economicsgpowell6.weebly.com/uploads/5/6/1/5/56150665/econ_department_final...illustrate a circular...

TRANSCRIPT

ECONOMICS UNIT TWO REVIEW

MICROECONOMICS

ECON DEPARTMENT FINAL EXAM

• Your Economics Departmental Final Exam is cumulative and will count as 5% of your

class grade.

• Following is our Review Schedule:

• Tuesday – we’ll review Unit One and Unit Two

• Wednesday – we’ll review Unit Three and Unit Four

• Thursday – we’ll review Unit Five and finish with a wrap-up game!

ECON DEPARTMENT FINAL EXAM

Econ Study CardsTo help you, you’ll create one Study Card per

unit.

• You can write as much as you want on each

index card – front and back

• They will help you study and prepare!

• Each Study Card will count for a classwork

grade – 25 points/Study Card

Your Name on each card Unit 1, 2, 3, 4 or 5

COMPLETE YOUR STUDY CARD AS YOU REVIEW!

• As you review each unit, capture key information on your Study Card.

• At the end of each unit review, there will be questions you have to answer.

• These will receive a grade, so take them seriously!

• Hint – everyone should make a 100% because you can go back and find the answer if you

don’t know it!

HERE’S YOUR TIMING

• First half of class (45 min.)

• 30-35 minutes – review the unit and capture important info on your index card

• 10-15 minutes – answer the review questions

• When you’re done, come show me your index card and I’ll give you the access code for the

next unit to review.

• Second half of class (45 min)

• 30-35 minutes – review the unit and capture important info on your index card

• 10-15 minutes – answer the review questions

UNIT TWO – MICROECONOMICSLEARNING STANDARD #1 OF 3

SSEMI1 Describe how households and businesses are interdependent and

interact through flows of goods, services, resources, and money.

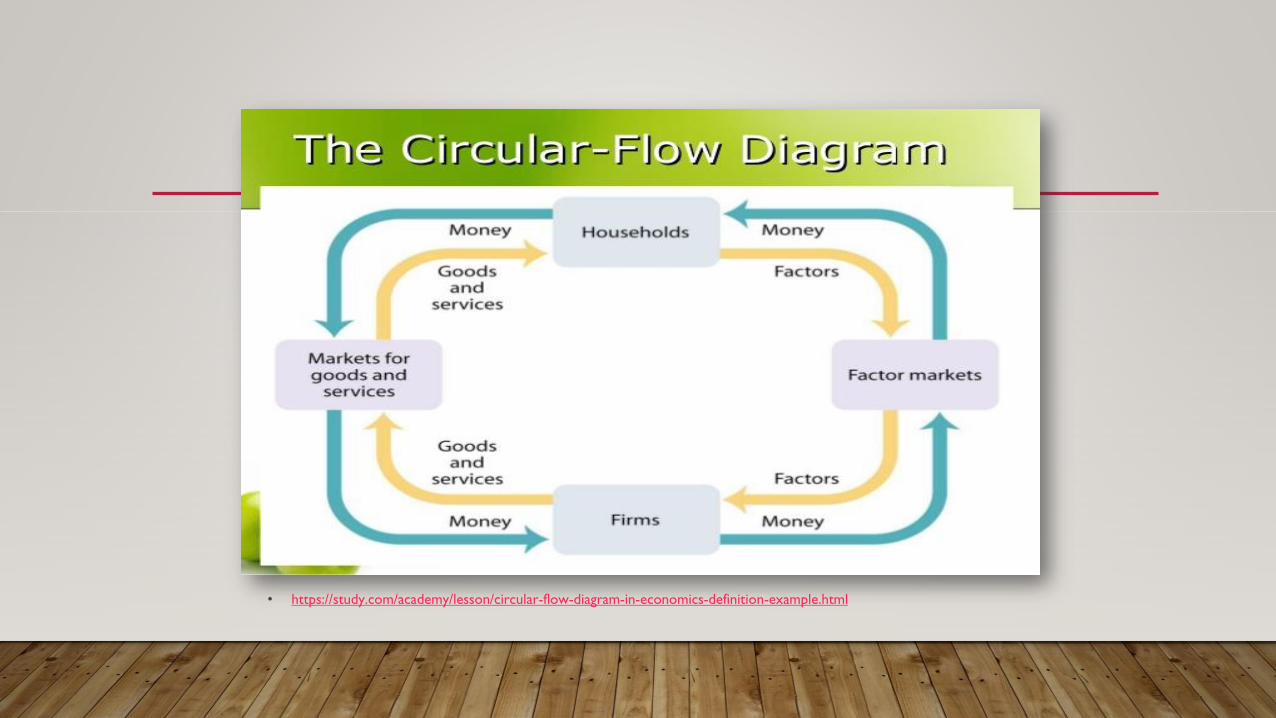

a. Illustrate a circular flow diagram that includes the product market, the

resource (factor) market, households, and firms.

b. Explain the real flow of goods, services, resources, and money between

and among households and firms.

MICROECONOMICS

The economy is a complex area of study – sometimes economists like to look at the small

parts instead of the whole structure

“Zooming in” on the small units that make up the economy is called

microeconomics

The two basic units of microeconomics are:

Producers: those who make goods or provide services for others in the society

They own businesses that provide these outputs

Consumers: those who purchase goods and services

They make up households in the economy

WHY STUDY MICROECONOMICS?

This study can help you understand why consumers choose to buy the things they do and why

producers make the things they do

This relationship – between businesses and households – is described in the circular flow of economics

The circular flow shows a lot of things! :

That consumers and producers participate in voluntary exchange

That resources and goods flow throughout the economy from businesses to

households and then back again

That money flows from households to businesses and then back again

The Circular Flow of

Economics

Resource Markets

PRODUCT

MARKETS

Households Businesses

AROUND THE MARKET

Businesses and Households are only half of the circular flow diagram

The rest is made up of markets:

The Product Market is the part of the economy where businesses sell their goods andservices and consumers purchases those goods and services

This exchange is made possible with MONEY!

The Factor or Resource Market is the place where businesses buy the resources theyneed and consumers offer their labor as a resource to businesses

Remember the 4 Factors of Production: Land, Labor, Capital & Entrepreneurs

This exchange is also made possible with CAPITAL INVESTMENT (purchasing L, L & C) andWAGES (workers’ income)!

• https://study.com/academy/lesson/circular-flow-diagram-in-economics-definition-example.html

DIFFERENT WAYS TO VIEW THE SAME INFORMATION

• Since it’s circular, the elements can be viewed from different

perspectives.

It’s the same information!

It’s just that the Businesses/Firms and

Households are on the left and right of the

diagram (instead of the top and bottom).

So don’t be confused!

TWO CIRCLES GOING IN OPPOSITE DIRECTIONS

• 1. Factor/Product Circle

• Just start with the households >>>

• Households sell land, labor & capital in the

Factor Market

• Businesses use the factors of production to

create goods & services

• Businesses sell these goods and services to the

households in the Product Market.

CIRCLE OF MONEY

• Money Flow Circle (going in the opposite direction as the Factor/Product circle)

• Once again, start with the Households >>>

• Households buy the goods and services

• These purchases become revenue for the businesses

• The business then use that revenue to pay for the factors of production

• One of the factors of production is labor/workers – the wages paid to workers becomes income to the

households which gives households the money to buy goods and services.

UNIT TWO – MICROECONOMICSLEARNING STANDARD #2 OF 3

SSEMI2 Explain how the law of demand, the law of supply, and prices work to determine production and

distribution in a market economy.

a. Define the law of supply and the law of demand.

b. Distinguish between supply and quantity supplied, and demand and quantity demanded.

c. Describe the role of buyers and sellers in determining market clearing price (i.e. equilibrium).

d. Illustrate on a graph how supply and demand determine equilibrium price and quantity.

e. Identify the determinants (shifters) of supply (e.g., changes in costs of productive resources, government regulations,

number of sellers, producer expectations, technology, and education) and illustrate the effects on a supply and demand

graph.

f. Identify the determinants (shifters) of demand (e.g., changes in related goods, income, consumer expectations,

preferences/tastes, and number of consumers) and illustrate the effects on a supply and demand graph.

g. Explain and illustrate on a graph how prices set too high (e.g., price floors) create surpluses, and prices set too low (e.g.,

price ceilings) create shortages.

SUPPLY AND DEMAND

In a market economy, producers and consumers interact to determine prices

Does that surprise you? Why?

This interaction responds to the economic laws of Supply and Demand

Supply: is the total quantity of a product that producers are willing to

make and sell at any market price

Demand: is the total quantity of a product that consumers are willing

and able to buy at any market price

THE LAWS THAT GOVERN

Supply and Demand interact in the market – but they

are trying to accomplish different things!

Producers want the highest possible prices that consumers are willing the

pay! (supply)

Consumers want the lowest possible prices that producers are willing to

sell for! (demand)

These two principles are called the Law of Supply and the Law of Demand –

they will hold true for all products/consumers in the marketplace!

Why do you think this is?

COMPROMISE

Eventually, the interaction of supply and demand will reach a compromise -

a price where both consumers and producers are happy

This is called the equilibrium price or the market clearing price

(because, ideally, at this price, all products would be sold)

Predicting where supply and demand will meet helps businesses price

their products in a way that they make a profit

STATISTICS!

So, businesses compile two types of data to help them predict supply and

demand:

Schedules: tables of data that show the quantities of a good willing to

be bought (demand) or produced (supply) at given prices

Curves: graphs of data that show the quantities of a good willing to be

bought (demand) or produced (supply) at given prices

Do you notice anything about how these statistics may be related?

EXAMPLES – SUPPLY SCHEDULE AND CURVE

Price Quantity

$45 50

$40 46

$35 39

$30 30

$25 24

$20 18

$15 8

$10 5

$5 1

$1 0

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

0 10 20 30 40 50 60

Quantity

Pri

ce

Series1

Schedule

Curve

A supply curve will always rise to the right on a graph

EXAMPLES – DEMAND SCHEDULE AND CURVE

Price Quantity

$45 0

$40 1

$35 5

$30 8

$25 18

$20 24

$15 30

$10 39

$5 46

$1 50

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

0 10 20 30 40 50 60

Quantity

Pri

ce

Series1

• Schedule

• Curve

The demand curve will always fall to the right

on a graph

FINDING AN EQUILIBRIUM

If we combine the data in our last two slides, we can find the

equilibrium price

Review: what is the equilibrium price?equilibrium

Equilibrium Price

$50

$45

$40

$35

$30

$25

$20

$15

$10

$5

$0

0 10 20 30 40 50 60

The X axis shows us the quantity thatQuantity

Pri

ce Demand

Supply

Where the two lines

meet is called the

The Y axis

shows us

the

equilibrium

price, or the

ideal price

the

producer

should

charge

($23)

consumers are willing to buy and that

producers should expect to sell (21)

SO HOW DO BUSINESSES SET PRICES?

Remember, the equilibrium price is an ideal price

– it doesn’t always start out that way!

Businesses will set a price for their product and then watch the market to see

what happens

At the end of the day, if there are extra products left over, the business

knows that the price was too high

This is called a surplus

At the end of the day, if there are more customers asking for the product,

but there are no more on the shelf, the business knows that the price

was too low

This is called a shortage

ON THE

GRAPHPrice set at

$25 – it’s

above the

equilibrium.

Result:

SURPLUS

Equilibrium

Price and Quantity

Surplus

ON THE GRAPH Quantity Demanded

Quantity Supplied

Equilibrium

Price and Quantity

Price set at $10 – it’s

below the equilibrium.

Result: SHORTAGE

Shortage

REACHING EQUILIBRIUM

Based on their study of surplus and shortage,

businesses will adjust their prices over time

Eventually, when all products are sold and no one

is asking for more, the price is just right!

This is called the market clearing price (or equilibrium)

There is no “shaded area” on the graph this time, because a shaded

area always resembles something that’s wrong with the market – either

too many goods or too many consumers!

A COG IN THE WORKS

The price adjustment process is not the only way that a shortage or surplus is

created in the market

The company or government may place restrictions on certain goods or

services that force those items’ prices to NEVER reach equilibrium!

Remember: governments are involved in market economies to promote

fairness and equity – sometimes that requires adjusting prices!

PRICE FLOORS

Any time a price is set at the MINIMUM possible price, it is called a price

floor

Price floors set the price for an item above the equilibrium, keeping the

price artificially high

Yes, it seems backwards – but just believe it!

Based on what you know, what happens if the price is above

the equilibrium??

A good real-life example is the minimum wage!

The government sets a minimum wage that is higher than the

equilibrium would be

Businesses make less profit per worker - what

do they do?

Surplus

Unemployment

PRICE CEILINGS

Any time a price is set at the MAXIMUM possible price, it is called a price ceiling

Price ceilings set the price for an item below the equilibrium, keeping the price

artificially low

Again, yes; it’s backwards – just deal with it!

Based on what you know, what happens if the price is

below the equilibrium??

A good real-life example is low-income housing!

The government sets a maximum rent that can be charged that is lower than the

equilibrium would be

The company makes less profit, so what do they do?

So, what will consumers do when they see the low

price?

Shortage

OTHER CHANGES IN PRICE

Sometimes the price of a good or service changes because the supply or

demand itself has changed

This means something has happened that affects ALL prices at ANY

quantity (so, graphically, the entire curve changes!)

This means that the previous equilibrium price is now either above or

below what should be the new equilibrium price!

So…at first, there will be a shortage or surplus!

In other words, there will be the same market symptoms (effects),

but there may be a different market diagnosis (cause)

CHANGES IN SUPPLY

Sometimes the way producers produce, or conditions outside of their control,will change the supply of a good or service

The price of the raw materials could go up or down, causing a change in supply

Ex: a natural disaster could destroy a crop and make the cost of that crop higher in the market

The technology of production could change, causing a change in supply

Ex: new machinery could be introduced that saves the business moneywhen they produce something

No matter what the cause, supply changes when the cost of production goesup or down!

CHANGE IN SUPPLY ON A GRAPH

On the graph, S1 represents the

original supply and S2 shows the

new supply curve after a change

in supply

You can also see that the

equilibrium price changes from

$16 to $13

When the supply curve shifts to the right, there is an increase in supply

>>>>> Increase

When the supply curve shifts to the left, there is a decrease in supply

<<<<<Decrease

CHANGES IN DEMAND

Sometimes the demand for goods will change as the condition of people in the

market changes

If people’s incomes change, their demand changes

If a close substitute for a product becomes available, demand for the original

product will change

If two products are complements and demand for one changes, demand for the

other will change also

If the population of an area changes, demand changes

If people’s tastes for certain products or styles change, then the demand for those

products will change

No matter what causes the change, demand will change when consumers change their

buying habits

CHANGE IN DEMAND ON A GRAPH

On the graph, D1 representsthe original demand and D2shows the new demandcurve after a change in demand

You can also see that theequilibrium price changesfrom$16 to $19

When the demand curve shifts to the right, there is an increase in demand>>>>>> increase in demand

When the demand curve shifts to the left, there is a decrease in demand<<<<<< decrease in demand

SOME GOOD RULES TO KNOW!

• If supply increases,

price goes down

• If supply decreases,

price goes up

• If demand increases,

price goes up

• If demand decreases,

price goes down

Can you think of some examples of an increase or decrease in supply or

demand?

Change S/D Change Price

Supply

Supply

Demand

Demand

EFFECTS OF CHANGES IN S/D

When price changes to reflect a change in supply or demand, the actual marketresult can vary based on a number of conditions

One such condition is whether or not a good orservice is elastic or inelastic

Elasticity, or the measure of how responsive the demand or supply of a goodis to a change in its price, is determined by several factors

If a good is found to be elastic, that means that asmall change in price will GREATLY affect its S/D

If a good is found to be inelastic, that means that any change in price will have a SMALL impact on its S/D

ELASTICITY OF DEMAND

Whether or not demand for a product is elastic or inelastic depends on several

factors

First, can the purchase be put off to a later time?

Second, are enough substitutes available for the good?

Third, does the purchase take up a large portion

of income?

The more “yes’s” you get to these questions, the more likely a good is elastic;

the more “no’s” you get, the more likely a good is inelastic

Let’s practice! Think about these goods:

Salt, gasoline, watermelon, television, bicycle, bread

ELASTICITY OF SUPPLY

Having an elastic supply is a little harder: elasticity of supply depends on how

quickly a producer can change their supply to meet changes in price

They want to produce more as price goes up, and less as price goes down

If the producer can respond easily and change production, the supply is

elastic

If the company produces the same amount of a good regardless of its

price, or it would take the company a long time to change production, the

supply is inelastic

Let’s practice! Consider producers of these goods:

Cotton candy, oil, computers, corn, hand-made baskets

UNIT TWO – MICROECONOMICSLEARNING STANDARD #3 OF 3

SSEMI3 Explain the organization and role of business and analyze the four types of market

structures in the U.S. economy.

a. Compare and contrast three forms of business organization—sole proprietorship,

partnership, and corporation with regards to number of owners, liability, lifespan,

decision-making, and taxation.

b. Identify the basic characteristics of monopoly, oligopoly, monopolistic competition, and

pure (perfect) competition with regards to number of sellers, barriers to entry, price

control, and product differentiation.

COMPETITION

• Competition is when businesses and firms try to get you to buy

their good/service over one of their competitors.

• Competition helps consumers because it gives them the power

to choose

• Businesses are forced to keep the quality of their goods and

services up and their prices low to effectively compete

LEVELS OF COMPETITION

• There are four levels of competition:

1. Perfect Competition

2. Monopoly

3. Oligopoly

4. Monopolistic Competition

More companies competing Fewer companies competing

PERFECT COMPETITION

• A market with perfect competition is subject only to the laws of supply and

demand with no government involvement (Laisse faire)

# of

Sellers

Barriers

to Entry

Price Control Product

Differentiation

Requirements

Unlimited None

Anyone can

start a

business

None

Completely up to

supply & demand

Sometimes called

Price Takers

None

All products are

identical

Examples: farm

products

1. Many buyers and sellers

participate in the market

2. Sellers offer identical

products

3. Buyers and sellers are

well informed about

products

4. Sellers are able to enter

and exit the market

freely

MONOPOLISTIC COMPETITION

• Monopolistic Competition offers consumers the most product variety

and price options. Each firm makes products that are slightly different

from the others – either in reality or in people’s minds.

# of

Sellers

Barriers

to Entry

Price Control Product

Differentiation

Requirements

Many,

but not

unlimited

Low

Relatively

easy to

enter

Some

can be

increased by

differentiation>>

High Level

Products are highly

differentiated with

marketing, advertising,

brand names

Examples:

Shampoos, toothpastes,

restaurants, etc.

No formal

MONOPOLISTIC COMPETITION

• Monopolistic Competition offers consumers the most product variety and price

options. Each firm makes products that are slightly different from the others –

either in reality or in people’s minds.# of

Sellers

Barriers

to Entry

Price Control Product

Differentiation

Requirements

Many,

but not

unlimited

Low

Relatively

easy to

enter

Some

can be

increased by

differentiation>>

High Level

Products are highly

differentiated with

marketing, advertising,

brand names

Examples:

Shampoos, toothpastes,

restaurants, etc.

No formal

OLIGOPOLY

# of

Sellers

Barriers

to Entry

Price Control Product

Differentiation

Requirements/

Additional

Comments

Few Higher Limited by

mutual

dependence

Considerable

with collusion or

cartels (illegal in

U.S., but not

overseas)

Standardized or

differentiated

Examples:

Soft drinks,

airlines,

electronics, gas

Competition between

companies can lead to

price wars

In this case, a few small firms dominate the market instead of just one –

but they still have the ability to influence price like a monopoly

But, they are still independent companies – they make decisions based

on what other firms do

MONOPOLY

# of

Seller

s

Barriers to

Entry

Price

Control

Product

Differentiation

Requirements/ Additional

Comments

One Very High

Legal Natural

Monopolies –

okay due to

costs of entry,

infrastructure

Complete

control, Price

Setters

Normally

NOT in

consumer’s

best interests

which is why

it’s illegal

Not necessary

except for limited

public relations

Examples of legal

monopolies:

public utility

companies

Considerable government

involvement to avoid illegal

monopolies and to

monitor/manage legal

monopolies

Legal monopolies are also

allowed for patents,

copyrights & other

intellectual property

protections

• All monopolies have one trait in common – a single seller in the market

• Illegal in the U.S., unless it’s in the public’s best interests – then it is

officially approved as a legal monopoly

A QUICK COMPARISON