a principal’s manual for internal accounting

TRANSCRIPT

St. Lucie County School Board

A Principal’s Manual for Internal

St. Lucie County School Board

A Principal’s Manual for Internal Accounting

A Principal’s Manual for Internal

A Principal’s Manual for Internal Accounting Page i

About this manual

This internal account manual is to be used as a training manual and as a reference manual.

For questions, comments, changes, and additions regarding this manual, please contact:

Sharon L. Bell Senior Accountant

Finance/Business Services 7724293989

This manual was first approved by the St. Lucie County School Board on January 23, 2007. The latest updated manual was Board approved on January 25, 2011.

A Principal’s Manual for Internal Accounting Page ii

Contents

Daily Procedures for Internal Accounts ........................................................................... 1

Month End Procedures for Internal Accounts .................................................................. 1

Year End Procedures for Internal Accounts .................................................................... 1

Adding an Account .......................................................................................................... 2

Bank Reconciliation Steps ............................................................................................... 6

Bank Reconciliation Tips ............................................................................................... 16

Charges for Bank Supplies ............................................................................................ 20

Charitable Contributions ................................................................................................ 21

Checks .......................................................................................................................... 22

Deposits ........................................................................................................................ 25

How to Access Skydocs (the Skyward help tutorials) .................................................... 28

Locating SLCSB Policies ............................................................................................... 33

Lost Textbook Funds ..................................................................................................... 36

Monthly Report Submission .......................................................................................... 37

Outstanding Manatee Accounting Checks .................................................................... 38

Sample letter ............................................................................................................. 39

Outstanding/Stale Dated Checks .................................................................................. 40

Sample 90 day letter .................................................................................................. 41

Sample 150 day letter ................................................................................................ 41

Principal’s Report .......................................................................................................... 42

Retention of Records ..................................................................................................... 46

Sales Tax Guidance ...................................................................................................... 47

Void Checks .................................................................................................................. 48

Worthless Checks ......................................................................................................... 50

A Principal’s Manual for Internal Accounting Page 1

Daily Procedures for Internal Accounts 1. Receive cash collections. 2. Add and post cash receipts on Skyward. 3. Complete bank deposits slips. 4. Receive check requests/requisitions. 5. Add and post checks on Skyward.

Month End Procedures for Internal Accounts 1. Reconcile the bank statement. 2. Print the principal’s report. 3. Submit copies of the bank statement, signed and dated bank reconciliation

report, and signed and dated principal’s report to the district accounting department.

Year End Procedures for Internal Accounts 1. Record the year end transfers. At the end of the year, all accounts that do not

carry over to the next year are closed and the funds are transferred out. See page 75 of the Redbook, 2.3 (f) (1).

2. Send a check to the district office for the balance in the lost textbook account. 3. Reconcile the bank statement. 4. Print the principal’s report. 5. Submit the following reports to the district accounting office:

a. Copy of June bank statement. b. Copy of signed and dated June bank reconciliation report. c. Copy of the signed and dated June 2009 principal's report. d. Any outstanding accounts receivable. e. Any outstanding accounts payable. f. Any amounts due to or due from School Board (District). g. Year end inventory(ies).

A Principal’s Manual for Internal Accounting Page 2

Adding an Account 1. All internal account numbers begin with “8”. The second number in an account

number is determined by the purpose and type of account, using page 710 of the Redbook for guidance. For example a trust account number would begin with “86” (86xxx). In addition, there are account numbers reserved for specific purposes, as follows:

Project Number Project Description Project Number Project Description 81020 Baseball 81281 Volleyball, JV 81040 Basketball 81282 Volleyball, Varsity 81041 Basketball, Boys 81300 Wrestling 81042 Basketball, Girls 81995 Athletic Officials 81043 Basketball, JV 81996 General Athletic Operations 81060 Bowling 81997 District Reimbursement 81080 Cheerleaders 81998 Athlete Processing Fees 81081 Cheerleaders, JV 81999 Athletic Gate Receipts 81082 Cheerleaders, Varsity 82020 Band 81100 Cross Country 82040 Chorus 81120 Football 82060 Music 81121 Football, Varsity 84020 National Honor Society 81140 Golf 84040 National Jr. Honor Society 81141 Golf, Boys 84060 Safety Patrol 81142 Golf, Girls 84080 Student Council 81160 PE Uniforms 85020 Guidance 81180 Soccer 85040 Library 81181 Soccer, Boys 85060 Newspaper 81182 Soccer, Girls 85080 Yearbook 81184 Soccer, JV Girls 86020 Lost Textbooks 81200 Softball 86040 PTO 81220 Swimming 86060 Stale Dated Checks 81240 Tennis 86080 United Way 81241 Tennis, Boys 86099 QZAB 81242 Tennis, Girls 87001 General Misc 81260 Track 87020 Pictures 81261 Track, Boys 87040 School Store 81262 Track, Girls 87060 Sunshine 81280 Volleyball 87080 Vending, Faculty/Staff 87100 Vending, Student

A Principal’s Manual for Internal Accounting Page 3

Adding an Account (continued) 2. After the account number to be added has been determined, on Skyward go to

SBAA, Chart of Accounts. Select Add Account.

A Principal’s Manual for Internal Accounting Page 4

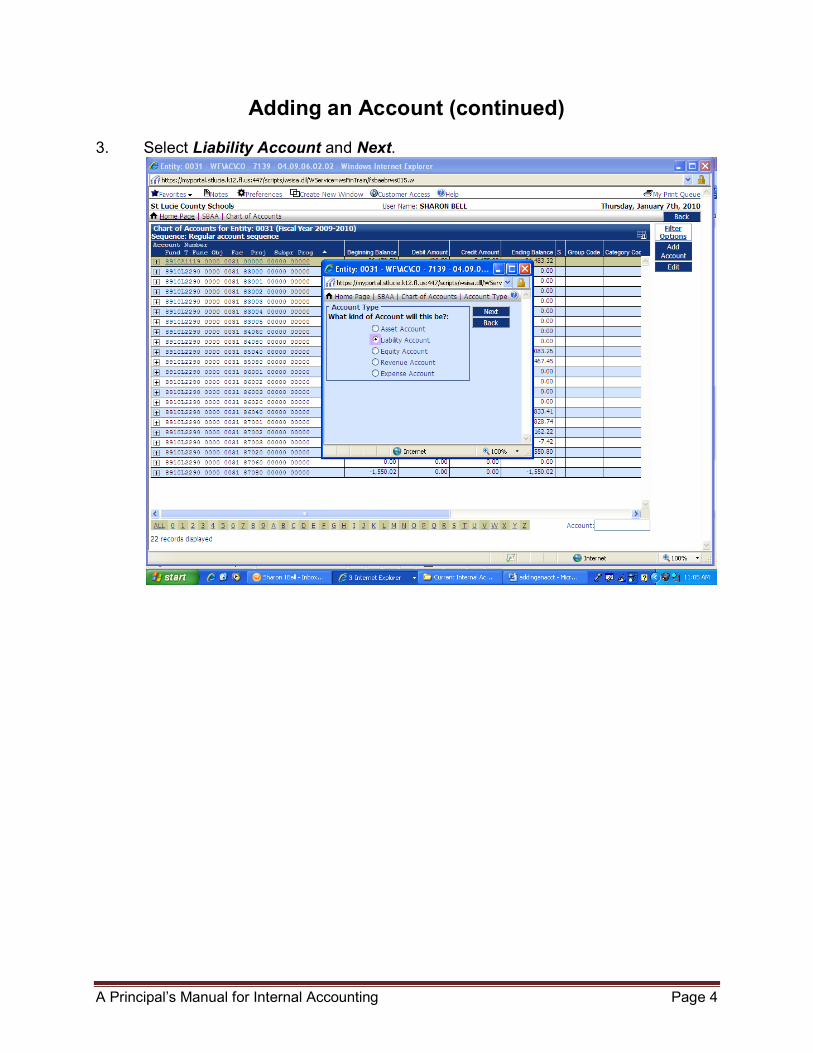

Adding an Account (continued) 3. Select Liability Account and Next.

A Principal’s Manual for Internal Accounting Page 5

Adding an Account (continued) 4. Verify that the type is “L”. Function should be 2290. Type the account number in

the Project field. Type the account title in the Acct Level Desc field. Then select Save.

A Principal’s Manual for Internal Accounting Page 6

Bank Reconciliation Steps 1. Obtain the bank statement. On Skyward, select Financial Management,

School Based Accounting, Bank Processing.

A Principal’s Manual for Internal Accounting Page 7

Bank Reconciliation Steps (continued) 2. Select Check Reconciliation.

A Principal’s Manual for Internal Accounting Page 8

Bank Reconciliation Steps (continued) 3. Select Mass Add Statement Date.

4. Change the date to the last date of the month being reconciled. Then select

Select Checks to Apply Statement Date.

A Principal’s Manual for Internal Accounting Page 9

Bank Reconciliation Steps (continued) 5. Place a check mark beside each check that has cleared the bank in the month

being reconciled. Then select Save.

6. Select Back.

A Principal’s Manual for Internal Accounting Page 10

Bank Reconciliation Steps (continued) 7. Select Bank Reconciliation.

A Principal’s Manual for Internal Accounting Page 11

Bank Reconciliation Steps (continued) 8. Select Add.

A Principal’s Manual for Internal Accounting Page 12

Bank Reconciliation Steps (continued) 9. Enter the last date of the month being reconciled and the ending balance as

shown on the bank statement. Then select Continue. Next select Calculate Amounts.

A Principal’s Manual for Internal Accounting Page 13

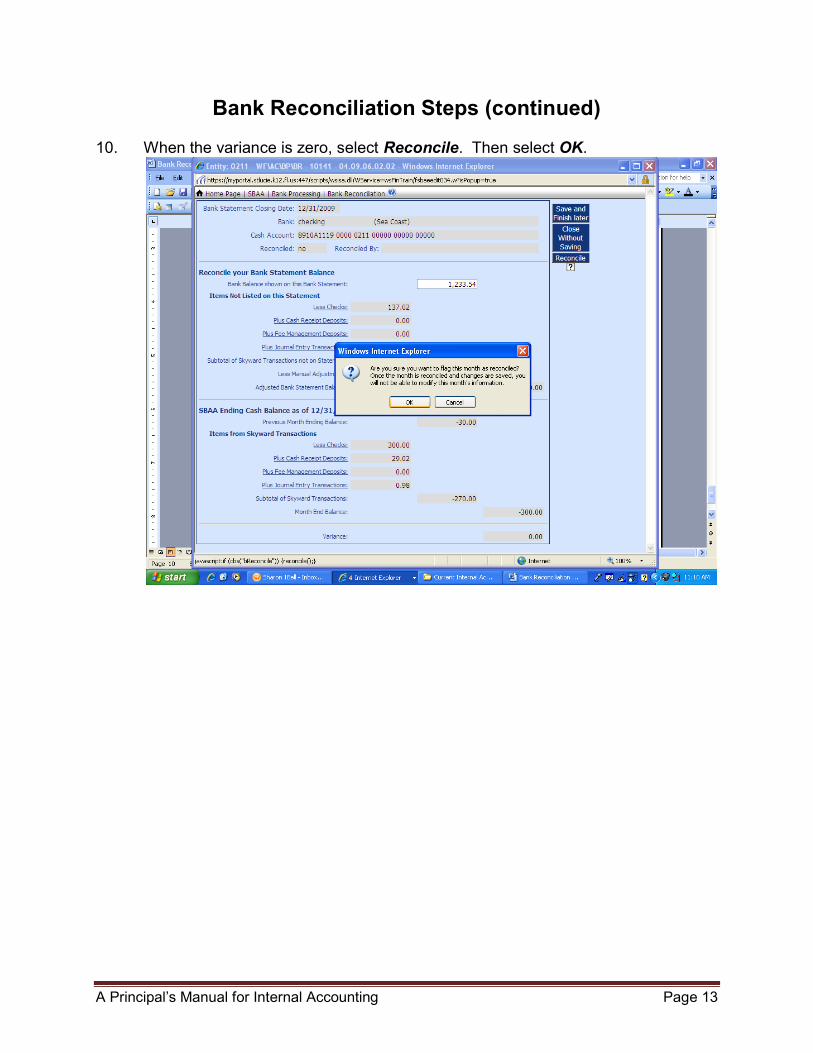

Bank Reconciliation Steps (continued) 10. When the variance is zero, select Reconcile. Then select OK.

A Principal’s Manual for Internal Accounting Page 14

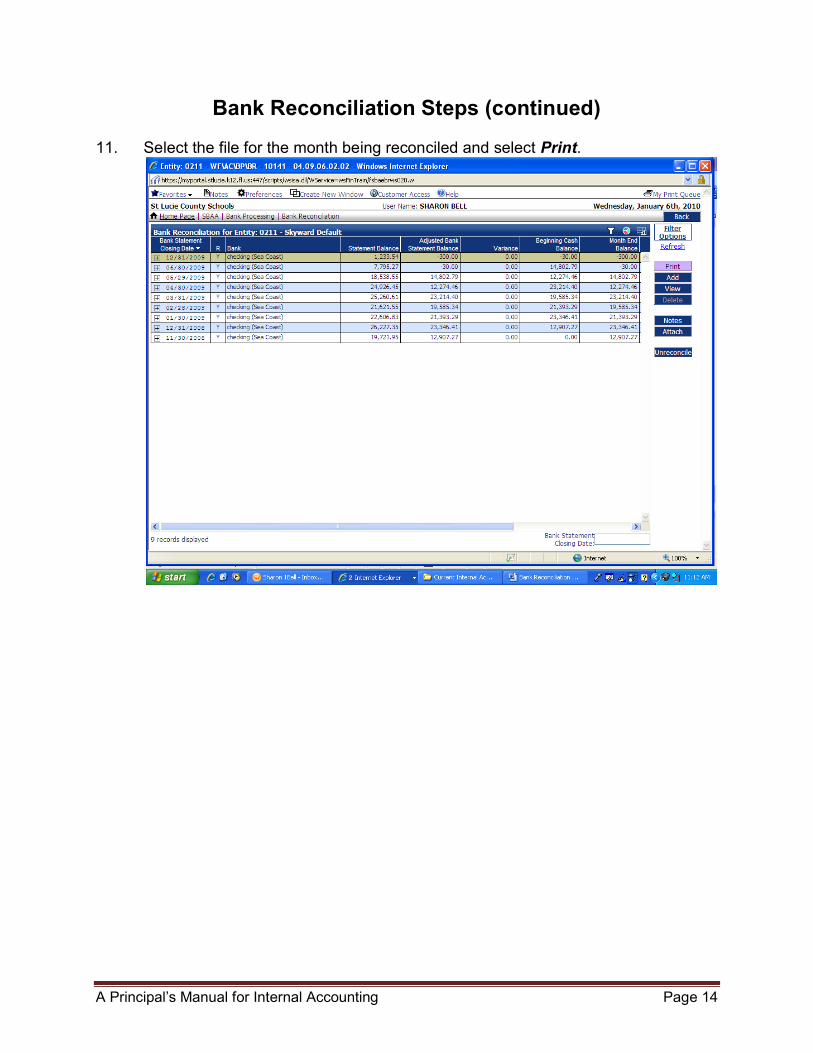

Bank Reconciliation Steps (continued) 11. Select the file for the month being reconciled and select Print.

A Principal’s Manual for Internal Accounting Page 15

Bank Reconciliation Steps (continued) 12. Select Detail, Transactions not on Bank Statement.

13. Print the bank reconciliation report on paper. Sign and date and have the

principal sign and date. Send a copy to Sharon Bell along with a copy of the bank statement and principal’s report. For more information, see Monthly Report Submission.

A Principal’s Manual for Internal Accounting Page 16

Bank Reconciliation Tips If the monthly bank reconciliation report is out of balance, follow these tips: 1. Look on the bank statement for any charge backs/debits (returned checks, bank

fees, etc.) and/or credits (deposit adjustments, bank fee refunds). Investigate them and create adjustments (i.e. journal entries) as necessary. Call the bank to have charges removed if they have been charged in error. (Note: The date on journal entry adjustments should be the same as the statement month being reconciled.)

2. Go to Bank Processing, Bank Reconciliation. Edit the bank reconciliation report. Click on the words Less Checks (in blue).

A Principal’s Manual for Internal Accounting Page 17

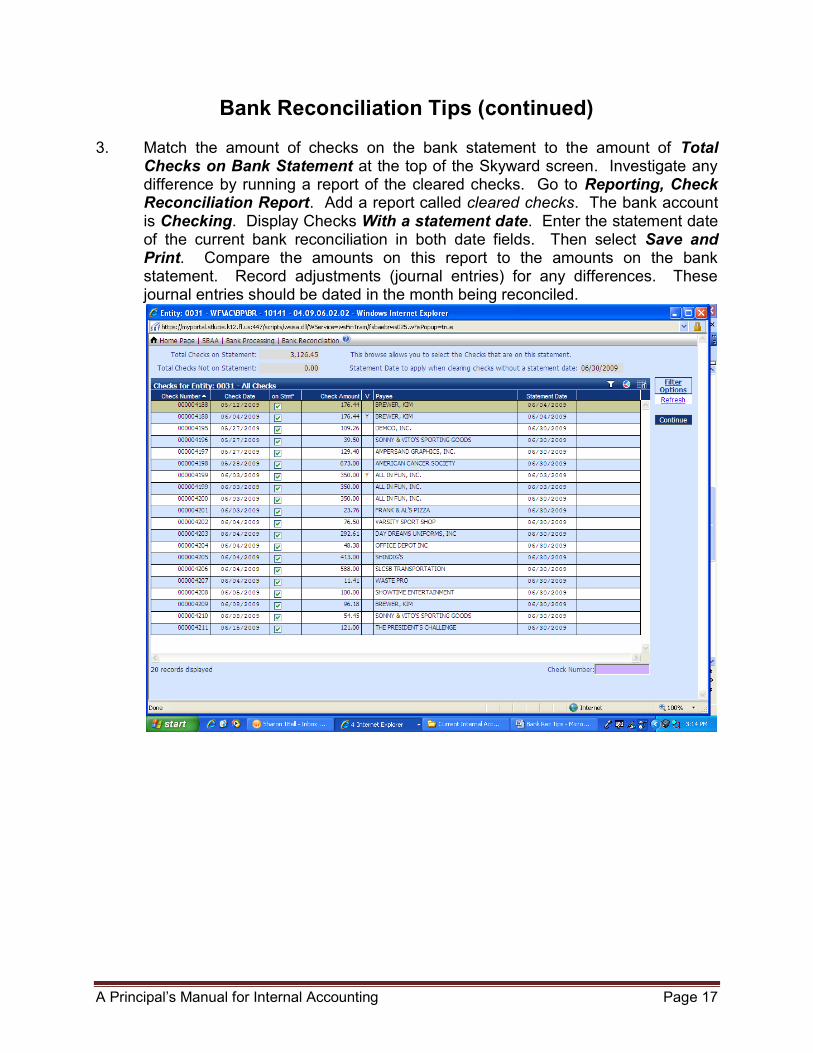

Bank Reconciliation Tips (continued) 3. Match the amount of checks on the bank statement to the amount of Total

Checks on Bank Statement at the top of the Skyward screen. Investigate any difference by running a report of the cleared checks. Go to Reporting, Check Reconciliation Report. Add a report called cleared checks. The bank account is Checking. Display Checks With a statement date. Enter the statement date of the current bank reconciliation in both date fields. Then select Save and Print. Compare the amounts on this report to the amounts on the bank statement. Record adjustments (journal entries) for any differences. These journal entries should be dated in the month being reconciled.

A Principal’s Manual for Internal Accounting Page 18

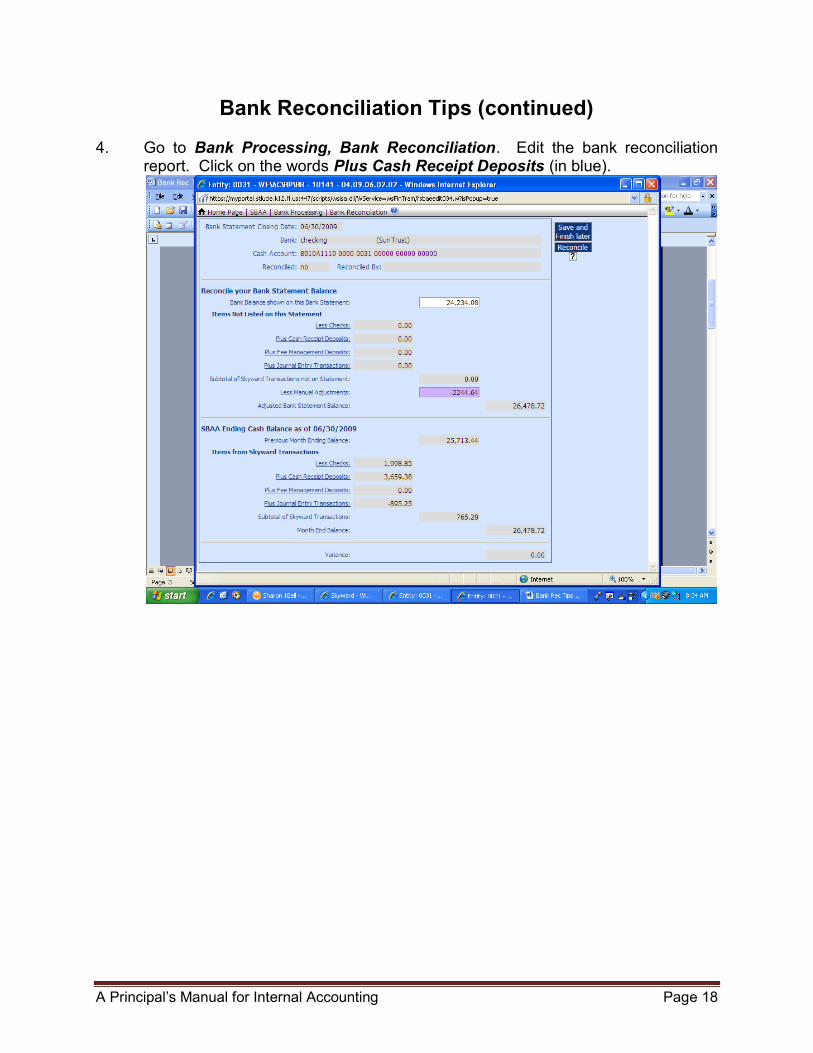

Bank Reconciliation Tips (continued) 4. Go to Bank Processing, Bank Reconciliation. Edit the bank reconciliation

report. Click on the words Plus Cash Receipt Deposits (in blue).

A Principal’s Manual for Internal Accounting Page 19

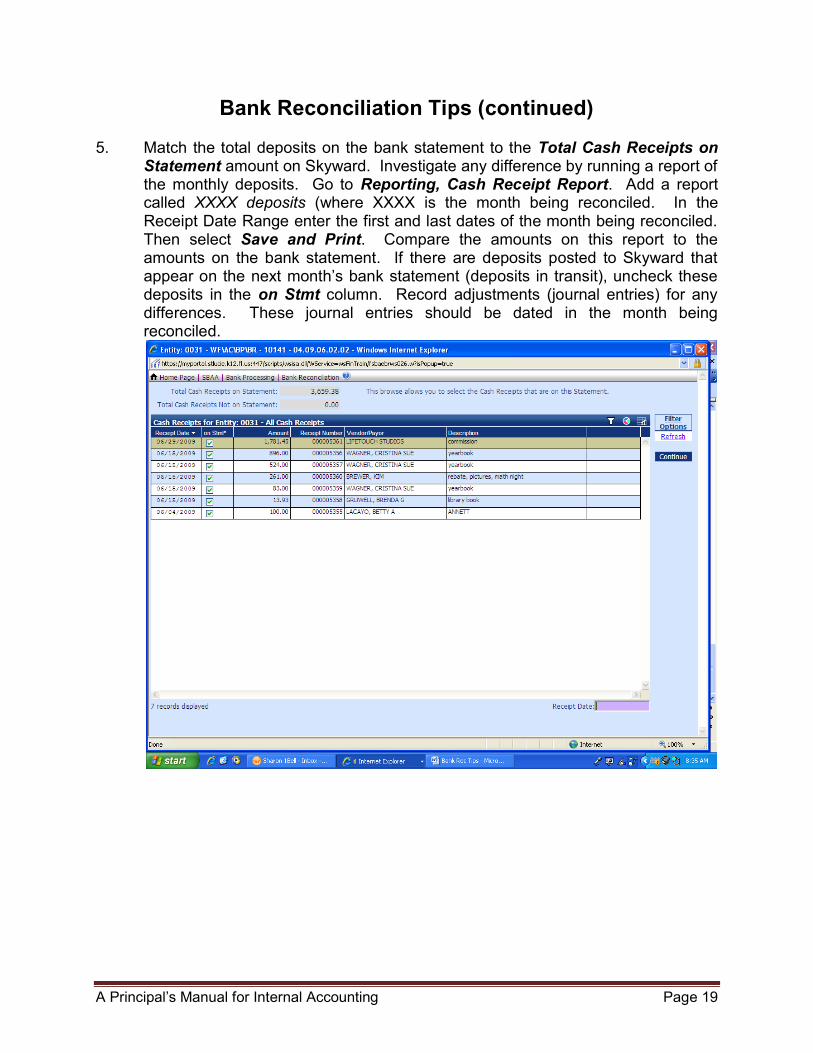

Bank Reconciliation Tips (continued) 5. Match the total deposits on the bank statement to the Total Cash Receipts on

Statement amount on Skyward. Investigate any difference by running a report of the monthly deposits. Go to Reporting, Cash Receipt Report. Add a report called XXXX deposits (where XXXX is the month being reconciled. In the Receipt Date Range enter the first and last dates of the month being reconciled. Then select Save and Print. Compare the amounts on this report to the amounts on the bank statement. If there are deposits posted to Skyward that appear on the next month’s bank statement (deposits in transit), uncheck these deposits in the on Stmt column. Record adjustments (journal entries) for any differences. These journal entries should be dated in the month being reconciled.

A Principal’s Manual for Internal Accounting Page 20

Charges for Bank Supplies

Charges for internal account bank supplies are to be charged to the general miscellaneous account, account number 87001.

A Principal’s Manual for Internal Accounting Page 21

Charitable Contributions Every time a school receives a charitable contribution (donation) of $250.00 or more, the school must issue a contemporaneous written acknowledgement. Per IRS publication 1771:

Although it is a donor’s responsibility to obtain a written acknowledgment, an organization can assist a donor by providing a timely, written statement containing the following information:

1. Name of organization (i.e. school name). 2. Amount of cash contribution. 3. Description (but not the value) of noncash contribution. 4. Description and good faith estimate of the value of goods or

services, if any, that an organization provided in return for the contribution.

It is not necessary to include either the donor’s social security number or tax identification number on the acknowledgment.

There are no IRS forms for the acknowledgment. Letters, postcards, or computergenerated forms with the above information are acceptable. An organization can provide either a paper copy of the acknowledgment to the donor, or an organization can provide the acknowledgment electronically, such as via an email addressed to the donor.

Examples of Written Acknowledgments:

• “Thank you for your cash contribution of $300 that (organization’s name) received on December 12, 2008. No goods or services were provided in exchange for your contribution.”

• “Thank you for your cash contribution of $350 that (organization’s name) received on May 6, 2008. In exchange for your contribution, we gave you a cookbook with an estimated fair market value of $60.”

• “Thank you for your contribution of a used oak baby crib and matching dresser that (organization’s name) received on March 15, 2008. No goods or services were provided in exchange for your contribution.”

A Principal’s Manual for Internal Accounting Page 22

Checks 1. Prior to issuing a check, a check requisition/request form must be completed and

signed by the principal, sponsor, and student officer. (Have the assistant principal sign as teacher/sponsor if there is no teacher/sponsor.)

2. On Skyward, select Financial Management, School Based Accounting, Check Request.

3. Select Add.

A Principal’s Manual for Internal Accounting Page 23

Checks (continued) 4. In the Check Request Information section, enter vendor name. Today’s date will

automatically fill in. 5. In the Check Request Detail Line Entry section enter the description. The

Invoice Number and Invoice Date fields are optional. Check the 1099 box if the check is issued for rents, services (including parts and materials), prizes and awards, and other income payments. Do not check the 1099 box if the check is issued for merchandise, telegrams, telephone, freight, storage, and similar items. Enter the amount of the check to be charged to the first internal account number. Enter the account number to be charged.

6. Tab to the next description field if there are more accounts to be charged and repeat step 5.

7. After all the accounts to be charged have been entered, select Assign Check Number and Print.

A Principal’s Manual for Internal Accounting Page 24

Checks (continued) 8. Double check the check number, amount, and payee information. If everything is

correct, select Process Check and Print. 9. The check shows up as a .pdf file.

10. Place the check voucher in the printer and select File, Print. 11. Have the check signed by two authorized signers.

A Principal’s Manual for Internal Accounting Page 25

Deposits 1. On Skyward, click Financial Management, School Based Accounting, Cash

Receipts.

2. Click Add to enter a new receipt.

In the Cash Receipt Information section, enter the name of the person you received the funds from as Payor and enter the Description. Today’s date will automatically fill in. In the Cash Receipt Detail Line Entry section, enter the Description and the Account in which the funds are to be deposited. The amount of the receipt is entered in the Credit Amount box. Up to ten lines can be entered for each cash receipt. When the cash receipt is complete, choose Assign Receipt Number and Print. (If the Cash Receipt is not ready to be updated to history, choose Save and Print Later.)

A Principal’s Manual for Internal Accounting Page 26

Deposits (continued) 3. Review the information for accuracy. Then select Process Receipt and Print.

4. Select Display Cash Receipt.

A Principal’s Manual for Internal Accounting Page 27

Deposits (continued) 5. When the report is complete, the cash receipt will be displayed.

6. Print the cash receipt. Sign and date the cash receipt. 7. Prepare a (duplicate) bank deposit ticket for all the day’s cash receipts. Write the

Skyward cash receipt number(s) on the deposit ticket. Write the bank bag number on the deposit slip. Place the original copy of the deposit ticket in the bank bag with the deposit and seal.

Note: A complete deposit package contains:

1. Validated deposit receipt. 2. Copy of the deposit slip, including the handwritten Skyward cash receipt

numbers and bank bag number. 3. Copies of all signed and dated cash receipts. 4. Monies collected forms (signed and dated by both parties) for all cash

receipts. Auditors will need to be able to trace money from receipt at the school through to the

bank statement.

A Principal’s Manual for Internal Accounting Page 28

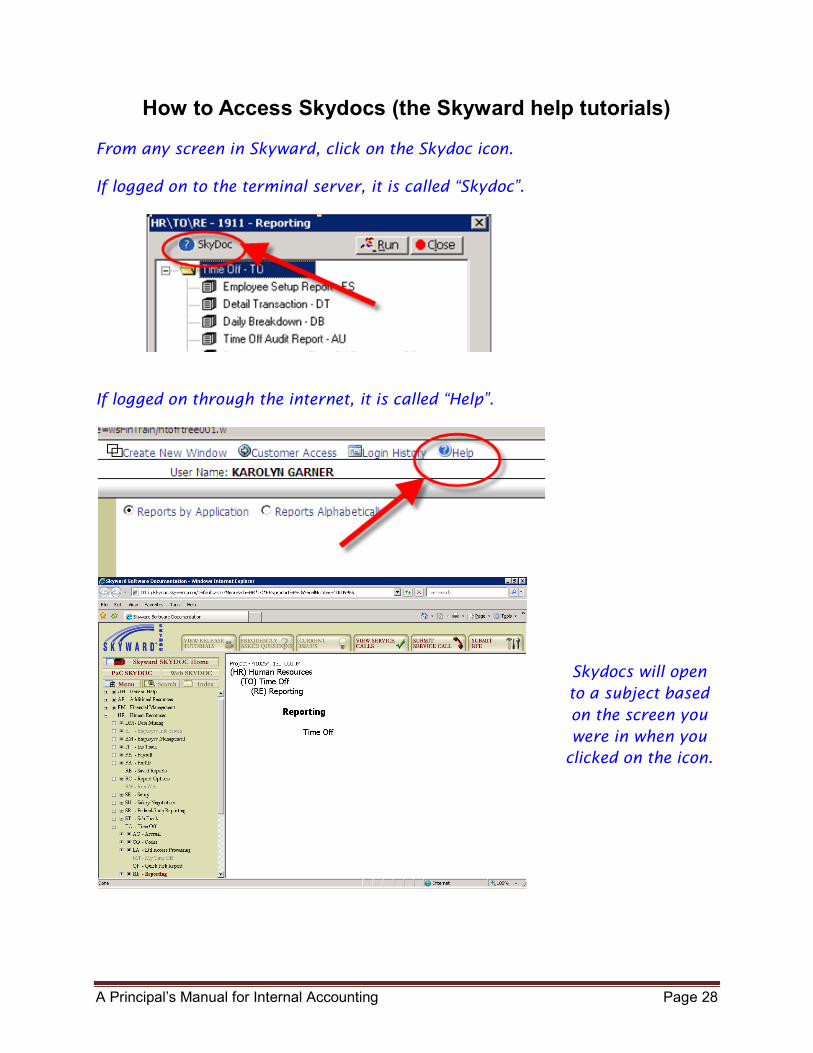

How to Access Skydocs (the Skyward help tutorials) From any screen in Skyward, click on the Skydoc icon. If logged on to the terminal server, it is called “Skydoc”.

If logged on through the internet, it is called “Help”.

Skydocs will open to a subject based on the screen you were in when you

clicked on the icon.

A Principal’s Manual for Internal Accounting Page 29

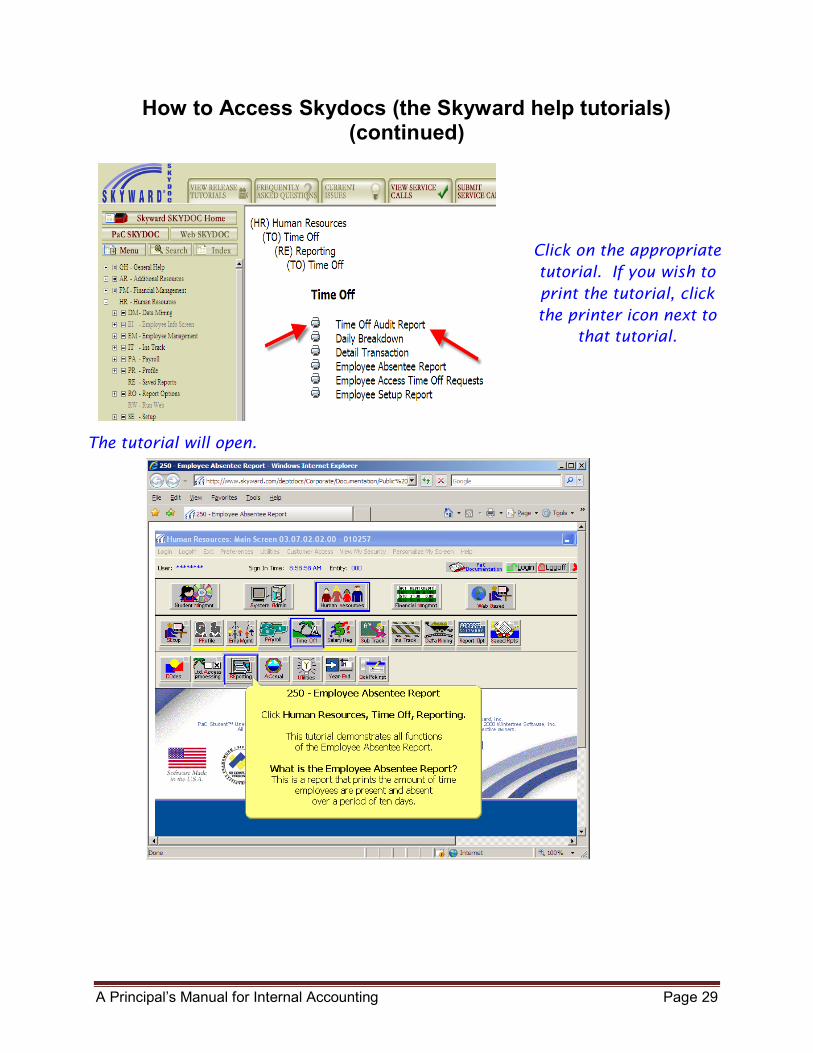

How to Access Skydocs (the Skyward help tutorials) (continued)

Click on the appropriate tutorial. If you wish to print the tutorial, click the printer icon next to

that tutorial.

The tutorial will open.

A Principal’s Manual for Internal Accounting Page 30

How to Access Skydocs (the Skyward help tutorials) (continued)

By clicking the maximize button in the top, right hand corner, you will gain access to the button controls for the

tutorial.

The tutorial moves automatically from screen to screen every 60 seconds.

You can override that and move

A Principal’s Manual for Internal Accounting Page 31

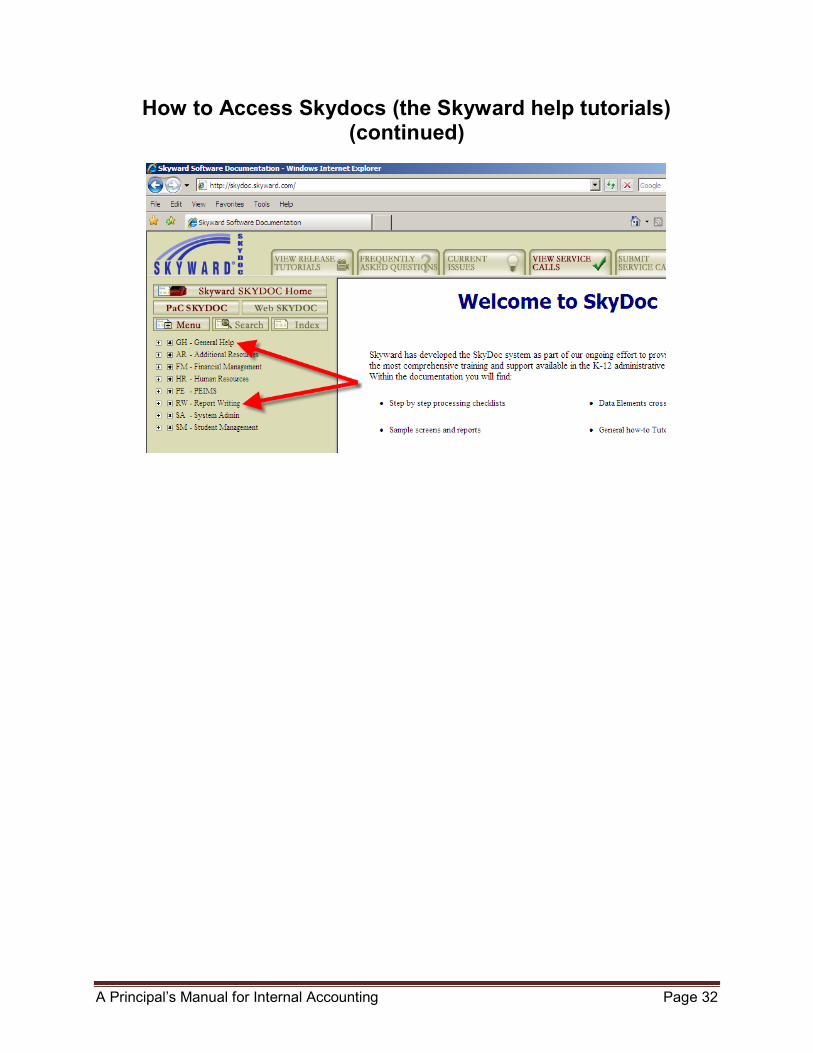

How to Access Skydocs (the Skyward help tutorials) (continued)

If you have a question on another topic, simply

click one of the subjects listed on the left of the

screen.

To access Skydocs if you are not in Skyward, simply go to Internet Explorer, type the

following on the address line, and choose a topic from the

menu on the left.

http://skydoc.skyward.com

A Principal’s Manual for Internal Accounting Page 32

How to Access Skydocs (the Skyward help tutorials) (continued)

A Principal’s Manual for Internal Accounting Page 33

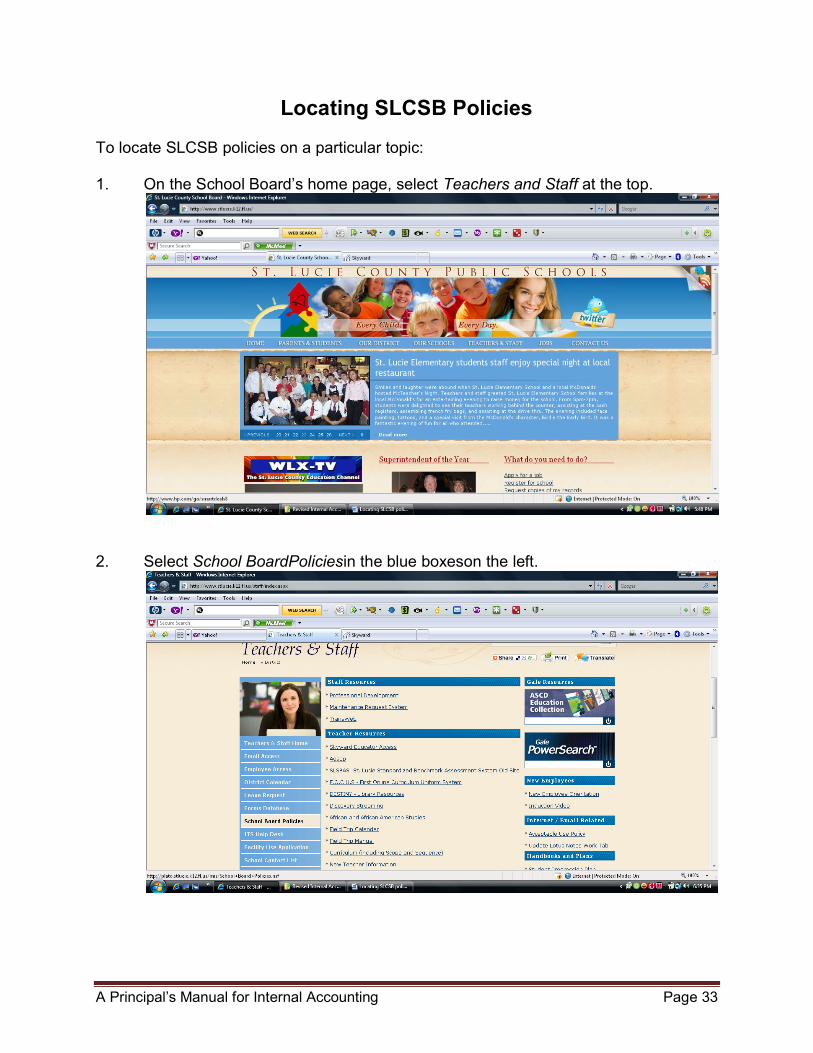

Locating SLCSB Policies To locate SLCSB policies on a particular topic: 1. On the School Board’s home page, select Teachers and Staff at the top.

2. Select School BoardPoliciesin the blue boxeson the left.

A Principal’s Manual for Internal Accounting Page 34

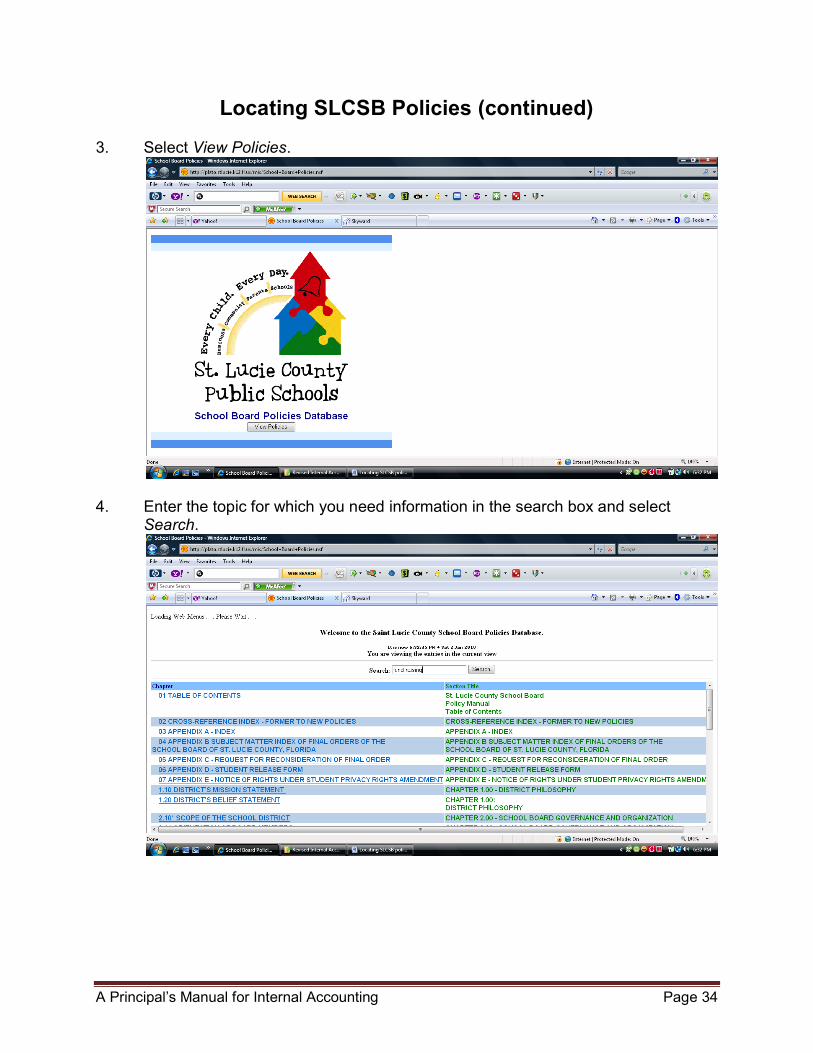

Locating SLCSB Policies (continued) 3. Select View Policies.

4. Enter the topic for which you need information in the search box and select

Search.

A Principal’s Manual for Internal Accounting Page 35

Locating SLCSB Policies (continued) 5. Select the document you want to read and/or print.

A Principal’s Manual for Internal Accounting Page 36

Lost Textbook Funds Funds collected throughout the year for lost textbooks are to be recorded in a trust fund number 86020, Lost Textbooks. At the end of the fiscal year, issue a check to SLCSB for the total balance in the lost textbook fund. Attach a note to the check explaining these are lost textbook funds. Send this check and note to Business Services.

A Principal’s Manual for Internal Accounting Page 37

Monthly Report Submission Copies of the signed and dated Principal’s (Monthly) Report, signed and dated bank reconciliation report, and bank statement are to be submitted to Sharon Bell, the internal account senior accountant in the district accounting department by the 20th of the following month. The principal’s report and the bank reconciliation report must be signed and dated by the bookkeeper/secretary and the principal.

A Principal’s Manual for Internal Accounting Page 38

Outstanding Manatee Accounting Checks First, write a letter (see sample letter) to the payee requesting that the payee contact you. Keep a copy of this letter with the backup for the check. Retain all correspondence (including any envelopes returned in the mail), with the backup for the check. After three weeks from the date you mailed the above letters and no contact from the payee, the check will need to be voided. To void a check issued from the Manatee Accounting System, a journal entry will need to be recorded on Skyward. Cash will be debited and the account that the check was written against will becredited.Next, record a transfer (journal entry) in the amount of the check from the accountthat the check had been written against into the Stale Dated Checks account, 86060. The account that the check was written against will be debited and the Stale Dated Checks account, 86060 will be credited. Keep a separate file folder for all stale dated checks (and their backup, including any correspondence). The balance in the Stale Dated Checks account should equal the total amount of the checks in the folder. Retain all stale dated check information for inclusion in the St. Lucie County School Board unclaimed property report. The senior accountant responsible for filing the state unclaimed property report will request stale check information from the schools annually. When the stale check information is requested, issue a check to SLCSB and send this check with the stale check folder to the senior accountant in Accounting.

A Principal’s Manual for Internal Accounting Page 39

Outstanding Manatee Accounting Checks (continued)

Sample letter Date Payee 123 Any Street Any Town, State 12345 Dear Payee, Our records indicate that school name issued check number xxx in the amount of $xx.xx dated xx/xx/xx.This check is now stale dated. Please contact me as soon as possible so that a replacement check can be issued. Thank you, Your Name Your school address Your school phone number

A Principal’s Manual for Internal Accounting Page 40

Outstanding/Stale Dated Checks After the monthly bank reconciliation has been completed, review the outstanding checks. For checks over 90 days old, write a letter (see sample 90 day letter) to the payee requesting that the check be cashed. Keep a copy of this letter with the backup for the check. If necessary, send a followup letter (see sample 150 day letter) when a check is 150 days (five months) old. Retain all correspondence (including any envelopes returned in the mail), with the backup for the check. When an uncashedcheck is six months old, it is stale dated. First, void the check. Second, record a transfer (journal entry) in the amount of the check from the accountthat the check had been written against into the Stale Dated Checks account, 86060. The account that the check was written against will be debited and the Stale Dated Checks account, 86060 will be credited. Keep a separate file folder for all stale dated checks (and their backup, including any correspondence). The balance in the Stale Dated Checks account should equal the total amount of the checks in the folder. Retain all stale dated check information for inclusion in the St. Lucie County School Board unclaimed property report. The senior accountant responsible for filing the state unclaimed property report will request stale check information from the schools annually. When the stale check information is requested, issue a check to SLCSB and send this check with the stale check folder to the senior accountant in Accounting.

A Principal’s Manual for Internal Accounting Page 41

Outstanding/Stale Dated Checks (continued) Sample 90 day letter Date Payee 123 Any Street Any Town, State 12345 Dear Payee, Our records indicate that school name issued check number xxx in the amount of $xx.xx dated xx/xx/xx. Please cash this check as soon as possible. If you have any questions, please contact me. Thank you, Your Name Your school address Your school phone number

Sample 150 day letter Date Payee 123 Any Street Any Town, State 12345

Second Notice Dear Payee, Our records indicate that school name issued check number xxx in the amount of $xx.xx dated xx/xx/xx. Please cash this check by xx/xx/xx. If you have any questions, please contact me. Thank you, Your Name Your school address Your school phone number

A Principal’s Manual for Internal Accounting Page 42

Principal’s Report After the monthly bank reconciliation has been completed and reconciled, run the principal’s report for that month. Sign and date the report. Have the principal review, sign, and date the report. Retain the original principal’s report at the school. Send a copy of the signed and dated principal’s report to (along with copies of the signed and dated bank reconciliation and bank statement) to Sharon Bell in Accounting/Finance by the 20th of the subsequent month.

How to Run Principal’s Report from PAC From Skyward PAC (To get to Skyward PAC you use yourSkyapps link to the remote

desktop): 1. Click on Financial Management. 2. On the second level, click on Account Management. 3. On the third level, click on Reporting.

4. On the Reporting Screen, under Balance Sheet – BS, choose Summary – SU

and click on Run.

A Principal’s Manual for Internal Accounting Page 43

Principal’s Report (continued)

5. On the Summary screen, check “View All Reports” at the top of the screen. Click

on the plus (+) next to Sharon Lynn Bell so that you can see the reports under her name and choose “User SBAA principals report”.

A Principal’s Manual for Internal Accounting Page 44

Principal’s Report (continued)

6. Click Run to begin running the reports. 7. This brings up the Run screen. On the left, choose the month and year for which

you want to run the report under “Select Reporting Month”.

A Principal’s Manual for Internal Accounting Page 45

Principal’s Report (continued) 8. Click Print which will bring up the Output Destination Screen. Leave all default

settings, but confirm that Output is set to “Screen” and click Ok to finally process/view the report.

9. When the Output Destination screen closes it will take you back to the Run

screen. The report will be queued to run. It takes a few seconds, but the report will come up. (Note: You may not see a message/hour glass until just before the report opens.)

10. Print out the report on paper and draw two lines, one for the Principal’s signature and dateand the other for the Preparer’s signature and date.

A Principal’s Manual for Internal Accounting Page 46

Retention of Records Section III, 4.5 Retention of Records, of Chapter 7 of the red book states that: Chapters 119 and 267, F.S., provide that public records may not be mutilated, destroyed, sold, loaned, or otherwise disposed of without the consent of the Bureau of Records and Information Management of the Department of State. All SLCSB district and school records destruction requests must be submitted to Lisa Huff. She can also provide assistance. These instructions are from Lisa Huff, record specialist: There is a Record Disposition form on our website that schools need to fill out before destroying anything. Each record up for disposition has an individual item number. There are two general record schedules that can be found on the state website: GS7 and GS1L. General Record Schedules can be viewed or copied from the following website: http://dlis.dos.state.fl.us/barm Select the Records Managers tab. Next, on the left, click on General Records Schedules. Scroll down until you locate GS7 or GS1L. Select PDF (GS7 or GS1SL). A document link of Record Disposition can be sent to Lotus notes database if school does not have it. Their schedules are also on this link. The one for the state has the descriptions under each title and item number. The General Record schedule on Lotus notes breaks it down per item number/retention. Once the form has been filled out, it is up to the school to destroy the information. They are several ways of destruction: shredding, incineration or dumpster. We usually contact the school maintenance department to destroy boxes and they take them to the land fill. Any questions or concerns you may contact me. Lisa Huff Record Specialist (772) 4295543 (772) 4295542 fax

A Principal’s Manual for Internal Accounting Page 47

Sales Tax Guidance The general rule for payment of sales tax is that all expenditures from internal accounts made for customary instructional activities and that do not represent expenditures for resale to individuals, including students and the general public, are exempt from sales tax. See Florida Administrative Code 12A1.0011 for guidance. So if items are purchased to resell, they are subject to tax. Any items used in fundraising events such as festivals and games, including prizes, are taxable. Sales of school materials and supplies are taxable regardless of by whom sold; however, for the sake of convenience, schools grades K through 12 and their respective PTAs or PTOs have been granted the privilege of paying tax to their suppliers on school materials and supplies that they purchase for resale to students and the tax is passed on to the student as part of the selling price (i.e. bookstore). Tangible personal property sold outright or rented through the school to students is subject to tax based on delivered cost to the school or on the amount charged the student upon sale or rental. Student photographs, candies, confections, and novelties sold to students or the public for fundraising purposes come within this rule. The sale of schoolbooks, including printed textbooks and workbooks, containing printed instructional material, and questions and answers for school purposes used in regularly prescribed courses of study in public, parochial, or nonprofit private schools grades K through 12 are exempt. The sale of yearbooks, magazines, newspapers, directories, bulletins, and similar publications distributed by schools offering grades K through 12 is exempt. Sales of Food and Beverages a) Food and beverages sold or dispensed through vending machines or other

dispensing devices located in the student lunchroom, student dining room, or other area designated for student dining in schools offering grades K through 12 are exempt.

b) Food and beverages sold through vending machines or other dispensing devices

located in a gymnasium, shop, teachers’ lounge, corridor, or other area accessible to the general public and not specifically designated for student dining are subject to tax at the rates established in Section 212.0515(2), F.S.

Vending Machine Sales Commissions Commissions paid to the schools by vending machine companies are subject to sales tax per Florida Administrative Code 12A1.044(5c). Recommendation When a contract is being written (i.e. for vending machine sales, school pictures, etc.), the contract should contain a statement that the vendor is responsible for paying sales tax. If the contract is silent, the school is liable for paying sales tax.

A Principal’s Manual for Internal Accounting Page 48

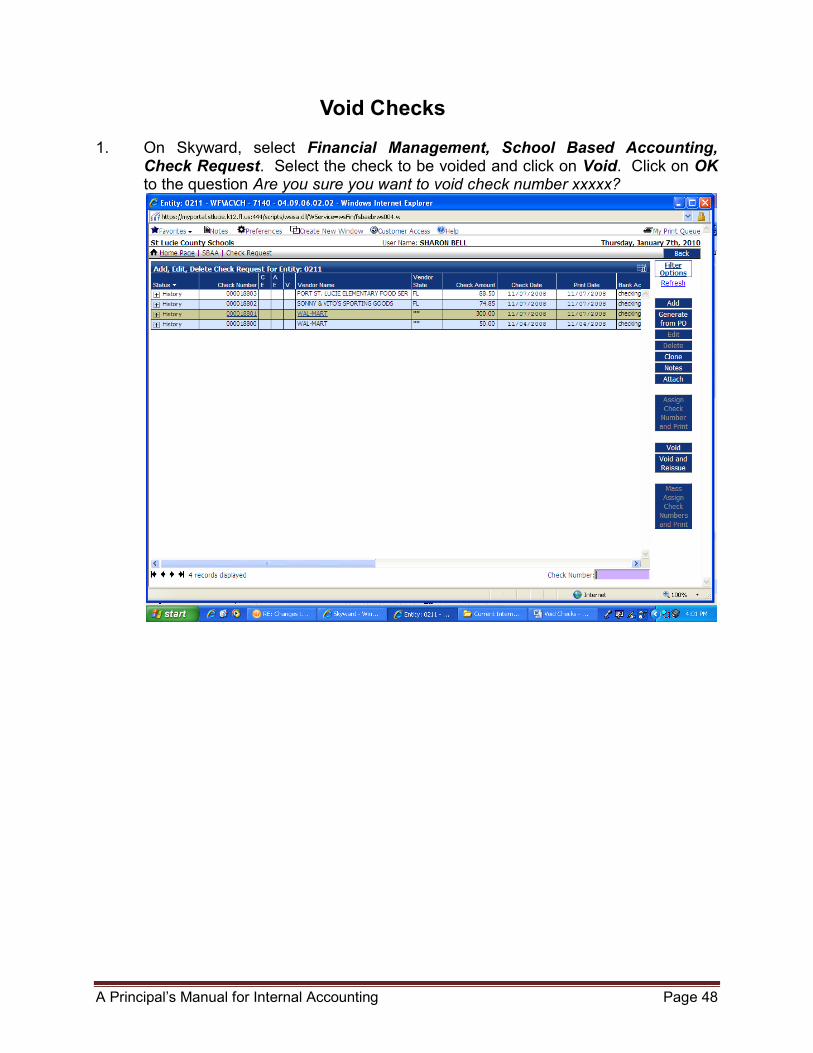

Void Checks 1. On Skyward, select Financial Management, School Based Accounting,

Check Request. Select the check to be voided and click on Void. Click on OK to the question Are you sure you want to void check number xxxxx?

A Principal’s Manual for Internal Accounting Page 49

Void Checks (continued) 2. Click on Process Check and Print. Then select Display Check and Open.

3. The pdf file of the voided check will open. Close the pdf file. Click on Check

Printing Complete – Press to Close. 4. On the paper check write VOID across the face of the check. Remove the area

where the signatures are written.

A Principal’s Manual for Internal Accounting Page 50

Worthless Checks Unpaid checks returned by the bank must be handled in a timely manner. 1. According to the Redbook, Section III, 1.6 Collections of Worthless Checks:

a. The principal is responsible for seeking reimbursement for any unpaid check returned by the bank.

b. A check can be declared uncollectible and written off the books only by action of the school board or designated officer (i.e. school principal). This action will be taken only after every legal and reasonable effort at collection by the principal has been exhausted.

c. The school principal may require payment for school obligations in cash, money order, or other form of guaranteed payment if it is deemed necessary.

2. For a check to be declared uncollectible, district procedures must be followed: a. Run a returned check through the bank a second time. b. If the check is returned a second time, contact the maker of the check to

attempt collection. Retain written documentation of attempts to collect the funds.

c. If unable to collect after all reasonable efforts have been attempted, write off the check as uncollectible.

Important: After a returned check has been returned the second time and cannot be redeposited, record an adjustment to subtract the check amount from cash account 1119, Internal Account Cash and the account to which it was originally deposited. Do not use a separate cash account for NSF checks. Although the check has been subtracted from the accounts, you can still attempt to collect the funds. Another option for handling returned checks is to use Payliance, a check collection service. There is no charge for this service. For more information contact Suzette Daggett, Sr. Merchant Services Representative:

[email protected] 251.653.0224 office

866.745.9517 toll free 251.653.1775 fax