9/19/2015multinational corporate finance prof. r.a. michelfelder 1 outline 6 6. currency futures and...

TRANSCRIPT

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

1

Outline 6

6. Currency Futures and Options6.1 Introduction6.2 Currency Futures 6.2.1 Forward & Futures Contracts6.2.2 Advantages / Disadvantages of Futures6.2.3 How to Use Futures 6.3 Currency Options 6.3.1 Pricing Currency Options6.4 How the Use of Currency Futures & Options Affects MC

Value

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

2

6.1 Introduction

• Derivatives:– Financial contracts or assets that derive their

value from other assets– FX derivatives values derived from the

underlying value of a currency– Used to manage FX risk and to take speculative

risks on currency changes– Future, option and forward contracts are

derivatives

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

3

6.2 Currency Futures

• Futures: contracts with standard volumes and future delivery dates for a currency– A futures contract is a standardized forward contract

• Volume and delivery dates are standard

• Exchange rate is fixed for the day

– Available for a limited number of currencies:• A$, Brazil real, £, CAD$, euro, ¥, Mex. Peso, NZ$, ruble, So.

African rand, Swiss franc

• Currency options availability depends upon demand

– Number of contracts outstanding is “open interest”

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

4

6.2 Currency Futures

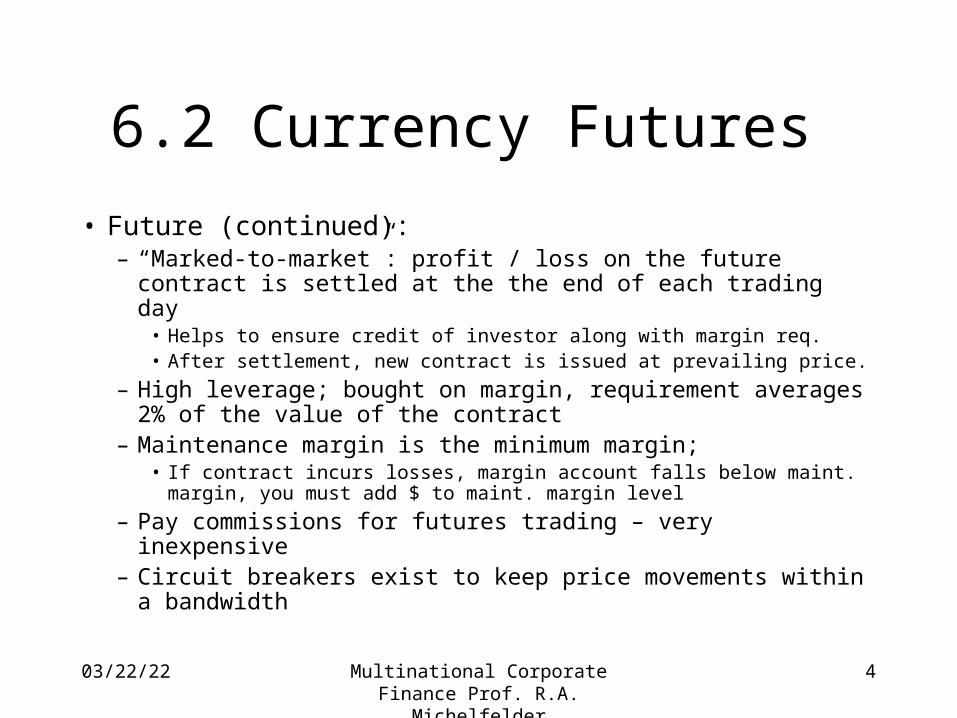

• Future (continued):– “Marked-to-market”: profit / loss on the future contract is

settled at the the end of each trading day• Helps to ensure credit of investor along with margin req. • After settlement, new contract is issued at prevailing price.

– High leverage; bought on margin, requirement averages 2% of the value of the contract

– Maintenance margin is the minimum margin;• If contract incurs losses, margin account falls below maint. margin, you

must add $ to maint. margin level

– Pay commissions for futures trading – very inexpensive– Circuit breakers exist to keep price movements within a

bandwidth

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

5

6.2 Currency Futures

• Future (continued):– If prices drops below floor, trading is halted until

maint. margin requirement is met to ensure payment of losses on the contract

– High leverage and low transactions costs encourages participation in the currency future markets

– Futures are traded on physical exchanges with traders interacting face-to-face

– See cme.com/prices/daily_settlement.cfm for daily futures price data

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

6

6.2 Currency Futures

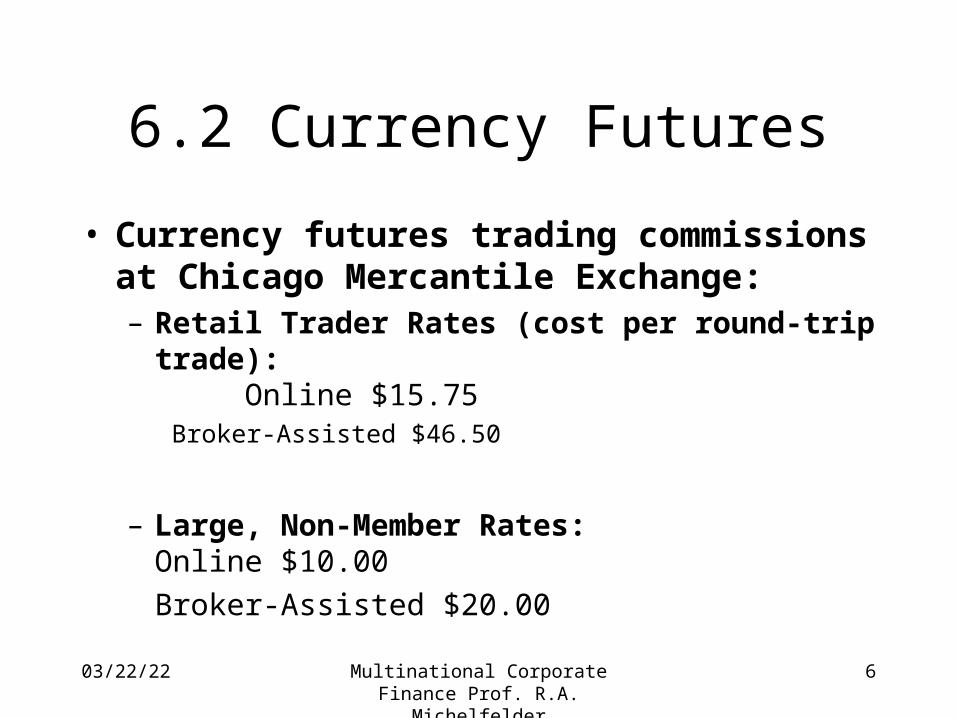

• Currency futures trading commissions at Chicago Mercantile Exchange:– Retail Trader Rates (cost per round-trip trade):

Online $15.75Broker-Assisted $46.50

– Large, Non-Member Rates:Online $10.00

Broker-Assisted $20.00

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

7

6.2 Currency Futures

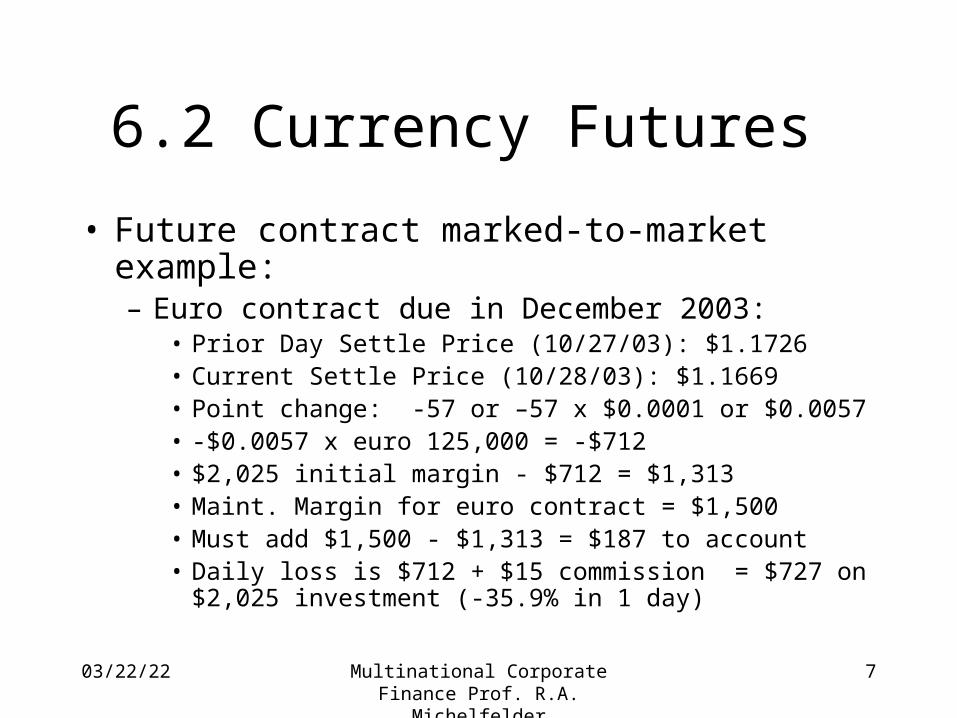

• Future contract marked-to-market example:– Euro contract due in December 2003:

• Prior Day Settle Price (10/27/03): $1.1726• Current Settle Price (10/28/03): $1.1669• Point change: -57 or –57 x $0.0001 or $0.0057• -$0.0057 x euro 125,000 = -$712 • $2,025 initial margin - $712 = $1,313• Maint. Margin for euro contract = $1,500• Must add $1,500 - $1,313 = $187 to account• Daily loss is $712 + $15 commission = $727 on $2,025

investment (-35.9% in 1 day)

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

8

6.2 Currency Futures

• Future contract marked-to-market example:– Canadian $ contract due in December 2003:

• Prior Day Settle Price (10/27/03): $0.7606

• Current Settle Price (10/28/03): $0.7617

• Point change: +11 or +11 x $0.0001 or $0.0011

• +$0.0011 x C$100,000 = +$110

• $608 initial margin + $110 = $719

• Maint. Margin for C$ = $450

• Daily profit is: $110 - $15 commission or $95 on $608 investment (+15.6% in 1 day)

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

9

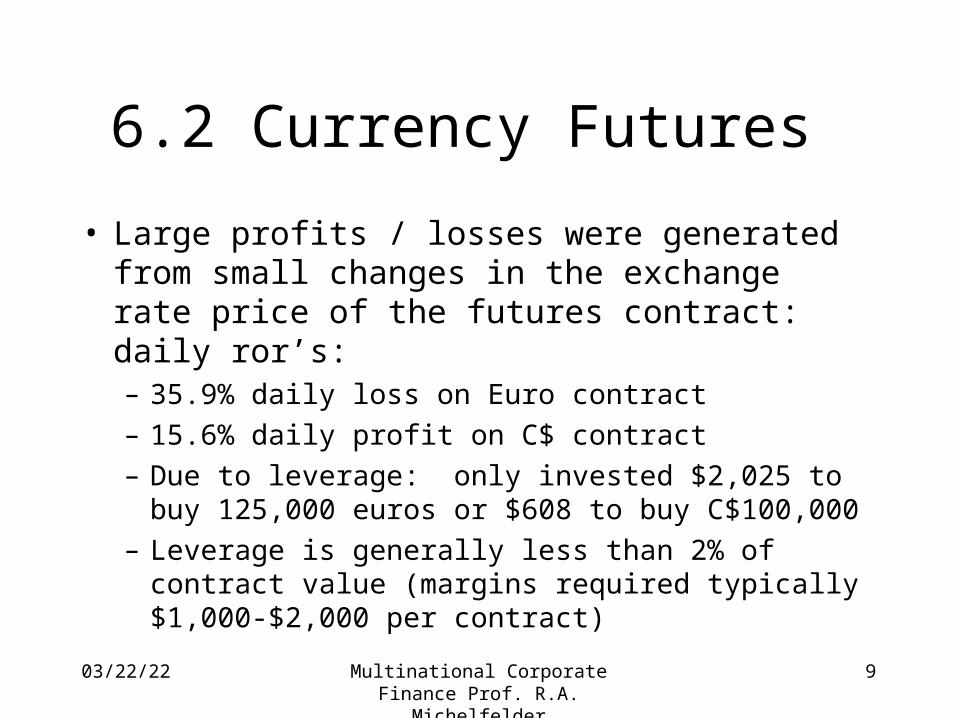

6.2 Currency Futures

• Large profits / losses were generated from small changes in the exchange rate price of the futures contract: daily ror’s:– 35.9% daily loss on Euro contract

– 15.6% daily profit on C$ contract

– Due to leverage: only invested $2,025 to buy 125,000 euros or $608 to buy C$100,000

– Leverage is generally less than 2% of contract value (margins required typically $1,000-$2,000 per contract)

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

10

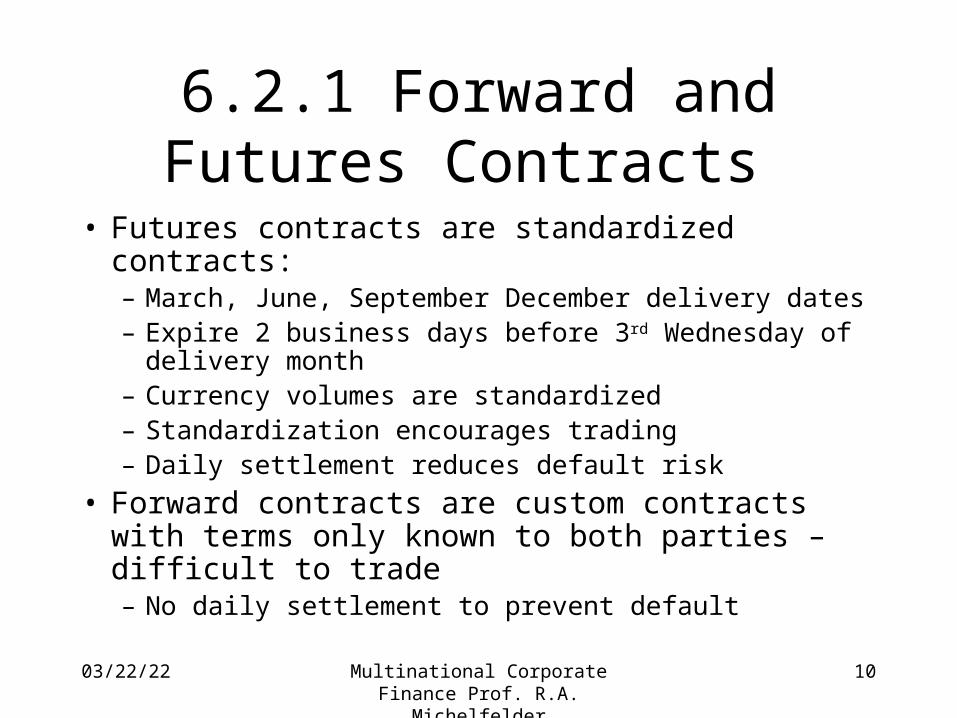

6.2.1 Forward and Futures Contracts

• Futures contracts are standardized contracts:– March, June, September December delivery dates– Expire 2 business days before 3rd Wednesday of

delivery month– Currency volumes are standardized– Standardization encourages trading– Daily settlement reduces default risk

• Forward contracts are custom contracts with terms only known to both parties – difficult to trade– No daily settlement to prevent default

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

11

Forward Futures

Contract Size Customized Standardized

Delivery Date Customized Standardized

Security Deposit None; bank balance required or letter of credit

Small security deposit

Marketplace Telephone Central exchange floors

Regulation Self-regulated Commodity Futures Trading Assoc., National Futures Assoc.

Transactions Costs Bank Bid-Ask Spread Broker Fees

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

12

6.2.2 Advantages / Disadvantages of Futures

Contracts • Small sizes and ability to liquidate any day before

maturity are advantages over forward• Limited currencies, rigid delivery dates, rigid

currency amounts• Futures will only be useful for businesses with a

regular stream of cash in foreign currency• Futures are otherwise too rigid to conform to

specific needs of a business

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

13

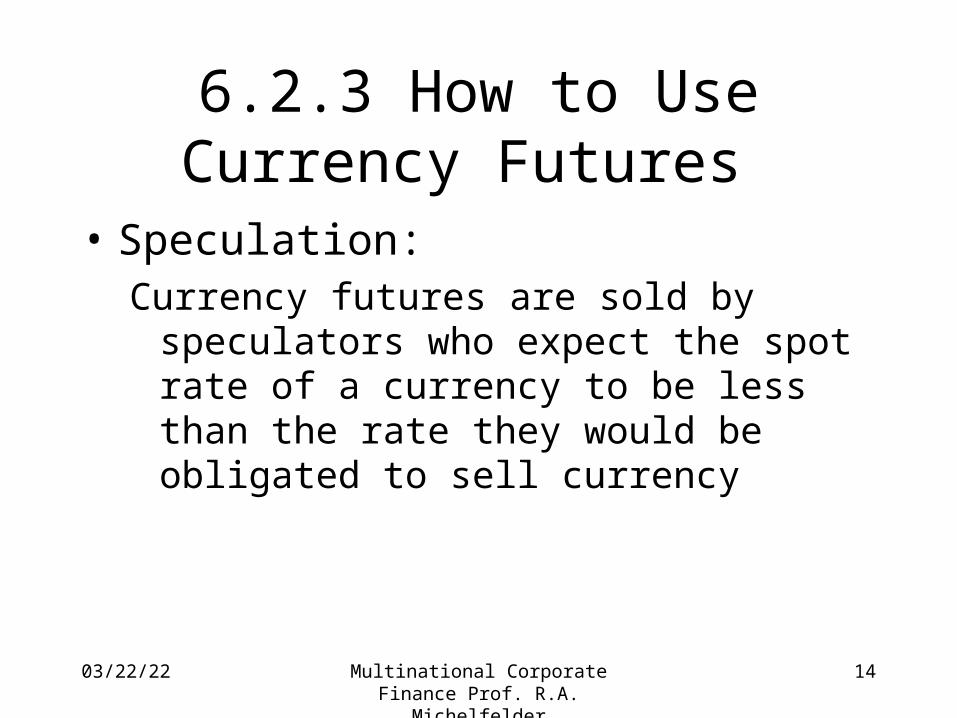

6.2.3 How to Use Currency Futures

• Speculation:– Expect a currency’s value to rise in the future,

buy a futures contract to lock-in the price the currency is bought at a future date

– On the settlement date, buy the currency at price specified by the contract

– Sell at the (hopefully) higher spot rate for a profit

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

14

6.2.3 How to Use Currency Futures

• Speculation:Currency futures are sold by speculators who

expect the spot rate of a currency to be less than the rate they would be obligated to sell currency

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

15

6.2.3 How to Use Currency Futures

• Speculation e.g.:

• April 4 Mexican pesos 500,000 futures contract with a June settlement date priced at $0.09

– On April 4 speculators expect peso to decline sell futures contracts

– On June 17 (settlement date) the spot rate is $0.08:

1. 4/4: Contract to sell 500k pesos: $0.09 x p500,000 = $45,000

2. 6/17: Buy pesos spot: $0.08 x p500,000 = $40,000

3. Sell p500,000 for $0.09 ($45,000) to fulfill the futures contract

4. Gain on the futures position is $5,000

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

16

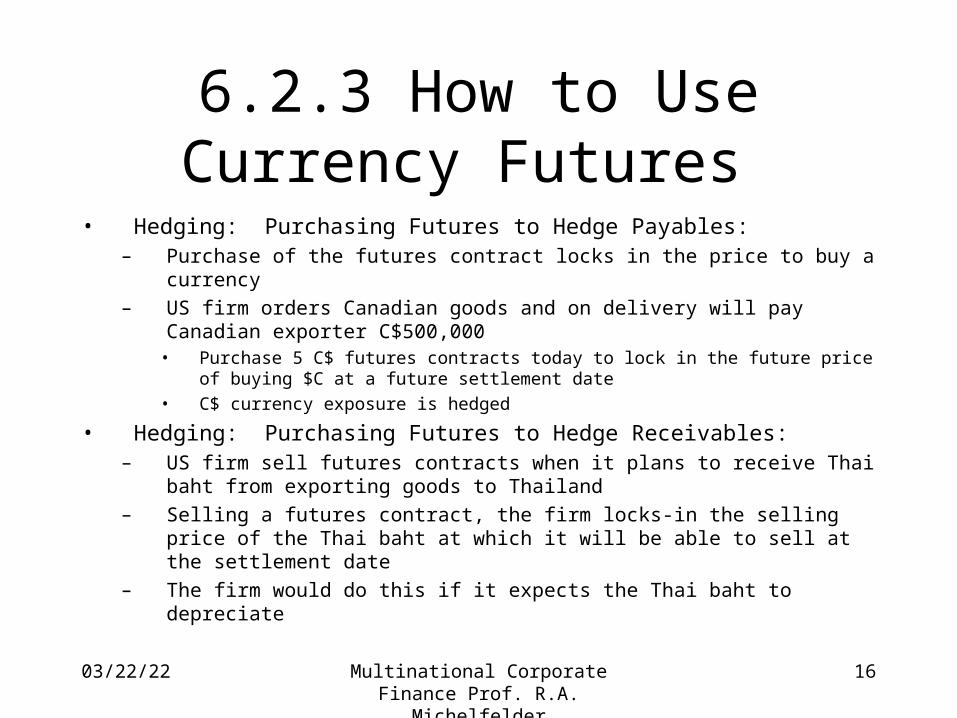

6.2.3 How to Use Currency Futures

• Hedging: Purchasing Futures to Hedge Payables:– Purchase of the futures contract locks in the price to buy a currency

– US firm orders Canadian goods and on delivery will pay Canadian exporter C$500,000

• Purchase 5 C$ futures contracts today to lock in the future price of buying $C at a future settlement date

• C$ currency exposure is hedged

• Hedging: Purchasing Futures to Hedge Receivables:– US firm sell futures contracts when it plans to receive Thai baht from

exporting goods to Thailand

– Selling a futures contract, the firm locks-in the selling price of the Thai baht at which it will be able to sell at the settlement date

– The firm would do this if it expects the Thai baht to depreciate

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

17

6.3 Currency Options

• Option: – Right but not the obligation to sell or buy a financial

instrument at a specified price and volume up to the expiration date

– Currency Call Option: right to buy a specified amount of a currency at a specific price within a specific period of time

– Currency Put Option: right to sell a currency– Standard volumes and future delivery dates

• Open Interest: number of contracts outstanding• Currency options contracts available for limited number of

currencies depending on demand

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

18

6.3 Currency Options

• Option: – The seller of the option must fulfill the contract if the

buyer desires to do so

– The option to not buy or sell has value, the buyer must pay a premium for this privilege

– Currency option has two sides: call (right to buy foreign currency) can be converted to a put (right to sell domestic currency)

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

19

6.3.1 Pricing Currency Options

• Factors that Affect Currency Call Option Premiums:

1. Level of existing spot price relative to strike price

Higher spot rate relative to strike price, the higher the option price

2. Length of time before the expiration date

The longer the time to expiration, the higher the chance the spot rate > strike price

3. Potential variability of currency

Higher the var. of spot rate, the higher the chance that the spot rate will be above the strike price – more volatile currencies have

higher call option prices

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

20

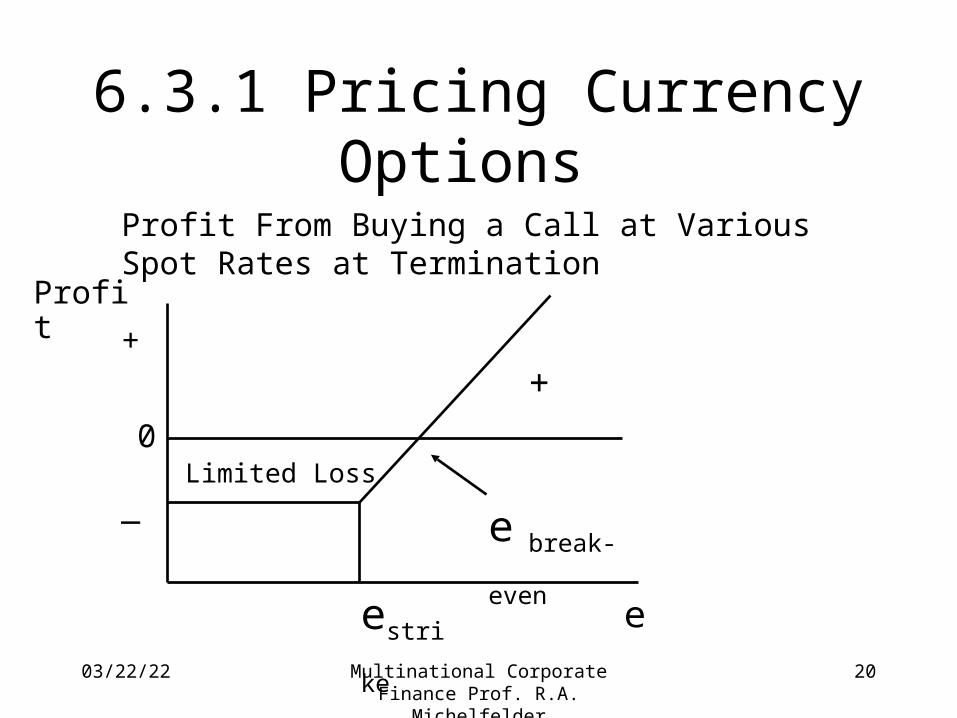

6.3.1 Pricing Currency Options

Profit From Buying a Call at Various Spot Rates at Termination

Profit

e

+

Limited Loss

estrike

0

+

_ e break-even

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

21

6.3.1 Pricing Currency Options

Profit From Selling a Call at Various Spot Rates at Termination

Profit

e

_

Profit = Call Prem.

estrike

0

+

_e break-even

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

22

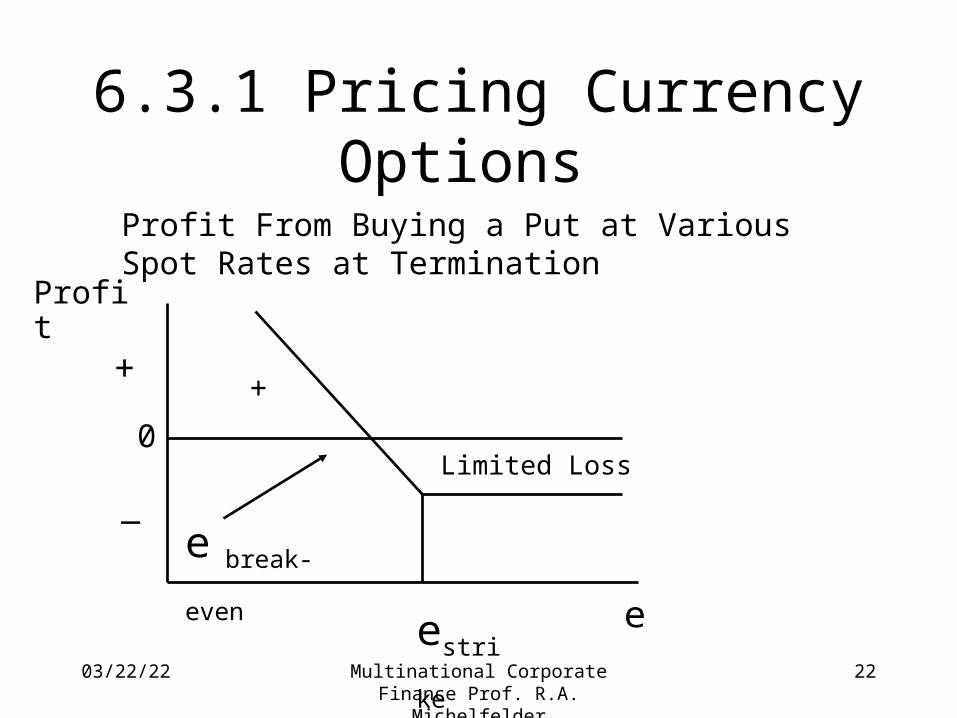

6.3.1 Pricing Currency Options

Profit From Buying a Put at Various Spot Rates at Termination

+

Profit

e

Limited Loss

estrike

0

+

_e break-even

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

23

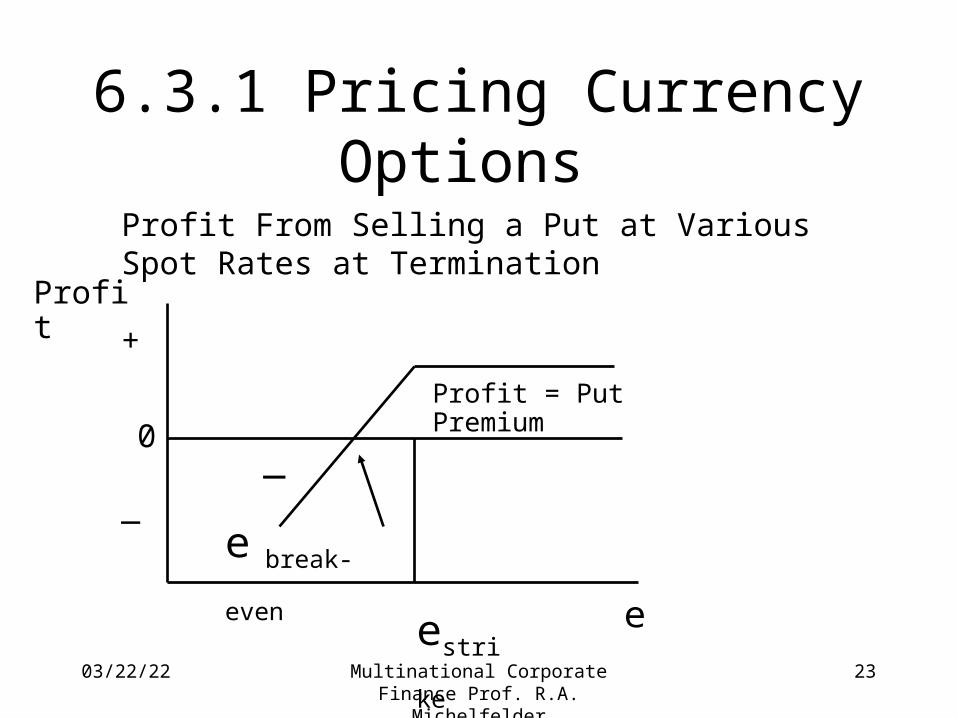

6.3.1 Pricing Currency Options

Profit From Selling a Put at Various Spot Rates at Termination

Profit

e

Profit = Put Premium

estrike

0

+

_e break-even

_

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

24

6.3.1 Pricing Currency Options

SEE EXHIBITS 7.5, 7.6, 7.7, and 7.8 on pp. 194-196

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

25

6.3.1 Pricing Currency Options

• Option Price:– Intrinsic value: difference between spot rate

and exercise or strike price

– Time value: premium above intrinsic value for chance that the option premium can grow or chance that an out-of-the-money option will be in the money (grows with greater time to expiration and volatility of spot rate)

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

26

6.3.1 Pricing Currency Options

• Option Pricing Models:– Will not discuss explicitly due to mathematical

complexity:• Black-Scholes options pricing and other models:

P = f(dom. Interest rate, foreign interest rate, spot rate, standard deviation of spot rate, option’s time to expiration, probability of spot rate > exercise price)

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

27

6.4 How the Use of Currency Futures & Options Affects MC

Value • Currency futures & options can affect the

value of a firm– Futures can prevent the possibility that the

value of foreign currency receipts will because of that currency against the $

04/19/23 Multinational Corporate Finance Prof. R.A. Michelfelder

28

6.4 How the Use of Currency Futures & Options Affects MC

Value • Currency options:

– Offer same protection against depreciation of currencies but allow more flexibility to capitalize on potential appreciation of the foreign currency, but they cost a premium, thereby reducing a MC’s cash flows