than any other decision you make.

14If you don’t stand for something, then you’ll fall for anything.

Construct an investment philosophy that you are comfortable with.

Paying for expert investment advice can assist you with this process, and also provide you with a reliable external party to keep you from making emotional decisions. A documented investment philosophy can form the anchor point for all future investment decisions for both the adviser and yourself.

The behaviour gap is up to 3.96% per year for stockmarket investors.

(Dalbar Inc 2012, USA)

Potentially 60% of your wealth in your lifetime may come from the day AFTER you retire.

(Russell, 2012)

15

At retirement, many people will have accrued the most money they will ever have in their lifetime.

As compound interest commences after retirement, and in an appropriately weighted diversified portfolio, the earnings each year may result in very significant numbers. This is what Russell term 60/30/10 – ie. 60% of wealth from compound interest in retirement, 30% of wealth from compound interest while working and 10% from contributions made during your working life.

As an example, let’s say you retire with $1m. A 10% return the first year of retirement is $100,000. It may have taken you 5-10+ years of your working life to save an equivalent amount to that $100,000 earnings.

This potential can be subsequently sacrificed if your own conservatism at retirement results in moving more money into cash. We also see more so-called Lifecycle funds (that are gaining popularity with institutions by moving your asset allocation of money into a more conservative weighting of assets as you age) do similar conservative weightings.

As people are living longer, and drawing more money out of retirement savings, this conservative shift may not necessarily be beneficial in retirement.

Often adult children and grandchildren value the family heirlooms as much, if not more than financial legacies.

16

56% of people aged 50+ would prefer to begin passing on their assets while living rather than at end of life.

Give away some of your treasures and memorabilia while you are alive so you can see and appreciate how they are enjoyed by your beneficiaries.

The timing may be right if you are considering downsizing your home.

Research shows planning for retirement 5-10 years ahead has an increase of wealth of $157,427 for people with a retirement plan, compared to those without a plan.

(Texas Tech, 2011)

17Constant buying and selling of shares, fixed interest or funds rarely work, particularly over the long term. It sells newspapers and magazines, but it can be a wealth hazard.

18

Learn more about academic principles that are evidence-based methodologies to save for, and distribute income, in retirement.

A good place to start is with free websites such as www.ifa.com (USA based), http://au.dimensional.com, www.vanguard.com.au, www.ssrn.com, and even our own www.smartretirement.com.au. We will continue to build our library of educational resources for both the psychology of retirement and retirement income planning.

It’s never too late to start planning and saving for your retirement, but the best time to start is always today.

Studies on loss aversion show that for most people, the pain of a $1 loss is about as intense as the pleasure of a $2 financial gain.

19

Overcome behavioural biases through construction of assets into ‘silos’ that prepare you for virtually anything that may happen.

Assets exposed to growth asset market volatility shouldn’t influence your necessary living expenses in the next 7 years or more.

Retirees are hyper-sensitive to losses. They have a response that a $1 loss is emotionally equivalent to $10 in gains.

Random chance can outperform active stock management. Even cats beat the experts.

20

Our belief is that saving for retirement should be founded upon ‘evidence-based’ principles. These principles include that markets work and we can capture the market return with very low costs.

I appreciate that it sounds counter-intuitive to what we learn growing up in school, but with financial markets, working harder and more often (ie. trading in and out of the market) often means earning less when investing.

The most common regret was having the courage to live a life true to myself, not the life others expected for me.

Be brave and individual, pursue your potential.

21

Read ‘The Top Five Regrets of the Dying’ by Bronnie Ware

22Minimise the need to draw down larger sums of money from retirement savings in the first few years.

Within your last 3 years of paid employment, start replacing expensive items that are likely to need replacing such as white goods (fridge, washing machine, car, etc).

Achieving your aspirations will often require you to spend one, or both, of two things - time and/or money.

23

Develop daily habits to live your life on purpose.

Build a financial plan that aligns your money with your values.

It’s never too late to be the person that you have always wanted to be. 24Research shows that working towards a specific goal boosts our happiness, and those with more ambitious aspirations are happier than those with lower expectations. Success has no age limit.

A terrific example is George Dawson, a slave’s grandson, who learnt to read at 98 years old, lived to 103, and co-authored an award winning best seller on his life and lessons on living.

“Things will be all right.

People need to hear that. Life is good, just as it is.

There isn’t anything I would change about my life.”

—George Dawson

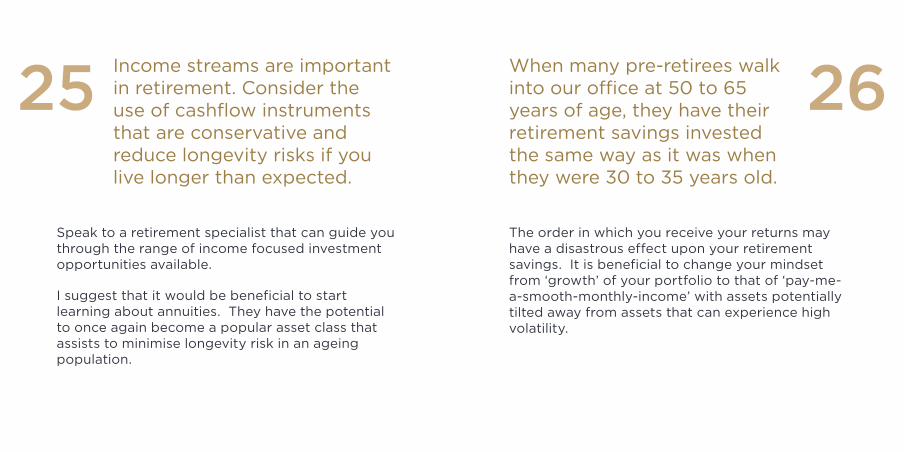

Income streams are important in retirement. Consider the use of cashflow instruments that are conservative and reduce longevity risks if you live longer than expected.

25

Speak to a retirement specialist that can guide you through the range of income focused investment opportunities available.

I suggest that it would be beneficial to start learning about annuities. They have the potential to once again become a popular asset class that assists to minimise longevity risk in an ageing population.

When many pre-retirees walk into our office at 50 to 65 years of age, they have their retirement savings invested the same way as it was when they were 30 to 35 years old.

26

The order in which you receive your returns may have a disastrous effect upon your retirement savings. It is beneficial to change your mindset from ‘growth’ of your portfolio to that of ‘pay-me-a-smooth-monthly-income’ with assets potentially tilted away from assets that can experience high volatility.

A successful retirement is one with no surprises.27

Lifestyle planning should be focused around your Life Values (eg. family, education, new experiences, philanthropy, etc).

If you are spending your most precious resources, ie. time and money each day on those activities in alignment with your Life Values, then your day can be seen as ‘fulfilling’. Alternatively, if your daily activities are not in alignment, then you’re just ‘time-filling’.

Financial retirement plans should adopt prudent, evidence-based investment philosophies, so that you have scientific reason as an ally.

In total contrast to this methodology is implementation of investments using mythical people that supposedly can provide higher returns than the marketplace, with lower risk. Consider these types of claims as a hazardous warning to your wealth.

Retirement income planning is complex. Professor Wade Pfau’s research shows that up to 14% of your lifetime of retirement wealth can be determined by what earnings (or losses) are made on your savings in the first 12 months of retirement.

Your retirement is too important to leave to chance. Either use the services of an expert on retirement income, or become one. The choice is yours. The risk in self-managing your retirement monies is that by it’s very definition, it is impossible to be ‘objective’. Even if you hire an experienced retirement specialist on a ‘second opinion’ time basis, the cost would be well worth it so as to have an impartial, disciplined perspective on the maximising of opportunities and balancing of risks and returns to your needs.

The ‘sandwich generation’ - supporting both children and parents can be difficult in retirement.

Think about how you intend to support your children and parents.

If suitable, a discussion with them about what support you can provide would be beneficial. Be aware that family issues can sometimes be one, if not the, major derailer for a prosperous retirement.

28If you are over 55, then consider options to minimise tax and maximise retirement savings.

29Learn more about Transition To Retirement pensions or seek professional advice. They offer an alternate means for you to potentially reduce your working hours without affecting your household income, or using the tax efficiencies of the strategy to boost your superannuation balance.

Financial literacy declines by about 2% per year after age 60 - yet confidence remains as high as when we were young.

Reduced abilities and high confidence can explain poor investment choices as we age.

30

Establish a written investment policy statement to adhere to for decisions.

Consider the use of a trusted adviser to assist with portfolio management and ongoing financial decisions that influence your retirement.

Actuaries estimate that people aged 65 currently have a 1 in 3 chance of living past the age of 90, and 1 in 5 will live past 95. (Actuaries Institute, 2013)

The use of longevity style investments such as Annuities can be considered to reduce this risk.

Combined with other income focused investments or benefits, such as Government or Corporate Bonds, Employer Defined Benefit Pensions, Centrelink Aged Pension, they can all assist to form a “Lifetime Floor of Income.”

31

In general, we identify 8 commonly found financial risks in retirement.32

Read more about, or receive advice to minimise these following risks:

1. Enough savings

2. Sufficient income stream

3. Sequence of returns risk

4. Market volatility risk

5. Longevity risk

6. Liquidity risk

7. Inflation risk

8. Investor behaviour risk

At the Retirement Advice Centre, we consider Seven Option Solutions (SOS) for Retirement Income Planning.

33When in withdrawal phase of your retirement savings, the options are generally limited as to what action you can take. Here are our Seven Option Solutions:

1. Die sooner

2. Work longer

3. Adjust inflation

4. Spend less

5. Save more or delay withdrawal

6. Increase your rate of return

7. Combination of options

Intentions with paid ‘work’ for retirees is undergoing significant changes. 34Think about your options.

The most popular intent in the USA is for 43% retirees to cycle their week between work and leisure (for example, contract work then learning and leisure).

UK research, as well as our own practical experience with clients, shows that retirees have a high risk of overspending in the early years of retirement.

(LV= Survey, 2014)

Be prepared. Think ahead as to what you intend to do in retirement and what your expenses are ‘likely’ to include.

This spending issue is commonly tied to the male retiree losing status that they had with their job. The search with hobbies, travel, expensive toys can result in overspending for the initial years in retirement. One in five surveyed in the UK strongly regret overspending during their first few years of retirement.

35

Draft a budget that focuses upon a ‘need’ level of income, and a ‘desired’ level of income.36

Use software such as Xero, ANZ Money Manager or Excel to analyse your budget history.

Then plan out your yearly/monthly/daily lifestyle to give you a better understanding of what an active retirement would appear like, and the likely expenses that would include. This provides a much better framework to understand your Needs and Desired Income.

Also, visit http://www.superannuation.asn.au/resources/retirement-standard as they provide financial estimates for Moderate and Comfortable retiree living standard research on a quarterly basis.

Retirement is a journey that is not linear. 37Age Wave (2005) have provided this research for retirement’s emotional phases:

Phase Duration Comments

Imagination 5-15 years prior to retirement

88% surveyed expect to be happy

Anticipation 0-5 years prior to retirement

91% expect to be happy and 80% believe that they will achieve their desired retirement

Liberation 1st year of retirement

78% say they are enjoying retirement. Highest use period for professional advice.

Reconfirmation 1-15 years after retirement

Depression risk, and realisation stage. Health issue risks. A purpose to get up in the morning is needed.

Reconciliation Deep in retirement

Come to terms with their lives. Substantial concern about the cost of living.

For every $20 that you put into your retirement savings, it can generate $1 of retirement income per year.

(Russell Investments, 2009).

38

No matter how small, or how close to retirement, continue to maximise your savings into superannuation.

Since 1996, those aged between 55 and 64 have had a higher rate of entrepreneurial activity than those aged 20 to 34.

Dane Stangler, 2007

39

Don’t let your dreams die because you’re retiring.

For many retirees, it’s a time of energetic reflection and an opportunity to pursue your passions and interests

You are who you are - Continuity Theory 40Human beings don’t like change in our lives, so when we try something new or change situations, our brains find ways to find normalcy. It’s a good idea to attempt habitual changes well before retirement.

Advertisers sell products based upon the allure of ‘pleasure’ under the guise that it will make you happy.

41

Understand that pleasure is tied to external influences, happiness is linked to internal satisfaction. Pleasure is generally fleeting and non-permanent.

Happiness is longer lasting and has greater permanency.

Spending time and money on your values and experiences, rather than products, can increase happiness.

230,000 previously retired Australians, the majority women, were back at work or looking for work in 2010-11, according to the ABS.

The most common reason was money (41 per cent) but boredom came next (28 per cent).

42

Preparing yourself financially through budgeting and forecasting, combined with understanding what you are retiring ‘to’, can prevent you from suffering boredom or lack of money.

A recent phenomenon that is becoming increasingly popular with retirees is for them to have a ‘year off’ prior to ‘official retirement’.

43

A gap year is often defined as a year of transition out of education or paid employment. Typically, a gap year conjures up an image of 18 year olds travelling to Bali, Europe, etc for parties and life experience.

That’s all starting to change.

A recent study by Halifax in the UK (2013), found nearly half of 55 to 64 year olds would love to take a year out travelling and the idea is catching on fast.

Prior to the commencement of official retirement, pre-retirees are now planning a year ‘off’ work prior to transitioning into the next phase of their life. The popularity of this holiday has seen the rise of the term ‘grey gap year’ and niche travel agents catering for this demand.

Your first reaction may be that it sounds like a novel idea. I’d suggest that it might be worth serious consideration as you fulfill some of your travel aspirations, while giving you the opportunity to explore a new environment and contemplate your lifestyle values, as well as the challenges and opportunities you would like to engage in your next phase of life.

Retirees have expressed their view that a Grey Gap Year allows them to explore more of the world, while many are undertaking voluntary philanthropic work so as to feel that they are giving something back. They also comment that they are viewing this time as a break in their career, as they intend to do similar or different careers upon their return. Food for thought.

Maximise your tax efficient income in retirement. 44If you have assets that are owned personally, or outside of superannuation, then they may be subject to income tax, and capital gains tax, regardless of your age. If those assets are owned within superannuation, and you retire past the age of 60, then the earnings on those assets may be tax free, and if sold, capital gains tax free. In addition, the pension stream that you receive may also be tax free. This is a significant benefit and a key reason why structuring your assets correctly prior to retirement can have benefits in the tens of thousands of dollars in a lifetime.

Please note you should seek specialist tax advice for your particular situation before making any investment decisions.

I married you for love (but not for lunch).

Divorces for those at pre-retirement age are rising fast

worldwide.

In the UK, divorce has tripled among people over the age of 60 (ONS, 2013), while in the USA, couples in their 60’s are divorcing a rate faster than any other decade in history (US Census, 2014). In Australia, divorces ending after 20 years of marriage has more than doubled from 13% (1990) to 28% in 2011 (AIOFS, 2013).

45While we may believe that introspectively, it is us an individual that is retiring from work, it is also likely that retirement will have a significant impact upon life as a couple. Each person is likely to have their own view of what the next phase of their lives will look like, and what’s necessary to achieve it.

As partners, if you have had a history of low communication, then it’s possible that this problem will only be emphasised in retirement.

Discuss with your spouse how your retirement will look like for you as individuals, as well as a couple.

Talking about what your ideal year, month and day in retirement will look like for each of you will enable you both to talk about any compromises and plans for retirement and how that can be achieved, shared and enjoyed.

Self Managed Super Funds (SMSF’s) are undoubtedly popular, flexible and a terrific structure for many people to build retirement savings.

Yet we are receiving queries more often now from pending retirees that have one, and the consideration of closing them down at retirement.

46SMSF’s can vary from simple to highly complex, therefore it is impossible to have a hard and fast rule. Getting advice is my first recommendation and see a SPAA Accredited Adviser (ie. SMSF Specialist).

My next suggestion is to learn more about how much it costs to run your SMSF, whether you have illiquid assets (eg. property) that mean you have no choice to keep the SMSF unless you sell the property, and whether there are simpler options for you in retirement with other superannuation funds such as wholesale, retail or industry pension funds.

Finally learn more yourself about terms such as ‘anti-detriment’ benefits, creating reserves within an SMSF and think about your estate planning wishes. These factors, as well as many others, may influence your decision to keep or wind up your SMSF at retirement.

Consider Generational Wealth plans prior to retirement.47

Seek professional advice from an adviser and estate planning solicitor. They can touch upon issues such as nomination of beneficiary types, how your estate could be distributed, anti-detriment benefits or re-contribution strategies.

Your estate plan may wish to give consideration to a general and an enduring power of attorney as well as guardianship and testamentary trust inclusions.

Take advantage of every government incentive available to maximise your retirement savings.

48Learn more, or seek advice early, about Centrelink eligibility strategies particularly with regards to the Health Care Card and Seniors Card.

When it comes to choice of home, staying in your home (also known as ‘Ageing-In-Place’) is much more common than retiring to a sea-change or a tree-change.

49

If you are considering moving from your home, carefully consider the implications such as health care facilities, and potential isolation from friends and family. It can be difficult to move away from your support network.

An idea may be to rent your existing home, and rent in the area you are considering. Buying and selling real estate is an expensive exercise with stamp duty, real estate agent costs, etc, so to

minimise mistakes, dip your toe in the water first by simply renting for a 6-12 month period and then make a decision to buy or sell your home.

If there are financial constraints, then other options to allow you to stay in your home may include:

1. Convert your land into a dual occupancy so that you can live in half, and the other half rented or sold.

2. Rent out some rooms or as is growingly popular, build a granny flat in the yard so that you can rent out or move into. There are social security and tax implications so seek advice before acting).

3. Consider a reverse mortgage loan if you need extra cash. It’s a good idea to discuss this move with the beneficiaries of your estate so that they have an understanding before you seek advice from professionals.

Renowned ageing scientists, such as Martin Seligman, have identified that from age 25 we get slower neuroconductivity, have less stamina, poorer memory and reasoning that is poorer and slower. Our originality also deteriorates.

The first four health issues are irreversible. The fifth, originality, we can act upon.

50

Appreciate and utilise the benefits that Seligman has shown that Ageing provides. Focus upon the positive attributes that Ageing provide, particularly when it comes to Creativity. Seligman outlined these recently:-

1. Knowledge – To be creative, we need expertise. As we age, we may have forgotten more, but we know more both in general life terms, as well as domain focused niches. We are aware of how to apply that knowledge.

2. Pattern recognition – As we age, out intuition builds and can recognise patterns from past experience.

3. Shortcuts (heuristics) – As we age, we take more and more shortcuts. Seligman in his talk in Sydney (March 2014) spoke about how at 21, he would read all of the academic papers from front to back. Nowadays, he reads about 10% of each paper as he knows the foundations and research methods of each

paper through experience and education. These are shortcuts not available when young.

4. Diversity of experience – We get more rigid and less original as we age, but we get more perspective and diversity through experience and understanding.

5. Sense of the audience – We get better at perspective taking for the audience around putting ourselves in place of other people. It is also beneficial for persuasion.

All of these 5 factors are teachable and can be done at any age. This is beneficial for the future as an ageing population can build more creativity in the world.

“Providing prudent guidance about retirement income

is much harder than giving advice on investing for a given retirement goal – both theoretically and

practically.”

Nobel Laureate Dr Harry Markowitz (RIAA Journal 2012, V2 N.1).

9) How safe are safe withdrawal rates in retirement? An Australian perspective (Prof. Drew and Prof. Walk, Financial Services Institute of Australia, 2014) http://www.finsia.com/docs/default-source/policy-archive/rrz---final-030314-web.pdf?sfvrsn=0

11) Healthy Ageing Literature Review (Department of Health, Victoria, 2012) http://www.health.vic.gov.au/agedcare/maintaining/downloads/healthy_litreview.pdf

14) Quantatitive Analysis of Investor Behavior (2013) Dalbar Inc, Research and Communications Division http://ww.qaib.com/public/downloadfile.aspx?...advisoreditionfreelook.pdf

15) The Russell 10/30/60 Retirement Rule https://www.russell.com/CA_FP/PDF/Invest4Retir_InvestrFinal.pdf

16) Family & Retirement: The Elephant In The Room. (Merrill Lynch study conducted with Age Wave (2013)) http://www.wealthmanagement.ml.com/wm/Pages/Age-wave-Survey.aspx

17) Behavioral Finance for Financial Planners (Professor James, Texas Tech University, 2011) http://www.slideshare.net/rnja8c/behavioral-finance-for-financial-planners (Slide 42)

Listed References (As per each item)

1) Aging and muscle: a neuron’s perspective (Manin, Hong and Clark, 2013) http://www.ncbi.nlm.nih.gov/pmc/articles/PMC3868452/

2) So You Think You’re Ready To Retire, (Barry La Valley & David Reed, 2014)

3) The Holmes-Rahe Life Stress inventory, The American Institute of Stress http://www.stress.org/holmes-rahe-stress-inventory/

4) Work Longer, Live Healthier (Institute of Economic Affairs, Paper No.46), Sahlgren, G, May 2013. http://www.iea.org.uk/sites/default/files/publications/files/Work%20Longer,%20Live_Healthier.pdf

5) Population Reference Bureau (2006, USA); Australian Bureau of Statistics (2009) http://www.prb.org/Publications/Articles/2006/ElderlyWhiteMenAfflictedbyHighSuicideRates.aspx http://www.abs.gov.au/ausstats/[email protected]/ 6) Age Wave, Dan Veto (2007) http://finance.yahoo.com/news/pf_article_103649.html

7) So You Think You’re Ready To Retire, (Barry La Valley & David Reed, 2014)

34) Americans Perspectives on New Retirement Realities and the Longevity Bonus (Merrill Lynch and Age Wave, 2013) http://wealthmanagement.ml.com/publish/content/application/pdf/GWMOL/2013_Merrill_Lynch_Retirement_Study.pdf

35) New retirees spend 33,00 pounds on luxuries in five years (Nelson Research for LV=, 2014) http://www.lv.com/adviser/working-with-lv/news_detail/?articleid=3213362

37) The New Retirement Mindscape Study (Ameriprise, Age Wave, Harris Interactive, 2005) http://www.agewave.com/research/landmark_retirementMindscape.php

38) The Russell Retirement Rule of $20 (Russell Investments, vol.9, issue 1, 2009) http://www.tedlee.ca/The%20Russell%20Retirement%20Rule%20of%20$20%20(Russel%20Investments).pdf

39) Ewing Marion Kauffman Foundation, Dane Stangler via Small Biz Trends, Scott Shane http://smallbiztrends.com/2010/05/should-we-worry-about-older-entrepreneurs.html

40) A continuity theory of normal aging, Robert C Atchley, PhD (Oxford Journal) http://gerontologist.oxfordjournals.org/content/29/2/183.abstract

19) Behavioral Finance and the Post-Retirement Crisis (Shlomo Benartiz, UCLA, Allianz, 2010) http://www.dol.gov/ebsa/pdf/1210-AB33-617.pdf

20) Moggy shames experts in shares game (SMH, 15 January 2013) http://www.smh.com.au/executive-style/culture/moggy-shames-experts-in-shares-game-20130115-2crbz.html

21) The 5 principles of no-regrets leading and living (Forbes 12 Oct 2013) http://www.forbes.com/sites/kevincashman/2013/12/10/the-5-principles-of-no-regrets-leading-and-living/

27) Lifetime Sequence of Returns Risk (Professor Wade Pfau, 27 September 2013) http://wpfau.blogspot.com.au/2013/09/lifetime-sequence-of-returns-risk.html

30) Old Age and the Decline in Financial Literacy (Finke, Howe and Huston, 2011) http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1948627

31) Actuaries warn of retirement underfunding risk (Actuaries Institute, 14 November 2013) http://www.actuaries.asn.au/Library/MediaRelease/2013/131114RetirementUnderfunding.pdf

42) Retirement: who’s a happy little vegemite? (Adele Horin) reference Australian Bureau Statistics http://adelehorin.com.au/2013/07/15/retirement-whos-a-happy-little-vegemite/

43) Could you take a grey gap year? (Lima Curtis) http://www.thirdage.co.uk/could-you-take-a-grey-gap-year/

45) 20 year itch – increase in divorce after long marriages (Australian Institute of Family Studies - 27 May 2013) http://www.aifs.gov.au/institute/media/media130527.html The number of people aged 60 and over getting divorced has risen since the 1990’s (Office For National Statistics, 6 August 2013) http://www.ons.gov.uk/ons/rel/family-demography/older-people-divorcing/2011/sty-divorce.html Is the US divorce rate going up rather than going down? (Professor Robert Hughes Jr) http://www.huffingtonpost.com/robert-hughes/is-the-us-divorce-rate-go_b_4908201.html

50) Your Brain and the Future (Ideas at the House, 9 March 2014 https://www.youtube.com/watch?v=FnhHLjYnW Qby+Subject/4125.0~Jan+2012~Main+Features~Suicides~3240