a comparison of denmark with singapore and hong kong...

TRANSCRIPT

Benchmark of Maritime Nations: A comparison of Denmark with Singapore and Hong Kong

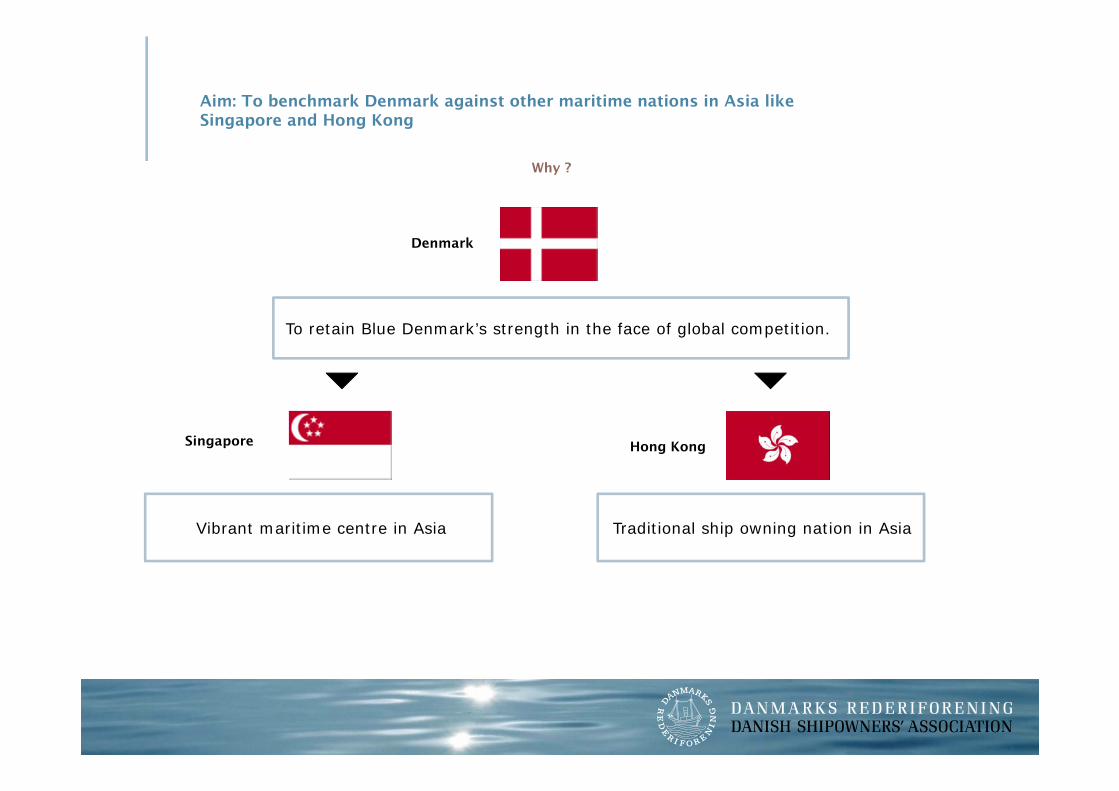

Aim: To benchmark Denmark against other maritime nations in Asia like Singapore and Hong Kong

Singapore Hong Kong

Denmark

Vibrant maritime centre in Asia Traditional ship owning nation in Asia

To retain Blue Denmark’s strength in the face of global competition.

Why ?

Dimensions in Benchmark Study

Comparison on Attractiveness

of Maritime NationShip Registry

Tax

Technical

Social

Dimensions in Benchmark Study

Comparison on Attractiveness

of Maritime NationShip Registry

Tax

Technical

Social

Requirements to own ships Ship Registration Fees Annual Tonnage Tax Market Access

• Newbuilding/Modification• cost• Port State Control• Recognised Organisations• Low age of fleet• IMO’s meeting attendance • Flag of Convenience

• Union Fees• Crew Flexibility• Crew Cost (not examined • in this study)

Tax schemes

Tax

Shipping Tax Regime

• Governments wanting to grow their countries into major shipping centers have put in place different models oftaxation options to transform the viability of shipping companies.

• 3 main categories of tax regimes:

1. Advantageous Tax Regime 2. Special Tax Regime 3. Tonnage Tax Regime

Advantageous tax regime, akin to taxhaven, and relatively relaxed vesselownership structures have caused theFOCs (or open registries) to attract abouthalf the world’s tonnage.

Income derived is exemptedfrom profit tax.

Tonnage tax is the tax levied on the tonnageof shipping companies, as opposed to normalcorporate tax, which is based on the profitsearned by them.

It is a method of calculating theoreticalincome which are then taxed with the normalcorporate income.

Tonnage tax companies pay tax based on thenet tonnage of the ships operated rather thanby reference to the profits earned from suchoperations.

Eg: Panama Eg: Singapore, Hong Kong Eg: Denmark, China

PAGE 6

Tax Scheme in Denmark

Ordinary corporate income tax

Danish Tonnage Tax Regime

Shipping companies pay corporate income tax at 25 % inDenmark. As an alternative to the general rule, they canchoose to calculate their taxable income under the Danishtonnage tax regulations.

• Danish Tonnage Tax regime is based on EU guidelines, under regular reviews (every 7 years).• The choice to be taxed under Danish Tonnage Tax regime is binding for 10 years.• If the tonnage tax system is opted for, the rules automatically apply to all ships, owned or time chartered, andother assets connected with the shipping activities of the company. It applies to all affiliated companies inDenmark.• Time-chartered tonnage may be included in a 1:4 ratio in terms of its own tonnage; including vessels that havebeen chartered as well as time-chartered vessels. If the total gross tonnage of chartered vessels exceeds thetotal gross tonnage of the company’s own ships by more than a 1:4 ratio, the excess vessels will be taxed underthe general rules.•Taxable income is computed based on deemed profits calculated using the tonnage based formula below.

Taxable Income per vessel per day

Per 100 NT 2010 onwards (DKK) * US$

0 to 1,000 NT 8.97 1.61

1,001 to 10,000 NT 6.44 1.16

10,001 to 25,000 NT 3.85 0.69

Over 25,000 NT 2.53 0.46

Based on exchange rate of 1.00 DKK = 0.18 USD

* A 15% increase in tonnage tax since 2010.

Tax Scheme in Singapore

Shipping Taxes

Ship Owning/Operations

Ship Management

Maritime Finance

Ship Broking,

FFA Trading

In the absence of MSI-AIS taxscheme, companies are taxed atcorporate rate of 17%.

Ship Registration Fees (Block Transfer Scheme)

Ordinary corporate income tax

MSI-AIS Scheme

Tax Scheme in Singapore

Maritime Sector Incentive (MSI) - Approved International Shipping Enterprises (AIS) Scheme

• Certainty of the AIS scheme is granted for 30 years from 2007.• Exemption from corporate income tax on all income earned by ships registered in Singapore or abroadin respect of all international shipping activities conducted from or outside Singapore.• No expiry date as long as ships continue to be Singapore flag.• For owning and/or operating foreign flag from Singapore, the exemption is given to a shipping companyon a 10 year period, subjected to a major review after 5 years.• To qualify for exemption, a shipping company must:

be a company resident in Singapore. be a significant owner/operator of ships. must have a certain minimum level of annual local business spending (eg: manpower cost,rental, repairs, bunkers, etc) in Singapore. No clear guidelines on the amount from the authorities.

• A Singapore ship is defined as a ship for which a permanent certificate of registry has been issued underthe Merchant Shipping Act in Singapore. This has been expanded to include offshore industry mobileunits, (eg: oil rigs in the form of jack-ups, semi-submersibles and submersibles) as well as floatingproduction storage and loading vessels, dredgers, seismic vessels and more.

• Under this scheme, withholding tax exemption will be extended to qualifying payments made in respect of qualifyingloans taken from foreign lenders to finance or construct Singapore-flagged ships, subjected tocertain conditions. proceeds from sale of ships on Singapore-flagged ships are tax exempted.

Ship Owning, Ship Operating

Tax Scheme in Singapore

Maritime Sector Incentive (MSI) - Approved Shipping and Logistics (ASL) Scheme

• Tax concessionary rate of not less than 10% on approved incremental income derived from the provision ofinternational freight and logistic services.• For ship agencies, ship management companies, logistic companies and freight forwarders to apply.• This incentive is granted for a period of 10 years, with a major review after 5 years.

Ship Management

Maritime Sector Incentive (MSI) – Maritime Finance Incentive (MFI) Scheme

• Tax concessionary rate of 10% on income in connection with and incidental to the management of a vesselportfolio, eg: fund management, performance and bonus fees, for Approved Shipping Investment Managers.• The approved ship investment vehicle can be in the form of a ship leasing company, partnership, shipping fund orshipping trust.• Tax concession is given for qualifying finance and operating income derived from leasing activities.

Maritime Finance

Maritime Sector Incentive (MSI) – Maritime Finance Incentive (Container) Scheme

• The MSI- MFI was enhanced to cater for container boxes financing and leasing activities.• Tax concessionary rate of 10% on income derived by an Approved Container Investment Manager.• Qualifying income includes trustee fees, management fees, performance and bonus fees and administrative servicefees.

Incentive for Ship Brokers and Forward Freight Agreement ( FFA) Traders

• Tax concessionary rate of 10% on incremental fees or commissions derived from qualifying shipbroking activitiesand gains derived from forward freight agreement trading.• Incentive is given for 5 years.

Ship Broking, FFA Trading

Ship Registration Fee Structure in Singapore

Singapore Flag

Registration Fee S$

New Registration 2.50 per NTSubjected to a

Minimum Fee 1,250.00 (500 NT)Maximum Fee 50,000.00 (20,000 NT)

Discounted Scheme: Block Transfer SchemeQualifying Criteria:- 2 ships aggregating at least 40,000 NT- 3 ships aggregating at least 30,000 NT- 4 ships aggregating at least 20,000 NT- 5 ships of any aggregating tonnageNew Registration 0.50 per NT

Subjected to aMinimum Fee 1,250.00 (2,500 NT)Maximum Fee 20,000.00 (40,000 NT)

Annual Tonnage Fee

0.20 per NTSubjected to a

Minimum Fee 100.00 (500 NT)Maximum Fee 10,000.00 (50,000 NT)Note: Payable at the start of each year even if vessel may be closed for the year. Unpaid fees and tonnage taxconstitute maritime liens on vessel.

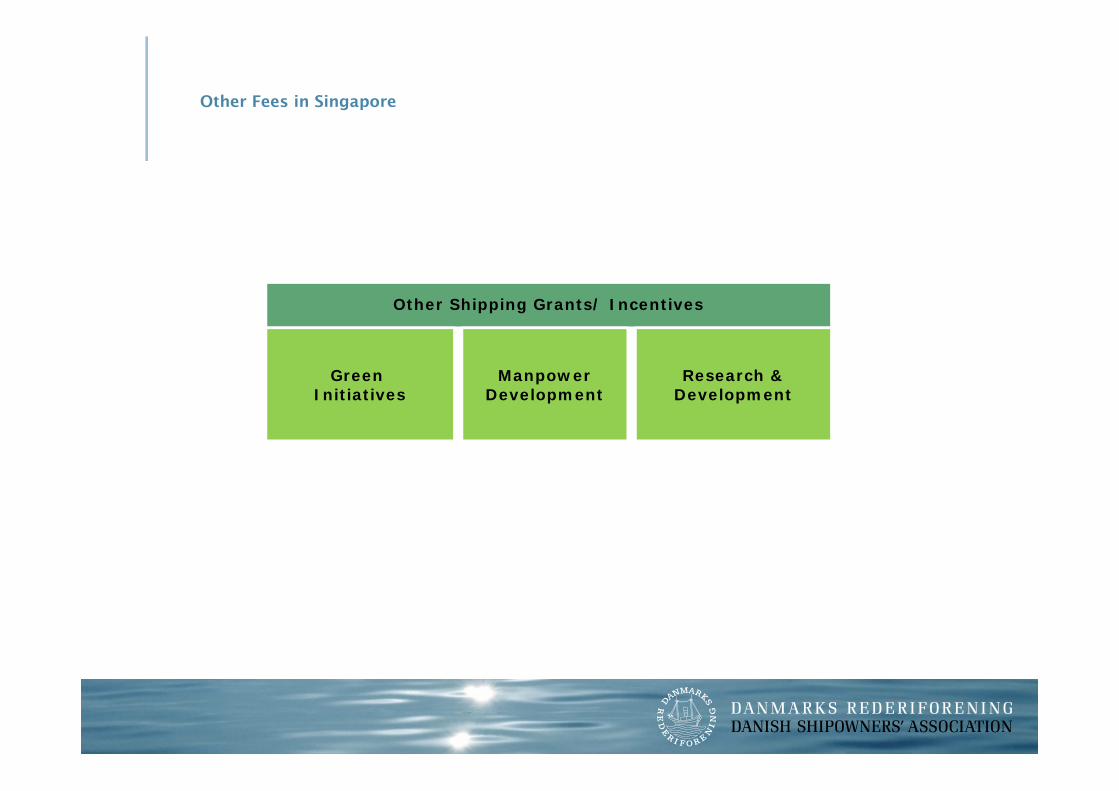

Other Fees in Singapore

Other Shipping Grants/ Incentives

Green Initiatives

ManpowerDevelopment

Research &Development

Shipping Grants/ Incentives in Singapore offered by the MPA

Green Initiatives

Green Ship

Green Port Green Technology

Maritime Singapore

Green Initiative

• Encourage the use of energy efficient ship designs that reduce fuel consumption andcarbon dioxide emissions.• Ships which go beyond the IMO’s Energy Efficiency Design Index (EEDI) will qualify.• Qualifying Singapore-flagged ships will enjoy 50% reduction in initial registration feesand 20% rebate on Annual Tonnage Tax (a yearly fee paid to maintain the ships in theregistry) .

• Encourage ocean-going ships calling at the Port ofSingapore to reduce the emission of pollutants.

• 15% concession in port dues will be granted toocean-going vessels that use type-approvedabatement/scrubber technology or clean fuels duringthe port stay within Singapore Port Limits.

• Encourage local maritime companies to develop andadopt green technologies.

• Provide grants of up to 50% of total qualifying costs toco-fund the development and adoption of greentechnologies. Capped at S$2 million per project.

Shipping Grants/ Incentives in Singapore

Manpower Development

Maritime Cluster Fund (MCF)

• S$45 million to support new biz developments• S$50 million grant to develop manpower expertise in the maritime industry

Training@MaritimeSingapore: co-fund 60% course fee/programme attended by local staff Talent@MaritimeSingapore: co-fund 50% expenses for overseas attachment training (up to S$50k per trainee) Investmanpower@MaritimeSingapore: Funding for developing training infrastructure, HR processes, coursescurrently not available

Research & Development

MPA Maritime Innovation & Technology (MINT) Fund

• S$100 million grant to develop into a global maritime knowledge hub for 10 years (2003 to 2013)• Help companies and research institutes transform R&D concepts to commercial products

Co-fund up to 50% of total direct R&D project costs (eg: equipment, material, professional services, intellectualproperty, ancillary cost, manpower costs to engage external research)

EDB Research Incentive Scheme for Companies (RISC)

• Co-share up to 50% of manpower related costs related to staff employed for the new R&D centre• Manpower related costs refers to basic salary, living allowance, economy airfare.

- Hong Kong’s tax regime is governed by the "territorial principle" under which Hong Kong only taxes income sourcedfrom within the jurisdiction.

- There are no capital gains tax, no withholding tax on service fees or interest payments, no interest tax, no sales tax,no VAT, no estate duty and no annual net worth tax in Hong Kong.

- Because of its liberal tax regime in general, there are no specific incentives/subsidies for the shipping companies.

- There is, however, the Annual Tonnage Charge (ATC) reduction scheme to encourage quality fleet.

Tax Scheme in Hong Kong

US$Initial

Registration Fee

Annual Tonnage

Fee1 year 3 year 5 year 7 year

Without ATC 1,933 9,989 11,922 31,900 51,878 71,856

With ATC 1,933 9,989 11,922 26,905 41,889 56,872

An illustration on how a well operated ship without any detentions can come out cheaper :

Ordinary corporate income tax

Activities outside Hong Kong’s jurisdiction are not taxed.

Annual Tonnage Charge (ATC) reduction scheme

To encourage better quality and safety standards of itsregistered tonnage, Hong Kong flag-state reduces theATC on ships by 50% for the following year uponcompletion of 2 years of continuous registry (qualifyingperiod) with zero detention record.

In Danish International Ship Register (DIS)

• Denmark has chosen tax incentives as a means of reducing manning costs.

• Seafarers, being Danish or non-Danish, is thus exempted from paying personal income tax in Denmark of their DIS salary.

• As a consequence collective agreements or individual contracts of agreement will be able to set wages as net wages.

• The legal basis for this positive measure is provided by the EU Guidelines on state aid to maritime transport which allows for reduced rates of income tax, reduced rates of contributions to social protection etc. for seafarers onboard ships registered in a EU member state, for example Denmark. These Guidelines will normally be reviewed every seven years, and a review is taking place for the time being.

In Singapore

• Income of a crew member of a ship operated in international traffic may be exempted from Hong Kong salaries tax.

In Hong Kong

• The employment income of crew working on Singapore ships is specially exempted from tax where the employment is substantially outside Singapore.

Seafarers Taxation

Ship Registry

PAGE 18

Requirements to Own Ships

Requirements to Own Ships

Ship owners must register an agency, branch or subsidiary company in Denmark. The ship must be Danish owned or owned by a foreign company in which a Danish citizen orcompany owns at least 20% of the capital and exercises a considerable degree of influence invoting rights. The foreign company must also appoint a representative in Denmark.EU companies can register provided that a certain amount of control takes place in Denmark.

Ships must be registered under companies incorporated in Singapore or Singapore citizensand permanent residents. Companies can be locally owned or foreign owned. A locally owned company is one with themajority of its shares owned by locals. A foreign owned company is one where the majority ofshares are held by non-Singaporeans. Company must have a minimum paid up capital of S$50,000.

The majority interest in the ship must be owned by a qualified person i.e. a Hong Kongresident, a body corporate incorporated in Hong Kong or an overseas company registered witha place of business in Hong Kong. An authorised representative must also be appointed in Hong Kong.

Singapore

Hong Kong

Denmark

Size of 8,000 TEU Container

94,193 GT

53,271 NT

1 Calculated based on the Block Transfer Scheme does not taken into account Singapore’s Green Ship incentive.2 Does not take into account the 50% discount on Annual Tonnage Charge for ships with no detentions over 2 years.3 However, a registration fee of 0.1% of the purchase price is applicable for second-hand tonnage.

Tax/Fee Comparison on Ship Registries (8,000 TEU Container Vessel)

Cumulative Fee (US$)

Cumulative Fee (US$)

Cumulative Fees

In US$ Initial Fees

Annual Tonnage

Fees 1-year 2-year 3-year 4-year 5-year 6-year 7-year 8-year 9-year 10-year

Singapore1 16000 8000 24000 32000 40000 48000 56000 64000 72000 80000 88000 96000

Hong Kong2 1933 9989 11922 21911 31900 41889 51878 61867 71856 81845 91834 101823Denmark DIS3 # 0.00 31729 31729 63459 95188 126918 158647 190376 222106 253835 285565 317294

Exchange Rates: 1.00 SGD = 0.8 USD , 1.00 HKD = 0.13 USD, 1.00 DKK = 0.18 USD

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

Singapore

Hong Kong

Denmark DIS

0

50000

100000

150000

200000

250000

300000

350000

Singapore

Hong Kong

Denmark DIS

Market Access

Denmark

Allowed to trade worldwide in international trade.

Access to cabotage in EU member states with some limitations re. islandand mainland cabotage in some South European countries.

Access to Greenlandic trade.

Are to comply with EU sanctions regulation. These restrictive measureswhich may comprise trade restrictions and other measures, have frequentlybeen imposed by the EU in recent years, both on an autonomous EU basis orimplementing Resolutions of the Security Council of the UN. However, Danishcompanies will generally have to comply with these measures regardless offlag chosen.

Singapore

Allowed to trade worldwide in international trade.

Follows a policy of implementing Resolutions of the Security Council of theUN.

Hong Kong

Allowed to trade worldwide in international trade.

Hong Kong’s diplomatic relations are the responsibility of the PRC and assuch sanctions being imposed against other countries are limited and usuallybased on implementing Resolutions of the Security Council of the UN.

Technical

Technical aspects of flag state performance

Paris MOU White List

TokyoMOU White

List

USCG QUALSHIP

21

Recognisedorganisations/class societies

Low Age of Fleet

IMO Meeting’s Attendance

Not recognised as

FOC by ITF

An indicator on the effective enforcement of international rules and that the ship is manned and operated in compliance with these rules.

Whether classsocieties are members of the International Association of Classification Society (IACS).

Assumption is that a flag with younger ships is more likely to attract quality tonnage.

Flag state that attends the major IMO meetings are thought more likely to be seriously committed to the implementation and enforcement of IMO rules.

The International Transport Workers' Federation’s (ITF) Fair Practices Committee (a joint committee of ITF seafarers' and dockers'unions) publicly declares a listof flag states as Flag of Conveniences.

✓Denmark

Singapore

Hong Kong

✓ ✓ ✓ ✓

All 3 flag states are competitive in the technical aspects of benchmarking.

Port State Control

Social

Crew Flexibility

Denmark

No crewing restrictions.

However, a maximum of 40% of vessels are allowed to have a master fromnon-EU countries.

Singapore No crewing restrictions.

Hong Kong No crewing restrictions.

PAGE 26