accounting for goodwill -...

TRANSCRIPT

1

Alex Sokratous – Economics Department

Accounting for goodwill

2

Goodwill

Goodwill = Selling price as a going concern –

Fair value of separate net assets

Goodwill = Selling price – (Assets – Liabilities)

3

Goodwill

Buyer may be willing to pay more for a business as a going

concern because of:

- Good location

- Good customer relations

- Good reputation

- Well-known products

- Experienced and efficient employees and management team

- Good relation with suppliers

4

Types of Goodwill

Inherent Goodwill

Purchased Goodwill

5

Inherent Goodwill• Goodwill generated internally because of the above

advantages

• Inherent goodwill is only an estimation. Therefore, it should not be brought into the books, and no accounting entry is required

6

Purchased Goodwill•It is the goodwill generated during the acquisition of a

business

•It is the difference between the selling price of a business as

a going concern and the total value of its separable net assets

•It can be treated as an intangible fixed asset.

•Some companies may write it off immediately against

reserves, or amortized through the profit and loss account

over its useful economic life

7

Calculation of Goodwill

Subjective Judgement

Average Sales/Fees/Profits Method

Super Profit Method

8

Subject Judgement

Estimate the value of goodwill with reference

to some intangible factors and according to

their professional judgement

9

Average Sales/Fees/Profit Method

It can be calculated on gross average or

weight average

Goodwill = Average annual sales/fees/profits

over a stated number of years * a factor

The factor is usually stated as a certain number of

years’ purchase of the average sales/fees/profits

10

Example 1

11

Year Annual Sales

$

1995 100000

1996 200000

1997 300000

(a) Goodwill is valued at 3 years’ purchase of the average annual sales of the past

3 years:

Average annual sales = ($100000+200000+300000 ) /3

= $200000

Goodwill = $200000 X3

= $600000

12

(b) Goodwill is valued at the 3 years’ purchase of the weighted average

of the annual sales of the past 3 years

Weighted average annual sales

= (100000 x 1 + 200000 x 2 + 300000 x 3)

1+2+3

= 1400000

6

= 233333 (Calculation to the nearest dollar)

13

Super Profit Method

A business with goodwill is expected to be

able to earn more profit than a business

without goodwill

The extra profit earned is called the super

profitStatement Calculating Super Profit

Average annual net profit X

Less: Reasonable remuneration to the owner X

Reasonable return on the capital employed in the

tangible assets X X

Super profit X

14

Example 2

15

Chan is leaving the partnership, and goodwill is to be revalued at 3 years’ purchase of the super profit. The expected rate of return on net tangible assets is 10 %, after paying a management fee of $500. The calculation of the super profit is to be based on the average profits of the last four years.

Net profit from 1994-1997 is $5000, $6500, $6500, $7000

Expected return on net tangible assets = Net tangible assets * 10%. Expected return is $5000.

16

Answer

Statement Calculating Super Profit

$ $

Average net profit

(5000+6500+6500+7000)/4 6250

Less: Management fee 500

Expected rate of return

on net tangible assets 5000 5500

Super profit 750

Goodwill= $750 X 3

= $2250

17

Accounting for Goodwill in

Partnership

18

Accounting for goodwill in partnership

Only purchased goodwill is to be brought into the accounts. In sole trader’s accounts, goodwill is to be recognized and recorded in the books only if the business is acquired as a going concern

In partnerships, however, goodwill is brought into the books whenever there is a change in the partnership such as:

Admission of a new partner

Retirement of an old partner

Change of the profit-sharing ratio

19

Each partner has a share of the profit-sharing

ratio. At a change in the partnership, goodwill

must be taken into account and shared among

the existing partners, according to the existing

profit-sharing ratio

20

Goodwill on the admission of

a new partner

21

Goodwill on the admission of a new

partner

The new partner is required to pay for his share of

the tangible assets as well as the goodwill, according

to the profit-sharing ratio

On the admission of a new partner, goodwill must be

revalued

However, not all business keep a goodwill account

in their books. Goodwill adjustments can be done:

Goodwill account opened

Goodwill account not opened

22

Goodwill account opened

The value of the goodwill will be credited to the old

partners’ capital accounts, which represents an

increase in the resources they own, while the new

partner will not have a share of the goodwill

Dr Goodwill account

Cr Capital account ( old partners

only

With the value of goodwill

With their share of goodwill in old

ratio

Dr Goodwill account

Cr Capital account ( old partner

With the increase in the value of

goodwill, share in the old ratio

Dr Capital account (old partner)

Cr Goodwill account

With the decrease in the value of

goodwill, share in the old artio

23

Goodwill account not opened

Goodwill is intangible in nature. It cannot be disposed of

separately. Therefore, some businesses prefer not to maintain

a goodwill account

The new partner may be required to pay extra cash, or have

his capital balance reduced, for his share of goodwill

Dr Goodwill account

Cr Capital account (old

partners only)

Share goodwill among old partners in old

profit-sharing ratio

Dr Capital account ( all

partners)

Cr Goodwill account

Written off goodwill among all partners

in the new profit-sharing ratio

24

Example 3

25

Chan and Wong were partners sharing profits and losses

equally.

On 1 January 1998, they admitted Lee as a new partner who

was required to introduce $600 as capital. The profits are

now to be shared among Chan, Wong and Lee equally.

Goodwill is valued at $300. The balance sheet before the

admission of the new partner is shown as follows:

Chan and Wong

Balance Sheet as at 31 December 1997

Assets 1,200 CapitalChan 600

Wong 600

1,200 1,200

26

Goodwill account opened

GoodwillCapital: Chan (1/2) 150

Wong (1/2) 150

300 300

Capital

Chan Wong Lee Chan Wong Lee

Balance c/f 750 750 600

Goodwill 150 150

Cash 600

750 750 600 750 750 600

Balance c/f 300

Balance b/f 600 600

27

Goodwill account opened

Balance Sheet as at 31 December 1998

Assets

Goodwill 300

Capital

Chan 750

Other Assets (1,200 + 600) 1,800 Wong 750

Lee 600

2,100 2,100

New capital balance

28

Goodwill account not openedCapital

Chan Wong Lee Chan Wong Lee

Goodwill :

new ratio 100 100 100 Goodwill: old ratio 150 150Cash 600

750 750 600 750 750 600

Balance c/f 650 650 500

Balance b/f 600 600

Before admission After admission

Partner Old ratio Share of

goodwill

New ratio Share of

goodwill

Gain/loss

Chan 1/2 $150 1/3 $100 $50 loss

Wong 1/2 $150 1/3 $100 $50 loss

Lee 1/3 $100 $100 gain

$300 $300

29

Goodwill account not opened

Balance Sheet as at 31 December 1998Assets Capital

Chan 650

Wong 650

Lee 500

1,800 1,800

Assets (1,200 + 600) 1,800

30

Goodwill on the

Retirement of a Partner

31

Goodwill on the Retirement of a

Partner

When a partner wants to withdraw from a partnership, the

partnership should revalue all the assets which belongs to the

leaving partner in order to compute the total amount of

money that he can withdraw from the partnership

Goodwill adjustment should be calculated in order to

compensate the leaving partner

32

Example 4

33

Ho, Tang and Lau were partners sharing profits and losses

equally.

On 31 December 1997, Lau left the partnership. The other

two partners agreed to share profits and losses equally.

The goodwill is revalued at $10,000. Lau received cash from

the partnership for the amount due to him on 31 December

1997.

The balance sheet before Lau’s retirement is shown as follows:

Ho, Tang and Lau

Balance Sheet as at 31 December 1997

Goodwill 1,000 CapitalHo 14,000

Tang 14,000Other Assets 41,000

Lau 14,000

42,000 42,000

34

Goodwill account openedGoodwill

Balance b/f 1,000

Capital

Ho Tang Lau Ho Tang Lau

Balance b/f 14,000 14,000 14,000

Goodwill 3,000 3,000 3,000

17,000 17,000 17,000

Capital: Ho (1/3) 3,000

Tang (1/3) 3,000

Lau (1/3) 3,000 9,000

10,000 10,000

Balance c/f 17,000 17,000

17,000 17,000 17,000

Bank 17,000

Balance c/f 10,000

35

Ho and Tang

Balance Sheet as at 31 December 1998

Goodwill 1,000 CapitalHo 17,000

Tang 17,000Other Assets

(41000-17000) 24,000

34,000 34,000

36

Goodwill account not openedCapital

Ho Tang Lau Ho Tang LauBank 17,000

Goodwill :

old ratio 3,000 3,000 3,000

17,000 17,000 17,000

Balance c/f 12,000 12,000

17,000 17,000 17,000

Goodwill:

new ratio 5,000 5,000

Ho and Tang

Balance Sheet as at 31 December 1998

Assets (41,000 – 17,000) 24,000 Capital: Ho 12,000

Tang 12,000

24,000 24,000

Balance b/f 14,000 14,000 14,000

Goodwill on a change in

the profit-sharing ratio

38

Goodwill on a change in the profit-

sharing ratio

When there is a change in the profit-sharing

ratio, the value of goodwill should also be re-

assessed, so as to ascertain the amount of

resources a partner has to give up ( in terms of

a reduction in the relative capital balance) for

the gain in his share of profits/loss.

39

Example 5

40

Yip, Chow and Au are partners in a trading firm and share

profits and losses in the ratio 3:3:2.

On 31 December 1997, they wanted to change the profit-

sharing ratio to 1:1:1.

The goodwill is revalued at $9,000.

The firm’s balance sheet on 31 December 1997 was:

Yip, Chow and Au

Balance Sheet as at 31 December 1997

Goodwill 1,000 Capital: Yip 30,000

Chow 30,000

80,000 80,000

Other Assets 79,000Au 20,000

41

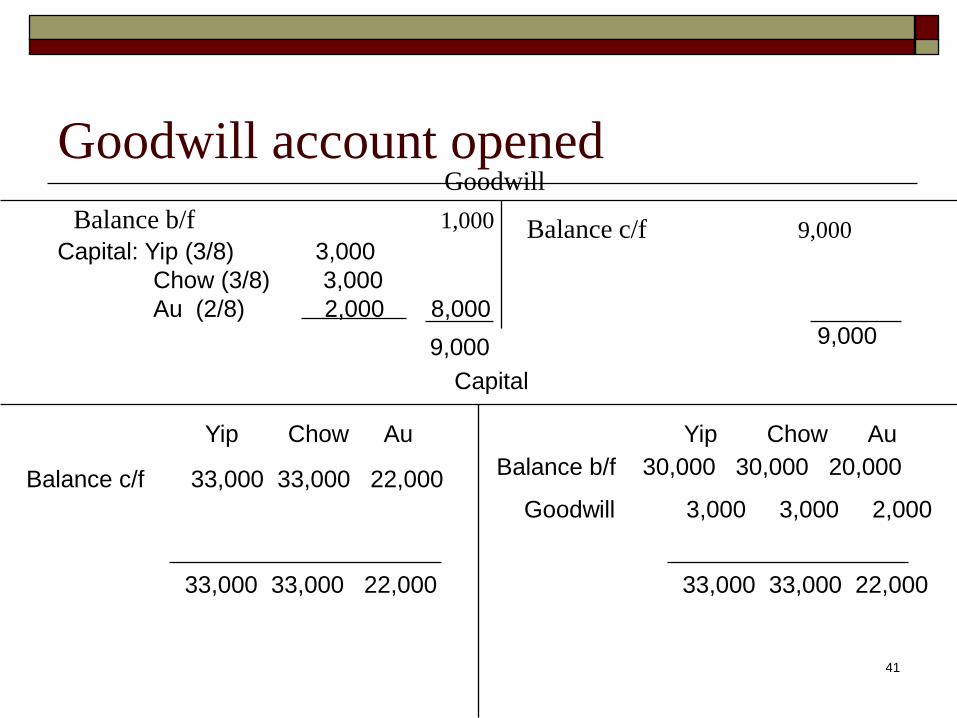

Goodwill account openedGoodwill

Balance b/f 1,000

Capital

Yip Chow Au Yip Chow Au

Balance c/f 33,000 33,000 22,000

Goodwill 3,000 3,000 2,000

33,000 33,000 22,000

Capital: Yip (3/8) 3,000

Chow (3/8) 3,000

Au (2/8) 2,000 8,000

9,0009,000

33,000 33,000 22,000

Balance b/f 30,000 30,000 20,000

Balance c/f 9,000

42

Goodwill account openedBalance Sheet as at 31 December 1998

Goodwill 9,000 CapitalYip 33,000

Chow 33,000

Au 22,000

Other Assets 79,000

88,000 88,000

43

Goodwill account not openedCapital

Yip Chow Au Yip Chow Au

Balance b/f 30,000 30,000 20,000

Goodwill:

old ratio 3,000 3,000 2,000

33,000 33,000 22,000

Balance c/f 30,000 30,000 19,000

33,000 33,000 22,000

Goodwill:

new ratio 3,000 3,000 3,000

44

Yip, Chow & Au

Balance Sheet as at 31 December 1998

Assets 79,000 Capital: Yip 30,000

Chow 30,000

79,000 79,000

Au 19,000

Cindy and Candy were in partnership. They shared profits and losses

in ratio of 3:2 On 1 January 2001, they decided to admit Joe.

Goodwill is valued at one year’s purchase of the average annual

profits (weighted average) of the past four years. Goodwill is not to

be brought into the partnership’s book. Joe brought $40,000 cash

into the business for capital. No extra cash is paid for goodwill. The

new profit-sharing ratio is 3:2:1.

The balance sheet as at 31 December2000 before the admission of

Joe is as follows:

Assets 110,000 Capital : Cindy 65,000

Cash 25,000 Candy 70,000

Annual net profits for 1997 to 2000 were $25,000,$40,000, $75,000 and $60,000 respectively.

Record the above change in the partnership in the partners’ capital accounts in columnar form, and show the balance sheet after the admission of Joe.

Valuation of Goodwill :

25,000 x1 + 40,000x2 + 75,000 x3 + 60,000 x 4

1 + 2 + 3 + 4

57,000