acacia mining plc · profit forecast or estimate and no statement made should ... bank of america...

TRANSCRIPT

Acacia Mining plc

Bank of America Merrill Lynch

Global Metals and Mining

Conference

May 2017

Important Notice

This presentation includes “forward-looking statements” that express or imply expectations of future events or results as opposed to historical facts. These

statements include, financial projections and estimates and their underlying

assumptions, statements regarding plans, objectives and expectations with respect to future production, operations, costs, projects, and statements

regarding future performance. Forward-looking statements are generally

identified by the words “plans,” “expects,” “anticipates,” “believes,” “intends,” “estimates” and other similar expressions.

All forward-looking statements involve a number of risks, uncertainties and

other factors, many of which are beyond the control of Acacia, which could cause actual results and developments to differ materially from those expressed in, or

implied by, the forward-looking statements contained herein. Factors that could

cause or contribute to differences between the actual results, performance and achievements of Acacia include, but are not limited to, changes or developments

in political, economic or business conditions or national or local legislation or

regulation in countries in which Acacia conducts - or may in the future conduct -business, industry trends, competition, fluctuations in the spot and forward price

of gold or certain other commodity prices (such as copper and diesel), currency

fluctuations (including the US dollar, South African rand, Kenyan shilling and Tanzanian shilling exchange rates), Acacia’s ability to successfully integrate

acquisitions, Acacia’s ability to recover its reserves or develop new reserves,

including its ability to convert its resources into reserves and its mineral potential into resources or reserves, and to process its mineral reserves

successfully and in a timely manner, Acacia’s ability to complete land

acquisitions required to support its mining activities, operational or technical difficulties which may occur in the context of mining activities, delays and

technical challenges associated with the completion of projects, risk of trespass,

theft and vandalism, changes in Acacia’s business strategy and ongoing implementation of operational reviews, as well as risks and hazards associated

with the business of mineral exploration, development, mining and production

and risks and factors affecting the gold mining industry in general.

Although Acacia’s management believes that the expectations reflected in such forward-looking statements are reasonable, Acacia cannot give assurances that

such statements will prove to be correct. Accordingly, investors should not place

reliance on forward-looking statements contained in this presentation.

Any forward-looking statements in this presentation only reflect information

available at the time of preparation. Subject to the requirements of the Disclosure

and Transparency Rules and the Listing Rules or applicable law, Acacia explicitly disclaims any obligation or undertaking publicly to update or revise any forward-

looking statements in this presentation, whether as a result of new information,

future events or otherwise. Nothing in this presentation should be construed as a profit forecast or estimate and no statement made should be interpreted to mean

that Acacia’s profits or earnings per share for any future period will necessarily

match or exceed its historical published profits or earnings per share. Mineral reserves and mineral resources estimates contained in this presentation have

been calculated as at 31 December 2016 in accordance with National Instrument

43-101 as required by Canadian securities regulatory authorities. Canadian Institute of Mining, Metallurgy and Petroleum (CIM) definitions were followed

for mineral reserves and resources. The reserves and resources figures stated are

estimates. No assurances whatsoever can be given that the indicated quantities of metal will be produced and totals stated may not add up due to rounding.

You are reminded that you have received this presentation on the basis that you

are a person to whom this presentation may be lawfully made and delivered. You may not and are not authorised to: (i) reproduce or publish this presentation; or

(ii) distribute, disclose or pass on this presentation to any other person, in whole

or in part, by any medium or in any form, in breach of any applicable securities laws. BY ACCEPTING THIS PRESENTATION, YOU ACKNOWLEDGE AND

AGREE TO THE CONTENTS OF THIS DISCLAIMER AND YOU AGREE TO BE

BOUND BY THE FOREGOING LIMITATIONS.

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 2

Company Overview

A leading African asset portfolio with a high-grade R&R of 27.5Moz

Our Assets Business Overview

North MaraHigh-grade open pit / UG mine

At least 10 year mine life

Bulyanhulu

High grade U/G mine nearing

geological potential

At least 18 year mine life

Buzwagi

Low-grade open pit which

completes mining at end of 2017

Will process stockpiles until 2020

Exploration

Maiden high-grade resource

declared in West Kenya

Built a pan-African portfolioProducing mines Exploration properties

Kenieba Belt JVsMali

West Kenya ProjectKenya

BulyanhuluTanzaniaHoundé Belt JVs

Burkina Faso

North MaraTanzania

BuzwagiTanzania

3

Nyanzaga ProjectTanzania

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

Our Operating Philosophy

We run de-centralised operations and outsource any function where we can’t

be a world leader

Four areas we will never outsource:

Technical prowess

Discovery

Leadership

Government and Community relationship

Capital allocation is centralised and led by the CEO

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 4

Operational focus on creating sustainable free cash flow

Creating a sustainable competitive advantage based on core

competencies

We have transformed our business

At this stage, despite current concentrate ban, we continue to expect

further production and AISC improvement in 2017

5May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

1,561

1,346

1,105 1,112

958 880-920

626

642

719

732

830

850-900

600

650

700

750

800

850

900

0

300

600

900

1,200

1,500

1,800

2012 2013 2014 2015 2016 2017E

Pr

od

uc

tio

n (

ko

z)

AIS

C (

US

$/o

z)

AISC Progression vs Production

AISC Gold production

(1) 2017 chart represents mid-point of guidance range

Q1 2017 Performance

Gold production of 220koz, 15% higher than Q1 2016

Gold sales were 35koz lower than production

Primarily as a result of the Tanzanian Government’s directive stopping the export of metallic mineral concentrate

AISC was below previous quarter at US$934/oz

EBITDA of US$82 million, 25% higher than Q1 2016

Due to sales lagging production and indirect tax outflows net cash decreased to US$196 million

Continuing strong operational performance, financials impacted by ban

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 6

959 926 998 958 934 938

854 901 921 878

0

200

400

600

800

1,000

1,200

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17

$ /

ou

nc

e

All In Sustaining Cost per Ounce

AISC AISC ex RSU

37 43 40 42 60

78 7953

80 63

75100

11391 97

0

50

100

150

200

250

Q1 16 Q2 16 Q3 16 Q4 16 Q1 17

Pr

od

uc

tio

n (

ko

z)

Production

Buzwagi Bulyanhulu North Mara

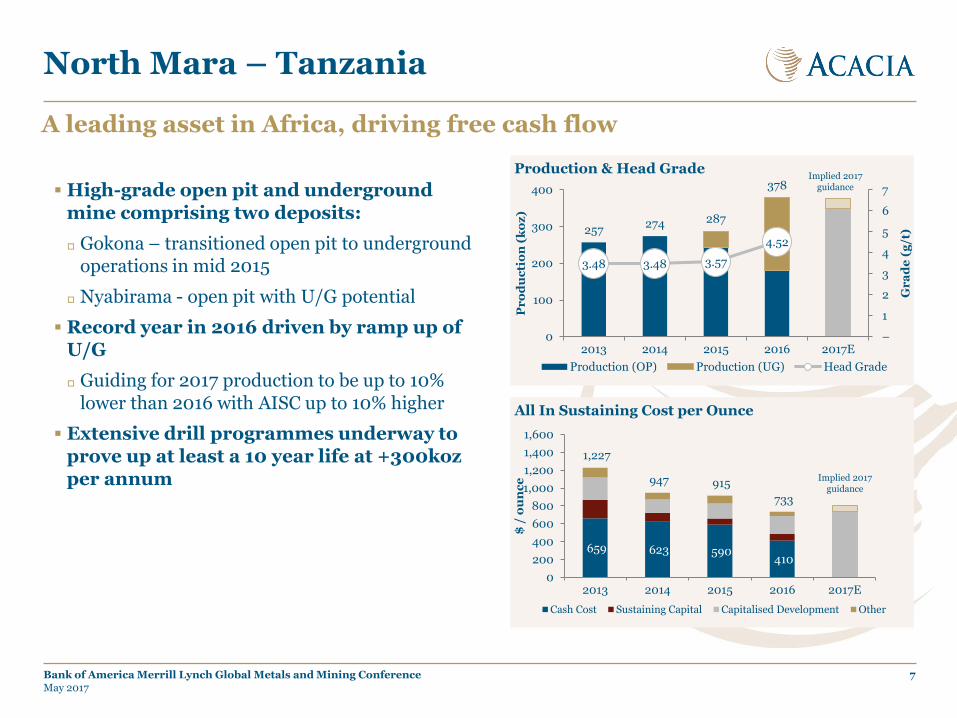

North Mara – Tanzania

High-grade open pit and underground mine comprising two deposits:

Gokona – transitioned open pit to underground operations in mid 2015

Nyabirama - open pit with U/G potential

Record year in 2016 driven by ramp up of U/G

Guiding for 2017 production to be up to 10% lower than 2016 with AISC up to 10% higher

Extensive drill programmes underway to prove up at least a 10 year life at +300koz per annum

A leading asset in Africa, driving free cash flow

7May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

659 623 590 410

1,227

947 915

733

0

200

400

600

800

1,000

1,200

1,400

1,600

2013 2014 2015 2016 2017E

$ /

ou

nc

e

All In Sustaining Cost per Ounce

Cash Cost Sustaining Capital Capitalised Development Other

257274 287

378

3.48 3.48 3.57

4.52

–

1

2

3

4

5

6

7

0

100

200

300

400

2013 2014 2015 2016 2017E

Gr

ad

e (

g/t

)

Pr

od

uc

tio

n (

ko

z)

Production & Head Grade

Production (OP) Production (UG) Head Grade

Implied 2017 guidance

Implied 2017 guidance

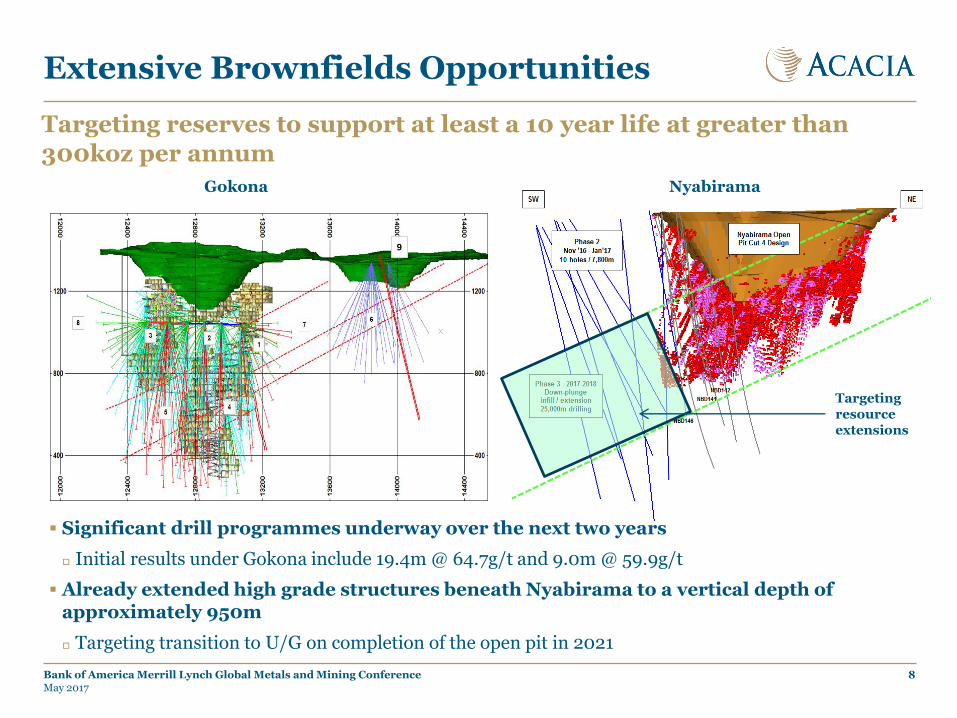

Extensive Brownfields Opportunities

8May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

9

Gokona Nyabirama

Targeting resource extensions

Targeting reserves to support at least a 10 year life at greater than

300koz per annum

Significant drill programmes underway over the next two years

Initial results under Gokona include 19.4m @ 64.7g/t and 9.0m @ 59.9g/t

Already extended high grade structures beneath Nyabirama to a vertical depth of approximately 950m

Targeting transition to U/G on completion of the open pit in 2021

Bulyanhulu - Tanzania

High grade narrow vein deposit

Geological endowment of over 20 million ounces*

History of under-delivery and lack of free cash generation

Undertaken re-engineering of the mine to ensure delivers to its geologic potential

2016 was the highest production since 2006 as mine starts to deliver on potential

AISC has fallen significantly as changes to mine take effect

Ramping production to +300kozpa over the coming years

Continuing to operate normally and stockpiling concentrate production

Represents ~45% of mine production

Continuing the transformation

9

* Including produced ounces

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

198 222 240 255

–12

34 35

198

235

274289

7.808.70 8.58

9.28

4.0

6.0

8.0

10.0

12.0

14.0

0

50

100

150

200

250

300

350

2013 2014 2015 2016 2017E

Gr

ad

e (

g/t

)

Pr

od

uc

tio

n (

ko

z)

Production & Head Grade

Production (UG) Production (Tails) Head Grade (ROM)

889 812 797 722

1,344 1,266 1,253

1,058

0

200

400

600

800

1,000

1,200

1,400

1,600

2013 2014 2015 2016 2017E

$ /

ou

nc

e

All In Sustaining Cost per Ounce

Cash Cost Sustaining Capital Capitalised Development Other

Implied 2017 guidance

Implied 2017 guidance

Buzwagi - Tanzania

Set up to deliver additional cash flow from re-sequencing open pit

Bulk tonnage open pit mine

Q1 17 production of 60koz , 62% higher than Q1 2016, at an AISC of US$773/oz

Driven by a 64% increase in head grade

Extended mining by six months until the end of 2017

Will process stockpiles until 2020

Adds 150koz of production over the LOM

Expect a 40% increase in production and up to 30% reduction in AISC in 2017

Continuing to operate normally and stockpiling concentrate production

Represents ~55% of mine production

10May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

945 791

1,046 1,031

1,507

1,055 1,187

1,095

–

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2013 2014 2015 2016 2017E

$/o

un

ce

All In Sustaining Cost per Ounce

Cash Cost Sustaining Capital Capitalised Development Other

182 210

171 162

1.46

1.73

1.39

1.21

0.6

0.8

1.0

1.2

1.4

1.6

1.8

-

50

100

150

200

250

300

2013 2014 2015 2016 2017E

Gr

ad

e (

g/t

)

Pr

od

uc

tio

n (

ko

z)

Production & Head Grade

Production (OP) Production (UG) Head Grade

Implied 2017 guidance

Implied 2017 guidance

Major contributor to host economies

Tanzania continues to received increased benefits from our operations

Over time we have agreed to follow a number of the 2010 Mining Code regulations

Despite the terms of the stabilisation agreements signed with the Government

Contributes to the Tanzanian Government’s aim of self-funding the national budget

The voluntary concessions include:

Local service levies at each mine increased from US$200k to 0.3% of revenues (~US$1mpa per mine)

Increasing royalty payments to 4% in 2012, which has increased the royalty paid to the Government by US$50 million in last 4 years

Led to total local tax contribution of US$164 million in 2016

Incurred a corporate tax charge amounting to US$55 million

Royalties of US$47 million

Payroll taxes of US$40 million

Other taxes of approximately US$22 million

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 11

Metallic Mineral Concentrate Ban

In March 2017, the Ministry of Energy and Minerals announced a ban on the export of metallic mineral concentrates

In order to promote the creation of a domestic smelting industry

Impacts approximately 45% of Bulyanhulu’s revenues and 55% of Buzwagi’s revenues

North Mara is not impacted as it only produces doré

Continuing to engage with Government to achieve a resolution

Operating Bulyanhulu and Buzwagi as normal and stockpiling concentrate at each of the sites

Taken a range of actions to help manage the significant financial impact of the deferral of sales

During Q1 this negatively impacted cashflow by US$33 million due to loss of sales

Will re-assess the operational plans of the two mines if we cannot reach a resolution in the coming weeks

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 12

Impacting approximately 30% of group revenues

Local listing requirements

Focus from the Government to increase transparency of business in Tanzania

Enacting regulation on a sector by sector basis, to make companies list on the local stock exchange

First sector to be impacted was Telecommunications followed by mining

Mining regulations impose two main obligations

30% local shareholding obligation through listing on the local stock exchange

Obligation for each of the entities that own Bulyanhulu, Buzwagi and North Mara to individually list

Deadline for listing is 23 August 2017

Acacia Mining plc cross-listed on the DSE in 2011, to promote Tanzanian ownership

Engaging with the relevant authorities in Tanzania

To find a route forward that is both beneficial and practical for all stakeholders

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 13

Sector wide legislation to promote local ownership

Investing in Our Future

Systematically created a pan-African

greenfield exploration footprint

Exploration pipeline with over 60 targets

12 rigs drilling greenfields projects across

the portfolio

135,000 metres drilled in 2016

190,000 metres budgeted for 2017

2017 greenfield budget increased by 15% to

US$25m

Key projects for 2017:

West Kenya

Houndé Belt

North Mara (Gokona UG & Nyabirama UG)

We believe in exploration as a key driver of value and our approach is

beginning to deliver results

14

Brownfield projects Greenfield projects

Kenieba JVsMali

West Kenya ProjectKenya

Houndé Belt JVsBurkina Faso

BulyanhuluTanzania

Nyanzaga ProjectTanzania

North MaraTanzania

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

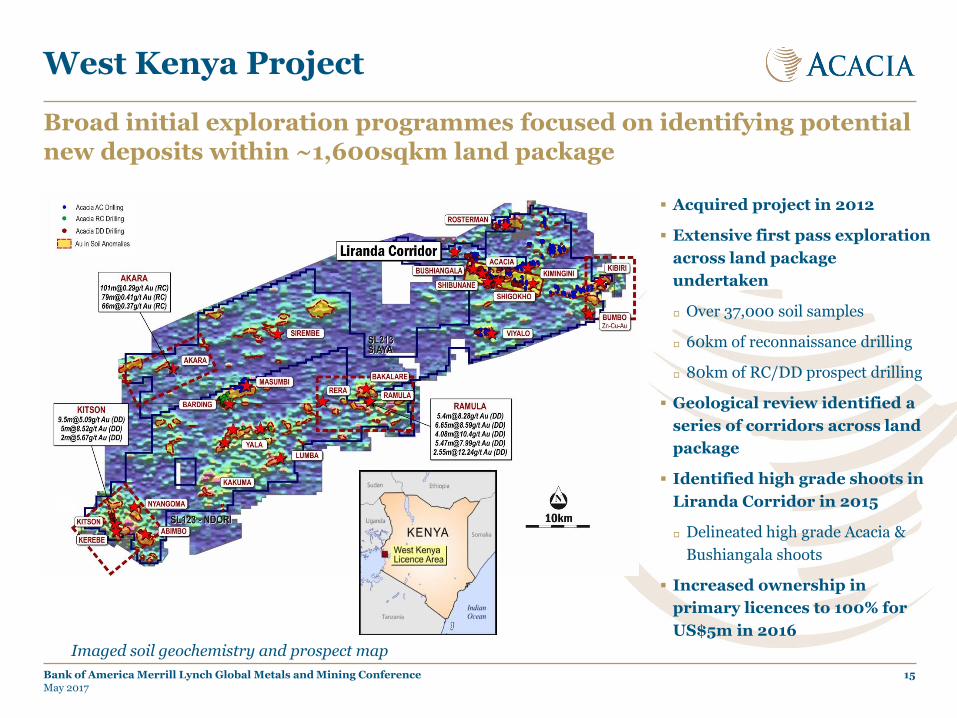

West Kenya Project

May 2017

Broad initial exploration programmes focused on identifying potential

new deposits within ~1,600sqkm land package

Bank of America Merrill Lynch Global Metals and Mining Conference 15

Acquired project in 2012

Extensive first pass exploration

across land package

undertaken

Over 37,000 soil samples

60km of reconnaissance drilling

80km of RC/DD prospect drilling

Geological review identified a

series of corridors across land

package

Identified high grade shoots in

Liranda Corridor in 2015

Delineated high grade Acacia &

Bushiangala shoots

Increased ownership in

primary licences to 100% for

US$5m in 2016

Imaged soil geochemistry and prospect map

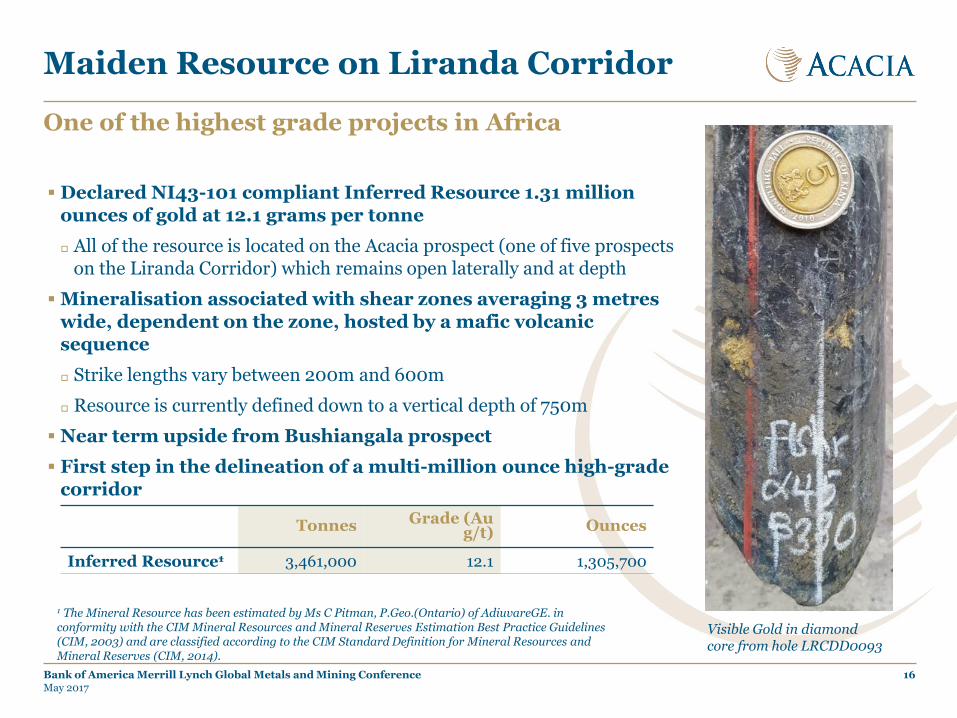

Maiden Resource on Liranda Corridor

One of the highest grade projects in Africa

16

Declared NI43-101 compliant Inferred Resource 1.31 million ounces of gold at 12.1 grams per tonne

All of the resource is located on the Acacia prospect (one of five prospects on the Liranda Corridor) which remains open laterally and at depth

Mineralisation associated with shear zones averaging 3 metreswide, dependent on the zone, hosted by a mafic volcanic sequence

Strike lengths vary between 200m and 600m

Resource is currently defined down to a vertical depth of 750m

Near term upside from Bushiangala prospect

First step in the delineation of a multi-million ounce high-grade corridor

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference

Tonnes Grade (Au g/t) Ounces

Inferred Resource1 3,461,000 12.1 1,305,700

1 The Mineral Resource has been estimated by Ms C Pitman, P.Geo.(Ontario) of AdiuvareGE. in conformity with the CIM Mineral Resources and Mineral Reserves Estimation Best Practice Guidelines (CIM, 2003) and are classified according to the CIM Standard Definition for Mineral Resources and Mineral Reserves (CIM, 2014).

Visible Gold in diamond core from hole LRCDD0093

Liranda Corridor – New targets evolving

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 17

Potential for a multi-million ounce gold camp emerging

Bushiangala Acacia Shigokho-Shibunane

1km

Focus of 2016 drilling

Primary focus of 2017 drilling

Potential further upside being tested in 2017

Investment Case

Continue to expect a fifth consecutive year of increased production

Will represent a 40%(1) uplift from 2012

Further reduction in costs across the business

AISC will have fallen by US$775(1) per ounce since Q4 2012

Portfolio of assets set up to deliver free cash flow with a strong balance sheet to withstand impact of concentrate ban

Net cash position of US$196 million

Delivering success through the drill bit across Africa

West Kenya Project on the cusp of delivering high grade resource ounces

Engaging with Government to build long-term partnership that provides mutual success and stakeholder value

Focused on long term value creation for all of our stakeholders

(1) Mid point of 2017 guidance ranges

May 2017Bank of America Merrill Lynch Global Metals and Mining Conference 18