9/9/2011 bot 1 10:30 a.m. - penn state university - board ... · penn state investment council,...

TRANSCRIPT

9/9/2011 BOT 1

10:30 a.m. -

1. Roll Call

2. Approval of the Minutes of Previous Meeting

Will the Board of Trustees approve the minutes of the meeting of the Board held on July 15, 2011?

3. President's State-of-the-University Message

4. Informational Report on Research Activities

Henry C. Foley, Vice President for Research, Dean of the Graduate School, will offer a broadoverview of research activity at Penn State.

1:30 p.m. -

5. Reports from Standing Committees

Discussion of action and/or information items by the Standing Committees for consideration by theBoard of Trustees:

A. Committee on Campus Environment - Michael DiBerardinis, Chair

B. Committee on Educational Policy - David M. Joyner, Chair

C. Committee on Finance and Physical Plant - Linda B. Strumpf, Chair

1) Discussion of Consent Agenda Items Provided for Information or Approval ofthe Committee on Finance and Physical Plant:

Information Items - a) East Campus Low Pressure Steam Line Extension, University Parkb) Naming of Rooms, Portions of Buildings, and Plazasc) Status of Major Construction Programs and Borrowingd) Capital Budget Request for Fiscal Year 2012-2013e) Summary and Designation of Gifts Received by the University

Action Items -

f) Proposed Sale of Former Mellon Property to Church of Jesus Christ of LatterDay Saints, State College

g) Summary of Revisions to Existing Scholarships, Fellowships, Etc.h) Acknowledgments of Endowments and Other Major Commitments

(See Appendix I)

9/9/2011 BOT 2

5. Reports from Standing Committees (Continued)

C. Committee on Finance and Physical Plant - Linda B. Strumpf, Chair (Continued)

2) Proposed Naming of the New Level III Biosafety Laboratory the "Eva J. PellLaboratory for Advance Biological Research,'' University Park

The Facilities Naming Committee has recommended that the Board of Trusteesname the new Level III Biosafety Laboratory the "Eva J. Pell Laboratory forAdvanced Biological Research" in honor of the former Senior Vice President ofResearch and Dean of the Graduate School, Eva J. Pell, who as a scientist andadministrator for over 30 years, brought Penn State to the fore in the biologicalsciences. National Institutes of Health (NIH) funds are being used for thisconstruction.

Will the Committee on Finance and Physical Plant recommend to the Board ofTrustees adoption of the following resolution:

RESOLVED, That the new Level III Biosafety Laboratory atUniversity Park is named the "Eva J. Pell Laboratory for AdvancedBiological Research."

(See Appendix II)

3) Appointment of Non-University Employees to the Penn State InvestmentCouncil

In September 2000, Penn State's Board of Trustees established the Penn StateInvestment Council to provide direct oversight of the University's endowment andlong-term investment program. In accordance with the foregoing resolution, thePenn State Investment Council, appointed by the Board of Trustees, includes the:Senior Vice President for Finance and Business/Treasurer of the University (Chair);Executive Director, Office of Investment Management; and five to ninenon-University members (at least one of whom is a member of the Board ofTrustees). [In his capacity as Interim Senior Vice President for Finance andBusiness, it is noted that Gary C. Schultz will serve as chair of the Council; at suchtime as the Senior Vice President for Finance and Business is appointed,Mr. Schultz will resume his responsibilities as a non-University member of theCouncil.] The terms are staggered as follows:

2011 - Arthur D. Miltenberger, Vice President and Chief Financial Officer (Retired),R. K. Mellon & Sons (Ligonier, PA)J. David Rogers, Chief Executive Officer, J.D. Capital Management(Greenwich, CT)Gary Glynn, President and Chief Investment Officer, US Steel and CarnegiePension Fund (New York, NY)

2012 - Timothy J. Crowe, Managing Director, Anchor Point Capital LLC (CoralGables, FL)Edward R. Hintz, Jr., President, Hintz Capital Management, Inc. (Chatham,NJ)Gary C. Schultz, Senior Vice President for Finance and Business/TreasurerEmeritus, The Pennsylvania State University (State College, PA)

9/9/2011 BOT 3

5. Reports from Standing Committees (Continued)

C. Committee on Finance and Physical Plant - Linda B. Strumpf, Chair (Continued)

3) Appointment of Non-University Employees to the Penn State InvestmentCouncil (Continued)

2013 - Carmen Gigliotti, Managing Director, Private Equities of DuPont CapitalManagement (Wilmington, DE)Colleen Ostrowski, Vice President and Treasurer, ITT Corporation(Scarsdale, NY)Linda B. Strumpf, Chief Investment Officer (Retired), The HelmsleyCharitable Trust (New York, NY)

It is proposed to appoint J. David Rogers and Gary Glynn to membership with termsexpiring in 2014.

Will the Committee on Finance and Physical Plant recommend to the Board ofTrustees adoption of the following resolution:

RESOLVED, That J. David Rogers and Gary Glynn,non-University employees, are appointed to the Penn StateInvestment Council for terms ending in 2014.

4) Consideration of Request for 2012-2013 Appropriation for Operations

Will the Committee on Finance and Physical Plant recommend to the Board ofTrustees adoption of the following resolution:

RESOLVED, That the Officers of the University areauthorized to submit to the Legislature, appropriate departments,and offices of the Commonwealth of Pennsylvania, a StateAppropriation Request for fiscal year 2012-2013 in the amount of$293,689,000.

5) Capital Plan Update

Mr. Albert G. Horvath, Senior Vice President for Finance and Business/Treasurer,will provide an update for capital construction projects under consideration throughthe end of the current capital plan, FY 2012/13.

6) Update on the Status of Borrowing and Remaining Debt Capacity

In May 2007, the Board of Trustees authorized an increase in the long-termborrowing for the University. Updates are provided on an annual basis with respectto the status of borrowing and the remaining debt capacity.

9/9/2011 BOT 4

5. Reports from Standing Committees (Continued)

C. Committee on Finance and Physical Plant - Linda B. Strumpf, Chair (Continued)

7) Proposed Appointment of an Architect, Greater Philadelphia InnovationCluster Hub, Philadelphia Navy Yard Building 661 Retrofit, Philadelphia

The Subcommittee on Architect/Engineer Selection will make a report andrecommendation on the appointment of an architect for the Greater PhiladelphiaInnovation Cluster Hub, Philadelphia Navy Yard Building 661 Retrofit inPhiladelphia.

8) Proposed Appointment of an Architect, Old Main Renovations, University Park

The Subcommittee on Architect/Engineer Selection will make a report andrecommendation on the appointment of an architect for Old Main Renovations atUniversity Park.

9) Investment Review of Endowment and Similar Funds as of June 30, 2011

Appendix III is an informational report on the University’s Endowment and SimilarFunds as of June 30, 2011. A brief presentation will be made at the meeting.

(See Appendix III)

10) Photo Report on Selected Construction Projects

A photo report on the progress of selected construction projects will be presentedat the meeting.

6. Legal Matters

Cynthia A. Baldwin, Vice President and General Counsel, will present an informational report onUniversity legal matters and/or policies normally considered by a Standing Committee of the Board.

7. Recommendation for Approval to Grant Honorary Degrees

Will the Board of Trustees approve the following resolution:

RESOLVED, that the Board of Trustees approves the granting of theHonorary Doctorate of Humane Letters to Eric Thomas, M.D. and the granting of theHonorary Doctorate of Humane Letters to Dr. Gary Orfield at upcomingcommencement ceremonies.

8. Proposed Election of Officer

Dr. Graham B. Spanier, Secretary of the Board of Trustees, will nominate Gary C. Schultz(replacing Albert G. Horvath) as Treasurer of the Board of Trustees, effective September 12, 2011,to serve until the annual election in January 2012.

9. Announcements by the Chairman of the Board of Trustees

9/9/2011 - Consent Agenda F&PP

(Appendix I)- 1 -

1. East Campus Low Pressure Steam Line Extension, University Park

The University is planning to construct approximately 1,000 feet of low pressure steam piping extending fromnear East Area Locker Room to Bigler Road near the Millennium Science Complex. This new service willsupport future low pressure steam systems in this vicinity. The project cost estimate is $1,700,000.

(See Appendix I.1)

2. Naming of Rooms, Portions of Buildings and Plazas

The Facilities Naming Committee has made certain recommendations to the President on the naming ofrooms, portions of buildings and plazas. In accordance with the Policy on Naming University Facilities, theBoard of Trustees is hereby informed that the President has approved the following naming actions:

A. Several spaces within Moore Building as follows:

1) Conference Room, 250 Moore Building, for a gift from the estate of Harold H. and Harriet BBenjamin. The recognition plaque should read:

Harold H. and Harriet B. Benjamin Conference Room

2) Laboratory, 459 Moore Building, for a gift from Herschel and Eileen Leibowitz. Therecognition plaque should read:

Herschel W. and Eileen Wirtshafter Leibowitz Laboratory

3) Conference Room, 467 Moore Building, for a gift from Hellene Runtagh. The recognitionplaque should read:

Hellene Runtagh Conference Room

4) Advising Office. 125E Moore Building, for a gift from Margaret "Peg" West The recognitionplaque should read:

Margaret A. West, 1972, Advising Office

5) Laboratory, 607 Moore Building, for a gift from Gary and Linda Kaplan. The recognitionplaque should read:

Gary and Linda Kaplan Laboratory

B. Several spaces within the Sheetz Center for Entrepreneurial Excellence at Penn State Altoona asfollows:

1) Trading Room for a commitment from Michael and Gail Irwin. The recognition plaque shouldread:

Michael and Gail Irwin Family Trading Room

2) Conference Room (first floor) for a gift from Young, Oakes, Brown and Company. Therecognition plaque should read:

Young, Oakes, Brown and Company Conference Room

3) Lounge (first floor) for a gift-in-kind from the Hite Company. The recognition plaque shouldread:

Hite Company Lounge

9/9/2011 - Consent Agenda F&PP

(Appendix I)- 2 -

2. Naming of Rooms, Portions of Buildings and Plazas (Continued)

B. Several spaces within the Sheetz Center for Entrepreneurial Excellence at Penn State Altoona asfollows: (Continued)

4) Incubator (second Floor) for a commitment from the Students in Free Enterprise (SIFE)Business Advisory Board. The recognition plaque should read:

Students in Free Enterprise (SIFE) Business Advisory Board Business Incubator

5) Lounge/Dining Area (first floor) for a commitment from Phillip and Rosalind Sky and Neil andMarilyn Port families. The recognition plaque should read:

Port-Sky Lounge

6) Lobby (first floor), for a commitment from Don and Sherry Brett. The recognition plaqueshould read:

Brett Lobby

C. The engineering classroom, Room 322 at Penn State Lehigh Valley, for a commitment from Daniel L.Puchyr. The recognition plaque should read:

This laboratory named in recognition of generous support from Judy and Dan Puchyr

D. Rename the "South Annex" in the Bryce Jordan Center the "Basketball Practice Facility."

E. Several spaces in the Knowledge Commons, Pattee Library, as follows:

1) Quick Access Service Area for a gift from Joseph DiGiacomo. The recognition plaque shouldread:

Joseph DiGiacomo Quick Access Service Area

2) Atrium seating area for a gift from Cindy Joyce. The recognition plaque should read:

Cindy Joyce Atrium Seating

3) Atrium seating area for a gift from Virginia Todd Chapel. The recognition plaque should read:

In Memory of Bob and Loretta Todd Atrium Seating

3. Status of Major Construction Programs and Borrowing

(See Appendix I.2)

4. Capital Budget Request for Fiscal Year 2012-2013

Penn State has identified several projects as a priority and annually submits a list of those projects to theCommonwealth's Department of Education for further consideration by the Legislature. In order for theGovernor to release funds for capital projects, the projects must have prior authorization and approval by theLegislature. The Capital Budget Request consists of those projects for which the University is seekingauthorization for subsequent funding by the Governor.

9/9/2011 - Consent Agenda F&PP

(Appendix I)- 3 -

4. Capital Budget Request for Fiscal Year 2012-2013 (Continued)

For fiscal year 2012-2013, the University will submit a Capital Budget Request to the Commonwealth forauthorization of $187.6 million of which $159 million is for construction projects and the remaining$28.6 million is for original equipment.

(See Appendix I.3)

5. Summary and Designation of Gifts Received by the University

Appendix I.5 is a summary and designation of gifts received by the University during the period July 1, 2010through June 30, 2011.

(See Appendix I.4)

6. Proposed Sale of Former Mellon Property to Church of Jesus Christ of Latter Day Saints, State College

In July 1999, the University acquired approximately 1,100 acres of undeveloped land at various locationsthroughout Centre County, Pennsylvania, from the Mellon Family Trust and the Richard King MellonFoundation. The purchase resulted in the University acquiring six (6) tracts of land, comprised of sixteen (16)separately deeded parcels, for $3,800,000. Terms of this purchase do not obligate the University to retainthese tracts, and since that time the University has sold several parcels to various municipalities for public parkand recreation use.

The University has received a purchase offer for one such parcel, comprised of .254 undeveloped acreslocated in State College Borough, from the Corporation of the Presiding Bishop of the Church of Jesus Christof Latter Day Saints in the amount of $25,000.

RESOLVED, That the Board of Trustees approves the sale of .254 acres in StateCollege, Centre County, Pennsylvania, to the Corporation of the Presiding Bishop of theChurch of Jesus Christ of Latter Day Saints in the amount of $25,000.

BE IT FURTHER RESOLVED, That the Officers of the University are authorized anddirected to take such steps as are necessary to make effective this resolution.

(See Appendix I.5)

7. Summary of Revisions to Existing Scholarships, Fellowships, Etc. (For the period June 20, 2011through August 12, 2011)

Will the Committee on Finance and Physical Plant recommend to the Board of Trustees adoption of thefollowing resolution:

RESOLVED, That the conditions governing certain existing scholarships, fellowships,awards, and similar funds previously established at the University be revoked and that theOfficers of the University are authorized to put into effect the revised regulations as requestedby the donors.

8. Acknowledgments of Endowments and Other Major Commitments

The Committee on Finance and Physical Plant is advised that for the period June 20, 2011, throughAugust 12, 2011, 28 new funds totaling approximately $4,454,361 were accepted by the University, includingscholarships, fellowships, etc. All of these items conform to established University policies and regulations.

9/9/2011 - Consent Agenda F&PP

(Appendix I)- 4 -

8. Acknowledgments of Endowments and Other Major Commitments (Continued)

For the period May 1, 2011 through June 30, 2010, 48 major commitments were accepted by the Universitytotaling approximately $27,289,375.

Will the Committee on Finance and Physical Plant recommend to the Board of Trustees adoption of thefollowing resolutions:

RESOLVED, That the Board of Trustees gratefully acknowledges the generouscontributions of the many friends of the University in support of endowments, funds, and othermajor commitments as reported to the Committee on Finance and Physical Plant at itsmeeting of September 9, 2011.

FURTHER BE IT RESOLVED, That the Officers of the University are authorized toconvey the Board's appreciation to these generous benefactors who provide opportunitiesfor many students to receive a quality education.

(Appendix I.1) -1-

9/9/2011 F&PP

N

Un

iver

sity

Par

k

Eas

t C

amp

us

Lo

w P

ress

ure

Ste

am L

ine

Ext

ensi

on

Pol

lock

Roa

d

Bigler Road

University Drive

Mill

enni

um S

C

East Area

Locker Room

Hol

uba

Hal

l

Bry

ce J

orda

n C

ente

r

Aug

ust 3

1, 2

011

Bol

d -

Com

plet

ed, I

talic

s -

Pro

ject

ed

Bud

get C

omm

onw

ealth

Gift

Arc

h/En

gFi

nal P

lan

Star

t C

ompl

etio

n C

ampu

sPr

ojec

t Nam

eA

mou

ntFu

ndin

gA

mou

ntSe

lect

ion

App

rova

lD

ate

Dat

e

Alto

ona

Por

t Sky

Caf

é$5

,400

,000

$0$0

N/A

03/1

105

/12

08/1

2

Ber

ksG

aige

Tec

hnol

ogy

and

Bus

ines

s In

nova

tion

Bui

ldin

g$2

5,70

0,00

0$0

$3,0

00,0

0011

/07

01/1

004

/10

10/1

1

Chi

ldre

n's

Hos

pita

l$2

06,5

00,0

00$1

4,00

0,00

0$6

5,00

0,00

011

/05

11/0

903

/10

10/1

2

Sup

port

Ser

vice

s B

uild

ing

$19,

000,

000

$0$0

01/0

903

/10

06/1

011

/11

Bea

ver

Sta

dium

Sco

rebo

ard

Upg

rade

s$6

,800

,000

$0$0

07/1

111

/11

12/1

108

/12

Bea

ver

Sta

dium

N. E

nd Z

one

and

AD

A R

enov

atio

n$9

,898

,885

$0$0

N/A

09/1

012

/10

08/1

1

Bio

Beh

avio

ral H

ealth

Bui

ldin

g$4

8,10

0,00

0$4

0,00

0,00

0$0

01/0

807

/10

12/1

010

/12

Bio

logi

cal R

esea

rch

Labo

rato

ry

$23,

000,

000

$0$0

11/0

711

/10

09/1

112

/12

Ced

ar B

uild

ing

Ren

ovat

ions

$7,9

50,0

00$7

,140

,000

$003

/11

11/1

102

/12

08/1

3

Eas

t Cam

pus

Ste

am L

ine

$13,

500,

000

$11,

000,

000

$0N

/A03

/11

06/1

108

/12

Env

ironm

enta

l Im

prov

emen

ts B

FP

Inst

alla

tions

$8,1

20,0

00$7

,000

,000

$0N

/AN

/A06

/08

08/1

4

Ess

entia

l Ser

vice

s P

rogr

am$1

1,95

0,00

0$3

,000

,000

$0N

/AN

/A12

/05

12/1

4

Hen

ders

on S

outh

(P

hase

II)

$56,

500,

000

TB

D$0

01/0

8T

BD

TB

DT

BD

HU

B A

dditi

on$2

5,80

0,00

0$0

$003

/11

TB

DT

BD

TB

D

Peg

ula

Ice

Are

na$8

9,00

0,00

0$0

$89,

000,

000

11/1

001

/12

01/1

209

/13

IM B

uild

ing

Add

ition

$24,

000,

000

$0$0

01/1

1T

BD

TB

DT

BD

Moo

re B

uild

ing

Add

ition

$26,

100,

000

$23,

190,

000

$1,8

00,0

0007

/08

05/1

006

/10

12/1

1

Moo

re B

uild

ing

Ren

ovat

ion

Sta

ge$2

1,90

0,00

0$2

0,05

0,00

0$1

,200

,000

07/0

811

/11

02/1

208

/13

Pol

lock

Din

ing

Com

mon

s R

enov

atio

n$1

1,70

0,00

0$0

$0N

/A11

/10

01/1

108

/11

Sou

th F

rear

Ren

ovat

ions

$6,1

10,0

00$2

,460

,000

$0N

/A03

/11

05/1

101

/13

Sou

th H

alls

Ren

ovat

ions

(P

hase

I)$3

0,00

0,00

0$0

$003

/11

TB

DT

BD

TB

D

Ste

am P

rodu

ctio

n M

odifi

catio

ns$2

5,00

0,00

0$0

$001

/11

07/1

2T

BD

TB

D

Tra

nsfo

rmer

Rep

lace

men

t Pro

gram

$9,6

00,0

00$1

,000

,000

$0N

/AN

/A06

/07

12/1

3

Wat

er F

iltra

tion

Pla

nt$3

0,00

0,00

0$2

5,00

0,00

0$0

01/1

107

/12

06/1

206

/13

Wes

t Cam

pus

Chi

lled

Wat

er$1

1,90

0,00

0$6

,500

,000

$0N

/A03

/11

05/1

103

/12

Wes

t Pat

tee

Libr

ary

Ren

ovat

ions

$7,0

00,0

00$0

$7,0

00,0

00N

/A03

/11

05/1

112

/11

Sum

mar

y of

Uni

vers

ity L

ong-

Term

Deb

t - $

(000

) (ex

clud

ing

PCT)

Aut

horiz

ed B

orro

win

g St

atus

- $(

000)

(exc

ludi

ng P

CT)

$1,0

41,9

30B

orro

win

g A

utho

rity

per

May

200

7 B

oard

of T

rus

$600

,000

Cap

ital L

ease

s, B

onds

, & N

otes

Issu

ed

($31

2,08

7)

Fut

ure

Cap

italiz

ed L

ease

s &

Oth

er A

ntic

ipat

ed C

($6,

100)

Est

imat

ed A

utho

rity

Rem

aini

ng$2

81,8

13

BO

T M

ilest

ones

Her

shey

Uni

vers

ity P

ark

Con

stru

ctio

n is

app

roxi

mat

ely

12%

com

plet

e.

Con

stru

ctio

n is

app

roxi

mat

ely

10%

com

plet

e.

Con

stru

ctio

n is

app

roxi

mat

ely

30%

com

plet

e.

Pro

ject

pro

gram

is a

ppro

xim

atel

y 65

% c

ompl

ete.

Con

stru

ctio

n is

app

roxi

mat

ely

50%

com

plet

e.

Con

stru

ctio

n is

app

roxi

mat

ely

95%

com

plet

e.

STA

TU

S O

F M

AJO

R C

ON

STR

UC

TIO

N P

RO

GR

AM

S A

ND

BO

RR

OW

ING

( >

$5

Mill

ion

)

Con

stru

ctio

nPr

ojec

t Dat

a N

otes

Pro

ject

in d

esig

n.

Con

stru

ctio

n is

app

roxi

mat

ely

95%

com

plet

e.

On

HO

LD.

Con

stru

ctio

n is

app

roxi

mat

ely

70%

com

plet

e.

Est

imat

ed b

onds

, not

es a

nd c

apita

l lea

ses

as o

f Jun

e 30

, 201

1 (u

naud

ited)

Pro

ject

beg

inni

ng d

esig

n.

Con

stru

ctio

n ex

pect

ed to

sta

rt in

Sep

tem

ber

2011

.

Pro

ject

in d

esig

n.

On

HO

LD.

Pos

tpon

ed.

Pro

ject

pro

gram

is a

ppro

xim

atel

y 50

% c

ompl

ete.

Pro

ject

beg

inni

ng d

esig

n.

Con

stru

ctio

n is

app

roxi

mat

ely

95%

com

plet

e.

Pro

ject

in d

esig

n.

Con

stru

ctio

n is

app

roxi

mat

ely

35%

com

plet

e.

Pro

ject

in s

chem

atic

des

ign.

Pro

ject

in d

esig

n.

Con

stru

ctio

n is

app

roxi

mat

ely

90%

com

plet

e.

Pro

ject

pro

gram

is a

ppro

xim

atel

y 55

% c

ompl

ete.

Con

stru

ctio

n is

app

roxi

mat

ely

5% c

ompl

ete.

Pro

ject

in d

esig

n.

Pro

ject

in d

esig

n.

(Appendix I.2) -1-

9/9/2011 F&PP

TH

E P

EN

NS

YL

VA

NIA

ST

AT

E U

NIV

ER

SIT

Y

PR

OP

OS

ED

CA

PIT

AL

BU

DG

ET

RE

QU

ES

T F

OR

201

2-13

Pri

ori

ty

Am

ou

nt

Nu

mb

er

201

2-20

13 C

on

stru

ctio

n P

roje

cts

R

equ

este

d

1.

Cap

ital

Ren

ewal

, P

has

e V

(U

niv

ers

ity

Par

k)

$40

,000

,000

Thi

s pr

ojec

t is

par

t fiv

e of

an

effo

rt t

o m

ake

sign

ifica

nt c

ompr

ehen

sive

upg

rade

s to

the

bui

ldin

gs a

t U

nive

rsity

Par

k.

The

re a

re o

ver

600

bui

ldin

gs a

t th

e

Uni

vers

ity P

ark

Cam

pus

that

we

re c

onst

ruct

ed f

rom

the

ear

ly 1

900’

s th

roug

h th

e 19

70’s

. L

imite

d fu

ndin

g fo

r m

aint

enan

ce h

as a

llow

ed o

nly

for

the

supp

ort

of

com

pone

nt r

ep

lace

men

t of

alr

ead

y a

ntiq

uate

d s

yste

ms

and

pie

cem

eal i

mpr

ovem

ent

s, le

avin

g m

an

y of

the

old

er f

acili

ties

bare

ly a

ccep

tabl

e fo

r th

eir

prog

ram

s an

d oc

cup

ants

. T

his

proj

ect

will

allo

w t

he

Uni

vers

ity t

o re

plac

e, i

nsta

ll or

upg

rade

as

appr

opria

te s

yste

ms

in m

ajor

aca

dem

ic,

rese

arch

and

ad

min

istr

ativ

e

build

ings

acr

oss

cam

pus

that

we

re n

ot a

ddre

ssed

in th

e ot

her

phas

es o

f ren

ew

al.

Mos

t of

the

bu

ildin

gs h

ave

exc

eed

ed t

hei

r el

ectr

ical

cap

acity

an

d th

e l

ight

ing

and

wir

ing

is

old

an

d de

terio

ratin

g.

The

age

an

d e

xten

sive

use

of

mo

st o

f th

e pu

blic

bui

ldin

gs

is n

otic

eab

le i

n t

hat

floor

ing

is d

amag

ed,

ceili

ngs

are

sta

ined

, pa

int

and

oth

er i

nter

ior

finis

hes

are

cra

cke

d,

pee

ling

and

wo

rn,

and

pub

lic

rest

room

s ar

e di

ng

y.

Thi

s pr

ojec

t w

ill a

llow

the

Uni

vers

ity t

o ad

dres

s th

ese

item

s an

d w

ill p

rovi

de a

n op

port

unity

to

ad

dres

s va

ryin

g sa

fety

issu

es a

nd

ener

gy

effic

ienc

y an

d co

nser

vatio

n.

Wor

k m

ay in

clud

e co

nnec

tion

or u

pgra

des

to c

entr

al u

tility

sys

tem

s, s

uch

as c

hille

d w

ater

, w

ater

, ele

ctric

, et

c.

2.

Cap

ital

Ren

ew

al, P

has

e IV

(E

aste

rn R

egio

n C

amp

use

s)

$28,

000

,000

The

Com

mon

we

alth

Cam

puse

s ar

e n

ot e

xem

pt f

rom

cha

nge

s in

tec

hno

log

y, p

rogr

ams,

clie

nt e

xpec

tatio

ns,

safe

ty a

nd

bui

ldin

g co

des,

res

earc

h an

d

inst

ruct

iona

l d

eman

ds o

n th

eir

faci

litie

s.

Lim

ited

ma

inte

nan

ce f

und

ing

has

on

ly s

uppo

rted

com

pon

ent

repl

acem

ent

of

alre

ady

ant

iqua

ted

syst

ems,

allo

we

d

piec

emea

l im

prov

emen

ts a

nd b

arel

y ke

pt m

ost

of t

he o

lder

fac

ilitie

s ac

cept

able

for

the

pro

gram

s an

d oc

cupa

nts.

T

his

proj

ect,

pha

se t

hre

e of

a s

erie

s, w

ill

cont

inue

the

effo

rt a

t th

e U

nive

rsity

’s E

aste

rn R

egio

n C

ampu

ses

(Wor

thin

gton

Scr

anto

n, W

ilkes

-Bar

re,

Haz

leto

n, L

ehig

h V

alle

y, B

erks

, A

bing

ton,

Bra

ndyw

ine

and

Gre

at V

alle

y) t

o re

plac

e, i

nsta

ll or

upg

rade

ce

ntra

l h

eatin

g, v

entil

atio

n, m

ech

anic

al a

nd

air

con

ditio

nin

g sy

ste

ms

in m

ajor

aca

dem

ic,

rese

arch

an

d

adm

inis

trat

ive

bui

ldin

gs.

The

pro

ject

will

re

plac

e ro

of s

yste

ms,

up

grad

e or

rep

lace

bu

ildin

g st

ruct

ura

l an

d e

xter

ior

syst

ems,

ins

tall

or u

pgra

de t

o cu

rren

t bu

ildin

g co

des

, el

ectr

ical

and

oth

er u

tility

ser

vice

s, r

epa

ir m

ajor

bui

ldin

g e

ntra

nces

, pr

ovid

e ne

w e

nerg

y ef

ficie

nt w

indo

ws

an

d lig

htin

g s

yste

ms

and

repl

ace

antiq

uate

d w

ater

an

d p

lum

bin

g sy

stem

s.

Upg

rade

s an

d m

oder

niza

tion

to

inte

rior

bui

ldin

g fin

ish

es,

room

co

nfig

urat

ions

an

d re

st r

oom

fac

ilitie

s w

ill b

e co

mpl

eted

as

app

ropr

iate

. U

pgr

ades

or

new

con

stru

ctio

n to

cen

tral

po

wer

or

utili

ty p

lant

s w

ill b

e in

clud

ed a

s ne

cess

itate

d b

y th

e pr

ojec

t.

3.

Cap

ital

Ren

ew

al,

Ph

ase

IV (

Cen

tral

Reg

ion

Cam

pu

ses

) $2

8,0

00,0

00

The

Com

mon

we

alth

Cam

puse

s ar

e n

ot e

xem

pt f

rom

cha

nge

s in

tec

hno

log

y, p

rogr

ams,

clie

nt e

xpec

tatio

ns,

safe

ty a

nd

bui

ldin

g co

des,

res

earc

h an

d

inst

ruct

iona

l d

eman

ds o

n th

eir

faci

litie

s.

Lim

ited

ma

inte

nan

ce f

und

ing

has

on

ly s

uppo

rted

com

pon

ent

repl

acem

ent

of

alre

ady

ant

iqua

ted

syst

ems,

allo

we

d

piec

emea

l im

pro

vem

ent

s an

d b

arel

y ke

pt m

ost

of t

he o

lde

r fa

cilit

ies

acce

ptab

le f

or t

he

prog

ram

s a

nd o

ccup

ants

. T

his

pro

ject

, p

hase

thr

ee

of a

ser

ies,

will

co

ntin

ue t

he e

ffor

t at

the

Uni

vers

ity’s

Cen

tral

Reg

ion

Ca

mpu

ses

(Alto

ona

, M

ont

Alto

, H

arris

bur

g, S

chu

ylki

ll, Y

ork

and

Dic

kins

on

Sch

ool

of L

aw

-Car

lisle

) to

re

plac

e, in

stal

l or

upgr

ade

cent

ral h

eatin

g, v

entil

atio

n, m

ech

anic

al a

nd a

ir c

ondi

tioni

ng s

yste

ms

in m

ajor

aca

dem

ic,

rese

arch

and

adm

inis

trat

ive

build

ings

. T

he

proj

ect

will

rep

lace

roo

f sy

ste

ms,

upg

rad

e or

rep

lace

bui

ldin

g st

ruct

ura

l an

d e

xter

ior

syst

ems,

inst

all

or u

pgra

de t

o c

urre

nt b

uild

ing

cod

es,

elec

tric

al a

nd

othe

r ut

ility

ser

vice

s, r

epai

r m

ajor

bui

ldin

g e

ntra

nce

s, p

rovi

de n

ew

en

erg

y ef

ficie

nt w

ind

ow

s an

d lig

htin

g sy

stem

s a

nd r

epl

ace

antiq

uat

ed w

ater

an

d pl

umbi

ng

sy

stem

s.

Up

grad

es a

nd

mod

erni

zatio

n t

o in

terio

r bu

ildin

g f

inis

hes

, ro

om c

onfig

urat

ions

and

res

t ro

om f

aci

litie

s w

ill b

e c

ompl

ete

d as

app

ropr

iate

. U

pgr

ades

or

new

con

stru

ctio

n to

cen

tral

po

wer

or

utili

ty p

lant

s w

ill b

e in

clud

ed a

s ne

cess

itate

d by

the

pro

ject

.

(Appendix I.3) -1-

9/9/2011 F&PP

4.

Cap

ital

Ren

ew

al,

Ph

ase

IV (

Wes

tern

Reg

ion

Cam

pu

ses

) $2

8,0

00,0

00

The

Com

mon

wea

lth C

ampu

ses

are

not

exe

mpt

fro

m c

hang

es i

n te

chno

logy

, pr

ogra

ms,

clie

nt e

xpec

tatio

ns,

safe

ty a

nd b

uild

ing

code

s, r

esea

rch

and

in

stru

ctio

nal

dem

ands

on

thei

r fa

cilit

ies.

L

imite

d m

ain

ten

ance

fun

din

g h

as o

nly

sup

port

ed c

omp

onen

t re

plac

eme

nt o

f al

read

y a

ntiq

uate

d sy

stem

s, a

llow

ed

pi

ecem

eal

imp

rove

me

nts

and

bar

ely

kept

mos

t of

the

old

er

faci

litie

s ac

cept

able

for

th

e pr

ogra

ms

and

occ

upan

ts.

Thi

s pr

oje

ct,

pha

se t

hre

e of

a s

erie

s, w

ill

cont

inue

the

effo

rt a

t th

e U

nive

rsity

’s W

est

ern

Reg

ion

Ca

mpu

ses

(Eri

e, S

hen

ango

, D

uB

ois,

Be

aver

, N

ew

Ken

sing

ton,

Gre

ater

Alle

ghen

y an

d F

aye

tte)

to

repl

ace,

inst

all o

r up

grad

e ce

ntra

l hea

ting,

ven

tilat

ion,

mec

han

ical

and

air

con

ditio

ning

sys

tem

s in

maj

or a

cade

mic

, res

ear

ch a

nd a

dmin

istr

ativ

e bu

ildin

gs.

The

pr

ojec

t w

ill r

epla

ce r

oof

syst

em

s, u

pgra

de

or r

epla

ce b

uild

ing

stru

ctur

al a

nd

ext

erio

r sy

stem

s, in

sta

ll or

upg

rade

to

cur

rent

bui

ldin

g c

odes

, el

ectr

ical

an

d ot

her

utili

ty s

ervi

ces,

rep

air

maj

or b

uild

ing

ent

ran

ces,

pro

vide

ne

w e

ner

gy

effic

ient

win

do

ws

and

light

ing

syst

ems

and

re

plac

e an

tiqu

ated

wat

er a

nd

plum

bin

g

syst

ems.

U

pgr

ades

an

d m

oder

niza

tion

to

inte

rior

build

ing

fin

ish

es,

room

con

figur

atio

ns a

nd r

est

room

fa

cilit

ies

will

be

com

ple

ted

as a

ppro

pria

te.

Up

grad

es o

r ne

w c

onst

ruct

ion

to c

entr

al p

ow

er o

r ut

ility

pla

nts

will

be

incl

uded

as

nece

ssita

ted

by t

he p

roje

ct.

5.

Dis

aste

r R

eco

very

/Bu

sin

ess

Co

nti

nu

ity

Dat

a C

ente

r (l

oca

tio

n t

o b

e d

eter

min

ed)

$35,

000,

000

T

he U

nive

rsity

has

be

enas

sess

ing

its b

usin

ess

cont

inui

ty v

uln

erab

ility

in t

he e

vent

of

a ca

tast

roph

ic lo

ss o

f co

mpu

ter

data

an

d sy

stem

s at

Uni

vers

ity P

ark.

To

addr

ess

this

co

ncer

n, c

ons

ulta

nts

have

rec

om

men

ded

th

e de

velo

pmen

t o

f a

mirr

or s

ite t

hat

can

be

fully

ope

ratio

nal i

n m

omen

ts if

suc

h an

eve

nt s

ho

uld

occu

r.

The

faci

lity

nee

ds to

be

with

in a

n ap

pro

xim

ate

sixt

y-m

ile d

ista

nce

of th

e U

niv

ersi

ty P

ark

Cam

pus.

T

his

proj

ect

will

inc

lud

e th

e a

cqui

sitio

n of

an

app

ropr

iate

site

in

the

serv

icea

ble

are

a th

at c

an b

e re

adi

ly d

eve

lop

ed t

o m

eet

the

nee

ds

of t

his

typ

e o

f fa

cilit

y.

The

faci

lity

will

hou

se s

erve

r ra

cks

to a

ccom

mod

ate

the

curr

ent n

eeds

of t

he U

nive

rsity

and

allo

w f

or e

xpan

sion

as

the

nee

d ar

ises

. T

he s

ite w

ill a

ccom

mod

ate

outs

ide

supp

ort

spac

e an

d e

qui

pmen

t. O

ther

item

s in

clu

ded

in t

he

proj

ect

are

ext

ensi

on o

f an

y an

d a

ll ut

ilitie

s to

th

e si

te,

cle

aran

ce/d

emol

ition

of

an

y e

xist

ing

stru

ctur

es,

park

ing

and

acce

ss r

oads

, sp

ecia

lized

sec

urity

sys

tem

s, a

nd u

nint

erru

pted

po

wer

sys

tem

s (U

PS

) fo

r ba

ckup

po

we

r se

rvic

e in

the

eve

nt o

f ut

ility

po

we

r ou

tage

.

2012

-13

To

tal

Co

nst

ruct

ion

Pro

ject

s $1

59,

000,

000

(Appendix I.3) -2-

9/9/2011 F&PP

TH

E P

EN

NS

YL

VA

NIA

ST

AT

E U

NIV

ER

SIT

Y

PR

OP

OS

ED

CA

PIT

AL

BU

DG

ET

RE

QU

ES

T F

OR

201

2-13

Pri

ori

ty

Am

ou

nt

Nu

mb

er

2012

-201

3 O

rig

inal

Eq

uip

men

t

Req

ues

ted

1.C

apita

l Re

new

al, P

hase

V (

Uni

vers

ity P

ark)

$

6,00

0,0

00

2.C

apita

l Ren

ew

al, P

hase

IV (

Eas

tern

Re

gion

Cam

puse

s)

$ 4,

200,

000

3.C

apita

l Re

new

al, P

hase

IV (

Cen

tral

Reg

ion

Cam

pus

es)

$ 4,

200,

000

4.C

apita

l Ren

ew

al, P

hase

IV (

Wes

tern

Reg

ion

Cam

puse

s)

$ 4,

200,

000

5.D

isas

ter

Rec

over

y/B

usin

ess

Con

tinui

ty D

ata

Cen

ter

(loca

tion

to b

e de

term

ined

)

$

10,0

00,0

00

20

12-1

3 T

ota

l O

rig

inal

Eq

uip

men

t $

2

8,60

0,00

0

20

12-

13 T

OT

AL

RE

QU

ES

TE

D

$ 18

7,6

00,0

00

(Appendix I.3) -3-

9/9/2011 F&PP

Gift

sD

olla

rsG

ifts

Dol

lars

Gift

sD

olla

rsG

ifts

Dol

lars

AL

UM

NI

129,

705

131,

421,

878

128,

378

65,2

58,5

801,

327

66,1

63,2

9812

8,37

865

,258

,580

FR

IEN

DS

159,

053

39,1

15,4

5915

3,32

336

,533

,747

5,73

02,

581,

712

153,

323

36,5

33,7

47

CO

RP

OR

AT

ION

S13

,943

53,1

08,8

1613

,346

53,5

39,1

6059

7(4

30,3

44)

13,3

4653

,539

,160

FO

UN

DA

TIO

NS

1,90

230

,474

,260

1,34

331

,800

,701

559

(1,3

26,4

41)

1,34

331

,800

,701

OR

GA

NIZ

AT

ION

S3,

421

20,7

11,6

283,

220

16,5

18,6

1020

14,

193,

018

3,22

016

,518

,610

TO

TA

LS

308,

024

$274

,832

,041

299,

610

$203

,650

,798

8,41

4$7

1,18

1,24

329

9,61

0$2

03,6

50,7

98

(7/0

1/09

- 6

/30/

10)

Yea

r-T

o-D

ate

Yea

r-T

o-D

ate

Yea

r-T

o-D

ate

(As

of 6

/30/

11)

(As

of 6

/30/

10)

(Fro

m 2

010

- 20

11)

TH

RO

UG

H J

UN

E 2

011

Thi

s Y

ear

Last

Yea

rC

hang

eLa

st F

isca

l Yea

r G

rand

Tot

als

TH

E P

EN

NS

YL

VA

NIA

ST

AT

E U

NIV

ER

SIT

Y

OF

FIC

E O

F U

NIV

ER

SIT

Y D

EV

EL

OP

ME

NT

YE

AR

TO

DA

TE

RE

PO

RT

- A

LL

SO

UR

CE

S

TY

PE

DO

NO

R R

EP

OR

T (

GIF

TS

)

Gift

sD

olla

rsG

ifts

Dol

lars

Gift

sD

olla

rsG

ifts

Dol

lars

UN

RE

ST

RIC

TE

D8,

492

1,03

8,85

38,

354

1,44

6,75

713

8(4

07,9

04)

8,35

41,

446,

757

AC

AD

EM

IC D

IVIS

ION

S18

,324

5,20

6,15

619

,398

5,36

0,18

0(1

,074

)(1

54,0

24)

19,3

985,

360,

180

FA

CU

LT

Y R

ES

OU

RC

ES

545

26,6

66,7

9765

411

,827

,681

(109

)14

,839

,116

654

11,8

27,6

81R

ES

EA

RC

H4,

071

34,9

60,6

824,

070

43,9

42,0

861

(8,9

81,4

04)

4,07

043

,942

,086

PU

BL

IC S

VC

& E

XT

22,9

954,

669,

058

23,4

564,

187,

259

(461

)48

1,79

923

,456

4,18

7,25

9L

IBR

AR

Y1,

718

290,

800

1,99

238

6,31

3(2

74)

(95,

513)

1,99

238

6,31

3P

HY

S. P

LA

NT

MA

INT

.17

730

,908

200

13,0

16(2

3)17

,892

200

13,0

16S

TU

DE

NT

AID

51,1

6160

,422

,491

46,9

4139

,897

,817

4,22

020

,524

,674

46,9

4139

,897

,817

S

CH

OLA

RS

HIP

S15

,595

33,9

69,1

7113

,944

23,2

92,0

231,

651

10,6

77,1

4813

,944

23,2

92,0

23

ST

UD

EN

T L

OA

NS

176

1,05

0,55

837

4,20

013

91,

046,

358

374,

200

G

RA

DU

AT

E F

ELL

OW

SH

IPS

778

4,05

8,76

573

31,

528,

081

452,

530,

684

733

1,52

8,08

1

AT

HLE

TIC

GR

T-I

N-A

ID34

,612

21,3

43,9

9732

,227

15,0

73,5

132,

385

6,27

0,48

432

,227

15,0

73,5

13P

RO

P/B

LD

GS

/EQ

UIP

8,71

376

,384

,690

8,90

247

,135

,072

(189

)29

,249

,618

8,90

247

,135

,072

OT

HE

R P

UR

PO

SE

S19

1,82

865

,161

,606

185,

643

49,4

54,6

176,

185

15,7

06,9

8918

5,64

349

,454

,617

TO

TA

LS

308,

024

$274

,832

,041

299,

610

$203

,650

,798

8,41

4$7

1,18

1,24

329

9,61

0$2

03,6

50,7

98

(7/0

1/09

- 6

/30/

10)

Yea

r-T

o-D

ate

Yea

r-T

o-D

ate

Yea

r-T

o-D

ate

(As

of 6

/30/

11)

(As

of 6

/30/

10)

(Fro

m 2

010

- 20

11)

TH

RO

UG

H J

UN

E 2

011

Thi

s Y

ear

Last

Yea

rC

hang

eLa

st F

isca

l Yea

r G

rand

Tot

als

YE

AR

TO

DA

TE

RE

PO

RT

- A

LL

SO

UR

CE

SP

UR

PO

SE

OF

GIF

T

Gift

sD

olla

rsG

ifts

Dol

lars

Gift

sD

olla

rsG

ifts

Dol

lars

AB

ING

TO

N1,

354

400,

644

1,21

260

6,45

814

2(2

05,8

14)

1,21

260

6,45

8A

GR

ICU

LT

UR

AL

SC

IEN

CE

S4,

907

7,91

9,73

85,

054

10,0

01,7

94(1

47)

(2,0

82,0

56)

5,05

410

,001

,794

AL

TO

ON

A2,

343

1,69

7,80

32,

045

2,26

4,22

329

8(5

66,4

20)

2,04

52,

264,

223

AR

TS

& A

RC

HIT

EC

TU

RE

7,11

117

,704

,577

6,91

67,

963,

645

195

9,74

0,93

26,

916

7,96

3,64

5B

EA

VE

R98

243

7,48

691

852

5,99

064

(88,

504)

918

525,

990

BE

HR

EN

D3,

682

6,62

7,32

93,

637

4,86

1,25

845

1,76

6,07

13,

637

4,86

1,25

8B

ER

KS

1,69

339

1,38

386

130

7,29

583

284

,088

861

307,

295

BR

AN

DY

WIN

E69

721

9,96

968

62,

866,

895

11(2

,646

,926

)68

62,

866,

895

CO

MM

UN

ICA

TIO

NS

1,62

41,

841,

389

1,60

71,

931,

400

17(9

0,01

1)1,

607

1,93

1,40

0D

ICK

INS

ON

SC

HO

OL

OF

LA

W89

080

8,83

498

97,

372,

746

(99)

(6,5

63,9

12)

989

7,37

2,74

6D

UB

OIS

1,00

132

4,98

01,

157

319,

894

(156

)5,

086

1,15

731

9,89

4E

AR

TH

& M

INE

RA

L S

CIE

NC

ES

3,77

413

,604

,867

4,05

813

,961

,403

(284

)(3

56,5

36)

4,05

813

,961

,403

TH

E E

BE

RL

Y C

OL

LE

GE

OF

SC

IEN

CE

5,50

65,

836,

682

5,70

54,

653,

661

(199

)1,

183,

021

5,70

54,

653,

661

ED

UC

AT

ION

4,84

03,

034,

634

4,94

81,

349,

337

(108

)1,

685,

297

4,94

81,

349,

337

ED

UC

AT

ION

AL

EQ

UIT

Y60

447

8,99

041

164

2,29

119

3(1

63,3

01)

411

642,

291

EN

GIN

EE

RIN

G10

,659

18,8

20,7

6811

,246

22,6

73,2

02(5

87)

(3,8

52,4

34)

11,2

4622

,673

,202

FA

YE

TT

E, T

HE

EB

ER

LY

CA

MP

US

546

433,

174

577

864,

930

(31)

(431

,756

)57

786

4,93

0G

RE

AT

VA

LL

EY

511

87,0

6559

625

9,76

2(8

5)(1

72,6

97)

596

259,

762

GR

EA

TE

R A

LL

EG

HE

NY

1,21

840

7,95

279

241

2,99

642

6(5

,044

)79

241

2,99

6H

AR

RIS

BU

RG

3,37

189

0,27

13,

135

1,79

0,03

523

6(8

99,7

64)

3,13

51,

790,

035

HA

ZL

ET

ON

859

433,

564

816

716,

659

43(2

83,0

95)

816

716,

659

HE

AL

TH

& H

UM

AN

DE

VE

LO

PM

EN

T5,

898

10,5

40,3

636,

013

6,31

8,73

2(1

15)

4,22

1,63

16,

013

6,31

8,73

2H

ER

SH

EY

124,

037

35,2

56,8

4312

1,79

533

,551

,278

2,24

21,

705,

565

121,

795

33,5

51,2

78IN

FO

RM

AT

ION

SC

IEN

CE

S &

TE

CH

NO

LO

GY

507

2,25

4,01

947

11,

237,

756

361,

016,

263

471

1,23

7,75

6IN

TE

RC

OL

LE

GIA

TE

AT

HL

ET

ICS

40,2

8383

,000

,518

36,8

4829

,875

,868

3,43

553

,124

,650

36,8

4829

,875

,868

LE

HIG

H V

AL

LE

Y62

011

7,65

449

711

9,11

112

3(1

,457

)49

711

9,11

1L

IBE

RA

L A

RT

S5,

989

19,5

25,0

206,

324

10,9

84,0

55(3

35)

8,54

0,96

56,

324

10,9

84,0

55M

ON

T A

LT

O1,

339

733,

466

1,51

861

3,12

2(1

79)

120,

344

1,51

861

3,12

2N

EW

KE

NS

ING

TO

N74

837

6,49

374

766

1,66

61

(285

,173

)74

766

1,66

6O

UT

RE

AC

H25

,078

6,55

1,95

125

,638

5,67

8,09

2(5

60)

873,

859

25,6

385,

678,

092

RE

SE

AR

CH

& G

RA

DU

AT

E S

CH

OO

L36

71,

026,

037

432

3,59

1,94

9(6

5)(2

,565

,912

)43

23,

591,

949

SC

HR

EY

ER

HO

NO

RS

CO

LL

EG

E

1,74

24,

948,

194

1,52

02,

421,

245

222

2,52

6,94

91,

520

2,42

1,24

5S

CH

UY

LK

ILL

985

592,

515

956

312,

835

2927

9,68

095

631

2,83

5S

HE

NA

NG

O

666

250,

453

709

357,

700

(43)

(107

,247

)70

935

7,70

0T

HE

SM

EA

L C

OL

LE

GE

OF

BU

SIN

ES

S8,

667

7,58

2,03

68,

768

7,01

3,60

3(1

01)

568,

433

8,76

87,

013,

603

ST

UD

EN

T A

FF

AIR

S9,

084

1,00

2,79

03,

396

732,

474

5,68

827

0,31

63,

396

732,

474

UN

DE

RG

RA

DU

AT

E E

DU

CA

TIO

N2,

638

5,44

4,28

22,

223

3,38

9,89

141

52,

054,

391

2,22

33,

389,

891

UN

IVE

RS

ITY

LIB

RA

RIE

S4,

545

2,09

0,60

14,

933

2,11

6,66

2(3

88)

(26,

061)

4,93

32,

116,

662

UN

IVE

RS

ITY

WID

E13

,396

9,08

3,58

916

,288

5,64

3,91

9(2

,892

)3,

439,

670

16,2

885,

643,

919

WIL

KE

S-B

AR

RE

1,

102

381,

783

1,11

91,

289,

800

(17)

(908

,017

)1,

119

1,28

9,80

0W

OR

TH

ING

TO

N S

CR

AN

TO

N96

698

5,56

089

494

7,52

172

38,0

3989

494

7,52

1Y

OR

K1,

195

685,

775

1,15

544

7,64

540

238,

130

1,15

544

7,64

5

TO

TA

L30

8,02

4$2

74,8

32,0

4129

9,61

0$2

03,6

50,7

988,

414

$71,

181,

243

299,

610

$203

,650

,798

(As

of 6

/30/

11)

(As

of 6

/30/

10)

(Fro

m 2

010

- 20

11)

(7/0

1/09

- 6

/30/

10)

Thi

s Y

ear-

To-

Dat

eLa

st Y

ear-

To-

Dat

eC

hang

e in

YT

D T

otal

sLa

st F

isca

l Yea

r G

rand

Tot

als

Endowment & Similar Funds Investment Review for Fiscal 2011 Submitted September 2011

This cover page provides a summary overview of the Pennsylvania State University Endowment and Similar Funds for Fiscal Year 2011. The second page summarizes Endowment-related data that is discussed on the remaining pages, along with in depth Endowment performance analysis.

Executive Overview Endowment Performance

Annualized net investment returns for the Penn State University Endowment (adjusted for the impact of gifts and spending, and after external investment management expenses) are shown below for periods ending June 30, 2011:

Fiscal 11 3 Years 5 Years 10 Years

23.2% 3.9% 5.9% 6.5%

Endowment & Similar Funds Market Value (pg 3)

Penn State University’s Endowment was valued at $1,708 million as of June 30, 2011, with an additional $123 million in Similar Funds. Review of Investment Markets (pg 4)

The graph below compares respective returns for 12-months ending June 30, 2010 and 2011 for the S&P 500, MSCI All Country World (ACW) ex-US, 91-day US Treasury Bills, Barclays Aggregate Bond, and publicly-traded Real Estate Investment Trusts (REITs) Indexes. As shown below, both US and non-US public equity returns for fiscal 2011 outpaced their 2010 performances, while domestic real estate (REITs) again outperformed other asset classes. For both years, bonds were positive while T-Bill returns were again negligible.

Investment Diversification and Asset Mix (pg 5)

At fiscal year-end, 59% of Endowment assets were invested in public equities (domestic and foreign), 17% in fixed income/cash, and 24% in private capital partnerships (venture capital, private buyouts, real estate, and natural resources).

Comparative Fund Performance (pg 6)

Penn State’s Endowment returned 23.2% net for the year ending June 30, 2011 versus 22.5% for the Passive Policy Portfolio, largely due to strong public equity manager performance relative to passive benchmarks. The Endowment’s 3- and 5-yr relative performance was slightly better than respective passive benchmarks.

Endowment Liquidity (pg 7)

With approximately one-half of its assets convertible to cash in a matter of days, the Endowment maintains adequate liquidity to satisfy anticipated cash requirements.

Endowment Performance and Spending (pg 8)

The Penn State Endowment’s average annual net returns of 6.5% and 8.8% over the last 10 and 20 years, respectively, have allowed the Endowment to maintain inflation-adjusted spending while achieving long-term intergenerational equity.

14.4 10.9

0.29.5

53.9

30.7 30.3

0.2 3.9

34.1

S&P World Ex US Tbills Bonds REITs

2010

2011

Investment Market Returns Fiscal Years Ending June 30

9/9/2011 F&PP

(Appendix III) - 1 -

5-Year Endowment Facts and Figures

Penn State Investment Council (PSIC) Meetings

August 13, 2010:

Committing $15 million to Wellspring Capital Partners V, L.P. October 29, 2010:

Maintain Penn State’s Endowment spending at a 4.5% annual rate. Committing $10 million to Yorktown Energy IX, L.P. Committing $15 million to EnCap Energy VIII, L.P.

December 12, 2010:

Committing $15 million to Oaktree Real Estate Opportunities Fund V, L.P. March 17, 2011:

Committing $4M to IDG Accel China Growth Fund III, L.P. Committing $6M to IDG Accel China Capital Fund II, L.P.

June 24, 2011:

Committing $3M to Accel Growth Fund II, L.P. Committing $2M to Accel XI, L.P Committing $10M to Emergence Capital Partners III, L.P. Committing $10M to GSR Ventures IV, L.P.

Please note that commitments made to Limited Partnerships (LPs) are not immediately invested and are called (paid in) over several years until commitment is satisfied, except as noted.

----———-—— Annual Periods Ending June 30 —————---- 2011 2010 2009 2008 2007 Investment Performance Endowment1 23.2% 14.3% -20.1% -1.9% 21.2% (annualized net returns) Market Values ($ millions) Endowment1 1,708.4 1,341.5 1,183.9 1,487.9 1,538.7 Similar Funds2 122.7 97.6 97.4 127.7 131.5 Endowment and Similar Funds 1,831.1 1,439.1 1,281.3 1,615.6 1,670.2 Gifts & Other Additions ($ mils) 136.3 62.5 61.2 47.8 55.2 Current Spending ($ mils) 66.0 63.4 65.1 60.4 58.3 1) Endowment assets over which Penn State’s Office of Investment Management (OIM) has investment responsibility, as approved by the Penn State Investment Council (PSIC).

2) Similar Funds — includes donor-restricted and deferred gifts, plus funds in transit to Endowment.

9/9/2011 F&PP

(Appendix III) - 2 -

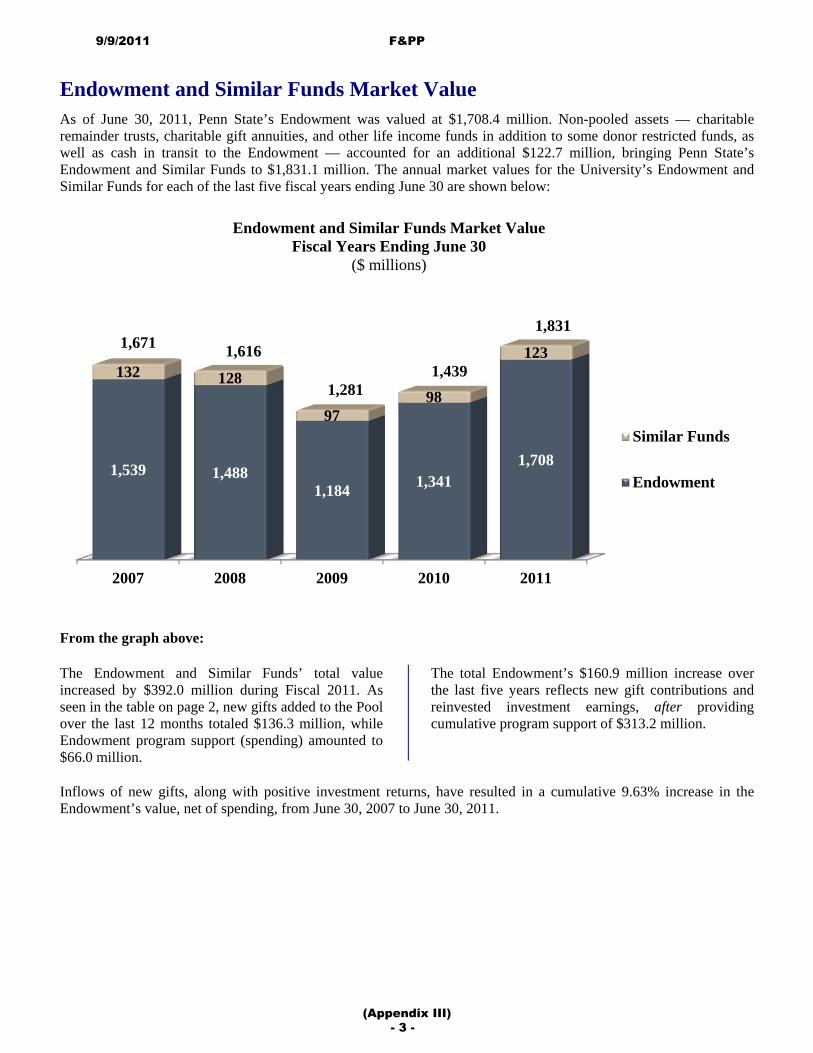

Endowment and Similar Funds Market ValueAs of June 30, 2011, Penn State’s Endowment was valued at $1,708.4 million. Non-pooled assets — charitable remainder trusts, charitable gift annuities, and other life income funds in addition to some donor restricted funds, as well as cash in transit to the Endowment — accounted for an additional $122.7 million, bringing Penn State’s Endowment and Similar Funds to $1,831.1 million. The annual market values for the University’s Endowment and Similar Funds for each of the last five fiscal years ending June 30 are shown below:

From the graph above:

The Endowment and Similar Funds’ total value increased by $392.0 million during Fiscal 2011. As seen in the table on page 2, new gifts added to the Pool over the last 12 months totaled $136.3 million, while Endowment program support (spending) amounted to $66.0 million.

The total Endowment’s $160.9 million increase over the last five years reflects new gift contributions and reinvested investment earnings, after providing cumulative program support of $313.2 million.

Inflows of new gifts, along with positive investment returns, have resulted in a cumulative 9.63% increase in the Endowment’s value, net of spending, from June 30, 2007 to June 30, 2011.

2007 2008 2009 2010 2011

1,539 1,4881,184 1,341

1,708

132 128

9798

123

Similar Funds

Endowment

1,671 1,616

1,281 1,439

Endowment and Similar Funds Market Value Fiscal Years Ending June 30

($ millions)

1,831

9/9/2011 F&PP

(Appendix III) - 3 -

Review of Investment Markets in Fiscal 2011 Following a year of strong double-digit gains, equities in Fiscal 2011 again handily outperformed fixed income returns, while non-US indexes generally lagged domestic equity markets. The performance of investment markets that directly impact Penn State University’s Endowment is discussed below. US Equities

The S&P 500 returned 30.7% for the 12 months ending June 30, 2011, compared to 14.4% for Fiscal 2010, while the large-cap biased Dow Jones Industrial Index returned 30.4% and 18.9%, respectively. Small-capitalization stocks, as measured by the Russell 2000 Index, returned 37.4% versus 21.5% last year. The Nasdaq Index’s 31.5% return was comparable to the broad domestic indexes in fiscal 2011, and exceeded its 2010 return of 14.9%. Non-US Equities

Equities outside the United States generally matched those in the US as the Morgan Stanley All Country World (ACW) Index ex-US returned 30.3% for the 12-month period ending June 30, 2011. This was well above its Fiscal 2010 return of 10.9%. Emerging market equities in developing countries returned 28.2% over the last 12 months, somewhat above their 23.5% return in Fiscal 2010. Fixed Income

Barclays Capital Aggregate Bond Index (various maturities of US Government and non-government domestic bonds) returned 3.9% in Fiscal 2011 versus 9.5% in 2010. US Treasury Bonds returned -1.1% in Fiscal 2011 versus 12.0% a year earlier.

For Fiscal 2011, 91-day Treasury Bills again earned 0.2% and Treasury Inflation Protected Securities (TIPS) returned 7.7% in Fiscal 2011 compared to 9.5% in Fiscal 2010. Real Estate

Publicly-traded Real Estate Investment Trusts (REITs) returned 34.1% for the Fiscal year ended June 2011 compared to 53.9% in 2010. Privately-held real estate investment partnerships, as measured by the largely commercial property NCREIF Index, rebounded to earn 16.0% in Fiscal 2011 compared to -9.6% in 2010. Alternatives

Private Equity Buyouts and Venture Capital increased as well, averaging returns of 21.3% and 18.4%, respectively, for the 12 months ending March 31, 2011 (private capital partnerships are reported on a 3-month lag). In the previous 12-month period ending March 31, 2010, Private Equity returned 22.5%, while Venture Capital was at 6.4%. By comparison, the Russell 2000 Index of small-capitalization stocks returned 25.8% for the 12 months ending March 31, 2011 and 62.8% for the year ending March 31, 2010.

Economic and Market Outlook

In the 12 months ending June 30, 2011, global equity markets continued the rally that began in March of 2008. However, unlike 2009, US equities lead the world indexes. Fixed income markets provided a fourth consecutive year of positive returns, as the Federal Reserve continued to hold down interest rates to alleviate credit market distress brought on by the decline in housing prices and the accompanying deleveraging. Looking ahead, expectations for domestic corporate profits have brightened in the face of improving credit concerns and a recovering economy.

Penn State’s well-diversified endowment portfolio — consisting of public equities, private partnerships, bonds, and hedge funds in addition to inflation-sensitive “real assets” — continues to be the most appropriate investment approach for long-term growth and sustainable spending.

9/9/2011 F&PP

(Appendix III) - 4 -

Investment Diversification and Asset Mix

Asset allocation is a primary determinant of investment performance and risk control. The Endowment’s asset mix combines three very broad asset categories - public equities, private capital, and fixed income - to maximize potential returns, while tempering volatility. Reflecting a desire to support generous spending and the need to preserve purchasing power in light of changing market and economic conditions, the Penn State Investment Council (PSIC) regularly reviews the Endowment’s investment policy.

In the graph below, the three macro categories – public equities, fixed income, and private capital – are shown in the outermost ring with their June 30, 2011 allocations of 59%, 17%, and 24%, respectively.

At a more granular level, the Endowment’s diversified portfolio includes a variety of asset classes that comprise the three macro categories, as shown by the slices within the inner pie (percentages are rounded):

59% in Public Equities includes publicly-traded US (37%) and non-US (14%) common stocks, and equity-oriented hedge funds (8%).

17% in Fixed Income includes 13% in nominal bonds (largely US government bonds), 3% in Global Treasury Inflation Protected Securities (Global TIPS), and 1% in an absolute-return hedge fund.

24% in Private Capital includes the following private partnerships: 14% private equity (venture capital, leveraged buy-outs, distressed-debt), and 10% in real assets (private and public real estate, and energy).