accounting and accountability in islamic religious...

TRANSCRIPT

ACCOUNTING AND ACCOUNTABILITY IN ISLAMIC RELIGIOUS ORGANIZATIONS: A CASE STUDY OF PESANTREN IN THE PROVINCE OF NANGGROE

ACEH DARUSSALAM - INDONESIA

by

HASANBASRI

Thesis submitted in fulfillment of the requirements for the degree of

Doctor of Philosophy

October 2010

848323

rb

.Q ttf'; ~ 1 ~ \\~4-4-:rO\O

ACKNOWLEDGEMENTS

As a Muslim, I thank Allah who has given me His blessing, and the

strength to complete my PhD programme at the School of Management, University

of Science Malaysia. I would also like to express my profound gratitude to my

supervisor Dr. Hj.Siti Nabiha Abdul Khalid for her guidance and supervision during

my doctoral study. Her guidance has been invaluable for the completion of my PhD

programme. I am really indebted to her for her friendship and professional support.

My appreciation is also for Dr Amirul Shah Md Shahbudin and Dr Sofri Yahya for

their comments and suggestions.

I also thank all the Muslim scholars that were interviewed, both in

Malaysia and Indonesia, as well as the director and all members of the case

organization for their cooperation. Without their commitment, this thesis would not

have been possible

I would also like to record a word of thanks to my employer, Syiah Kuala

. University, Aceh, Indonesia that has. given me the opportunity and financial support

to undertake this study programme and all my friends both in Malaysia and Indonesia ~

who participated and assisted me in this research. My gratefulness is also addressed

to my wife Qunuti and my daughter Intan Farhana for their support, understanding

and encouragement.

Finally, my deepest gratitude goes to my mother Allahu Yarhamha Hj.

Anisah Abdullah, and my father Allahu Yarharnhu H. Afifuddin Jacob who taught

me sincerity, perseverance and discipline. May Allah provide them with a place for

the righteous in heaven.

11

TABLE OF CONTENTS

ACK.NOWLEDGEMENTS

TABLE OF CONTENTS

LIST OF TABLES

LIST OF FIGURES

LIST OF GLOSSARY AND ABBREVIATIONS

LIST OF CONFERENCE PAPERS

ABSTRAK

ABSTRACT

CHAPTER 1: INTRODUCTION

1.1 Background of the Study

1.2 Statement of the Problem

1.3 The Objectives of the Study

1.4 Research Questions

1.5 Contribution of the Study to Theory and Practices

1.6 The Outline of the Thesis

11

1ll

Vll

Vlll

IX

Xlll

XIV

XVI

1

4

4

5

5

6

CHAPTER 2: ACCOUNTING AND ACCOUNTABILITY- IN NON-PROFIT

ORGANIZATIONS

2.0 Introduction 10

2.1 The Nature of Non-Profit Organizations 10

2.2 Increasing Demand for Accountability in Non-Profit Organizations 12

2.3 Meaning and Conventional Concept of Accountability 14

2.4 The Principles of Accountability in Non-Profit Organizations 17

2.5 Trust and Accountability in Non-Profit Organizations 19

2.6 Competition in Non-Profit Organization Sector 20

2.7 Regulations for Non-Profit Organizations 22

2.8 The Role of Financial Reporting in Enhancing Accountability of

Non-Profit Organizations 26

2.9 Measuring Perfonnance of Non-Profit Organizations 29

2.10 Summary 33

iii

CHAPTER 3: ACCOUNTABILITY IN RELIGIOUS ORGANIZATIONS

3.0 Introduction

3.1 The Nature of Religious Based Organizations

3.2 The Practices of Philanthropy Institutions in an Islamic Context

3.3 Accounting and Accountability in Islam

3.3.1 Accounting and Islam

3.3.2 Accountability in Islam

3.3.2.1 The Essence of Accountability in Islam

3.3.2.2 The Scale of Accountability in Islam

3.4 Previous Researches on Accounting and Accountability Aspects of

Religious Organizations

3.5 The Role of Religious Organizations in Indonesia

3.6 The Brief of Pesantren

3.7 Summary

CHAPTER 4: THE THEORETICAL APPROACHES TO GOVERNANCE

AND ACOUNTABILITY

4.0 Introduction

35

35

38

39

39

42

42

44

47

54

56

61

64

4.1 Agency Theory ~ 64 4.2 Stakeholder Theory 68

4.3 Stewardship Theory 71

44 Summary 74

CHAPTERS: RESEARCH METHODOLOGY

5.0 . Introduction 77

5.1 Qualitative Approach 77

5.2 The Use of the Interpretive Case Study in This Research 80

5.3 Research Design 82

5.4 Techniques for Data Collection 84

5.5 Data Analysis 87

5.6 Grounded Theory 89

IV

5.7 Summary 92

CHAPTER 6: CASE FINDINGS, THE MUSLIM SCHOLAR VIEWS

6.0 Introduction 94

6.1 Good Governance and Islam 95

6.2 The Importance of Accountability in an Islamic Religious Organization 100

6.3 The Role of Accounting and Financial Reporting in Enhancing

Accountability 105

6.4 To Whom Should the Islamic Organization be Accountable? 109

6.5 How to Show Accountability in Islam? 111

6.6 Trust [Amanah] and Accountability 116

6.7 The Role of Accounting: Sacred or Secular Activities 118

6.8 Concerns Regarding the Accounting and the Accountability Practices

in Pesantren 122

6.9 Factors Contributing to the Unsatisfactory Practices of Accounting and

Accountability of Pesantrens 124

6.10 Summary 130

CHAPTER 7: CASE ORGANIZATION FINDINGS

7.0 Introduction 1'33

7.1' Overview of The Case Organization: A Closer Look 133

7.2 Management of Pesantren Peace 139

7.3 Financial Transparency in Pesantren Peace 142

7.4 Accountability Relationship in Pesantren Peace 150

7.5 The Role of Accounting in Pesantren Peace 154

7.6 Internal Control and Financial Arrangement of the Case Organization 159

7.6.1 Receipts 160

7.6.2 Disbursements 162

7.7 The Role of the Board [Foundation Committee] in Enhancing the

Accountability of Pesantren Peace 164

7.8 Summary 168

v

CHAPTER 8: DEVELOPING THEORIES

8.0

8.1

8.2

Introduction

The Central Phenomenon

Conditioning Context

8.2.1 Religious and Secular Divide

170

172

173

174

8.2.2. Accountability Mechanisms: To whom and How? 175

8.2.3 The Implementation of Accounting and Accountability

in the Islamic Religious Organizations 183

8.3 Summary

CHAPTER 9: CONCLUSION, RESEARCH CONTRIBUTIONS,

LIMITATIONS AND RECOMMENDATIONS

9.0 Introduction

9.1 Recapitulation

9.1.1 Theoretical Contributions

9.1.2 Practical Contributions

9.2 Limitations of the Research

9.3 Suggestions for Future Researches

REFFERENCES

APPENDICES

191

193

193

195

203

204

204

't

206

Appendix A: The list of people interviewed 223

Appendix B: Linkage Between Research Questions, Data Sources and Method 226

vi

LIST OF TABLES

Table 3.1 The Criteria Used to Determine the Types ofPesantren in the NAD

Province.

. Table 4.1 Comparison of Three Governance Theories

Table 7.1 A Summary a Various Accountability Tools Used By

Pesantren Peace

Vll

Page

58

73

152

Figure 2.1

Figure 2.2

Figure 4.1

Figure 5.2

Figure 7.1

Figure 7.2

Figure 7.3

LIST OF FIGURES

Page

Accountability Relationship: A Summarized Picture of Theoretical

Insight 16

The Financial Reporting System 28

A Generalized Accountability Model 67

The Data Analysis Process 88

Organization Structure ofKita Foundation 134

Organization Structure of Pesantren Peace 141

The Financial Accountability Relationship Adopted by

Pesantren Peace. 153

Vlll

LIST OF GLOSARIES AND ABBREVIATIONS

Amanah: The Arabic tenn, meaning the trust or responsibility

Baitul-Mal: An Islamic institution responsible for the administration and distribution of zakat revenues for disadvantaged Muslims.

BAZIS: The abbreviation of Badan Amil Zakat Infaq dan Shadaqah [Zakat Infaq and Sadaqah Collector Board], an organization established in 1968 by the government of Indonesia to manage Zakat, infaq and sadaqah in Indonesia.

Badan Pembinaan dan Pendidikan Dayah [ Dayah Supervisory and Development Agency):

A government agency established in 2008, by the government of Nanggroe Aceh Darussalam (NAD) province- Indonesia that primarily responsible for pesantren development in the NAD province.

BandaAceh: The name of the capital city of the NAD province, Indonesia

Bupati [Regent]:

BRR:

BOS:

Dayah:

Fiqh:

Haram:

The head ofKabupaten [District] in Indonesia.

The abbreviation of Badan Rehabilitasi dan Rekonstruksi [Rehabilitation and Reconstruction Board], the organization established on April 16, 2005 by Indonesian government to implement Aceh and Nias post-tsunami r~construction.

The abbreviation of "biaya operasioanal sekolah", refers to special financial aid from government agencies such as from Department of Religious Affair to cover operating cost of schools 't

Acehnese tenn for Islamic boarding school. The name of Dayah come from the Arabic word "Zawiyah" which literally means a comer, which was believed by the Acehnese to have been first used for the comer of the mosque of Madinah where Prophet Muhammad taught the people. This zawiyah word is pronounced as Dayah by Acehnese. In spite of this, the tenn of pesantren is now more popular and commonly used by the people in the province of Nanggroe Aceh Darussalam.

An Arabic tenn meaning "deep understanding" or "full comprehension". Technically it refers to the science of Islamic law extracted from detailed Islamic sources (which are studied in the principles of Islamic jurisprudence).

The Arabic term, meaning "forbidden". In Islam it is used to refer to anything that is prohibited by the faith.

IX

Haj:

Hesab:

Hijab:

Infaq:

Kitab:

A pilgrimage to Mecca during the month of Dhu'l Hijja, made as an objective of the religious life of a Muslim

In its generic sense, relating to one's obligation to "account" to God on all matters pertaining to human endeavor, for which every Muslim is accountable.

The Arabic term, frequently used in Malaysia, refers to the dress worn by Muslim women that cover hair and neck.

An Arabic word meaning charity simply to please God without asking for any favor

An Indonesianised Arabic word, meaning book. In Bahasa Indonesia, the meaning changes to religious books, e.g. Kitab kuning, Kitab Al Qur'an etc.

Kitab kuning: Classical Islamic texts book written in Arabic. Called kuning, yellow, after the tint paper of books brought from middle East in the early twentieth.

Kyai: An Indonesian "Jawa" term indicating an Islamic scholar, teacher and leader of pesantren. Kyai is always male.

Khalafi: An Indonesianised Arabic word indicating something modem.

Khalifah: The Arabic word, meaning successor or substitute. It is used in the Qur' an to establish Adam role as representative of Allah on earth. The more general meaning of khalifah refers to the successor of Prophet Muhammad.

Madrasah: An Arabic word, literally, a place of learning, in Indonesia this term means an Islamic school.

Madrasah Tsanawiyah: The term used referred Islamic junior high school

Madrasah A'liyah:

Mudir:

Mufti:

Nahwu:

Nash:

The term used referred to Islamic senior high school

An Indonesianised Arabic Word, meaning the top leader ofPesantren.

A Muslim legal expert and adviser on the Islamic law.

A subject: Arabic grammar

An Indonesianised Arabic word indicating sources from Qur'an and Sunnah.

x

NAD:

NPOs:

NGO:

The abbreviation of Nanggroe Aceh Darussalam referred to the name of one of the province in Indonesia. This province is the only part of Indonesia which has the legal right to apply Islamic law.

The abbreviation of non profit organizations

Non governmental organization

Perkumpulan: The Indonesian tenn of association, referred to a type of legal entity for non profit exists in Indonesia.

Pesantrell: The word referred to the name of traditional Islamic boarding school operating in Indonesia. There has been a controversy about the origin of pesantren in Indonesia. However the speculation tend to say that the origin of pesantren has very strong relationship with educational institution that existed prior to the arrival of Islam in Indonesia. It was then continued through the process of adjustment and changed.

PBUH: The abbreviation of peace be upon him, a phrase that practicing Muslim often say after saying or hearing the name of prophet of Islam

Riba: Literally means 'to grow; to increase.' Technically, it denotes the amount that a lender receives from a borrower at a fixed rate in excess of the principal. It is of two kinds: 1. Riba Nasi'a - taking interest on loaned money. 2. Riba Fadal - taking something of superior quality in exchange for

giving less of the same kind of thing of poorer quality

Sadaqah: Donation to others only to please Allah and to get His nearmess .Any kind of help which you give to others in cash or ill any form is an act ofsadaqah.

Shalat:

Santri:

Saraf:

Sirah:

Shari'ah:

Sunnah:

The second pilar of Islam, it is a prescribed liturgy performed five times a day and oriented toward Mecca

A pesantren student

Arabic morphology

The Arabic tenn used to the various traditional Muslim biographies, and it was first used in the literature for the biography of the Prophet Muhammad.

The Arabic term meaning the Islamic law. It is a comprehensive code of life regulating the entire spiritual and material life of Muslim.

The Arabic word, lexically, means road or practice. In hadith terminology it denotes any saying, action, approval, or attribute whether physical or moral ascribed to the Prophet, whether before or after the beginning of his prophethood.

Xl

Sahabah:

Salaft:

Tengku:

Ulama:

Umma:

Ustad:

Waqaf:

Yayasan:

Zakat:

Refers to some one who saw the Prophet Muhammad PBUH and believed in him as well as died as Muslim

An Indonesianised Arabic word indicating something traditional.

The title given to religious leaders, e.g. Leader of Mosque, Leader of pesantren. Tengku is always male.

An Indonesianised Arabic word, meaning Muslim scholars

The Muslim community.

An Indoriesianised Arabic word, meaning a ma1e teacher

The Arabic term. It is an Islamic endowment, literally means hold, confinement or prohibition. This word is used in Islam in the meaning of holding certain property and preserving it for the confined benefit of certain philanthropy and prohibiting any used or disposition of it outside that specific objective.

The Indonesian term of foundation, referred to a type of legal entity for non profit organization exists in Indonesia.

Arabic word (almsgiving), it is one of the five pillars ofIslam and it is an obligatory payment made once a year under Islamic law which is used for charity and religious purposes.

XlI

LIST OF CONFERENCE PAPERS

1. Hasan Basri and A.K., Siti-Nabiha (2007) Accounting and Accountability in Faith Based organizations: The Case of Islamic Institutions, 3rd

UNIT.I!-"'N International Business Management, Melaka, Malaysia, December 16-18.

2. Hasan Basri and A.K., Siti-Nabiha (2009) Accountability in Islamic Religious Organizations: The View of Muslim Scholars, r' International Seminar on Islamic Thought, National University of Malaysia, Kuala Lumpur, Malaysia, October 6-7.

3. Hasan Basri and A.K., Siti-Nabiha (2009) Accounting and Accountability in Islamic Religious Based Organizations: The Case of Pesantren in Indonesia, 1 dh Asian Academic Accounting Association Annual Conference, Kadir Has University, Istanbul, Turkey, November 15-18.

4. Hasan Basri and A.K. Siti Nabiha (2010) Towards Good Accountability: The Role of Accounting in Islamic Religious Organization. The International Conference on Business, Economics and Finance, World, Academy of Science, Engineering and Technology, Paris, France, June 28-30, 2010,

Xlll

PERAKAUNAN DAN AKAUNTABILITI ORGANISASI ISLAM: KAJIAN KES PESANTREN DI WILAYAH NANGGROE ACEH DARUSSALAM,

INDONESIA

ABSTRAK

Kajian ini meneliti persepsi Sarjana Muslim mengenai bagaimana

sesebuah organisasi Islam mendemonstrasikan akauntabiliti kewangan mereka dan

peranan laporan kewangan dalam meningkatkan akauntabiliti, serta praktis

perakaunan dan akauntabiliti di sebuah pesantren yang terpilih di daerah Nanggroe

Aceh Darussalam (NAD), Indonesia. Kajian ini menggunakan kaedah kualitatif di

mana data secara umumnya diperolehi daripada temu bual berbentuk separa-

struktur, semakan dokumentasi yang berkaitan dan juga pemerhatian aktiviti seharian

di pesantren.

Hasil daripada temubual bersama para sarjana Muslim mendapati bahawa,

terdapat kerisauan dalam praktis perakaunan dan akauntabiliti di organisasi-

organisasi Islam. Majoriti sarjana Islam yang ditemubual menyatakan bahawa

~

organisasi-organisasi Islam mempunyai kewajipan untuk bertanggungjawab kepada

masyarakat, seperti pemberi sedekah, penerima dan juga kepada Tuhan. Mereka

menekankan bahawa akauntabiliti di dalam Islam difahami dalam konteks yang lebih

luas daripada apa yang difahami secara konvensional, di mana ia tidak

mengambilkira hubungan luar daripada masyarakat. lni dengan secara jelas

dinyatakan bahawa aktiviti perakaunan dan akauntabiliti memainkan peranan yang

penting semasa sejarah Islam dan aktiviti-aktiviti tersebut adalah sebahagian

daripada aktiviti keagamaan kerana Islam tidak membezakan di antara aktiviti

keagamaan dan aktiviti keduniaan.

XIV

Dalam konteks kes organisasi kaj ian , pengurusan Pasantren "Peace"

melihat laporan kewangan sebagai satu instrumen yang mempunyai peranan yang

sangat penting dalam meningkatkan akauntabiliti, dan aktiviti perakaunan dilihat

sebagai aktiviti yang tidak bertentangan dengan misi pesantren. Walau

bagaimanapun, tanggapan umum mengenai aktiviti perakaunan di kes organisasi ini

kurang dibangunkan dan hanya memfokuskan kepada pengawalan penerimaan dan

pengeluaran dana yang hanya dilaporkan melalui penyediaan laporan-Iaporan

bulanan dan tahunan pengeluaran dan penerimaan, dimana, kebanyakan hanya

digunakan untuk tujuan akauntabiliti sahaja. Tiada laporan kewangan gabungan yang

dihasilkan yang menggambarkan keadaan kewangan organisasi secara keseluruhan.

Pengurusan dan kakitangan organisasi tersebut melihat bahawa mereka

bertanggungjawab terhadap tiga tahap "stakeholder", dimana secara asasnya terdiri

daripada menaik, mendatar dan menurun. Tambahan pula, kes organisasi ini juga

mengakui Tuhan dalam hubungan akauntabiliti. Walaupun demikian, kesanggupan

kes organisasi ini dalam menerapkan akauntabiliti kepada "stakeholder" tidak

terlepas daripada penguatkuasaan pihak-pihak lain.

xv

ACCOUNTING AND ACCOUNTABILITY IN ISLAMIC RELIGIOUS ORGANIZATIONS: A CASE STUDY OF PESANTREN IN THE PROVINCE

OF NANGGROE ACEH DARUSSALAM - INDONESIA

ABSTRACT

This study concerns the perceptions of Muslim scholars regarding

how the Islamic religious organizations demonstrate their financial

accountability and the role of financial reporting in enhancing such

accountability, as well as the practice of accounting and accountability in a selected

pesantren in the Nanggroe Aceh Darussalam (NAD) province, Indonesia. The study

takes a qualitative approach in which the data is mainly derived from semi-structured

interviews and relevant documentary materials as well as observation of the

pesantren daily life.

The findings suggest that the "Muslim scholars" interviewed have

concerns regarding accounting and accountability practices in Islamic religious

organizations. The majority of Muslim scholars interviewed pointed out that Islamic

religious org~zations have an obligation to be accountable to society, such as to~the

donors and their beneficiaries and to God as well. They emphasize that

accountability in Islam is understood as being broader than what is generally

understood in conventional accountability, which is not deemed to extend beyond

human society. It is clearly stated that accounting and accountability activities playa

very significant role in Islamic history and that they are part of the sacred activities,

as the division between religious and secular is unknown in Islam.

In the context of case organization, the management of Pesantren Peace

views the financial report as an instrument that plays a very significant role in

enhancing accountability, and that accounting activities are viewed as activities that

XVI

have no contradiction with the pesantren mission. However, accounting practices in

the case organization are less developed and only focuses on the control of receipts

and the disbursement of funds through providing monthly and annual cash receipts

and cash disbursement reports, which are mainly used for accountability purposes.

There is no consolidated financial report provided to picture the organization's

overall financial condition. The management and their staff .see themselves as

accountable to three levels of stakeholders, which are typically upward, lateral, and

downward. In addition, this case organization also recognizes God in the

accountability relationship. However, the willingness of this case organization to

demonstrate its accountability to its stakeholders is not free from the enforcement of

other parties.

XVll

CHAPTER 1

INTRODUCTION

This chapter describes the background and objectives of the study. It begins with a

brief discussion of the role of accounting and accountability practices in non-profit

organizations, particularly, religious organizations and how they lead to the current

study. Then, the problem statement is presented followed by the objectives of the

study, a brief explanation of the research questions and contributions of the research

to theory and practice. Finally, this chapter provides an outline of the contents of the

remainder of the thesis.

1.1 Background of the Study

Over the last 20 years, non-profit organizations (NPOs) 1 have become

important providers of social services in many countries. Of the several million

NPOs in existence, an increasing nwnber of organizations define themselves as

religious, spiritual, or faith-based NPOs (see Berger, 2003). The scope, scale and ~

range of non-profit organizations activities focus not only on the traditional domain

of charity but include other services such as job training, community and economic

development, housing, substance abuse programmes, refugee placement, and others.

Examples of such organizations are the Salvation Army, World Vision, and Catholic

Relief Services, which, together, enjoyed a combined annual revenue of over US$I.6

billion and claimed an outreach of nearly 150 million in 2001 (Berger, 2003). Major

sources of these non-profit organizations' funding come from membership dues,

I There are many terms used to describe non-profit organizations (NPOs) such as independent, third sector, voluntary, charitable, philanthropic, social, public benefit, faith-based, tax exempt, non governmental organization or civil society organization (Cameron, 2004). The term used in this thesis is non-profit organization.

1

grants from government and private donations. Some NPOs depend heavily on

governments for their funding. Such dependence on government funding has

increased over the years (Hall, 2002).

Similarly, Islamic-based religious organizations play an important role in

society, especially, in the Muslim world. In Muslim society, the total amount of

philanthropic giving is estimated to range between $250 million to $1 trillion

annually (see Alterman, Hunter, and Philips, 2005). Clearly, Islamic and other types

of religious organizations make up a significant proportion of organizational

activities in many countries, and tend to control a sizeable proportion of human,

financial and other resources of that society.

In Indonesia, the country with the largest Muslim population, Islamic

religious organizations have provided services for society. One of the most important

institutions is the pesantren, an Islamic boarding school that provides education

services at minimal cost to students. Poor Indonesian families who cannot send their

children to public schools rely on religious schools or pesantren, to provide at least

some form of education (Bremer, 2004). Currently, there are 14,656 pesantrens . It

(Islamic Boarding Schools) operating in the country (see Directorate of Religious

Education and Pesantren, 2005, p. 18).

However, accounting and accountability practices in the religious

organizations are not developed and lack proper financial control (Siino, 2004). As

such, there has been a call for good accounting and accountability practices in these

organizations. Since they are viewed as a public trust, existing for the benefit of

society, they are accountable to society for the resources received. The management

of religious organizations are argued to be agents of the public whose duties include

ensuring the proper functioning of the organization. Furthermore, accountability is

2

regarded as more important in these organizations because of the various financial

scandals and lawsuits involving them Some examples of fraudulent practices in this

type of organization are the theft by leaders of the Episcopal and Baptist churches

and improper use of funds by the head of the National Association for the

Advancement of Colored People (see Keating and Frumkin, 2001; Hamilton, 2006).

Even though religious organizations make up a significant proportion of

organizational activity in many countries and tend to control a sizeable proportion of

human, financial and other resources of society, there is still a lack of knowledge

about accountability practices. There has been growth in research concerning

religious organizations as noted by many researchers (see Laughlin, 1988, 1990;

Walker, 2002; Booth, 1993; Rahim and Goddard, 1998; Lewis, 2001, 2006), but

there are only a few researches that have directly examined the issues of accounting

in religious organizations (Booth, 1993). Most researches in this area have focused

on economic and political factors. Only recently, have researchers begun to look at

some of the broader, managerial issues of non-profit organizations. Consequently,

there is a growing amount of literature on non-profit organizations that attempts to ~

understand accounting and accountability as an organizationally situated practice.

However, only a limited number of researchers have examined Islamic religious

organizations, especially those that provide education. These types of organization

play an important role in society, especially in Indonesia.

In the province of Nanggroe Aceh Darussalam, the only part of Indonesia

that has the legal right to apply Islamic law (shari'ah), there are 852 Dayah (they are

typically called pesantren elsewhere in Indonesia) in 2007? These pesantrens are

mainly owned by foundations and private owners. As such, their operations mainly

2 Sources: The Department of Religious Affairs, Banda Aceh-Indonesia.

3

depend on public trust. Due to the lack of information regarding financial

accountability in these organizations, there seems to be a perception that the majority

of pesantrens lack transparency and have no accountability to the public, especially

their donors.

Thus, the issues regarding research on accounting and accountability in

Islamic religious organizations have been generally unexplored in accounting

academic literature (see Carmona and Ezzamel 2006). Hence, a study is needed to

examine accounting and accountability practices in Islamic religious organizations.

1.2 Statement of the Problem

Literature on accounting and accountability practices in non-profit

organizations indicates that accounting and accountability in religious organizations

are less developed and that there is a lack of financial control. This is evidenced by. a

number of examples in which the mechanism of religious non-profit organizations -

the collection of resources from donors and its redistribution for charitable purposes

- has been misused or misappropriated (see for example, Siino, 2004; Keating and It

Frumkin, 2001; Hamilton, 2006). However, the abuse of this financial control often

occurred without the knowledge of the donor or even of members of the management

and staff of the organization itself.

1.3 The Objectives of the Study

The objective of this study is to discuss the views and opinions of Muslim

scholars about organizational accountability in Islam and to empirically investigate

the phenomenon of the practices of accounting and accountability in one of Islamic

religious organizations ''pesantren'' as well as to understand how these practices

4

relate to the' belief systems held by the pesantren and organizational aspects of

pesantren

1.4 Research Questions

This research will seek to answer the following research questions:

1. What are the conventional views of accountability?

2. What are the Muslim scholars' views of accountability and the role of

financial reporting in enhancing accountability of Islamic religious

organizations?

3.' Do pesantrens show accountability to their stakeholders?

(i) If yes, how and in what way do they show their accountability?

(ii) If no, why not?

4. What are the control systems and mechanisms practiced by pesantren?

(i) How are the funds received from various sources administered?

(ii) How are the funds of the organization being spent?

1.5 Contribution of the Study to Theory and Practices

This study will provide an understanding and explanation of the practices

of accounting and accountability in pesantrens. As such, this study makes a

contribution to accounting and accountability research in religious organizations.

Since this study is undertaken on pesantren, it contributes to much needed literature

concerning accounting and accountability research in such organizations.

Furthermore, this study contributes to the theory and practice of management

accounting in the religious based organizations, especially in Islamic organizations.

5

As a qualitative research, this study aims to generate or develop theory.

Therefore, additional theoretical insights concerning the issues of accounting and

accountability in Islamic religious organizations will be obtained. In addition, a

better understanding of accounting and accountability practices in religious

organizations will be beneficial to practitioners as guidance for implementing good

accounting and accountability practices in Islamic religious organizations. Moreover,

the result of this study is also expected to contribute to better management and

monitoring of pesantren by both government and non-profit umbrella organizations

through the development of regulations to promote better accounting and

accountability practices within Islamic religious organizations.

1.6 The Outline of the Thesis

This thesis is organized into 9 chapters, Chapter One is the introduction.

This chapter explains the background of the study and demonstrates the reasons that

influence the choice of this topic of study, statement of the problem, the objective of

the study, research questions, and contributions of the study as well as the outline of . it

the thesis.

Chapter Two provides a literature review on accounting and accountability

in non-profit organizations. It starts with a brief explanation of the nature of non-

profit organizations and the increasing demand for accountability in non-profit

organizations. It is followed by discussions of the meaning and conventional concept

of accountability and the explanations of the principles of accountability in non-

profit organizations. This chapter also describes trust and accountability in non-profit

organizations as well as competition in the non-profit organization sector. It then

proceeds to discuss the government regulations for non-profit organizations in

6

Indonesia and the role of financial reporting in non-profit organizations

accountability. Lastly, this chapter discusses measuring performance of non-profit

organizations.

Chapter Three reviews a number of studies of religious organizations. It

begins with the nature of religious based organizations. This is followed by a review

of the literature concerning the practices of philanthropic institutions within an

Islamic context and accounting and accountability in Islam. It then proceeds to

discuss previous researches on the accounting and accountability aspect of religious

organizations, followed by a discussion of the role of religious organizations in

Indonesia. Finally, the chapter provides explanations concerning the brief of

pesantrens .

Chapter Four discusses the theoretical approaches which are commonly

used in corporate governance and accountability researches. It begins with a

discussion of the agency theory. This is followed by the stakeholder theory and

stewardship theory.

Chapter Five explains the research methodology that was employed for ~

this study. It starts with a discussion of the qualitative approach and the justifications

for using interpretive case study research. Subsequently, the research design,

techniques for data collection and data analysis within qualitative research are

explained. The chapter ends with the justifications for using grounded theory of this

research.

Chapter Six presents the data findings that focus on Muslim scholars'

views of accountability and the role of financial reporting in enhancing

accountability in Islamic religious organizations as well as their related issues. The

chapter starts with a discussion concerning good governance and Islam. It then

7

proceeds to discuss the importance of accountability in religious Islamic

organizations. This is followed by a discussion of the role of accounting and

financial reporting in enhancing accOlmtability and to whom that the Islamic

religious organizations should be accountable. The chapter also examines how

accountability should be shown in Islam and the issues pertaining to accountability in

the relationship between trust (amanah) and accountability as well as descriptions of

sacred and secular activities. Finally, concerns regarding the accounting and the

accountability practices in pesantrens and factors contributing to the unsatisfactory

practices of accounting and accountability of pesantrens are also discussed in this

chapter.

In Chapter Seven, the findings from the case organization are presented.

First, a detailed overview of the case organization is provided. This is followed by a

description of the management of the case organization. It then proceeds to explain

the financial transparency of case organization and its accountability relationship.

This chapter also describes the role of accounting in case organization as well as the

arrangement of fund received and spent by the organization. The chapter ends with a It

section explaining the role of the board (foundation committee) in relation to

enhancing the accountability of the case organization.

Chapter Eight presents the emergent theoretical insights of the research

findings. The chapter begins with a discussion of the core or central phenomenon

generated by the study. It then proceeds to discuss the conditioning context, which

consists of religious and secular divide, accountability mechanism: to whom and how

accountability should be demonstrated, and the implementation of accounting and

accountability in Islamic religious organizations.

8

Chapter Nine offers some conclusions, starting with a recapitulation of the

study. The chapter is then continued by presenting the theoretical contributions and

practical contributions of the study. The chapter ends with the explanation of

limitations of the study and brief suggestions for future researches.

~.

9

CHAPTER 2

ACCOUNTING AND ACCOUNTABILITY IN NON-PROFIT

ORGANIZATIONS

2.0 Introduction

This chapter provides a review of the literature on the topic of accounting

and accountability in non-profit organizations. The purpose of this chapter is to gain

an understanding of the accounting and accountability concept of non-profit

organizations. Various aspects of the concept of accountability and its related topics

will be discussed in this chapter. A search of the pertinent literature reveals that

several studies have been undertaken to examine accounting and accountability

practices in non-profit organizations. It starts with a brief explanation of the nature of

non-profit organizations and the increasing demand for accountability in non-profit

organizations. This is followed by a discussion of the meanings and conventional

concepts of accountability and an explanation of the principles of accountability in

non-profit organizations. This chapter also discusses the issues of trust and 't

accountability as well as competition in non-profit organizations. It then proceeds to

discuss the government regulations for non-profit organizations in Indonesia and the

role of financial reporting in non-profit organizations. Lastly, this chapter discusses

measuring the performance of non-profit organizations.

2.1 The Nature of Non-profit Organizations

Non-profit organizations differ from profit organizations in a number of

ways. Some of the non-profit organizations carry out activities for the benefit of

their members, while others carry out activities for the public benefit. Traditionally,

10

there are two types of non-profit organizations recognized by civil law; an

organization of persons (individuals), typically called an "association" and

r: organizations involving the dedication of material resources, typically called a

'"" t "foundation" (Simon, 2005, p.12).

A study on global civil society as quoted by Asia Pacific Philanthropy

Consortium (2006, p.l) provides the following four structural-operational features

that define an organization within the non-profit organizations sector. The features

are:

• Organized, i.e., they have some structure and regularity to their opemtions, whether or not they are formally constituted or legally registered. More than legal or formal recognition, this qualification stresses organizational permanence and regularity, reflected in regular meetings, a membership, and legitimate decision-making structures and procedures.

• Private, i.e., they are not primarily commercial in purpose and do not distribute profits to a set of directors, stockholders, or managers. While NPOs may generate a surplus from time to time, they must reinvest these resources back into the objectives of their respective organizations.

• Self-governing, i.e., they h~ve their own mechanisms for internal governance, they are able to cease operation on their own authority, and are fundamentally in control of their own affairs.

• Voluntary, i.e., membership or participation in them is not legally required or otherwise compUlsory. ~ .

It is argued that these four characteristics encompass both formal and

informal, religious and secular, those with paid staff and those staffed entirely by

volunteers and organizations performing expressive functions (i.e., advocacy,

cultural expression, community organizing, environmental protection, human rights,

religion, representation of interests, and political expression) as well as those

performing service functions (i.e., provision of health, education and welfare

services) (Asia Pacific Philanthropy Consortium, 2006).

11

Clearly, non-profit organizations exist for the benefit of the community

and not for that of the management or their owners. This kind of organization is

prohibited from distributing income to a set of directors, managers, individuals or

any private shareholders. This is due to the absence of ownership of non-profit

organizations themselves. Both management and the board of the organizations are

expected to operate as agents in the public's interest in ensuring the proper

functioning of the organizations.

2.2 Increasing Demand for Accountability in Non-profit Organizations

The current environment is making increased accountability a fact of life

for profit and non-profit organizations alike. The public want to be assured that their

investment in both types of organization is being properly managed. This can be seen

as a response to the growing number of lawsuits against those organizations resulting

from bribery or misuse of resources.

Every non-profit organization operates in society on the basis of public

trust to provide some social services. Therefore, it is accountable to society for the ~

resources received from the society. Without doubt, donors are more discerning than

ever before. They want to know "where the $$ go!" (Campbell, 1998, pAO). Donors

today are looking at the relative value of work for each non-profit organization they

are thinking about supporting. They are looking critically at the accomplishments of

the organizations, and some donors are even scrutinizing accounting documents to

determine just how effective and efficient these organizations really are (see,

Campbell, 1988; Ensman, 1996).

According to Herman and Renz (1998, pA) "non-profit organizations

(NPOs) are increasingly being required to become more accountable for

12

demonstrating that they are making a difference and delivering results". This means

there is the perception that most non-profit organizations have not shown their

accountability to their stakeholders. Seen from this point of view, the stakeholders

have put more emphasis on people or organizations being accoWltable and for the

accountability process to be made more transparent.

The demand for accoWltability in non-profit organizations has come from

the government, third party actors and the media (Lee, 2004). It is agued that with

more state funds being disbursed to non-profit organizations, governments will

definitely demand higher levels of accountability. Third party actors, such as

corruption watchdogs, have also played a significant role in the emergence and

emphasis of accoWltability by non-profit organizations. In addition, the media has

reported quite widely on the matters of accoWltability in non-profit organizations

(see Eisenberg, 2005).

The increased demand for accountability of non-profit organizations has

come from various stakeholders with sometimes different demands to be satisfied

(Mark and Brown, 2001). Donors demand that the non-profit organizations be ~ .

accountable for the integrity, efficiency, and impact of programmes that they have

funded. Beneficiaries press non-profit organizations to live up to their rhetoric about

fostering locally-determined development rather than imposing their own priorities.

The internal staff expects non-profit organizations to live up to the high purposes that

drew their commitment to the enterprise. Partners who non-profit organizations have

recruited in their efforts to achieve their goals (such as other non-profit

organizations, government agencies, businesses) expect the non-profit organizations

to live up to promises they made in forging their partnerships. Even those who are

the targets of non-profit organizations demand a kind of accountability from them.

13

They want to know to whom the non-profit organizations are accountable and for

whom the non-profit organizations speak so that they can gauge the force and

1\ legitimacy of the claims that these organizations are making against them (Mark and f ~

Brown, 2001).

Thus, non-profit organizations have various stakeholders to whom they

might owe the accountability. The problems of accountability usually arise because

the claims of the various stakeholders are sometimes not necessarily coherently

aligned with one another. Consequently, the leaders of the non-profit organizations

have to make choices to embrace or resist particular stakeholders and this can have a

profound impact on their missions. This, of course, creates difficulty for non-profit

organizations since resisting demands for accountability from specific stakeholders

can weaken their support. Financiers may withdraw support to non-profit

organizations that are seen as unwilling to be accountable for the efficient use of

resources. Committed staff can stop working hard if the non-profit organization fails

to embody the values and missions that brought them to the organization (Mark and

Brown, 2001).

2.3 Meaning and Conventional Concept of Accountability

The concept of accountability has attracted considerable research interest

m various academic disciplines. Accountability has been used to describe the

responsibility of those who manage or control resources to others (Coy and Pratt,

1998). The concept, in general, shows a relationship between two parties in which

one party, whether it is an individual, group, company, government, or organization,

is directly or indirectly accountable to another party for something, such as an action,

process, output, or outcome (Kearns, 1994; Walker, 2002). However, the precise

14

meaning and implications of this concept are still vague. There are various

conceptualizations of accountability, from a literal view that is mainly concerned

with reporting activity, to encompassing activities in providing explanation or

justification of actions. The concept has sometimes been related to the presence of a

contractual relationship between two parties for particular actions. Gray et aI., 1987,

as quoted by Laughlin (1990, p.96) say that "accountability only occurs when

contracts are in existence between principal and agent". This means that

accountability occurs if contracts exist between the one who holds to account and the

one who accounts.

Paul (1991) as noted by Keams (1994, p.186) says that accountability is

"holding individuals and organizations responsible for performance measured as

objectively as possible". This definition means an individual or organization being

answerable to a higher authority for action taken and for handling resources they

received.

A broader definition of accountability is given by Romzek and Dubnick

(1987) as quoted by Keams (1994, p. 187) "accountability involves the means by , which public agencies and their workers manage the diverse expectations generated

within and outside the organization". This definition contains elements not found in

other previous definitions. It introduces an element of strategy wherein management

attempt to forecast diverse expectations and position their agency for proactive as

well as reactive response. The managers' role is transformed from a passive one into

one of active participation in framing and articulating the standards by which they

are judged.

15

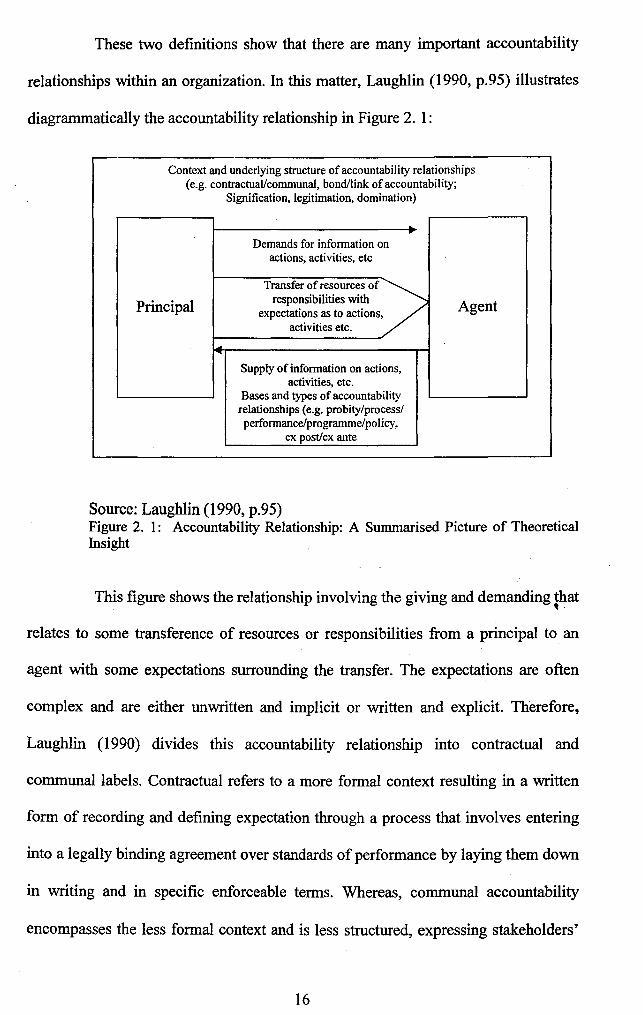

These two definitions show that there are many important accountability

relationships within an organization. In this matter, Laughlin (1990, p.95) illustrates

diagrammatically the accountability relationship in Figure 2. 1:

Context and underlying structure of accountability relationships (e.g. contractuaVcommunal, bond/link of accountability;

Signification, legitimation, domination)

Demands for information on actions, activities, etc

Transfer of resources of ~

Principal responsibilities with Agent expectati~n~ .as to actions/ actiVIties etc.

Supply of information on actions, activities, etc.

Bases and types of accountability relationships (e.g. probity/process/ performance/programme/policy,

ex post/ex ante

Source: Laughlin (1990, p.95) Figure 2. 1: Accountability Relationship: A Summarised Picture of Theoretical Insight

This figure shows the relationship involving the giving and demanding that 't .

relates to some transference of resources or responsibilities from a principal to an

agent with some expectations surrounding the transfer. The expectations are often

complex and are either unwritten and implicit or written and explicit. Therefore,

Laughlin (1990) divides this accountability relationship into contractual and

communal labels. Contractual refers to a more formal context resulting in a written

form of recording and defining expectation through a process that involves entering

into a legally binding agreement over standards of performance by laying them down

in writing and in specific enforceable terms. Whereas, communal accountability

encompasses the less formal context and is less structured, expressing stakeholders'

16

needs through consultation and seeking their involvement in the decision-making

process (see Laughlin, 1990; Demirag et aI., 2004).

However, Roberts and Scapens (1985) view accountability as a moral

order that involves a system of reciprocal rights and obligation. This means that the

parties are bound up not only in narrow, calculable ways, but broader than what is

generally understood and must serve the moral or spiritual goals of the organization.

Seen from this point of view, those in charge of economic resources must give

account of their stewardship. Stewardship refers to "a person who manages another's

or financial affairs; one who administers anything as an agent of another or others"

(lASB, 2005, p. 2). This stewardship function has been a regular feature of organized

human activities from the earliest time. Stewardship and accountability are regarded

by some as similar and interchangeable (Lewis, 2006).

2.4 The Principles of Accountability in Non-profit Organizations

The principles of accountability of non-profit organizations are not much

different from other organizations. Since accountability is about a relationship that It

involves the giving and demanding of reasons for conduct in which some individuals,

or organizations have certain rights to make demands over the conduct of another as

well as seek reasons for the actions taken.

However, there are certain issues pertaining to accountability in non-profit

organizations that have received little attention in the accounting literature.

According to Gray and Bebbington (2006), those matters relate to issues of size and

formality. They argue that regardless of the size of the organization, accountability

will naturally occur through some combination of personal contact and the visibility

of activities undertaken by the non-profit organization. (If one can, for example, drop

17

in to a non-profit organization and ask it about its activities then a formal specific

account is not required). They further argue that the formal form of accountability

could be burdensome on many non-profit organizations, especially the small ones.

Another issue pertaining to non-profit organizations is that there are many

stakeholders who do not need formal accountability or who believe that the

accountability owed to them is discharged in another manner. Rowl (1972), as

quoted by Gray and Bebbington (2006, p. 335), notes that "all relationships involve

degrees of closeness it is only in the absence of this closeness that a formal

accountability is required". Non-profit organizations, particularly, grass roots non-

profit organizations are the extreme essence of closeness. Much like familial,

friendship, neighbourly, and other relationships within civil society, their very

essence is one of complex, close interaction. In short, as a general rule, the greater

the closeness, the less the need for formal systems.

In addition, it is suggested that the relationship between the organization

and the stakeholders, especially their financiers, is not a purely economic one as

generating profit is not the objective. It is a more complex relationship and reflects ~

more complex attitudes and interaction between the organization and its various

stakeholders. Often the accountability relationship in non-profit organizations may

not be, nor need to be, as formal as that between profit oriented institutions and their

shareholders. Matters such as trust, social contracts, mutuality and conscience all

enter into th~ accountability relationship of non-profit organizations.

To conclude, the principles of accountability in non-profit organizations

can be discharged in many ways, trust sometimes plays a very significant role in this

matter. The information can be obtained through an existing channel, mediated either

by a close approach or through formal systems of accountability.

18

I r 2.5 Trust and Accountability in Non-profit Organizations

t ~ As Philanthropic institutions, non-profit organizations especially, strongly

depend on the public's trust since their major sources of funding come from public

donations. The word trust is used to show the attitude of agents towards other agents

and it also describes behaviour (Sosis, 2005). Therefore, to trust is to act on the

attitude of confidence about another person or group's reliability.

Trust is an important element of charitable giving and is part of all

accountability relationships. The significance of trust in an accountability

relationship is the fact that the agent may react spontaneously according to the

principal's interest rather than responding to contractual obligation and incentive. A

lack of trust results in reluctance to take risks in areas like saving and investment

(Bekkers, 2003; Seal and Vincent, 1997).

In non-profit religious organizations trust plays an essential role as the

resources have to be maintained on the basis of trust rather than the exchange of

something tangible such as a goods or services in return. "Muslims are trustees

(stewards) for God; Man therefore aggresses to assume this great responsibility in a

covenant with God" (Rahim and Goddard, 2003, p.2). Another reason in this

accountability relationship is that trust can become a key aspect to create a positive

attitude between the agent and the principal.

It is argued that the utilization of a monitoring mechanism undertaken

through formal accounting systems could destroy trust (Seal and Vincent, 1997,

pA07). They also recognize the existence of low and high levels of trust in

organizations. Seen from a control systems point of view, when low levels of trust

exist, it will lead to the need for contractual forms of account. Hence, the expectation

of the principal can be expressed in more specific tenus. Whereas, when the level of

19

trust is high, ''there is no need for contract. .. the introduction of fonnal mechanisms

such as contracts may displace human linkages and therefore breakdown trust" (Seal

and Vincent, 1997, p. 407).

From an accountability point of view, it is likely that the presence of high

trust will lead to the use of a communal fonn of accountability. Nevertheless, it is

argued that efficient contracting cannot come about other than in an environment of

trust. Therefore, the real task is to detennine the empirical circumstance under which

formal accounting and contracting processes are compatible with the development of

trust and compel the philanthropic organizations to follow a set of a best practices

and ethical behaviours to build accountability, transparency and trust (Seal and

Vincent, 1997). This is vital; because access to available financial information can

help the organizations maintain a good level of accountability and inform the donors

about how their donations are used in carrying out their activities. Without access to

financial infonnation, as a product of a fonnal accounting, donors will not be able to

make optimal decisions. Accordingly, accounting and fonnal accountability has

become a key component of long-tenn trust in any relationship.

2.6 Competition in the Non-profit Organization Sector

With over a million non-profit organizations in existence today, there is

competition among these organizations for financial resources. People may argue

that there is.not a market place in the non-profit world due to the absence of a profit

motive. However, Leonard (2004, p. 2) says that "wherever goods or services are

exchanged, there is a market place in operation". Those who are involved in an

exchange make transactions based on some level of knowledge about the benefits of

participating in the "trade". The greater the knowledge each participant in a

20

transaction has regarding the potential benefit or making an exchange, the more

likely "a trade" will take place. Despite the absence of profit motivation in non

profit organizations, there remains an exchange of donor money for the satisfaction

of knowing that those in need have been blessed. With this donation comes a

stewardship responsibility of the management of non-profit organizations to both the

giver and receiver to see that it has been administered appropriately. Donors will not

donate if they believe that their donation will be wasted or misappropriated.

Naturally, donors will ask the non-profit organizations to provide

information that enables them to gain assurance that their giving was administered

wisely. Leonard (2004, p.2) says that "the market place transaction for non-profits is

simply the exchange of money for knowledge that the donation will likely achieve its

desired goal of helping those in need". He argues that failure to satisfy the need of

the donors can weaken their support. Donors may withdraw support to non-profit

organizations that are seen as unwilling to be accountable for the use of resources.

Consequently, it can have a profound impact on a non-profit organization's mission

and operation.

For commercial organizations, customers who buy their products and

services confer both legitimacy and financial support. According to Mark and

'Brown, (2001, p. 11) "the customer's decision to spend money on the organization's

products and services simultaneously provide a revenue stream that allow

organization to remain in operation (support), and provide evidence that the

organization is producing something that individuals value (a kind oflegitimacy)". In

contrast, the issues of legitimacy and support are more complex for non-profit

organizations. To a certain degree, support in the non-profit organization means the

same thing that it does in the profit sector, namely, a flow of money and material

21

resources that allows the organization to stay in operation. However, only a small

portion of a non-profit organization's support comes from sales to paying customers.

Instead, financial resources of non-profit organizations come from financial

contributors - individuals, foundations or governments - who are willing to pay for

delivering services to beneficiaries who cannot pay for the services themselves

(Mark and Brown, 2001).

Clearly, with today's information about non-profit organizations more

readily available, especially through the Internet, donors are able to choose who they

fund more carefully. Consequently, non-profit organizations are now operating as

serious competitors for societal resources. Financiers now talk about accountability

and measuring performance and results. Thus, non-profit organizations are now

asked to demonstrate their impact on society and their cost effectiveness. Much of

the pressure for this has come from the funding community, consisting of both

government and philanthropic sources. Failure to do so will seriously harm their

ability to raise funds from private donors. Therefore, to ensure their future· survival

and produce results, no~-profit organizations management must focus, mobilize, and

s1,lstain partnerships and coalitions rather than attend exclusively to their own

organization.

2.7 Regulations for Non-profit Organizations

In almost every country with an active and groWing non-profit

organization and philanthropic sector, both the government and the non-profit sector

itself have sought ways to strengthen the sector's transparency and accountability.

Consequently, the regulation for controlling these kinds of organizations has

increased. ~xpertshave argued that the non-profit organizations sector ought to be

22

similarly controlled to that of profit organizations. Much has been written about the

lack of regulation for the non-profit sector. Non-profit organizations are most likely

to be unregulated except for control that might be exercised by hierarchies or

association groups to which the organization may belong.

Greater transparency and accountability can be achieved through multiple,

often simultaneous and overlapping means. National or sub-national (state or

provincial) governments can increase direct regulatory focus and enforcement on the

sector. Governments can also require or urge the non-profit sector to adopt self-

regulatory means to strengthen accountability and transparency, or as a method for

collaborating with the government on measures (such as tax exemption) that benefit

the sector and society. Also, the non-profit sector itself can adopt self-regulating

mechanisms of its own accord, either as a defensive or proactive measure (Sidel,

2003).

In spite of this, no single pattern fits or describes the variety of non-profit

self-regulation mechanisms. Since this case study is conducted in one of the non-

profit organizations in the province of Nanggroe Aceh Darussalam, Indonesia, this , section will review the current regulations of non-profit organizations in Indonesia.

There are two types of legal entities for non-profit organiZations that exist

m Indonesia, called "yayasan" (foundations) and "perkumpulan" (associations).

Y ayasan was first acknowledged as a legal body during the Dutch colonial time

(1870) as non-membership organizations. Most yayasans were established under the

European legal system, while some adhered to other legal systems such as wakaf

(donations or grants under Islamic law). Their objectives are normally social,

religious educational or humanitarian in nature. Perkumpulans are established by a

number of people to serve the interests of its members or the public. Perkumpulans

23

are non-membership organizations and established on the basis of membership or a

group of people with a common social service objective and not for profit making

purposes (Antl6v et aI., 2005).

However, facts show that most yayasans and perkumpulans in Indonesia

have been used to illegally accumulate wealth for founders or board members.

Antl6v et aI., 2005, p. 6) quotes what is stated in the preamble to law 16/2001 as

follows:

Facts indicate the tendency of some members of society to establish yayasan to take shelter behind the legal status of yayasan which are used not only to develop social, religious, humanitarian activities but also to accumulate wealth for the founders, board members and supervisors. Along with this tendency, a number of problems have emerged in relation to yayasan activities that are not in line with the purpose and objectives stipulated in its articles of Association and the suspicion that yayasans have been used to accommodate illegally gotten wealth of founders or other parties.

Consequently, to restore the function of yayasan as a non-profit

organization with social, religious and humanitarian goals, and to promote its

accountability and transparency, the government of Indonesia established regulations

for non-profit organizations as follows:

• The yayasan is obligated to issue an annual program and financial reports, by at least placing an announcement in the notice board of the yayasan's office (Article 52 Clause 1)

• A yayasan receiving funding from the state, overseas donors or other parties in the amount of Rp500 million (approximately US$55,000) or more or having assets of more than Rp20 billion (approximately US$2.2 million) is obligated to publish its financial report in an. Indonesian language newspaper (article 52 Clause 2).

• A yayasan receiving funding equal to or more than Rp500 million or having assets amounting to Rp20 billion must be audited by a public accountant (article 52 Clause 3).

• Annual financial reports of a yayasan must be prepared based on the Indonesian Standard of Accountancy (article 52 Clause 5) (See, Antl6v, et al., 2005, p.6)

In addition, the Indonesian gove~ent has also urged the non-profit

sector to adopt self-regulatory means to strengthen accountability and transparency.

24