accompanies you - fabricato · • at delima marsh s. a.ceo and executive vice president at holasa...

TRANSCRIPT

A C C O M P A N I E S Y O U

T h e P r e s i d e n t ’ s R e p o r tP A G E 1 0

01

T h e F u t u r eP A G E 3 8

04T h e P a s t

P A G E 1 6

02

S u s t a i n a b i l i t yP A G E 4 2

05I n d i v i d u a l F i n a n c i a l

S t a t e m e n t sP A G E 5 4

06C o n s o l i d a t e d F i n a n c i a l

S t a t e m e n t sP A G E 1 0 6

07

T h e P r e s e n tP A G E 2 8

03

Writing, Journalistic and Graphic EditingTaller de Ediciónwww.tallerdeedicion.co

FABRICATO S.A.

Carrera 50 No. 38 – 320

Telephone: (+57 – 4) 448 – 3500

Email: [email protected]

Bello, Antioquia, COLOMBIA

www.fabricato.com

INDEX

FIGURESB I L L I O N S O F P E S O S ( C O P )

10.7%$35.386

SALES$366.231

$330.845

LEVEL OF FINANCIAL INDEBTEDNESS

FINANCIAL DEBTVS. EBITDA

OPERATING PROFIT$15.916-$8.808

$24.724

7,0%4,3%-2,7%

Margen Operacional

NET PROFIT$33.942-$32.760

9,3%-9,9%

Margen Neto

$66.702

19,2%

EBITDA$23.841

-$4.048

$27.889

6,5%-1,2%

Margen EBITDA

7,7%

OPERATING MARGIN

4.3%-2.7%

7%

NET MARGIN9.3%-9.9%

19.2%

EBITDA MARGIN6.5%-1.2%

7.7%

2014 2015

3.2%6.5

2.9%0.98

(Financial Liabilities vs. Total Assets)

(Times)

E X P O R T S *

DENIM KNIT TECHNICAL AND RECOVERED

TEXTILES

INSTITUTIONALTWILL AND POPLIN

19%Presence in 11 countries: Mexico, Peru, Ecuador, Bolivia, Venezuela, Costa Rica, the Dominican Republic, Guatemala, El Salvador, Honduras and Spain.

Clothing Institutional Technical and Recovered Textiles

81%

B Y B U S I N E S S U N I T

B Y B U S I N E S S L I N E *

VestuarioInstitucionalTextiles técnicos y recuperables67%

26%7%

27%

$97.538

26%

$90.792$105.119

29%

$43.547

11%

$29.235

7%

5 3 . 6 M I L L I O N M E T E R S O F F A B R I C

S O L D

2P L A N T A

2 . 6 5 4 E M P L O Y E E S

* Participation in Pesos (COP)

* Figures in Billions of Pesos (COP)

D O M E S T I C M A R K E T *

8 9

Juan Octavio Mejía Arias» Operations Director

Armando Castillo Builes» Marketing and Sales Director

Andrés Antonio Hincapié» Secretary General

Vacant» Administrative and Financial Director

Ernest & Young Audit S.A.S.

PrincipalJuan Carlos González Gómez

AlternateLuis Javier Yánez Cuadrado

S T E E R I N G C O M M I T T E E F I S C A L A U D I T O R

A l ternate Members

» Work Experience• Vice President of Planning at

Coltejer • CEO and Executive Vice

President at Holasa• CEO at Edospina• CEO at Cementos Andinos• Deputy Defense Minister• Advisor to the National Coffee

Growers Federation in New York• Founding partner of Banca de

Inversión Q&A• Founding partner of Fondo de

Inversión Colombo Suiza LQA• Negotiator representing

Colombian businessmen in the G3 (Mexico, Venezuela and Colombia) Business Group

» Academic Training• Administrative Engineer

from the National University; Medellín

• MBA from the University of Georgia

• Masters in Economics from the University of Oxford

• International Business Fellow, Harvard University

» Experiencia laboral• Secretary General and

Assistant to the President at Delima Marsh S. A.

• Executive President of the Cali Chamber of Commerce

• Executive President of the Unidad de Acción Vallecaucana

• Consul General at the Colombian Consulate in London

• Member of various Boards of Directors and councils

» Academic Training• High Government Program

at Universidad de los Andes

• Specialization in Labor Law at Universidad Nuestra Señora del Rosario

• Law and Political Science, Universidad La Gran Colombia in Bogotá

» Work Experience• President of Valorar Futuro

S. A.• Financial Vice President

of Colinversiones (Compañía Colombiana de Inversiones), today Celsia ESP S. A.

• General Manager of Colombiana Kimberly Colpapel S. A.

• Vice President of the Fundación para el Progreso de Antioquia

• Member of various Boards of Directors

» Academic Training• MBA from Louisiana State

University• Chemical Engineer from

Louisiana State University

» Work Experience• President of Peldar S. A.• President of Owens Illinois

Europe• Member of various Boards

of Directors

» Academic Training• BSc in Industrial

Engineering from the University of Michigan

• Advanced Marketing Program at Harvard University

• Senior Management from INCOLDA at Columbus University

• Company Presidents at Universidad de los Andes

• Negotiation Workshop. Conflict Management Group; Universidad de los Andes–Harvard

Ricardo Toro Ludeke* Roberto Arango Delgado*

» Work Experience• Latin American Director

of Marketing and Global Director of Supply Strategies at The Goodyear Tire & Rubber Company

• President of Goodyear de Colombia

• President of Kimberly–Clark Andean Region

• General Manager of Colpapel

• General Manager of Kimberly–Clark Chile

• General Manager of Colombiana Kimberly

• Member of various Boards of Directors

» Academic Training• MSc in Krannert at Purdue

University• Senior Management

courses at Insead (France), The Leadership Institute, Thunderbird and Kellogg

• Chemical Engineer from Universidad Pontificia Bolivariana

Carlos Santiago Restrepo Posada

*Independent Member

Federico Molina Soto Gilberto Restrepo Vásquez*

Carlos Alberto de Jesus

» Work Experience• General Manager of Vicunha Ecuador• Member of various Boards of Directors in Ecuador• Associate Director at RPM443, Brazil• Commercial Director at Machasa, Chile• Commercial Director at Grafa, Argentina• Business Manager at Santista, Brazil » Academic Training• Bachelor’s Degree in Business Administration from UNICID; São Paulo• Postgraduate Degree in Marketing from ESPM; São Paulo

T H E B O A R D O F D I R E C T O R S

Principal Members

P R E S I D E N T

» Work Experience• Executive Director

of Konfigura Capital• Minister of the Treasury

and Public Credit (2003 – 2007)

• Dean of the Faculty of Economics at Universidad de los Andes

• Economic Advisor to the Office of the Comptroller General of the Republic

• Associate Researcher at Fedesarrollo

• Associate Professor at Universidad de los Andes

• Chief Research Economist at the Inter–American Development Bank (Washington)

• Technical Director of the Banco de la República

• Member of various Boards of Directors

» Academic Training• Ph. D. and MSc. from

the University of Illinois Department of Economics

• Economist from the Universidad de los Andes

» Work Experience• President of Banco de

Occidente• President of Fundación

FES• Technical Vice President

of the Colombian Banking Association

• Permanent Member of the Rationalization of Expenditure and Public Finance Commission (1995 – 1997)

• Director General of Public Credit

• Director of the National Planning Department’s Global Programming Unit

• Economist; International Monetary Fund’s Department for the Western Hemisphere

• Director of Cabrera, Bedoya y Asociados S. A.

• Member of various Boards of Directors

» Academic Training• Ph. D. from the London

School of Economics• Masters in Economics

from the Universidad de los Andes

• Bachelor’s Degree in Philosophy from the Pontificia Universidad Javeriana

» Work Experience• Legal and Administrative

Vice President of Coopcentral

• General Manager of Coopdesarrollo

• President of Banco del Estado

• Assistant Legal, Financial and Treasury Director of the Bogotá Secretary of the Treasury

• Inspector of Fondo Premium

• Professor at Universidad Externado de Colombia

• Member of various Boards of Directors

» Academic Training• Attorney–at–Law;

Specialist in Commercial Law; Universidad Externado de Colombia

» Work Experience• Former Governor of the

Department of Caldas• Former President of Banco

Central Hipotecario (BCH)• Former President of the

Instituto de Fomento Industrial (IFI)

• Liquidator of Banco Cafetero

• Liquidating Agent of Interbolsa Holding

• Professional practice as an Attorney–at–Law

• Member of various Boards of Directors

» Academic Training• Doctor in Legal Sciences;

Pontificia Universidad Javeriana.

» Work Experience• President of Smurfit

Kappa Latin America• President of Smurfit

Kappa Cartón de Colombia, Smurfit Kappa Cartón de Venezuela and Smurfit Kappa Cartón y Papel de México

• Member of various councils and committees

• Member of various Boards of Directors

» Academic Training• Masters in Industrial

Administration; Purdue University

• Chemical Engineer; the University of Alabama

Alberto Carrasquilla Barrera* Pablo Muñoz Gómez Roberto Silva Salamanca* Alejandro Revollo Rueda Gabriel Mauricio Cabrera Galvis*

T H E P R E S I D E N T ’ S R E P O R T

A N N U A L R E P O R T 2 0 1 5

E F F I C I E N C Y A N D C O M P E T I T I V E N E S S

-- Annual Report 2015 --

12 13We present the Report of the Fabricato Board of Directors and the Presidency for the 2015 fiscal year for your consideration.

In 2015, the Colombian economy, as well as the majority of the economies in the coun-tries of the region, was strongly affected by the sharp decline in the price of commodities in-cluding oil and the appreciation of the dollar; the combination of these two factors generat-ed pressure on prices, interest rates and a lower level of economic activity.

Faced with an unfavorable macroeconom-ic scenario, in which the reduction of eco-nomic activity was imminent, an opportunity for strengthening the Colombian economy

Accumulated as of December

2015 (in billions of Pesos

– COP)

Accumulated as of December

2014 (in billions of Pesos

– COP)

Variation 2015 vs. 2014

(in billions of Pesos – COP)

Variation %

2015 vs. 2014

Sales 366.231 330.845 35.386 10.7

Operating Profit 15.916 - 8.808 24.724

Operating Margin 4.3% - 2.7% 7.0

Net Profit 33.942 - 32.760 66.702

Net Margin 9.3% - 9.9% 19.2

EBITDA 23.841 - 4.048 27.889

EBIDTA Margin 6.5% - 1.2% 7.7

emerged. First, and in the short term, by re-placing imported products. Second, and in the medium and long term, by the recovery of businesses abroad.

The favorable environment for businesses in the Colombian industrial sector, which be-gan in late 2014 and was maintained through-out 2015 coincided, in the case of Fabricato, with the conclusion of the restructuring and optimization process, planned at the end of 2013.

As a result of this combination of timeli-ness and efficiency, we obtained a significant improvement in the 2015 results, compared to the previous year:

Carlos Alberto de Jesus, President

D E A R S H A R E H O L D E R S :

-- The President’s Report --

It is important to note that net profit was pos-itively affected by the net result of the sale of 30% of the fiduciary rights of the Pantex lot; the operating profit for the textile business in the period was COP 15.916 billion.

Another important issue for the future of the Company was the definition of real–estate development, in the specific case of the Pantex lot. This is an area of 106,000 m2, located in the municipality of Bello, on which a real–es-tate complex – with apartments, a shopping center and service towers – will be built.

The model adopted by Fabricato for the project was a private tender, in which leading companies from the sector, both in Colombia and abroad, were invited to participate to make an offer for the development under the param-eters pre–established by Fabricato.

The main objective was to choose the companies with which we would associate. Therefore, it was decided to contribute the land as a 70% compensation in a real–estate trust and the consortium, which offered the greatest contribution of resources as a compensation for the remaining 30%, was chosen.

The companies Arquitectura y Concreto, Londoño Gómez, and Fondo de Inversión In-moval, managed by Credicorp Capital, formed the winning consortium; they are currently the holders of, respectively, 6%, 6% and 18% of the fiduciary rights of the Pantex lot.

By selling 30% of the fiduciary rights, Fab-ricato received COP 70 billion, used to pay suppliers, the substitution of costly financial liabilities, and working capital. The real–estate project should begin to generate revenue be-ginning 2017.

The combination of the positive profit re-sults and cash generation, together with the careful destination of the aforementioned resources from the Pantex project, helped to consolidate an important stage in this process

of Fabricato’s recovery. This achievement can be perceived through several management indicators, but it is specifically reflected in the EBITDA/Financial Indebtedness ratio: At the close of 2015, this indicator was 0.98.

Also noteworthy in 2015 was the renewal of our ISO 9001 Certification for three years and the renewal of the collective agreement until 2019, reflecting our commitment to the inte-grated quality system and with our employees, with whom we are especially grateful for all their effort and commitment.

Likewise, we thank our clients and suppli-ers, who have accompanied and supported us so closely this year.

Finally, we reaffirm that the binomial of effi-ciency and competitiveness remain our master line for growth, for which we will invest USD 8 million in 2016.

$70Billion Pesos

were received through the sale of 30% of the fiduciary rights, used in working capital and the substitution of financial liabilities.

-- Annual Report 2015 --

14 15L E G A L A S P E C T SFabricato’s relationships with managers have been reduced to the performance of their du-ties and the payment of the respective remu-neration, that the Company has made subject to the law and the Bylaws. This means that there were no operations between sharehold-ers and managers.

In regard to shareholders, operations made by them have been approved as they were con-fined to provisions and permitted by law for Fa-bricato as an issuer.

In order to comply with Law 603 of 2000, the Company’s administration adopted the measures necessary to protect the industrial property and copyrights of the software insta-lled, through verification that permitted esta-blishing that the Company is the holder of the brands, names, emblems, slogans and distinc-tive signs that it uses in its products, services or computer programs. Through Resolution Number 83680, dated December 29, 2014, the Superintendency of Industry and Com-merce granted the registration of the Fabrimax mixed brand to Fabricato S. A. in Class 40 of the Nice Classification for ten years.

The Company complied with the provisions of the Colombian Financial Superintenden-

cy, in External Circular 062 of 2007 and the internal handbook related to the instructions to prevent and control money laundering and the financing of terrorism; no deficiencies were presented in the design and operation of the internal controls in this case.

In the work environment, control and mon-itoring of processes presented by retired per-sonnel were maintained. The final balance accrued as of December 31, 2015, was COP 2.339 billion.

The legal processes in favor of and against the Company were promptly responded to by the General Secretariat, supported, in some cases, by external professional specialists, whose processes are constantly reviewed and monitored.

During 2015, there were no significant events that could relevantly impact the performance of the Company in the immediate future.

As for the issues indicated in Article 446 of the Commerce Code, the following is stated:

• The value of the expenditures for salaries, fees, travel expenses, entertainment ex-penses, bonuses, allowances for transport and other expenses perceived by Company executives are included in Note 22 of the Financial Statements, as well as the outlays for the same concepts listed herein for ad-visors and managers, whose function was to transact business with public or private entities, or advise or prepare studies to con-duct such businesses, and the expenses for advertising and public relations.

• During 2015, the Company did not transfer money or other assets, free of charge or of any other type that could be likened to this, made in favor of natural or legal persons.

• Accounts Payable in foreign currency is in-cluded in Notes 13 and 16 of the Financial Statements.

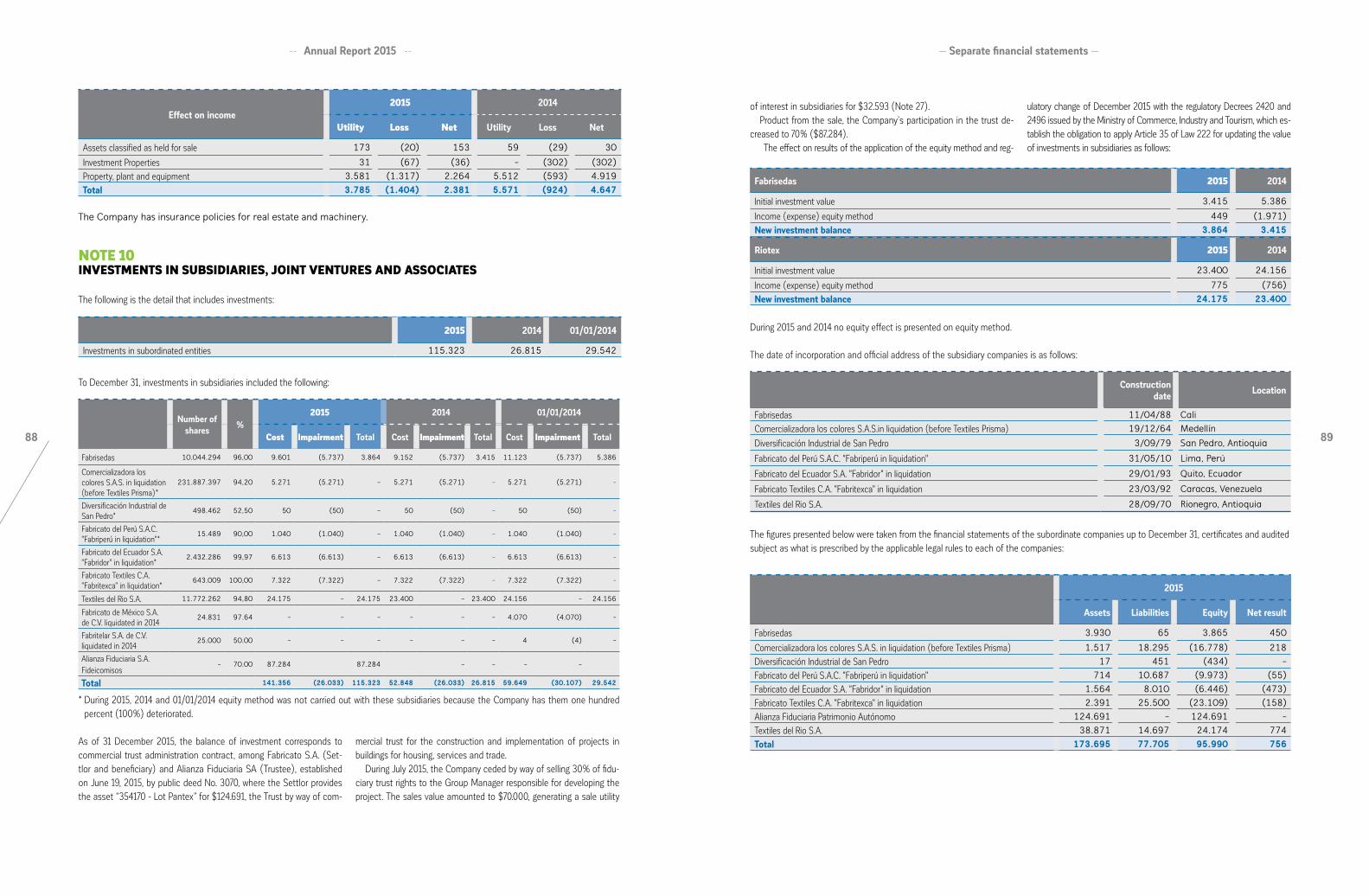

• Company investments discriminated in other domestic or foreign companies are included in Note 10 of the Financial Statements.

This document is part of the information that was available to shareholders during the pe-riod provided by law to exercise the right of inspection.

C E R T I F I C A T E S A N D R E C O R D SIn accordance with the provisions of Article 46 of Law 964 of 2005, we state that the Financial Statements and other relevant annexes and reports that are presented do not contain any errors, inaccuracies or errors that could prevent the true financial situation or operations of Fabricato from being known.

As indicated in Article 47 of Law 964 of 2005, we certify that the Company has deve-loped policies and procedures, the operation of which is supervised by Internal Auditing and the Fiscal Auditor, with the assistance of the Audit Committee. This allows us to state that, under application, the financial information has adequate disclosure and control systems.

The 2015 Financial Statements were stu-died and approved by the Audit Committee, before being presented for consideration to the Board of Directors and the General Assembly of Shareholders.

To comply with the provisions in the para-graph of Article 87 of Law 1676 of 2013, we cer-tify that the administration of Fabricato has not hindered the free movement of invoices issued by sellers or suppliers of the Company.

C O D E O F C O N D U C T A N D E T H I C S H O T L I N EThe Code of Conduct is mandatory for all employees and di-rectors of the Company. This is how we ensure that all stake-holders are covered by these guidelines and policies, which must always be observed. Breaches of the Code of Conduct imply the application of the procedures established in the In-ternal Work Regulations regarding sanctions and may even involve the termination of the employment contract.

The Ethics Hotline is a reserved, anonymous communi-cation and reporting tool, where employees and stakeholders may report unethical actions or situations that may affect the interest of the Company.

T H A N K Y O U V E R Y M U C H

Carlos Alberto de JesusPresident

-- The President’s Report --

T H E P A S T

A N N U A L R E P O R T 2 0 1 5

A H I S T O R Y L I N K E D T O T H E G R O W T H O F I N D U S T R Y A N D T H E C O M P A N Y

-- Annual Report 2015 --

18 19

T H E W A R POn Tuesday, December 19, 1922, at 1:00 P. M., four cars of the Antioquia Railroad stopped at the Bel-lo station. They were loaded with openers, warpers, cards and other machinery purchased by Don Jorge Echavarría so that, two years after founding the Fábri-ca de Hilados y Tejidos del Hato (Fabricato), finally, what was going to be one of the most important in-dustries in the country, began to operate. That same Tuesday, and in the year–end summer, the first group of workers began working. Their mission was to clean the machines with which the first fabric would be woven, the origin of the millions of meters that have been produced in 96 years of history.World War I had ended in 1918; imports of fabrics from Europe and other countries were held back, and other textile companies in Antioquia – such as Colte-jer and Compañía de Tejidos Resellón – became thriv-ing businesses.

By 1913, Bello had already acquired the status of municipality. It was a territory with about 5,000 in-habitants, almost all from the countryside, who had settled in its surrounding areas hoping to become workers in the textile industries that operated there. It was the perfect place for an industrial complex, due to the proximity of water sources and because there was enough manpower to operate the process.

On Wednesday, August 8, 1923, the Company was inaugurated; the machines – that months before had been unloaded from the trains – were started. That Tuesday, the history of Fabricato began to be wo-ven with each worker who passed through and helped build it, together with the development of the munic-ipality of Bello and the textile industry of the country.

1 9 1 9

1 9 2 0

In December, the land for the factory was purchased.

The Fabricato Articles of Incorporation

On February 26, the Fábrica de Hilados y Tejidos del Hato was established through a public deed as a corporation.

-- The Past --

1 9 2 2 1 9 2 3

1 9 3 2

On December 19, four cars arrived at the Antioquia Railroad station in Bello with the first boxes of machinery.

Jorge Echavarría, first administrator of

Fabricato

The Fabric of Perfect ThreadsOn August 8, Fabricato was inaugurated with the presence of General Pedro Nel Ospina Gómez, President of Colombia.

The production of plaids, towels and fancy fabrics began.

-- Annual Report 2015 --

20 21

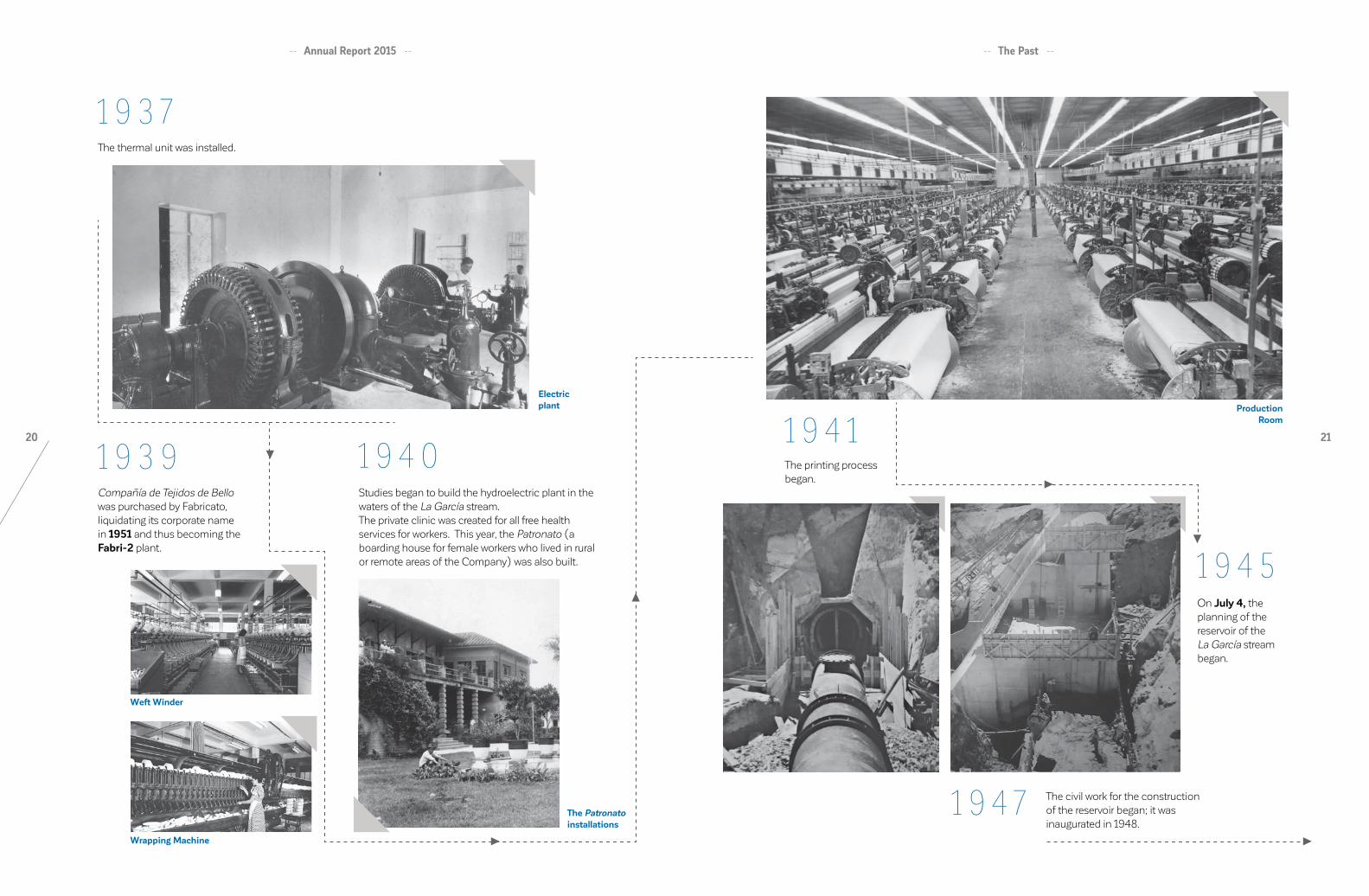

1 9 3 7

1 9 3 9 1 9 4 0

The thermal unit was installed.

Compañía de Tejidos de Bello was purchased by Fabricato, liquidating its corporate name in 1951 and thus becoming the Fabri-2 plant.

Studies began to build the hydroelectric plant in the waters of the La García stream.The private clinic was created for all free health services for workers. This year, the Patronato (a boarding house for female workers who lived in rural or remote areas of the Company) was also built.

Electric plant

Weft Winder

The Patronato installations

Wrapping Machine

1 9 4 1

1 9 4 5

1 9 4 7

The printing process began.

On July 4, the planning of the reservoir of the La García stream began.

The civil work for the construction of the reservoir began; it was inaugurated in 1948.

Production Room

-- The Past --

-- Annual Report 2015 --

22 23

1 9 4 8

1 9 5 0

1 9 5 1

1 9 5 7

The worker housing program began, with the construction of the Barrio Obrero (with 320 modern architecture homes, a theatre, church, micro–soccer field and parks).

Inauguration of the Fabricato building.

On July 26, the La García hydroelectric plant began operation.

On March 18, the charter of the Fabricato Workers Cooperative (Cooperativa de Trabajadores de Fabricato, Cotrafa) was signed.

1 9 6 1

1 9 6 4

1 9 7 0

1 9 7 1

Fabric exports began.

On September 28, the Riotex Corporation was established.

Riotex began operations.

With Pantex, Fabricato participated in the founding of Enka de Colombia.

-- The Past --

-- Annual Report 2015 --

24 25

1 9 7 3

1 9 7 6

1 9 8 5

Fabricato received the Order of Boyacá during the Presidency of Misael Pastrana Borrero.

Fabricato received the Quality Award, the first company to obtain this distinction.

The Concordato, composition with creditors, was signed for 12 years.

Misael Pastrana Borrero (left) in Fabricato’s 50th anniversary

1 9 8 6

1 9 8 7

The payment of the Concordato debt and the process of industrial reorganization began.

The Concordato ends early.Aerial view of Fabricato and Pantex

1 9 8 9Market launch of the bond issue for a total of COP 4 billion.

Visit by Ernesto Samper (third from the right),

Minister of Development in October 1990

2 0 0 0

2 0 0 5

Fabricato merged with Tejicóndor.

Fabricato purchased Fibratolima.

-- The Past --

-- Annual Report 2015 --

26

2 0 0 8After an investment of USD 40 million, the most modern indigo plant in Latin America was inaugurated. This allowed expanding production by one million additional meters.

2 0 1 3The Board of Directors appointed Carlos Alberto de Jesus as President, responsible for leading the Company’s transformation strategy.

Fabricato selected the companies responsible for the real–estate development of the Pantex lot: Londoño Gómez S.A.S., Arquitectura y Con-creto S.A.S. and Fondo de Inversión Inmoval, administered by Credicorp Capital. There, a commercial and urban project will be built.2015

T H E P R E S E N T

S T A B I L I T Y A N D O P T I M I Z A T I O N

A N N U A L R E P O R T 2 0 1 5

-- Annual Report 2015 --

30 31

-- The Present --

With the investments we have made, in 2016 this will be one of the most modern companies in the world.”

Carlos Alberto de Jesus, president

-- Annual Report 2015 --

32 33

The year 2015 was a difficult one for the economies of the region. In Colombia, the macroeconomic environment was marked by the volatility of the Dollar; the uncertainty caused by falling oil prices; the beginning of El Niño, which lasted until 2016; and inflation of 6.77%, the highest since 2009.

In such a complex environment, Fabricato’s results were outstanding: 53.6 million meters of fabric sold; COP 366.231 billion in sales; EBITDA for COP 23.841 billion; operating profit of COP 15.916 billion and a consolidated net profit of COP 33.942 billion.

The figures are the result of a res-tructuring and optimization process that began in late 2013; it was executed in 2014 and began to show positive re-sults in 2015.

$53.6 million

meters of fabric sold in 2015.

This restructuring involved reviewing operating costs; renewing the portfolio; starting a technological restructuring plan; and setting goals for growth and expansion in the coming years.

The optimization required closing two of the four plants that were operat-ing in 2014 (Fibratolima in Ibagué and Notejidos in Bello, which joined the Rionegro plant). Similarly, the admin-istrative structure was simplified: four Vice Presidencies were eliminated and a structure – formed by the President,

BUSINESS UNITS

67%Clothing

Denim 27%

Twills and Poplins 29%

Knits 11%

26%Institutional

Military Line 16%

Work 10%

7%Technical and

Recovered Textiles

O R G A N I Z A T I O N A L C H A R T

PresidentCarlos Alberto de Jesus

Secretary GeneralAndrés Hincapié

Administrative and Financial DirectorVacant

OperationsDirector Juan Octavio Mejía

Marketing and SalesDirectorArmando Castillo

three directorates (Operations, Marketing and Sales, and Administra-tive and Financial) and a third level of managers that support it – was configured.

The renewal of the portfolio meant concentrating on five strategic lines: denim, twills, knitwear, nonwovens and institutional, and the elim-ination of three lines that did not fit the Company’s new focus: home, wools and pre–dyed plain fabric.

Additionally, the Company’s sales offices in Colombia, Peru, Ecua-dor, Mexico and Venezuela were closed, in order to increase the working capital efficiency.

-- The Present --

-- Annual Report 2015 --

34

Our goal is to specialize in clothing and institutional lines, with products that are differentiated by their fibers, by the structure of their fabrics or by the finishings, as well as for our service and technical assistance, so that we can make a garment that differs from those in the market.”Armando Castillo, Marketing and Sales Director

M A R K E T P R E S E N C EWith two plants less and focused on five business lines, in 2015 the Compa-ny sold the same meters of fabric as in 2014, while sales grew 10.7% in Pesos.

Most of its production – 81% – was sold in the domestic market; the remaining 19%, internationally where South America and Central America are the main destinations.

The goal for 2016 is to continue growing in sales and increase the share of exports. To do this, the Company is already reaching new markets with sales representatives. There are contacts with brands in Spain and Italy to establish al-liances and sell the whole package.

It is projected that in the long term, exports will reach 35% of total sales, which will constitute a natural hedge to mitigate the impacts of the exchange rate. The alliances and the Central American market will be important in achieving that goal.

DOMESTIC AND INTERNATIONAL

MARKET

81%Domestic Market

19%Exports

C H A L L E N G E SAs a result of the volatility of the exchange rate, last year there was a decrease in the imports of fabrics of nearly 8%, representing an opportunity for local industries. However, that was a situation that reflected a variable market condi-tion and it is clear that to grow, not only a strategy – but also facing some challenges – is required.

The reduction of tariff quotas on products from China, economic opening and trade agreements make the scenario complex.

The entry of imported fabrics at prices below production costs, technical and open contraband, and informality in the garment sector are current challenges.

The strategic focus of competitiveness through effi-ciency is the only option to compete in an environment of economic liberalization and fair competition. Also, it is clear that, in an environment of unfair competition – in which bad practices abound – it is necessary that the Government in-tervene to combat them and favor the formal industry.

-- Annual Report 2015 --

36 37

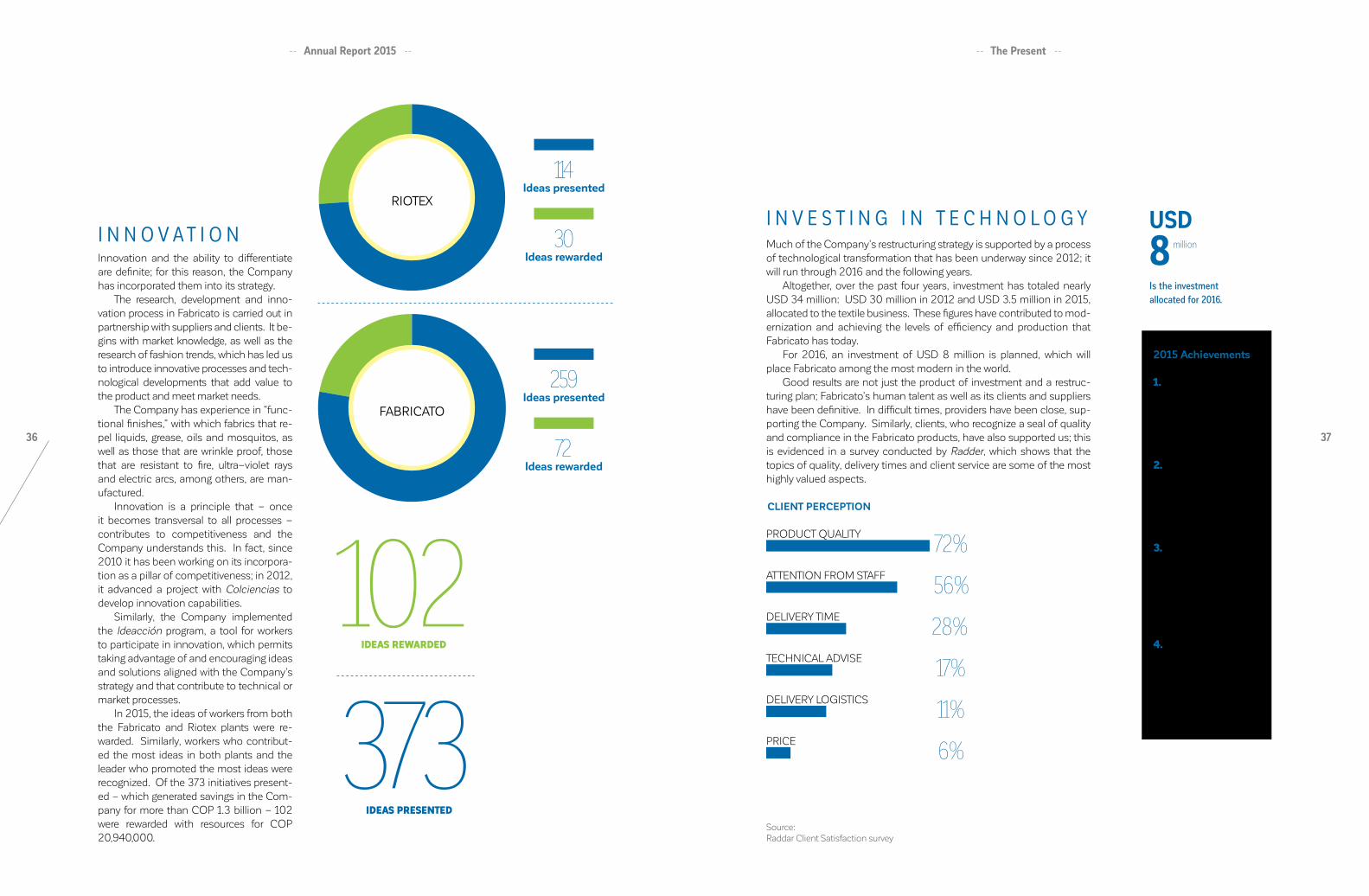

I N N O V A T I O NInnovation and the ability to differentiate are definite; for this reason, the Company has incorporated them into its strategy.

The research, development and inno-vation process in Fabricato is carried out in partnership with suppliers and clients. It be-gins with market knowledge, as well as the research of fashion trends, which has led us to introduce innovative processes and tech-nological developments that add value to the product and meet market needs.

The Company has experience in “func-tional finishes,” with which fabrics that re-pel liquids, grease, oils and mosquitos, as well as those that are wrinkle proof, those that are resistant to fire, ultra–violet rays and electric arcs, among others, are man-ufactured.

Innovation is a principle that – once it becomes transversal to all processes – contributes to competitiveness and the Company understands this. In fact, since 2010 it has been working on its incorpora-tion as a pillar of competitiveness; in 2012, it advanced a project with Colciencias to develop innovation capabilities.

Similarly, the Company implemented the Ideacción program, a tool for workers to participate in innovation, which permits taking advantage of and encouraging ideas and solutions aligned with the Company’s strategy and that contribute to technical or market processes.

In 2015, the ideas of workers from both the Fabricato and Riotex plants were re-warded. Similarly, workers who contribut-ed the most ideas in both plants and the leader who promoted the most ideas were recognized. Of the 373 initiatives present-ed – which generated savings in the Com-pany for more than COP 1.3 billion – 102 were rewarded with resources for COP 20,940,000.

FABRICATO

RIOTEX

114Ideas presented

30Ideas rewarded

259Ideas presented

72Ideas rewarded

102

373IDEAS REWARDED

IDEAS PRESENTED

I N V E S T I N G I N T E C H N O L O G YMuch of the Company’s restructuring strategy is supported by a process of technological transformation that has been underway since 2012; it will run through 2016 and the following years.

Altogether, over the past four years, investment has totaled nearly USD 34 million: USD 30 million in 2012 and USD 3.5 million in 2015, allocated to the textile business. These figures have contributed to mod-ernization and achieving the levels of efficiency and production that Fabricato has today.

For 2016, an investment of USD 8 million is planned, which will place Fabricato among the most modern in the world.

Good results are not just the product of investment and a restruc-turing plan; Fabricato’s human talent as well as its clients and suppliers have been definitive. In difficult times, providers have been close, sup-porting the Company. Similarly, clients, who recognize a seal of quality and compliance in the Fabricato products, have also supported us; this is evidenced in a survey conducted by Radder, which shows that the topics of quality, delivery times and client service are some of the most highly valued aspects.

2015 Achievements

1. Stabilize the business, meet the sales budget, and generate margin and profit.

2. Renew the portfolio of products and refocus the channel.

3. Finalize the commercial restructuring process in all the countries where we are present.

4. Recover client trust and credibility regarding quality, delivery times and type of products.

PRODUCT QUALITY

ATTENTION FROM STAFF

DELIVERY TIME

TECHNICAL ADVISE

DELIVERY LOGISTICS

PRICE

CLIENT PERCEPTION

72%

56%

28%

11%

6%

17%

Source: Raddar Client Satisfaction survey

USD

8 million

Is the investment allocated for 2016.

-- The Present --

T H E F U T U R E

G R O W T H I S T H E G O A L

A N N U A L R E P O R T 2 0 1 5

-- Annual Report 2015 --

40 41

After the organizational restructuring and the changes that have been implemented in recent years, Fabricato is already working on the strat-egy for the future.

The Company began the investment plan for the coming years, including resources to continue technological innovation and main-tain efficiency and growth.

Partnerships with garment manufacturers will allow us to offer finished products, com-plete the link in the chain and become a pro-vider of markets that until now have been im-possible to penetrate.

I N V E S T M E N T I N T H E R E A L –E S T A T E S E C T O RWhile Fabricato’s core business continues to be in the textile sector, the Company is open to the possibilities that the market offers. There-fore, in 2014 Fabricato made the decision to enter the real–estate business, an alternative that will allow us to have an additional cash flow in the future and take advantage of an as-set that was not in use.

Thanks to the partnership with Arquitectura y Concreto, Londoño Gómez and the Fondo de Inversión Inmoval, administered by Cred-icorp Capital, the eleven hectares, where until four years ago Pantex operated, will become a real–estate development that not only contrib-utes to Fabricato and the project partners, but also to the municipality of Bello.

A shopping center, housing and a service center will operate on the old lot, which is considered one of the most valuable assets of the Company, not only for its size, but also be-cause it is situated in a strategic location north of the city.

With the sale of 30% of the lot, the Com-pany managed to implement the restructuring plan. With the remaining 70%, it will participate in a real–estate development that will allow it to receive income from the businesses that will operate there beginning in 2017.

Fabricato is very clear that its entry into the real–estate sector is an opportunity to generate income, which – although it will become a new business unit – does not mean a shift in its tex-tile industry

In addition to founding Pantex, Enka and Comercia (today, Factoring Bancolombia), Fabricato has participated in various business-es, such as Texmeralda, and cotton and agricul-tural companies, among others. So, more than a surprise, our entry into the real–estate busi-ness is an opportunity in the growth strategy.

The possibilities are in the market. There are as many as there are competitors. While continuing to grow and create value, Fabrica-to’s work is to explore the alternatives that most benefit it.

Fabricato is going to be a Company that aims for

excellence of what the textile business is and

be an investor, associated with large real–estate

companies, to leverage assets available for the

process to optimize production.”

Carlos Alberto de Jesus, President

For Fabricato comes smart – not unbridled – growth, with a very clear portfolio.

Challenges 2016

1. Growth and optimal use of technological reconversion.

2. Reach new key markets to the strategy, including Central America, Europe and the United States.

3. Maintain the proposal of differentiated collections and products.

4. Increase exports.

5. Take advantage of trade agreements.

-- The Future --

S U S TA I N A B I L I T Y

R E S P O N S I B L E G R O W T H

A N N U A L R E P O R T 2 0 1 5

-- Annual Report 2015 --

44 45

Being sustainable means generating profits, guaranteeing the future of the or-ganization over time, being environmen-tally friendly, and, above all, generating value for the stakeholders. This means growing, avoiding environmental deteri-oration, seeking the welfare of employ-ees, but also of the community in which it is located; this is what Fabricato has been doing throughout its history.

Although a Department of Environ-mental Management did not exist, since the late 1960’s concern for the issue became a priority.

Anticipating legislation, in that de-cade Fabricato began a program to reduce levels of pollution from waste being discharged into the atmosphere and water.

Many years later, when Colombian law required companies to create areas that assumed these responsibilities, Fabricato had already created its Depart-ment of Environmental Management.

Today, the Company has an Environ-mental Committee, composed of plant managers; it meets monthly to analyze, map out, implement and monitor the Company’s environmental activities, es-tablish guidelines, and decide on com-mitments with clients and suppliers.

The Company has focused its envi-ronmental work in three fields of action: emissions, water consumption, and discharges. This work is carried out with responsibility and the commitment to return benefits to the environment from

which it draws resources for its operation.Precisely, in environmental issues,

Fabricato is a pioneer. It was one of the first companies in the industry in Antioquia to sign a Clean Production Agreement. It was signed in 1984 in the Rionegro (Riotex) plant, and it has been renewed three times. In 2000, in its plant in Bello, it signed voluntary agreements with the Ministry of the Environment and Sustainable Develop-ment and the regional environmental authorities: the Aburrá Valley Metropol-itan Area and the Regional Autonomous Corporation of Central Antioquia (Cor-poración Autónoma Regional del Cen-tro de Antioquia, Corantioquia). These commitments enable the achievement and evaluation of new targets, the im-plementation of clean production sys-tems, the measurement of impacts, the optimization of activities, and the recovery of water and steam.

These agreements are now called Sustainable Production and Consump-tion Conventions, as proposed in the Ministry’s Sustainable Consumption Policy. The last convention signed for the Bello plant was in 2011 and will be renewed in 2016; the convention for the Rionegro plant will be renewed in 2017.

Fabricato is aware that the textile sector requires water resources and knows the importance of good man-agement to avoid polluting processes. It knows that in today’s world, large re-ductions and savings are presented with the use of new technologies; thus, tech-nological renovation has been a priority. In 2016, construction will be completed on the Wastewater Treatment plant with Color Removal and Water Reuse.

These decisions seek care for the environment and generate benefits in every respect for the Company. Mod-ernization has implied an environmen-tal benefit because saving resources contributes to their moderated use. Precisely, the investment of USD 8 million planned for 2016 will improve efficiency while contributing to environ-mental care.

-- Sustainability --

E M I S S I O N SThere are several actions that Fabricato has taken since the 1940s to avoid contamination: It purchased measurement equipment, thought of the possibility to stop using coal as the main fuel and – because of the impossibility of doing so – opted to import purification equipment, which was inaugurated in 1979 and con-tributed to environmental decontamination.

At the end of that decade, with the implementa-tion of the process to purify dust emissions, gases and fumes expelled by the chimneys were reduced 95%; once sedimented, they were used to make cement.

With the purchase of this equipment, Fabricato properly managed the carbon soot and controlled the management of particulate material.

Another decision that contributed to controlling emissions was the use of natural gas – instead of diesel – in boilers, as it is a more environmental friendly fuel and has low emissions of carbon dioxide (CO

2). What

is remarkable is that in the moment when the Compa-ny made this decision, the topic of emissions was not part of the environmental discourse in the country.

This shows that this is not a recent concern, nor is it due solely to legal compliance; rather, it is part of the culture of the organization, an environmental con-sciousness that has been gestating since its birth.

Since 2008, the Company has a team to collect ash, an acquisition that contributes to the air quality of surrounding communities. Even today, the coal ash burned in the boilers is collected in its entirety and sold as raw material for the construction industry.

Additionally, to have efficient waste management, in the Bello plant there are two permanent operators of the companies in charge of separating all the materials, including the management line for hazardous waste.

Noteworthy is that, in 2015, Fabricato extended its commitment to suppliers. Through meetings and visits, jointly reviewed were their environmental man-agement plans and their strengths and opportunities for improvement with the goal that environmental re-sponsibility and sustainable consumption are carried out throughout the production chain.

The Company participates in a pilot project to continuously

monitor emissions.

-- Annual Report 2015 --

46 47

Similarly, in 2015 the Company worked on im-plementing ISO 14000, an international envi-ronmental–management standard; it is a tool that helps companies improve their relation-ship with the environment by controlling and reducing the impacts of their operations.

The Energy Production Plant, which in a textile company requires special treatment to reduce its environmental impact, has sophis-ticated systems to collect all emissions to filter all hazardous elements, according to Colombi-an environmental regulations. At the present time, environmental authorities measure the emissions and recommend actions that must always be fulfilled.

Looking ahead, the Company already has a plan, participating in a pilot project for the con-tinuous monitoring of emissions, and togeth-er with the Aburrá Valley Metropolitan Area, it signed a memorandum of understanding with the Clinic Care Institute to install equipment that will measure emissions in the Bello plant in 2016.

W A T E R C O N S U M P T I O NWith regard to water consumption, Fabricato has implemented policies to use and reuse wa-ter resources for efficient consumption, avoid-ing its contact with contaminated material and assisting in its conservation, not only for its contribution to the productive process, but also because we consider it essential for humanity.

In the Bello plant, recovery of cooling wa-ter amounts to 70%. The heat sealers work with vapor that is then channeled and reused in the boilers in their production processes; it is a resource that – by arriving hot – re-quires less fuel to raise it to the required tem-peratures. The water used is provided by the

La García hydroelectric plant, which be-longs to Fabricato. The liquid is collected at the intake and reaches the water plant, where seven pools receive treatment, de-pending on their final use, including human consumption. Monthly, nearly 220,000 m3 of water are treated.

Additionally, the Company always aims to acquire low water–consumption technol-ogy, which allows a bath ratio (RB, the num-ber of liters of water required for a kilo of fab-ric to be dyed) of four (4), an optimum level in global measurements and far from a BR of 20, common in the industry decades ago.

A modern industry generates employment, economic growth, currency for the country and taxes for the municipality, many benefits… and minimizes its impact.”Carlos Alberto de Jesus, President

D I S C H A R G E SIn 2015, the Company strengthened its envi-ronmental and social commitment to the prop-er management of its discharges, so much of our waste is classified as reusable or recyclable.

Since 2007, Fabricato joined a collection plan produced by Empresas Públicas de Me-dellín (the Medellín Public Utilities Company) with agencies that regulate discharges. The de-cision was to take the discharges to a central-ized treatment plant and then process them in the wastewater treatment plant in Bello, located in the Navarra sector.

However, in 2015, the Company defined the construction of a Wastewater Treatment plant with Color Removal and Water Reuse, which will permit separating the liquid from the inks that fall in it and treat about 30% of the water consumptions of the textile plant.

E N E R G Y G E N E R A T I O NIn a visionary decision that meant a large in-vestment at the time, between 1947 and 1951 the Company built its own hydroelectric plant in the La García stream, located in the San Felix hamlet of the municipality of Bello.

It has two generators that produce 6,000 kWh; the energy is transported to the plant in Bello, and in 2015 – together with the ther-moelectric plant – it contributed to supply an average of 83% of the energy needs; in several months, self–generation reached 90%. This – our own supply – depends on the level of water in the reservoir; when it fails to self–generate, the company connects to the Empresas Públi-cas de Medellín electrical system.

The thermoelectric plant, located in the Bel-lo plant and which generates 8,000 kWh, was inaugurated on July 5, 1979. At that time, the investment amounted to COP 80 million and was presented as a contribution from the pri-vate sector and a share of social responsibility.

Self–generated energy represents a savings of approximately 45% for Fabricato, compared to the value that it would have to pay Empresas Públicas de Medellín in case its interconnec-tion were required.

CertificationsFabricato has ISO 9001 certification for its Quality Management System (QMS), standards accredited by IQNet, a global certification au-thority. In 2015, QMS was renewed until 2018 and covers the plants in Rionegro and Bello. This certification demonstrates the continuous improvement of the QMS; the efficient use of resources; objective, evidence–based decision making; client satisfaction; and the sustained success of the organization, among others.

Fabricato also has certification of products from the Colombian Institute of Technical Stan-dards and Certification (Instituto Colombiano de Normas Técnicas y Certificación, ICONTEC), for fabrics through the tender with the Armed Forces. These seals position the product brand and generate greater recognition and market opportunities. This certificate is validated by the National Accreditation Agency of Colom-bia (Organismo Nacional de Acreditación de Colombia, ONAC) and the American Nation-al Standards Institute (ANSI). Fabricato thus demonstrates that its products meet technical references through manufacturing systems and effective, reliable controls, which give backing and security to the end consumer. Current-ly, there are 11 products with seals, which were certified under the Colombian Ministry of De-fense Technical Standards (Normas Técnicas del Ministerio de Defensa, NTMD) 0328, 0053, 0067, 0075, 0146 and 0186.

The renewal of these seals was received by the Company in 2015 and extends to 2017.

Self–generated energy represents an approximate savings of 45% in the energy cost that the Company pays.

-- Sustainability --

-- Annual Report 2015 --

48 49

H U M A N R E S O U R C E SFabricato closed 2015 with 2,654 employees; six unions, each with 10 union representatives; and a collective agreement agreed upon until 2019, signed with the majority union.

The policy implemented by Human Re-sources is part of the Company’s overall strate-gy, which has included – as a fundamental pillar of its activity – concepts inherent to the sustain-ability of the Company and maintaining decent work to offer all its employees. These are also involved in interior pillars, supported by admin-istrative transparency, coherence, respect for human rights and environmental protection.

The aforementioned guidelines make the actions of Human Management on the welfare of employees and their families imperative; it also involves their training in activities associ-ated with the textile process and related to their daily life, attaining the professionalization of an important human nucleus.

To achieve this, Fabricato has implemented programs that include training, development plans and training in skills related to an activity. Likewise, it contributes to improving the quality of life of their family environment with academ-ic and recreational and leisure activities.

Work aimed at improving this welfare per-mits joint work with all the sectors that contrib-ute to the same intention. For example, with the Company unions, it seeks the continuous

strengthening of work conditions and condi-tions outside the workplace, and has signed agreements, such as the Wellness Program, which offers labor guarantees, even greater that those required by Colombian law.

H O U S I N GThe history of Fabricato and the municipality of Bello has been linked by both geographic loca-tion and by the Company’s contribution to the development and quality of life of the people of Bello (known as Bellanitas).

The Obrero (1941), San José (1963) and Santa Ana (1973) neighborhoods (barrios) were born through Fabricato and its housing policy for employees. Other barrios, such as El Carmelo, Salento and Manchester, benefitted from the business contribution of its employ-ees to purchase homes.

Even today, after decades of work, housing programs remain highly valued by employees. When five–year or seniority anniversaries are celebrated, employees state that among the greatest benefits they have received by being employed by Fabricato are the support to pur-chase a home or for their own education or that of their children.

E D U C A T I O N A N D T R A I N I N GTraining is a benefit enjoyed by employees since 1940, when the schol-arship program for children and siblings was instituted; this support con-tinues today.

By the end of 2015, Fabricato had a total of 2,654 employees; 2,240 in Fabricato and 414 in Riotex, of which more than 50% had completed their high school studies; some have technical and technological training and, to a lesser extent, others have higher education and post –graduate degrees.

FABRICATO RIOTEX

7%Primary 195

12%Unfinished

high school 359

51%High School 1.527

12%Technicians 348

11%Technologists 341

6%Professionals 173

1%Specialization 40

0%Masters 9

5%Primary 23

8%Unfinished

high school 37

64%High School 307

8%Technicians 38

13%Technologists 64

2%Professionals 10

0%Specialization 1

-- Sustainability --

-- Annual Report 2015 --

50

Incentives to access formal education also extend to the family group of each one of the employees, thanks to the economic contribution of the Scholarship Fund. In 2015, it amounted to COP 1.240 billion and benefitted 686 employees with the pay-ment of tuition in primary, secondary and higher education.

Employee children have access to the Scholarship Fund and, in many cases, it also benefits their spouses and siblings, who also participate in informal education, such as workshops in painting, sewing and crafts.

But besides contributing to technical, technological or professional training, em-ployees are trained in technical occupations related to the textile activity and other areas of personal growth.

In Fabricato’s history, the permanence of the Workers’ Training Center (Centro de En-trenamiento para Trabajadores) is recorded; it was founded in 1960 to offer courses that instructed them in activities related to the company, and, therefore, in the 1990s, Uni-versidad de la Tela was institutionalized. It is an internal entity in charge of programming

training sessions on topics that the Compa-ny requires and managing learning contracts with higher–education institutions. Its ob-jective is the certification of workers’ skills to perform their jobs through theoretical–prac-tical programs and validations. From 2008 to 2015, 8,935 employees have been certified.

In addition to Universidad de la Tela, Fab-ricato offers opportunities for training in tech-nical and technological programs that con-tribute to increasing the skills of its employees and accessing professional opportunities. As part of this program, in 2015, 14 employees graduated as technicians in logistics; 18 as technicians in electronic and industrial main-tenance, which is an academic program car-ried out in partnership with Coltejer and TCC, and which is expected to conclude in 2017.

On the other hand, each year the Compa-ny conducts induction and training programs. In 2015, the investment was COP 167 million, of which 10% was subsidized through an agreement with SENA (the Colombian Ap-prenticeship Service). Altogether 3,458 em-ployees participated and the total of training hours amounted to 89,605.

FABRICATO

RIOTEX

HOURS OF TRAINING BY PLANT

68.225TOTA

L

21.380TOTA

L

54.415During work hours

13.810During

worker’s time

20.660During work hours

720During

worker’s time

-- Annual Report 2015 --

52 53

A Diploma program in Integrated Management was established with the Metropolitan Technological In-stitute (Instituto Tecnológico Metropolitano, ITM) for production managers; it was attended by 22 supervi-sors. A Diploma program in Cost Management was es-tablished with the School of Engineering of Antioquia (Escuela de Ingeniería de Antioquia, EIA), in which 14 people from the Areas of Costs, Accounting and Engi-neering participated, as well as production heads and managers, in order to acquire tools to adjust the cost structure to be more profitable and more competitive.

Also, the relationship of Fabricato with other edu-cational institutions is given through:

• Scholarships for employees, both administrative and those covered by the collective agreement, who are able to carry out undergraduate and gra-duate programs in different universities in the city.

• The professionalization of employees with techni-cal and technological programs developed on site.

• Participation in summons that allow employees to obtain Government subsidies for up to 50% of the value of specialized continuous –training programs.

• Agreements to conduct specialized programs with universities such as EAFIT, the School of En-gineering of Antioquia (EIA), the Metropolitan Te-chnological Institute (ITM) and the University of Antioquia, among others.

• Internship students from various institutions to contribute to specific projects in the Company.

• Participation in the University, Company and Sta-te Committee, a strategic alliance that brings to-gether institutions from different sectors for joint ventures.

• The SENA –Fabricato agreement allows refresher courses, development and certification of labor skills through programs tailored to the needs of the Company. During 2015, 460 operational sta-ff members participated. In addition, 26 people took part in the Focused Improvement training program, which seeks to incorporate knowledge for analysis and troubleshooting.

In SENA, a course was also taught to qualify forklift operators and thus avoid accidents. It had 78 partici-pants during 4,620 hours.

As additional programs, it is worth noting that some were conducted to protect health, decrease and prevent accidents, as well as offering training courses for working at heights. In these courses there were a total of 219 employees: 45 certified in heights, 166 re-certified and eight certified as coordinators of working at heights.

In the health risk program I Value Myself, I Take Care of Myself (Me valoro, Yo me cuido), which seeks to raise awareness about self –care and the care of the health and physical integrity of workers, 115 people participated.

COP 1.24 Billion were invested in the Scholarship Fund for formal education in 2015, which benefitted 686 employees.

FOOD AND TRANSPORT SERVICEFabricato offers food and transport service to all employees, with an in-vestment that – in 2015 – amounted to COP 4.102 billion.

Food service consists of offering a daily meal at a very low economic cost. The rate is low compared to average market prices and corresponds to the type of contract and salary, with values ranging from COP 50 to COP 3,500 per day. It provides breakfast for the 6:00 AM to 2:00 PM shift; lunch for the 7:00 AM to 5:00 PM shift; supper for the 2:00 to 10:00 PM shift; and dinner for those who work from 10:00 PM to 6:00 AM.

Similarly, all operational staff ben-efit from the transport service, which connects the plants, through existing agreements with transportation com-panies. The routes reach several desti-nations in the Aburrá Valley.

Fabricato has been involved in

the development of the municipality

of Bello.

CORPORATE SOCIAL RESPONSIBILITYThe contribution to the welfare of the Company’s stakeholders is a job that is constantly carried out; it also forms part of Fab-ricato’s history. Its presence in the municipality of Bello led to the commitment to develop that community. The construction of the hospital that is today managed by Nueva EPS, to the hut where Marco Fidel Suárez – 33rd Colombian President from 1918 to 1921 – lived, as well as the creation of entire barrios endowed with water and sewage, and the campus of Colegio La Salle, are evidence of Fabricato’s commitment to the environment, a com-mitment that continues today and leads the Company to plan activities to benefit its inhabitants.

In 2015, under the strategic line “Community Involvement and Social Fabric,” the training program in knowledge of the tex-tile sector stands out. The summons was made in the barrios in the municipality of Bello with the lowest index of social devel-opment; 60 young people answered the summons, of which 11 were hired by Fabricato.

The commitment also extends to having the pensioner pay-roll up to date; in 2015, it amounted to COP 14 billion for 2,200 people (800 directly with Fabricato and 1,400 shared), an eco-nomic resource that is provided even in the difficult financial sit-uations of the Company.

-- Sustainability --

S E P A R A T E F I N A N C I A L

S T A T E M E N T S

A N N U A L R E P O R T 2 0 1 5

56 57

— Separate financial statements —-- Annual Report 2015 --

STATUTORY AUDITORS´ REPORT

ON THE SEPARATED FINANCIAL STATEMENTS

To the Shareholders of Fabricato S.A.

I have audited the accompanying separated financial statements of Fabricato S.A., which comprise the separated statement of financial position as at December 31, 2015 and the separated income statement, statement of comprehensive income, separated statement of chang-es in equity and separated statement of cash flows for the year then ended, and the summary of significant accounting policies and other explanatory notes.

Management is responsible for the preparation and fair presentation of the separated financial statements, in accordance with Accounting and financial information standards accepted in Colombia; of designing, im-plementing, and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatements whether due to fraud or error; and selecting and ap-plying appropriate accounting policies and making estimates that are reasonable in the circumstances.

My responsibility is to express an opinion on these separated financial statements based on my audits. I obtained the necessary information to comply with my functions and performed my examinations in accor-dance with auditing standards generally accepted in Colombia. Those standards require me to comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the separated financial statements are free from material misstatement.

An audit includes examining, on a test basis, evidence supporting amounts and disclosures in the separated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risk of material misstatements in the separated fi-nancial statements. In making those risk assessments, the auditor con-siders the internal controls relevant to the entity’s preparation and fair presentation of the separated financial statements in order to design audit procedures that are appropriate in the circumstances. An audit also includes evaluating the appropriateness of accounting principles used and the reasonableness of significant estimates made by man-agement, as well as evaluating the overall presentation of the financial statements. I believe that my audits provide a reasonable basis for my audit opinion.

In my opinion, the accompanying separated financial statements, taken from the accounting books, present fairly, in all material respects, the financial position of Fabricato S.A., as of December 31, 2015, the results of its operations and the cash flows for the year then ended, in accor-

dance with Accounting and financial information standards accepted in Colombia.

As described in Note 1 of the Separated Financial Statements, on No-vember 7th, 2000, the Company formalized a restructuring agreement with its internal and external creditors, under the guidelines stablished in the Law 550. To the date, we have no evidence that the Company has breached the commitments made in the economic restructuring agreement mentioned above.

Further, based on the scope of my audits, I am not aware of situations indicating that the Company has not: 1) kept minute books, the share-holders’ register and the accounting records in accordance with legal re-quirements and the accounting technique; 2) carried out its operations in accordance with the by-laws and the decisions of the Shareholders’ and of the Board of Directors, and of the rules related with the integral social security; 3) retained correspondence and the accounting vouchers; and, 4) adopted internal control measures for the maintenance and custody of the Company’s assets and those of third parties held by it. Addi-tionally, there is agreement between the accompanying financial state-ments and the accounting information included in the management report prepared by the management, which includes the representation by management on the free circulation of invoices with endorsement issued by vendors or suppliers

Medellín, Colombia February 29, 2016

JUAN CARLOS GONZÁLEZ GÓMEZ

Statutory Auditor Professional Card 54009-T Designated by Ernst & Young Audit S.A.S. TR-530

The undersigned Legal Representative and Certified Public Accountant under whose responsibility the financial statements were prepared, we hereby certify:

As for issuing the statement of financial position at 31 December 2015, and the state of profit or loss and other comprehensive income, statement of changes in equity and cash flow statement for the year ended on that date, which according to the regulations are made available to sharehold-ers and third parties, the statements contained therein and figures taken faithfully from the books have been previously verified.

Such statements, explicit and implicit, are as follows:

Existence: The consolidated assets and liabilities of Fabricato S.A. there on the closing date and recorded transactions have been made during the year.

Integrity: All economic events have been recognized.

Rights and Obligations: The consolidated assets represent probable future economic benefits and liabilities represent probable future economic sacrifices, obtained by Fabricato S.A. on the cutoff date.

Valuation: All items have been recognized by appropriate amounts.

Presentation and disclosure: The economic facts have been properly classified, described and disclosed.

The opening financial statements at January 1, 2014 and transition at December 31, 2014, detail the off-balance figures obtained following the guidelines described in Note 2.6 first-time adoption of Accounting Standards and Financial Reporting accepted Colombia.

CERTIFICATION OF THE SEPARATED

FINANCIAL STATEMENTS

CARLOS ALBERTO DE JESUS

Legal representative LUZ BIBIANA HINCAPIÉ RÍOS

AccountantProfessional Card No. 73063-T

59

— Separate financial statements —

CARLOS ALBERTO DE JESUS

Legal Representative(See attached certification)

LUZ BIBIANA HINCAPIÉ RÍOS

General AccountantProfessional Card # 73063-T(See attached certification)

JUAN CARLOS GONZÁLEZ GÓMEZ

Fiscal AuditorProfessional Card # 54009-T Designated by Ernst & Young Audit S.A.S TR-530(See my inform of February 29 2016)

58

-- Annual Report 2015 --

CERTIFICATION OF FINANCIAL STATEMENTS

LAW 964 OF 2005

CARLOS ALBERTO DE JESUS

Legal representative

General Shareholders’ Meeting of Fabricato S. A.

Medellín

THE UNDERSIGNED LEGAL REPRESENTATIVE OF FABRICATO S. A.

CERTIFIES:

The financial statements and management report corresponding to year 2015 and 2014 do not contain any errors, inaccuracies or flaws that pre-vent knowing the true financial condition or operations of the Company..

The company also certifies that the financial statements were reviewed and approved by the Audit Committee before being submitted for consid-eration by the Board and the General Assembly of Shareholders.

For the record, this certification is signed on February 19th 2016.

Assets Notes 2015 2014 01/01/2014

Current assets

Cash and cash equivalents 5 24.504 9.028 6.661

Trade receivables and other receivables, net 6 93.170 57.337 62.187

Accounts receivable related parties and associated 18 2.324 10.055 39.274

Inventories, net 7 92.917 84.221 83.412

Tax assets 8 7.749 4.950 3.888

Other financial assets 12 670 9 45

Other non-financial assets 1.006 902 1.677

Assets classified as held for sale 9 23 638 5.308

Total current assets 222.363 167.140 202.452

Non-current assets

Property, plant and equipment 9 424.448 422.476 584.826

Investment Property 9 21.528 146.987 5.091

Intangible assets 129 39 -

Investments in subsidiaries, joint ventures and associates 10 115.323 26.815 29.542

Trade receivables and other receivables 6 2.436 4.183 5.438

Accounts receivable related parties and associated 18 5.716 8.084 7.358

Deferred tax assets 11 54.430 57.412 60.247

Other financial assets 12 3.421 3.421 3.421

Total non-current assets 627.431 669.417 695.923

Total assets 849.794 836.557 898.375

SEPARATE STATEMENTS OF FINANCIAL SITUATIONTo 31 December 2015, 2014 and 01 January 2014 / In million of Colombian pesos

See attached notes.

60 61

— Separate financial statements —

CARLOS ALBERTO DE JESUS

Legal Representative(See attached certification)

CARLOS ALBERTO DE JESUS

Legal Representative(See attached certification)

LUZ BIBIANA HINCAPIÉ RÍOS

General AccountantProfessional Card # 73063-T(See attached certification)

LUZ BIBIANA HINCAPIÉ RÍOS

General AccountantProfessional Card # 73063-T(See attached certification)

JUAN CARLOS GONZÁLEZ GÓMEZ

Fiscal AuditorProfessional Card # 54009-T Designated by Ernst & Young Audit S.A.S TR-530(See my inform of February 29 2016)

JUAN CARLOS GONZÁLEZ GÓMEZ

Fiscal AuditorProfessional Card # 54009-T Designated by Ernst & Young Audit S.A.S TR-530(See my inform of February 29 2016)

-- Annual Report 2015 --

Equity and Liabilities Notes 2015 2014 01/01/2014

Liabilities

Current liabilities

Financial liabilities 13 23.842 23.758 33.440

Employee Benefits 14 24.923 21.613 23.173

Other provisions 15 1.606 369 898

Trade payables and other payables 16 42.447 52.215 56.271

Accounts payable related parties and associated 18 3.764 3.832 508

Tax liabilities 17 6.397 5.161 7.116

Total current liabilities 102.979 106.948 121.406

Non-current liabilities

Financial liabilities 13 442 2.874 6.183

Employee benefits 14 103.969 113.935 118.150

Other provisions 15 6.077 5.396 7.350

Trade payables and other payables 16 9.500 8.856 12.856

Deferred tax liabilities 11 70.000 74.669 76.039

Total non-current liabilities 189.988 205.730 220.578

Total liabilities 292.967 312.678 341.984

Equity

Issued capital 19 36.807 36.807 36.807

Issue premium 19 207.194 207.194 207.194

Exercise outcome 33.942 (32.760) -

Accumulated earnings 19 181.734 214.494 214.494

Other comprehensive income (746) 248 -

Reservations 19 97.896 97.896 97.896

Total equity 556.827 523.879 556.391

Total equity and liabilities 849.794 836.557 898.375

SEPARATE STATEMENTS OF FINANCIAL SITUATIONTo 31 December 2015, 2014 and 01 January 2014 / In million of Colombian pesos

See attached notes.

Continuing operations Notes 2015 2014

Ordinary activities income 20 366.231 330.845

Sales cost (318.914) (306.646)

Gross profit 47.317 24.199

Other income 24 17.349 16.495

Distribution costs 21 (2.286) (3.476)

Selling and administrative expenses 21 (15.614) (13.454)

Expenses for employee benefits 22 (16.327) (15.280)

Impairment losses 23 (2.308) (6.028)

Other expenses 24 (12.215) (11.264)

Gain (loss) from operating activities 15.916 (8.808)

Profit from the net monetary position 26 261 43

Financial income 25 1.179 1.436

Financial costs 25 (15.476) (18.411)

Profits (losses) - equity method 27 1.223 (2.725)

Other income from subsidiaries 27 32.593 -

Gain (loss) before taxes 35.696 (28.465)

Tax expense 11 (1.754) (4.295)

Gain (loss) from continuing operations 33.942 (32.760)

Net profit (loss) for the year 33.942 (32.760)

Other comprehensive income

(Losses) profit on defined benefit plans (1.565) 437

Deferred tax components of other comprehensive income 11 571 (189)

Components of other comprehensive income, net of tax (994) 248

Net income (loss) Total comprehensive income for the year 32.948 (32.512)

Basic and diluted Earnings (losses) per share * 3,69 (3,56)

SEPARATE STATEMENTS OF INCOME AND OTHER COMPREHENSIVE INCOME To 31 December 2015, 2014 / In million of Colombian pesos

See attached notes.

* Calculated on the result of the period

62 63

— Separate financial statements —

CARLOS ALBERTO DE JESUS

Legal Representative(See attached certification)

CARLOS ALBERTO DE JESUS

Legal Representative(See attached certification)

LUZ BIBIANA HINCAPIÉ RÍOS

General AccountantProfessional Card # 73063-T(See attached certification)

LUZ BIBIANA HINCAPIÉ RÍOS

General AccountantProfessional Card # 73063-T(See attached certification)

JUAN CARLOS GONZÁLEZ GÓMEZ

Fiscal AuditorProfessional Card # 54009-T Designated by Ernst & Young Audit S.A.S TR-530(See my inform of February 29 2016)

JUAN CARLOS GONZÁLEZ GÓMEZ

Fiscal AuditorProfessional Card # 54009-T Designated by Ernst & Young Audit S.A.S TR-530(See my inform of February 29 2016)

-- Annual Report 2015 --

Equity

Equity attributable to controller owners

TOTAL

Reservations

Issued

capital

Issue

premium

Legal

reserve

Occasional

reserve

Other

reserves

Other

comprehensive

income

Profit for

the year

Collected

earnings

Equity at the beginning of the period - January 2014

36.807 207.194 17.724 41.596 38.576 - - 214.494 556.391

Profit for the year - - - - - - (32.760) - (32.760)

Other comprehensive income - - - - - 248 - - 248

Equity at end of period - December 2014

36.807 207.194 17.724 41.596 38.576 248 (32.760) 214.494 523.879

Profit for the year - - - - - - 33.942 - 33.942

Appropriations results - - - - - - 32.760 (32.760) -

Other comprehensive income - - - - - (994) - - (994)

Equity at end of period - December 2015

36.807 207.194 17.724 41.596 38.576 (746) 33.942 181.734 556.827

SEPARATE STATEMENTS OF CHANGES IN EQUITYTo 31 December 2015, 2014 and 01 January 2014 / In million of Colombian pesos

See attached notes.

SEPARATE STATEMENTS OF CASH FLOWTo 31 December 2015, 2014 / In million of Colombian pesos

2015 2014

Operating activities

Types of cash receipts from operating activities

Proceeds from sales of goods and services 348.909 365.689

Proceeds from royalties, fees, commissions and other revenue 20.799 58.269

Proceeds from premiums and claims, annuities and other policy benefits 1.218 67

Types of cash payment from operating activities

Payments to suppliers for goods and services (297.983) (284.981)

Payments to and on behalf of employees (82.972) (92.553)

Payments for premiums and claims, annuities and other policy benefits (1.384) (1.729)

Payments for value added tax (IVA) (11.458) (6.024)

Net cash flow (used in) from operations (22.871) 38.738

Interest paid (374) (779)

Income taxes paid - (13)Taxes, fees and charges (11.447) (13.261)

Net cash flow (used in) from operating activities (34.692) 24.685

Investing activities

Resources for changes in subsidiary ownership interests 68.250 -

Purchases of property, plant and equipment (10.054) (5.739)

Payments arising from future contracts, forwards, options and swap (392) -

Dividends received 375 270

Other cash inflows 66 251

Net cash flow from (used in) investing activities 58.245 (5.218)

Financing activities

Proceeds from loans 8.411 26.335

Loan refunds (16.757) (43.468)

Other cash outflows (12) (97)

Net cash flow used in financing activities (8.358) (17.230)

Net increase in cash and cash equivalents before the effect of changes in the exchange rate 15.195 2.237

Effects of variations in the exchange rate on cash and cash equivalents

Effects of variations in the exchange rate on cash and cash equivalents 281 130

Net increase in cash and cash equivalents 15.476 2.367

Cash and cash equivalents at beginning of year 9.028 6.661

Cash and cash equivalents at end of year 24.504 9.028

See attached notes.

64 65

— Separate financial statements —-- Annual Report 2015 --

nancial statements based on the Accounting Standards and Financial Reporting accepted in Colombia requires the use of management judg-ment for the application of accounting policies, which are described in Section 2.28.

2.2. CONVERSION OF TRANSACTIONS AND BALANCES IN FOREIGN CURRENCY(a) Functional currency and presentation currency Items included in the financial statements are expressed in the

currency of the primary economic environment in which the entity operates (Colombian pesos). The financial statements are present-ed in “Colombian Pesos”, which is the functional currency of the Company and the presentation currency.

(b) Transactions and balances in foreign currency Transactions in foreign currency are initially recorded at the

exchange rates prevailing at the dates of the transactions. 1. Monetary assets and liabilities denominated in foreign cur-rencies are translated to the functional currency at the end of each period with the exchange rate as market certified by the Superintendencia Financiera de Colombia. Gains and losses differences are recognized in the income statement. 2. Non-monetary items that are measured at historical cost in for-eign currency are translated using the rates prevailing at the date of the transaction. Non-monetary items that are measured at their reasonable value are translated at the exchange rate of the date when the reasonable value is determined.

2.3. CLASSIFICATION OF ASSETS AND LIABILITIESAssets and liabilities are classified according to the intended use or according to their degree of realization, availability, enforceability or liq-uidation, in terms of time and values.

For this purpose, it is understood as current assets those things that will be achievable or available within a period not exceeding one year and as current liabilities, those amounts shall be due or payable also within a period not exceeding one year.

2.4. CASH AND CASH EQUIVALENTSFor purposes of preparing the cash flow statement, the cash and banks and highly liquid investments with maturity less than three months, are considered cash and cash equivalents.

The accompanying cash flow statement was prepared using the di-rect method, which is to redo the income statement using the cash system, primarily to determine the cash flow from operating activities.