a fixed-income investor conference

TRANSCRIPT

MANAGING GROWTH: CREDIT, SURVEILLANCE AND CAPITAL

A FIXED-INCOME INVESTOR CONFERENCE

Presented by Financial Guaranty Insurance CompanyFriday, September 22, 2006

Frank J. Bivona, Chief Executive Officer

WELCOME TO FGIC’SFixed Income Investor Conference

TODAY’S FOCUSMANAGING GROWTH

•• Credit Credit –– Risks We Insure and the Risks We Insure and the Related ProcessRelated Process

•• SurveillanceSurveillance –– Review and Oversight of Review and Oversight of Insured ExposureInsured Exposure

•• Capital Capital –– Managing Our Resources to Managing Our Resources to Support TripleSupport Triple--A RatingsA Ratings

EXPANDING THE FRANCHISEMANAGING GROWTH

•• Established in 1983Established in 1983 –– Leader in the Leader in the Industry in Market and Product ExpansionIndustry in Market and Product Expansion

•• MidMid--1990’s 1990’s –– Pull Back by Then Parent Pull Back by Then Parent (GECC) (GECC) –– Low Risk Municipal FocusLow Risk Municipal Focus

•• Ownership Change in December 2003 Ownership Change in December 2003 ––New Strategy and DirectionNew Strategy and Direction

STRATEGYMANAGING GROWTH

Selectively Expand & Develop the FGIC FranchiseSelectively Expand & Develop the FGIC Franchise

Reenter Markets Where FGIC ParticipatedReenter Markets Where FGIC Participated

Where Other Industry Participants Have Proven Business ModelsWhere Other Industry Participants Have Proven Business Models

Focus on Excellent Risk, Growth and Return CharacteristicsFocus on Excellent Risk, Growth and Return Characteristics

EXECUTION OF STRATEGYMANAGING GROWTH

ACTIONS

• Established State of the Art Risk Management and Corporate Governance

• Hired Experienced Market Leaders in New Product Areas

• Re-established London Office – International Franchise

• Extensive Client Marketing to Highlight Ability to Execute

• Expanded Investor Reporting and Transparency, Reinforced by Calling Campaign to Promote Top-notch Trading Value

EXECUTION OF STRATEGYMANAGING GROWTH

RESULTS

• Re-established Our Presence in Virtually Every Major Financial Guaranty Market

• More Than Doubled Staffing Levels – Senior Management is the Most Tenured in the Industry

• Robust Investor Relations Programs that Support Superior Trading Value

• Financial Results and Claims-paying Resources Have Grown at Exceptional Levels

Frank J. Bivona, Chief Executive [email protected] J. Bivona is Chief Executive Officer and a member of the Board of Directors of FGIC Corporation. Before joining FGIC, Mr. Bivona was Vice Chairman and Chief Financial Officer of Ambac Financial Group, Inc. and Ambac Assurance Corporation. In addition to his CFO role, other responsibilities while at Ambac included: Group Head of the Financial Services Group; senior member of the Portfolio Risk Management Committee; President of the Construction Loan Insurance Company (Connie Lee), an Ambac subsidiary; and head of several Ambac businesses, including investment arbitrage, derivative products, third party investment management; investor relations, rating agency relationships and reinsurance. Prior to Ambac, Mr. Bivona was with Citibank in various finance positions, including CFO of Citibank's Global Insurance Division. He also worked in the Northern European Division based in London and played a key role in establishing new offices in Scandinavia. He is a member of the Board of Directors of the YMCA of Greater New York. Mr. Bivona received a BS from Adelphi University.

MANAGING CREDIT

Sandy D’Imperio, Chief Credit Officer

CREDIT RISK MANAGEMENT

•• Establish Credit PolicyEstablish Credit Policy

•• Ensure Compliance & ConsistencyEnsure Compliance & Consistency

•• Communicate Risk ToleranceCommunicate Risk Tolerance

ROLE OF CREDIT RISK MANAGEMENTCREDIT RISK MANAGEMENT

ESTABLISH CREDIT POLICYESTABLISH CREDIT POLICY

•• Review Underwriting CriteriaReview Underwriting Criteria

•• Set Risk LimitsSet Risk Limits

•• Modify Credit Policy as NecessaryModify Credit Policy as Necessary

•• Communicate Changes InternallyCommunicate Changes Internally

ROLE OF CREDIT RISK MANAGEMENTCREDIT RISK MANAGEMENT

•• CRM InvolvementCRM Involvement

•• Credit Committee StructureCredit Committee Structure

•• Standardized DocumentationStandardized Documentation

ENSURE COMPLIANCE AND CONSISTENCYENSURE COMPLIANCE AND CONSISTENCY

ROLE OF CREDIT RISK MANAGEMENTCREDIT RISK MANAGEMENT

COMMUNICATE RISK TOLERENCECOMMUNICATE RISK TOLERENCE

•• Deal MeetingsDeal Meetings

•• Senior Credit CommitteeSenior Credit Committee

•• Portfolio Risk CommitteePortfolio Risk Committee

•• Surveillance MeetingsSurveillance Meetings

CRM TEAM

•• Three Deal ManagersThree Deal Managers

•• One Financial Institutions AnalystOne Financial Institutions Analyst

•• One Modeling ManagerOne Modeling Manager

•• Sovereign Risk ConsultantSovereign Risk Consultant

Sandy D’Imperio, Chief Credit Officer

[email protected]@fgic.com

Alessandra V. D'Imperio, Senior Managing Director and Chief Credit Officer, has overall responsibility for FGIC's underwriting risk management for new business production. Ms. D'Imperio joined FGIC in April 2005. Prior to that, she was a Managing Director and Head of Credit Risk Management, Public Finance, at Ambac. She began her career at MBIA. Ms. D'Imperio holds a BA from the State University of New York at Albany and an MPA from New York University.

FGIC U.S. PUBLIC FINANCE

Jeffrey R. Fried, Senior Managing Director

BOOK OF BUSINESSU.S. PUBLIC FINANCE

Limited ProviderLimited Provider

Single Skill SetSingle Skill Set

Narrow Book of BusinessNarrow Book of Business

Single-risk ConcentrationSingle-risk Concentration

Market Share FocusMarket Share Focus

Low RiskLow Risk

FGIC AS OF 12/03

Leases3%

Transportation12%

Excise12%

Net Par In Force

$189.4 Billion $189.4 Billion

Tax-Supported52%

Utility Revenue17%

Education4% Other PF

<1%

BOOK OF BUSINESSU.S. PUBLIC FINANCE

FGIC AS OF 6/06

Return FocusReturn Focus

Still Low RiskStill Low Risk

Risk DispersionRisk Dispersion

Diversified Book of BusinessDiversified Book of Business

Multiple Skill SetMultiple Skill Set

Full Service ProviderFull Service Provider

Excise12%

Net Par In Force$219.9 Billion

Net Par In Force

$219.9 Billion $219.9 Billion

Other PF<1%

Leases7%

Tax-Supported42%

UtilityRevenue

16%

Transportation11%

Education5% Health Care

3%

Investor-OwnedUtilities 2%

Housing<1%

BOOK OF BUSINESS

12/0312/03

U.S. PUBLIC FINANCE

6/066/06

Excise12%

Net Par In Force$219.9 Billion

Net Par In Force

$219.9 Billion $219.9 Billion

Other PF<1%

Leases7%

Tax-Supported42%

UtilityRevenue

16%

Transportation11%

Education5% Health Care

3%

Investor-OwnedUtilities 2%

Housing<1%

Leases3%

Transportation12%

Excise12%

Net Par In Force

$189.4 Billion $189.4 Billion

Tax-Supported52%

Utility Revenue17%

Education4% Other PF

<1%

Where We’re Going

CONTINUED EXPANSION AS INDUSTRY LEADERS

Guiding Principles

• Focus on Value Added Market Sectors

• Relationships and Execution Capabilities

• Creative Credit Enhancement Solutions

• Maintain Risk / Reward Discipline

U.S. PUBLIC FINANCE

Where We’re Going

BUILDING BLOCKS

Core InfrastructureCore Infrastructure

• Maintain Balanced Portfolio

• Keep Steady Deal Flow

• Service Client Base

•• Maintain Balanced PortfolioMaintain Balanced Portfolio

•• Keep Steady Deal FlowKeep Steady Deal Flow

•• Service Client BaseService Client Base

Select Enterprise SectorsSelect Enterprise Sectors

• Health Care• Municipal Electric Utilities• Cultural Institutions• Land-secured Deals• Municipal Leasing• Transportation

•• Health CareHealth Care•• Municipal Electric UtilitiesMunicipal Electric Utilities•• Cultural InstitutionsCultural Institutions•• LandLand--secured Dealssecured Deals•• Municipal LeasingMunicipal Leasing•• TransportationTransportation

Public / Private Partnerships (P3s) and Project Finance• Potential High Growth• Essential Assets• Execution Capabilities

Public / Private Partnerships (P3s) and Project Finance• Potential High Growth• Essential Assets• Execution Capabilities

U.S. PUBLIC FINANCE

RISKRISK

Construction

YANKEE STADIUM

CREDIT ANALYSIS EXPERTISEU.S. PUBLIC FINANCE

Construction Risk

Bankruptcy Risk

Environmental Risk

Enterprise Risk

Financing Risk

Structural Risk

Construction RiskConstruction Risk

Bankruptcy RiskBankruptcy Risk

Environmental RiskEnvironmental Risk

Enterprise RiskEnterprise Risk

Financing RiskFinancing Risk

Structural RiskStructural Risk

CREDIT ANALYSIS EXPERTISE

YANKEE STADIUM EXAMPLE

RISKSRISKS

ConstructionConstructionConstruction EnvironmentalEnvironmentalEnvironmental

StructuralStructuralStructural EnterpriseEnterpriseEnterpriseFinancingFinancingFinancing

BankruptcyBankruptcyBankruptcy

U.S. PUBLIC FINANCE

Construction Risk

Bankruptcy Risk

Environmental Risk

Enterprise Risk

Financing Risk

Structural Risk

Construction RiskConstruction Risk

Bankruptcy RiskBankruptcy Risk

Environmental RiskEnvironmental Risk

Enterprise RiskEnterprise Risk

Financing RiskFinancing Risk

Structural RiskStructural Risk

CREDIT ANALYSIS EXPERTISE

YANKEE STADIUM EXAMPLE

MITIGANTSMITIGANTS

ConstructionConstructionConstruction

GuarantiesGuarantiesSuretiesSuretiesContingenciesContingencies

BankruptcyBankruptcyBankruptcy

Stadium CompanyStadium Company

EnvironmentalEnvironmentalEnvironmental

Impact SurveyImpact Survey

EnterpriseEnterpriseEnterprise

Credit AnalysisCredit AnalysisStress TestStress Test

ReservesReserves

StructuralStructuralStructural

Property Tax Property Tax AnalysisAnalysis

FinancingFinancingFinancing

Derivative ExpertiseDerivative Expertise

U.S. PUBLIC FINANCE

GOALS

• Deep Relationships Built on Trust• Deep Relationships Built on Trust

• Leader in Value Added Sectors• Leader in Value Added Sectors

• Insurer of Choice for Complex Transactions

• Insurer of Choice for Complex Transactions

• Expand Range of Products and Services

• Expand Range of Products and Services

• Maintain Strict Credit Risk Standards

• Maintain Strict Credit Risk Standards

U.S. PUBLIC FINANCE

Jeffrey R. Fried, Senior Managing [email protected]

Jeffrey R. Fried, Senior Managing Director, leads FGIC’s Public Finance Group. Before joining FGIC, he was General Counsel, since 1998, of Ambac Assurance Corporation's Public Finance Department and Financial Services Division. Mr. Fried was also a voting member of Ambac's Public Finance credit committee. In 1995, Mr. Fried joined Ambac from Greenberg Traurig LLP, where he served as bond counsel and underwriters' counsel. He holds a BS from the State University of New York at Albany and a JD from Fordham University School of Law.

INTERNATIONAL FINANCETimothy S. Travers, Senior Managing Director

TIMELINEINTERNATIONAL FINANCE

FGIC Founded

1983 12/03

Sale to New Investor Group

Opened London and Paris Offices

1990s

• Obtained Branch Licenses – UK and France

• Closed London and Paris Offices – Branches Kept in Place

TIMELINE: 12/2003 – 8/2006

FGIC12/03

6/04 First Hires

London Office Opens10/04

11/04FSA Approves

License for FGIC UK Limited Ltd

Insures 1st Deal11/04

1/051st New

IssuePriced

FGIC Credit Products

Ltd ObtainsFSA License

7/05

9/05Closes 1st Two

Future Flow Deals

Insures 1stUtility New

Issue11/05

6/06Insures 1st New IssuePFI Deal

Insures 1st Euro Market & 1st Italian Deal

6/06

8/06Awarded 1stMandate forAustralian

Deal

INTERNATIONAL FINANCE

FOCUSED CREDIT CULTURE

Time Zones. . .

…and Technology

INTERNATIONAL TEAM

Credit FocusedCredit Focused • One Credit Committee – Streamlined, Consistently Applied Standards

• One Credit Committee – Streamlined, Consistently Applied Standards

Skill Base Strength

INTERNATIONAL FINANCE

ExperiencedExperienced • Real Time Feedback• Proven Track Records• Real Time Feedback• Proven Track Records

Execution OrientedExecution Oriented • Nimble / Responsive • Promises Kept• Nimble / Responsive • Promises Kept

Local Market KnowledgeLocal Market Knowledge

• Languages – French, Spanish, Italian, Portuguese, Greek

• Markets – London, Sydney, Hong Kong, Tokyo, Paris, Madrid

• Languages – French, Spanish, Italian, Portuguese, Greek

• Markets – London, Sydney, Hong Kong, Tokyo, Paris, Madrid

BOOK OF BUSINESSINTERNATIONAL FINANCE

Net Par In Force

$0.17 Billion$0.17 Billion

12/200312/200312/2003

International Sovereign

68%

Sub-Sovereign32%

Sub-Sovereign4%

Public FinanceInfrastructure

14%

Other1%

Future Flow7% Sovereign

1%

Pooled Debt Obligations

39%

Utility32%

Toll Road2%

6/30/20066/30/20066/30/2006

Net Par In Force

$8.3 Billion$8.3 Billion

COUNTRY BREAKDOWN

Australia9%

United Kingdom37%

Turkey5%

Singapore2%

France2%

Italy4%

Brazil1%

Canada<1%

Kazakhstan1%

Diversified38%

$8.3 Billion Net Par Outstanding$8.3 Billion Net Par Outstanding$8.3 Billion Net Par Outstanding

INTERNATIONAL FINANCE

WHERE ARE WE GOING?

Exporting Our ExpertiseExporting Our ExpertiseP3 FrontierP3 Frontier

New Asset ClassesNew Asset Classes

Acceptable Risk ProfilesAcceptable EconomicsAcceptable Risk ProfilesAcceptable Economics

New Geography?New Geography? Central & Eastern Europe, Latin America, AsiaCentral & Eastern Europe, Latin America, Asia

New Offices?New Offices? Sydney, Tokyo, Mexico City, Madrid, Paris, Milan, Frankfurt, TorontoSydney, Tokyo, Mexico City, Madrid, Paris, Milan, Frankfurt, Toronto

INTERNATIONAL FINANCE

BIRMINGHAM HOSPITAL PFI EXAMPLE

CREDIT ANALYSIS EXPERTISEINTERNATIONAL FINANCE

CREDIT ANALYSIS EXPERTISE

BIRMINGHAM HOSPITAL PFI PROJECT EXAMPLE

RISKSRISKS

ConstructionConstructionConstruction Trust DefaultTrust DefaultTrust DefaultService ContractService ContractService Contract

Force MajeureForce Force MajeureMajeureFoundation Trust Vires

Foundation Trust Foundation Trust ViresVires

INTERNATIONAL FINANCE

CREDIT ANALYSIS EXPERTISE

BIRMINGHAM HOSPITAL PFI PROJECT EXAMPLE

MITIGANTSMITIGANTS

ConstructionConstructionConstruction

ExperienceExperienceGuarantiesGuarantiesTA ReviewTA Review

Service ContractService ContractService Contract

ExperienceExperienceCompetitive SuppliersCompetitive Suppliers

TA ReviewTA Review

Trust DefaultTrust DefaultTrust Default

Secretary of State Secretary of State GuaranteeGuarantee

of Trust Obligationof Trust Obligation

StandstillStandstillDSRADSRA

TerminationTerminationForce MajeureForce Force MajeureMajeure

QC OpinionQC OpinionAuditors OpinionAuditors OpinionStringent Legal AnalysisStringent Legal Analysis

Foundation Trust ViresFoundation Trust Foundation Trust ViresVires

INTERNATIONAL FINANCE

WHERE WE ARE. . .WHERE WE ARE GOING

?? ??

INTERNATIONAL FINANCE

Timothy Travers is Senior Managing Director of International Finance and Global Utilities of FGIC Corporation. Prior to joining FGIC, Mr. Travers held various positions at Ambac Assurance Corporation, most recently Managing Director-European Structured Finance and Securitization. He served as Ambac's Managing Director-Global Utilities from 1993 through 2002. Mr. Travers received a BS from New York University’s School of Business and Public Administration.

Timothy S. Travers, Senior Managing Director [email protected]

U.S. STRUCTURED FINANCE

Thomas J. Adams, Senior Managing DirectorKenneth L. Degen, Managing Director

MBS84%

FGIC’S EVOLUTION

Very Limited ParticipationVery Limited Participation

Broad Participation Across Market SpectrumBroad Participation Across Market Spectrum

2006

U.S. STRUCTURED FINANCE

Narrow FocusNarrow Focus Building Portfolio Similar to PeersBuilding Portfolio Similar to Peers

CDOsCDOsCommercial AssetsCommercial AssetsConsumer AssetsConsumer Assets

2003

MBS84%

BOOK OF BUSINESSU.S. STRUCTURED FINANCE

Conduits6%

Credit Card5%

Net Par In Force

12/200312/200312/2003

$17.2 Billion $17.2 Billion $17.2 Billion

MBS83%

Other6%

MBS84%

BOOK OF BUSINESSU.S. STRUCTURED FINANCE

MBS83%

Auto5%

6/20066/20066/2006

$61.2 Billion$61.2 Billion$61.2 Billion

MBS59%

CDO22%

Credit Card1%

Other <1%

Other ABS6%

Pooled Aircraft4% Receivables

3%

Conduits6%

Credit Card5%

Net Par In Force

12/200312/200312/2003

$17.2 Billion $17.2 Billion $17.2 Billion

MBS83%

Other6%

HIRED STRUCTURED FINANCE PROFESSIONALSTO SUPPLEMENT EXISTING TEAM

MBS84%

U.S. STRUCTURED FINANCE

ANALYSIS

ABS CONSUMER

SUB-PRIME AUTO LOAN TRANSACTIONS

MBS84%

SUB-PRIME AUTO LOAN TRANSACTIONS

ABS CONSUMERU.S. STRUCTURED FINANCE

RISKSRISKS

Collateral

• Borrower Credit Quality

• New vs. Used Car

• Borrower Equity

• Loan Terms

Counterparty

• Underwriting Guidelines / Process

• Collection Efforts

• Ability to Liquidate / Repossess Collateral

Market

• New Car Market -Incentives, Supply, etc.

• Used Car Price

• Volatile Asset Performance

MBS84%

ABS CONSUMERU.S. STRUCTURED FINANCE

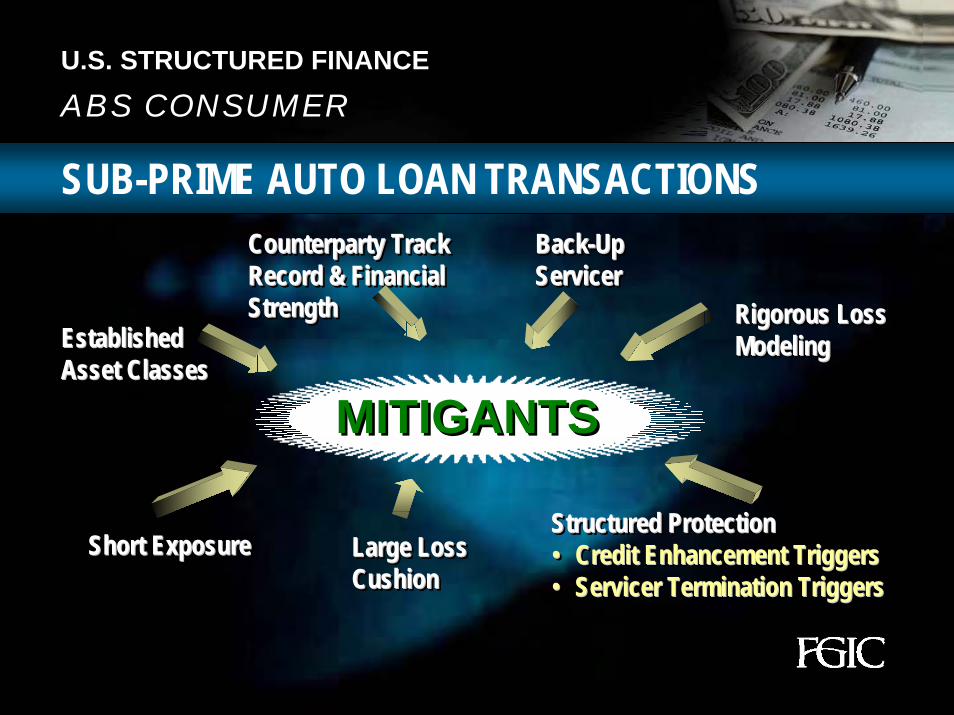

MITIGANTSMITIGANTS

Established Asset ClassesEstablished Established Asset ClassesAsset Classes

Rigorous Loss ModelingRigorous Loss Rigorous Loss ModelingModeling

Structured Protection• Credit Enhancement Triggers• Servicer Termination Triggers

Structured ProtectionStructured Protection•• Credit Enhancement TriggersCredit Enhancement Triggers•• Servicer Termination TriggersServicer Termination Triggers

Large Loss CushionLarge Loss Large Loss CushionCushion

Short ExposureShort ExposureShort Exposure

Back-Up ServicerBackBack--Up Up ServicerServicer

Counterparty Track Record & Financial Strength

Counterparty Track Counterparty Track Record & Financial Record & Financial StrengthStrength

SUB-PRIME AUTO LOAN TRANSACTIONS

MBS84%

U.S. STRUCTURED FINANCE – ABS CONSUMER

SAMPLE AUTO POOL

0%

10%

25%

1 Month 68 Months30 36 42

BreakevenLoss Curve

Base CaseLoss Curve

Worst Performing Vintage

FGIC’S LOSS COVERAGE PROVIDES A SUBSTANTIAL CUSHION

ABS COMMERCIALU.S. STRUCTURED FINANCE

TRIPLE-X

CREDIT ANALYSIS EXPERTISE

MBS84%

U.S. STRUCTURED FINANCE

WHAT IS TRIPLE–X INSURANCE SECURITIZATION?

ABS COMMERCIALU.S. STRUCTURED FINANCE

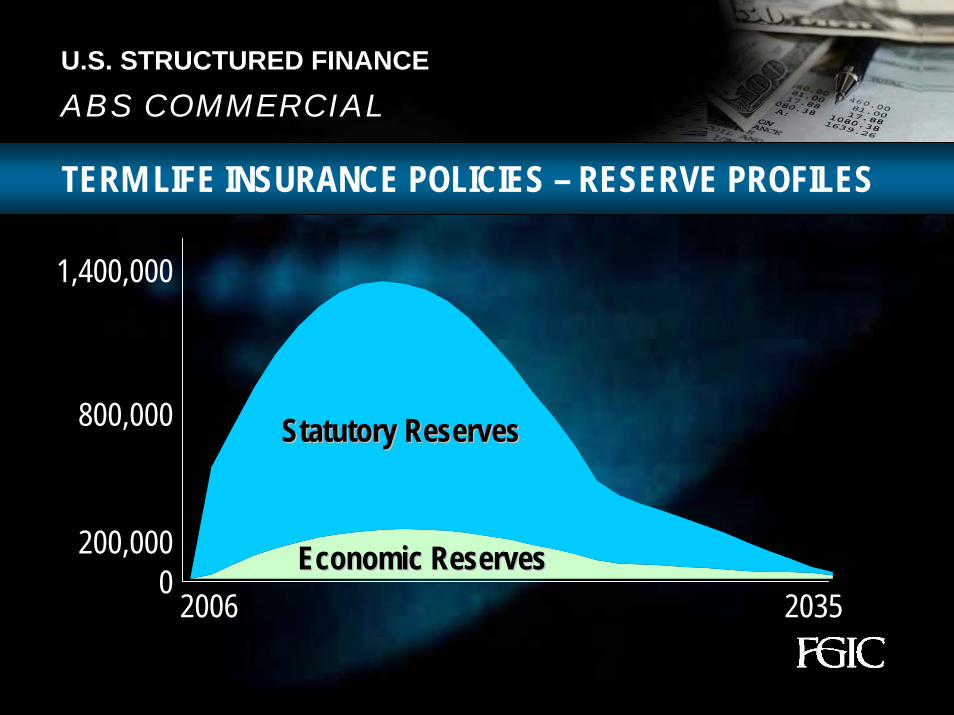

ABS COMMERCIAL

• Statutory Reserve Requirements under Regulation Triple-X Created Significant Excess Reserve Requirements for Life Companies

Standard Valuation Mortality Tables are Based on Outdated Mortality Data of the Insured Population

Do Not Adjust for Historical Mortality Improvements

Do Not Adjust for Variance in Mortality Experience Among Different Risk Classes

MBS84%

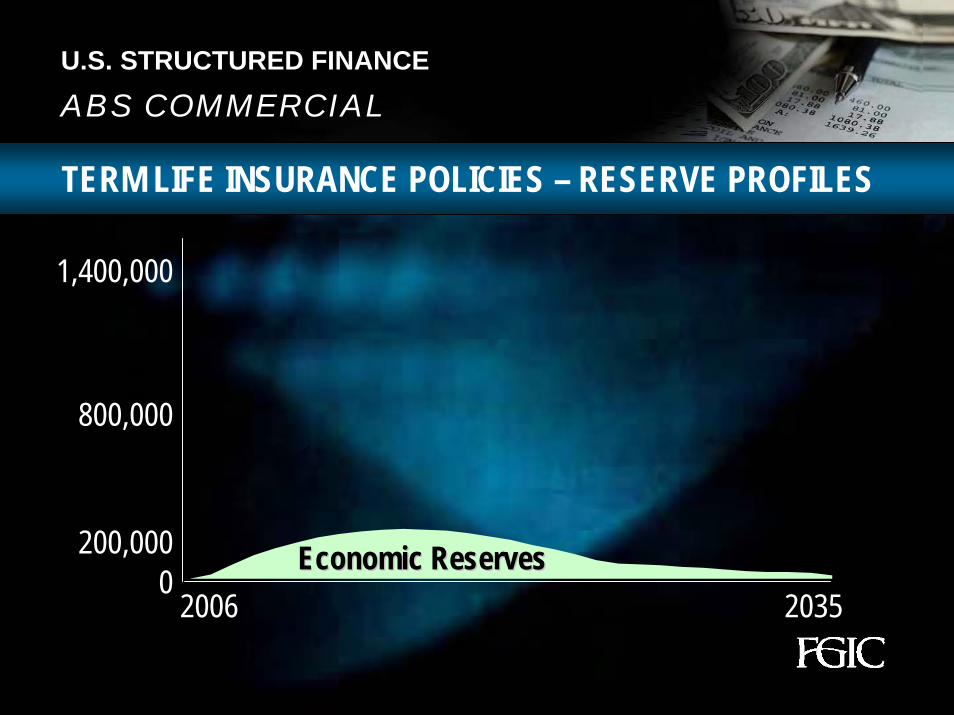

TERM LIFE INSURANCE POLICIES – RESERVE PROFILES

U.S. STRUCTURED FINANCE

ABS COMMERCIAL

2006 20350

1,400,000

800,000

200,000 Economic ReservesEconomic Reserves

MBS84%

U.S. STRUCTURED FINANCE

ABS COMMERCIAL

Statutory ReservesStatutory Reserves

Economic ReservesEconomic Reserves

TERM LIFE INSURANCE POLICIES – RESERVE PROFILES

0

1,400,000

800,000

200,000

2006 2035

MBS84%

U.S. STRUCTURED FINANCE - COMMERCIAL

CREDIT ANALYSIS EXPERTISE

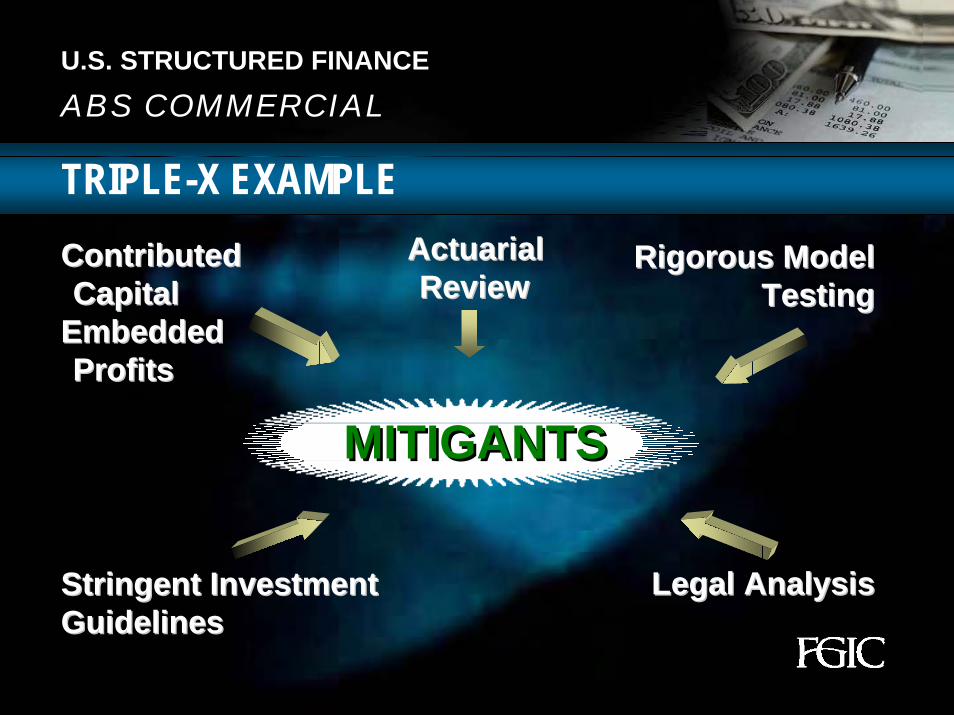

TRIPLE-X EXAMPLE

RISKSRISKS

MortalityMortalityMortality UnderwritingUnderwritingUnderwriting

AssetAssetAsset InsolvencyInsolvencyInsolvency

LapseLapseLapse

MBS84%

U.S. STRUCTURED FINANCE

ABS COMMERCIAL

MITIGANTSMITIGANTS

Contributed Contributed CapitalCapital

Embedded Embedded ProfitsProfits

Actuarial Actuarial ReviewReview

Rigorous Model Rigorous Model TestingTesting

Legal AnalysisLegal AnalysisStringent Investment Stringent Investment GuidelinesGuidelines

TRIPLE-X EXAMPLE

MBS84%

WHERE WE’RE GOING

CONTINUED EXPANSION AS INDUSTRY LEADERS

U.S. STRUCTURED FINANCE

• Balance Opportunities with Prudent Risk Taking

• Drive Business through Expertise, Execution and Relationships

• Continue to Diversify for Effective Capital Allocation

Thomas J. Adams, Senior Managing Director

Thomas J. Adams, Senior Managing Director, leads FGIC's Consumer Asset-Backed Securities Group. Before joining FGIC, Mr. Adams was a Managing Director at Ambac responsible for Mortgage-Backed Securities and mortgage-related collateral. Prior to that, he worked at Moody's Investors Service in the Asset-Backed Securities Group and in the Residential Mortgage-Backed Security Group. Until 1992 Mr. Adams worked in the Structured Finance Group of Thacher Proffitt & Wood. He holds a BA from Colgate University and a JD from Fordham University School of Law.

Kenneth L. Degen, Managing [email protected]

Ken Degen joined FGIC in May 2004, and he is the head of the Commercial Asset-Backed Group. In this role he is responsible for all commercial asset transactions, including aviation, operating and leasing securitizations, as well as all financial institution products. Prior to joining FGIC, Mr. Degen spent 14 years with the bond insurer MBIA where he was responsible for insuring more than $12 billion in asset-backed transactions. He has been involved in the securitization of numerous asset classes including residential mortgages, rail stock, shipping containers and other corporate assets. Mr. Degen also has seven years experience at Standard & Poor’s. He has a BS from Temple University and an MPA from Syracuse University Maxwell School.

SURVEILLING RISK

A. Edward Turi, III, Senior Vice President and General Counsel

SURVEILLING RISK

RISK CLIMATE

WHY SURVEILLANCE?

“Housing Market Cools”

“Got Downgraded”

“Hurricane Hits New Orleans”

“Will Interest Rates Continue to Rise?”

“Medicare Reform Introduced”

DEVELOPMENTS

• Since 12/03, FGIC’s Business Has Grown Significantly

Insured Portfolio Up 40%Substantial Increase in New Sectors / Countries

• Surveillance Department is Growing and Changing to Meet These Demands

• And Will Continue to Adapt with FGIC’s Growth and Diversification

SURVEILLING RISK

CORE SURVEILLANCE RESPONSIBILITIES

• Credit Monitoring

• Remediation of Impaired Credits

• Portfolio Risk Assessments

PROACTIVE MONITORING LEADS TO EARLY DETECTION AND FACILITATES LOSS PREVENTION

SURVEILLING RISK

OPERATING MODEL

INTEGRATED PROCESS HELPS MAINTAIN FGIC’S HIGH QUALITYINSURED PORTFOLIO

SURVEILLING RISK

UnderwritingUnderwriting

SurveillanceSurveillance

Credit, Legal, Structural Analyses

Performance Assessments

Lessons Learned and Reinforced

STRONG, EXPERIENCED TEAM IS CRITICAL TO SURVEILLANCE QUALITY

SURVEILLANCE INFRASTRUCTURE

FRAMEWORK FOR HIGH QUALITY PORTFOLIO MONITORING

• Implemented Surveillance Policies / Procedures for New Sectors

• Developed Risk Management DatabaseAutomated Surveillance CalendarEnhanced Tracking of ExposuresDeal Specific Performance for ABS and CDOs

• Enhanced FGIC’s Modeling Capabilities

• Instituted Portfolio Sector Reviews

• Enhanced Oversight

SURVEILLING RISK

OVERSIGHT OF SURVEILLANCE ACTIVITIES

STRONG MANAGEMENT AND BOARD OVERSIGHT IN PLACE

FGIC’s Watch List Committee

FGIC’s Portfolio Risk Committee

The FGIC Board’s Credit and Investment Committee

• Surveillance Department Operates Independent of Underwriting and Credit Departments

• Reports to General Counsel

• Frequent, Regular Meetings

SURVEILLING RISK

HOW WE DO IT

SURVEIL TO A “NO SURPRISE” LEVEL OF OVERSIGHT

• Sign off by Managing Director, Portfolio Risk

• Calendar Reset

FullyPerforming

REGULAR SURVEILLANCE

FORMAL REVIEWSEach Transaction Monitored in Accordance with a “Risk-Adjusted” Review Schedule

• Monthly / Quarterly Performance Tracking

• Financial Database

• More Frequent Review List

• Counterparty Diligence Visits

• Rating Agency Feeds

• Market Trend Analysis

PLUS

SURVEILLING RISK

HOW WE DO IT

SURVEIL TO A “NO SURPRISE” LEVEL OF OVERSIGHT

Recommend for Watch List

Remediation Process Begins

• More Frequent and Heightened Surveillance Reviews• Proactive Remediation Efforts• Regular Review by Senior Management and Board Committee

ISSUES IDENTIFIED

SURVEILLING RISK

ImpairmentDetected

SURVEILLANCE OVERVIEW

CONSUMER ASSET–BACKED SECURITIES EXAMPLE

Monthly Surveillance

• Track Deal Performance

• Review Comparative Performance

Issuer by Vintage

Industry Comparisons

• Track Market Trends

Annual Surveillance

• Written Deal Reviews

• Issuer Financial and Performance Review

• Servicer and Issuer On-Site Due Diligences

• Cash Flow Analysis on Seasoned Transactions

• Report Market Trends

SURVEILLING RISK

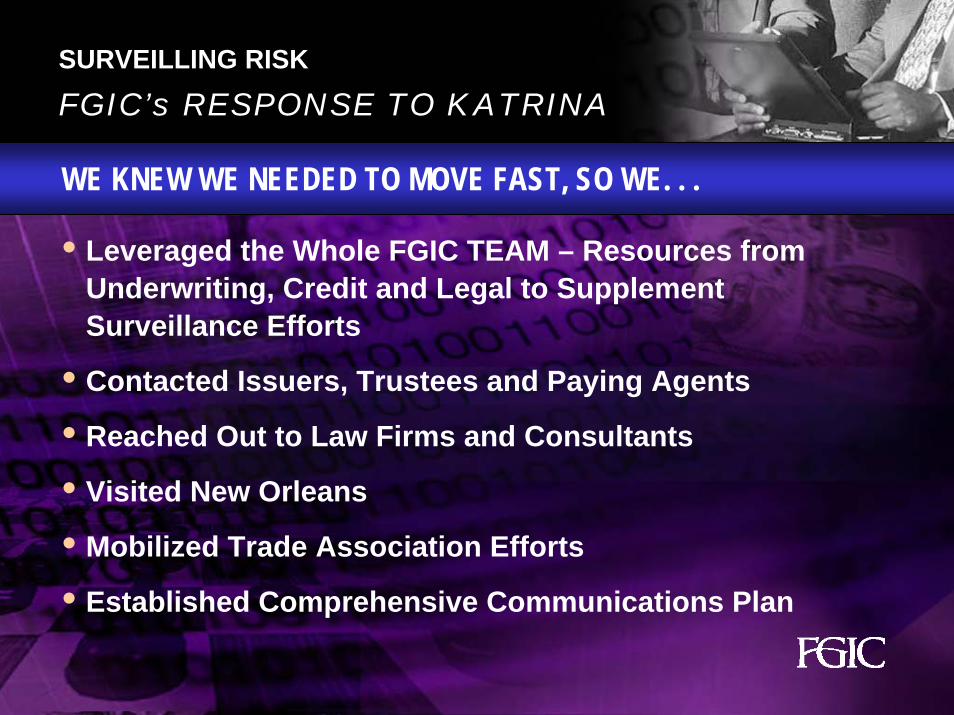

KATRINA…HOW DID WE REACT?

FGIC’s RESPONSE TO KATRINA

• Leveraged the Whole FGIC TEAM – Resources from Underwriting, Credit and Legal to Supplement Surveillance Efforts

• Contacted Issuers, Trustees and Paying Agents

• Reached Out to Law Firms and Consultants

• Visited New Orleans

• Mobilized Trade Association Efforts

• Established Comprehensive Communications Plan

WE KNEW WE NEEDED TO MOVE FAST, SO WE. . .

SURVEILLING RISK

FGIC’s RESPONSE TO KATRINA

FGIC’S PROACTIVE SURVEILLANCE EFFORTS YIELDED:

• Informed Assessments of Potential Exposure

Publicly Posted September 2005

Determined Impaired Credits

Reserves Established Where Appropriate

• Credibility with Issuers, Investors and Other Participants

Opens Up Dialogue and Information Flow

Seat at the Negotiating Table

SURVEILLING RISK

• Ability to Influence and Act Quickly on Loss Mitigation Opportunities

KATRINA EXPOSURE TODAY

• $1 Billion Par on FGIC Watch List

• Essential Services Restored

• Housing / Population Coming Back Slowly

• Remediation Efforts Continue

• Federal and State Aid Flowing

• We Are Cautiously Optimistic

SURVEILLING RISK

SURVEILLANCE GOING FORWARD

• Will Continue to Evolve to Meet FGIC’s Needs

• Will Always Play a Critical Role

• Will Provide Ongoing Value and Comfort to FGIC’s Investors

SURVEILLING RISK

A. Edward Turi, III, Senior Vice President and General [email protected]

A. Edward Turi, III, has served as General Counsel of FGIC Corporation and FGIC Insurance since September 1995. He joined FGIC in July 1991 and was Co-General Counsel from January 1992 to September 1995. Mr. Turi was an attorney at Cravath, Swaine & Moore from August 1984 until he joined FGIC. He holds a BS from Georgetown University and a JD from the University of Virginia School of Law.

MANAGING CAPITAL

Donna J. Blank, Chief Financial Officer

Managing Capital • An Integrated Approach Focused On:

Protecting a Solid Triple-A

While Maximizing Return on Capital

INTEGRATED APPROACHMANAGING CAPITAL

Deal Level “Capital Charge”

Single Obligor / Servicer Limits

•S&P Margin of Safety Cushion•Moody’s Capital Ratios Margins•Fitch Capital Model•NYSID Aggregate Insured Limits

Equity Allocated to Each Deal

Limits on Portfolio Concentrations

Overall Financial Strength Requirements

+

+

=AAA

MAINTAINING STABLE TRIPLE-AMANAGING CAPITAL

AAA

FGIC TRIPLEFGIC TRIPLE--A CAPITAL STRUCTURE DEFINED AT MULTIPLE LEVELSA CAPITAL STRUCTURE DEFINED AT MULTIPLE LEVELS

CLAIMS PAYING RESOURCESMANAGING CAPITAL

12/2003 12/2004 12/2005 6/2006

($ in Millions)

$1,835 $2,011 $2,198 $2,289

$300$300 $300$895

$1,062$1,273 $1,374

$111$192

$393$520

$300

Present Value of Installment Premiums

$4,483$4,164

$3,566$3,141

14%17%

8%

Statutory Capital

Soft Capital

Unearned Premiums and Loss & LAE

CAPITAL ADEQUACY RESULTS

Capital Adequacy TrendMANAGING CAPITAL

1.44*

1.78Moody's

Total Capital Ratio

S&P Margin of Safety

2001 2002 2003 2004 2005

1.75

1.93

1.46

1.3 - 1.4x

1.5 - 1.6x

1.3 - 1.4x 1.3 - 1.4x 1.3 - 1.4x

* Published as of 1H05

CAPITAL TO MEET TRIPLECAPITAL TO MEET TRIPLE--A CRITERIA A CRITERIA

CAPITAL PLANNINGMANAGING CAPITAL

2003 2004 2005

Total Claims Paying Resources

Capital Usage

• Net Consumer of Capital Currently

• Growth Will Reach a Level Where Returns on Capital Fund New Business Growth

BALANCE CAPITAL GENERATION WITH CAPITAL USEBALANCE CAPITAL GENERATION WITH CAPITAL USE

FOCUSED ATTENTION FROM A CORPORATE FINANCE AND BUSINESS PERSPECTFOCUSED ATTENTION FROM A CORPORATE FINANCE AND BUSINESS PERSPECTIVEIVE

HOW WE MANAGE CAPITALMANAGING CAPITAL

Critical Levers

GoalOptimize Capital Structure, Given Rating Agency Criteria

Corporate Capital Structure

Corporate Capital Structure

• Financial Leverage• Soft Capital

Utilization• Dividend Policy• Liquidity Position

Target Profitable Product Mix, While Maintaining Risk Diversity across the Insured Portfolio

Business Performance

Business Performance

• Product Mix• Sector Capital

Requirements• Expense Efficiency

HOW WE MANAGE CAPITAL: CORPORATE LEVEL

MANAGING CAPITAL

Since the Sale of FGIC in December 2003• Introduced Financial Leverage at the Holding

Company

• Introduced Market-Standard Soft Capital Facility

• Have Reinvested Capital Generated in the Business to Support New Business Growth

GOAL: OPTIMIZE CAPITAL STRUCTURE GIVEN RATING AGENCY CRITERIAGOAL: OPTIMIZE CAPITAL STRUCTURE GIVEN RATING AGENCY CRITERIA

HOW WE MANAGE CAPITAL: BUSINESS PERFORMANCE

MANAGING CAPITAL

GOAL: TARGET PROFITABLE PRODUCT MIX, MAINTAIN PORTFOLIO DIVERSITGOAL: TARGET PROFITABLE PRODUCT MIX, MAINTAIN PORTFOLIO DIVERSITYY

Since the Sale of FGIC in December 2003• Diversified the Product Mix, Notably in Areas that

Offer Attractive Risk/Return Dynamics

• Building the Scale to Achieve Improved Operating Efficiency Going Forward

2004

ACHIEVING GROWTH IN EARNINGS AND RETURNSACHIEVING GROWTH IN EARNINGS AND RETURNS

MANAGING CAPITAL

HOW WE MANAGE CAPITAL:BUSINESS PERFORMANCE

Year

-ove

r-Ye

ar E

arni

ngs

Gro

wth

’04-

1H06

Year-over-Year ROE Growth Rate

-10%

10%

15%

30%40%

-10%

2005

1H 2006

Diversification of Product Lines

Building Operating Efficiency

MANAGING CAPITAL

RETURN ON EQUITY

2004 2005 1H 2006

8.6%9.5%

11.1%

CREATING POSITIVE PROFITABILITY DYNAMIC CREATING POSITIVE PROFITABILITY DYNAMIC

MANAGING CAPITAL

• Managing Capital Efficiently is a Key Strategic Imperative for FGIC

• FGIC, as Planned, is Now a Capital Consumer

• FGIC’s Capital Structure Aligned to Support Business Growth

SUMMARY

CAPITAL PLANNING: WELL POSITIONED FOR THE FUTURE CAPITAL PLANNING: WELL POSITIONED FOR THE FUTURE

Donna Blank has served as the Chief Financial Officer of FGIC Corporation since March 2003. Ms. Blank joined FGIC in 1997, and after serving in several financial roles, is currently responsible for directing the company’s financial operations including financial reporting, financial and capital planning, accounting, treasury, and tax. She also manages the Information Technology department. Prior to joining FGIC, Ms. Blank held several management positions, including Manager of Financial Planning and Analysis for a GE insurance business unit, and Director of Budget and Planning for the Robert Plan Insurance Company. Ms. Blank received a bachelor’s degree from the University of Michigan. She holds an MBA in Finance, and a Master in International Affairs, both from Columbia University.

Donna J. Blank, Chief Financial [email protected]

MANAGING GROWTH: CREDIT, SURVEILLANCE AND CAPITAL

A FIXED-INCOME INVESTOR CONFERENCE

Presented By Financial Guaranty Insurance CompanyFriday, September 22, 2006

MANAGING GROWTH

Howard C. Pfeffer, President

ADJUSTED GROSS PREMIUM BY BUSINESS LINES 2003-2005

MANAGING GROWTH

12/0312/03 12/0412/04 12/0512/05

Public FinancePublic Finance

Structured Structured FinanceFinance

InternationalInternationalFinanceFinance

224.2224.2

49.349.3

00

371.0371.0

195.2195.2

71.771.7$ in Millions$ in Millions

•• Growth of Capital MarketsGrowth of Capital Markets

•• Niche MarketsNiche Markets

•• Convergence of Public & Structured FinanceConvergence of Public & Structured Finance

•• Exportation of Products to New MarketsExportation of Products to New Markets

•• Advancement of Existing Core MarketsAdvancement of Existing Core Markets

FUTURE GROWTH

•• New Structures, TechnologyNew Structures, Technology

•• Strategic RelationshipsStrategic Relationships

MANAGING GROWTH

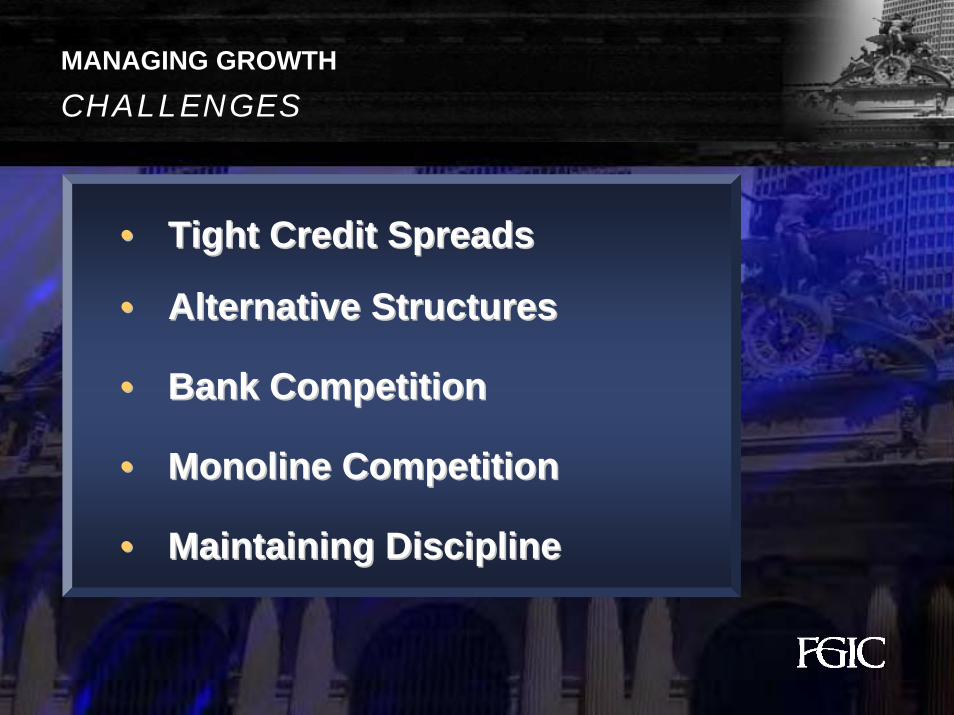

•• Tight Credit SpreadsTight Credit Spreads

•• Alternative StructuresAlternative Structures

•• Bank CompetitionBank Competition

•• Monoline CompetitionMonoline Competition

•• Maintaining DisciplineMaintaining Discipline

CHALLENGESMANAGING GROWTH

•• Disciplined Business ExpansionDisciplined Business Expansion

•• Organizational FlexibilityOrganizational Flexibility

•• Consistent Risk ManagementConsistent Risk Management

•• Superior Transaction ExecutionSuperior Transaction Execution

HOW WE WILL GROWMANAGING GROWTH

HOW WE WILL GROW

•• Exercise Risk / Return DisciplineExercise Risk / Return Discipline

•• Optimize Capital UsageOptimize Capital Usage

•• Enhance Risk DistributionEnhance Risk Distribution

•• Maintain TransparencyMaintain Transparency

MANAGING GROWTH

EVOLUTION OF A LEADER

•• Global FranchiseGlobal Franchise

•• Buyer and Seller of Credit RiskBuyer and Seller of Credit Risk

•• Diversified Insured PortfolioDiversified Insured Portfolio

•• Execution Capability in All MarketsExecution Capability in All Markets

•• Remain at Forefront of Risk ManagementRemain at Forefront of Risk Management

•• Low Risk Insured PortfolioLow Risk Insured Portfolio

•• Transparent OrganizationTransparent Organization

FGIC IN 5 YEARS

MANAGING GROWTH

Howard C. Pfeffer, [email protected]

Howard C. Pfeffer is President and a member of FGIC Corporation’s Board of Directors. He is responsible for all of FGIC’s domestic and international underwriting businesses. Mr. Pfeffer Joined FGIC in December 2003. Prior to joining FGIC, he was a Vice Chairman of Ambac Financial Group, which he joined in 1989. During his 14 years at Ambac, he had responsibility for a variety of Ambac’s businesses including Public Finance and Structured Finance. In 2003, he assumed responsibility for Ambac’s Investment Portfolio and Financial Services Group. Mr. Pfeffer was a member of Ambac’s Senior Credit Committee and Portfolio Risk Management Committee. Prior to joining Ambac, Mr. Pfeffer was a Vice President in Citicorp’s Investment Bank’s Municipal Finance Division. During his tenure at Citicorp, he specialized in innovative structured finance transactions utilizing Citibank credit and derivative products. In addition, Mr. Pfeffer was a member of Citicorp Investment Bank’s recruiting committee. He holds a Bachelor of Business Administration degree from Baruch College and completed an Executive Management Program at Stanford University.

The information contained in this presentation is of a general nature and includes forward-looking statements. Actual results may differ, and FGIC does not undertake to update the forward-looking statements or any other information contained in this presentation. This presentation is not intended to be, and should not be, relied upon for the purpose of making any investment decisions whatsoever. Under no circumstances does it constitute an offer or invitation to invest in FGIC or any securities or investments guaranteed by FGIC.

DISCLAIMER