accounting practices 501 chapter 7 cash controls and bank reconciliation cathy saenger, senior...

TRANSCRIPT

Accounting Practices 501

Chapter 7

Cash Controls and

Bank Reconciliation

Cathy Saenger, Senior Lecturer, Eastern Institute of Technology © Pearson 2011

Cash control proceduresCash control procedures• All cash and cheques received should be banked

intact.• Keep as little cash as possible.• All payments should be made by cheques except

small payments.• Keep a petty cash fund for small payments.• Bank reconciliation should be done.• Segregation of duties.• Rotation of duties.• Cash register.

Bank Reconciliation

Ch7A - Bank Recon 3

Each month a business will receive a bank statement from the bank

The balance of the Bank Statement will normally not be the same as the balance in the business’s Bank account in the General Ledger, due to various reasons:Unpresented cheques

Outstanding deposits

Automatic payments

Bank charges

Dishonoured cheques

Errors

A Bank Reconciliation then needs to be prepared

Bank Reconciliation

Ch7A - Bank Recon 4

Let’s look at an example

The following is a very simplified reconciliation as the slides have limited

space

Ch7A - Bank Recon 5

Cash Sales 100

Acc Receiv 300

Cash Sales 500

Cash Sales 700

Cash Sales 900

Teleph (#12) 200

Purch (#13) 400

Acc Pay (#14) 600

Cash Receipts Journal (June)

Cash Payments Journal (June)Ban

kBank

Bank reconciliation as at 31 May

Balance as per Bank statement $200Less Unpresented cheq #10 50

Balance as per Gen Ledger Bank acct

$150

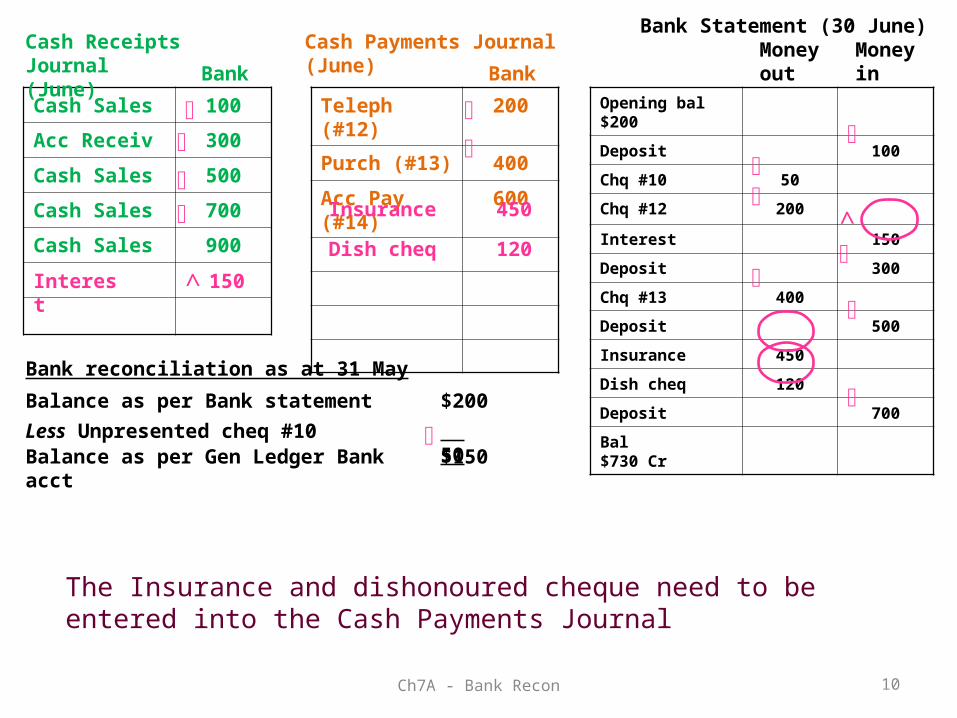

We have the Cash Receipts Journal (CRJ), the Cash Payments Journal (CPJ) and the previous Bank Reconciliation of the business as well as the Bank Statement received from the bank

Opening bal $200

Deposit 100

Chq #10 50

Chq #12 200

Interest 150

Deposit 300

Chq #13 400

Deposit 500

Insurance 450

Dish cheq 120

Deposit 700

Bal $730 Cr

Bank Statement (30 June)Money in

Money out

Ch7A - Bank Recon 6

Cash Sales 100

Acc Receiv 300

Cash Sales 500

Cash Sales 700

Cash Sales 900

Teleph (#12) 200

Purch (#13) 400

Acc Pay (#14) 600

Cash Receipts Journal (June)

Cash Payments Journal (June)Ban

kBank

Bank reconciliation as at 31 May

Balance as per Bank statement $200Less Unpresented cheq #10 50

Balance as per Gen Ledger Bank acct

$150The Bank Statement has to be compared to the two cash

journals to find items that do not yet appear in the journals and to find items that do not yet appear in the Bank Statement.

We do that by ticking off the items from the Bank Statement.

Let’s start with comparing Money In to the Cash receipts journal

Opening bal $200

Deposit 100

Chq #10 50

Chq #12 200

Interest 150

Deposit 300

Chq #13 400

Deposit 500

Insurance 450

Dish cheq 120

Deposit 700

Bal $730 Cr

Bank Statement (30 June)Money in

Money out

Ch7A - Bank Recon 7

Cash Sales 100

Acc Receiv 300

Cash Sales 500

Cash Sales 700

Cash Sales 900

Teleph (#12) 200

Purch (#13) 400

Acc Pay (#14) 600

Cash Receipts Journal (June)

Cash Payments Journal (June)Ban

kBank

Bank reconciliation as at 31 May

Balance as per Bank statement $200Less Unpresented cheq #10 50

Balance as per Gen Ledger Bank acct

$150

Opening bal $200

Deposit 100

Chq #10 50

Chq #12 200

Interest 150

Deposit 300

Chq #13 400

Deposit 500

Insurance 450

Dish cheq 120

Deposit 700

Bal $730 Cr

Bank Statement (30 June)Money in

Money out

The $150 on the Bank Statement does not appear in the CRJAdd it to the Cash Receipts Journal

Interest

150

Ch7A - Bank Recon 8

Cash Sales 100

Acc Receiv 300

Cash Sales 500

Cash Sales 700

Cash Sales 900

Teleph (#12) 200

Purch (#13) 400

Acc Pay (#14) 600

Cash Receipts Journal (June)

Cash Payments Journal (June)Ban

kBank

Bank reconciliation as at 31 May

Balance as per Bank statement $200Less Unpresented cheq #10 50

Balance as per Gen Ledger Bank acct

$150

Opening bal $200

Deposit 100

Chq #10 50

Chq #12 200

Interest 150

Deposit 300

Chq #13 400

Deposit 500

Insurance 450

Dish cheq 120

Deposit 700

Bal $730 Cr

Bank Statement (30 June)Money in

Money out

Interest

150

Now we can tick off the Interest amount and the rest

^

^

Ch7A - Bank Recon 9

Cash Sales 100

Acc Receiv 300

Cash Sales 500

Cash Sales 700

Cash Sales 900

Teleph (#12) 200

Purch (#13) 400

Acc Pay (#14) 600

Cash Receipts Journal (June)

Cash Payments Journal (June)Ban

kBank

Bank reconciliation as at 31 May

Balance as per Bank statement $200Less Unpresented cheq #10 50

Balance as per Gen Ledger Bank acct

$150

Opening bal $200

Deposit 100

Chq #10 50

Chq #12 200

Interest 150

Deposit 300

Chq #13 400

Deposit 500

Insurance 450

Dish cheq 120

Deposit 700

Bal $730 Cr

Bank Statement (30 June)Money in

Money out

Interest

150

^

^

Now we can compare Money Out to the Cash payments journal

Ch7A - Bank Recon 10

Cash Sales 100

Acc Receiv 300

Cash Sales 500

Cash Sales 700

Cash Sales 900

Teleph (#12) 200

Purch (#13) 400

Acc Pay (#14) 600

Cash Receipts Journal (June)

Cash Payments Journal (June)Ban

kBank

Bank reconciliation as at 31 May

Balance as per Bank statement $200Less Unpresented cheq #10 50

Balance as per Gen Ledger Bank acct

$150

Opening bal $200

Deposit 100

Chq #10 50

Chq #12 200

Interest 150

Deposit 300

Chq #13 400

Deposit 500

Insurance 450

Dish cheq 120

Deposit 700

Bal $730 Cr

Bank Statement (30 June)Money in

Money out

Interest

150

^

^

The Insurance and dishonoured cheque need to be entered into the Cash Payments Journal

Insurance

450

Dish cheq

120

Ch7A - Bank Recon 11

Cash Sales 100

Acc Receiv 300

Cash Sales 500

Cash Sales 700

Cash Sales 900

Teleph (#12) 200

Purch (#13) 400

Acc Pay (#14) 600

Cash Receipts Journal (June)

Cash Payments Journal (June)Ban

kBank

Bank reconciliation as at 31 May

Balance as per Bank statement $200Less Unpresented cheq #10 50

Balance as per Gen Ledger Bank acct

$150

Opening bal $200

Deposit 100

Chq #10 50

Chq #12 200

Interest 150

Deposit 300

Chq #13 400

Deposit 500

Insurance 450

Dish cheq 120

Deposit 700

Bal $730 Cr

Bank Statement (30 June)Money in

Money out

Interest

150

^

^

Insurance

450

Dish cheq

120

Now we can tick the Insurance and Dishonoured cheque

^ ^

^ ^

To be continued ……

Ch7A - Bank Recon 12