a 2014 injection molding industry report - marketresearch · pdf file2014 injection molding...

TRANSCRIPT

• Increased demands by OEM customers, a lack oftechnicalpersonnelandreshoringfromAsiaarekeytrendsimpactingtheinjectionmoldingindustry.

• On average, the injection molding sector hasexpanded in the range of 4-5 percent per yearsince hitting bottom during the recession – withexpectations this growth will hold steady for theforseeablefuture.

• Theautomotive,electronics,applianceandtechnicalmolding markets dominate northern Mexico asmultinationalOEMshavesetupproduction.

• Reshoring may be exposing a coming toolingshortageattimewhennewcarsrequiremoremoldsand dies –which could prove to have a significantfinancial impact on injection molders serving theautomotiveindustry.

• Sales of injection molding equipment have beenon the rebound since the end of 2008-2009 – abenchmarkfortheeconomichealthanddirectionoftheindustry.

2014 InjectIon MoldIng Industry report

FInAncIAl outlook & key trendsIMpActIng the north AMerIcAn MArket

INSIDE THIS REPORT

sample

Visit www.plasticsnews.com/data for

additional details.

Entirecontentscopyright2014CrainCommunicationsInc.Allrightsreserved.Thismaterialmaynotbepublished,broadcast,rewrittenorredistributedwithoutthepermissionofPlastics News’ ResearchDivision.

Other PN Market Reports

Flexible Packaging Market OutlookReleased: December 2013

Plastics in Building & ConstructionReleased: January 2014

Mold Making & Tooling Market Outlook

Released: January 2014

statistical data contained in this report is compiled by primary and secondary research and in-house analysis by Plastics News’ team of experts.

to view our complete library of market reports and data products, please visit: www.plasticsnews.com/data

Look for our June report:Shale Gas Market Trends & Analysis

Table of Contents

InjectionMoldingMarketOverview.................................3EconomicForecast.................................................................. 16FinancialIssues&Trends...................................................... 20SuccessionPlanning............................................................... 24MachineryOperations&SalesTrends........................... 27Automation&TechnologicalAdvances....................... 32Lights-OutProduction.......................................................... 39TechnologyOverview............................................................ 41Labor,Skills&TrainingTrends............................................ 45

Tables

ForecastedGDPGrowth2014-2017..................................5LDPEQuarterlyVolumeAverage..................................... 13PolycarbonateQuarterlyVolumeAverage.................. 13PolypropyleneQuarterlyVolumeAverage................. 14HDPEQuarterlyVolumeAverage.................................... 15PVCQuarterlyVolumeAverage........................................ 15LLDPEQuarterlyVolumeAverage................................... 16

PolystyreneQuarterlyVolumeAverage........................ 16PerformanceofKeyEndMarkets............................. 18-19M&ATrends................................................................................ 22TransactionswithFinancialBuyers................................ 26TransactionswithStrategicBuyers................................. 26Employment,Rubber&Plastics2004-2014............... 46Unemployment,Rubber&Plastics2004-2014......... 47YoungestPopulationbyHighestGrade....................... 50

Executive Spotlight

WilliamCarteaux,President&CEO,SocietyofthePlasticsIndustry;PhilKaten,President,PlastikosInc.andMicroMoldCo.Inc.;JohnW.Saxon,

President&CEO,DLHIndustriesInc.;RonRicotta,President&CEO,CenturyMoldCo.Inc.;DaleEvans,President,EvcoPlastics-Pages53-61

Injection Molder Profiles

CompanyProfiles............................................................62-132

Plastics NewsResearchDivision,Copyright©2014CrainCommunicationsInc. 2

crain communications inc.1155 Gratiot ave.detroit, mi 48207-2732United statesPhone: +1-313-446-6000Fax: +1-313-567-7681Web: www.crain.com

publisherBrennan [email protected]

editor donald [email protected]

director, digital strategy & marketing pam [email protected]

director, research & data productsKelley [email protected]

research analystdavid [email protected]

contributorsBill [email protected]

Bill [email protected]

research coordinatorHollee [email protected]

production assistantamelia mcKean

Thisreportprovidesin-depthanalysisofcur-renttrendsandtheirfinancial impactontheinjectionmoldingindustryinNorthAmerica.

Relying on primary and secondary research,thereportalsoexaminestheimpactofauto-mation,machinery,technologyandtheskillsgaponinjectionmolders’financialstatus.

Economist Bill Wood provides an economicforecast that examines current trends in keyendmarkets.

Wereview77leadingcompaniesintheinjec-tionmolding industry, interviewingmanyoftheir executives and assessing their growthinitiatives and performance metrics over 10years, including sales revenues, throughput,plantsandpresses,employmentandmateri-alsprocessed.

In addition, exclusive interviews with fiveindustry thought leaders offer competitiveinsightonkeytrendsandissuesimpactingin-jectionmolderstoday.

Inside this report:

PlasticsNewsResearchDivision,Copyright©2014CrainCommunicationsInc. 3

2014 Injection Molding Industry Report

InjectIon MoldIng MArket overvIew

PlasticsNewsResearchDivision,Copyright©2014CrainCommunicationsInc. 4

2014 Injection Molding Industry Report

growth, opportunity in sight for injection molders in 2014Everything frommaterials andmachin-erytolaborandnewtechnologyhasanimpacton thefinancialoutlookof theinjectionmoldingindustry.

North American injectionmolders havehad to tighten their belts and becomemore competitive toweather the reces-sion of 2008-2009. Today, molders aregaining a competitive advantage by in-vesting inpeople, equipmentand seek-inginroadsintonewmarketsonaglobalscale.

Inthewakeoftheeconomicturbulenceearlierinthisdecade,molderstodayfindthemselves in much better shape. Tosurvive, they lowered their costs struc-turesduringtherecessionandhavemain-

tained their labor costs since the down-turn. Profit margins thus expanded and

lowerinterestrateshaveallowedfirmstolightentheirdebtsandgeneratecash.

As the third largest manufacturingindustryintheUnitedStates,theplastics

industry has an undeniable impact ontheeconomy,accordingtoSocietyofthe

“Six percent growth has barelymovedutilization.Companiesareinvesting andbuying equipmentbut not hiringmore employees.”- Bill Wood, economist

This rePorT iNcludes Q&A iNTervieWs WiTh iNdusTry ThoughT leAders ...

Plastics News Research Division, Copyright © 2014 Crain Communications Inc. 1

Injection Molding Industry Report – April 2014

Executive Spotlight | William CarteauxPresident & CEO, Society of the Plastics Industry

SPI President and CEO William Carteaux began his tenure at the association in February 2005. He came to SPI from Demag Plastics Group, where he was named president and chief executive of-ficer of the Americas and co-executive managing director of the global busi-ness in 2002. Carteaux previously served as the company’s executive vice presi-dent. Prior to joining Demag, Carteaux spent eight years with Autojectors, a manufacturer of vertical injection mold-ing machines, including four years as its president. He had been actively involved as an SPI member, taking on numerous leadership roles for more than 15 years. While a member, Carteaux served as chair of SPI’s Equipment Council, the NPE Finance Committee and the NPE Operations Committee. He was vice-chairman elect of SPI when he assumed his current position. Carteaux has an MBA from Indiana Wesleyan University and a BS from Purdue, where he has re-ceived several awards since graduating. He currently serves on the Board of Di-rectors for the Council of Manufacturing Associations at the National Association of Manufacturers and is Director Gener-al of CIPAD, the Council of International Plastics Association Directors.

Q: SPI recently issued its most recent statistics on industry growth. What are some of the trends you see in these numbers and does it indicate that the U.S. plastics industry has just about re-covered from the Great Recession?

A: I would say that some sectors have cer-tainly recovered from the recession and other sectors are getting better. The auto-motive sector has done well in the last cou-ple of years and is poised to continue to do well in this country with the forecast of the new builds and also the number of new product launches and new model change-overs the OEMs are coming out with.

The packaging industry saw the normal recessionary drop-off in some areas with consumers not spending as much, but it definitely is back. Medical is doing well

and the housewares market is doing well with housing starts, but it isn’t at pre-re-cession levels yet.

From my perspective, when you look at some of those numbers, the consumption overall in the U.S. and per capita contin-ues to go up, and if you dig into the num-bers you can see that. We are right at pre-recession levels overall. When we come out with the 2013 numbers, we believe that will happen.

We are seeing the benefit of reshoring. There aren’t great numbers yet, but there certainly are pockets that we are seeing taking advantage of the increased costs internationally of transportation. That is a trend we expect to see to continue.

Q: Other than for resin, trade num-bers for the U.S. plastics industry are running at a deficit for machinery and finished products. What can SPI do to help promote the U.S. plastics industry globally?

A: One of the big things that we have been doing and continue to do is that when we have new free trade agreements, we fo-cus a lot of effort on trying to help com-panies move into those markets. Of all of the free trade markets the United States has, and that number is at 19 now, or 20, there is only one country that the plastics industry overall doesn’t have a positive trade surplus with and it is based on resin coming in from Oman.

We led several trade missions last year to countries that we have trade agreements with or developing countries. We have a couple more scheduled this year.

Through our International Trade division, we supply a lot of information to com-panies to help them understand and get into these markets. We are trying to edu-cate people that people around the world want U.S. products. As much as the rest of the world wants that, there are a lot of people who thought the U.S. was a large enough market and have since found out that it is not the case.

If you look at our processor base in the United States, many more of them are ex-porting than ever before. Our large trade deficit, especially on the product side, comes from China. We have revered that and stopped the bleeding, though we are not where we need to be. China is our third-largest market.

On the machinery side, we just don’t have the producers that we used to have. The trend really started in the late 1980s and accelerated in the 1990s. I don’t think we are ever going to see a large swing to the positive side, simply because we don’t have the number of producers we used to have.

On the mold making side, I think we are going to see our deficit on molds contin-ue to decrease. We have the opportunity to turn that into a net export market for us. In certain segments of the processing side we have that same capability.

Q: While reshoring is a real trend, the numbers suggest that the Chinese plastics industry is still growing faster than the North American plastics in-dustry. What can the industry continue to do to move more of that business back to North America?

A: I think one of the things that people need to do is look at true total cost. That may be an overused term with all of the

PlasticsNewsResearchDivision,Copyright©2014CrainCommunicationsInc. 5

2014 Injection Molding Industry Report

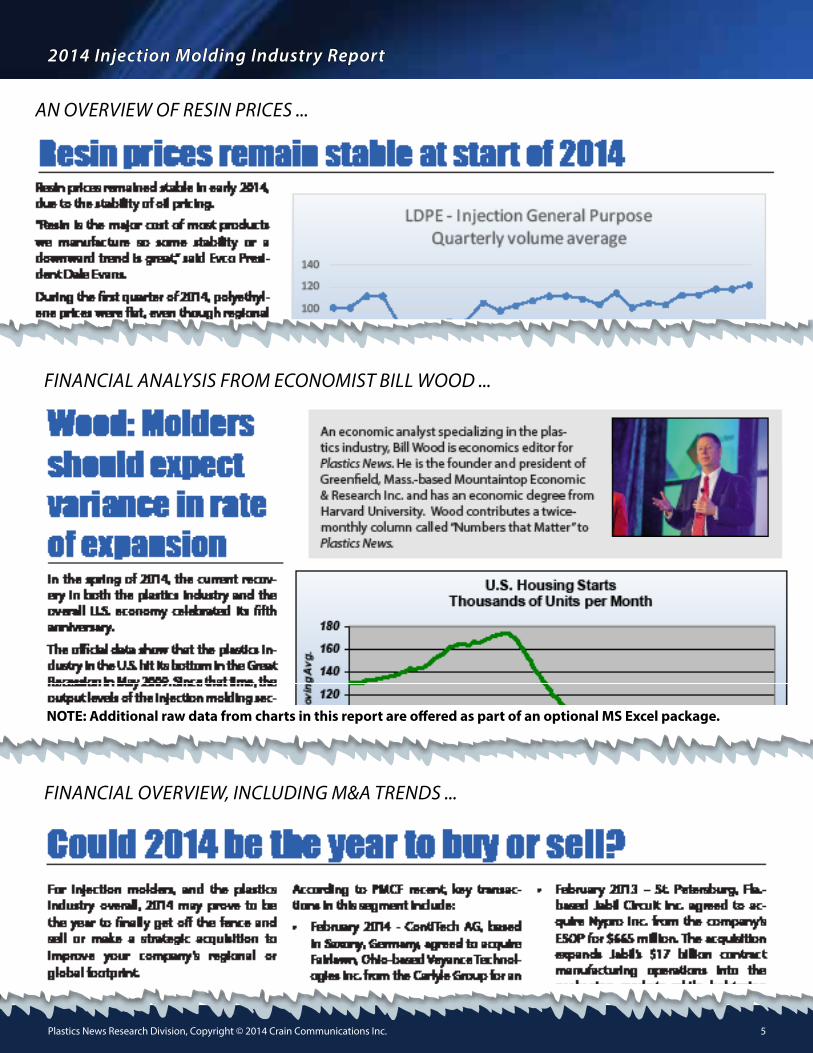

AN overvieW oF resiN Prices ...

FiNANciAl ANAlysis From ecoNomisT Bill Wood ...

FiNANciAl overvieW, iNcludiNg m&A TreNds ...

note: additional raw data from charts in this report are offered as part of an optional ms excel package.

PlasticsNewsResearchDivision,Copyright©2014CrainCommunicationsInc. 6

2014 Injection Molding Industry Report

AuTomATioN ANd roBoTics TreNds ...

Plastics News Research Division, Copyright © 2014 Crain Communications Inc. 1

2014 Injection Molding Industry Report

The injection molding industry is highly networked and specialized, with plastic production, plastic processing and me-chanical engineering all closely interlinked.

Plastics are used in virtually every sec-tor: from the automotive and electronics industries to the consumer goods and food industries. Mechanical engineer-ing plays an important role here as the link between the production and the processing of plastics. Injection mold-ing machines and tools process the raw material to form innovative, precise and robust end products or intermedi-ate products for further processing — production steps that can be carried out more efficiently, cost-effectively and reliably with automation solutions.

Robots and automation is having a sig-

nificant impact on injection molding by increasing production levels and decreasing production costs.

ROBOT SALES NEAR RECORDAccording to Arturo Baroncelli, president of the International Federation of Robot-ics, 2013 was a record-setting year in robot sales, reaching 168,000 units.

The main driver of the new record is the impressive demand in the Asian market, which confirms the growth achieved during recent years as well as the

expected projections.

“The never-ending improvements in performance, quality and competitive-ness of robots have generated a thrust at the basis of such success,” Baroncelli said.

Baroncelli added that demand for in-dustrial robots is increasing due to the accelerating trend towards automation all over the world.

Robot sales to the Americas continued to increase due to necessary automation processes in the North American industry. Robot sales to Asia rose considerably due to strong demand from China, South Ko-rea and other growing Asian markets. In the fourth quarter of 2013, the start of re-covery in the euro-zone pushed robot de-mand substantially. Due to the rather weak

development in the first three quarters, robot sales in Europe stagnated in 2013.

Between 2010 and 2013 the annual in-crease of global robot sales was about 12 percent on average despite the critical economic situation in some key countries.

“One basic reason for the continuous growth in the use of robotics is its never ending technological development in re-lation with market and industrial require-ments, accounting for product quality and competitiveness as well as safe pro-cesses,” Baroncelli noted.

According to Joe Gemma, IFR vice president, industry leaders are not sur-prised by the growth as many factors have contributed to the increased use of robotics worldwide, some of which has been driven directly from the automa-tion equipment manufacturers.

“The software to work with and run ro-bots and automation cells has developed rapidly over the last few years and the ease of use has transcended into more applications under a very demanding and dynamic manufacturing landscape that would not have been tackled in the past,” he said. “This has enabled manufacturers to provide products to the market quicker and with flexibility of variations to meet consumer demand and at the same time insure the quality required and the per-

formance demanded. Additionally, develop-ment tools have en-abled more R&D varia-tions on traditional product portfolios and has provided the pos-sibility to ‘push the en-velope’ to bring more innovation quicker to the market place. Certainly the volume increases over the last several years has cre-ated a cost benefit that is shared to the auto-mation consumers and is now more attractive to non-traditional mar-

kets.”

Gemma added that these changes and others have contributed to the advance-ment and increase for worldwide demand for automation solutions. He added the future is through embracing automation and sharing the advances it represents.

Yoshikatsu Minami, corporate vice presi-dent and general manager of the robot-ics division for Yaskawa Electric Corp. in Japan, said the automotive industry has made major investments in Asian countries, including China.

Industrial robotics making mark on injection molding

Arturo BaroncelliInjection molding machine with a side-mount option. File photo

Plastics News Research Division, Copyright © 2014 Crain Communications Inc. 1

2014 Injection Molding Industry Report

Labor, skills gap remain issues for molders

EmploymEnt of production and nonsupErvisor EmployEEs rubbEr & plastics 2004-2014

yEarmonth

Jan fEb mar apr may Jun Jul aug sEpt oct nov dEc

2004 622.6 622.7 622.1 623.8 626.1 627.2 628.2 626.7 627.2 627.4 627.7 625.12005 622.3 620.2 624.1 620.8 618.6 616.7 617.2 617.9 621.1 621.5 622.7 621.42006 621.1 622.2 621.9 619.4 616.1 615.2 610.9 607.5 600.4 587.6 587.3 584.92007 598.2 595.7 593.5 595.5 595.9 592.2 591.7 590.5 587.8 589.8 587.4 589.82008 588.4 588.8 588.4 584.0 583.1 580.9 577.8 571.4 565.0 555.0 540.4 528.92009 513.8 505.4 493.7 485.4 475.6 470.0 463.2 460.9 461.3 460.4 463.5 463.62010 466.9 466.5 467.5 469.6 471.7 472.9 475.4 476.1 474.6 474.8 475.4 476.82011 481.3 480.4 481.4 480.0 481.3 481.1 481.7 482.7 484.1 481.9 483.3 483.62012 481.5 483.5 485.0 485.0 485.3 486.9 488.4 489.4 488.0 488.8 490.2 490.32013 491.0 491.8 494.0 495.1 494.6 492.6 493.7 491.1 492.8 494.8 499.3 501.92014 505.0 505.1 504.2

Source: Bureau of Labor Statistics; Sales inthousands(P) Preliminary

The injection molding industry taps an ar-ray of skills in its production and covers a diverse range of products, and with such unique requirements for skilled positions, labor has been a key concern among molders and remains an issue in 2014.

According to economist and plastics spe-cialist Bill Wood, the skills gap presents a real threat to the injection molding sector of the plastics industry.

“From what I have seen, companies more and more often are finding that high-tech and even entry level jobs are tough to fill,” Wood said. “What used to be, say, simply a welding job now demands computer skills, robotics, adaptability and flexibility.”

According to Rick Walters, president of Butler, Ind.-based DeKalb Molded Plas-tics the skilled labor issue is a problem that is everywhere.

“Certainly, it is what everyone is talk-ing about, especially in this industry,” he said. “The higher you go, the bigger the gap you will see. The companies really have to get involved. You look around to see who is providing the training and re-sources and who is addressing this. Quite frankly, we are the people who are going to be addressing this. It is not going to be someone else. The answer is going to have to come from within the industry.”

John W. Saxon, president and CEO of Can-ton, Ohio-based injection molder DLH Industries, agreed that there is a current

shortage of technical talent.

“This has forced businesses like ours to increase recruitment efforts, and increase pay for technical employees,” he said. “This is an adverse situation. Molders can over-come some of this issue through invest-ment in technology, but also through in-vestment in training existing employees.”

Terry Minnick, president of Molding Busi-ness Services, a Florence, Mass.-based plastics industry consulting firm, said he is in the recruiting business as well as the M&A business

“If we run across a good project engi-neer or a good process engineer and he doesn’t want to move, we reach out to the molders out there and ask if they are in-terested in a good engineer,” he said. “Ev-ery one of them are.”

Minnick pointed out that during the tur-bulence of the last decade, many people left the industry.

“The economy is turning around and the industry is growing again,” he said. “As a result, it is difficult to find good people. This is limiting molders’ ability to grow. Most molders are looking at a good profit over the next five or 10 years, but this can have an impact on their growth.”

Minnick said it affects molders because they can’t grow because they can’t take on new business without adequate labor. It turns into a Catch-22 because they also

can’t invest in automation because they don’t have the labor to grow.

“If they are able to invest, they can put their money in automation,” he said. “It also may push them to locate in areas where there is a good labor force.”

In the last few years, businesses have moved to places where there are relative-ly more technical people that they can hire, including the Southeast and Mexico.

“I run across engineers in Michigan or Ohio or the Northeast,” Minnick said. “They either want to stay where they are or they want to go to North Carolina, South Carolina or Georgia.”

Many skilled workers are attracted to the Southeast by the amount of business growth going on in the region as mold-ers locate closer to customers, including automakers who are expanding in the region.

For injection molders, the skills gap is a problem that is projected to worsen, de-spite efforts to promote the industry. The Society of Manufacturing Engineers pre-dicts that by 2015, the shortfall of skilled factory workers in the United States could reach 3 million, driven by a rebound in manufacturing and a surge in baby boomer retirements.

The 2008-09 recession was catastrophic in terms of U.S. job loss and the extended duration of unemployment. While the

The skills gAP ANd iTs imPAcT oN iNjecTioN molders ...

ProFiles oF 77 leAdiNg iNjecTioN molders ...